2 1.Highlights of 2006 2.Consolidated Operations 3.Operations by Business Area 4.Assets Quality and...

40

-

Upload

agatha-hall -

Category

Documents

-

view

218 -

download

0

Transcript of 2 1.Highlights of 2006 2.Consolidated Operations 3.Operations by Business Area 4.Assets Quality and...

2

1. Highlights of 2006

2. Consolidated Operations

3. Operations by Business Area

4. Assets Quality and Solvency

5. Other Indicators

General Index

3

Highlights of Activity in 2006

• Consolidated net income up 36.5% to EUR 733.7 million

• Highest level of income before tax and minority shareholders’ interests in financial sector, in 2006, at EUR 989.8 million

• Income tax of EUR 222.6 million, comprising an effective tax rate of 23.3%

• Net operating income up 21.9% to EUR 2,977.3 million

• Net-interest income (from banking and insurance) up 23%

• Net commissions up 14.1%

• Technical margin on insurance operations up 13.1%

4

Highlights of Activity in 2006 (cont.)

• Net assets up 11.3% to EUR 96.3 billion

• Loans and advances to customers (gross) up 12.8% to EUR 58.8 billion

• Total resources taken by Group up 10.6% to around EUR 87.6 billion

• Gross return on equity (ROE) of 21.3%

• Improvement in cost-to-income ratio from 61.4% to 54.7%

• Improvement in credit quality and provisioning indicators

• Solvency ratio of 10.6%, with Tier 1 and Core Tier 1 of 7.1% and 6.0% respectively

• CGD continues to be the Portuguese bank with the best ratings

5

Principal Indicators

2005 2006 Change %

Net Income EURm 537.7 733,7 36.5%

Net Operating Income (1) EURm 2,441.5 2,977.3 21.9%

Net interest income (banking and insurance)EURm 1,454.5 1,788.3 23.0%

Non-interest income (1) EURm 474.4 609.2 28.4%

Technical Margin - Insurance EURm 512.6 579.9 13.1%

Net Assets EURm 86,461 96,252 11.3%

Loans and Advances to Customers EURm 52,153 58,834 12.8%

Total Resources Taken EURm 79,202 87,563 10.6%

Shareholders’ Equity EURm 4,325 5,006 15.8%

Cost-to-Income % 61.4% 54.7% -6.7 p.p

ROE % 18.3% 21.3% 3.0 p.p

ROA % 0.81% 1.10% 0.3 p.p

Solvency Ratio % 12.4% 10.6% -1.8 p.p

Tier I % 7.4% 7.1% -0.3 p.p

Note: Considering the consolidation of Compal by the equity accounting method

(1) Excluding the capital gains realised on the disposal of the Unibanco investment in 2005.

6

1. Highlights of 2006

2. Consolidated Operations

3. Operations by Business Area

4. Assets Quality and Solvency

5. Other Indicators

General Index

7

Consolidated Net Income for 2006

EURm 2005 2006 Charge %

+ Net interest Income 1,454.5 1,788.3 23.0%

+ Non-interest Income 658.3 609.2 -7.5%

Non-interest Income (1) 474.4 609.2 28.4%

+ Technical Margin - Insurance 512.6 579.9 13.1%

= Net Operating Income 2,625.4 2,977.3 13.4%

Net Operating Income (1) 2,441.5 2,977.3 21.9%

- Operating Costs 1,627.8 1,689.3 3.8%

= Gross Income 997.6 1,288.1 29.1%

- Impairment and Provisions 348.9 408.0 16.9%

+Income from Subsidiary and Associated Companies 25.0 109.7 338.0%

= Income before Tax 673.8 989.8 46.9%

- Tax 119.0 222.6 87.0%

- Minority Shareholders’ Interests 17.1 33.5 95.9%

= Net Income 537.7 733.7 36.5%

Note: Considering the consolidation of Compal by the equity accounting method

(1) Excluding the capital gains realised on the disposal of the Unibanco investment in 2005.

8

Annual Growth of Net Income

36%36%

EURm

654.0 665.0 667.0

448.0

537.7

733.7

2001 2002 2003 2004 2005 2006

9

Evolution of Net Interest Income

26%

23%23%

Net interest income (banking+insurance)

EURm

-18%

89

73

1,454

1,788

1,365

1,715

2005 2006

1.715

Dividends

Net Interest Income

10

89.0

73.0

2005 2006

Equity Capital Instruments

Evolution of Income from Equity Capital

Instruments

-18%-18%

EURm

PT Multimedia

BCP

PT

EDP

1.11.0

4.85.8

24.618.1

17.532.7

20062005

Principal Equity Investments

GALP 10.9-

Unibanco -18.5

Cimpor 2.0-

11

474.4

609.2

2005 2006

319.4

364.4

2005 2006

Evolution of Non-Interest Income

Evolution of Non-interest Income *

Commissions (net)

28%28% 14%14%

(*) Excluding the capital gains realised on the disposal of the Unibanco investment, in 2005.

