19-1 P ROCESS C OST S YSTEMS CHAPTER 19 19-2 F Used for production of small, identical, low-cost...

56

19-1 PROCESS COST SYSTEMS CHAPTER 19

Transcript of 19-1 P ROCESS C OST S YSTEMS CHAPTER 19 19-2 F Used for production of small, identical, low-cost...

19-1

PROCESS COST SYSTEMS

CHAPTER 19CHAPTER 19

19-2

Used for production of small, identical, low-cost items. Mass produced in automated continuous production process. Costs cannot be directly traced to each unit of product.

Used for production of small, identical, low-cost items. Mass produced in automated continuous production process. Costs cannot be directly traced to each unit of product.

Process CostingProcess Costing

19-3

Similarities forSimilarities forJob and Process CostingJob and Process Costing

Same objective: to determine the cost of products

Same inventory accounts: raw materials, work in process, and finished goods

Same overhead assignment method:predetermined rate times actual activity

19-4

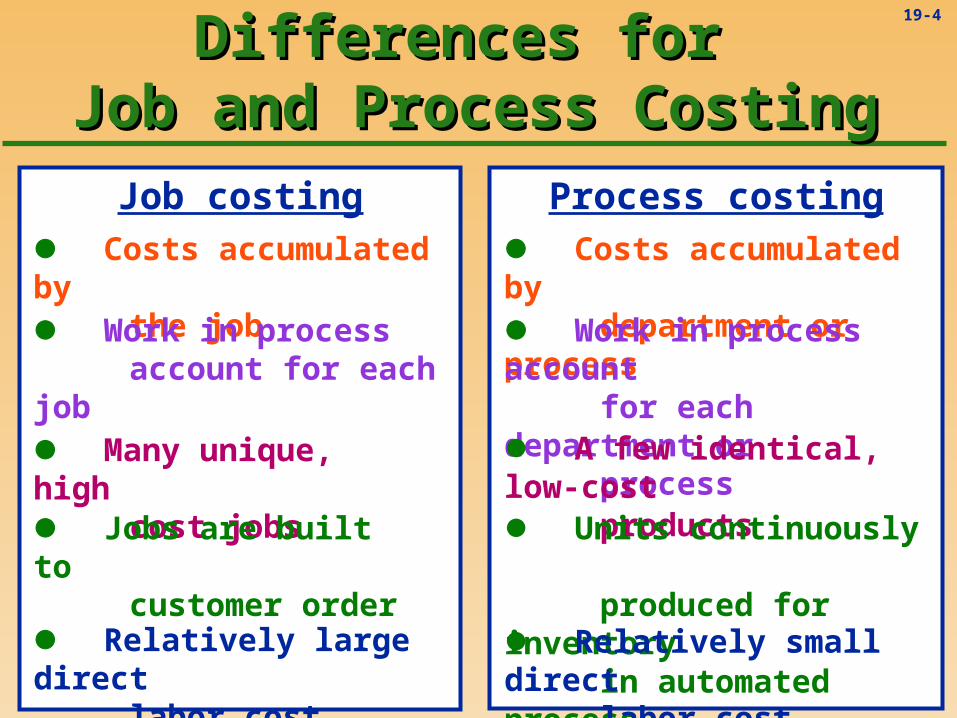

Differences for Differences for Job and Process CostingJob and Process Costing

Job costing Process costing Costs accumulated by the job

Costs accumulated by department or process Work in process

account for each job Work in process account for each department or process A few identical, low-cost products

Many unique, high cost jobs Jobs are built to customer order

Units continuously produced for inventory in automated process Relatively small direct labor cost component

Relatively large direct labor cost component

19-5

Process CostingProcess CostingDirect

Material

Type of Product Cost

Do

llar

Am

ou

nt

ManufacturingOverhead

DirectLabor

Direct labor costs are small compared to other productcosts because of the high level of automation.

