130807 Automotriz Esp

44

The Automotive Industry Business Intelligence Unit

-

Upload

eduardo-gq -

Category

Documents

-

view

48 -

download

1

Transcript of 130807 Automotriz Esp

The Automotive Industry

Business Intelligence Unit

Research and Analysis: Alejandro Pulido Morán

Design and Layout: Gibran Quiroga

© 2013, ProMexico

Camino a Santa Teresa No.1679

Col. Jardines del Pedregal

Del. Álvaro Obregón,

01900, Mexico D.F.

First edition (not for commercial sale)

Mexico City, June 2013

No part of this publication, including the cover

design, may be reproduced, stored or transmitted

in any fashion or by any media without express

written consent from ProMexico.

ProMexico is not responsible for any errors or

inaccuracies in the information contained herein

resulting from updates after the publication date.

Contents

1. Introduction .................................................................................................................................................. 21.1 Objective ............................................................................................................................................................................................ 21.2 What’s New ....................................................................................................................................................................................... 22. Industry Overview ........................................................................................................................................ 42.1 Segmentation .................................................................................................................................................................................... 42.1 Global Key Indicators for 2012 ....................................................................................................................................................... 52.2 Mexican Key Indicators 2012 ......................................................................................................................................................... 53. Global Outlook ............................................................................................................................................ 73.1Production ........................................................................................................................................................................................... 73.1.1 Light vehicles .......................................................................................................................................... 73.1.2 Heavy vehicles ......................................................................................................................................... 73.2 Consumption ..................................................................................................................................................................................... 73.3 Geographic Segmentation ............................................................................................................................................................... 83.4 Industry Trends ................................................................................................................................................................................. 83.4.1 Strategic alliances .................................................................................................................................... 83.4.2 Major Role of Emerging Countries ......................................................................................................... 83.4.3 Eco-friendly vehicles ............................................................................................................................... 93.4.4 International presence of assemblers ........................................................................................................ 93.5 Leading World Companies ...........................................................................................................................................................104. The Industry in Mexico ............................................................................................................................... 144.1 Production ........................................................................................................................................................................................144.2 Consumption ...................................................................................................................................................................................164.3 International Trade ..........................................................................................................................................................................174.3.1 Light Vehicles ........................................................................................................................................ 174.3.2 Mexico’s consolidation as fourth largest exporter internationally .......................................................... 174.3.3 Heavy vehicles ....................................................................................................................................... 184.4 Foreign Direct Investment .............................................................................................................................................................184.4.1 Mexico: A Proven Investment Destination ........................................................................................... 184.5 International Companies in Mexico .............................................................................................................................................194.6 Jobs ....................................................................................................................................................................................................214.7 Chambers and Associations ...........................................................................................................................................................214.8 Automotive Engineering and Design Centers ...........................................................................................................................214.9 Other Relevant Initiatives in Automotive Engineering and Design ........................................................................................244.10 Mexico: Consolidation in the International Automotive Industry .........................................................................................245. Export Business Case ................................................................................................................................. 276. Investment Business Case ................................................................................................................................................................297. Legal Framework ........................................................................................................................................ 317.1 PROSEC, Regla Octava, IMMEX and Drawback for the Automotive Industry ................................................................317.2 Automotive Decree .........................................................................................................................................................................317.3 International Standards and Certifications ..................................................................................................................................318. Market Access ............................................................................................................................................ 349. Future Trends on Employment and Design Centers .................................................................................. 3610. Conclusions .............................................................................................................................................. 38

Tables and Graphs Index

Figures

Figure 1. Location of light vehicle manufacturing facilities in Mexico..................................................................................................................... 20Figure 2. Location of heavy vehicle manufacturing facilities ................................................................................................................................... 20Figure 3. Location of design centers and testing tracks ............................................................................................................................................ 23Figure 4 ProMéxico’s ACT Model ........................................................................................................................................................................... 27

Gráficas

Graph 1 Share Of The Automotive Sector Based On Production In 2012 ................................................................................................................ 7Graph 2 Light Vehicle Sales At International Level 2011-20162016 ........................................................................................................................ 7Graph 3 Heavy Vehicle Sales At International Level 2011-2016 .............................................................................................................................. 8Graph 4 Light Vehicles Sales By Region .................................................................................................................................................................. 8Graph 5 Heavy Vehicle Sales By Region .................................................................................................................................................................... 8Graph 6 Vehicle Production 2006-2012 (Millions Of Units ...................................................................................................................................... 9Graph 7 Light Vehicle Production 2005-2016 ......................................................................................................................................................... 14 Graph 8 Heavy Vehicle Production 2005-2016 ...................................................................................................................................................... 15Graph 9 Top 5 Plants In North America ................................................................................................................................................................. 15Graph 10 Light Vehicles Sales In Mexico 2008-2017 (Units) ................................................................................................................................. 16Graph 11 Heavy Vehicle Sales In Mexico 2008-2017 (Units) ................................................................................................................................. 16Graph 12 Segmentation of Heavy Vehicle Sales In Mexico ..................................................................................................................................... 16Graph 13 Main Light Vehicle Exporters ................................................................................................................................................................. 17(Millions Of Units) .................................................................................................................................................................................................. 17Graph 14 Heavy Vehicle Exports And Imports (2007-2012) .................................................................................................................................. 18Graph 15 Foreign Direct Investment In The Automotive Sector (2006-2012) ........................................................................................................ 18Graph 16. Total Market Value And Investment Opportunity In The Supply Chain Of The Automotive Industry In Mexico (Billions Of Dollars) 29Graph 17. Total Market Value And Investment Opportunity In The Supply Chain Of The Automotive Industry In Mexico (Billions Of Dollars) 29

