2 nd session: Principal – Agent Problem Performance Evaluation IMSc in Business Administration...

35

2 nd session: Principal – Agent Problem Performance Evaluation IMSc in Business Administration October-November 2008

-

Upload

melvin-jordan -

Category

Documents

-

view

216 -

download

0

Transcript of 2 nd session: Principal – Agent Problem Performance Evaluation IMSc in Business Administration...

2nd session:Principal – Agent Problem

Performance EvaluationIMSc in Business Administration

October-November 2008

Principal Agent Model

• This lecture is mostly based on:

Richard A. Lambert , Contracting Theory and Accounting, Journal of Accounting & Economics,

Vol. 32, No. 1-3, December 2001

Agency theory and Accounting

1. How do features of information, accounting and compensation systems affect incentive problems?

2. How does the existence of incentive problems affect the design and structure of information, accounting, and compensation systems?

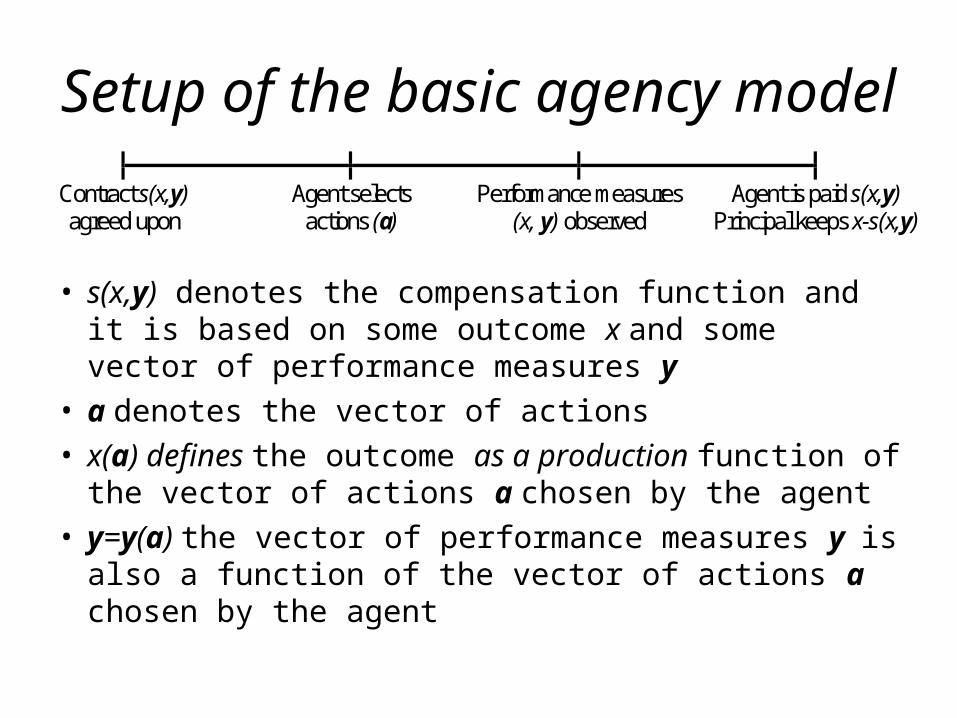

Setup of the basic agency model

• s(x,y) denotes the compensation function and it is based on some outcome x and some vector of performance measures y

• a denotes the vector of actions• x(a) defines the outcome as a production function of the

vector of actions a chosen by the agent• y=y(a) the vector of performance measures y is also a

function of the vector of actions a chosen by the agent

Contract s(x,y) agreed upon

Agent selects actions (a)

Performance measures (x, y) observed

Agent is paid s(x,y) Principal keeps x-s(x,y)

Extensions of the basic model

• The outcome x may be unobservable, which makes information signals on x critical

• Or it may be the case that the information signals are themselves produced by the agent:–moral hazard problems on the agent

reporting truthfully

Extensions of the basic model

• The information signal might also be generated by a third party (an auditor, for instance), – the incentives of such an independent

third party to be modelled too• Finally the performance measures

may be the stock price – trust the market to aggregate all the

relevant information–What information is available on the

market?

