2 45 wayne de veydt

14

Navigating the Health Insurance Landscape: What to Expect and What Surprises are in Store Annual Insurance Executive Conference Wayne DeVeydt Executive Vice President, Chief Financial Officer December 17, 2013

-

Upload

summit-professional-networks -

Category

Business

-

view

342 -

download

12

description

Transcript of 2 45 wayne de veydt

Navigating the Health Insurance Landscape:What to Expect and What Surprises are in Store

Annual Insurance Executive Conference

Wayne DeVeydtExecutive Vice President, Chief Financial Officer

December 17, 2013

A Health Benefits Leader

2

`̀

BC or BCBS licensed plans

Medicaid presenceBC or BCBS licensed plans + Medicaid presence

BC or BCBS plans in 14 states andMedicaid presence in 19 states

Medicare4%

BlueCard14%

Medicaid13%

Individual 5%

National Accounts19%

LocalGroup41%

FEP4%

Diverse customer base of36 million medical members

Projected Sources of Insurance Coverage2012-2021

3

2012

2021

Employer

-10%Uninsured

-38%Exchanges Medicaid

+20%Medicare

+30%

14052 54 50

12632 30 65 65

Source: Analysis of Avalere / Booze & Co. / McKinsey / WellPoint Enrollment Models; Assumes 15 states opt out of Medicaid expansion: AK, AL, GA, IA, ID, IN, LA, MS, NE, NC, OK, SC, TX, VA, WI