Tablas

Table 1 Top Ten Manufacturing countries (million units) .......................................................................................................................................... 7Table 2 Sales Of The Leading Automotive Companies Internationally ................................................................................................................... 10Table 3 Some Light Vehicles Produced In Mexico .................................................................................................................................................. 14Table 4 Some Heavy Vehicles Produced In Mexico ................................................................................................................................................. 14Table 5 Light Vehicle Sales In Latin America ......................................................................................................................................................... 16Table 6 Share in sales by heavy vehicle company in Mexico ..................................................................................................................................... 17Tabla 7. Mexican Light Vehicle Exports .................................................................................................................................................................. 17Tabla 8. Mexican Light Vehicle Imports .................................................................................................................................................................. 17Table 9 Producing Companies Established In Mexico ............................................................................................................................................. 19 Table 10 Sales By The Main Industry Players In Mexico ........................................................................................................................................ 21

I Introduction

2

1. Introduction

1.1 Objective

The purpose of this document is to provide an overview of the do-mestic and international vehicle manufacturing industry, as a tool to identify the business opportu-nities offered by the industry in Mexico.

The study includes a reference framework with some key indi-cators, at both the international and domestic level, including the following: production, sales, ma-jor trends, consumption, trade, in-vestment and regulations, among other topics.

It paints the landscape of the do-mestic industry, focusing on mar-ket, trade, existing clusters, cham-bers and associations, programs and the current legal framework.

The document includes informa-tion aimed to help identify Mexico as a great destination for foreign investment and define its expor-ting potential.

1.2 What’s New

The Diagnosis of the Terminal Au-tomotive Industry 2013 edition will give readers an update on the main domestic and international indicators and it offers new sec-tions that were not included in the 2012 edition to provide a more complete overview of the sector in Mexico.

The following are some of the changes in this edition:

In this edition, we analyzed and separated the value of vehicles based on the categorization of the Mexican industry. Therefore, there is a difference with values presented in the previous edition, which were created based on the categorization established by the International Organization of Mo-tor Vehicle Manufacturers (OICA).

Updated information regarding the leading companies interna-tionally and their ranking in terms of sales in recent years. New trends in the automotive in-dustry that affect production and

consumption patterns in the in-dustry.

Analysis of Mexico’s ranking as the fourth largest exporter inter-nationally.

New investments made in recent years for light and heavy vehicle manufacturing. In addition, this edition includes new arguments on the achievements of the Mexi-can industry.

Updating of export and inves-tment cases, which mention se-veral opportunities identified by ProMexico and support from other government institutions to continue positioning Mexico in the international arena.

Conclusions based on existing efforts in Mexico from various key players such as associations, ins-titutions and companies that seek to increase the dynamism of the industry and boost its short- and medium-term growth.

3

II Industry Overview

4

The automotive industry is constituted by two sectors: terminal and auto parts.

This study will focus on activities carried out by vehicle manu-facturers.

2.1 Segmentation

On an international level, the terminal industry typically divides the production of automotive vehicles into two segments: light and heavy vehicles. This study will use the following definition based on the Mexican industry:

Light vehicles: passenger vehicles; those motor vehicles used for passenger transportation, and comprising no more than eight seats (including driver).

Light commercial vehicles: motor vehicles used to transport go-ods and passengers; the category includes pick-ups, SUVs, mini-vans and panel trucks.

Heavy vehicles: also known as commercial vehicles, they include light commercial vehicles, heavy trucks and buses.

Heavy trucks: vehicles used for goods transportation. Their weight is over 7 tons.

Buses: vehicles used to transport more than eight passengers, with a capacity of over 7 tons.

2. Industry Overview

The gap in vehicle

production between Mexico (8th) and Brazil (7th) diminished

from 715,863 units in 2011 to 319,670 units in

2012.

5

2.1 Global Key Indicators for 2012

1. Source: Marketline, estimates 2. Source: ProMexico with data by OICA 3. Source: Fortune Global 500, 2012 4. Source: OICA 5. Source: AMIA6. Source: ProMexico with data by Global Trade Atlas 7. Source: ANPACT 8. Source: ANPACT 9. Source: INEGI 10. Source: Ministry of Economy

2.2 Mexican Key Indicators 2012

Light vehicle production value$1,221,834 Million Dollars (Md)1

Global heavy vehicle production value$211,510 (md)1

North America’s share in production European Union’s share in production

Rest of the world’s share in production

Main producing countries2

Asia-Pacific’s share in production

Leading companies by international sales3

Light units produced80.0 million vehicles2

Heavy units produced4.1 million vehicles2

Share of the automotive industry as % of the GDP 20119

4%

Share of the automotive industry in FDI10 21%

Global producer of light vehicles5

2.88 million vehicles

Exporter of light vehicles6

2.35 million vehicles

Mexico’s global ranking as heavy vehicle producer7

138,078 vehicles

Exporter of heavy vehicles7

104,155 vehicles

Share of the automotive industry as % of the manufacturing GDP 2011 920%

Share of the automotive industry in total exports6

27%

Number of jobs created9

62,196 JobsMexico’s global ranking as vehicle ma-nufacture4

3.02 million vehicles

$

52% 29%

1%18%

51% 17%

3%29%

235,364 md 221,551 md 150,276 md

China, United States and Japan

8th

8th

4th

7th

4to

6

III Global Outlook

7

3. Global OutlookIn 2012, China ratified the size of its market and production in-ternationally by becoming the leading producer in the industry, surpassing the United States and Japan.11

According to OICA´s ranking of forty countries and based on their vehicle production, Mexico maintained its eighth position among the leading manufacturers worldwide, above countries such as Spain, France, Russia, the United Kingdom and Belgium.

