2 · Web viewFigure 4.3 Loans of Danish households broken down into mortgage loans and other loans...

38

Room documents 5 STATISTICS DIRECTORATE National Accounts Household Financial Wealth: Trends, Structures and Valuation Methods Betina Sand Christensen and Tue Mollerup Mathiasen Paper Prepared for the 27 th General Conference of The International Association for Research in Income and Wealth - Stockholm, Sweden. August 18 – 24, 2002 OECD MEETING OF NATIONAL ACCOUNTS EXPERTS Château de la Muette, Paris 8-11 October 2002 Beginning at 9:30 a.m. on the first day

Transcript of 2 · Web viewFigure 4.3 Loans of Danish households broken down into mortgage loans and other loans...

Room documents 5

STATISTICS DIRECTORATE

National Accounts

Household Financial Wealth: Trends, Structures and Valuation MethodsBetina Sand Christensen and Tue Mollerup Mathiasen

Paper Prepared for the 27th General Conference of The International Association for Research in Income and Wealth - Stockholm, Sweden. August 18 – 24, 2002

OECD MEETING OF NATIONAL ACCOUNTS EXPERTS

Château de la Muette, Paris8-11 October 2002

Beginning at 9:30 a.m. on the first day

Session Number: Plenary session 3Session Title: Measuring Savings, Assets, and Liabilities:

From Macro- and Microeconomic PerspectivesPaper Number: 3Session Organizer: Barbara Fraumeni, Bureau of Economic Analysis, Washington, DC, USA

Thesia Garner, Bureau of Labor Statistics, Washington, DC, USADiscussant: Anne Harrison

Paper Prepared for the 27th General Conference ofThe International Association for Research in Income and Wealth

Stockholm, Sweden. August 18 – 24, 2002

Household Financial Wealth: Trends, Structures and Valuation Methods

Betina Sand Christensenand

Tue Mollerup Mathiasen

For additional information please contact:

Betina Sand Christensen and Tue Mollerup MathiasenSejrøgade 11DK-2111 København Ø[email protected] and [email protected]

This paper is placed on the following websites: www.iariw.org www.econ.nyu.edu/iariw

The views expressed in this paper are those of the authors. They do not necessarily represent the views of Statistics Denmark.

2

Abstract

Financial Accounts are now available in most of the EU countries in a comparable framework. The measurement of household financial wealth over time is one of the core issues of these statistics. Developments in household financial wealth are important for the analysis of consumer behaviour, which is central to the size and duration of recessions in the economy and the speed of subsequent recoveries. Therefore, the structure of financial wealth of the household sector, the valuation principles and the separation of transactions from revaluations are important topics.

Starting from the issue of the household sector debt situation, the paper offers a range of arguments favouring the study of Financial Accounts. The paper then deals with important quality issues from both a conceptual and a practical viewpoint concerning full accounts versus detailed instrument classification, consistency between non-financial National Accounts and Financial Accounts plus the problem of valuing unquoted shares and other equity. Finally, the structures and developments in household financial wealth are analysed for the EU countries.

1. Introduction

The purpose of this paper is to show how detailed information on households' financial wealth provided by Financial Accounts make possible a richer discussion of the household sector 1 debt situation. In section 2, a range of issues in measuring household debt are highlighted including servicing the debt, the phenomenon of risk, the micro-macro link and the lack of data on non-financial wealth.

In section 3, the quality and comparability of Financial Accounts in the EU+ 2 is in focus. First, the framework and the consistency restrictions on the full Financial Accounts are presented to form the basis for a discussion of calculation/publication strategies concerning full/partial accounts, the level of detail of the instrument classification, the issue of consistency between non-financial National Account and Financial Accounts and the calculation strategies concerning unquoted shares and other equities. In section 3.1, a partial evaluation of Financial Accounts is performed by comparing interest rate developments with revaluations of securities other than shares held by households. In section 3.2, the published household sector net lending/net borrowing from the capital account and the financial transactions account are compared for the EU+ countries. Finally, in section 3.3, calculation methods and results for household holdings of unquoted shares and other equity are presented for EU+ countries where possible. A partial analysis of variance across different implementation strategies for the same calculation method for valuation of unquoted companies in Denmark is outlined.

An economic analysis of household sector financial wealth for the EU+ countries is presented in section 4. The analysis is largely based on Financial Accounts data. Section 4.1 deals with the financial liabilities of the household sector focusing on transactions in loans, households' debt as a proportion of disposable gross income, mortgage loans and the development in real estate prices. As an illustration of the issue of households' ability to service debt, Danish mortgage lending, debt service payments to mortgage banks and household disposable income are compared. Section 4.2 turns to the asset side of the household sector balance sheet. Financial assets are compared to financial liabilities and the developments in the composition of financial assets across the EU+ is described with a reference to transactions and price changes. Finally, in section 4.3, the micro-macro link is in focus when discussing the net wealth of households.

1 Throughout the paper, the "household sector" includes Non Profit Institutions Serving Households (NPISH) if otherwise not stated. The impact of the inclusion to the analyses performed is marginal.

2 Throughout the paper, EU+ refers to EU Member States excluding Luxembourg, Greece and Ireland but including Norway.

3

2. Measurement of household debt

Over the last decade, a rise in household sector gross debt relative to disposable income has been observed in a number of western economies. It is sometimes argued3 that the level of indebtedness is partly determined by procyclical behaviour in the financial system and partly by one of the main features of "New Economics"; high growth and low inflation increasing the scope for households' "money illusion"4. Because of the observations on household debt, it is discussed whether the level of the household sector indebtedness is important for the size and duration of a recession/downturn in an economy and the speed of the eventual recovery. The reason behind this is that a high level of indebtedness in the beginning of a recession should not give much room for an expansive monetary policy to work through the monetary transmission mechanism5. The higher a fixed interest rate debt proportion to total debt, the more relevant this argument seems.

Because of the fact that the discussion derives from the observation of an increased gross indebtedness, it is important to explore; what is the best way to measure indebtedness in a macroeconomic perspective, and how is this related to the microeconomic perspective?

The most direct macroeconomic effect from changes in household gross debt works through debt service payments6. The level of debt service payments is affected by the level of debt, interest rates and the maturity of the debt. Therefore, an increased level of household gross debt may not lead to an increased direct burden on households if real interest rates are falling and/or the maturity of the debt is increased, which may be facilitated by rising prices of real estate. Households' debt service relative to disposable income has been calculated for a few countries only (to our knowledge the U.S. and the U.K.) and shows more diverse patterns over the past ten years than is the case for the simpler measure of gross debt relative to disposable income.

A fundamental question to ask, is whether – in a macroeconomic perspective – the idea of discussing the indebtedness solely by looking at the households' liability side is too narrow after all?7 Many economists argue that the worries based on indicators of households' liability side are exaggerated because information on the asset side is ignored – financial as well as non-financial.

First, debt service payments relative to disposable income is a measure of the debt burden based on the liability side of households. If a net measure were to be considered sufficient for macroeconomic analysis, it should be made probable that individual households (at the micro level) simultaneously engage in borrowing and lending with free funds. This is not very likely, because most households would find it very difficult to make any profits from such arrangements.

Secondly, if we look at household net wealth as opposed to household gross debt, three main issues have to be considered: The phenomenon of risk, the micro-macro link and the lack of data on non-financial wealth.

As for risk, households' net wealth does not contain any information on the risk exposure of households – risk exposure in the sense of variability of net wealth due to interest rate and price fluctuations and in the sense of differences in liquidity of financial instruments and non-financial assets. Examples of financial and non-financial transactions having no effect on either net wealth or on risk exposure can be found – but they are rare and often without much logic. Such an example is taking a bank loan and parallel to that, making a bank deposit. If no interest rate difference on loans and deposits is assumed, the present and future net wealth and risk exposure is unaffected. If instead the proceeds from the bank loan are invested in 3 See e.g. The Economist, January 26th 2002, "Dicing with debt".4 "Money illusion" is exemplified by the phenomenon where borrowing at low nominal interest rates is considered

cheaper compared to borrowing at high nominal interest rates although the real interest rates may be unchanged.5 The "monetary transmission mechanism" partly works through the fact, that lowering interest rates creates

increased demand for loans thereby adding to the growth of the economy by raising demand.6 The household debt-service burden is the ratio of household debt payments (interest and repayment) to disposable

income.7 See e.g. Federal Reserve Bulletin, July 2001, "The U.S. Flow of Funds Accounts and Their Uses".

