2003 Financial Results - Essilor · 35 Australia–New Zealand A U.S.-type market • 1989 – 1995...

59

[ 2003 RESULTS March 4, 2004 ]

Transcript of 2003 Financial Results - Essilor · 35 Australia–New Zealand A U.S.-type market • 1989 – 1995...

[ 2003 RESULTSMarch 4, 2004 ]

2

• Introduction Xavier Fontanet

• 2003 Results Philippe Alfroid

• Asia – Pacific Patrick Cherrier

• Conclusion Xavier Fontanet

• Questions and answers

3

2003 ResultsPhilippe Alfroid

4

4Growth modest in the beginning of the year, strong in the fourth quarter

4Sharp improvement in margins

4Numerous acquisitions

Essilor in 2003

5

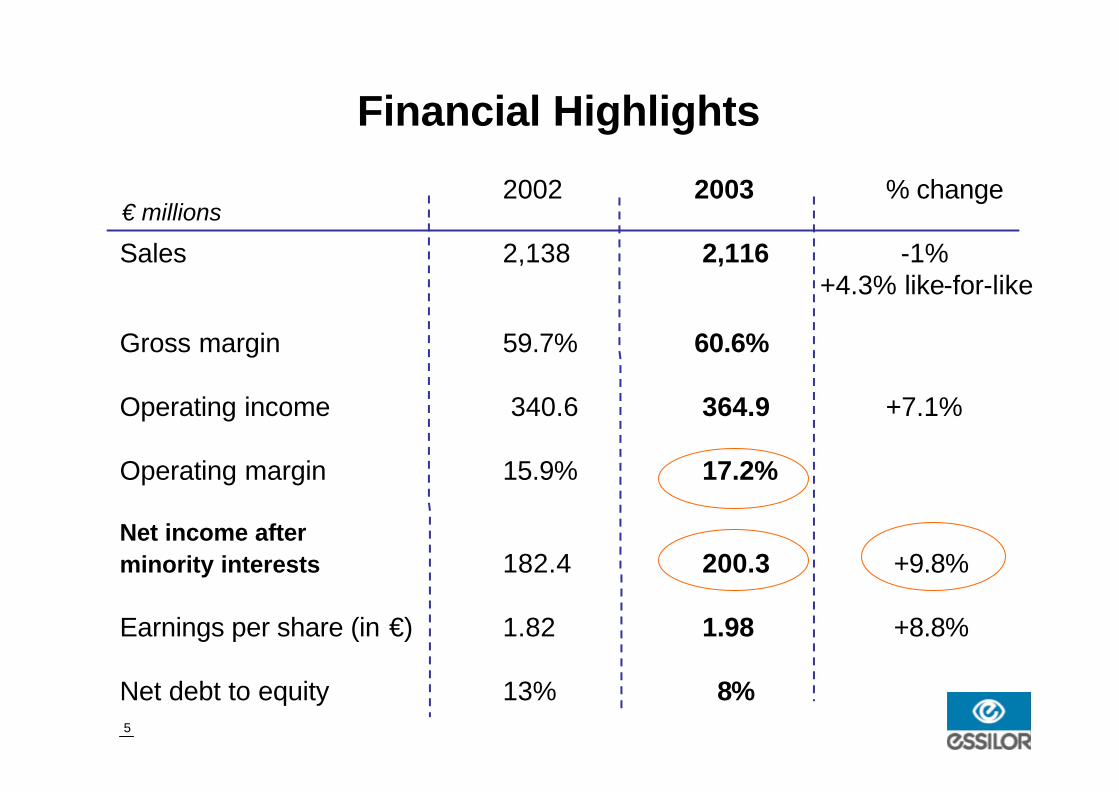

2002 2003 % change

Sales 2,138 2,116 -1%+4.3% like-for-like

Gross margin 59.7% 60.6%

Operating income 340.6 364.9 +7.1%

Operating margin 15.9% 17.2%

Net income afterminority interests 182.4 200.3 +9.8%

Earnings per share (in €) 1.82 1.98 +8.8%

Net debt to equity 13% 8%

