14 feb-17 rdc investor-presentation - final

37

Rowan Strong: Safe. Reliable. Efficient. February 14, 2017 1

-

Upload

rowancompanies -

Category

Investor Relations

-

view

306 -

download

0

Transcript of 14 feb-17 rdc investor-presentation - final

Rowan Strong: Safe. Reliable. Efficient. February 14, 2017

1

Forward-Looking Statements

Statements herein that are not historical facts are forward looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, including, without limitation, statements as to the expectations, beliefs and future expected business, financial and operating performance and prospects of the Company. These forward-looking statements are based on our current expectations and are subject to certain risks, assumptions, trends and uncertainties that could cause actual results to differ materially from those indicated by the forward-looking statements.

Among the factors that could cause actual results to differ materially include oil and natural gas prices, the level of offshore expenditures by energy companies, variations in energy demand, changes in day rates, cancellation, early termination or renegotiation by our customers of drilling contracts, risks associated with fixed cost drilling operations, cost overruns or delays in transportation of drilling units, cost overruns or delays in maintenance and repairs, cost overruns or delays for conversion or upgrade projects, operating hazards and equipment failure, risks of collision and damage, casualty losses and limitations on insurance coverage, customer credit and risk of customer bankruptcy, conditions in the general economy and energy industry, weather conditions and severe weather in the Company’s operating areas, increasing complexity and costs of compliance with environmental and other laws and regulations, changes in tax laws and interpretations by taxing authorities, civil unrest and instability, terrorism, piracy and hostilities in our areas of operations that may result in loss or seizure of assets, the outcome of disputes and legal proceedings, effects of the change in our corporate structure, and other risks disclosed in the Company’s filings with the U.S. Securities and Exchange Commission.

Each forward-looking statement speaks only as of the date hereof, and the Company expressly disclaims any obligation to update or revise any forward-looking statements, except as required by law.

2

Company Overview & Investment Highlights

Market Dynamics

Delivering Value

Conclusion

Rowan has evolved into a pure play, high-specification offshore driller

4

COMPANY OVERVIEW & INVESTMENT HIGHLIGHTS MARKET DYNAMICS DELIVERING VALUE CONCLUSION

Rowan is well positioned to navigate the current challenging market and capitalize on investments to dramatically improve our return on capital

Rowan is well positioned to navigate the current challenging market and capitalize on investments to dramatically improve our return on capital

(1) Approximate value as of January 31, 2017 (2) Ultra-deepwater (UDW) refers to floating drilling rigs rated for water depths of 7,500 feet or greater (3) High-specification defined as rigs with a two million pound or greater hookload capacity

Company Overview

• RDC: NYSE-listed

• ~2,800 direct employees worldwide(1)

• 29 offshore drilling units

• 4 UDW(2) drillships

• 25 Jack-ups

• 19 High-Specification(3)

• 6 Premium

Investment Highlights

1

2

3

4

5

Groundbreaking partnership with Saudi Aramco ensures long-term growth

Competitive differentiation in drilling demanding wells

Modern high-specification fleet strategically positioned in global markets

Experienced and proven workforce & processes focused on performance

Backlog diversified among premium customer base, geographic regions, and asset types

Strong & flexible financial position 6

5

COMPANY OVERVIEW & INVESTMENT HIGHLIGHTS MARKET DYNAMICS DELIVERING VALUE CONCLUSION

Groundbreaking partnership with Saudi Aramco ensures long-term growth 1

6

COMPANY OVERVIEW & INVESTMENT HIGHLIGHTS MARKET DYNAMICS DELIVERING VALUE CONCLUSION

Groundbreaking partnership with Saudi Aramco ensures long-term growth

Global drilling experience,

best-in-class performance

and technical expertise

World Class

Drilling

Expertise

Acquire Saudi built rigs and

support the training and

development of a local

drilling workforce

Partnership

in Local

Development

Demand

Certainty

Through a long-term

relationship with Saudi Aramco

Scale &

Growth

Benefit from economies of

scale by providing Saudi

Aramco with a significant

portion of its rig requirements

Rowan Saudi Aramco

New Company

The new company benefits from the partners’ unique contributions

1

7

COMPANY OVERVIEW & INVESTMENT HIGHLIGHTS MARKET DYNAMICS DELIVERING VALUE CONCLUSION

Groundbreaking partnership with Saudi Aramco Key details (1 of 2)

Scope Rowan and Saudi Aramco will form a 50/50 joint venture to own and operate jack-up

drilling rigs in Saudi Arabia.