4

shares or property, the risk exposure is changed both in the sense of net wealth variability and exposure to differences in liquidity, although this is not the case for current net wealth. In the case of real estate investment e.g., risk exposure to price changes due to changes in interest rates8 can be minimised by the use of financing based on bonds with long maturity which will tend to create parallel fluctuations of assets and liabilities. This, however, only moderates the fact that financial and non-financial transactions in general do affect risk exposure.

The second issue when focusing on household sector net wealth (based on macro-statistics) concerns the micro-macro link. In general, no micro-based financial household wealth statistics are available with the same consistent approach regarding stocks, transactions and revaluations as found in the "Financial Accounts" of the "System of National Accounts" (SNA93) / "European System of Accounts" (ESA95).

Financial Accounts form an integrated part of National Accounts. The non-financial National Accounts show how income is created as a result of the productive activity in an economy, distributed and re-distributed to form the basis for consumption and investment and conclude with the capital account's expression of financial net lending/net borrowing. The Financial Accounts show the financial investments and funding with a direct link to the net lending/net borrowing of each individual sector. In Financial Accounts, both the actual transactions, revaluations, defaults and stocks of a complete range of financial instruments are presented.

The weakness of Financial Accounts for macroeconomic analysis of the household sector concerns the macro-foundation of the accounts. The investments and funding of the sector form an aggregated picture, and must be analysed as such. The redistribution of wealth within the sector is not accounted for. This gives rise to classical problems when analysing and predicting the macroeconomic effects of changes to inflation, interest rates, asset prices etc. due to heterogeneity of financial wealth characteristics across individual households.

The third issue to take into account when advocating the use of household sector net wealth, as opposed to household sector gross debt in macroeconomic analysis, is the widespread lack of information on non-financial wealth of households - primarily made up of real estate. This information is an integral part of the System of National Accounts, but balance sheets for the household sector are currently only in the process of being developed in the EU countries. Information on household wealth in non-financial assets is essential in order to assess the risk exposure of households.

Two conclusions can be drawn: First, debt service payments relative to disposable income seem to be an unrivalled measure of the direct macroeconomic effects of household debt. As the calculations of this measure are partly based on detailed Financial Accounts9, more countries should in future be able to calculate this measure. In this paper, a first partial estimate is presented for Denmark10. Secondly, both practical problems and theoretical arguments against a complete shift of focus in macroeconomic analysis from household sector gross debt to household sector net wealth can be listed. Nevertheless, the information on financial wealth provided by Financial Accounts would seem to allow a richer discussion of the household sector debt situation.

3. Financial Accounts - quality and comparability within the EU+

The quality of Financial Accounts is essential to the applicability of these statistics. Financial Accounts - being a part of National Accounts - form a consistent set of accounts. Consistency is a quality in its own right, but also the tool for improving quality by means of reconciliation of data derived from different sources. Due to lack of available sources, consistency restrictions (accounting identities) are used broadly across Financial Accounts in the account, sector and instrument dimensions to close the gaps. Therefore, the quality assessment of data published in Financial Accounts should be viewed in the light of consistency/inconsistency, the results of 8 Often, econometric models show a link between real estate prices and the level of nominal interest rates interpreted

to be a result of the link between debt service payments and interest rates.9 For more information about the calculation/estimation of debt service burden, see

http://www.federalreserve.gov/releases/housedebt/about.htm10 This estimate is not based on Financial Accounts.

5

macroeconomic quality checks, the sources available and the calculation methods used. It is clear that the more detailed the instrument and sector breakdown, the more precise the macroeconomic quality checks. Last but not least, to users of Financial Accounts the level of detail and publication delays are central issues of quality.

There are three consistency restrictions on the Financial Accounts: Consistency across accounts. Consistency across sectors. Consistency between non-financial National Accounts and Financial Accounts.

Consistency across accounts is achieved if for each instrument, sector and asset/liability side the following identity holds:

beginning of period stock +financial transactions + other changes in volume11 + revaluations

end of period stock

Consistency across sectors is achieved, if for each instrument and account the sum over sectors on the asset side equals the liability side. E.g., net borrowing of one sector is financed by net lending of other sectors.

Consistency between non-financial National Accounts and Financial Accounts is achieved if the net lending/net borrowing in the capital account of each sector is identical to the net transactions by sector in the financial transactions account.

3.1 The issue of full accounts versus detailed instrument classification

In the European Union, a detailed programme of National Accounts data deliveries within the framework of ESA95 has been laid down in a Council Regulation12. Concerning Financial Accounts, the regulation stipulates the minimum requirements of the Member States. The requirements are shown in table 3.1.

Table 3.1 Financial Accounts; minimum requirements of European Union Member States13

Accounts Instruments SectorsIII.2 Financial account (trans.)

(A)F.1 Monetary gold and SDR

S.1 Total economy

IV Balance sheets (A)F.2 Currency and deposits

S.11 Non-financial corporations

(A)F.3 Securities other than shares

S.12 Financial corporations

(A)F.4 Loans S.121/S.122 Central Bank and other monetary financial institutions

(A)F.5 Shares and other equity

S.123 Other financial intermediaries

(A)F.6 Insurance technical reserves

S.124 Financial auxiliaries

(A)F.61 Net equity of households in

S.125 Insurance corporations and pension funds

life insurance reserves and in pension

S.13 General government

funds reserves S.1311/S.1312 Central and state government(A)F.62 Prepayments of insurance

S.1313 Local government

premiums and reserves for S.1314 Social security fundsoutstanding claims S.14/S.15 Households and non-profit institutions

serving households

11 E.g. losses.12 Council Regulation (EC) No 2223/96 of 25 June 199613 During a transition period up to January 2005, derogations from the base program have been given to certain

Member States concerning the level of detail and delay of transmission.

6

(A)F.7 Other accounts receivable/payable

S.2 Rest of the world

If countries only satisfy the minimum requirements, consistency across accounts is no longer a restriction on the published accounts because the other changes in volume and revaluation accounts are not required. Still, a macroeconomic quality check of the non-compulsory accounts - calculated as a residual - is an indirect quality check of the accounts published.

Comparing revaluations on household holdings of securities other than shares with observed interest rate fluctuations is an example of a macroeconomic quality check. The comparison is most relevant, because interest rates and the price of bills, bonds, commercial papers, financial derivatives etc. are negatively correlated. It may be argued that the negative correlation in regard to household sector holdings may be disturbed by changes in the term structure of interest rates and changes in the duration of household portfolios. In figure 3.1, interest rates on 10-year government bonds and 3-month interest rates for four countries outside the euro area and Germany (euro area from 1999) is presented. Long-term interest rates across the EU+ have moved in parallel for some years. Focusing on the period 1998-1999, a sharp fall in long-term interest rates in 1998 (except for Norway) and a sharp rise in 1999 is observed. Looking at short-term interest rates, it is seen that the term structure has indeed changed over the period (most pronounced for Norway). Still, short-term interest rates were in general falling across the EU+ up to the introduction of the euro, and they were in general stable in 1999.

In figure 3.214 and 3.3 revaluations (including other changes in volume if calculated as a residual15), transactions and holdings of securities other than shares by households are presented. Figure 3.2 presents EU+ countries with published revaluations, figure 3.3 EU+ countries with no published revaluations.

14 Note of interpretation: Denmark - left axis; holdings of securities other than shares decreasing over time due to (right axis; transactions and revaluations) net sales in 1996-1999 and decreasing positive revaluations (negative in 1999). Euro-conversions create minor inconsistencies.