€ millions

Financial Highlights

6

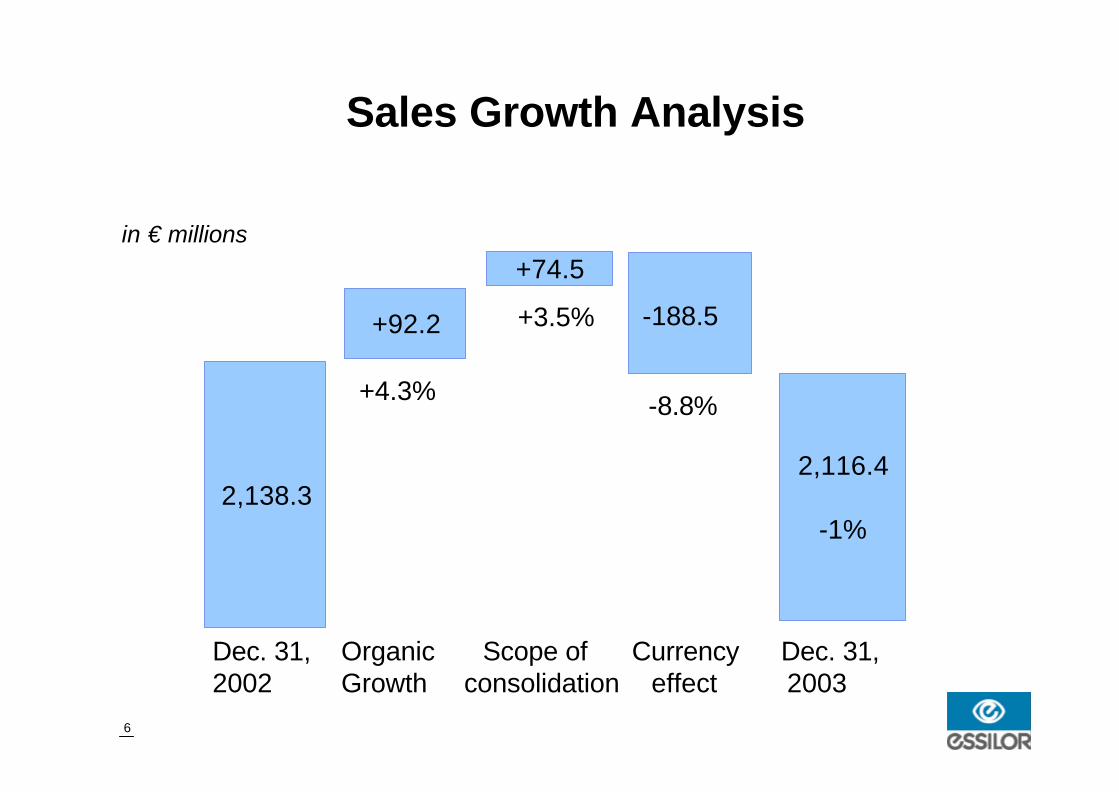

2,138.3

+92.2

+74.5

2,116.4

-1%

Dec. 31, Organic Scope of Currency Dec. 31, 2002 Growth consolidation effect 2003

+4.3%

+3.5% -188.5

Sales Growth Analysis

-8.8%

in € millions

7

0

2

4

6

8

1996 1997 1998 1999 2000 2001 2002 2003

5.7% 5.7% 6%

4.2%

6.5%5.6%

7%

4.3% 1H +2.3%2H +6.5%

Organic Growth(1996 - 2003)

8

Sales by Region

Europe North America South America Asia

973

1,048

970 869

51 49 143 150

+7.3%+1%

+17% +2%

% growth like-for-like

9

Sales by Region

Europe North America South America Asia

973

1,048

970 869

51 49 143 150

+9%+5.5%

+17% +12.2%

% growth excluding currency effect

10

2003 Highlights (1)

4Growth in Europe led by France, United Kingdom, Spain, Eastern Europe and Germany in the fourth quarter

4US down in the first half, with an upturn in the third quarter and strong growth in the fourth