In 2017, Rowan contributes the Gilbert Rowe, the Bob Keller, and the J.P. Bussell, related inventory and local shorebase operations; Saudi Aramco contributes two rigs, related inventory and additional cash to make up the difference in value of asset contributions between the partners.

In late 2018, Rowan contributes the Hank Boswell and the Scooter Yeargain, as they complete their current contracts, and Saudi Aramco will contribute equivalent value.

The new company will manage Rowan’s existing rigs until current contracts expire, when the new company will lease the rigs from Rowan as needed.

Rig Contributions and Matching Contributions

Cash Capital Contributions

Both partners intend for the new company to be self and externally funded.

No additional equity injections are expected (although both Saudi Aramco and Rowan remain fully committed to the success of the new company).

Financials and Expected Returns

Both partners are committed to progressively implementing efficiencies and optimizing costs to improve profitability over time.

Expected returns are commensurate to Rowan’s target for similar risk profile opportunities.

1

8

COMPANY OVERVIEW & INVESTMENT HIGHLIGHTS MARKET DYNAMICS DELIVERING VALUE CONCLUSION

Newbuild Strategy

Management Rowan will nominate CEO and head of operations; Saudi Aramco will nominate Chairman and CFO.

Governance

Saudi Aramco and Rowan will each own 50%, with proportional voting rights and Board representation.

The new company will operate independently with a separate dedicated management team, ensuring an arm’s length relationship.

The new company plans to order up to 20 rigs to be delivered over ten years beginning as early as 2021 to meet base load offshore drilling demand in the Kingdom.

Rig purchases will be supported by contracts from Saudi Aramco as customer, at defined returns commensurate to similar risk profile opportunities.

Groundbreaking partnership with Saudi Aramco Key details (2 of 2) 1

9

COMPANY OVERVIEW & INVESTMENT HIGHLIGHTS MARKET DYNAMICS DELIVERING VALUE CONCLUSION

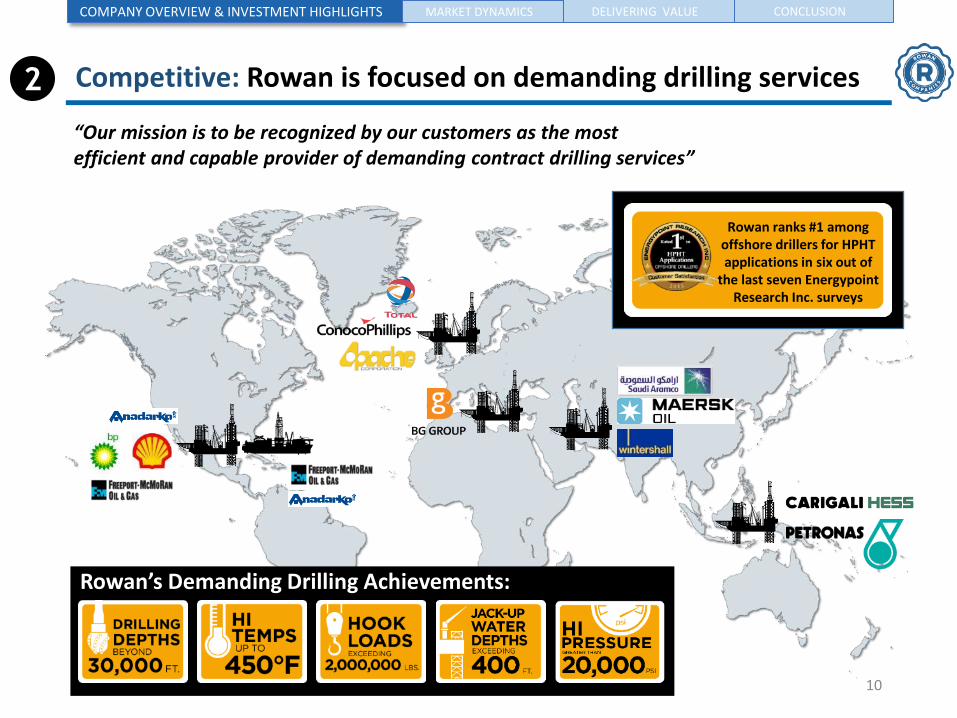

Competitive: Rowan is focused on demanding drilling services

“Our mission is to be recognized by our customers as the most efficient and capable provider of demanding contract drilling services”

