18-0 Week 11 Lecture 11 Ross, Westerfield and Jordan 7e Chapter 18 Dividends and Dividend Policy.

37

18-1 Week 11 Lecture 11 Ross, Westerfield and Jordan 7e Chapter 18 Dividends and Dividend Policy

-

Upload

lily-richards -

Category

Documents

-

view

226 -

download

2

Transcript of 18-0 Week 11 Lecture 11 Ross, Westerfield and Jordan 7e Chapter 18 Dividends and Dividend Policy.

18-1

Week 11

Lecture 11

Ross, Westerfield and Jordan 7e

Chapter 18

Dividends and Dividend Policy

18-2

Last Week..

• Capital Structure• Effect of Financial Leverage• M&M propositions I and II

• Case 1 – No Costs• Case 2 – With Taxes• Case 3 – With Taxes and Bankruptcy Costs

• Bankruptcy Costs• Direct & Indirect

• Optimal Capital Structure

18-3

Chapter 18 Outline

• Cash Dividends and Dividend Payment

• Does Dividend Policy Matter?

• Some Real-World Factors Favoring a Low Payout

• Some Real-World Factors Favoring a High Payout

• A Resolution of Real-World Factors

• Establishing a Dividend Policy

• Stock Repurchase: An Alternative to Cash Dividends

• Stock Dividends and Stock Splits

18-4

Cash Dividends

• Regular cash dividend • – cash payments made directly to

stockholders, usually each quarter

• Extra cash dividend • – indication that the “extra” amount may not be

repeated in the future

• Special cash dividend • – similar to extra dividend, but definitely won’t

be repeated

• Liquidating dividend • – some or all of the business has been sold

18-5

Dividend Payment - Chronology

• Declaration Date • Board declares the dividend and it becomes a liability

of the firm• Ex-dividend Date

• Two business days before date of record• Stock bought on or after this date, will not receive

the dividend• Stock price generally drops by about the amount

of the dividend• Date of Record

• Holders of record are determined • Date of Payment

• Cheques are mailed

18-6

Figure 18.2 - Price Behavior around ex date

18-7

Example 18.1

• Divided Airlines has declared a $2.50 dividend per share payable on Tuesday, May 30, to shareholders of record as of Tuesday, May 9.

• An investor buys 100 shares of this company on Tuesday May 2 for $150 each.

• What is the ex date? What are the events happening with respect to the dividend and stock price?

18-8

Example 18.1 continued..

• Purchase: Tuesday 2nd of May• Ex date: Friday 5th of May

Saturday 6th do not count

Sunday 7th Monday 8th of May

• Date of record: Tuesday 9th of May• Checks mailed: Tuesday 30th of May

2nd 5th 9th 30th Purchase Ex-date Record date Payment

18-9

Example 18.1 continued..

Value of stock around ex-dividend date

$150 $147.50

-t . . . 0 . . . t

$2.50 ex-dividend price drop

Investor’s wealth at dividend payment date:• $147.50 x 100 shares = $14,750• $2.50 x 100 shares = $250