15 In the remainder of the paper the term "revaluation" will be used both in the case of published revaluations and revaluations calculated as a residual. The residual does also include other changes in volume, but - in general - these changes are relatively small and should not affect the conclusions drawn.

7

Figure 3.1 Interest rates in selected countries

2345678

1994 dec. 1995 dec. 1996 dec. 1997 dec. 1998 dec. 1999 dec. 2000 dec.

Pct. (monthly average) GERMANY

23456789

10

1994 dec. 1995 dec. 1996 dec. 1997 dec. 1998 dec. 1999 dec. 2000 dec.

Pct. (monthly average) DENMARK

3456789

1994 dec. 1995 dec. 1996 dec. 1997 dec. 1998 dec. 1999 dec. 2000 dec.

Pct. (monthly average) NORWAY

2

4

6

8

10

12

1994 dec. 1995 dec. 1996 dec. 1997 dec. 1998 dec. 1999 dec. 2000 dec.

Pct. (monthly average) SWEDEN

4

5

6

7

8

9

1994 dec. 1995 dec. 1996 dec. 1997 dec. 1998 dec. 1999 dec. 2000 dec.10-year government bond 3-month interest rate

Pct. (monthly average) UNITED KINGDOM

Source: Danmarks Nationalbank

Figure 3.2 Securities other than shares held by households (EU+ countries with published revaluations)

25.00026.00027.00028.00029.00030.00031.000

1995 1996 1997 1998 1999 2000-3.000-2.000-1.00001.0002.0003.000

DENMARKEnd-of-year stockmill. euro

Transactions/revaluationsmill. euro

70.000

80.000

90.000

100.000

110.000

1995 1996 1997 1998 1999 2000-30.000

-20.000

-10.000

0

10.000FRANCEEnd-of-year stock

mill. euroTransactions/revaluations

mill. euro

24.00025.00026.00027.00028.00029.000

1995 1996 1997 1998 1999 2000-3.000-2.000-1.00001.0002.000

NETHERLANDSEnd-of-year stockmill. euro

Transactions/revaluationsmill. euro

500

1.000

1.500

2.000

2.500

1995 1996 1997 1998 1999 2000-500

0

500

1.000

1.500

Transactions Revaluations End-of-year stock

NORWAYEnd-of-year stockmill. euro

Transactions/revaluationsmill. euro

8

Source: New Chronos

9

Figure 3.3 Securities other than shares held by households (EU+ countries with no published revaluations and an EU+ total)

15.000

20.000

25.000

30.000

35.000

1996 1997 1998 1999 2000-10.000

-5.000

0

5.000

10.000AUSTRIAEnd-of-year stock

mill. euroTransactions/revaluations

mill. euro

150.000

154.000

158.000

162.000

166.000

1995 1996 1997 1998 1999 2000-8.000

-4.000

0

4.000

8.000

End-of-year stockmill. euro

Transactions/revaluationsmill. euroBELGIUM

340.000

350.000

360.000

370.000

380.000

1996 1997 1998 1999 2000-20.000

-10.000

0

10.000

20.000GERMANYEnd-of-year stock

mill. euroTransactions/revaluations

mill. euro

13.00015.00017.00019.00021.00023.000

1996 1997 1998 1999 2000-4.000-2.00002.0004.0006.000

SPAINEnd-of-year stockmill. euro

Transactions/revaluationsmill. euro

1.0001.5002.0002.5003.0003.5004.000

1996 1997 1998 1999 2000-2.000-1.500-1.000-50005001.000

FINLANDEnd-of-year stockmill. euro

Transactions/revaluationsmill. euro

400.000

450.000

500.000

550.000

600.000

1996 1997 1998 1999 2000-100.000

-50.000

0

50.000

100.000ITALYEnd-of-year stock

mill. euroTransactions/revaluations

mill. euro

1.000

2.000

3.000

4.000

5.000

1996 1997 1998 1999 2000-2.000

-1.000

0

1.000

2.000PORTUGALEnd-of-year stock

mill. euroTransactions/revaluations

mill. euro

12.00014.00016.00018.00020.00022.000

1996 1997 1998 1999 2000-6.000-4.000-2.00002.0004.000

SWEDENEnd-of-year stockmill. euro

Transactions/revaluationsmill. euro

35.00040.00045.00050.00055.00060.00065.000

1995 1996 1997 1998 1999 2000-15.000-10.000-5.00005.00010.00015.000

UNITED KINGDOMEnd-of-year stockmill. euro

Transactions/revaluationsmill. euro

1.150.0001.200.0001.250.0001.300.0001.350.0001.400.000

1996 1997 1998 1999 2000-150.000-100.000-50.000050.000100.000

Transactions Revaluations End-of-year stock

EU+End-of-year stockmill. euro

Transactions/revaluationsmill. euro

Source: New Chronos

10

Looking at the interest rate fluctuations in figure 3.1, we would expect (possibly with the exception of Norway) positive revaluations in household holdings of securities other than shares in 1998 and negative revaluations in 1999.

Four out of four countries publishing full accounts are seen to have interest rate compatible patterns of revaluations during 1998 and 1999. On the other hand, only one out of nine countries (Italy) are seen to have interest rate compatible patterns of revaluations when calculated as a residual. This would suggest a strong case for setting up a consistent system with full possibilities for checking the revaluations in a systematic way.

Turning to the classification issue, the more detailed the instrument and sector classifications the more accurate the checks and uses of Financial Accounts. The instrument classification publication strategies (via Eurostat's New Chronos database) across the EU+ are presented in table 3.2.

Table 3.2 Instrument classification publication16 strategies

Instrument/Country1 AT

BE

DE

DK

ES

FI

FR

IT

NL

NO

PT

SE

UK

(A)F.1 Monetary gold and SDR (A)F.2 Currency and deposits (A)F.21 Currency (A)F.22 Transferable deposits (A)F.29 Other deposits

(A)F.3 Securities other than shares (A)F.33 Securities other than shares, excluding financial derivatives

(A)F.331 Short-term - Securities other than shares, excluding financial derivatives

(A)F.332 Long-term - Securities other than shares, excluding financial derivatives

(A)F.34 Financial derivatives (A)F.4 Loans (A)F.41 Short-term - Loans (A)F.42 Long-term - Loans

(A)F.5 Shares and other equity (A)F.51 Shares and other equity, excluding mutual funds shares (A)F.511 Quoted shares (A)F.512 Unquoted shares (A)F.513 Other equity

(A)F.52 Mutual funds shares (A)F.6 Insurance technical reserves (A)F.61 Net equity of househ. in life ins. reserves and in pension funds reserves

(A)F.611 Net equity of households in life insurance reserves (A)F.612 Net equity of households in pension funds reserves

(A)F.62 Prepayments of insurance premiums and reserves for outstanding claims

(A)F.7 Other accounts receivable (A)F.71 Trade credits and advances (A)F.79 Other accounts receivable/payable, except trade credits and advances

Source: New Chronos1 AT: Austria, BE: Belgium, DE: Germany, DK: Denmark, ES: Spain, FI: Finland, FR: France, IT: Italy, NL:

Netherlands, NO: Norway, PT: Portugal, SE: Sweden, UK: United Kingdom

Comparing the evidence on published accounts (New Chronos) and published instrument classification (table 3.2), EU+ countries can be grouped according to publication strategies (table 3.3).

16 It should be noted that some countries' national publication strategies differ markedly from what is published internationally (via Eurostat's New Chronos database). E.g. in the case of the UK, a much more detailed national publication strategy is observed compared to the international strategy.

11

Table 3.3 Publication strategy - full accounts versus detailed instrument classification

Publication strategy/Country AT

BE

DE

DK

ES

FI

FR

IT

NL

NO

PT

SE

UK

Detailed instrument classification and full accounts Detailed instrument classification; less than full accounts Full accounts; aggregated instrument classification Minimum requirements

Source: New Chronos

Based on the very simple - and yet indicative - quality check above, a strategy giving high priority to a detailed instrument classification alone does not seem to be the optimal strategy. Furthermore, comparability across countries may be harmed by differences in publication and calculation strategies.