Rowan ranks #1 among offshore drillers for HPHT applications in six out of

the last seven Energypoint Research Inc. surveys

Rowan’s Demanding Drilling Achievements:

2

10

COMPANY OVERVIEW & INVESTMENT HIGHLIGHTS MARKET DYNAMICS DELIVERING VALUE CONCLUSION

Global: Rowan’s fleet is strategically positioned in key markets

• HP/HT Deep Gas

• Key location for demanding UDW

US Gulf of Mexico 2 JU; 4 UDW

• Demanding environmental

conditions

Central & South America 3 JU

• Harsh environment HP/HT market

• Super Gorilla / N-Class well suited

North Sea 6 JU

• Most active jack-up region

in the world

Middle East 13 JU

Featuring:

4 UDW

Drillships

19 High-Spec

Jack-ups

4*

Premium

Jack-ups

* Gorilla II and Gorilla III were sold in 2016; excludes two cold stacked older rigs (Cecil Provine and Rowan California)

COMPANY OVERVIEW & INVESTMENT HIGHLIGHTS MARKET DYNAMICS DELIVERING VALUE CONCLUSION

3

11

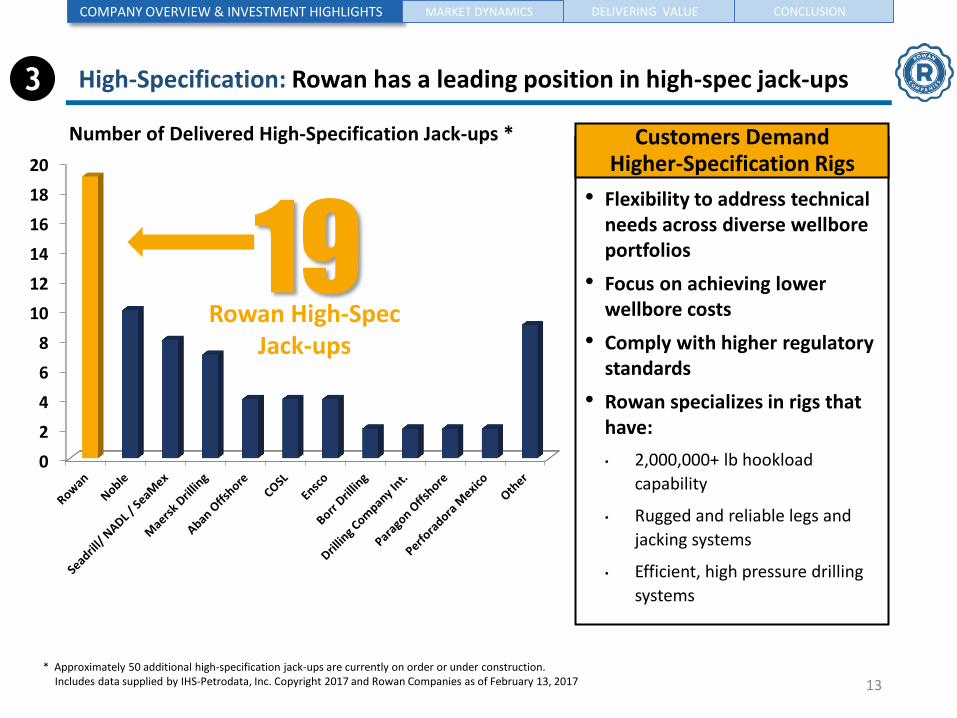

High-Specification: Rowan has a leading position in high-spec jack-ups

COMPANY OVERVIEW & INVESTMENT HIGHLIGHTS MARKET DYNAMICS DELIVERING VALUE CONCLUSION

3

12

0

2

4

6

8

10

12

14

16

18

20

19 Rowan High-Spec

Jack-ups

Customers Demand Higher-Specification Rigs

• Flexibility to address technical needs across diverse wellbore portfolios

• Focus on achieving lower wellbore costs

• Comply with higher regulatory standards

• Rowan specializes in rigs that have:

• 2,000,000+ lb hookload

capability

• Rugged and reliable legs and

jacking systems

• Efficient, high pressure drilling

systems

Number of Delivered High-Specification Jack-ups *

* Approximately 50 additional high-specification jack-ups are currently on order or under construction. Includes data supplied by IHS-Petrodata, Inc. Copyright 2017 and Rowan Companies as of February 13, 2017