Total = $15,000

18-10

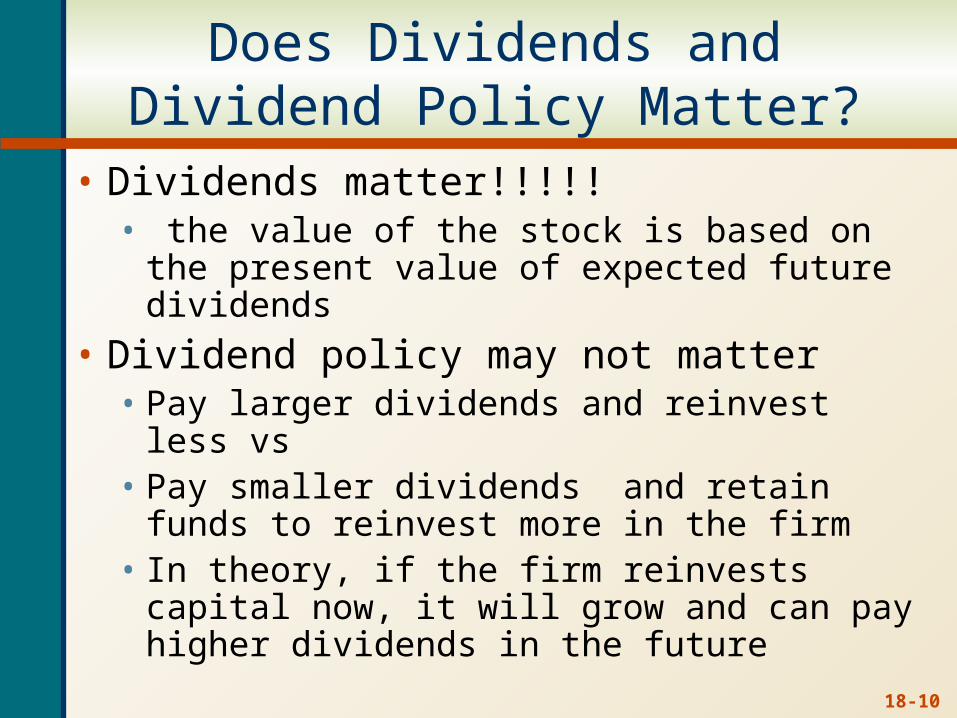

Does Dividends and Dividend Policy Matter?

• Dividends matter!!!!!• the value of the stock is based on the present

value of expected future dividends

• Dividend policy may not matter• Pay larger dividends and reinvest less vs• Pay smaller dividends and retain funds to

reinvest more in the firm• In theory, if the firm reinvests capital now, it

will grow and can pay higher dividends in the future

18-11

Irrelevance Theory

• Modigliani and Miller’s (1961) irrelevance theory makes use of home-made dividends and relies on a number of assumptions: • No company taxes, no transaction costs or market

imperfections.• No personal taxes• A fixed capital budgeting program

• The value of a firm:• is determined by the earning power of the firm’s

assets• is not affected how the income is split between

dividends and retained earnings.

18-12

Illustration of Irrelevance

• Palm Inc. is a firm with 2 year life and 100 shares • Policy 1: pay out dividends of $100 each year • Policy 2: pay $90 dividend year 1, reinvest the

other $10 into the firm and then pay $111.20 next year. Investors require a 12% return.

• Which policy is the best?• It doesn’t matter !! Value is the same

• Market Value with constant dividend = $16,900.51• PV = 10,000 / 1.12 + 10,000 / 1.122 = 16,900.51

• Market Value with reinvestment = $16,900.51• PV = 9000 / 1.12 + 11,120 / 1.122 = 16,900.51

18-13

• Operating CF = $10,000; Net Investment = $8,000• Shares Outstanding = 1,000 Shares; • Price per share = $42. Firm has a finite life.

Bianchi Inc. Policy 1 Policy 2$2 Div. $3 Div

Dividends 2,000 $3,000Ex-dividend Price per share $40 $39New Equity Issued $0 $1,000Shares Outstanding 1,000 1,025.64Value of the Firm $40,000 $40,000

($40 x 1000) ($39 x 1025.64)

Irrelevance of Dividend Policy - Example

18-14

Homemade Dividend Policy

• Investors will not pay higher prices for firms with higher dividend payouts.

• In other words, dividend policy will have no impact on the value of the firm because investors can create whatever income stream they prefer by using homemade dividends.

• Homemade Dividend Policy = Tailored dividend policy created by individual investors to undo corporate dividend policy

18-15

Homemade Dividend - Example

• A company has a choice between 2 dividend policies. Req. rate of return is 10%

• The company implements Policy 2 – pay $110 now• Investor X prefers Policy 1 – he wants $100 each year• Homemade Dividend:

• X can retain only $100 and reinvest the extra $10. • At 10% it will grow to $11. • In year 2, X receives 89+11= 100, the desired amount.

Policy 1 Policy 2

Year 1 $100 $110

Year 2 $100 $89

18-16

Homemade Dividends - Example

• Bianchi Inc. (slide 12) is a $42 stock about to pay a $2 dividend.• Bob Investor owns 80 shares and prefers $3 dividend.• Bob’s homemade dividend strategy:

• Sell 2 shares ex-dividend

if co. pays $2 Dividendhomemade dividends

Cash from dividend $160

Cash from selling stock $80

Total Cash Desired $240

Value of Stock Holdings $40 × 78 =

$3,120Total Wealth $3,360

same as if co. paid

$3 Dividend

$240

$0

$240

$39 × 80 =

$3,120

$3,360

18-17

Dividend Policy is Irrelevant

• Since investors do not need dividends to convert shares to cash, dividend policy will have no impact on the value of the firm.

• In the above example, Bob Investor began with total wealth of $3,360:

80 shares x $42 = $3,360

• After a $3 dividend, his total wealth is still $3,360:$240 + (80 shares x $39) = $3,360

• After a $2 dividend, and sale of 2 ex-dividend shares, his total wealth is still $3,360:

$160 + (2 shares x $40) + (78 shares x $40) = $3,360

18-18

Contrary Views

• Others believe dividend policy is relevant.