State HIX Federal HIX State Agency

2.3MDetermined Eligible

for Medicaid

ACA Medicaid Expansion Eligibility Determinations

4

65%

12%

23%

Federal and State Exchange Enrollment

365,000

227KState Total

138KFederal Total

October November

Source: HHS Enrollment Update; December 11, 2013

70%

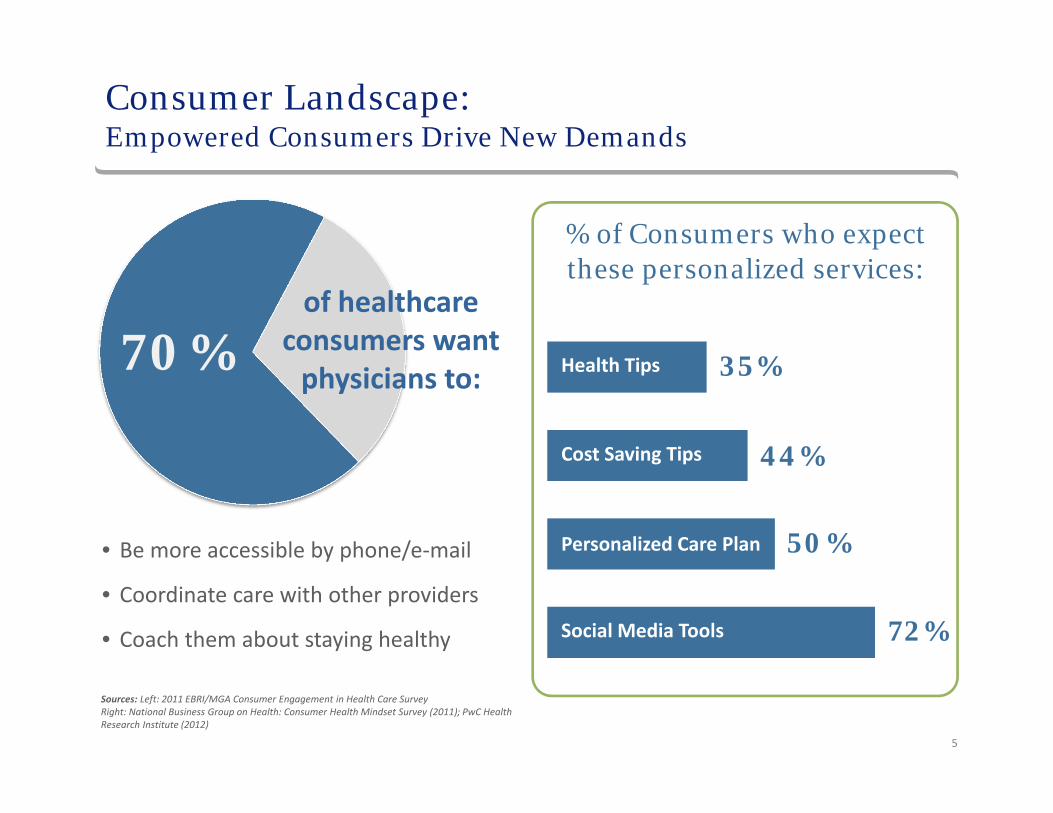

Consumer Landscape: Empowered Consumers Drive New Demands

of healthcare consumers want physicians to:

• Be more accessible by phone/e‐mail

• Coordinate care with other providers

• Coach them about staying healthy

50%

44%

35%

72%Social Media Tools

Personalized Care Plan

Cost Saving Tips

Health Tips

% of Consumers who expect these personalized services:

Sources: Left: 2011 EBRI/MGA Consumer Engagement in Health Care Survey Right: National Business Group on Health: Consumer Health Mindset Survey (2011); PwC Health Research Institute (2012)

5

675

725

775

825

875

925

2008 2010 2015 2020 2025

DemandSupply

Source: American Academy of Medical Colleges

Americans without access to primary care

60million

Average wait for non-emergency appointment

20.3days

PCPs accepting new patients 49.8%

National Association of Community Health Centers. March 2009. Primary Care Access: An Essential Building Block of Health Reform; Merritt Hawkins and Associates: 2009 Survey of Physician Appointment Wait Times; Center for Studying Health System Change: 2008 Health Tracking Physician Survey 6

Consumer Landscape: Supply & Demand of Physicians

Physicians (in 000s)

Consumer Landscape:Preference for Less Expensive Plans & Narrower Networks

7

Numbers are rounded; Source: McKinsey Consumer Exchange Simulation 2011‐2013

Source: Hospital and Health Networks; Physician Compensation and Production Survey, Medical Group Management Survey, 2002‐012; Merritt Hawkins 2012 Review of Physician Recruiting Incentives; Dealogic

Provider Landscape:National Trend Towards Provider Consolidation

8

78% of hospitals are consolidating or exploring consolidation

0%

10%

20%

30%

40%

50%

60%

70%

80%

2002 03 04 05 06 07 08 09 10 2011

Physician owned Hospital Owned

Hospital employment of physicians is increasing nationwide

Source: Avalere Health. (2010. analysis of American Hospital Association Annual Survey)

2,373 2,321 2,251 2,172 2,142 2,044

2,542 2,606 2,668 2,755 2,868 2,941

2000 2002 2004 2006 2008 2010

Independent Hospitals In Health Systems

9

31%

10%

1%3%

23%

11%

19%

2% Primary Care

Internal Medicine

Pediatrics

General Surgery

Surgical Specialties

Emergency Medicine

Other Specialties

Unknown

2010 Physician Assistants by Specialty

Source: 2010 AAPA Physician Assistant Census Report

Decrease in healthcare workforce productivity 1992-2012

94%Increase in Nurse Practitioner

Jobs Projected by 2025

Average Annual Growth over 20 Years

0.6%

Provider Landscape:Blurring Lines Between Providers & Payers

Source: Hospital and Health Networks; Physician Compensation and Production Survey, Medical Group Management Survey, 2002‐12;

23%16%

40%

63%71%

53%

14%14%7%

Managing carecoordination

Performancemeasurement

Population healthmanagement

Not at all Prepared Somewhat Prepared Very Prepared

Numbers are rounded. Source: Executive Survey on Hospital and Physician Affiliation Strategies, Sponsored by McKesson. 10