High-Specification: Rowan has a leading position in high-spec jack-ups 3

13

COMPANY OVERVIEW & INVESTMENT HIGHLIGHTS MARKET DYNAMICS DELIVERING VALUE CONCLUSION

High-Specification: Rowan’s ultra-deepwater drillships are best-in-class 3

14

COMPANY OVERVIEW & INVESTMENT HIGHLIGHTS MARKET DYNAMICS DELIVERING VALUE CONCLUSION

Best-in-Class Specifications:

• 1,250 ton hookload

• Dual 7-ram blowout preventers

• Managed Pressure Drilling capable

• Advanced Riser Gas Handling

• 12,000 ft water depth equipped

• IMO Tier III emissions compliance

Few rigs possess the specifications required for today’s demanding wells and tightening regulations

13

105

16 32

166

1,250 tons Dual BOP

1,250 tons Single BOP

1,000 tons 750 tons All UDW

Under 20% of UDW Rigs*

High-Specification: Rowan’s ultra-deepwater drillships are best-in-class 3

15

14 each 1,250 ton dual stack 40 cold stacked – 9 x 750 27 x 1000 4 x 1250 (1 is dual BOP) * Includes data supplied by IHS-Petrodata, Inc; Copyright 2017; Rowan estimate, excludes eighteen 1,000-ton and twenty-two 1,250-ton newbuilds; as of January 4, 2016.

COMPANY OVERVIEW & INVESTMENT HIGHLIGHTS MARKET DYNAMICS DELIVERING VALUE CONCLUSION

94-year history of operating excellence

Culture of continuous improvement

Experienced employees with proven industry leadership

Strong commitment to performance ̶ delivering safe, reliable and efficient operations for our customers

4 Proven: Rowan has an experienced workforce and established processes

16

COMPANY OVERVIEW & INVESTMENT HIGHLIGHTS MARKET DYNAMICS DELIVERING VALUE CONCLUSION

Backlog Diversified: Rowan has solid backlog with diversity of customers, geographic regions, and asset types 5

Total backlog of $1.7B* that extends to 2024

* Backlog as of February 14, 2017; does not reflect the impact from joint venture anticipated to commence operations in 2Q 2017

52%

30%

11% 5%

1% 1%

Middle East Deepwater Norway Trinidad UK US GOM

Majors / Independents 46%

NOCs 54%

Over 85% of backlog is with NOCs or investment grade customers

Contract Backlog by Region & Asset Type

Contract Backlog by Customer Type

Rowan has key competitive advantages in adding new backlog: • Solid track record as a capable and

efficient driller of demanding wells • Modern, high-specification fleet • Deep customer relationships • Strong financial counterparty to

customers

17

COMPANY OVERVIEW & INVESTMENT HIGHLIGHTS MARKET DYNAMICS DELIVERING VALUE CONCLUSION

$60 $150 $1,289

$0

$209

$657

$398

$500

$400 $400

$0

$250

$500

$750

$1,000

$1,250

$1,500

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2042 2043 2044

USD

Mill

ion

s

Revolver Due

Purchased via Tender**

Purchased in Open Market

Current Bond Debt

6 Strong Financial Position: Our robust balance sheet and highly visible runway bolster our financial health through the cycle

• Strong balance sheet provides the ability to invest counter-cyclically to significantly improve our return on capital

• Retired ~$740 million of debt since 4Q 2015, while issuing $500 million of unsecured debt not due until 2025

• Attractive debt maturity profile with significant untapped borrowing capacity available from $1.5B revolver*

• Current cash balance combined with our untapped revolver exceeds our total outstanding debt

*As of February 13, 2017; availability under the facility is $1.5 billion through January 23, 2019, declining to $1.44 billion through January 23, 2020, and to

approximately $1.29 billion through the maturity in 2021. All debt is unsecured.