• They argue that:

• investors prefer high dividend policy because

dividends are cash, and so are less risky than capital

gains that depend on future market sentiment.

• Differential tax treatment for dividends and capital

gains can either favour or penalise a dividend policy.

18-19

Low Payout Please

• Why might a low payout be desirable?• Individuals in upper income tax brackets might

prefer lower dividend payouts, given the immediate tax liability, in favor of higher capital gains with the deferred tax liability

• Flotation costs – low payouts can decrease the amount of capital that needs to be raised, thereby lowering flotation costs

• Dividend restrictions – debt contracts might limit the percentage of income that can be paid out as dividends

18-20

High Payout Please

• Why might a high payout be desirable?1)Desire for current income

• Individuals that need current income, i.e. retirees

• Groups that are prohibited from spending principal (trusts and endowments)

2)Uncertainty resolution – no guarantee that the higher future dividends will materialize

3)Taxes• Dividend income taxed less for corporation shareholders

• Tax-exempt investors don’t have to worry about differential treatment between dividends and capital gains

18-21

Dividends and Signals

• Asymmetric information – managers have more information about the health of the company than investors

• Information Content Effect > Changes in dividends convey information > Cause market reaction• Dividend increases

• Management believes it can be sustained• Expectation of higher future dividends, increasing present value• Signal of a healthy, growing firm

• Dividend decreases• Management believes it can no longer sustain the current level of

dividends• Expectation of lower dividends indefinitely; decreasing present value• Signal of a firm that is having financial difficulties

18-22

Clientele Effect

• Some investors prefer low dividend payouts and will buy stock in those companies that offer low dividend payouts

• Some investors prefer high dividend payouts and will buy stock in those companies that offer high dividend payouts

• If a firms changes the dividend policy from low to high or vice versa, it doesn’t matter!!

18-23

Types of Dividend Policies

• Residual dividend policy

• Constant growth dividend policy – dividends increased at a constant rate each year

• Constant payout ratio – pay a constant percent of earnings each year

• Compromise dividend policy

• Dividend Reinvestment Plans – DRPs

18-24

Residual Dividend Policy

• Determine capital budget• Determine target capital structure• Finance investments with a combination of

debt and equity in line with the target capital structure• Remember that retained earnings are equity• If additional equity is needed, issue new

shares

• If there are excess earnings, then pay the remainder out in dividends

18-25

Example – Residual Dividend Policy

• Given• Need $5 million for new investments• Target capital structure: D/E = 2/3• Net Income = $4 million

• Finding dividend• 40% financed with debt (2 million)• 60% financed with equity (3 million)• Net Income – equity financing = $1 million,

paid out as dividends

18-26

Dividend Stability

• Strict Residual Policy may lead to very unstable dividend payout• Depends on profitable investment

opportunities

• When earnings are seasonal, quarterly dividends can vary• Eg. Department stores before/after Christmas

• Stable dividend policy is in the interest of the firm and its shareholders.• Decrease uncertainty of future dividends

18-27

Compromise Dividend Policy

• Goals, ranked in order of importance• Avoid cutting back on positive NPV projects to

pay a dividend• Avoid dividend cuts• Avoid the need to sell equity• Maintain a target debt/equity ratio• Maintain a target dividend payout ratio

• Companies want to accept positive NPV projects, while avoiding negative signals

18-28

Dividend Reinvestment Plans - DRPs

• Cash dividends are used to buy additional newly issued shares in the company

• Advantages to the Company:• cheap and effective means of raising capital and

conserving cash• promotes good shareholder relations

• Disadvantages to the company:• administration costs• promotion of the plan• may lead to excessive capital raising

18-29

• Benefits to Investors• taxation benefits• flexibility• savings program• no transaction costs involved• sometimes offered at a discount

• Disadvantages to investors• non-participants get diluted when participants get new

shares at a discount.