4Sales still lower in Japan but stable in the fourth quarter

MARKETS

11

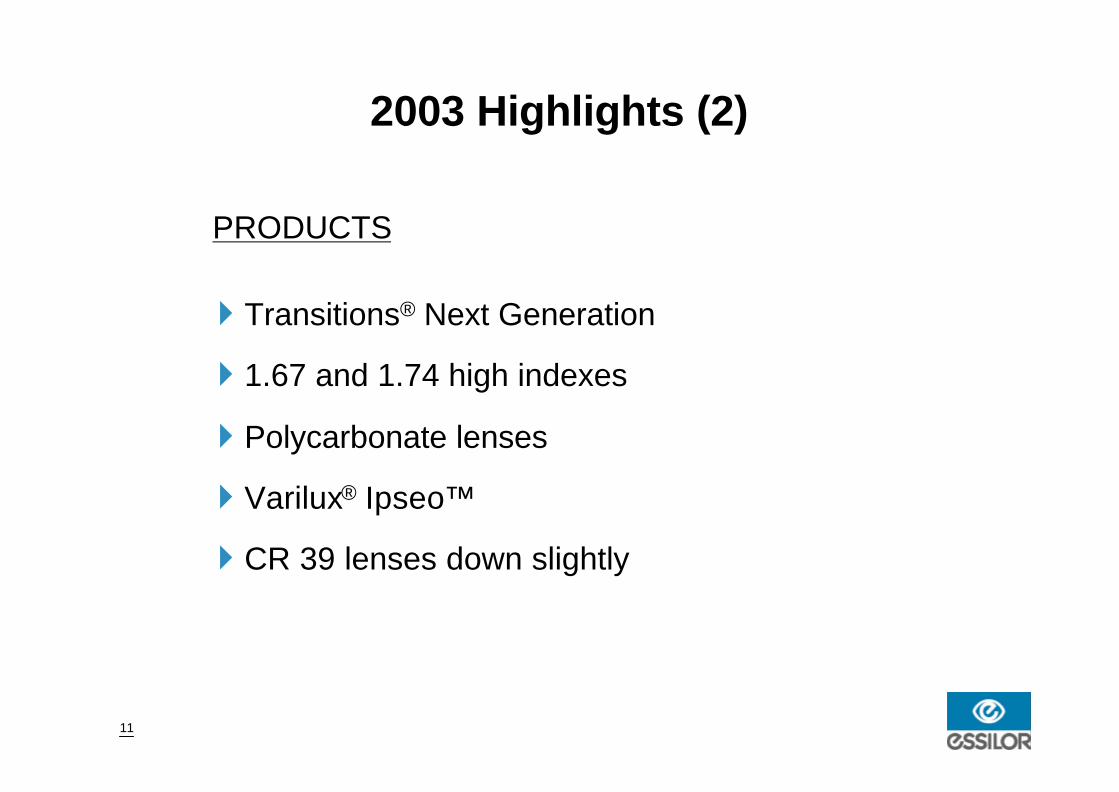

2003 Highlights (2)

4Transitions® Next Generation

41.67 and 1.74 high indexes

4Polycarbonate lenses

4Varilux® Ipseo™

4CR 39 lenses down slightly

PRODUCTS

12

€ millions

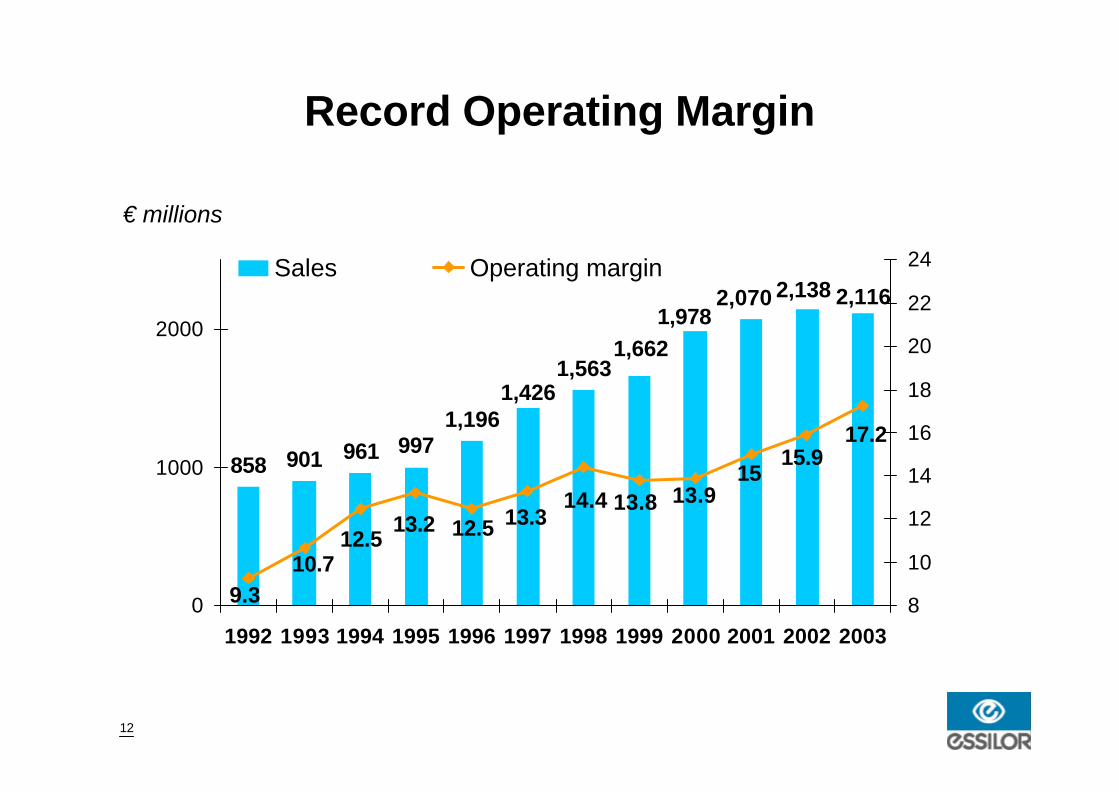

Record Operating Margin

858 901 961 997

2,1162,1382,0701,978

1,6621,563

1,4261,196

9.310.7

12.513.2 12.5 13.3

14.4 13.8

17.2

13.915

15.9

0

1000

2000

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 20038

10

12

14

16

18

20

22

24Sales Operating margin

13

Breakdown of Operating Margin Gain

4Product mix added 0.9 point to gross margin

4Transitions®

4Cost control: 0.4 point

4Germany in 4Q: 0.4 point

1.3 pointincrease

14

Sales and Operating Income Analysis

340.6

+45.9+9.8 -31.3

364.9+7.1%

2,138.3

+92.2

+74.5

-188.5

2,116.4

-1%

+13.4%

+2.9%-9.2%Op.

income

Sales

+4.3%

+3.5%

-8.8%

Dec. 31, Organic Scope of Currency Dec. 31, 2002 Growth consolidation effect 2003

15

2003 2003Actual € rate 2002 € rate

Sales 2,116.4 -1% 2,304.9 +7.8%

Op. income 364.9 +7.1% 396.3 +16.4%

Op. margin 17.2% 17.2%

Net income 200.3 +9.8% 214.9 +17.8%

Net margin 9.5% 9.3%

Op. margin 17.2% 17.2%

Currency Effect = Translation Adjustment

16

2003 2003 2003Actual € m in ¥ bn in $ m

Sales 2,116.4 -1.0% 278.9 +10.5% 2,416.8 +19%

Op. inc. 364.9 +7.1% 48.1 +19.6% 416.7 +29%

Op. margin 17.2% 17.2% 17.2%

Currency Impact on Sales and Operating Income