**Following the tender offer, the remaining ~$92 million of the 2017 bonds were retired on February 8, 2017

18

7.875% 4.875% 4.750% 7.375% 5.400% 5.850%

COMPANY OVERVIEW & INVESTMENT HIGHLIGHTS MARKET DYNAMICS DELIVERING VALUE CONCLUSION

Company Overview & Investment Highlights

Market Dynamics

Delivering Value

Conclusion

Supported by higher oil prices, global drilling & completions spending is forecast to be up slightly in 2017, but favors onshore in the near term

Independents and national oil companies (majority of land & jack-up demand) are forecast to increase their spending in 2017, with majors (significant source of floater demand) expected to delay incremental offshore spending until cash flows accumulate above their dividend expense

NAM Onshore Offshore & Int’l Onshore Global Overall

Drilling & Completion Budget Forecasts*

* Source: Wells Fargo Securities, January 11, 2017

COMPANY OVERVIEW & INVESTMENT HIGHLIGHTS MARKET DYNAMICS DELIVERING VALUE CONCLUSION

2017 est. +7% 2017 est. +55% 2017 est. -9%

Floaters: Throughout the market cycles, higher specification drilling units provide higher levels of utilization

40

60

80

100

<5,000' 5,000'-7,499' 7,500'+ / <1,250 tons 7,500'+ / 1,250+ tons

%

Includes data supplied by IHS-Petrodata, Inc; Copyright 2017, as of February 13, 2017

Worldwide Floater Total Utilization by Water Depth / Hookload

61 units

103 units

83 units 36 units

21

COMPANY OVERVIEW & INVESTMENT HIGHLIGHTS MARKET DYNAMICS DELIVERING VALUE CONCLUSION

* Includes data supplied by IHS-Petrodata, Inc., Copyright 2017; and Rowan Analysis; as of January 4, 2017

50

192

94

0

50

100

150

200

250

300

350

Projected Future

Supply Range

190 - 240

Potential Newbuild

Cancellations

Cold Stacked Post 1996

Contracted Pre-1996

Stacked Pre 1996

Total Current Supply

336

Potential Floater Supply Attrition ?

Roll-off of Contracted Floater Fleet

Floaters Under Construction

Fleet Post-1996 Floaters

Fleet Pre-1996 Floaters

0

50

100

150

200

250

YE’

25

YE’

24

YE’

23

YE’

22

YE’

21

YE0

7

YE0

6

YE’

16

YE1

5

YE1

4

YE1

3

YE’

20

YE’

19

YE’

18

YE’

17

YE1

2

YE1

1

YE1

0

YE0

9

YE0

8

• 2017 brings a dramatic increase in roll-offs of contracts signed in the 2011 to 2014 up cycle

• 28% of all floaters are older than 20 years; they currently represent 24% of working floaters

• New contracts will favor modern rigs; older rigs will be much less competitive, unless they have a “niche”

22

Fleet Pre 1996 - Existing Contracts

Fleet Post 1996 - Existing Contracts

Contracted Rig Demand (Estimated)

Contracted Rig Demand (Actual)

A Floaters: In 2017, there is a substantial roll off of the current floater contracts; we believe this will force attrition of remaining older rigs

COMPANY OVERVIEW & INVESTMENT HIGHLIGHTS MARKET DYNAMICS DELIVERING VALUE CONCLUSION

Jack-ups: Throughout the market cycles, newer higher specification drilling units provide higher levels of utilization

* Jack-ups with two million pound or greater hookload

Includes data supplied by IHS-Petrodata, Inc; Copyright 2017 as of February 13, 2017

64 units 117 units

147 units 139 units

20

40

60

80

100

IS, MS, MC <300'IC 300'IC 350'+ IC High Spec*

%

Worldwide Jack-up Total Utilization by Rig Class

55 units

23

COMPANY OVERVIEW & INVESTMENT HIGHLIGHTS MARKET DYNAMICS DELIVERING VALUE CONCLUSION

Jack-ups: In 2017 there is a substantial roll off of the current jack-up contracts; we believe this will force attrition of older rigs

• 2017 brings a dramatic increase in roll-offs of contracts signed in the 2011 to 2014 up cycle

• 39% of all JUs are older than 20 years; they currently represent 45% of working JUs

• Fewer niches for older rigs to “hide” than in floater market

• Many newbuilds will require a change of ownership before they can be marketed effectively

24

COMPANY OVERVIEW & INVESTMENT HIGHLIGHTS MARKET DYNAMICS DELIVERING VALUE CONCLUSION

104

254

233

0

100

200

300

400

500

600

Projected Future

Supply Range

350 - 425

Potential Newbuild

Cancellations

Cold Stacked Post 1996

Contracted Pre 1996

Stacked Pre 1996

Total Current Supply

591

Roll-off of Contracted Jack-up Fleet

JUs Under Construction

Post-1996 Jus

Pre-1996 JUs

0

50

100

150

200

250

300

350

400

YE’

