1.7.6.G1 © Family Economics & Financial Education –March 2008 – Financial Institutions –...

19

1.7.6.G1 © Family Economics & Financial Education –March 2008 – Financial Institutions – Online Banking Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at the University of Arizona Online Banking Take Charge of your Finances

-

date post

19-Dec-2015 -

Category

Documents

-

view

219 -

download

3

Transcript of 1.7.6.G1 © Family Economics & Financial Education –March 2008 – Financial Institutions –...

1.7.6.G1

© Family Economics & Financial Education –March 2008 – Financial Institutions – Online BankingFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at

the University of Arizona

Online Banking

Take Charge of your Finances

1.7.6.G1

© Family Economics & Financial Education –March 2008 – Financial Institutions – Online BankingFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at

the University of Arizona

Online Banking

• In the year 2006, 63 million Americans reported that they used online banking

• 43% of internet users in the United States bank online

1.7.6.G1

© Family Economics & Financial Education –March 2008 – Financial Institutions – Online BankingFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at

the University of Arizona

Online Banking• Online banking – also known as

internet banking, allows consumers to complete transactions with wireless technology. Wireless technology includes: – Personal Computers (PCs) – Personal Digital Assistants (PDAs)– Cellular phones

1.7.6.G1

© Family Economics & Financial Education –March 2008 – Financial Institutions – Online BankingFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at

the University of Arizona

Online Banking• Consumers can access account

information and statements

1.7.6.G1

© Family Economics & Financial Education –March 2008 – Financial Institutions – Online BankingFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at

the University of Arizona

Online Banking• Consumers can transfer funds

1.7.6.G1

© Family Economics & Financial Education –March 2008 – Financial Institutions – Online BankingFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at

the University of Arizona

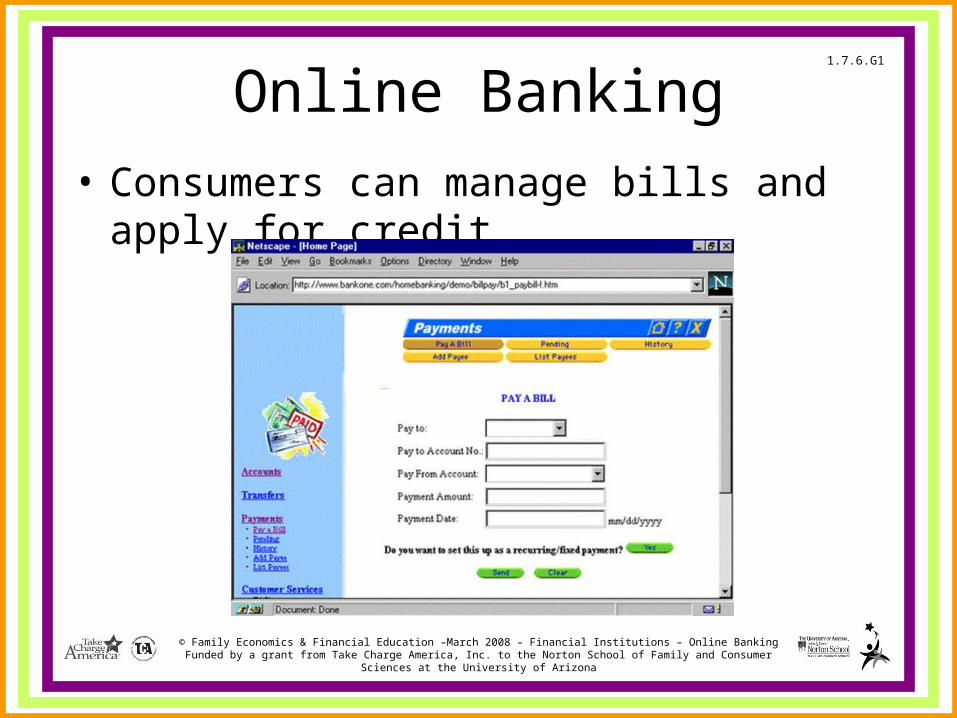

Online Banking• Consumers can manage bills and

apply for credit

1.7.6.G1

© Family Economics & Financial Education –March 2008 – Financial Institutions – Online BankingFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at

the University of Arizona

Online Banking• Advantages of online banking include:

– Decreased cost of paper and postage– Storing all statements online instead of keeping a

paper copy – Convenience – Paying bills online– Ability to access account anytime – No waiting for a monthly statement

