13

38

Copyright © 2000 by Harcourt, Inc. All rights reserved. 13-1 Chapter 13 Managing Nonbanks: Finance Companies, Financial Services Conglomerates, and Merger Consolidation

Transcript of 13

Copyright © 2000 by Harcourt, Inc. All rights reserved.

13-1

Chapter 13Managing Nonbanks: Finance Companies,

Financial Services Conglomerates, and Merger Consolidation

Copyright © 2000 by Harcourt, Inc. All rights reserved.

13-2

Finance Companies

They are like banks in that they make different types of loans.

They are unlike banks in that they do not have deposits as a source of funds.

They obtain funding to finance lending activities by:

• issuing commercial paper or bonds; and

• borrowing from financial institutions.

Copyright © 2000 by Harcourt, Inc. All rights reserved.

13-3

Consumer Finance Companies

Many are captive companies or sales companies, subsidiaries of large manufacturing firms, and provide financing to consumers for the firm’s product.

They are subject to state and federal laws governing the provision of credit.

They make both unsecured and secured loans.

Copyright © 2000 by Harcourt, Inc. All rights reserved.

13-4

Commercial Finance Companies

They make business loans, equipment leasing, asset-based loans and factoring.

They often sell participation in an asset-based loan to banks in exchange for cash. • Proceeds from the loan are divided between the

finance company and the bank according to their relative shares in the loan.

• Often, because bank lending rates are lower than finance company rates, the borrower is given a “blended” rate reflecting the relative shares of the two lenders.

Copyright © 2000 by Harcourt, Inc. All rights reserved.

13-5

Diversified Finance Companies and Credit Card Companies

Diversified companies make both consumer and business loans.

Credit card companies issue credit cards to consumers and businesses and make significant fee income from selling and securitizing credit card loans. They continue to earn fee income by servicing these loans. • Securitization is important to finance companies

because it provides liquidity, lower cost financing, and fee income.

Copyright © 2000 by Harcourt, Inc. All rights reserved.

13-6

Government Sponsored Enterprises (GSE) and Mortgage Banks

They originate loans and sell or securitize these loans, receiving a profit.

• In 1998, 53% of all home mortgages, 28% of consumer loans, and 15% of commercial real estate loans were in securitized pools.

They also receive income from servicing loans.

Copyright © 2000 by Harcourt, Inc. All rights reserved.

13-7

Unlike banks, mortgage banks originate loans with the intent to sell or securitize them right away. By doing so they avoid:

• liquidity problems; and

• funding gap problems.

Mortgage banks face potential capital losses with adverse movements in interest rates.

Mortgage bank profits are subject to the cycles in home buying and the real estate market.

Copyright © 2000 by Harcourt, Inc. All rights reserved.

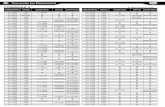

13-8Trends in Average U.S Finance Company Assets and Liabilities, Year-End

1991, and 3rd Quarter, 1998 (% Total)

Consumer 21.72%27.25%

Business 52.12 35.77Real Estate 11.72 10.51

Less Reserves for Unearned and Losses 12.12 7.00

Net Receivables 73.44 66.53Other Assets 26.55 33.48

Total Assets 100.0%100.0%

Receivables 1991

3rd Quarter

1998 Liabilities 1991

3rd Quarter

1998

Liabilities and Capital

Bank Loans 7.54% 2.66%

Commercial Paper 28.40 24.20

Debt:Owed to Parent 6.14 6.22Not Elsewhere

Classified 34.09 36.05All other Liab. 12.30 19.79Equity 11.53 11.06

Total Liab. & Capital 100.0%100.0%

Assets

Source: Information from the Federal Reserve Bulletin 79 (Jan. 1993), A35 and 85 (March 1999), A33.

Copyright © 2000 by Harcourt, Inc. All rights reserved.

13-9

The finance company industry is highly concentrated with the largest 20 firms controlling 71% of the nondepository finance company assets of $900b.

Large firms rely more heavily on CP for financing and are more highly leveraged.

Small companies rely on equity for almost half of their financing because they have limited access to the money and capital markets.

Copyright © 2000 by Harcourt, Inc. All rights reserved.

13-10

Finance companies need more equity capital since they don’t have deposit insurance and often have customers with higher risk profiles than do depository institutions.

Copyright © 2000 by Harcourt, Inc. All rights reserved.

13-11

Finance Company Profitability

The high interest rate environment of 1980-1981 resulted in increased interest cost for finance companies and reduced their ROA and ROE.

• For 1981 ROA was 1.0 and ROE was 8.6.

• For 1989 ROA was 1.3 and ROE was 13.7

Copyright © 2000 by Harcourt, Inc. All rights reserved.