So, direct labor and manufacturing overhead are oftencombined into one product cost called

conversion.

19-6

Process CostingProcess CostingDirect

Material

Conversion

So, direct labor and manufacturing overhead are oftencombined into one product cost called

conversion.

Type of Product Cost

Do

llar

Am

ou

nt

Direct labor costs are small compared to other productcosts because of the high level of automation.

19-7

Comparing Cost Flows for Comparing Cost Flows for Job and Process CostingJob and Process Costing

Direct Material

FinishedGoods

Cost of GoodsSold

Direct Labor

ManufacturingOverhead

Work inProcess

From Previous Chapter

19-8

Direct Material

FinishedGoods

Cost of GoodsSold

Direct Labor

ManufacturingOverhead

Jobs

The work in process account consists of individual jobs in a job cost system.

Comparing Cost Flows for Comparing Cost Flows for Job and Process CostingJob and Process Costing

19-9

Direct Material

FinishedGoods

Cost of GoodsSold

Direct Labor Products

The work in process account consists of

individual products in a process cost system.

ManufacturingOverhead

Comparing Cost Flows for Comparing Cost Flows for Job and Process CostingJob and Process Costing

19-10

Direct Material

FinishedGoods

Cost of GoodsSold

Direct Labor& Overhead

(Conversion)

When direct labor is a relatively smallamount compared to material and overhead,

it is often combined with overhead.

Products

Comparing Cost Flows for Comparing Cost Flows for Job and Process CostingJob and Process Costing

19-11

Process Costing Process Costing Cost FlowsCost Flows

Let’s examine the cost flows in a process cost

system with two departments. We will start

with materials.

19-12

Raw MaterialsPurchases

Mfg. Overhead

Work in Process-A

Work in Process-BTransferred

from Dept. A

Process Costing Process Costing Cost FlowsCost Flows

19-13

Work in Process-B

Raw MaterialsPurchases

Mfg. Overhead

Work in Process-A

Transferredfrom Dept. A

DirectMaterial

DirectMaterial

DirectMaterial

Process Costing Process Costing Cost FlowsCost Flows

19-14

Work in Process-B

Raw MaterialsPurchases

Mfg. Overhead

Work in Process-A

Transferredfrom Dept. A

DirectMaterial

DirectMaterial

DirectMaterialIndirectMaterial

Process Costing Process Costing Cost FlowsCost Flows

ActualOverhead

Costs

19-15

Next, let’s add labor costs to

the process cost flows. Are you

with me?

Process Costing Process Costing Cost FlowsCost Flows

19-16

Work in Process-B

Payroll SummaryActualWages

Mfg. Overhead

Work in Process-A

Transferredfrom Dept. A

DirectMaterial

DirectMaterial

ActualOverhead

Costs

Process Costing Process Costing Cost FlowsCost Flows

19-17

Work in Process-B

Payroll Summary

Mfg. Overhead

Work in Process-A

Transferredfrom Dept. A

DirectMaterialDirectLabor

DirectLabor

DirectMaterialDirectLabor

ActualOverhead

Costs

ActualWages

Process Costing Process Costing Cost FlowsCost Flows

19-18

Work in Process-B

Payroll Summary

Mfg. Overhead

ActualOverhead

Costs

Work in Process-A

Transferredfrom Dept. A

DirectMaterialDirectLabor

DirectLabor

Indirect Labor

DirectMaterialDirectLabor

ActualWages

Process Costing Process Costing Cost FlowsCost Flows

19-19

Work in Process-B

Payroll Summary

Mfg. Overhead

ActualOverhead

Costs

OverheadApplied to

Work inProcess

Work in Process-A

Transferredfrom Dept. A

DirectMaterialDirectLabor

Overhead

DirectLabor

Indirect Labor

DirectMaterialDirectLabor

Overhead

ActualWages

Process Costing Process Costing Cost FlowsCost Flows

19-20

Work in Process-B

Payroll Summary

Mfg. Overhead

ActualOverhead

Costs

OverheadApplied to

Work inProcess

Work in Process-A

Transferredfrom Dept. A

DirectMaterialDirectLabor

Overhead

Current Transfers to Dept. B

DirectLabor

Indirect Labor

DirectMaterialDirectLabor

Overhead

ActualWages

Process Costing Process Costing Cost FlowsCost Flows

19-21

Now, let’s complete the

goods and sell them. Still with

me?