• Disadvantages of online banking include: – Not as personal – Not able to access without technology – Decrease in safety features – Increase in risk for fraud

1.7.6.G1

© Family Economics & Financial Education –March 2008 – Financial Institutions – Online BankingFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at

the University of Arizona

Online Banking

Advantages• Decreased cost of

paper and postage• Storing all statements

online instead of keeping a paper copy

• Convenience • Paying bills online• Ability to access

account anytime • No waiting for a

monthly statement

Disadvantages• Not as personal • Not able to access

without technology • Decrease in safety

features • Increase in risk for

fraud

1.7.6.G1

© Family Economics & Financial Education –March 2008 – Financial Institutions – Online BankingFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at

the University of Arizona

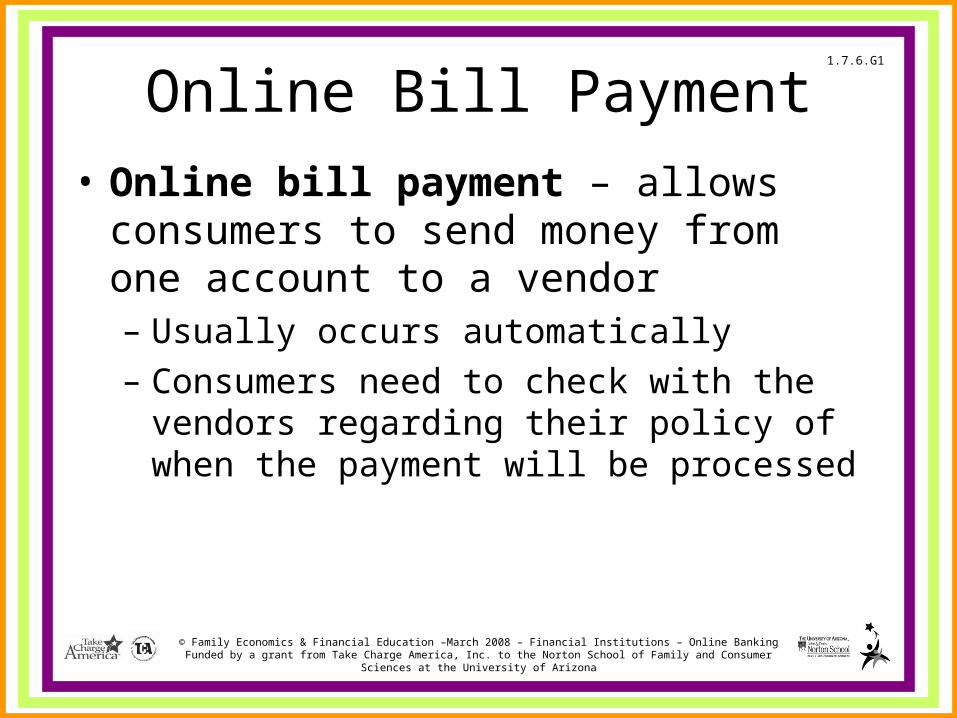

Online Bill Payment• Online bill payment – allows

consumers to send money from one account to a vendor – Usually occurs automatically – Consumers need to check with the

vendors regarding their policy of when the payment will be processed

1.7.6.G1

© Family Economics & Financial Education –March 2008 – Financial Institutions – Online BankingFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at

the University of Arizona

Online Bill Payment• Examples of companies that use online bill

payment include: – Retailer banks– Credit card companies– Insurance companies– Energy and utility companies– Health care– Transportation companies– Education expenses

1.7.6.G1

© Family Economics & Financial Education –March 2008 – Financial Institutions – Online BankingFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at

the University of Arizona

Online Bill Payment

1.7.6.G1

© Family Economics & Financial Education –March 2008 – Financial Institutions – Online BankingFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at

the University of Arizona

Online Bill Payment • Important financial aspects include:

– Checking with the vendor or company to understand their policy of when transactions are complete

– Confirming there are enough funds in the account to cover the expense of the bill

– Confirming bill will be paid, money will be taken out of the account, and the transaction will be completed

– Their financial information is secure and it is safe to make online transactions