Table 1 Top Ten Manufacturing countries (million units)

2009 2010 2011 2012

1 China – 13.8 China – 18.2 China – 18.8 China – 19.2

2 Japan – 7.9 Japan – 9.6 USA – 8.6 USA – 10.3

3 USA – 5.7 USA – 7.7 Japan – 8.3 Japan – 9.9

4 Germany – 5.2 Germany – 5.9 Germany – 6.3 Germany – 5.6

5 South Korea – 3.5

South Korea – 4.2

South Korea – 4.6

South Korea – 4.5

6 Brazil – 3.2 India – 3.5 India – 3.9 India – 4.1

7 India – 2.6 Brazil – 3.3 Brazil – 3.4 Brazil – 3.3

8 España – 2.1 España – 2.3 Mexico – 2.6 Mexico – 3.09

France – 2.0 Mexico – 2.3 España – 2.3 Tailandia – 2.4

10 Mexico – 1.6 France – 2.2 France – 2.2 Canadá – 2.4

Source: OICA** The ranking is based on production recorded by OICA; there may be differences with units produced in Mexico according to AMIA (Mexican Association of the Automotive Industry).

The gap in vehicle production between Mexico (8th) and Brazil (7th) decreased from 715,863 units in 2011 to 319,670 units in 2012.

3.1ProductionThe vehicle manufacturing segment accounts for close to 73.1% of the automotive industry’s total production.

Graph 1 Share Of The Automotive Sector Based On Production In 2012

11. Source: ProMéxico with data by OICA12. Source: Global New Cars, Marketline December 2012

Source: ProMéxico with data by Marketline

3.1.1 Light vehicles

In 2012, the light vehicle production reached a total value of 1,222 billion dollars or 80,055,578 vehicles produced. This represented a 22.4% growth in value compared to the previous year.

Estimates indicate that in 2016 light vehicle production will rea-ch 95 million vehicles, a 19.9% growth from 2011 to 2016, with a total value of 1,582 billion dollars.

3.1.2 Heavy vehicles

With regard to the heavy vehicle segment, in 2012 production reached 4,085,631 units, or 211.5 billion dollars, with a 4.3% in-crease compared to 2011.

Estimates indicate that in 2016 production of light vehicles will reach 289.7 billion dollars, with an estimated growth of 36.9% compared to 2012.

3.2 ConsumptionIn 2012, sales of light vehicles were estimated at 1,426 billion do-llars12, or a 9.2% increase compared to 2011.

Estimates indicate that by 2016 sales of light vehicles will reach 2,153 billion dollar, increasing 51.5% from its value of 2012.

Graph 2 Light Vehicle Sales At International Level (MD) 2011-2016

Source: ProMéxico with data by MarketLine

Autoparts26.9%

Auto OEM

Industry

73.1%

8

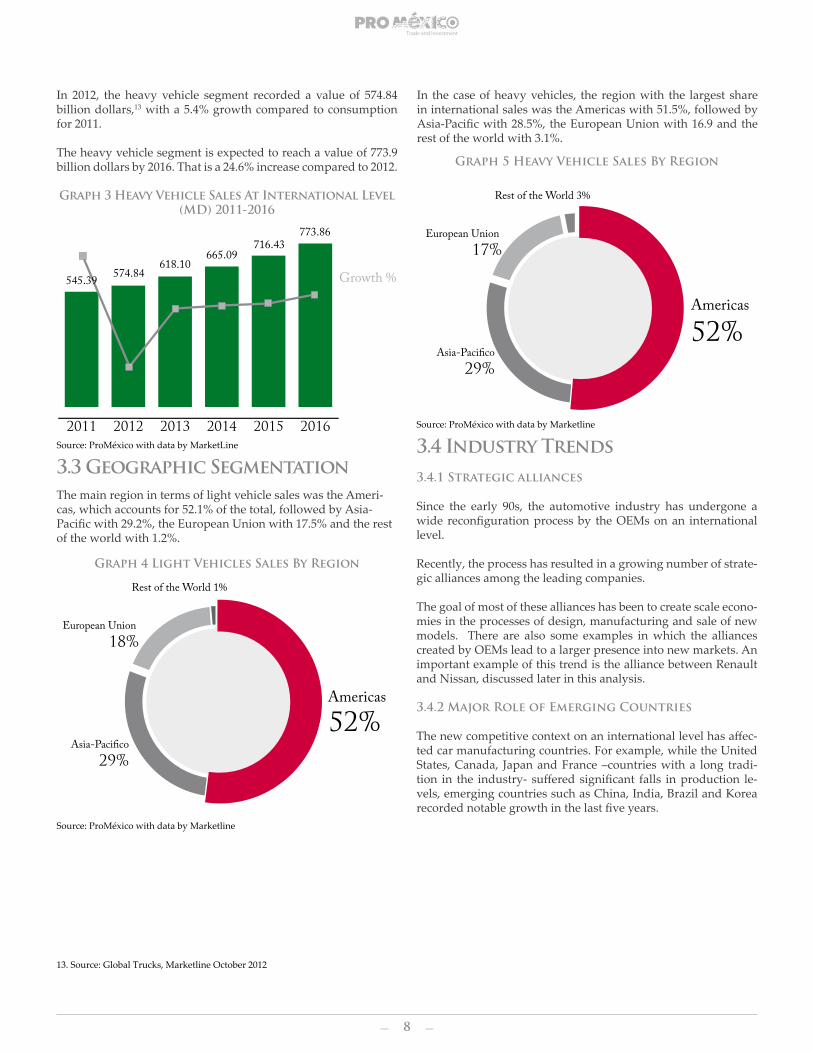

In 2012, the heavy vehicle segment recorded a value of 574.84 billion dollars,13 with a 5.4% growth compared to consumption for 2011.