Process Costing Process Costing Cost FlowsCost Flows

19-22

Finished Goods

Cost of Goods Sold

Work in Process-BTransferredfrom Dept. A

DirectMaterialDirectLabor

Overhead

Process Costing Process Costing Cost FlowsCost Flows

19-23

Finished Goods

Cost of Goods Sold

Cost ofGoodsMfg.

Work in Process-BTransferredfrom Dept. A

DirectMaterialDirectLabor

Overhead

Cost of Goods

Mfg.

Process Costing Process Costing Cost FlowsCost Flows

19-24

Finished Goods

Cost ofGoodsSold

Cost of Goods Sold

Cost ofGoodsMfg.

Cost ofGoodsSold

Work in Process-BTransferredfrom Dept. A

DirectMaterialDirectLabor

Overhead

Cost of Goods

Mfg.

Process Costing Process Costing Cost FlowsCost Flows

19-25

Costs are accumulated for a period of time by process or department.

Costs are accumulated for a period of time by process or department.

Unit cost is computed by dividing the accumulated costs by the number of

equivalent units produced in the period.

Unit cost is computed by dividing the accumulated costs by the number of

equivalent units produced in the period.

Process Costing Process Costing Equivalent UnitsEquivalent Units

19-26

Equivalent units is a conceptexpressing a number of partially

completed units as a smallernumber of fully completed units.

Equivalent units is a conceptexpressing a number of partially

completed units as a smallernumber of fully completed units.

Process Costing Process Costing Equivalent UnitsEquivalent Units

19-27

Two one-half full pitchers are equivalent to one full pitcher.

+ =

Equivalent UnitsEquivalent UnitsExampleExample

So, 10,000 units 70 percent complete is the equivalent of 7,000 complete units.

So, 10,000 units 70 percent complete is the equivalent of 7,000 complete units.