EURm

12

20,030 20,778

2005 2006

912

859 879

2005 2006

Base Costs Pension F. Indemnities

644 635

125 142

1,628 1,689

912 859

2005 2006

Depreciation Other administrative expenditureEmployee costs

Evolution of Operating Costs

Operating Costs

Employee Costs

4%4%

Evolution of Employees

EURm

1023

2%

6% 6%

6%

-1%

14%

-748-748

13

28,670 31,002

2005 2006

30,567 33,837

18,778

21,584

3,41352,153

58,834

2,808

2005 2006

Individual Customers Companies Public Sector

Loans and Advances to Customers

Loans and Advances to Customers

13%13%

EURm

11%

22%

15%

Mortgage Lending

8%8%

14

87,563

79,202

2005 2006

6,420 7,637

1,040

1,253

3,856

11,536

12,746

4,076

2005 2006

Unit Trust Funds Pension Funds

Wealth Management

47,957 51,587

19,709

23,230

67,666

74,817

2005 2006

Customer Deposits (*) Other Resources

Resources Taken and Under Management

+Balance Sheet

ResourcesOther Resources

TakenTotal Resources

Taken=

11%11%11%11% 10%10%

(*) Excluding Fixed-Rate Insurance Products recognised in Life Insurance branches.

EURm

8%

18%

19%

-5%

20%

15

0.8%

1.1%

2005 2006

18.3%21.3%

2005 2006

32.4%29.5%

2005 2006

Efficiency and Profitability Ratios

Note: Gross profitability ratios considering average shareholders’ equity and net assets values.

Employee Costs Cost-to-Income

Return on Average Equity

Return on Average Assets

57.7%51.6%

61.4%54.7%

2005 2006

Group Banking

16

1. Highlights of 2006

2. Consolidated Operations

3. Operations by Business Area

4. Assets Quality and Solvency

5. Other Indicators

General Index

17

734

456

60 28

38

153

CommercialBanking Portugal

Insurance International InvestmentBanking

Other Total

Contribution to Net Income by Business Area

EURm

% of Total

62%62% 21%21% 5%5% 4%4% 8%8%

18

Insurance

19

1,4721,753

1,422

2,9903,175

1,519

2005 2006

Non-life Life

24%

33%

Operations in Portugal

Insurance Premiums

6%6%

Non-life

Total

Life

20%

EURm

Ranking

1st

1st

1st

20

95.4% 97.8%

2005 2006

165 158

216

409

224

35 38

427

2005 2006

Depreciation / AmortisationOther Administrative Costs Employee Costs

Principal Indicators

Net IncomeCombined Ratio

(Non-life)

28%28% 2.4 pp.2.4 pp.EURm

Structure Costs

EURm

-4%-4%

120.1

154.3

2005 2006

21

22

36.1% 34.0%

2005 2006

25.0 30.0

2005 2006

54.1 63.2

2005 2006

Investment Banking

Net Operating Income

Net IncomeCommissions

Net Operating Income by Area

Cost-to-Income

17%17% 22%22% 20%20%

-2.1 pp.-2.1 pp.

EURm

35.4 43.2

2005 2006

Financial Advisory Venture Capital

Project Finance Capital Market

45%

6%

26%

23%

Assessoria Financeira Capital de Risco

Project Finance Mercado de Capitais

23

Principal Rankings

Ranking (No. Operations)

Equity Capital Markets

2005 2006Source: CMVM, CaixaBI

2nd Place 1st Place

Ranking (Value of Operations)

Debt Capital Markets

2005 2006

Source: Bloomberg

1st Place 1st Place

Ranking (Value of Operations)

Mergers & Acquisitions

2005 2006Source: Bloomberg

3rd Place 1st Place

Ranking (Value of Operations)

Project Finance

2005 2006

Source: Dealogic

1st Portuguese5th Iberian

31st European

1st Portuguese3rd Iberian

6th European

24

25

0.83 0.79

Consumer Finance

2005 2006

11.4

15.0

Property Leasing

2005 2006

930 1,070

512

609 145

404 1,646

2,144

2005 2006

Property Leasing Equipment Leasing

Factoring Consumer Finance

Specialised Credit

Loans and Advances to Customers

30%30%

59

61

EURm

Market Shares (%)

9.2 10.1

2005 2006

14.2 13.9

Factoring

2005 2006

Equipment Leasing

26

27

4349

9

112

3

7

961

72

2005 2006

Wealth Management and Advisory

Pension Funds

Unit Trust Funds

Property Funds

5,465 6, 381

9551,2411,0401,243

14,551

15,182

24,047

22,010

2005 2006

Wealth Management and Advisory

Pension Funds

Unit Trust Funds

Property Funds

Assets under Management and Commissions

Assets under Management

Commissions

9%9% 18%18%

EURm

28

22% 13%

6%

25%

Market Shares

Unit Trust Funds Property Funds

Pension Funds Wealth Management

2005

2nd

1st

2006

2005

6th

5th

2006

2005

3rd

2nd

2006

2005

3rd

2nd

2006

29

30

7,9148,619

2005 2006

4,551

6,515

2005 2006

Credit and Resources

Loans and Advances to Customers*

Customer Resources

43%43%

9%9%

EURm

(*) Excluding international funding in France branch.