13-12

After 1982, finance companies reported higher ROE than commercial banks. Contributing factors included:

• increased use of financial leverage by finance companies; and

• no default risk exposure to agricultural, energy and international lending.

The corporate scorecard of Business Week in March 1999 suggests that large finance companies continue to have higher ROE than commercial banks and other financial institutions.

Copyright © 2000 by Harcourt, Inc. All rights reserved.

13-13

Regulation for Finance Companies

They are regulated almost entirely at the state level.

They are subject to federal and state regulations on consumer, commercial and mortgage credit and the Uniform Commercial Code.

Copyright © 2000 by Harcourt, Inc. All rights reserved.

13-14

Low usury ceilings at the state level discourage finance companies from lending in those states.

• Low ceilings make it difficult to offer higher rates to cover costs and potential high loan losses.

More lenient bankruptcy laws have encouraged finance companies to diversify away from unsecured consumer lending into mortgage lending for protection.

Copyright © 2000 by Harcourt, Inc. All rights reserved.

13-15

Performance Measures

Liquidity Ratios

• Cash/Short-Term Debt

• Receivables Maturing in 12 Months/Total Receivables

• Unsecured Credit Lines/Open Market Debt

Credit Risk

• Direct Cash Loans/Gross Receivables

• Net charge-off/Average Net Receivables

Copyright © 2000 by Harcourt, Inc. All rights reserved.

13-16

Leverage Ratios

• Total Debt/Net Worth

• Interest Expense/Average Net Receivables

Efficiency/Productivity Ratios

• Operating Expenses(Exclusive of Loan Loss Expense)/Average Net Receivables

• Average Monthly Principal Collections/Average Net Monthly Receivables

• Annual Gross Finance Revenues/Average Net Receivables

Copyright © 2000 by Harcourt, Inc. All rights reserved.

13-17

Profitability Ratios

• Net Finance Profit/Average Net Receivables

• Net Interest Margin = (Gross Finance Revenue - Interest Expense)/Average Net Receivables

• Return on Net Worth =Net Income/Average Net Worth

Copyright © 2000 by Harcourt, Inc. All rights reserved.

13-18

1998 Events that Radically Changed the Financial Environment for Financial

Institutions

Citicorp-Travelers merger

• Forced Congress to deal with the issue of allowing insurance-securities-banking activities to be conducted together.

The OTS’s widespread approval of new unitary holding companies

• Opened the banking-commerce debate.

Copyright © 2000 by Harcourt, Inc. All rights reserved.

13-19

BankAmerica-NationsBank and other mega-bank mergers and acquisitions of securities firms by commercial banks

A contraction in net interest margins for banks favoring banks with greater sources of noninterest income

The emergence of the Internet

• Allows financial services to be carried out in Web space

Copyright © 2000 by Harcourt, Inc. All rights reserved.

13-20

Reasons for the Emergence of Financial Conglomerates

Firms can smooth their earnings by receiving interest and noninterest income from a variety of sources.

Smoother earnings allow firms to have greater debt capacity and lower overall cost of funds.

Firms can achieve operating synergies including economies of scale and scope and more productive resource utilization.

Copyright © 2000 by Harcourt, Inc. All rights reserved.

13-21

Firms in maturing industries, such as banking and insurance, can diversify for long-term survival and greater profitability and growth.

Managers can reduce unemployment risk by smoothing earnings or achieving greater ego satisfaction or compensation, if management compensation is related to growth.

By applying management competencies, firms can improve the efficiency of inefficient firms in a related industry.

Copyright © 2000 by Harcourt, Inc. All rights reserved.

13-22

Practical Considerations for the Development of Financial Conglomerates

The cost of entering different aspects of the financial services industry can be low, because a major investment in capital may not be needed, particularly for firms in the information or retail business.

Financial products have commodity-like characteristics which make products substitutable.

Copyright © 2000 by Harcourt, Inc. All rights reserved.

13-23

Many firms have entered new types of financial services business because they perceive it to be more profitable than their primary lines of business.

Some believe that the earnings of a diversified firm will exceed those of two or more firms operating separately and/or reduce the volatility of earnings of the two individual firms.

Copyright © 2000 by Harcourt, Inc. All rights reserved.

13-24

Trends in Financial Services Conglomerates

1970’s and 1980’s are characterized by a merger wave and the emergence of financial conglomerates.

1990’s is characterized as a time of restructuring through divestiture and spin-offs. Reasons for restructuring include:• problems blending cultures;• failure of the stock market to reflect the full value of

individual businesses; and• the need to refocus on a firm’s central lines of

business.

Copyright © 2000 by Harcourt, Inc. All rights reserved.