3.2 The issue of consistency between non-financial National Accounts and Financial Accounts

Consistency between non-financial National Accounts and Financial Accounts is also tackled differently across the EU+. Net lending/net borrowing in the capital account and financial (transaction) account of each sector are not required to be identical in the majority of countries even though conceptually they should be. Figure 3.4 shows published net lending/net borrowing figures of households for the two accounts.

Figure 3.4 Household sector net lending/net borrowing from the capital account and the financial account

-2,500,002,505,007,50

1995 1996 1997 1998 1999 2000

net lending/net borrowingpct. of GDP AUSTRIA

2,505,007,50

10,0012,50

1995 1996 1997 1998 1999 2000

BELGIUMnet lending/net borrowingpct. of GDP

0,002,505,007,50

10,00

1995 1996 1997 1998 1999 2000

GERMANYnet lending/net borrowingpct. of GDP

-5,00-2,500,002,505,00

1995 1996 1997 1998 1999 2000

DENMARKnet lending/net borrowingpct. of GDP

12

0,002,505,007,50

10,00

1995 1996 1997 1998 1999 2000

SPAINnet lending/net borrowingpct. of GDP

0,002,505,007,50

10,00

1995 1996 1997 1998 1999 2000

FINLANDnet lending/net borrowingpct. of GDP

0,002,505,007,50

10,00

1995 1996 1997 1998 1999 2000

FRANCEnet lending/net borrowingpct. of GDP

2,505,007,50

10,0012,50

1995 1996 1997 1998 1999 2000

Capital account Financial account

ITALYnet lending/net borrowingpct. of GDP

Figure 3.4 (continued)

-2,500,002,505,007,50

1995 1996 1997 1998 1999 2000

NETHERLANDSnet lending/net borrowingpct. of GDP

-2,500,002,505,007,50

1995 1996 1997 1998 1999 2000

NORWAYnet lending/net borrowingpct. of GDP

-2,500,002,505,007,50

1995 1996 1997 1998 1999 2000

PORTUGALnet lending/net borrowingpct. of GDP

-2,500,002,505,007,50

1995 1996 1997 1998 1999 2000

SWEDENnet lending/net borrowingpct. of GDP

-2,500,002,505,007,50

1995 1996 1997 1998 1999 2000

Capital account Financial account

UNITED KINGDOMnet lending/net borrowingpct. of GDP

Source: New Chronos and National Statistical Offices

13

Substantial differences in publication strategies can be observed across the EU+ countries. Belgium is an example of a country with continuously large published statistical discrepancies, Germany, Spain and Sweden are examples of countries publishing only minor discrepancies and Denmark is an example (the only one) of a country publishing fully balanced National Accounts. It is important to note that the published discrepancies are not a measure of data quality. Such a measure would have to rely on pre-balancing figures.

Figure 3.4 illustrates a problem to the users of non-financial National Accounts and Financial Accounts; how to deal with inconsistency / statistical discrepancies? The statistical discrepancy is analogous to the statistical discrepancies between the initial estimates of GDP from the output side (GDP(O)), the expenditure side (GDP(E)) and the income side (GDP(I)). As far as GDP (goods and services, primary income) is concerned, all EU countries have accepted that the National Accounts should be balanced. Some countries, which originally did not balance their non-financial National Accounts, but merely presented the three different estimates of GDP together with a simple arithmetic average of them, abandoned that practice more than a decade ago.

Given that all EU countries now accept that there should be no statistical discrepancies regarding GDP, it seems surprising that a similar consensus does not exist regarding net lending/net borrowing17. Perhaps this has to do with the fact that in the majority of Member States the non-financial National Accounts are compiled by the statistical offices, whereas the financial accounts are produced by the central banks. However, this institutional matter is of no relevance to the substance of the issue. Again, comparability across countries may be harmed by differences in publication and calculation strategies18.

3.3 Calculation strategies concerning unquoted shares and other equity

Through the work in the Financial Accounts Working Party (FAWP) led by Eurostat (the Commission of the EU) and in the Working Group on Monetary Union Financial Accounts led by the European Central Bank (ECB), a great deal of work has gone into harmonising calculation strategies in Financial Accounts across Europe (including Candidate Countries). One of the most difficult areas in this work concerns the valuation of unquoted shares and other equity. For the household sector, unquoted shares and other equity make up an important part of financial wealth and its development over time. The importance for the household sector in EU+ countries with published figures19 is presented in figure 3.520.

Household holdings of unquoted shares and other equity relative to total financial assets in 2000 range from 10.6 per cent in Norway to 33 per cent in France. In general, the importance has been growing since 1995 primarily due to substantial positive revaluations. In a number of countries revaluations on unquoted shares and other equity are the primary source of revaluations on households' total financial assets. These observations make the harmonisation of calculation strategies all the more important, given the fact that differences across countries may in part be the result of differing valuation and sectorisation methods.

17 See also Eurostat, 2002, "Manual on Sources and Methods - Financial Accounts".18 See also ECB, 14 May 2002, "Compilation of a Consistent Accumulation Account for the euro area" for suggested

solutions to the problem of inconsistency.19 In the case of Denmark, data concerning unquoted shares are not published via Eurostat's New Chronos database -

this might also be the case for other EU+ countries.20 Note of interpretation: Belgium - left axis; total financial asset holdings and holdings of unquoted shares and other

equity both rising steadily over time due to (right axis; transactions and revaluations) positive financial net transactions and revaluations. In 1995, 1997 and 2000, revaluations of unquoted shares and other equity (F.512 and F.513) and total revaluations (F.) are comparable in size.

14

Figure 3.5 Total financial assets and unquoted shares and other equity held by households

0

200.000

400.000

600.000

800.000

1995 1996 1997 1998 1999 2000-25.000

0

25.000

50.000

75.000

End-of-year stockmill. euro

Transactions/revaluationsmill. euroBELGIUM

0

100.000

200.000

300.000

1995 1996 1997 1998 1999 2000-10.000

0

10.000

20.000DENMARKEnd-of-year stock

mill. euroTransactions/revaluations

mill. euro

0

500.000

1.000.000

1.500.000

1996 1997 1998 1999 2000-100.000

0

100.000

200.000SPAINEnd-of-year stock

mill. euroTransactions/revaluations

mill. euro

0

1.000.000

2.000.000

3.000.000

4.000.000

1995 1996 1997 1998 1999 2000-200.000

0

200.000

400.000

600.000FRANCEEnd-of-year stock

mill. euroTransactions/revaluations

mill. euro

0

50.000

100.000

150.000

200.000

1996 1997 1998 1999 2000-5.000

0

5.000

10.000

15.000NORWAYEnd-of-year stock

mill. euroTransactions/revaluations

mill. euro

0100.000200.000300.000400.000500.000

1996 1997 1998 1999 2000-25.000025.00050.00075.000100.000

F. Transactions F.512/513 TransactionsF. Revaluations F.512/513 RevaluationsF. End-of-year stock F.512/513 End-of-year stock

SWEDENEnd-of-year stockmill. euro

Transactions/revaluationsmill. euro

Source: New Chronos and National Statistical Offices

Both ESA9521 and SNA9322 are quite specific when formulating the characteristics of an estimation method concerning market valuation of unquoted shares and other equity:

Reference to the values of quoted shares. Taking into account differences between quoted/unquoted shares, notably their

liquidity. Considering the reserves accumulated over the life of the corporation. Recommending a sector-based approach.

Variations in valuation methods chosen across the EU+ (presented in table 3.4) are partly being explained by differences in data availability and partly by the relative size of the market for quoted companies.