1.7.6.G1

© Family Economics & Financial Education –March 2008 – Financial Institutions – Online BankingFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at

the University of Arizona

Determine Security • The Uniform Resource Locator (URL)

ends in “s” which stands for secure • A closed lock to the right of the URL or

in the bottom right hand corner of the web browser to indicate a secure site

1.7.6.G1

© Family Economics & Financial Education –March 2008 – Financial Institutions – Online BankingFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at

the University of Arizona

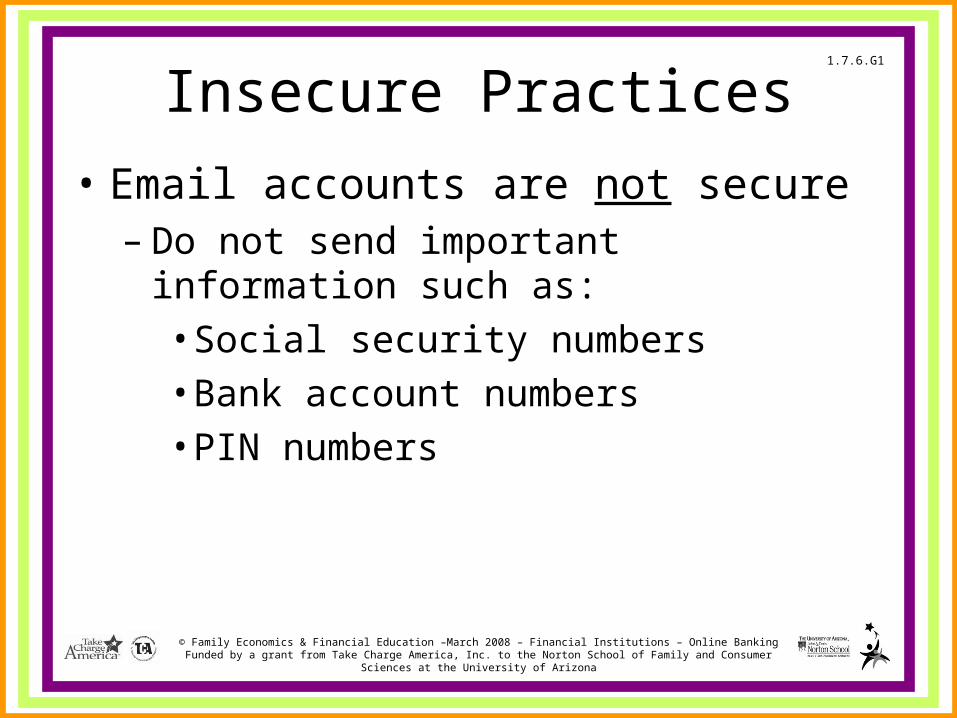

Insecure Practices• Email accounts are not secure

– Do not send important information such as:•Social security numbers •Bank account numbers•PIN numbers

1.7.6.G1

© Family Economics & Financial Education –March 2008 – Financial Institutions – Online BankingFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at

the University of Arizona

Consumer Protection• The Federal Bank of Chicago suggests the

following: – Passwords are a combination of letters and

numbers – Change passwords once a month– Keep all receipts and compare them to bank

statements monthly – Log out of depository institution Web sites

immediately after you finish working – Contact the depository institution directly with

any questions or concerns

1.7.6.G1

© Family Economics & Financial Education –March 2008 – Financial Institutions – Online BankingFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at