19-28

Equivalent UnitsEquivalent UnitsQuestionQuestion

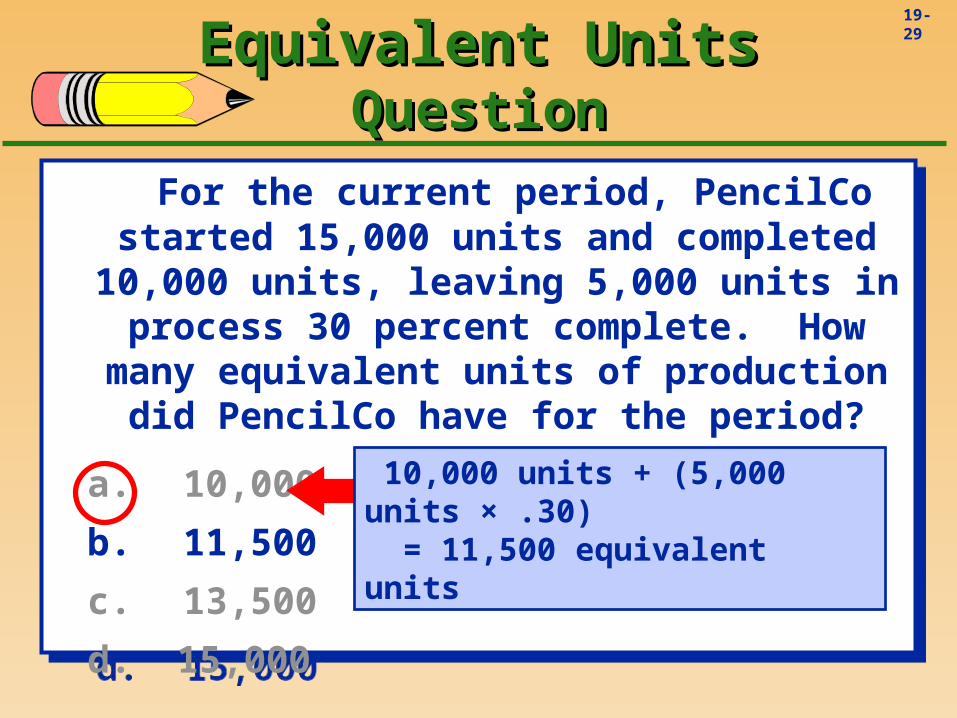

For the current period, PencilCo started 15,000 units and completed 10,000 units, leaving 5,000 units in process 30 percent complete. How many equivalent units of

production did PencilCo have for the period?

a. 10,000

b. 11,500

c. 13,500

d. 15,000

For the current period, PencilCo started 15,000 units and completed 10,000 units, leaving 5,000 units in process 30 percent complete. How many equivalent units of

production did PencilCo have for the period?

a. 10,000

b. 11,500

c. 13,500

d. 15,000

19-29

For the current period, PencilCo started 15,000 units and completed 10,000 units, leaving 5,000 units in process 30 percent complete. How many equivalent units of

production did PencilCo have for the period?

a. 10,000

b. 11,500

c. 13,500

d. 15,000

For the current period, PencilCo started 15,000 units and completed 10,000 units, leaving 5,000 units in process 30 percent complete. How many equivalent units of

production did PencilCo have for the period?

a. 10,000

b. 11,500

c. 13,500

d. 15,000

10,000 units + (5,000 units × .30) = 11,500 equivalent units

Equivalent UnitsEquivalent UnitsQuestionQuestion

19-30

Cost Per Equivalent UnitCost Per Equivalent Unit

Cost perequivalent

unit

= Product costs for the periodEquivalent units for the period

19-31

Equivalent UnitsEquivalent UnitsQuestionQuestion

Now assume that PencilCo incurred $27,600 in production costs. What was PencilCo’s cost per unit for the period?

a. $1.84

b. $2.40

c. $2.76

d. $2.90

Now assume that PencilCo incurred $27,600 in production costs. What was PencilCo’s cost per unit for the period?

a. $1.84

b. $2.40

c. $2.76

d. $2.90

19-32

Now assume that PencilCo incurred $27,600 in production costs. What was PencilCo’s cost per unit for the period?

a. $1.84

b. $2.40

c. $2.76

d. $2.90

Now assume that PencilCo incurred $27,600 in production costs. What was PencilCo’s cost per unit for the period?

a. $1.84

b. $2.40

c. $2.76

d. $2.90

$27,600 ÷ 11,500 equivalent units

= $2.40 per equivalent unit

Equivalent UnitsEquivalent UnitsQuestionQuestion

19-33

Production Cost ReportProduction Cost Report

ProductionCost Report

Shows the flowof units and coststhrough work in

process.

Shows division ofcosts between unitstransferred and unitsremaining in process.

Helps managerscontrol theirdepartments.

Provides costinformation for

financial statements.

19-34

Preparation includes four major steps: Trace the physical flow of units

Convert actual units to equivalent units

Compute cost per equivalent unit for eacheach cost element (material, conversion)

Use unit costs to determine cost of ending Work in Process (WIP) inventory and cost of goods transferred to Finished Goods.

Preparation includes four major steps: Trace the physical flow of units

Convert actual units to equivalent units

Compute cost per equivalent unit for eacheach cost element (material, conversion)

Use unit costs to determine cost of ending Work in Process (WIP) inventory and cost of goods transferred to Finished Goods.

Production Cost ReportProduction Cost Report

19-35

At this point, we need to look at an example to illustrate the concepts.