The heavy vehicle segment is expected to reach a value of 773.9 billion dollars by 2016. That is a 24.6% increase compared to 2012.

Graph 3 Heavy Vehicle Sales At International Level (MD) 2011-2016

13. Source: Global Trucks, Marketline October 2012

Source: ProMéxico with data by MarketLine

3.3 Geographic SegmentationThe main region in terms of light vehicle sales was the Ameri-cas, which accounts for 52.1% of the total, followed by Asia-Pacific with 29.2%, the European Union with 17.5% and the rest of the world with 1.2%.

Graph 4 Light Vehicles Sales By Region

Source: ProMéxico with data by Marketline

In the case of heavy vehicles, the region with the largest share in international sales was the Americas with 51.5%, followed by Asia-Pacific with 28.5%, the European Union with 16.9 and the rest of the world with 3.1%.

Graph 5 Heavy Vehicle Sales By Region

3.4 Industry Trends3.4.1 Strategic alliances

Since the early 90s, the automotive industry has undergone a wide reconfiguration process by the OEMs on an international level.

Recently, the process has resulted in a growing number of strate-gic alliances among the leading companies.

The goal of most of these alliances has been to create scale econo-mies in the processes of design, manufacturing and sale of new models. There are also some examples in which the alliances created by OEMs lead to a larger presence into new markets. An important example of this trend is the alliance between Renault and Nissan, discussed later in this analysis.

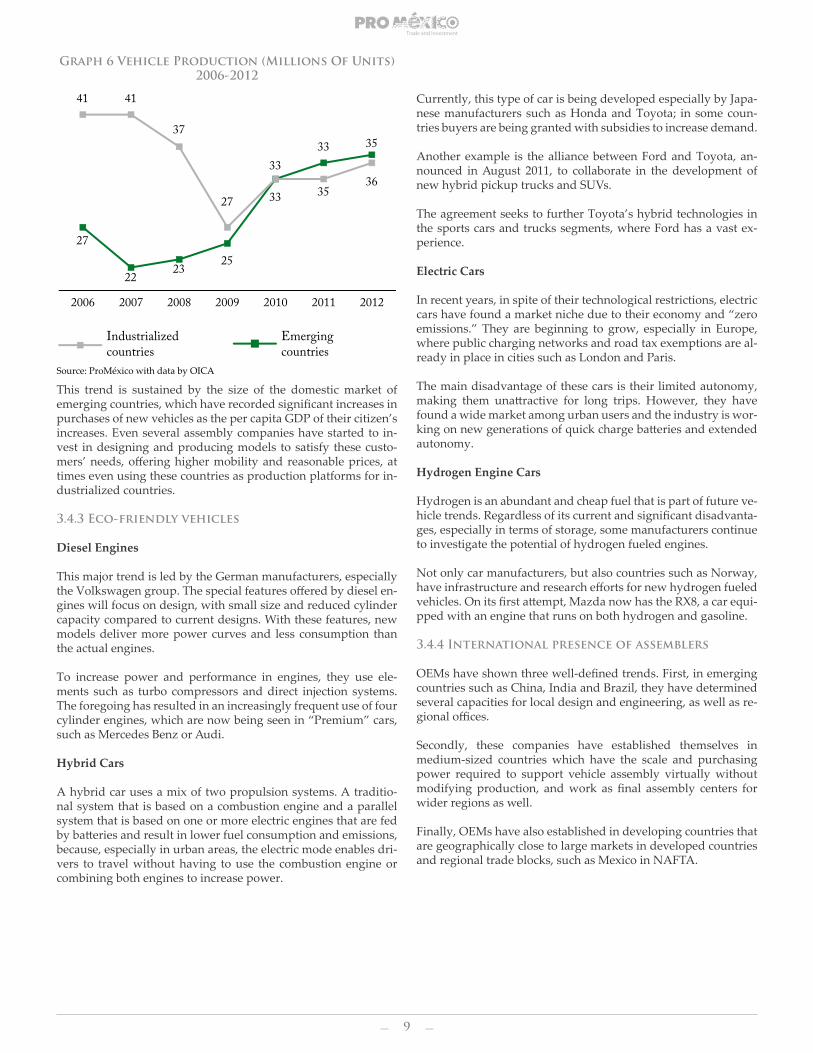

3.4.2 Major Role of Emerging Countries

The new competitive context on an international level has affec-ted car manufacturing countries. For example, while the United States, Canada, Japan and France –countries with a long tradi-tion in the industry- suffered significant falls in production le-vels, emerging countries such as China, India, Brazil and Korea recorded notable growth in the last five years.