17

2002 2003 % changerestated*

Operating income 340.6 364.9 +7.1%

Net interest expense (36.7) (33.5) -8.7%

Non-operating expense (20.1) (14.9)

Income tax (78.3) (90.3)

Net income (loss) of 0.5 (2.9)companies accounted forby the equity method

Amortization of goodwill (23.7) (22.5)

Net income after 182.4 200.3 +9.8%minority interests

€ millions

*VisionWeb accounted for by the equity method

Net Income

18

Non-Operating Expense

2002 2003

Bacou-Dalloz revaluation gain 8.2

Real Estate gain 4.5

US restructuring costs (9.5) (11.3)

Europe (10.8) (1.0)

Asset write-downs and other (8.0) (7.1)

TOTAL (20.1) (14.9)

(28.3) (19.4)

19

0

50

100

150

200

250

300

350

400

95 96 97 98 99 2000 2001 2002 20034

5

6

7

8

Stocks Rotation

232

326345 351

325310

255276

284

€ millions

Consolidated InventoryDown 5% like-for-like

20

0

40

80

120

160

200

1995 1996 1997 1998 1999 2000 2001 2002 2003

76 79

98

133

152

7.5% 7.4%6.9%

8.5%9.1% 8%

158

120

5.8%

€ millions

6.5%

140

6.6%

140

Net Capital Expenditure

21

UNITED STATES / CANADANassau / Stockhouse June 1SLC / Polarizing lenses March 3Optical Suppliers Hawaii / Laboratory July 11Omni Texas / Laboratory August 30Canadian laboratories February - September

ASIAEssilor Korea Chemiglas / Topex February 1Laboratories May

EUROPERupp & Hubrach October

TOTAL:Annual sales €169 millionTotal price €122 million

Consolidation date

Acquisitions Since January 1, 2003

22

ROA: EBIT / net assetsROA vs total net assets (€ millions)