25

YE’

24

YE’

23

YE’

22

YE’

21

YE’

20

YE’

19

YE’

18

YE’

17

YE’

16

YE1

5

YE1

4

YE1

3

YE1

2

YE1

1

YE1

0

YE0

9

YE0

8

YE0

7

YE0

6

Contracted Rig Demand (Actual)

Pre 1996 JUs - Existing Contracts

Post 1996 JUs - Existing Contracts

Contracted Rig Demand (Estimated)

* Includes data supplied by IHS-Petrodata, Inc., Copyright 2017; and Rowan Analysis; as of January 4, 2017

Company Overview & Investment Highlights

Market Dynamics

Delivering Value

Conclusion

Rowan has three company priorities to deliver value

Our customers want: • Safe, reliable & efficient

operations • Procedural discipline and

management of operational risk • Solid counterparties

Our investors want: • Thoughtful capital allocation to

drive strong returns • Exposure to a driller with a

sustainable capital structure

Our employees want: • To be part of a winning team • Some stability in a rough market • A company willing to develop and

challenge them

26

COMPANY OVERVIEW & INVESTMENT HIGHLIGHTS MARKET DYNAMICS DELIVERING VALUE CONCLUSION

We are focused on improving Rowan’s return on invested capital

The improvements we are making now will deliver results in the short and long run

Control spend and focus on capital allocation • Reduce drilling expense by improving procurement effectiveness: centralize and optimize

all spend • Strong inventory control through rigorous data analytics • Implementing a fleet-wide state-of-the-art maintenance system for improved reliability

and to optimize maintenance spending

Much of our cost is personnel-related • Preserve key talent through high-grading of onshore and offshore workforce; use of an

aggressive bump back strategy to preserve our talent in this downturn • Reduce overhead costs (SG&A and a portion of drilling expense) by improving the

efficiency and cost of business support functions

Proactively address organizational health to counter negative aspects of the downturn • Visible Leadership; lead from the front on cost cutting with pay cuts of executives • Continuously assess Organizational Health; continue to develop future leaders • Create Targeted Initiatives to improve alignment, execution, and renewal of key business

processes. Engage employees in these improvement initiatives.

27

COMPANY OVERVIEW & INVESTMENT HIGHLIGHTS MARKET DYNAMICS DELIVERING VALUE CONCLUSION

Rowan has an unrelenting focus on improving long-term return on invested capital

Rowan will consider all capital allocation options, but remains committed to maintaining an attractive credit profile and financial flexibility. During the current challenging business environment, we favor:

Increased Liquidity 3Q2016 – Generated $276 million of cash

during the quarter and currently have a balance in excess of $1.1 billion

Debt Reduction Retired ~$740 million of debt since 4Q 2015,

while issuing $500 million of unsecured debt not due until 2025

Opportunistic Asset Investments We continue to evaluate opportunistic

investments in assets Investments at attractive prices in the bottom

of the cycle should generate superior returns

Available

Capital

Allocation

Options

Preserve Liquidity

Dividends/ Share Repurchases

Asset Investments

Retire Debt

28

COMPANY OVERVIEW & INVESTMENT HIGHLIGHTS MARKET DYNAMICS DELIVERING VALUE CONCLUSION

Considerable improvement in operational performance and EBITDA margins over the last three years

$ in millions

Operational Performance has improved while costs have been reduced

From initial 2015 guidance issued in November 2014 – Current*: • 38 % reduction of TRIR

(Total Recordable Incident Rate)

• Downtime held essentially flat while delivering our final two drillships

280

135

1,145

95

650

-64%

-29%

-43%

Non-newbuild Capex

<100

SG&A Drilling Expense

Midpoint of Current Guidance for 2017

Midpoint of Initial Guidance for 2015

USD

mill

ion

s

* As of November 28, 2016; some portion of Drilling Expense reduction is due to the formation of the new drilling company with Saudi Aramco