Source: ProMéxico with data by Marketline

9

Graph 6 Vehicle Production (Millions Of Units) 2006-2012

Source: ProMéxico with data by OICA

This trend is sustained by the size of the domestic market of emerging countries, which have recorded significant increases in purchases of new vehicles as the per capita GDP of their citizen’s increases. Even several assembly companies have started to in-vest in designing and producing models to satisfy these custo-mers’ needs, offering higher mobility and reasonable prices, at times even using these countries as production platforms for in-dustrialized countries. 3.4.3 Eco-friendly vehicles

Diesel Engines

This major trend is led by the German manufacturers, especially the Volkswagen group. The special features offered by diesel en-gines will focus on design, with small size and reduced cylinder capacity compared to current designs. With these features, new models deliver more power curves and less consumption than the actual engines.

To increase power and performance in engines, they use ele-ments such as turbo compressors and direct injection systems. The foregoing has resulted in an increasingly frequent use of four cylinder engines, which are now being seen in “Premium” cars, such as Mercedes Benz or Audi.

Hybrid Cars

A hybrid car uses a mix of two propulsion systems. A traditio-nal system that is based on a combustion engine and a parallel system that is based on one or more electric engines that are fed by batteries and result in lower fuel consumption and emissions, because, especially in urban areas, the electric mode enables dri-vers to travel without having to use the combustion engine or combining both engines to increase power.

Currently, this type of car is being developed especially by Japa-nese manufacturers such as Honda and Toyota; in some coun-tries buyers are being granted with subsidies to increase demand.

Another example is the alliance between Ford and Toyota, an-nounced in August 2011, to collaborate in the development of new hybrid pickup trucks and SUVs.

The agreement seeks to further Toyota’s hybrid technologies in the sports cars and trucks segments, where Ford has a vast ex-perience.

Electric Cars

In recent years, in spite of their technological restrictions, electric cars have found a market niche due to their economy and “zero emissions.” They are beginning to grow, especially in Europe, where public charging networks and road tax exemptions are al-ready in place in cities such as London and Paris.

The main disadvantage of these cars is their limited autonomy, making them unattractive for long trips. However, they have found a wide market among urban users and the industry is wor-king on new generations of quick charge batteries and extended autonomy.

Hydrogen Engine Cars

Hydrogen is an abundant and cheap fuel that is part of future ve-hicle trends. Regardless of its current and significant disadvanta-ges, especially in terms of storage, some manufacturers continue to investigate the potential of hydrogen fueled engines.

Not only car manufacturers, but also countries such as Norway, have infrastructure and research efforts for new hydrogen fueled vehicles. On its first attempt, Mazda now has the RX8, a car equi-pped with an engine that runs on both hydrogen and gasoline.

3.4.4 International presence of assemblers

OEMs have shown three well-defined trends. First, in emerging countries such as China, India and Brazil, they have determined several capacities for local design and engineering, as well as re-gional offices.

Secondly, these companies have established themselves in medium-sized countries which have the scale and purchasing power required to support vehicle assembly virtually without modifying production, and work as final assembly centers for wider regions as well.

Finally, OEMs have also established in developing countries that are geographically close to large markets in developed countries and regional trade blocks, such as Mexico in NAFTA.

10

3.5 Leading World Companies

In 2012, for the third year in a row, Toyota was the largest light and heavy vehicle producer in the world, with 8.5 million units produced, followed by General Motors with 8.4 million units and Volkswagen with 7.3 million units.

In terms of sales values, Toyota earned 235 billion dollars in re-venues, followed by Volkswagen with sales of 221 billion dollars, General Motors with 150 billion dollars and Daimler with 148 billion dollars.

Table 2 Sales Of The Leading Automotive Companies Internationally (BD)

Ranking 2010 Ranking 2011 Ranking 2012

Toyota 204 Toyota 222 Toyota 235Volkswagen 146 Volkswagen 168 Volkswagen 221

Ford 118 GM 135 GM 150

Daimler 109 Daimler 129 Daimler 148

GM 105 Ford 129 Ford 136

Source: ProMéxico with data by Fortune Global 500, 2012, 2011 y 2010

In 2011, Ford and General Motors recorded a drop in comparison to their previous ranking, due largely to the 2009 crisis.

Ford was the only American company that did not receive fi-nancial aid, which left it exposed to remedy its finances after the crisis. Meanwhile, General Motors received aid from the gover-nment and was even the subject of corporate restructuring that resulted in the extinction of the Pontiac, Hummer and Saturn brands, and the sale of other brands such as Saab.

Meanwhile, Toyota profited from car sales after having suffered the lack of supply that resulted from the tsunami that hit Japan in 2011. After this event, many companies that manufactured products in Japan began to diversify their operations around the world. Mexico and Brazil are just some of the countries that re-ceived these operations.

The industry is expected to grow 42.4% by 2015, reaching 3.195 billion dollars. The industry has not recovered yet the income it had during 2007 that was of 2,374 million dollars.

Toyota

Currently the largest car manufacturer in the world, the com-pany focuses on the design, manufacturing and sale of light vehi-cles, minivans and trucks.

Toyota has more than 50 production plants in 26 countries. In the car segment, Toyota’s business is divided into conventional engine vehicles and hybrid vehicles. Toyota’s brands are To-

yota, Lexus, Hino and Daihatsu. Meanwhile, in Japan the com-pany sells its luxury cars under the Crown and Century brands. Toyota’s mass production hybrid car is the Prius.

According to Fortune Global magazine for 2012, Toyota is ranked 10th of the 500 largest companies in the world and first among Japan’s largest companies.