Table 3.4 Unquoted shares and other equity - (liability side sector23 specific) valuation methods

Valuation methods

AT BE DE DK ES FI4 FR IT NL NO5 PT SE UK6

21 See paragraph 7.54 and 7.5522 See paragraph 13.7323 See table 3.1 for sectorisation

15

COFBV1

S.122

S.11, 12

OFBV2 S.12 S.11 NOR3 S.11

Source: Eurostat, 2002, "Manual on Sources and Methods - Financial Accounts" and National Statistical Offices

1 Applying the ratio capitalisation to own funds at book value of quoted companies to unquoted corporations' own funds at book value

2 Own funds at book value

3 Capitalisation (with reference to quoted companies) of weighted moving average of net operating results (comparable to the price-earnings ratio method)

4 Method based on counterpart information

5 Unknown method 6 Method based on a historical study

From a theoretical point of view, also the method of "price-earnings ratio" (PER) is attractive due to its reference to information considered by the market in pricing stocks. Both the NOR and PER methods are very demanding in terms of data availability. As regards the valuation methods chosen by the EU+ countries, especially the COFBV and NOR valuation methods can be implemented with great flexibility allowing for substantial variations in output from each method. Concerning the COFBV method, implementation requires decisions in the following areas:

Delimitation of the population of quoted and unquoted companies to ensure "comparability".

Distinction of branches to balance the need for a sufficient representation in the market and the wish for a method to mirror differences in earnings prospects across branches.

The calculation method for ratios.

In figure 3.6, the ratio capitalisation to own funds at book value of quoted companies based on four possible strategies of implementing the COFBV method in Denmark is presented. The four strategies are:

Strategy 1; Most traded quoted companies excluded (KFX-index members) - 9 branch stratification

Strategy 2; Most traded quoted companies excluded (KFX-index members) - no stratification

Strategy 3; No delimitation of the population of quoted companies - 9 branch stratification

Strategy 4; No delimitation of the populations of quoted companies - no stratification

Figure 3.6 Ratio capitalisation to own funds at book value of quoted companies and market value of unquoted non-financial corporations - four possible strategies for implementing the COFBV method in Denmark

11,5

22,5

33,5

1994 1995 1996 1997 1998 1999 2000

Ratio

250005000075000

100000125000150000

1994 1995 1996 1997 1998 1999 2000Strategy 1 Strategy 2Strategy 3 Strategy 4

Mill. euro

Source: Statistics Denmark

It is evident that not only is the choice of method essential to the output by means of level and variability, so also is the choice of implementation strategy. This finding is in line with other pilot studies in the field. Currently, Statistics Denmark uses COFBV strategy 1 which is deemed to be the most appealing method from a theoretical point of view given the current availability of data on unquoted companies.

16

The estimated market value of unquoted non-financial corporations is directly mirrored in the holding of the household sector. Comparisons across countries are seriously inhibited by differences in methods and implementation strategy. In this light, a working group on unquoted shares has been created by the FAWP in order to increase the comparability of data on unquoted shares across countries within the general accounting principles of ESA95.

4. Analysis of the household sector financial wealth

The development of households' financial balance sheets is a daily focus point of many economic agents. Besides being an important issue for the individual household (and the individuals comprising the households), households' financial situation is of interest to both financial and non-financial enterprises.

As far as financial corporations are concerned, households' financial position is important due to the fact that the operating profits of financial corporations are determined to a considerable extent by their dealings with the household sector through deposit taking, writing of insurance as well as portfolio management. Thereby, households' portfolio choice and financial health influence the pattern of financial intermediation and disintermediation and the circumstances under which the financial corporations act.

Regarding the non-financial enterprises the importance of the development of the households' financial position is to a great extent connected to the real effects of the households' financial activity – that is the effect on spending. The real effect of changes in household financial position is related to the households' propensity to transform increases in financial wealth into spending or to finance consumption by credit. The latter is the well-known wealth effect in the consumption function24. The wide-ranging impact of changes of households' financial position, make the sector's financial balance sheet a factor of great interest to analysts dealing with tendencies in the financial as well as the real economy. Starting from the Financial Accounts of households reported by the EU+ countries for years 1995 to 2000, the financial position of the households will be examined below.

4.1 The financial liabilities of the household sector

Over the past couple of years, the development of households' debt in particular has been a subject of concern to many analysts. The focus is caused by a massive rise of household sector debt both in Europe and in the United States.

Referring to the end-of-year stock data of the Financial Accounts, the debt of the households of the EU+ countries has without exception undergone an increase from year 1995 to 2000 – in the EU+ as a whole, the debt of the households has increased by almost 47 per cent. However, the magnitude of the rise of the households' debt differs considerably from country to country from a 15 per cent increase in Finland to nothing less than a 108 per cent increase of the debt of the Portuguese households25. In comparison, the GDP at current prices of the euro area grew by approximately 21 per cent from 1995 to 200026.

The balance sheets of the Financial Accounts give a picture at a given point in time of the financial situation of the sectors. More precisely, they give the accumulated volume of the financial transactions carried out by the households over the years, inclusive of other changes in the form of for instance losses (i.e. other changes in volume) and asset price changes (i.e. revaluations). At the same time, the balance sheets make it possible to assess the composition of the financing of the sectors.

24 See for instance National Bureau of Economic Research, Nov. 2001, "Comparing Wealth Effects: The Stock Market Versus the Housing Market" by Karl E. Case, John M. Quigley and Robert J. Schiller.

25 The 108 per cent increase covers the increase of debt from 1995 to 1999, since no 2000-data are yet available on the households of Portugal .

26 European Central Bank, Jan. 2001 & May 2002, "Monthly Bulletin".

17

As might be expected, the liability side of the household sector is dominated by loans. In the EU+ as an aggregate, loans to households made up 92 per cent of the liabilities at the end of year 2000. Depending on the proportion of self-employed in the countries, other instruments may be a source of household financing – in particular other accounts payable. The relevance of loans to the development of household debt is demonstrated in figure 4.1, from which it appears that household indebtedness is largely explained by the sector's financial transactions in loans. The figure also shows that revaluations in loans have a relatively small influence on the development of household debt.

Figure 4.1 EU+ households' debt plus transactions and revaluations in loans

3.000.0003.500.0004.000.0004.500.0005.000.0005.500.000

1995 1996 1997 1998 1999 2000-100.0000100.000200.000300.000400.000

Transactions in loans Revaluations in loansEnd-of-year debt End-of-year loans

End-of-year debt/loansmill. euro

Transactions/revaluations mill. euro

Source: New Chronos

The question is whether the development of household debt is critical. Most individuals may consider debt to be a necessary evil in itself. From an economic point of view, a certain amount of debt is, however, desirable. Surplus savings is better off being lent to borrowers making profitable investments than to lie under the mattress of the savers – thereby, the establishment of debt through the financial intermediation of funds from savers to borrowers ensures the most profitable exploitation of the resources of an economy. Nevertheless, looking at gross debt as the sum of the households' liabilities as stated in the Financial Accounts, the development of household indebtedness certainly may look somewhat worrying. To assess the gravity of the evolution of household debt solely by looking at the development of gross debt is, however, not quite adequate. Overall, the seriousness of the remarkable rise in debt is, basically, a question of the ability of the households to service their loans.

In planning their borrowing, households make assumptions about loan terms, future income and future capital gains on assets to make sure that obligations can be met. That is why the households' debt service payment – i.e. household debt payment (interest and repayment) in proportion to disposable income – is a better measure of the sustainability of debt. In the lack of such measures, an immediate evaluation of the development of household debt has to involve at least the development of households' income after taxes. Therefore, household debt is set in proportion to gross disposable income of each EU+ country as shown in figure 4.2.

The figure shows that even when taking increases in population, prices and volume of economic activity into consideration, which is done by looking at debt as a proportion of disposable income, a substantial rise of household debt has taken place in many of the EU+ countries. Counting Finland as the only exception, household debt as a proportion of disposable income has been increasing throughout EU+. Dutch households account for the highest rise of debt in proportion to disposable income with a 45 per cent increase, while the household sector's debt rose 22 per cent in the EU+ as a whole. The EU+ household debt rose from a debt ratio of 78 per cent at the end of 1995 to a debt ratio of 96 per cent of disposable income in 2000.

Figure 4.2 also shows substantial differences among countries as to the level of the debt in proportion to disposable income, from a household debt ratio of about 45 per cent in Italy at the end of year 2000 to a ratio of 202 per cent in Denmark. The ratio implies that the average Danish household in 2000 owes a little more than two euro for each euro of disposable income.