Production Cost ReportProduction Cost Report

19-36

Sipp-Fizz Cola uses process costingto determine unit costs. It has only

one processing department.

Sipp-Fizz Cola uses process costingto determine unit costs. It has only

one processing department.

Sipp-Fizz uses the average cost procedure:

The number of equivalent units for each costelement equals the number of units completed

and transferred to finished goods plus the number of equivalent units in ending work in

process inventory for that cost element.

Sipp-Fizz uses the average cost procedure:

The number of equivalent units for each costelement equals the number of units completed

and transferred to finished goods plus the number of equivalent units in ending work in

process inventory for that cost element.

Production Cost ReportProduction Cost ReportExampleExample

19-37

Production Cost ReportProduction Cost ReportExampleExample

The following information is from Sipp-

Fizz records for the month of August.

The following information is from Sipp-

Fizz records for the month of August.

Using this information, compute: Equivalent units.

Cost per equivalent unit.

Cost of goods completed and transferred.

Cost of ending work in process inventory.

Using this information, compute: Equivalent units.

Cost per equivalent unit.

Cost of goods completed and transferred.

Cost of ending work in process inventory.

One 12-can case equals one unit.

19-38

Beginning work in process, August 1Units, conversion 50% complete 4,000 cases/unitsCosts: Direct materials $ 12,000

Direct labor $ 6,120 Manufacturing overhead applied $ 8,000

12,000 units were started in August.

Costs incurred in AugustDirect materials $ 36,000Direct labor $ 48,000Manufacturing overhead applied $ 60,000

Ending work in process inventory, August 31Units, conversion 70% complete 6,000 cases/units

All materials are added at the beginning of processing

Production Cost ReportProduction Cost ReportExampleExample

19-39

Our first two steps are . . .

Trace the physical flow of units.

Convert actual units to equivalent units.

Because material is added at the beginning of the process, the Sipp-Fizzies are 100 percent complete as to material when the process starts.

Production Cost ReportProduction Cost ReportExampleExample

19-40

Trace the Physical Flow of Units

Units in beginning inventory 4,000Units started during month 12,000

Units to account for 16,000

6,000Less: Units in ending inventory

10,000 Units completed & transferred

1

Production Cost ReportProduction Cost ReportExampleExample

19-41

Conversion

Convert Actual Units to Equivalent Units

Actual Equivalent Units Units

Units completed & transferred 10,000Units in ending inventory* 6,000 Units accounted for 16,000

*Units in ending inventory are 100% complete as to materials and 70%complete as to conversion.

2

Production Cost ReportProduction Cost ReportExampleExample

Materials

19-42

Conversion

Convert Actual Units to Equivalent Units

Actual Equivalent Units Units

Units completed & transferred 10,000Units in ending inventory* 6,000 Units accounted for 16,000

*Units in ending inventory are 100% complete as to materials and 70%complete as to conversion.

2

Production Cost ReportProduction Cost ReportExampleExample

Materials10,000

6,000 16,000

10,000 4,200** 14,200

** 6,000 units x 70%complete = 4,200

19-43

Now that we havecalculated equivalent

units for Sipp-Fizz, let’scalculate the cost per

equivalent unit.

Production Cost ReportProduction Cost ReportExampleExample

19-44

Our next two steps are . . . Using equivalent units for each cost item,

compute the cost per equivalent unit for Materials Conversion Total

Use cost per equivalent unit from to determine cost of goods completed and transferred and cost of ending work in process inventory.

