15.431: Entrepreneurial Finance · The World of Entrepreneurial ... Entrepreneurs have Higher...

25

15.431: Entrepreneurial Finance Spring 2002 Antoinette Schoar Sloan School of Management MIT 1

Transcript of 15.431: Entrepreneurial Finance · The World of Entrepreneurial ... Entrepreneurs have Higher...

15.431:Entrepreneurial Finance

Spring 2002

Antoinette Schoar Sloan School of Management

MIT 1

Course Overview: The World of Entrepreneurial

Finance

� Large increase in supply of and demand for venture

capital/private equity.

– Record amounts raised in every year 1995-2000.

– Even with drop in fundraising in 2001 it is about what it was

in 1998 and 17x the level in 1990.

– Likely to continue at relatively high rates, i.e. probably not

just boom part of cycle.

� Does this reflect a structural shift in the way new

businesses/projects are organized and financed?

2

$ b

illi

on

Unprecedented Flow of Funds into

Start-up Companies

120

100

80

60

40

20

0

1980 1985 1990 1995 2000

Investment Fundraising

Data Source: Venture Economics

3

What Is Special About Entrepreneurial Finance?

� Valuing New Ventures– Large uncertainties

– Massive option values

� Financing new ventures: – Large financing needs

– Severe information problems

– Severe agency problems

� These issues are common to all new “projects,” but

here we focus on how investors and entrepreneurs

deal with them.

4

Course Perspectives and Goals

� Understand the broader issues of investing in

entrepreneurial ventures

� Understand the more detailed issues of how to

evaluate and finance entrepreneurial investments

� Apply tools developed in 15.401 and 15.402, and go

beyond them:

– Issues here are more complex

– Finance most important in birth and death of firms

� Study interaction of finance and strategy

5

Course Perspectives and Goals

� Ultimately our goal is to give you some of the

tools you need to:

– Start a company and finance it

– Be a venture capitalist or private equity partner

– Invest in private equity partnerships

6

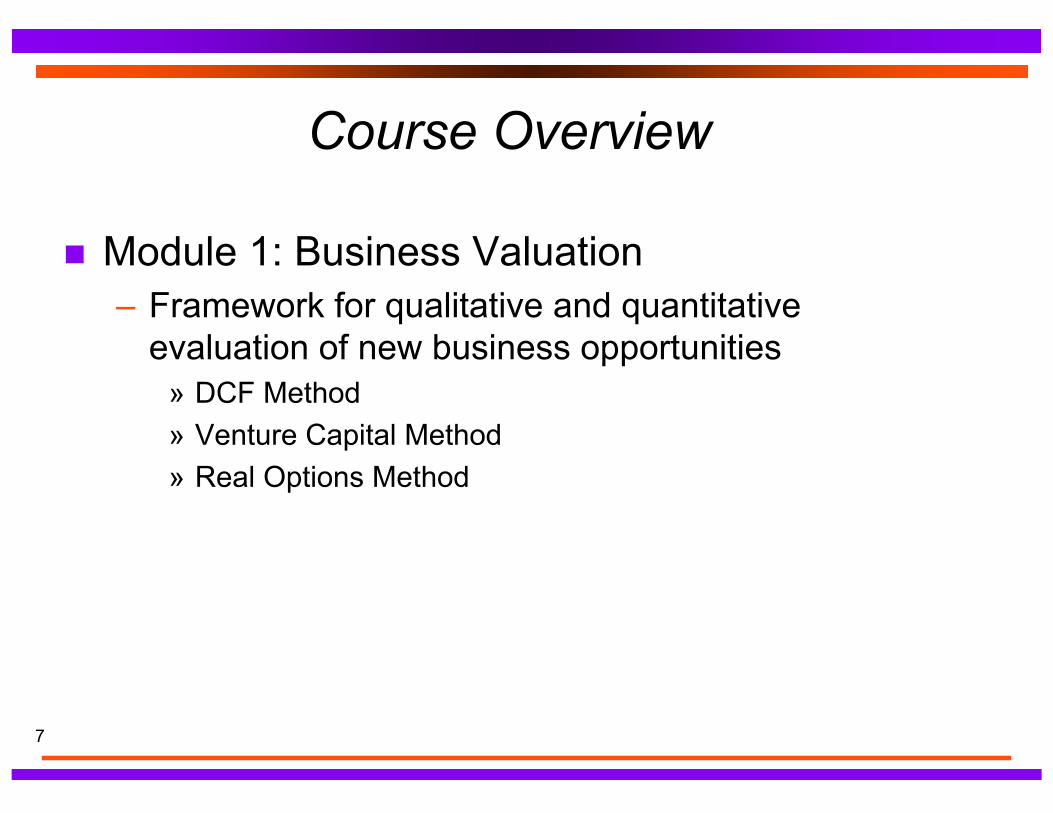

Course Overview

� Module 1: Business Valuation

– Framework for qualitative and quantitative

evaluation of new business opportunities

» DCF Method

» Venture Capital Method

» Real Options Method

7

Course Overview

� Module 2: Structuring Investments/Financing– Terms of the initial investment/financing