18

Figure 4.2 Households' debt as a proportion of disposable gross income

050

100150200250

1995 1996 1997 1998 1999 2000Austria Belgium Germany Denmark

Pct.

050

100150200250

1995 1996 1997 1998 1999 2000Spain Finland Italy

Pct.

050

100150200250

1995 1996 1997 1998 1999 2000France Netherlands Norway Sweden

Pct.

050

100150200250

1995 1996 1997 1998 1999 2000Portugal United Kingdom EU+

Pct.

Source: New Chronos and National Statistical Offices

What are the explanations for the sustained rise of household debt throughout EU+? Are the households simply being more (maybe even too) optimistic about their future income and their ability to service their loans? Since Danish households are the most indebted households of the EU+ seen in proportion to disposable income, it is worth taking a closer look at the development of the debt of households in Denmark.

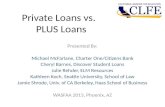

As is the case of every other EU+ country, the debt of Danish households is primarily comprised by loans. At the end of year 2000, loans made up 89 per cent of households' debt. The increase of the loans of the Danish households from 1995 to 2000 is largely explained by an increase in the stock of mortgage loans – approximately 71 per cent of the increase of household loans was caused by an increase in the stock of mortgage loans. The development of loans of Danish households broken down into mortgage loans and other loans is shown in figure 4.3.

Figure 4.3 Loans of Danish households broken down into mortgage loans and other loans

025.00050.00075.000

100.000125.000150.000175.000

1995 1996 1997 1998 1999 2000

End-of-year stock, mortgage loans End-of-year stock, other loans

End-of-year stockmill. euro

-5.000-2.500

02.5005.0007.500

10.000

1995 1996 1997 1998 1999 2000Transactions, mortgage loans Transactions, other loansRevaluations, mortgage loans Revaluations, other loans

Transactions/revaluationsmill. euro

Source: Statistics Denmark

The figure shows a considerable increase of transactions in mortgage loans from 1995 to 1998 after which point the level of transactions fall, though still being on a high level. However, the transactions in other loans have been quite stable, except for a leap in year 2000. In other words, the development of Danish households' loan activity seems to indicate that the answer

19

to the rise of household debt is to be found in changes in households' mortgage loan activity. The considerable increase in households' mortgage loans is not just a Danish phenomenon. ECB figures on MFI loans of the euro countries show that the increase of the monetary financial institutions lending to households from the fourth quarter of 1998 to the fourth quarter of 2000 by 83 per cent was caused by lending for house purchases. The MFI loans to households broken down into lending for house purchases, consumer credit and other lending of the fourth quarter of 1998 to 2000 are shown in figure 4.4.

Figure 4.4 MFI loans to households (excl. NPISH) of the euro countries

0500.000

1.000.0001.500.0002.000.0002.500.0003.000.0003.500.000

1998 1999 2000Lending for house purchase Consumer credit Other lending

Mill. euro

Source: European Central Bank, "Monthly Bulletin"

The substantial increase of Danish households' mortgage debt is without doubt connected with an extensive increase of the price of the owner-occupied dwellings in the second half of the 1990s – an increase, which has a counter part in the majority of the rest of the EU+ countries 27. Price indexes of three categories of owner-occupied dwellings: One-family houses, secondary homes and owner-occupied apartments confirm that Danish households' mortgage debt has been bound to rise as a financial counterpart to the development in the property market.

Figure 4.5 Price index of three categories of sales of real estate in Denmark

75100125150175200

1994K4 1995K4 1996K4 1997K4 1998K4 1999K4 2000K4One-family housesOwner-occupied appartmentsSecondary homes

Price index

Source: Statistics Denmark

This rise in debt outstanding has not necessarily been associated with an increase in the households' debt service payment, since the increase in mortgage debt may have been followed by changes of loan terms – for instance longer loan maturities. Though longer loan maturities enhance the interest expense over time, a lower periodic payment makes it possible for the households to hold higher outstanding amounts. Changes of loan terms regarding interest payments may also have lowered the households' costs of carrying mortgage debt. Low short- term interest rates relative to long-term interest rates have made interest-adjusted (variable interest) loans an attractive way to finance purchases of real estate. Interest-adjusted loans enable borrowers to carry larger outstanding amounts of mortgage debt and may even cause a greater proportion of households to become owners rather than tenants of their homes than would be the case under "standard terms". At the end of year 2000, approximately 9 per cent of the loans granted by Danish mortgage banks were variable interest loans, in 2001 this percentage has risen to over 20 per cent28 – the increase of mortgage debt from 2000 to 2001 was caused entirely by a rise in interest-adjusted mortgage loans. 27 OECD Economic Outlook 68, 2000: "House Prices and Economic Activity".

20

In other word, although the prices of owner-occupied dwellings may have compelled Danish households to increase their debt, their ability to service their loans may not automatically be jeopardized hereby because of changes of loan terms. Figure 4.6 lends support to the hypothesis that increases in mortgage debt of Danish households have been accompanied by changes in loan terms, a factor which has driven the debt service payment in the opposite direction. The figure shows the development of debt service payments of the Danish mortgage borrowers to the mortgage banks that finance the bulk of mortgage loans in Denmark, compared with the development of mortgage loans and disposable income. Clearly, the rise of households' debt service payments on mortgage loans is lower than the increase in mortgage loans.

Figure 4.6 Danish mortgage lending, debt service payments to mortgage banks and household disposable income

90100110120130140150

1995 1996 1997 1998 1999 2000Mortgage lending by mortgage banksDebt service payments to mortgage banksHousehold disposable income

Index

Source: Statistics Denmark and the Association of Danish Mortgage BanksNo

te

Mortgage lending by mortgage banks and debt service payments to mortgage banks cover lending/payments to/from all sectors.

What is also clear from the figure is that as far as mortgage loans are concerned an increase of the debt service payment has taken place – the increases of the prices of the owner-occupied dwellings are far from being compensated by changes in loan terms and general income growth. Though the development of the debt service payment does follow the evolution of household disposable income, the debt service payment rises at a higher rate than disposable income. Analysis by a major mortgage bank29 supports this picture by showing that the families of owner-occupied flats in Denmark, when entering the market today, spend more than 50 per cent of their income to service mortgage debt, in 1998 the percentage was about 40.

To make matters worse, an increase of the debt service payment is not the only result of the changes to households' loan activity. As a consequence of the popularity of interest-adjusted mortgage loans, households' indebtedness may also have become riskier. Besides being riskier as to the changes of interest rates, an increase of interest rate also hits the borrowers of the interest-adjusted mortgage loans indirectly due to the absence of a positive effect on the redemption rate. With a standard (fixed-interest 30 year) mortgage loan, an increase of the rate of interest would lead to a fall in the redemption rate of the remaining debt, so that the equity of the real estate will be largely retained – this mechanism does not work if an interest-adjusted mortgage loan is used to finance a house purchase. In other words, borrowers financing their real estate purchase through interest-adjusted loans are hit twice by an increase of the interest rate. Thereby borrowers have become more vulnerable to changes of interest rates, and changes sufficiently contrary to the assumptions about the future interest rates made by households when planning their borrowing seem more likely to be followed by financial distress.

The increase of households' debt service payment may indicate a general change in households' attitude towards debt – that households generally have become more willing to finance their purchases of assets or even consumption by running up debt. The increase in debt in proportion to income may also indicate that attention has to be paid to the return on 28 The Danish Financial Supervisory Authority, May 2002, "Markedsudviklingen i 2001 for realkreditinstitutter".29 Nykredit, 13th of May 2002, "Nykredit boligindeks".

21

assets. Households may have become more inclined to transform increases of financial as well as real estate wealth into spending, so that in planning their borrowing households attach less weight to the income and more to capital gains on assets. Thereby, an increased willingness of households to spend out of the rising value of their assets (houses, stocks) through mortgage loans (i.e. equity withdrawal) may have contributed to the rise in household debt. This indicates that to be able to say whether the level of household debt is critical or not, one has also to consider the wealth of households. In other words, analysing the development of the household indebtedness solely by looking at the households' liability side seems to be to narrow a concept.