29

COMPANY OVERVIEW & INVESTMENT HIGHLIGHTS MARKET DYNAMICS DELIVERING VALUE CONCLUSION

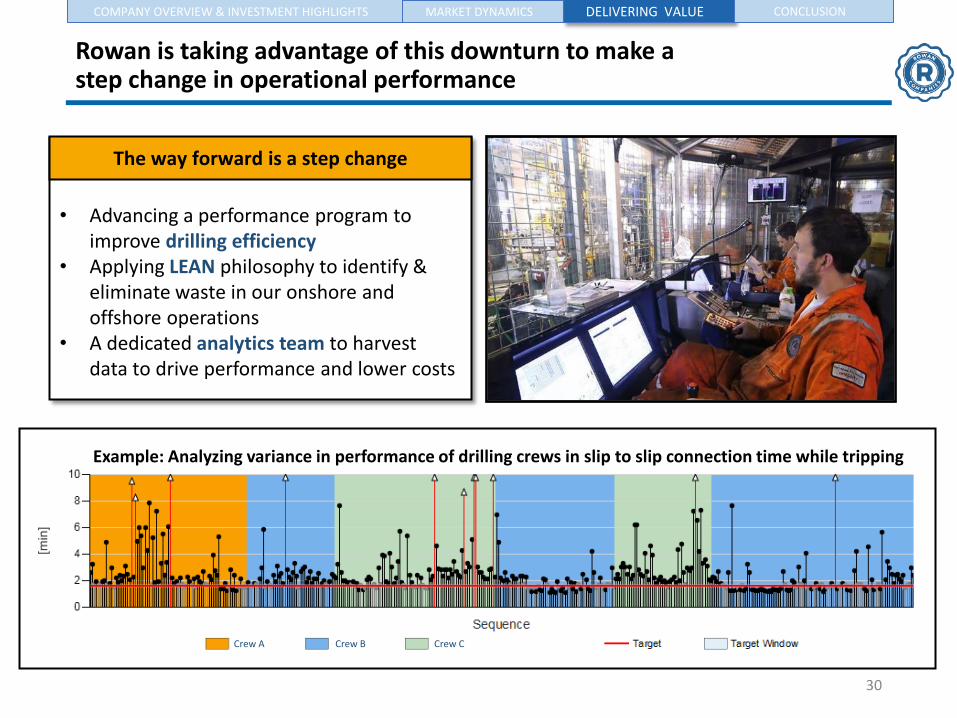

Rowan is taking advantage of this downturn to make a step change in operational performance

Continuously Improving Performance The way forward is a step change

• Advancing a performance program to improve drilling efficiency

• Applying LEAN philosophy to identify & eliminate waste in our onshore and offshore operations

• A dedicated analytics team to harvest data to drive performance and lower costs

Crew A Crew B Crew C Crew D

Example: Analyzing variance in performance of drilling crews in slip to slip connection time while tripping

30

COMPANY OVERVIEW & INVESTMENT HIGHLIGHTS MARKET DYNAMICS DELIVERING VALUE CONCLUSION

Company Overview & Investment Highlights

Market Dynamics

Delivering Value

Conclusion

Rowan is positioned to endure this challenging market and emerge a stronger company

Investment Highlights

1

2

3

4

5

Groundbreaking partnership with Saudi Aramco ensures long-term growth

Competitive differentiation in drilling demanding wells

Modern high-specification fleet strategically positioned in global markets

Experienced and proven workforce & processes focused on performance

Backlog diversified among premium customer base, geographic regions, and asset types