Extensions of the basic model

• Allowing agent and/or the principal to obtain information prior to the agent selecting his actions– Information on the productivity

of different actions, on the general setting, information on the agent’s type

Extensions of the basic model

• Include multiple periods– Repetition of the same action or

interdependent actions

• Include multiple agents– Team work or competitive work– Relative Performance Evaluation!

Single-period, single-action

•Principal’s problem is a constrained maximization problem in which he chooses the compensation function to

maximize the principal’s expected utility

subject to agent’s acceptable utility constraint

agent’s incentive compatibility constraints.

Principal’s utility

• Utility derived from the net proceeds generated

• Let G[x-s] denote the utility function• G’>0, meaning the principal prefers

more to less• G’’≤0, meaning that the principal is

risk averse or risk neutral.• If the principal is risk neutral, then:–G[x-s]=x-s

Principal’s utility

• The impact of the compensation on the utility of the principal is twofold:1. Each dollar paid to the agent is

one dollar less to the principal2. But the compensation mechanism

affects the action selection of the agent and consequently the outcome

Production technology

• Outcome and performance measures are affected randomly by the actions, among other exogenous variables.

• f(x,y|a) is the pdf of outcome x and the performance measures y given the selection of actions a.

Compensation function Individual Rationality

Constraint• The principal must ensure that this

function is attractive enough to offer an acceptable level of expected utility. The agent must want to take part!

• Minimal level to be guaranteed must beat the next best employment opportunity.

Compensation function Incentive Compatibility

Constraints• These represent the link between

the contract and the actions choice.• These constraints will condition the

compensation function such that the agent will choose the actions in accordance to the principal’s objectives.

Agent’s utility

• The agent’s utility is defined over two sets of variables:– The increasing utility he derives from the

monetary compensation he receives, denoted by s.– The disutility he suffers from the added effort of

undertaking actions a.

• Most models assume the agent’s utility is additively separable:– H(s,a) = U(s) – V(a).– Some models ignore the disutility of effort,

V(a)=0.

First-best solution

• Benchmark case, where the actions are chosen cooperatively with all parties’ interests in mind and everyone tells the truth…

• The principal chooses the action set that maximizes his utility.

• The agent simply guarantees that he will participate.

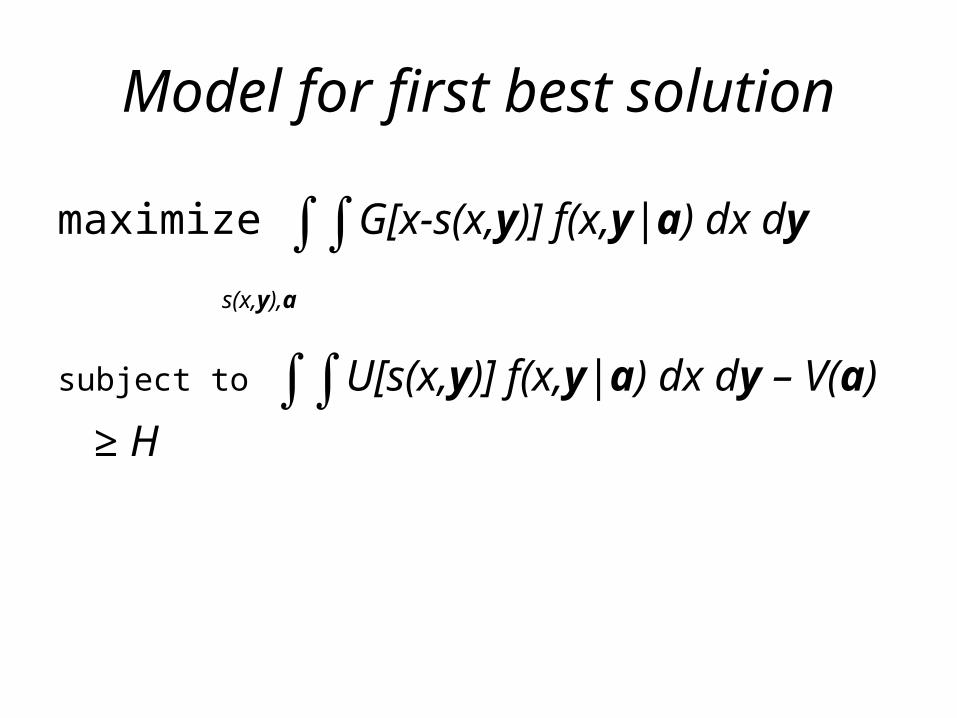

Model for first best solution

maximize ∫∫G[x-s(x,y)] f(x,y|a) dx dy

subject to ∫∫U[s(x,y)] f(x,y|a) dx dy –

V(a) ≥ H

s(x,y),a

Optimal contract

• Differentiate the objective function with respect to s for each possible (x,y) realization to deliver the following first-order condition:

• OPTIMAL RISK SHARING CONDITION

G’[x-s(x,y)] U’[s(x,y)]

=λ

Optimal contract

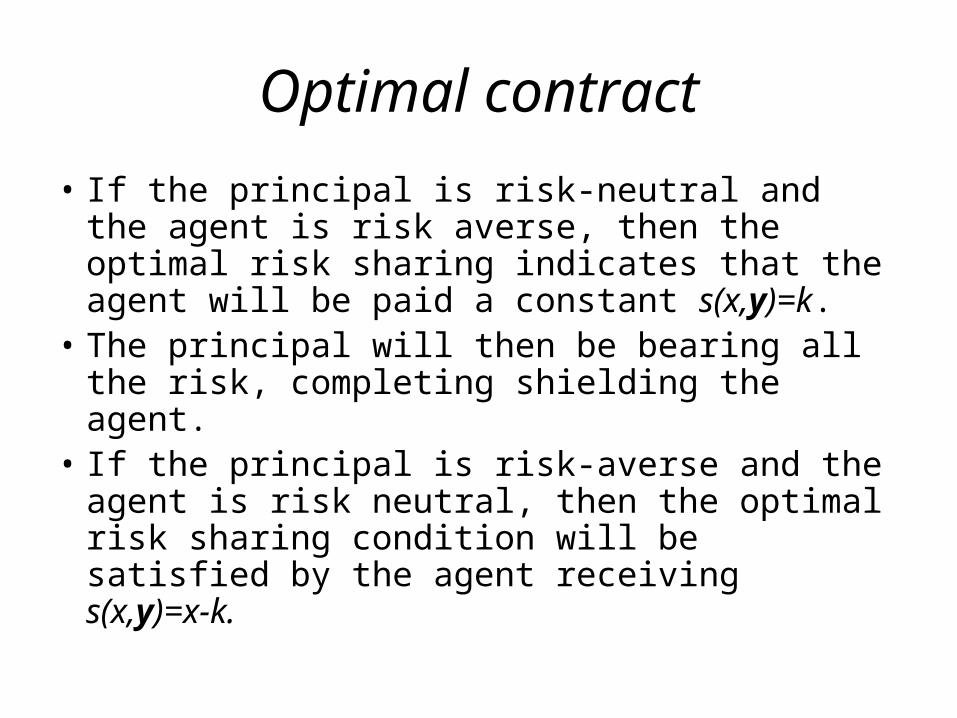

• If the principal is risk-neutral and the agent is risk averse, then the optimal risk sharing indicates that the agent will be paid a constant s(x,y)=k.

• The principal will then be bearing all the risk, completing shielding the agent.

• If the principal is risk-averse and the agent is risk neutral, then the optimal risk sharing condition will be satisfied by the agent receiving s(x,y)=x-k.

Possible First-Best Solutions

• Two conditions must hold:– Principal designs a contract that induces first best actions– Agent is imposed only the amount of risk under the pure risk sharing

condition

• Agent is risk neutral– Agent will bear all the risk and principal

receives a constant amount– This means that the agent actually

“bought the firm” from the principal and now chooses the action to maximize his own objective function

Possible First-Best Solutions

• Agent’s actions are observable– Principal can offer a “compound”

contract :• Agent paid according to the first best

contract if principal observes the first best actions• Agent is penalized substantially, if principal

observes otherwise

– This type of contract is called FORCING CONTRACT.

Possible First-Best Solutions

• No uncertainty in the outcome– If the principal can infer from the

outcome if the first best action was undertaken.

• If the outcome distribution exhibits MOVING SUPPORT:– If the set of possible outcomes changes

with the actions selected.

Second best solution

• Now the principal has no way to observe (directly or indirectly) the agent’s choice of action.