Accountable Care Preparedness

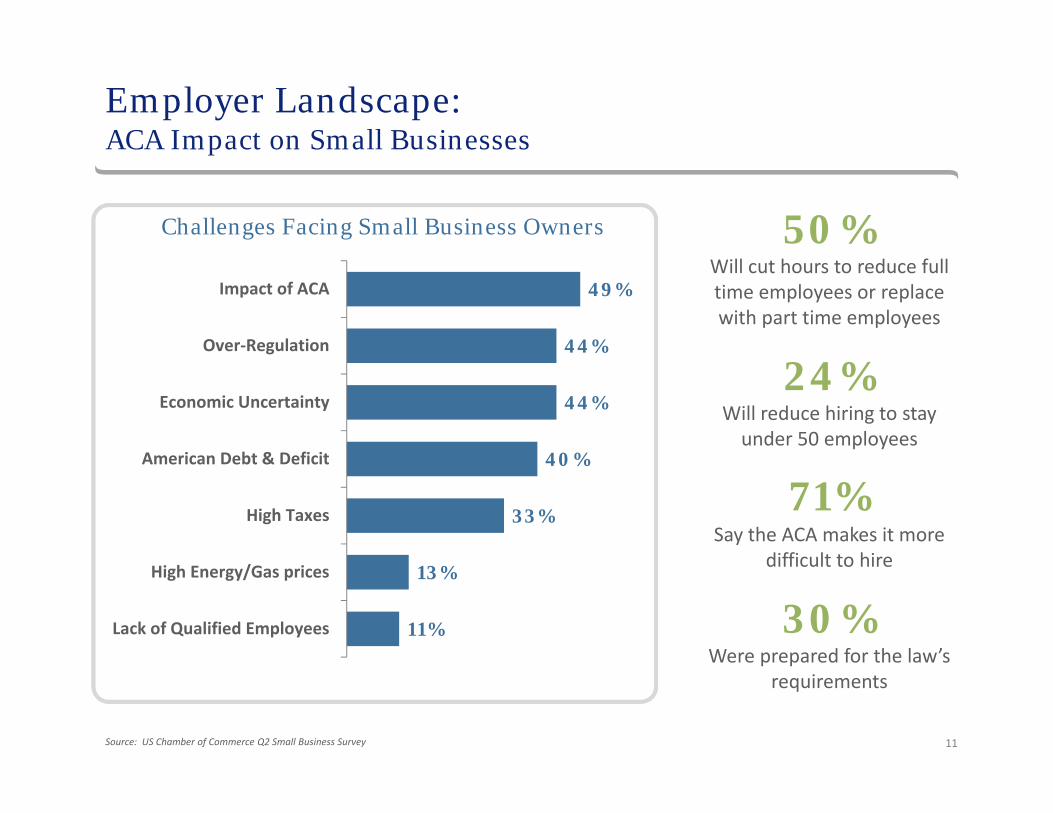

Employer Landscape:ACA Impact on Small Businesses

11

50%Will cut hours to reduce full time employees or replace with part time employees