Strong & flexible financial position 6

32

COMPANY OVERVIEW & INVESTMENT HIGHLIGHTS MARKET DYNAMICS DELIVERING VALUE CONCLUSION

Appendix

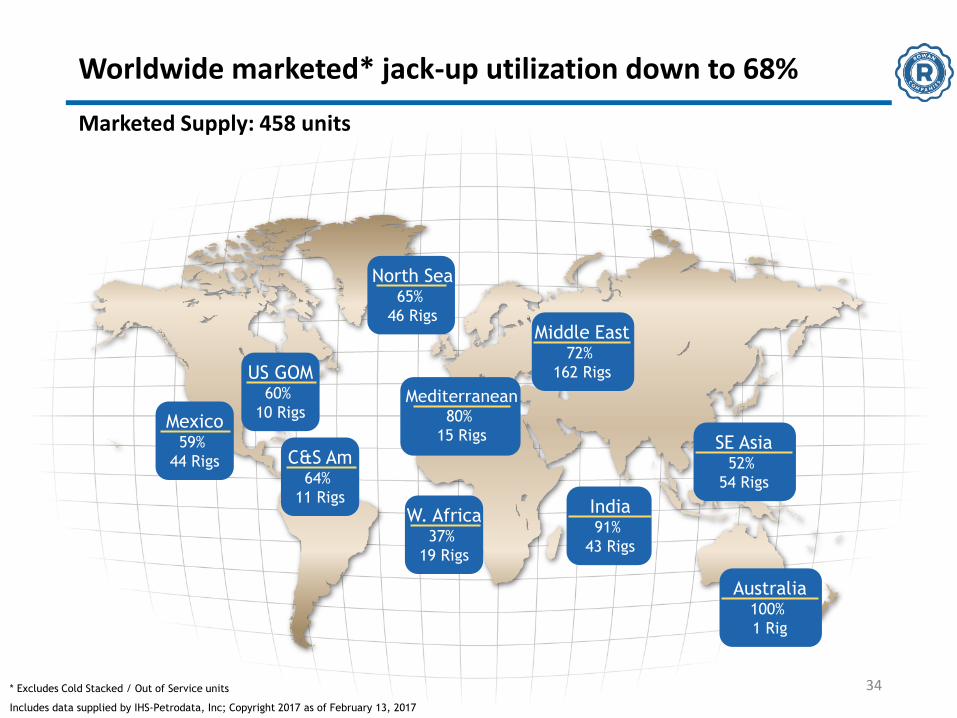

Worldwide marketed* jack-up utilization down to 68%

* Excludes Cold Stacked / Out of Service units

Includes data supplied by IHS-Petrodata, Inc; Copyright 2017 as of February 13, 2017

Marketed Supply: 458 units

US GOM 60%

10 Rigs Mexico

59%

44 Rigs C&S Am 64%

11 Rigs

W. Africa 37%

19 Rigs

North Sea 65%

46 Rigs Middle East

72%

162 Rigs

India 91%

43 Rigs

SE Asia 52%

54 Rigs

Australia 100%

1 Rig

Mediterranean 80%

15 Rigs

34

0%

1 Rig

Worldwide marketed* UDW** utilization has dropped to 71% Marketed Supply: 129 units

*Excludes Cold Stacked / Out of Service units

**UDW includes semis and drillships with a rated water depth of 7500’+

Includes data supplied by IHS-Petrodata, Inc; Copyright 2017 as of February 13, 2017

Far East 25%

4 Rigs

W. Africa 58%

31 Rigs

C&S Am 87%

31 Rigs

Mexico 75%

4 Rigs

USA 72%

36 Rigs

E. Canada 100%

1 Rigs

North Sea 86%

7 Rigs

Mediterranean 80%

5 Rigs SE Asia 60%

10 Rigs

35

APPENDIX

Rowan guidance as of November 28, 2016

Key metrics: FY 2015

Actual

3Q 2016

Actual

4Q 2016

Projected

FY 2016

Projected

FY 2017

Projected

Jack-up Operational

Downtime

(unbillable)

~1% Less than 2% ~2.5% <2% ~2.5%

Drillship Operational

Downtime (1) ~7% 0% ~5% < or ~1% ~5%

Contract Drilling Expenses

(excluding rebills) $950 MM $182 MM ~$190 MM ~$775

$600 - $700 MM(2)

SG&A $116 MM $24 MM ~$26 MM Slightly below

$105MM $90 - $100 MM

Depreciation $391 MM $102 MM Not Guided Slightly above

$400 MM $385 - $395MM

Interest Expense,

Net of Capitalized Interest $145 MM $39 MM Not Guided ~$155 MM $145 - $150MM

Effective Tax Rate

(normalized)

~11% Normalized

9.5% Not Guided Low to Mid Single Digits

Not Guided

Capital Expenditures $723 MM $24 MM Not Guided $125 - $130 MM(2) <$100 MM(2)

(1) Rowan expects operational downtime for the drillships to be approximately 5%.

(2) Rowan expects to incur full-year 2017 drilling expense of between $600 MM and $700 MM, depending upon whether certain idle rigs secure additional work.

(3) Rowan expects 2016 maintenance capital expenditures to range from $125 - $130MM and 2017 to be less than $100 MM, excluding any contractual modifications that

may arise due to securing additional work, none of which is currently planned. 36

Investor Contacts:

Chris Pitre VP, Investor Relations and Corporate Development [email protected] +1 713 968 6642 Carrie Prati Manager, Marketing and Investor Relations [email protected] +1 713 960 7581

37