• We focus on the simplest case:– One single dimensional action or effort: a– Effort is a continuous variable– Outcome is also a continuous random

variable–No other performance signal is available.

Production function

• f(x|a) is the probability density function of outcome x given effort a.

• More effort turns higher output more likely.

• No moving support:– If f(x|a)>0 for some a, then f(x|a)>0 for all

feasible effort levels.

• Increasing cost for higher efforts at increasing rate:– V’(a)>0 and V”(a)>0.

Model

maximize ∫G[x-s(x)] f(x|a) dx

subject to (Individual Rationality Constraint)

∫U[s(x)] f(x|a) dx – V(a) ≥ H

and to (Incentive Compatibility Constraint)

a=argmax( ∫U[s(x)] f(x|a) dx – V(a) )

s(x),a

Incentive Compatibility Constraint

• In order to make the ICC more tractable, this constraint is often replaced by the FOC of the agent’s problem:

– ∫U[s(x)] fa(x|a) dx – V’(a)=0

Optimal contract

• Differentiate the objective function with respect to s for each value of x to deliver the following first-order condition:

G’[x-s(x)] fa(x|a) U’[s(x)]

= λ + μ f(x|a)

What if μ=0?

• We reach the first best solution.• Holmstrom [1979] shows that μ>0,

as long as the principal wants to motivate more than the lowest possible level of effort.

FOC revisited

• This new condition implies that we analyze the term:

• We can look at this term from the classical statistical inference. Think of the maximum likelihood function, where x is the sample outcome and the probability distribution f(x|a) and a is the parameter to be estimated.

• The principal rewards those outcomes that indicate the agent worked hard.

fa(x|a) f(x|a)

If additional Performance Measures are available?

• The FOC turns into:

• Holmstrom’s informativeness condition: optimal contract is based on performance measures, iff the term fa(x,y|a)/f(x,y|a) also depends on y

G’[x-s(x,y)] fa(x,y|a) U’[s(x,y)]

= λ + μ f(x,y|a)

If additional Performance Measures are available?

• Holmstrom’s informativeness condition: implies that contracts will be based on many variables.

• “While it is not surprising that a variable is not valuable if the other variables are sufficient for, it is more surprising that a variable is valuable as long as the other available variables are not sufficient for it.

• “In particular, it seems plausible that a variable could be slightly informative, but be so noisy that its use would add too much risk into the contract.” The question, however, is how this variable will be ultimately used in the contract.

If additional Performance Measures are available?

• “When the signals are independently distributed, any signal which is sensitive to the agent’s action is useful in the contract”, even variables not controlled by the agent.

• What about when the performance measures are correlated?

What about when the performance measures are

correlated?• It may be the case that the correlation is

such that the additional variable does not add anything to the contract.

• But there can also be performances measures completely unrelated to the agent’s effort that become relevant.– Think of two employees affected by the same

random shock. You are the principal of one of them, and yet the performance of the other may be informative about what your agent is doing.

– Relative Performance Evaluation

Relative Performance Evaluation

• Used in several contexts:– Grading on the curve,– Employee of the month,– Sports tournaments

• Not so often in executive compensation:– First problem: controlability– Second problem: why compensate in a situation

of disaster, just because your disaster was smaller than others...

– Third problem: destructive competition...– Fourth problem: choose easy competitive path...– Fifth problem: may provide a safety to the agent

you don’t want him to have.

Other problems to be considered

• Window dressing and how incentives may be harmful– Agent can take actions to improve

performance measure, but not the outcome• Myopic performance measures– Performance measures not sensitive to long

term effects• Divisional versus firm-wide performance– Depending on the interconnection of the

divisions, should we use more or less firm-wide performance.

• Aggregation of information for valuation or for compensation is different

![R. Rajesh (Institute of Mathematical Sciences [IMSc])home.iitk.ac.in/~mkv/Conf/Talks_files/rajesh_iitk.pdf · R. Rajesh (Institute of Mathematical Sciences [IMSc]) C. Connaughton](https://static.fdocuments.us/doc/165x107/5fad89f2162ee96d7d652b5d/r-rajesh-institute-of-mathematical-sciences-imschomeiitkacinmkvconftalksfilesrajeshiitkpdf.jpg)