the University of Arizona

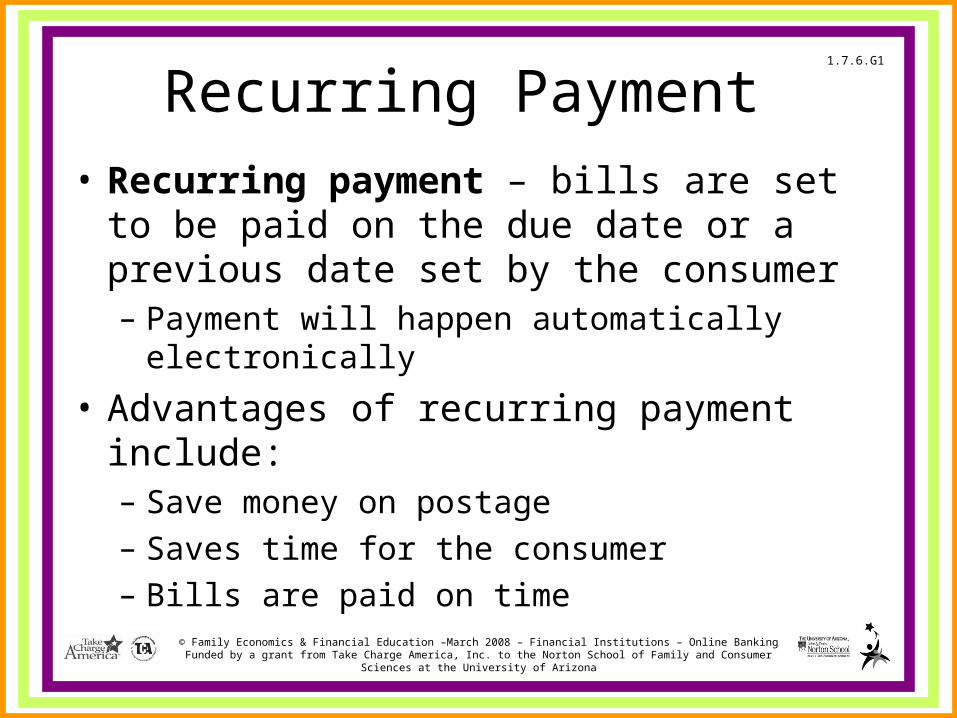

Recurring Payment • Recurring payment – bills are set to

be paid on the due date or a previous date set by the consumer – Payment will happen automatically

electronically

• Advantages of recurring payment include: – Save money on postage – Saves time for the consumer – Bills are paid on time

1.7.6.G1

© Family Economics & Financial Education –March 2008 – Financial Institutions – Online BankingFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at

the University of Arizona

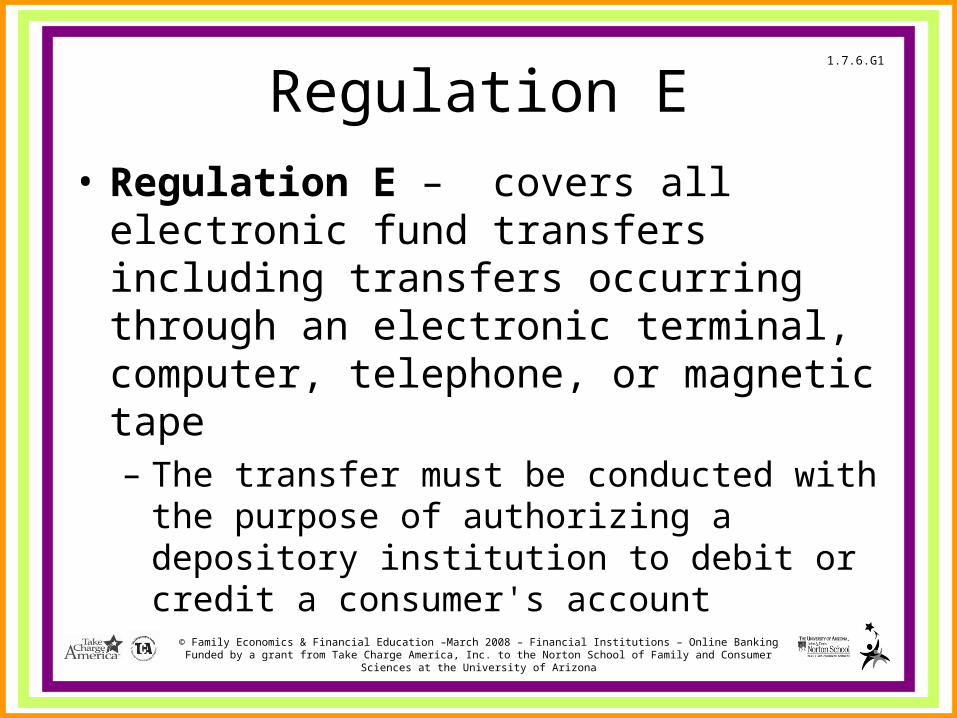

Regulation E• Regulation E – covers all electronic

fund transfers including transfers occurring through an electronic terminal, computer, telephone, or magnetic tape – The transfer must be conducted with the

purpose of authorizing a depository institution to debit or credit a consumer's account

1.7.6.G1

© Family Economics & Financial Education –March 2008 – Financial Institutions – Online BankingFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at

the University of Arizona

Consumer Protection• Privacy Policy outlines how a

consumer’s information will be used and protected

• Opting out of a financial policy allows a consumer to request a depository institution to share only a limited amount of personal information

1.7.6.G1

© Family Economics & Financial Education –March 2008 – Financial Institutions – Online BankingFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at

the University of Arizona

Conclusion• Review

– Define online banking – Review what transactions can be

completed through online banking– Discuss advantages and disadvantages of

online banking– Discuss online bill payment – What are secure and insecure online

banking practices?

• Any questions?