• comprehensive records to be maintained

• no control over the reinvestment price

Dividend Reinvestment Plans - DRPs

18-30

Stock Repurchase

• Company buys back its own shares of stock

• Tender offer – company states a purchase price and a desired

number of shares

• Open market – buys stock in the open market

• Similar to a cash dividend in that it returns cash from the

firm to the stockholders

• Supports the argument for dividend policy irrelevance in

the absence of taxes or other imperfections

• In a world with taxes, repurchases may be more

desirable due to the options provided to stockholders

18-31

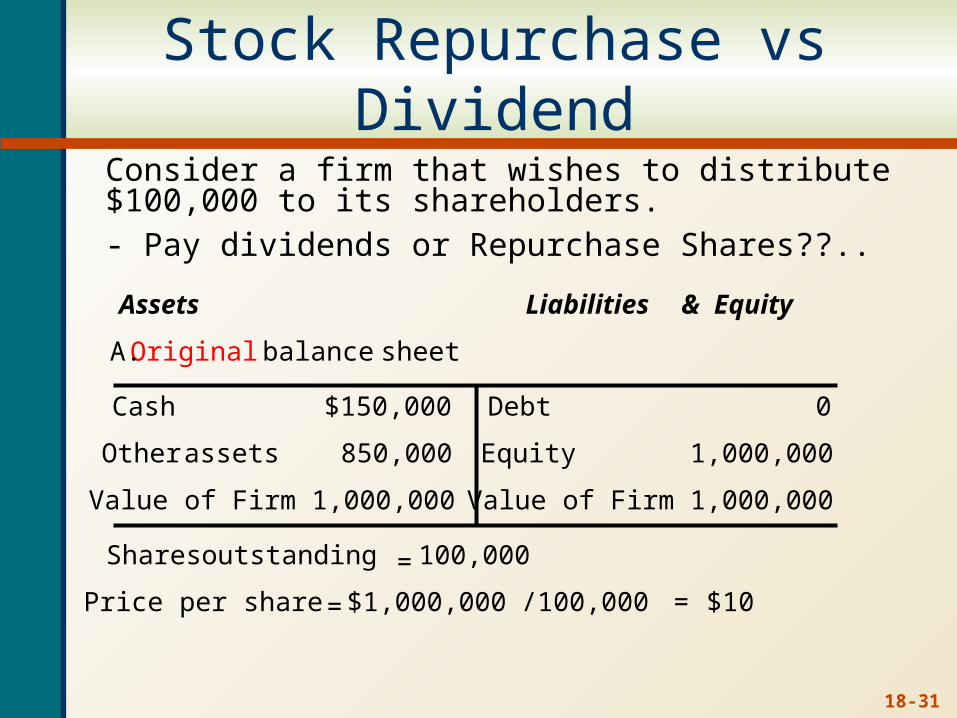

Stock Repurchase vs Dividend

$10=/100,000$1,000,000=Price per share

100,000=outstanding Shares

1,000,000Value of Firm1,000,000Value of Firm

1,000,000Equity850,000assetsOther

0Debt$150,000Cash

sheet balance Original A.

Equity &Liabilities Assets

Consider a firm that wishes to distribute $100,000 to its shareholders.- Pay dividends or Repurchase Shares??..

18-32

Stock Repurchase vs Dividend

$9=00,000$900,000/1 = shareper Price

100,000=outstanding Shares

900,000Firm of Value900,000Firm of Value

900,000Equity850,000assetsOther

0Debt$50,000Cash

dividendcash shareper $1After B.

Equity & Liabilities Assets

If they distribute the $100,000 as cash dividend, the balance sheet will look like this:

18-33

Stock Repurchase vs Dividend

Assets Li abilities & Equity

C. After stock repurchase

Cash $50,000 Debt 0

Other assets 850,000 Equity 900,000

Value of Firm 900,000 Value of Firm 900,000

Shares outstanding = 90,000

Price per share = $900,000 / 90,000 = $10

If they distribute the $100,000 through a stock repurchase, the balance sheet will look like this:

18-34

Stock Dividends

• Pay additional shares of stock instead of cash• Increases the number of outstanding shares• Small stock dividend – less than 20 to 25%• Large stock dividend – more than 20 to 25%• If you own 100 shares, at $30 each, and

the company declared a 10% stock dividend:• New total shares = old shares x (1+ %) = 110• New price = old $/(1+ %) = $27.27• Same value as before: $3000

18-35

Stock Splits

• Stock splits – essentially the same as a stock dividend except expressed as a ratio

• Stock price is reduced when the stock splits• If have 100 shares @ $30 each• A 2 for 1 stock split is the same as a 100% stock div.• New nr of shares = old nr. x (new nr./old nr.) = 200• New price = old $ x (old/ new) = $15

• Common explanation for split is to return price to a “more desirable trading range”

• Reverse split – number of share is reduced• If same data and have a 1 for 2 reverse split:• New nr of shares = old nr. x (new nr./old nr) = 50• New price = old $ x (old/ new) = $60

18-36

Conclusion

• Dividends are important because the value of a share is determined by expectations about future dividends.

• There is no ideal dividend policy. Boards must determine the dividend policy that best suits the type of business they are in, and the economic conditions they face.

18-37

End Chapter 18