General Motors

General Motors is an American company located in Detroit, Mi-chigan, that focuses on the design, development, manufacturing and sale of cars. It has presence in 31 countries.

In North America, the company sells the following brands: Buick, Cadillac, Chevrolet and GMC. Internationally, the company dis-tributes Opel, GMC, Vaux-hall, Buick, Cadillac, Isuzu, Holden, Chevrolet and Daewoo.

In 2009, as a result of the financial crisis, the US government acquired 61% of General Motors shares at an approximate price of 50 billion dollars.

One of GM’s main budgetary cuts to obtain federal funds, was to cease production and sales of the Pontiac brand vehicles, created in 1926 and sold in the United States, Canada and Mexico.

In May 2013, the US government announced the sale of a new round of General Motors stock, which it had acquired during the financial rescue. The US Treasury plans to sell 214.7 million dollars in shares during a 12 to 15 month period. In May, the government held approximately 18% of the company’s common stock and had recovered 94.6% of the financial rescue provided to General Motors.

According to Fortune Global magazine for 2012, General Motors is ranked 19th among the 500 largest companies in the world and 8th among the largest companies in the US.

Ford

One of the leading car companies internationally, Ford is head-quartered in Michigan in the United States.

It designs, manufactures and distributes cars through more than 65 plants around the world and it has 171,000 employees. The company’s brands are Ford and Lincoln, and it sells Motorcraft auto parts.

11

Region/Country

R&D Centers

Design Centers

Manufacturing Plants

Education Centers

Japan 7 -- 14 1

USA 2 1 3 --

Europe 1 1 3 --

Asia 4 1 14 --

Mexico, Latin Ame-ricaand the Caribbean

-- -- 3 --

Africa -- -- 3 --

Oceania -- -- 1 --

Chrysler

The current Chrysler Group LLC was founded in 2009 as part of a strategic alliance with the Italian Fiat S.p.A. It is headquartered in Auburn Hills, Michigan.

The group produces and sells cars under the Chrysler, Jeep, Do-dge, Ram, SRT, Fiat and Mopar brands. As part of its industrial Alliance with Fiat, Chrysler also produces and sells Fiat vehicles for North America. Likewise, Chrysler sells Mopar auto parts.

Approximately 10% of its vehicle sales in 2012 were outside Nor-th America, mainly Asia-Pacific, South America and Europe. Un-til 2007, Chrysler was part of Daimler-Chrysler, until it was sold to Cerberus Management LP.

Chrysler was one of the most affected by the 2009 financial crisis. That year, the company went bankrupt and the US government contributed 6.6 billion dollars to help the company continue to pay its debts and begin it’s restructuring. In May 2011, Chrysler paid 7.6 billion dollars to the US and Canadian governments (5.9 billion and 1.7 billion dollars, respectively).

The 2012 financial report shows that Fiat has 58.5% of the company’s shares, and the remaining 41.5% is owned by the Vo-luntary Employee Beneficiary Association (VEBA) and is contro-lled by the Union of Auto Workers (UAW) of the United States.

Volkswagen

Globally, Volkswagen is recognized as one of the leading vehicle manufacturers. Its headquarters are located in Wolfsburg, Ger-many.

Volkswagen Group has 100 production plants of which 50 are located in Europe; 28 in Germany, 17 in Eastern Europe, four in North America (one in the United States and three in Mexico), nine in South America (six in Brazil and three in Argentina), three in South Africa and 17 in Asia-Pacific (12 in China, four in India and one in Thailand).

The group is constituted by 12 brands: Volkswagen, Audi, Skoda, Seat, Porsche, Bentley, Bugatti, Lamborghini, Ducati (motorcy-cles), Scania, MAN and Volkswagen Commercial Vehicles.

Each of the brands operates as a separate entity. The group has approximately 550,000 employees.

Volkswagen is ranked 12th among the 500 largest companies in the world, according to Fortune Global 500’s ranking for 2012. In Germany, the company is ranked first