4.2 The financial assets of the household sector

Looking at Financial Accounts data of households it is clear that the value of the financial assets more than matches the value of the financial liabilities – this is the case for each of the EU+ countries. However, the proportion of financial assets to financial liabilities differs considerably from country to country. The highest value of assets to liabilities is to be found in Italy with an end-of-year 2000 stock of assets 7.6 times the stock of liabilities. At the other end of the scale is Norway and Denmark with a value of assets approximately 1.5 times the value of liabilities. Moreover, the development of the proportion of assets to liabilities differs substantially across the EU+. While Finish households experienced an increase of the value of assets to liabilities of 47 per cent from 1995 to 2000, the Portuguese households' proportion fell by approximately 39 per cent30. The development of households' financial assets to financial liabilities is shown in figure 4.7.

Figure 4.7 Household financial assets to financial liabilities

0

3

6

9

1995 1996 1997 1998 1999 2000Austria Belgium Germany Denmark

Ratio

0

3

6

9

1995 1996 1997 1998 1999 2000Spain Finland Italy

Ratio

0

3

6

9

1995 1996 1997 1998 1999 2000France Netherlands Norway Sweden

Ratio

0

3

6

9

1995 1996 1997 1998 1999 2000Portugal United Kingdom EU+

Ratio

Source: New Chronos

For a majority of the EU+ countries the proportion of assets to liabilities is practically unchanged from 1995 to 2000 indicating that the increase of debt has only just been matched by an increase of financial assets.

For the EU+ as a whole the proportion of assets to liabilities has increased from an asset value 3.4 times the liabilities in 1995 to a 3.7 proportion in 2000. This involves an end-of-year 2000 value of financial assets 60 per cent larger the value of 1995.

30 The 39 per cent decrease covers a decrease of the ratio from 1995 to 1999, since no 2000-data are yet available on the households of Portugal.

22

In contrast with the liability side, households' use of financial instruments is more diversified when it comes to their financial assets. The sector's instruments of financial investment consist of currency and deposits, securities other than shares, shares and other equity and insurance technical reserves. The latter is made up for instance of equity in the form of life insurance and pension funds reserves. Since pension funds and insurance corporations carry out investments of the funds placed in these corporations, households' financial transactions of insurance technical reserves can be considered as an indirect investment in the other three investment instruments in question. As shown in figure 4.8, the households' indirect investments in the form of insurance technical reserves carry a good deal of the financial transactions of households in the EU+ as a whole. The financial transactions in insurance technical reserves have been constantly rising from 1995 to 2000.

Figure 4.8 Financial transactions in assets of the EU+ households

-200.000-100.000

0100.000200.000300.000400.000

1995 1996 1997 1998 1999 2000Currency and deposits Securities other than sharesShares and other equity Insurance technical reservesOthers

Financial transactionsmill. euro

Source: New Chronos

In general, the financial transactions of households have changed somewhat over the period under consideration. What is clear is, however, that currency and deposits have been used to a steadily decreasing extent as a financial instrument of households. What is also clear is that the households' financial transactions of securities other than shares and shares and other equities develop in opposite directions, involving negative transactions of securities other than shares (i.e. the households sell securities other than shares at a higher value than they buy) in years of substantial positive financial transactions in shares and other equity. In 2000 households seem to regain interest in securities other than shares. Caused by the weakening of the global share market, which began in year 2000, the positive transactions of securities other than shares may indicate a gradual change of preference of the households in favour of securities other than shares.

The radical increase of the financial transactions of shares and other equity from 1995 to 1998 indicates an increase of the weight of shares in the households' financial wealth. As illustrated in figure 4.9, the proportion of shares to the total of household financial assets went up from 1995 to 1998 from 23 per cent to 30 per cent. In spite of a decrease in the financial transactions of shares and other equity in 1999 and 2000, while the transactions of the other instruments grew (except for a slight fall of currency and deposits from 1999 to 2000), the proportion of shares actually took a further leap to 34 per cent.

Figure 4.9 Composition of EU+ households' financial assets

35 31 27 25 22 22

11 9 8 6 7

23 24 27 30 34 34

28 29 30 30 31 31

4 6 6 6 7 7

11

020406080

100

1995 1996 1997 1998 1999 2000Currency and deposits Securities other than sharesShares and other equity Insurance technical reservesOthers

Pct.

23

Source: New Chronos

The further increase of household wealth in the form of shares and other equity in proportion to the total of household financial wealth was caused by the exceptional increases of share prices in 1999. Though not as distinct, also the value of households financial assets of insurance technical reserves is, due to the indirect investments in shares and other equities, dependent on the stock price changes. The development of household financial assets in the form of shares and other equities and insurance technical reserves is shown in figure 4.10.

Figure 4.10 Development of EU+ households' shares and other equity and insurance technical reserves

0

2.000.000

4.000.000

6.000.000

8.000.000

1995 1996 1997 1998 1999 2000-500.000

0

500.000

1.000.000

1.500.000

Transactions/revaluationsmill. euroShares and other equity

End-of-year stockmill. euro

0

2.000.000

4.000.000

6.000.000

8.000.000

1995 1996 1997 1998 1999 2000-500.000

0

500.000

1.000.000

1.500.000

Transactions Revaluations End-of-year stock

End-of-year stockmill. euro

Transactions/revaluationsmill. euroInsurance technical reserves

Source: New Chronos

The figure demonstrates the importance of revaluations to the development of household wealth. In particular, the share price increases in 1999 are decisive. In fact, approximately 32 per cent of the change in households' total financial assets from 1995 to 2000 was caused by revaluations in 1999.

As the transactions of shares and other equity increases in proportion to the total transactions of household assets, the development of revaluations to household wealth obviously becomes the more relevant. The accumulation of the considerable directly and indirectly investments of shares and other equity over the period under consideration (at least until 1998 as far as direct investments are concerned) has made the wealth of households the more likely to become jeopardized by drastical changes of share prices. Thereby, as the composition of households' financial wealth has changed away from the relatively secure bank deposits and securities other than shares to shares and other equities and insurance technical reserves, the financial wealth of the households has become riskier.

Furthermore, the liquidity of the financial assets of the households has changed. Financial assets in the form of currency and deposits are clearly the most readily disposable assets of the financial instruments in question. Since the households' assets shift away from currency and deposits, the liquidity of the household wealth is diminishing. At the same time, increases in the proportion of insurance technical reserves to total wealth may add to a decreasing liquidity of the financial assets of households. This is because an increasing proportion is held as insurance technical reserves and other pension reserves, which cannot easily be liquidated. As far as the rising proportion of shares and other equities is concerned, an analogous reasoning applies if the increased proportion is caused by transactions in shares and other equities in the form of unquoted shares and other equities.

In other words, though the increase of household debt of the EU+ as a whole is matched by an increase of financial assets, one has also to bear the changes of the composition of household wealth and the involved changes of risk and liquidity in mind.

Having said that, the composition of the financial assets of the households' of the EU+ countries differs considerably. Though the tendencies are similar (albeit, of varying magnitude), the wealth of the households is composed in very different ways. For instance, despite a substantial fall of the stock of currency and deposits, the end-of-year 2000 financial wealth of the Austrian households' is made up of 55 per cent currency and deposits. At the

24

other end of the scale is Sweden with a proportion of currency and deposits to the total sum of financial assets of 15 per cent. The proportion of securities other than shares is low and for some countries almost non-existing. The highest proportion of securities other than shares is to be found in Belgium with a value of securities other than shares of 20 per cent of the total sum of financial assets. As for shares and other equity, the households of Finland are noticeable. The financial assets of the Finish households are to 65 per cent made up of shares and other equity, which makes the wealth of the Finish households' rather sensitive to share price changes. At the same time, in proportion to the sum of financial assets, the Finish households are characterized by the lowest wealth in the form insurance technical reserves. In general, there seems to be a substitution between the investment in shares and other equities and insurance technical reserves. Countries with high proportions of insurance technical reserves, such as the Netherlands, the United Kingdom and Denmark, have relatively low proportions of shares and other equity, and vice versa.