13-25

Sears Financial Conglomerate

Allstate Insurance

• Spun-off in 1994. Coldwell Banker

• Sold. Dean Witter/Discover

• Discover was highly successful.

• Dean Witter was not a successful acquisition.

• Sold to Morgan Stanley in 1997. Also acquired a mortgage company and a S&L.

Copyright © 2000 by Harcourt, Inc. All rights reserved.

13-26

GE’s Financial Conglomerate

GEFS is a highly successful global diversified financial services firm with operations in 17 different businesses.

Services include:

• captive consumer finance company;

• leasing and equipment sales financing;

• accounts receivable financing;

• factoring commercial finance business; and

• property and casualty and reinsurance.

Copyright © 2000 by Harcourt, Inc. All rights reserved.

13-27

Kidder Peabody

• An investment banking and securities firm

• Unsuccessful venture

• Unable to mesh the different cultures

• Sold to PaineWebber in 1994

Copyright © 2000 by Harcourt, Inc. All rights reserved.

13-28

Merrill Lynch

Introduced bank-like services in 1977 with the Cash Management Accounts (CMAs).

Has mutual funds and asset management subsidiaries.

Offers CDs, Visa cards, and consumer loans through two nonbank banks.

Offers personal trust services through a trust company.

Copyright © 2000 by Harcourt, Inc. All rights reserved.

13-29

Through the acquisition of Paribus Becker in 1984 it enhanced its investment banking business.

• Acquisition was highly successful.

Engages in international banking through international banking subsidiaries.

Entered small business lending arena.

Copyright © 2000 by Harcourt, Inc. All rights reserved.

13-30

Prudential Insurance Company

In 1981 purchased Bache Group, a securities firm.

• Bache suffered large losses in 1984 and 1987.

• Low employee pay relative to competitors resulted in low productivity.

• Parent company had to inject equity capital into Bache in 1990.

• Rocked by a class action lawsuit in 1991.

• Discontinued most investment banking activities in 1992.

Copyright © 2000 by Harcourt, Inc. All rights reserved.

13-31

Prudential Asset Management Group offers investment operations, products, and services to commercial customers.

Prudential Bank and Trust, a limited service bank, offers services to individuals.

The insurance unit has suffered losses as a result of class action lawsuits.

Also owned but later divested itself of a mortgage company, a reinsurer, and billions of dollars worth of real estate.

Copyright © 2000 by Harcourt, Inc. All rights reserved.

13-32

The Rationale for the Financial Megaplayers in the 20th Century

The high valuation of financial services companies makes it cheaper to use stock to acquire another company.

There is enormous potential for efficiency improvements with consolidation and the ability to enter new markets and geographical regions.

Copyright © 2000 by Harcourt, Inc. All rights reserved.

13-33

Firms can have excess capital to do acquisitions.

With mergers across industry lines, new fee income can be gained from cross-selling of products.

Although the size of new mega-financial firms makes these new firms more complex and less nimble, the cost-benefits balances favors strong, skilled players.

Copyright © 2000 by Harcourt, Inc. All rights reserved.

13-34

Pricing and Earnings Dilution with Mergers

Pricing benchmarks include:

• market-to-book ratio; and

• P/E ratio. The premium percentage paid over book

value is given by

1ValueBook

PriceMarket

Copyright © 2000 by Harcourt, Inc. All rights reserved.

13-35

In a stock swap, the exchange ratio is given by

EPS dilution is given by

Market Price Per Share of the TargetMarket Price Per Share of the Acquirer

EPS of the acquirer - Expected EPS with consolidationEPS of the acquirer

Copyright © 2000 by Harcourt, Inc. All rights reserved.

13-36

Assume a target has earnings of $500,000, the typical P/E ratio for similar targets is 3, the target’s book value of equity is $750,000 and the typical market-to-book ratio is 2.

The starting valuation for the target using the P/E ratio would be

3 × $500,000 = $1,500,000The starting valuation for the target using the

Market-to-Book would be

2 × $750,000 = $1,500,00

Copyright © 2000 by Harcourt, Inc. All rights reserved.

13-37

The premium paid would be:

($1,500,000 ÷ $750,000) - 1 = 1 or 100%

The higher the premium paid, the more difficult it will be for the acquirer to earn a return on the investment to justify the purchase price and the risk involved with the acquisition.

If the target has 100,000 shares outstanding, its market price per share would be $15. Assuming the acquirer has a market price per share of $15, the exchange ratio in a stock swap would be 1.

Copyright © 2000 by Harcourt, Inc. All rights reserved.

13-38

If the acquirer has an expected EPS of $10 and the expected EPS with the consolidation is $8, the earnings dilution would be

($10 -$8) ÷ $10 = .20 or 20%

EPS dilution should not be greater than 5% to get a reasonable return on the acquisition.