Nissan

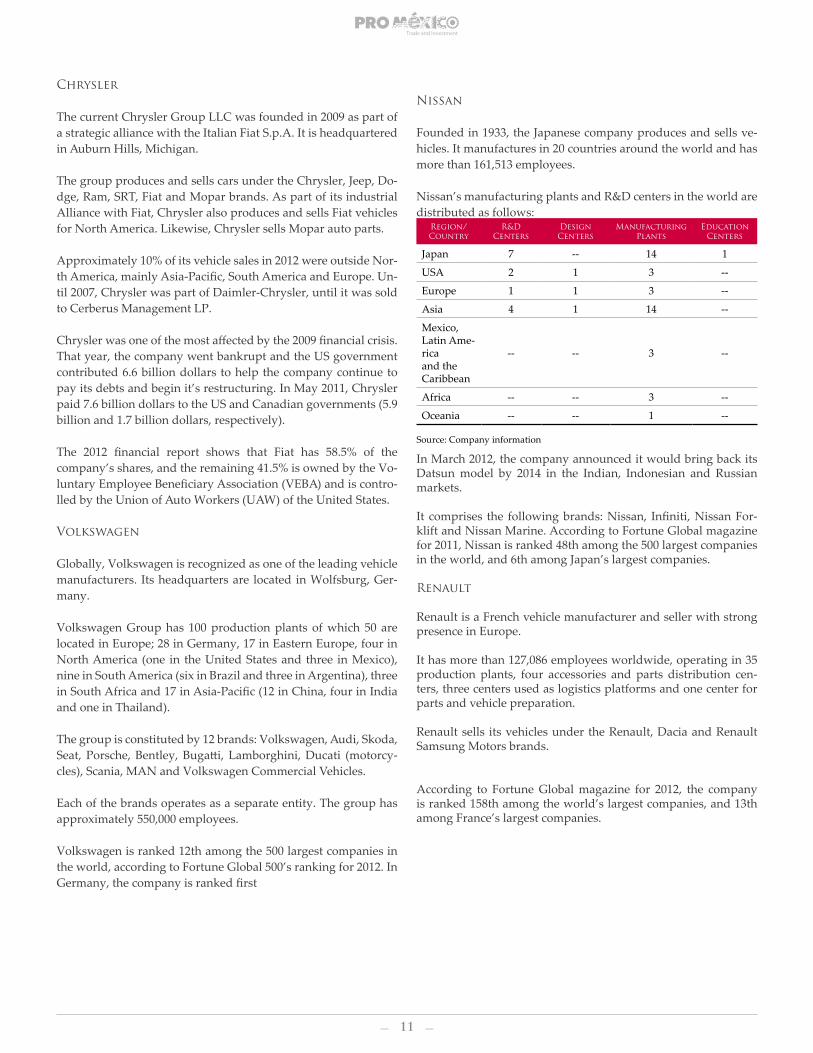

Founded in 1933, the Japanese company produces and sells ve-hicles. It manufactures in 20 countries around the world and has more than 161,513 employees.

Nissan’s manufacturing plants and R&D centers in the world are distributed as follows:

Source: Company information

In March 2012, the company announced it would bring back its Datsun model by 2014 in the Indian, Indonesian and Russian markets.

It comprises the following brands: Nissan, Infiniti, Nissan For-klift and Nissan Marine. According to Fortune Global magazine for 2011, Nissan is ranked 48th among the 500 largest companies in the world, and 6th among Japan’s largest companies.

Renault

Renault is a French vehicle manufacturer and seller with strong presence in Europe.

It has more than 127,086 employees worldwide, operating in 35 production plants, four accessories and parts distribution cen-ters, three centers used as logistics platforms and one center for parts and vehicle preparation.

Renault sells its vehicles under the Renault, Dacia and Renault Samsung Motors brands.

According to Fortune Global magazine for 2012, the company is ranked 158th among the world’s largest companies, and 13th among France’s largest companies.

12

Nissan-Renault Alliance

Founded in 1999, the Alliance between these assemblers was created with the goal of expanding and creating new projects and alliances internationally.

Goals for 2016 Situation in 2011

Sell 10 million units Sell 8 million vehicles

Put 1.5 million zero CO2 emission vehicles in circulation

The first year, 30,000 units were sold and combined they held

67% of the market

Earn average income of 9% Earned income of 8.4%

Source: Company information

Renault has 43.4% of Nissan’s shares, while Nissan has 15% of Renault’s shares. According to the companies, having shared stock benefits the Alliance because it leads to a “win-win” strate-gy for both companies.

Subsequently, in 2010, Daimler AG announced a collaboration agreement with the alliance to efficiently increase operations internationally. As part of the agreement, the Renault-Nissan

Alliance has 3.1% of Daimler’s shares, while Daimler acquired 3.1% of Renault’s shares and 3.1% of Nissan’s.

The following are actions that the Alliance has undertaken inemerging markets:

• Nissan uses Renault’s plant in Curitiba, Brazil, to have a pre-sence in the Brazilian market.

• In Russia, both companies manufacture Renault, Nissan and Lada models in the AVTOVAZ plant in Togliatti.

• In India, they use a joint platform to produce the Nissan Mi-cra-Renault Pulse and Nissan Sunny-Renault Scala models.

• Renault plans to invest with Nissan in a plant in Dongfeng, China.

According to the company, Mexico is the eighth most important market for the Alliance, with 27.4% of the market share, ranking above the United Kingdom and Italy and ranking below China, the United States, Russia, France, Japan, Brazil and Germany.

Mexico is the eighth most important market for the Nissan-Renault

Alliance, with 27.4% of market share,

ranking above the United Kingdom and

Italy.