» Understanding deal terms

» Evaluating deal terms

» Negotiating deal terms

– Follow-on investments

– Later Stage Deals

8

Course Overview

� Module 3: Venture Capital Funds– Structure of partnership compensation

» Structure of partnership covenants

» Partnership strategies

– Corporate Venture Capital Funds

– International Venture Capital Funds

9

Course Overview

� Module 4: Employment Issues

– Joining start-ups

– Valuing alternative compensation plans

� Module 5: Exit

– IPO

– Sale

– Liquidation

10

Course Mechanics

� Cases (16), Lectures (6), Guests (2)

� Guideline questions for each case available

– Work in study groups of no more than 4

– Expect to grope around

» Not meant to be easy, but you'll learn more

» Do not use outside sources (library, web) to find out what

happened

11

Memos

� Memos are 10% of grade

� Hand in memos for 12 out of 16 cases. Must do first

case, Technical Data Corporation

� Be ready to discuss cases even if you’re not handing

in memo

� Memos should answer two questions: – What is going on?

– What would you do?

� Write to major decision-maker

� Up to two pages of text – Attach exhibits / calculations

12

Class Participation

� 30% of final grade

– Individual

– Based on quality and quantity

– Good chance for to practice in low-risk

environment

– Isn't class participation grade subjective?

» Not after 20 cases

» TA will be taking notes in class

– Mid-term participation grades

13

Class Participation Process

� You know the basic rules� Listen to others and build

– Try not to change the subject

� Ask questions – Sometimes whole class is lost

� I may cold call

� Please don't come late!

14

Final Exam

� 60% of your grade

� Case based

� Take home exam

� I grade the exams, not T.A.

15

This Course Is Not For Everyone

� Requires Tolerance for Ambiguity:– Entrepreneurial ventures involve massive

uncertainty

– Not always a formula or “right answer”– Please do not take the course if you are looking

for cookbook answers

� Requires Work: – One Case/Memo Per Week

– Class Attendance

16

Scheduling: Guests

� John Chory (Hale and Dorr)– Thursday, April 4th

� Alan Spoon (Polaris Venture Partners)

– Tuesday, April 9th

17

Exciting Time for Entrepreneurship

� Large increase in supply and demand for

private equity

– Massive inflows of funds in to VC partnerships

– Record number of firms in the industry

� Huge opportunities

– New technologies

– Regulatory changes

– Organizational changes

18

$ b

illi

on

Unprecedented Flow of Funds into

Start-up Companies

120

100

80

60

40

20

0

1980 1985 1990 1995 2000

Investment Fundraising

Data Source: Venture Economics

19

20

World wide rise in New Venture

Financing

0

5000

10000

15000

20000

25000

30000

1989

1990

1991

1992

1993

1994

19

95

1996

19

97

1998

1999

0

5000

10000

15000

20000

25000

30000

Fund Flows into Companies - Europe 1989-1999

Year

EU

R i

n b

illi

on

s

New Funds Raised

Investments

Data Source: European Venture Capital Association

21

Unprecedented Number of IPOs

0

50

100

150

200

250

300

1980

19

82

1984

19

86

1988

19

90

1992

19

94

1996

19

98

2000

VC backed IPOs

VC backed IPOs

Data Source: SDC

But there are Differences ...

-150

-100

0

50

100

150

92 93 94 95 96 97 98

%

i

(%)

Mini

IRR For US Venture Capital Firms 1992-1998

-50

Year

Max mum IRR

Median IRR

mum IRR

Data Source: Venture Economics22

Why is Entrepreneurship Important?

� Central to Growth and Job Creation– Small companies earn 50% of GDP

– Small companies provide 50% of jobs in the US

� Important for Knowledge Creation

– Young firms patent “groundbreaking” innovations

� Entrepreneurs have Higher Upward Mobility

23

Small Firms are Increasing in Importance in the Economy

5

6

88 89 92 93 94 97 98

0

50

100

150

200

250

300

i

90 91 95 96

US Small Business Firms 1988 - 1998

4.4

4.6

4.8

5.2

5.4

5.6

5.8

Year

in m

illi

on

$ i

n m

illi

on

# of Start-up F rms

Tax Revenues

Data Source: U.S. Census Bureau 24

But Uncertainty is High

Business Turnover 1990 - 1998

700000

600000

500000

400000

300000

200000

100000

0

Fi i i

i

rm Term nat on

Firm B rth

90 91 92 93 94 95 96 97 98

Year

Data Source: U.S. Census Bureau 25