2001Chpt11

24

© 2002 McGraw-Hill Ryerson Limited.

description

messier

Transcript of 2001Chpt11

11-1

© 2002 McGraw-Hill Ryerson Limited.

All rights reserved.

11-2

© 2002 McGraw-Hill Ryerson Limited.

All rights reserved.

Part Fiv

eAUDITING ACCOUNTING APPLICATIONS AND RELATED ACCOUNTS

11-3

© 2002 McGraw-Hill Ryerson Limited.

All rights reserved.

Chap

ter1

1CHAPTER 11AUDITING THE PURCHASING CYCLE AND RELATED ACCOUNTS

11-4

© 2002 McGraw-Hill Ryerson Limited.

All rights reserved.

EXPENSE AND LIABILITY RECOGNITION

CICA does not have a definition for expense.

Expenses are outflows or other using up of assets or incurrences of liabilities (or a combination of both) from delivering or producing goods, rendering services, or carrying out other activities that constitute the entity’s ongoing major or central operations. (US standards)

11-5

© 2002 McGraw-Hill Ryerson Limited.

All rights reserved.

CATEGORIES OF EXPENSES

Product costs Period costs Allocable costs

11-6

© 2002 McGraw-Hill Ryerson Limited.

All rights reserved.

OVERVIEW OF THE PURCHASING CYCLE

Figure 11-1 presents a flowchart of a purchasing system, which serves as a framework for discussing control procedures and tests of controls.

11-7

© 2002 McGraw-Hill Ryerson Limited.

All rights reserved.

TYPES OF TRANSACTIONS

Purchase of goods and services for cash or credit. Payment of the liabilities arising from such purchases. Return of goods to suppliers for cash or credit.

11-8

© 2002 McGraw-Hill Ryerson Limited.

All rights reserved.

FINANCIAL STATEMENT ACCOUNTS AFFECTED

Purchase transaction: Accounts payable Inventory Purchases or cost of goods sold Various asset and expense accounts

Cash disbursement transaction: Cash Accounts payable Cash discounts

Purchase return transaction: Purchase returns Purchase allowances Accounts payable

11-9

© 2002 McGraw-Hill Ryerson Limited.

All rights reserved.

DOCUMENTS AND RECORDS

Purchase requisition. Purchase order. Receiving report. Vendor invoice. Voucher.

Voucher register/purchase journal. Accounts payable subsidiary ledger. Vendor statements. Cheque. Cash disbursements journal/cheque

register.

11-10

© 2002 McGraw-Hill Ryerson Limited.

All rights reserved.

MAJOR FUNCTIONS

Requisitioning Purchasing Receiving Invoice processing Disbursements Accounts payable General ledger

11-11

© 2002 McGraw-Hill Ryerson Limited.

All rights reserved.

KEY SEGREGATION OF DUTIES

The purchasing function should be segregated from the requisitioning and receiving functions.

The invoice-processing function should be segregated from the accounts payable function.

The disbursement function should be segregated from the accounts payable function.

The accounts payable function should be segregated from the general ledger function.

11-12

© 2002 McGraw-Hill Ryerson Limited.

All rights reserved.

STATEGIC SYSTEMS APPROACH INHERENT RISK ASSESSMENT

Auditor should gain a comprehensive understanding of the purchasing process

Industry-related factors Misstatements detected in prior audits

11-13

© 2002 McGraw-Hill Ryerson Limited.

All rights reserved.