France Branch Banco Caixa Geral

BNU Macao Other

France Branch Banco Caixa Geral

BNU Macao Other

9%

27%

47%

17%

16%

22%41%

21%

31

1. Highlights of 2006

2. Consolidated Operations

3. Operations by Business Area

4. Assets Quality and Solvency

5. Other Indicators

General Index

32

2.3% 2.7%

-0.4% 0.0%

2005 2006

Non-performing credit ratio

Non-performing credit ratio (net)

2.1% 2.4%

1.9% 2.2%

2005 2006

Total Overdue Credit Ratio

Credit overdue for more than 90 days

101.4% 115.3%

2005 2006

125.2% 138.2%

2005 2006

Non-performing Loans and Provisioning

Overdue Credit Coverage > 90 days

Total Overdue Credit Non-Performing Credit

Non-performing Credit Coverage

33

Equity Capital

2005 1 2006 1 Change in 2006

EDP 69.1 272.4 203.3

PT (35.9) 30.8 66.7

BCP 38.4 66.6 28.2

PT Multimedia (6.9) 7.3 14.2

CIMPOR 0.4 19.1 18.7

GALP - 6.8 6.8

Euronext 10.4 30.1 19.7

TOTAL 75.5 433.1 357.6

(1) Recognised in balance sheet in reserves

Other Relevant CGD Investments

REN 19.9% 160.0

AdP 20.4% 88.5

Investment (%) Acquisition Cost (EURm)

Potential accumulated capital gains/losses in availablefor sale share portfolio in CGD’s balance sheet

34

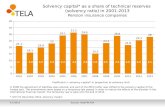

9.4%10.6%

12.4%

2004 2005 2006

Solvency Ratios

Note: Ratios calculated under Bank of Portugal regulations.

Total Ratio

Core Tier I Tier I

5.7% 6.2% 6.0%

2004 2005 2006

6.3%7.1%7.4%

2004 2005 2006

35

Pension Liabilities

100%100%Funding of Liabilities

419.2399.6Provisions

419.2399.6Medical Plan Liabilities

68.060.3Corridor Used

5.25%5.25%Fund Yield

2.00%2.00%Pensions Growth Rate

3.00%3.00%Wages Growth Rate

4.75%4.75%Discount Rate Used

20062005

6.53%9.22%Return on Pension Fund

TV 73/77TV 73/77Men’s Mortality Table

Women’s Mortality Table

Funding of Liabilities

Pension Fund

Pension Liabilities

TV 88/90

100%

955.3

955.3

TV 88/90

100%

824.6

824.6

EURm

121.7110.0Total Corridor

36

1. Highlights of 2006

2. Consolidated Operations

3. Operations by Business Area

4. Assets Quality and Solvency

5. Other Indicators

General Index

37

31%

30% 22%

24%

Market Shares

(*) Excluding securitised credits

Customer Deposits Loans and Advances to Customers*

Mortgage Lending * Insurance

1st

Ranking2006

1st

Ranking2006

1st

Ranking2006

2nd

Ranking2006

38

Long Term

Short Term

Ratings

A+

A-1

Aa3

P-1

AA-

F1+

Stable Stable NegativeOutlook

Standard & Poor’s

Moody’sFitch

Ratings

Standard & Poor’s (July 2006)“Caixa Geral de Depósitos’ ratings are based on the fact that the bank is fully owned by the Portuguese state (…); enjoying a solid position in domestic retail banking which provides the bank with a broad, stable low cost funding base and, particularly an adequate financial profile.”Moody’s (September 2006)“The rating awarded to Caixa Geral de Depósitos, has a stable trend, reflects the bank’s leading position in terms of market share in Portugal, its strong funding base and a low credit risk profile, with a diversified offer of products and services/diversified market position in which half of its credit portfolio is made up of mortgage lending. (…) CGD remains a benchmark operator in the banking system and enjoys a position, in the domestic market that very few European institutions enjoy in their respective countries.”

Fitch Ratings (September 2006)“Caixa Geral de Depósitos’ ratings reflect its quality as a state-owned bank and its strong position in the market with a dominant share of individual customers’ deposits and mortgage lending.”

A Group of Recognised Merit

Best Equity House in Portugal Euromoney 2006

1st national, 3rd Iberian and 6th European in Project FinancePFI - Project Finance International

Unit Trust Funds Leader in Portugal Associação Portuguesa de Fundos de Investimento, Pensões e Patrimónios

CGD continues to enjoy 1st place in terms of banking reliability in the eyes of the Portuguese

Portuguese still consider Fidelidade Mundial to be the leading, most trustworthy insurance companySelecções do Reader’s Digest

Highest ratings awarded to a Portuguese bankMoody’s, S&P, Fitch

2nd Insurance Group and 5th Bank in the Iberian Peninsula

1st Insurance Group in Portugal, leader in life and non-life insurance branchesAssociação Portuguesa de Seguradores

Best, most solid bank, best customer inquiries facilities, clearest and most reliable information; highest trust ratio levels in eyes of bank customersBasef 2006

Bank with most widely used internet banking service and highest customer satisfaction indices Netsonda 2006

40