0

200

400

600

800

1 000

1 200

1 400

1 600

1 800

1995 1996 1997 1998 1999 2000 2001 2002 20030

5

10

15

20

25

30

Actifs nets % EBIT / Actifs nets

18.6%

15.5%

18.3%

14.7%16.4% 15.7%

16.9%

21.2%24.1%

Net assets %EBIT / Net assets

23

348

6626

Cash flow

Share issueReduction innet debt

98

59

250

Capital expenditure(140)+ ∆ WCR (-41)

Dividends

150

Acquisitions, incl. purchasesof shares (24)

€ millions

Consolidated Cash Flow

24

€ millions in %

270161 143 164

466321

164 97

632

811938

1,2101,2141,209

1,0481,157

0

200

400

600

800

1000

1200

1400

96 97 98 99 2000 2001 2002 2003

Dette nette Capitaux propres

43

2015 14

44

26

138

05

10

152025

30354045

50

96 97 98 99 2000 2001 2002 2003

Ratio Dette / SNShareholders’ equity ratio Debt to equity ratioNet debt

Balance Sheet Structure at Dec. 31, 2003

25

ActualDec. 31, 2002

1,214.2

4.4+

Capitalincrease

Net of share cancellations

200.3+

Income

59-

Dividends

2.2-

Treasurystock

net of sharecancellations

Actual Dec. 31, 2003

1,210

150-

Translationadjustment

1.6+

Minorityinterests

€ millions

Consolidated Shareholders’ Equity

26

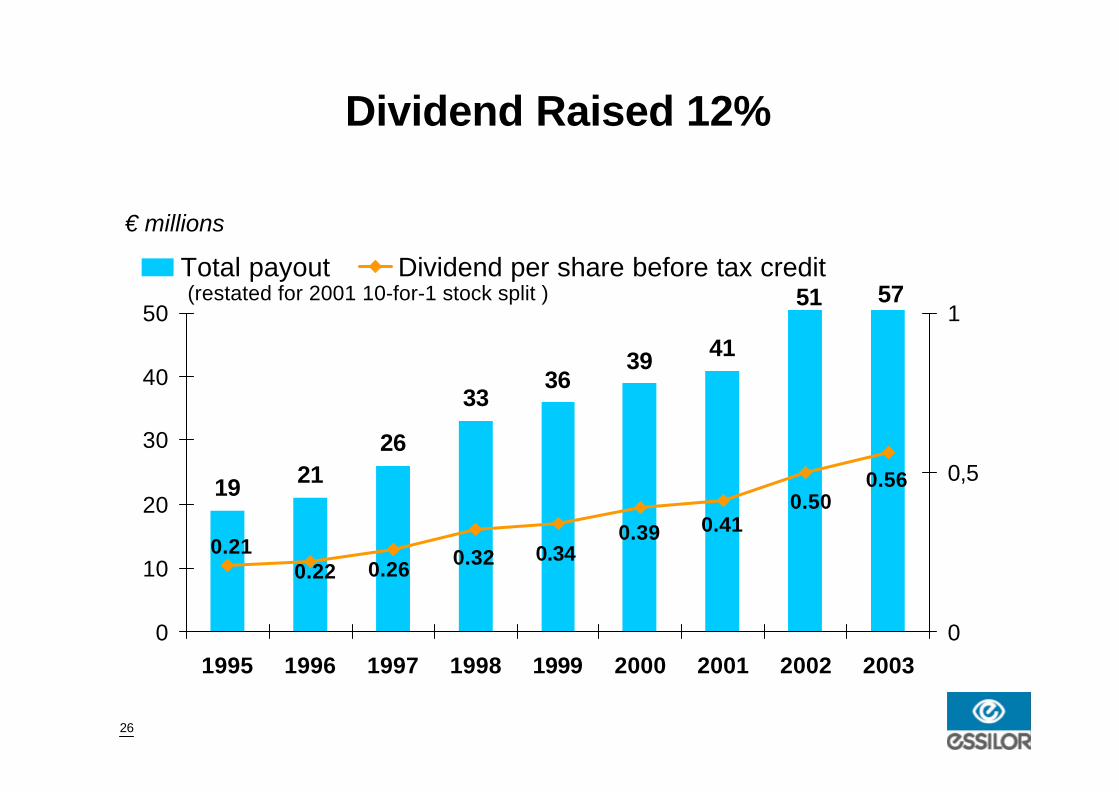

19 2126

3336

39 41

0.410.390.340.320.260.22

0.21

0.500.56

0

10

20

30

40

50

1995 1996 1997 1998 1999 2000 2001 2002 20030

0,5

1

Total payout Dividend per share before tax credit

€ millions

(restated for 2001 10-for-1 stock split ) 51 57

Dividend Raised 12%

27

Change in Issued Capital(Shares outstanding at Dec. 31, 2003)