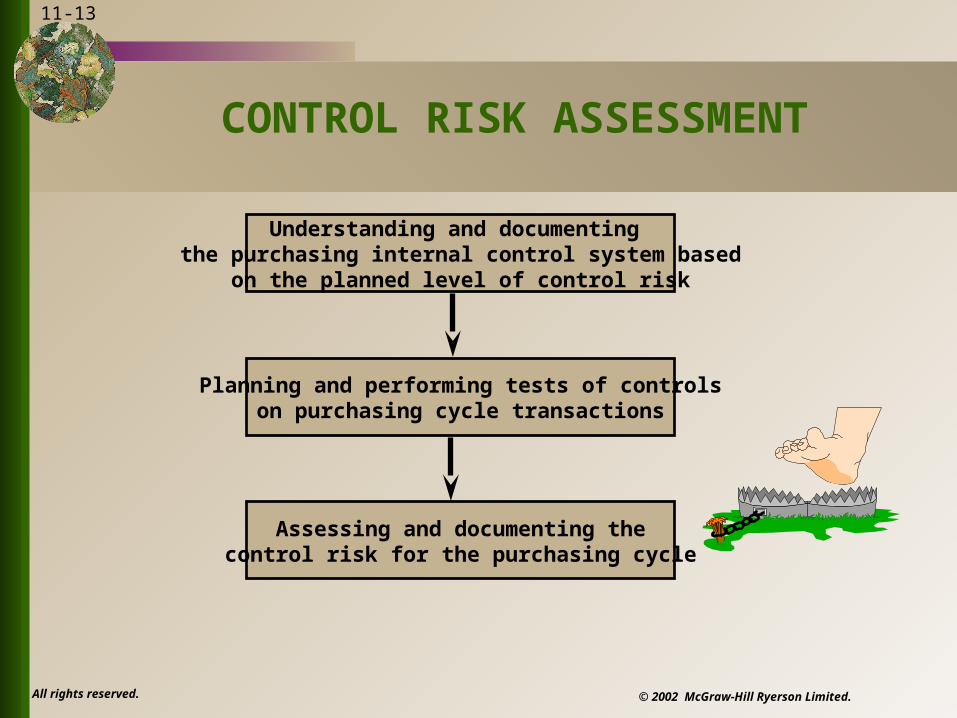

CONTROL RISK ASSESSMENT

Planning and performing tests of controlson purchasing cycle transactions

Understanding and documenting the purchasing internal control system based

on the planned level of control risk

Assessing and documenting thecontrol risk for the purchasing cycle

11-14

© 2002 McGraw-Hill Ryerson Limited.

All rights reserved.

UNDERSTANDING AND DOCUMENTING INTERNAL

CONTROL

Control environment Risk assessment Control activities Information and communication Monitoring

11-15

© 2002 McGraw-Hill Ryerson Limited.

All rights reserved.

CONTROL PROCEDURES AND TESTS OF CONTROLS -

PURCHASE TRANSACTIONS

Table 11-5 provides a summary of the internal control objectives, possible misstatements, internal control procedures, and tests of controls for purchase transactions.

11-16

© 2002 McGraw-Hill Ryerson Limited.

All rights reserved.

CONTROL PROCEDURES AND TESTS OF CONTROLS -

CASH DISBURSEMENT TRANSACTIONS

Table 11-6 provides a summary of the internal control objectives, possible misstatements, internal control procedures, and tests of controls for cash disbursement transactions.

11-17

© 2002 McGraw-Hill Ryerson Limited.

All rights reserved.

CONTROL PROCEDURES AND TESTS OF CONTROLS -

PURCHASE RETURNS TRANSACTIONS The number and magnitude of purchase returns

transactions is generally not material for most entities. Because of the possibility of manipulation the auditor

should at a minimum inquire about how the client controls purchase return transactions.

When goods are returned to a vendor, the client usually prepares a debit memo that reduces the amount of the vendor's accounts payable.

Analytical procedures are usually performed.

11-18

© 2002 McGraw-Hill Ryerson Limited.

All rights reserved.

AUDITING ACCOUNTS PAYABLE AND ACCRUED EXPENSES

Substantive tests of transactions Analytical procedures Tests of account balances

11-19

© 2002 McGraw-Hill Ryerson Limited.

All rights reserved.

SUBSTANTIVE TESTS OF TRANSACTIONS

The intended objective of such tests is to detect monetary misstatements.

Table 11-8 presents examples of substantive tests of transactions that may be used to test the audit objectives for accounts payable.

11-20

© 2002 McGraw-Hill Ryerson Limited.

All rights reserved.

ANALYTICAL PROCEDURES

Compare payables turnover and days outstanding in accounts payable to previous years’ and industry data.

Compare the current-year balances in accounts payable and accruals with prior years' balances.

Compare amounts owed to individual vendors in the current year's accounts payable listing to amounts owed in prior years.

Compare purchase returns and allowances as a percentage of revenue or cost of sales to prior years’ and industry data.

11-21

© 2002 McGraw-Hill Ryerson Limited.

All rights reserved.

TESTS OF ACCOUNT BALANCES

Table 11-10 summarizes the test of account balances for each audit objective.

11-22

© 2002 McGraw-Hill Ryerson Limited.

All rights reserved.

ACCOUNTS PAYABLE CONFIRMATIONS

Accounts payable confirmations are generally used less frequently by auditors than accounts receivable confirmations because the auditor generally has access to vendor invoices and monthly vendor statements.

The auditor focuses on large dollar accounts, regular vendors with small or zero balances, and a sample of other accounts.

11-23

© 2002 McGraw-Hill Ryerson Limited.

All rights reserved.

ACCOUNTS PAYABLE CONFIRMATIONS (cont.)

When confirming accounts payable, auditors generally use a form of positive confirmation referred to as a blank or zero balance confirmation.

See Exhibit 11-5 for a sample confirmation.

11-24

© 2002 McGraw-Hill Ryerson Limited.

All rights reserved.

EVALUATING THE AUDIT FINDINGS - PURCHASING

Compare total projected misstatement to tolerable misstatement.

Analyze misstatements for causes of errors. Conclude