24%Will reduce hiring to stay under 50 employees

71%Say the ACA makes it more

difficult to hire

30%Were prepared for the law’s

requirements

Source: US Chamber of Commerce Q2 Small Business Survey

49%

44%

44%

40%

33%

13%

11%

Impact of ACA

Over‐Regulation

Economic Uncertainty

American Debt & Deficit

High Taxes

High Energy/Gas prices

Lack of Qualified Employees

Challenges Facing Small Business Owners

12

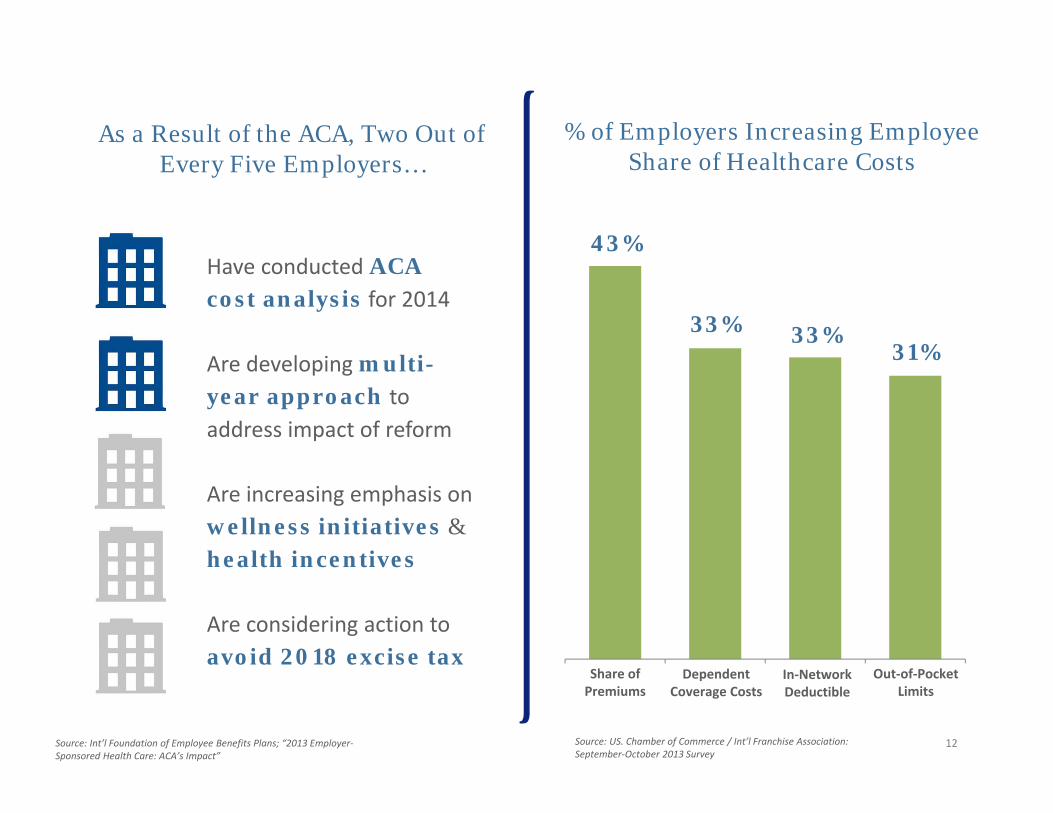

Share of Premiums

Dependent Coverage Costs

In‐Network Deductible

Out‐of‐Pocket Limits

% of Employers Increasing Employee Share of Healthcare Costs

33%31%

33%

43%Have conducted ACAcost analysis for 2014

Are developing multi-year approach to address impact of reform

Are increasing emphasis on wellness initiatives &health incentives

Are considering action to avoid 2018 excise tax

As a Result of the ACA, Two Out of Every Five Employers…

Source: Int’l Foundation of Employee Benefits Plans; “2013 Employer‐Sponsored Health Care: ACA’s Impact”

Source: US. Chamber of Commerce / Int’l Franchise Association: September‐October 2013 Survey

Employer Landscape:Interest in Private Exchanges

13Source: Private Exchange: Accenture analysis, based on data from: U.S. Census, Bureau of Labor and Statistics, Kaiser Employer Health Benefits 2012 Annual Survey. Calculations exclude post‐65 retirees and individuals.Public Exchange: Congressional Budget Office 2013 Estimate of the Effects of the Affordable Care Act on Health Insurance Coverage, CBO’s February 2013 Baseline, depicts average monthly enrollment, including spouses and dependents for individual and SHOP.

20% 26% 26% 23%

62% 57% 55%49%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

10 to 50 51 to 100 101 to 3000 >3,000

Would consider switching as long as they saw savings of at least 10%

Would consider switching for no savings

Percent of employers who would consider switching to a private exchange

9

15

2730 31

1

9

19

30

40

0

5

10

15

20

25

30

35

40

45

2014 2015 2016 2017 2018

Public Exchange Private Exchange

Enrollm

ent (millions)

Projected Public vs. Private ExchangeAnnual Enrollment

# of employees