4800,000 shares cancelled

4856,495 new shares issued

41,269,837 shares held in treasury

4101,470,271 shares outstanding excluding treasury stock

28

Outlook for 2004

4Global rollout of leading products:• Crizal® Aliz陕 Varilux® Ellipse• Varilux® Ipseo™

42003 and 2004 acquisitions

4Germany

Favorable Unfavorable

29

Asia - PacificPatrick Cherrier

30

Asia as a Percentage of Essilor’sBusiness

1998 2003 2025

3.3 7.1 25

31

Total population by region

People needing corrective lenses Percentage wearing corrective lenses

60%60%

15.5%15.5%

35%35%

16%16%

19%19%

World population: ~ 6 billionCorrection needs : ~ 4 billionWearers: ~ 1.3 billion

Correction Needs

32

1967Hoya JV

1979Philippinesplant

1985Thailandplant

1987 -1990SingaporeThailandHong KongMalaysiaSouth KoreaIndonesia

1991Hoya JVhaltedSouth Korean operations sold

1996ChinaWholesaleAustralia

2000Nikon

2003SouthKorea

1998IndiaLab.Australia

1999NewZealand

A Long-Standing Presence in Asia

33

Japan

China

Hong Kong

PhilippinesThailand

MalaysiaSingapore

IndonesiaAustralia

Korea

India

New Zealand

Distribution subsidiaries (13)

Asia-Pacific headquarters

Prescription laboratories (27) Chemi

One Asia or five?

34

One Asia or five?

• Australia / New Zealand• Japan / South Korea• Tigers and Dragons• China• India

35

Australia–New Zealand

A U.S.-type market

• 1989 – 1995 Initially, a laboratory in Sydney7 difficult years, Sola ultra market leader

• 1996 Direct Optical: contact with independentlaboratories. Volumes suddenly jump

• 1998 Perkins: a network of laboratories coveringall of Australia

• 1999 Success of Transitions, first sales to OPSM, which expands from just “one-hour service”

• 2003 Essilor is the market leader, on top of each niche (laboratories, sales to chains, sales to opticians)

36

Tigers and Dragons

• Each country has a structure similar to Australia and the

United States

• Essilor tailors its strategy to each country, but always

with the same goal

• Taiwan is the only country where Essilor is not present

37

Japan

• World’s second biggest market in value terms

• Difficult market that revived in mid-2003

• Competition: only integrated manufacturers

• Very strong concentration on sophisticated products: ultra high index materials and progressive lenses

• Nikon-Essilor has steadily won positions over the last three years, now No. 2 behind Hoya

• Nikon-Essilor is currently focusing on independent opticians and is starting to work with medium-sized chains

38

South Korea

• Startup in 1987, exit in 1993, return in 2002 through Samyung Trading joint venture

• Two goals: • Enter the laboratory market with Topex• Understand and support the strategy of Chemiglas, the leading

South Korean producer

• Multi-brand, multi-channel strategy similar to European practice

• Currently difficult South Korean market, in which Essilor is No. 2 (Topex/Chemiglas)

• Chemiglas is focusing on Asia and China in 1.6 index lensesA plant is coming on stream near Shanghai

39

China

• The region’s biggest market in volume terms (100 m lenses). Plastic lenses already dominate, but:

• Progressives are not widespread (people are near-sighted)• Prices are very low• Per capita consumption is still very weak

• Essilor has a two-pronged strategy:

• Essilor in the premium segment No. 1• Chemilens in the mass market No. 3 or 4 today

• The potential is enormous, but the road will be long (training opticians and developing the progressive lens concept with threelaboratories only)

40

India

• Market logic similar to China (70 m lenses)

• But progressives will expand• Hyperopic population• 40 million bifocals

• Essilor • Applies a strategy similar to China• Is developing a network of laboratories across the country,

both owned and in partnership

41

Conclusion

• Apart from South Korea and Japan, Essilor is No. 1 almost everywhere

• The potential is tremendous, but we have to expand distribution and train optometrists

• China and India: which will develop the fastest? Place your bets…But in any case, Essilor will be No. 1 in each market

42

Conclusion

Xavier Fontanet

43

• Asia

• 2003

• Organic growth and acquisitions

• Outlook for 2004

• Essilor and its customers

• The Essilor supply chain

• The future

44

Asia

• Obvious long-term potential

• A market share gain strategy that adapts to local conditions

• Value added / core market• Sales to opticians / sales to laboratories• Joint ventures / acquisitions