3

Production Cost ReportProduction Cost ReportExampleExample

19-45

Production Cost ReportProduction Cost ReportExampleExample

Materials Conversion Total

Beginning inventory 12,000$ 14,120$ 26,120$ Cost added in August 36,000 108,000 144,000

Costs to account for 48,000$ 122,120$ 170,120$

19-46

Production Cost ReportProduction Cost ReportExampleExample

Materials Conversion Total

Beginning inventory 12,000$ 14,120$ 26,120$ Cost added in August 36,000 108,000 144,000

Costs to account for 48,000$ 122,120$ 170,120$

Equivalent units 16,000 14,200

Equivalent units from and1 2

19-47

Production Cost ReportProduction Cost ReportExampleExample

Materials Conversion Total

Beginning inventory 12,000$ 14,120$ 26,120$ Cost added in August 36,000 108,000 144,000

Costs to account for 48,000$ 122,120$ 170,120$

Equivalent units

Cost per unit

Cost per unit for each cost element = Cost to account for ÷ Equivalent units

16,000 14,200

3.00$ 8.60$ 11.60$ 3

19-48

Production Cost ReportProduction Cost ReportExampleExample

Materials Conversion Total

Beginning inventory 12,000$ 14,120$ 26,120$ Cost added in August 36,000 108,000 144,000

Costs to account for 48,000$ 122,120$ 170,120$

Equivalent units

Cost per unit

Cost transferred out4

Cost per unit for each cost element = Cost to account for ÷ Equivalent units

16,000 14,200

3.00$ 8.60$ 11.60$ 330,000$ 86,000$ 116,000$

Cost transferred out = 10,000 units completed × cost per unit

19-49

Production Cost ReportProduction Cost ReportExampleExample

Materials Conversion Total

Beginning inventory 12,000$ 14,120$ 26,120$ Cost added in August 36,000 108,000 144,000

Costs to account for 48,000$ 122,120$ 170,120$

Equivalent units

Cost per unit

Cost transferred outEnding WIP inventory cost Costs accounted for

4

Cost per unit for each cost element = Cost to account for ÷ Equivalent units

16,000 14,200

3.00$ 8.60$ 11.60$ 330,000$ 86,000$ 116,000$18,000 36,120 54,120 48,000$ 122,120$ 170,120$

Cost transferred out = 10,000 units completed × cost per unit

Ending WIP inventory cost = equivalent units in ending inventory × cost per unit

19-50

Process CostingProcess CostingSpoilageSpoilage

Cost of goods lost during productionCost of goods lost during production

Normal spoilageis an expectedamount in an

efficient process.

Abnormal spoilageexceeds the expected

amount in anefficient process.

Cost isa loss in the

period ofproduction

Cost ispart of cost

of good unitsproduced

19-51

Process CostingProcess Costing

I see some journalentries for process

costing onthe horizon!

19-52

GENERAL JOURNAL

Page: 1

Date Description PR Debit Credit

Materials Inventory xxxxxx Accounts Payable xxxxxxTo record purchase of material

Work in Process Inventory xxxxxxManufacturing Overhead xxxxxx Materials Inventory xxxxxxTo record use of material

Process CostingProcess CostingTypical Accounting EntriesTypical Accounting Entries

19-53

GENERAL JOURNAL

Page: 1

Date Description PR Debit Credit

Work in Process Inventory xxxxxxManufacturing Overhead xxxxxx Payroll Summary xxxxxxTo record labor cost

Work in Process Inventory xxxxxx Manufacturing Overhead xxxxxxTo assign overhead to Work in Process

Process CostingProcess CostingTypical Accounting EntriesTypical Accounting Entries

19-54

GENERAL JOURNAL

Page: 1

Date Description PR Debit Credit

Finished Goods xxxxxx Work in Process Inventory xxxxxxTo record completion of work

Process CostingProcess CostingTypical Accounting EntriesTypical Accounting Entries

19-55

GENERAL JOURNAL

Page: 1

Date Description PR Debit Credit

Accounts Receivable xxxxxx Sales xxxxxxTo record sales

Cost of Goods Sold xxxxxx Finished Goods Inventory xxxxxxTo record cost of goods sold

Process CostingProcess CostingTypical Accounting EntriesTypical Accounting Entries

19-56

THE ENDTHE ENDIt’s been a long day. I’m ready to process some leisure time.