Figure 4.11 Composition of the households' financial assets

62 62 60 59 57 55

13 12 9 7 7

6 7 10 12 16 17

16 18 18 19 20 210 0 0 0 0 0

15

020406080

100

1995 1996 1997 1998 1999 2000

Pct. AUSTRIA

27 27 26 25 23 22

29 26 23 22 20

29 31 35 40 41 44

9 9 10 11 12 125 4 3 2 2 1

30

020406080

100

1995 1996 1997 1998 1999 2000

Pct. BELGIUM

42 41 39 38 35 34

13 12 11 10 10

18 19 21 23 27 27

26 26 27 27 27 281 1 1 1 1 1

14

020406080

100

1995 1996 1997 1998 1999 2000

Pct. GERMANY

29 28 27 28 27 25

15 14 12 10 10

15 16 19 17 18 19

38 39 39 41 43 44

2 2 2 2 2 2

16

020406080

100

1995 1996 1997 1998 1999 2000

Pct. DENMARK

52 46 40 35 33 36

2 2 1 2 2

29 36 44 49 51 46

10 11 11 11 11 136 5 3 3 3 3

3

020406080

100

1995 1996 1997 1998 1999 2000

Pct. SPAIN

36 31 29 26 24 23

3 2 2 1 1

53 57 60 61 66 65

7 8 9 9 9 101 1 1 1 1 1

3

020406080

100

1995 1996 1997 1998 1999 2000

Pct. FINLAND

31 33 31 29 25 25

4 3 3 2 2

34 36 38 41 47 46

21 22 23 23 21 239 5 6 5 5 4

5

020406080

100

1995 1996 1997 1998 1999 2000

Pct. FRANCE

40 38 34 29 25 25

31 2823 17 19

18 19 26 36 45 43

10 11 11 11 12 131 1 1 1 1 1

31

020406080

100

1995 1996 1997 1998 1999 2000

Pct. ITALY

25

21 21 19 18 17 183 3 3 2 2

19 20 22 21 23 23

52 53 52 54 54 56

4 3 3 4 4 1

3

020406080

100

1995 1996 1997 1998 1999 2000

Pct. NETHERLANDS

41 39 35 36 34 34

1 1 1 1 113 16 20 19 21 21

35 35 35 35 36 35

10 9 9 9 9 8

1

020406080

100

1995 1996 1997 1998 1999 2000Currency and deposits Securities other than sharesShares and other equity Insurance technical reservesOthers

Pct. NORWAY

Figure 4.11 (continued)

46 48 47 45 45

1 1 1 2

39 37 37 37 36

10 11 13 14 154 3 2 2 2

1

020406080

100

1995 1996 1997 1998 1999 2000

Pct. PORTUGAL

26 23 19 17 15 15

8 6 6 4 3

27 31 37 38 46 44

24 25 26 28 26 2914 14 12 11 9 9

8

020406080

100

1995 1996 1997 1998 1999 2000

Pct. SWEDEN

24 19 18 21 16 211 1 1 1 1

19 20 22 20 23 23

51 51 53 54 54 50

4 8 7 3 6 4

2

020406080

100

1995 1996 1997 1998 1999 2000Currency and deposits Securities other than sharesShares and other equity Insurance technical reservesOthers

Pct. UNITED KINGDOM

Source: New Chronos

The distribution of financial asset holdings across types of financial instruments may affect the households' view of wealth increases and influence their propensity to transform financial wealth into spending. Due to differences regarding risk, increases of wealth of various kinds may be viewed differently. Thereby, for instance, the wealth increases of shares and other equities may be viewed in a different way than wealth increases in securities other than shares, because the first may be considered as more uncertain than the latter. Moreover, the awareness of a wealth increase may differ with differently compositions of financial assets, thus causing differences in the influence that changes in asset values have on household spending. For instance, households may be more aware of increases in wealth in the form of shares and other equities and securities other than shares than in the case of insurance technical reserves. This is because the value of stocks and bonds can easily be followed (except for unquoted stocks) while the development of the indirect investments of e.g. pension funds can be hard to track31.

Bearing in mind the above consideration, one might expect to find a relation between the composition of households' financial assets and changes herein and the development of household debt. For instance, one might expect the positive development of the global stock market (except for year 2000) to incline the Finish households to borrow against the increase 31 See National Bureau of Economic Research, Nov. 2001, "Comparing Wealth Effects: The Stock Market Versus the

Housing Market" by Karl E. Case, John M. Quigley and Robert J. Schiller.

26

of wealth of shares and other equities. However, of the EU+ countries, Finland is the country experiencing the lowest increase of household debt. At the same time, the Finish households account for the highest increase of the ratio of financial assets to liabilities indicating that the rise of wealth in shares and other equities has not resulted in an increase in borrowing against financial wealth. The fact is, that looking at the Financial Accounts data of the EU+ countries, no obvious correlation between the development of the composition of household wealth and debt is found.

This is probably due to the fact that what really matters, quantitatively, as far as household wealth is concerned is housing wealth. Although households in the EU+ have experienced wealth increases in the form of shares and other equity, the value of shares and other equity of the households of the EU+ countries are generally rather small relative to the value of real estate. The majority of the EU+ countries have experienced substantial rises of house prices in the second half of the 1990s32 and today housing wealth account for 30-40 per cent of total household wealth in Western Europe33. Increases of the prices of real estate affect far more people than do increases in share prices, the wealth of which are far more concentrated in the hands of the better-offs of the households. As for risk, house prices tend to be less volatile and gains in house wealth may therefore be viewed as a more permanent gain than increases in share prices. Furthermore, the awareness of wealth increases of rises of house prices may be greater. Unlike for instance insurance technical reserves, the wealth of households in the form of real estate is physically existent to the owners. At the same time, marketing of mortgage refinancing and borrowing against housing equity makes households' awareness of wealth increases caused by house price increases even greater. However, housing wealth is rather illiquid. Housing wealth may not easily by liquidated in the event of sudden downward changes of prices, especially not since the houses serves as homes of most the households in addition to being objects of investment. Furthermore, downward changes of prices may have serious implications on households, when decreases of house prices causes the value of the real estate to get exceeded by the run up of debt in the house. In such cases, the households become technical insolvent and practically adscripted to their homes.

In other words, evaluating the debt and wealth of households on the basis of Financial Accounts data alone does not provide an exhaustive picture of the households' financial position. In particular, the lack of information on non-financial wealth in the form of real estate is critical. Despite of the obvious importance of housing wealth to household behaviour regarding financial as well as non-financial activities, no comparable data are available across Europe. To get an idea of the magnitude of housing wealth in comparison with financial assets of households, the value of real estate of the Danish households has been estimated based on the public tax assessment for income and property tax purposes. The public tax assessment of real property, however, typically underestimates the value of real estate. In year 2000 the value of real estate based on the tax assessment of real property of the Danish households (excluding NPISH) was 4.3 times the value of shares and other equity.

4.3 The net wealth of the household sector and the micro-macro link

The implications of the development of household debt can evidently not be judged solely by looking at the liability side of households' balance sheets. Looking at Financial Accounts data of households it is clear that the value of financial assets more than matches that of financial liabilities – on top of that, we have the wealth in the shape of non-financial assets, especially real estate. Going through the financial assets and liabilities of the households of the EU+ it is, however, also clear that a net measure of the wealth of households is far from being adequate if the changes to households' financial position are to be analysed. A net wealth measure does not give a thorough insight into the development of household financial position, since it does not contain information on changes as to risk and liquidity – changes that clearly seem to have taken place on the asset side as well as on the liability side of households' balance sheets.

As mentioned earlier, one of the weaknesses of the Financial Accounts when used for economic policy analysis is the macro perspective of the data. Obviously, a great variability occurs among households in respect of financial assets and liabilities. Looking at the development of 32 OECD Economic Outlook 68, 2000, "House Prices and Economic Activity".33 The Economist, March 2002, "Special report, House prices"

27