• So far, few competitors can withstand Essilor’s momentum

• Asia, Eastern Europe and Latin America share the same growth logic

45

2003: A year of turmoil that nonetheless strengthened…

… our long-term options

… market fundamentals

…. the responsiveness of our teams

46

2003

… Product mix and gross margin

… Offsetting Iraq and SARS

… Opex reined in as of January

47

-+

SARS / Iraq Germany 1990/2003

-+

2003: Sales weren’t lost… … they just moved elsewhere

48

Bettervision

PolarizationAnti-reflectivePhotochromic lenses

ThinnerMoretransparentMore resistant

Progressive lenses

IPSEOProgressives for optical chainsShort progressionWrap-arounds

Anti-reflective treatment

Alizé

Photochromic lenses

Transitions 1.67

Polarized lenses

BNLSLC

Tint / Protection

PhysiotintsMelanin

Materials

PC1.671.74

A large number of new products in 2004

49

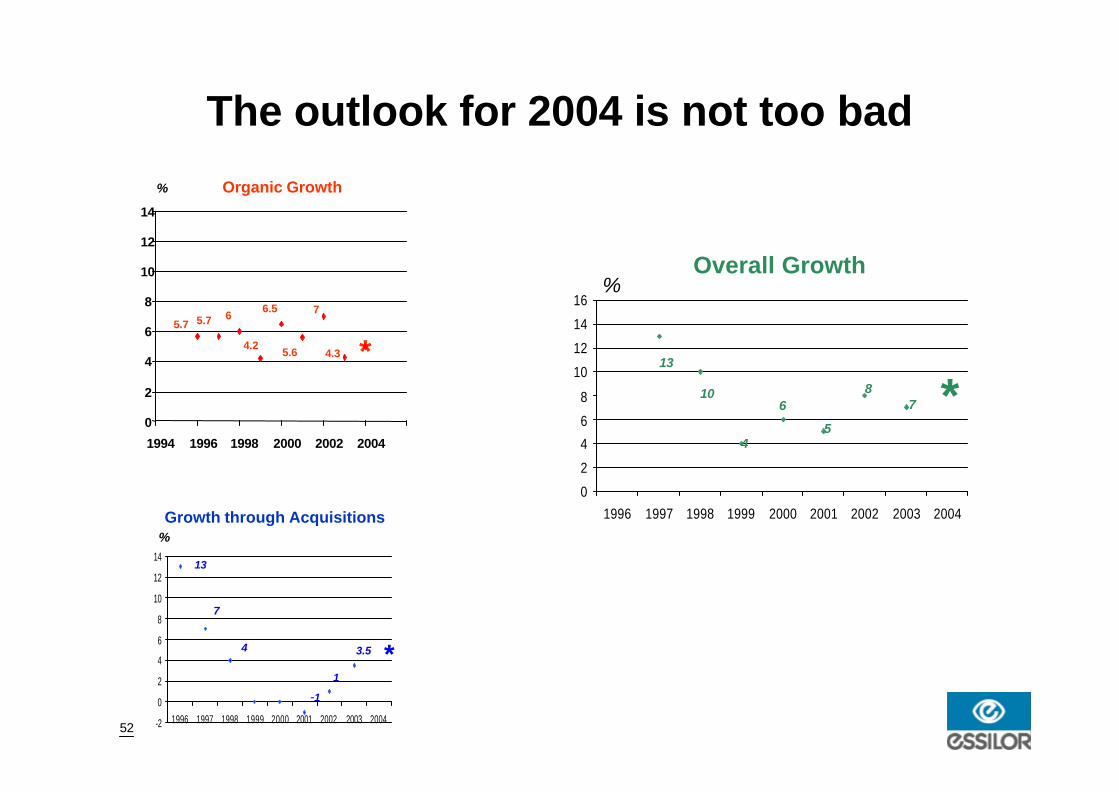

0

2

4

6

8

1996 1997 1998 1999 2000 2001 2002 2003 2004

5.7 5.7 6

4.2

6.5

5.6

4.3

7

*

%

Organic growth

50

D & A

Essilor’s experiencein laboratories

RUPP

NASSAU

The Essilorsupply chainand plants

TOPEX

TheEssilorlineup

SLCBNL

R&D andthe Essilor

network

2003 : Acquisitions in four niches, with obvious synergies in each

51

-2

0

2

4

6

8

10

12

14

1996 1997 1998 1999 2000 2001 2002 2003 2004

13

7

4

-11

3.5 *

%

Growth through acquisitions

52 -2

0

2

4

6

8

10

12

14

1996 1997 1998 1999 2000 2001 2002 2003 2004

13

7

4

-1

1

3.5 *

Growth through Acquisitions%

0

2

4

6

8

10

12

14

16

1996 1997 1998 1999 2000 2001 2002 2003 2004

13

10

4

6

5

87

Overall Growth

*

%

*5.7 5.7

6.56

4.25.6 4.3

7

Organic Growth%

0

2

4

6

8

10

12

14

1994 1996 1998 2000 2002 2004

The outlook for 2004 is not too bad

53

Essilor and its customers

Independents

Chains marketing mainly manufacturer brands

Chains marketing mainly theirown brands

Essilor

Nikon

BBGR

54

Sales Buildings

Back Office

Plants

Logistics

Breakthrough in rimless frames

Laboratories

55

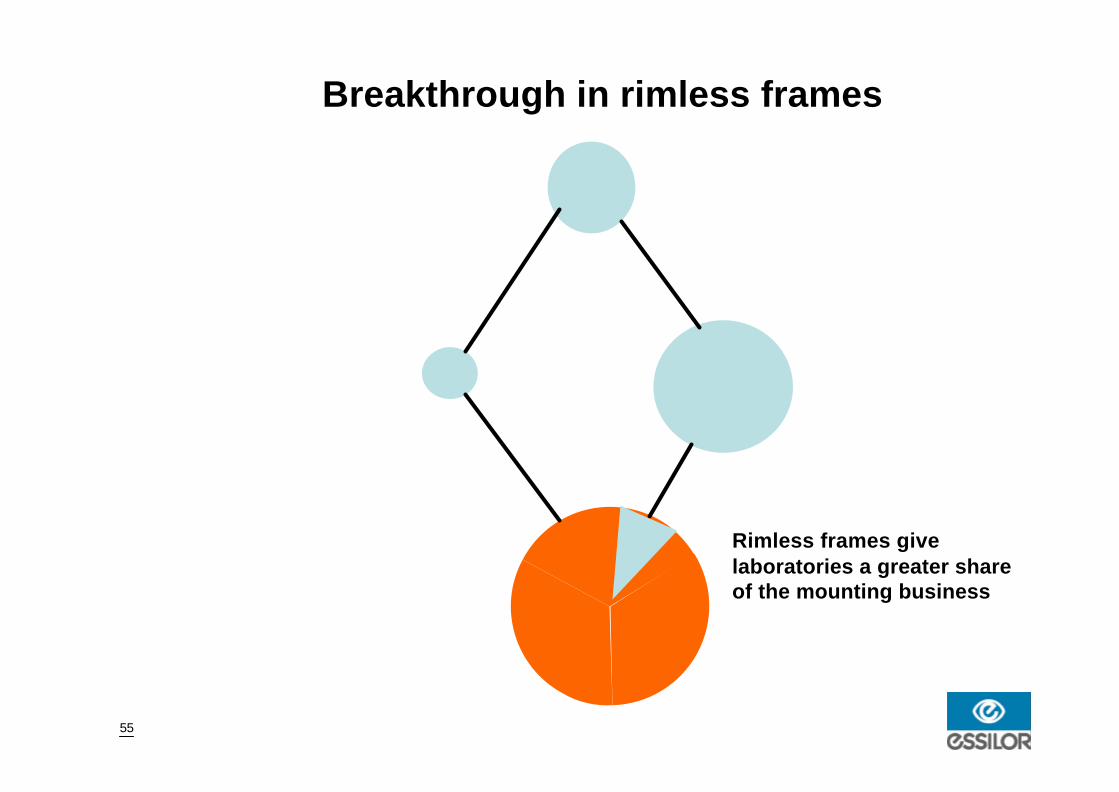

Breakthrough in rimless frames

Rimless frames givelaboratories a greater shareof the mounting business

56

Lower costs… across the board!

• Plant productivity gains• Ongoing relocation and automation programs

• Laboratory productivity gains• Products travel more easily and laboratories are specializing

• Rimless frames give laboratories a greater share of the mountingbusiness

• Information systems can significantly improve supply chain management

Thanks to its supply chain, Essilor is a creative, flexible, powerful partner for each of its customers

57

The future

• Volume Asia, Latin America and Eastern Europe

• Mix Europe, Japan and North America

• Vision Photochromic lenses, sunglass lenses, anti-reflective treatment, etc.

Essilor still has a lot to do!

58

Questions & Answers