13

IV The Industry in

Mexico

14

4. The Industry in Mexico

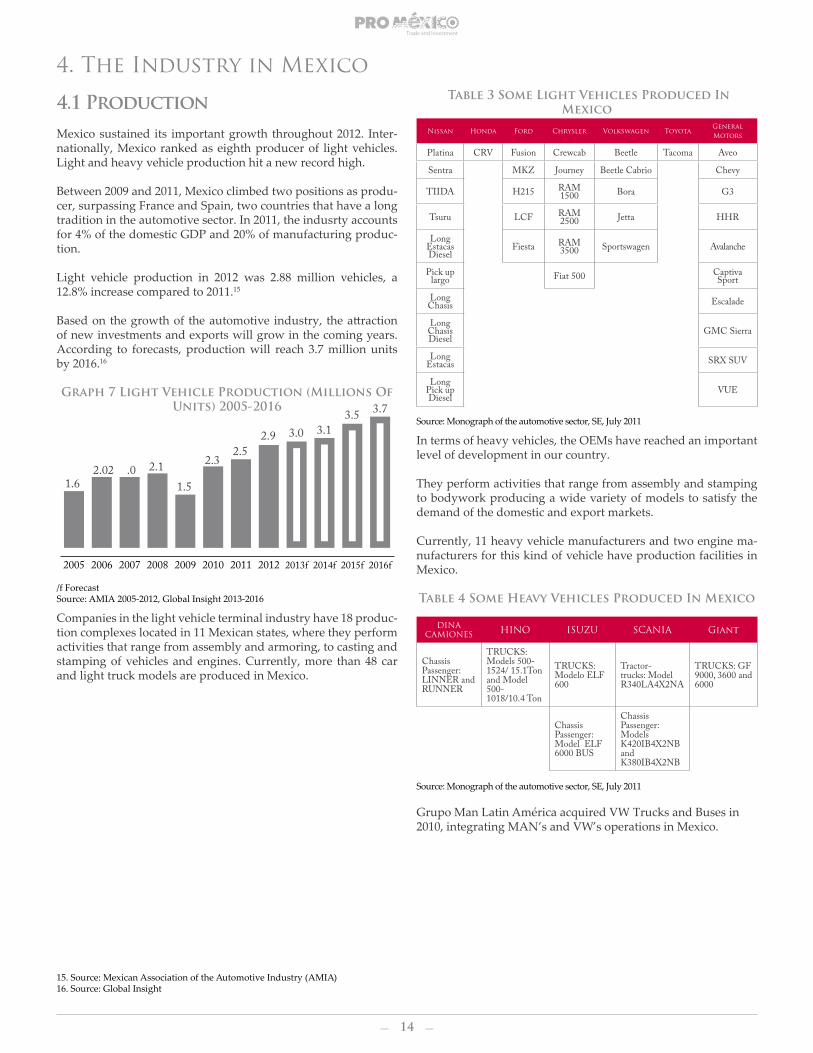

4.1 ProductionMexico sustained its important growth throughout 2012. Inter-nationally, Mexico ranked as eighth producer of light vehicles. Light and heavy vehicle production hit a new record high.

Between 2009 and 2011, Mexico climbed two positions as produ-cer, surpassing France and Spain, two countries that have a long tradition in the automotive sector. In 2011, the indusrty accounts for 4% of the domestic GDP and 20% of manufacturing produc-tion.

Light vehicle production in 2012 was 2.88 million vehicles, a 12.8% increase compared to 2011.15

Based on the growth of the automotive industry, the attraction of new investments and exports will grow in the coming years. According to forecasts, production will reach 3.7 million units by 2016.16

Graph 7 Light Vehicle Production (Millions Of Units) 2005-2016

15. Source: Mexican Association of the Automotive Industry (AMIA)16. Source: Global Insight

/f ForecastSource: AMIA 2005-2012, Global Insight 2013-2016

Companies in the light vehicle terminal industry have 18 produc-tion complexes located in 11 Mexican states, where they perform activities that range from assembly and armoring, to casting and stamping of vehicles and engines. Currently, more than 48 car and light truck models are produced in Mexico.

Table 3 Some Light Vehicles Produced In Mexico

Nissan Honda Ford Chrysler Volkswagen ToyotaGeneral Motors

Platina CRV Fusion Crewcab Beetle Tacoma Aveo

Sentra MKZ Journey Beetle Cabrio Chevy

TIIDA H215 RAM 1500 Bora G3

Tsuru LCF RAM 2500 Jetta HHR

Long Estacas Diesel

Fiesta RAM 3500 Sportswagen Avalanche

Pick up largo Fiat 500 Captiva

Sport

Long Chasis Escalade

LongChasis Diesel

GMC Sierra

LongEstacas SRX SUV

Long Pick up Diesel

VUE

Source: Monograph of the automotive sector, SE, July 2011

In terms of heavy vehicles, the OEMs have reached an important level of development in our country.

They perform activities that range from assembly and stamping to bodywork producing a wide variety of models to satisfy the demand of the domestic and export markets.

Currently, 11 heavy vehicle manufacturers and two engine ma-nufacturers for this kind of vehicle have production facilities in Mexico.

Table 4 Some Heavy Vehicles Produced In Mexico

DINA CAMIONES HINO ISUZU SCANIA Giant

Chassis Passenger: LINNER and RUNNER

TRUCKS:Models 500-1524/ 15.1Tonand Model 500- 1018/10.4 Ton

TRUCKS: Modelo ELF 600

Tractor-trucks: Model R340LA4X2NA

TRUCKS: GF 9000, 3600 and 6000

Chassis Passenger: Model ELF 6000 BUS

Chassis Passenger: Models K420IB4X2NB andK380IB4X2NB

Source: Monograph of the automotive sector, SE, July 2011

Grupo Man Latin América acquired VW Trucks and Buses in 2010, integrating MAN’s and VW’s operations in Mexico.

2016f2015f2014f2013f20122011201020092008200720062005

1.62.02 .0 2.1

1.5

2.32.5

2.9 3.0 3.13.5 3.7

15

Source: Monograph of the automotive sector, SE, July 2011

DAIMLER (Freighter y Mercedez

Benz)

INTERNATIONAL KENWORTH VOLKSWAGEN/ MAN* VOLVO

Trucks: M model

Trucks: 4300 and 4400 model

Trucks: T370, L700 and T800 models

Trucks: 8.150 and 9.150 models

Buses: Volvo 8300, 9700 and 9700 US/CAN

Road trucks: Cascadia, C, F and G models

Road trucks: Prostar and 9200 model

Road trucks: T800 and T660 models

Passenger chassis: 8.150 and 9.150 models

Construction: M model

Construction: 7600 model

Construction: T460 and T800 models

Buses : Lion’s Coach R07-464, Lion’s Top Coach R08-464 and A82.18.410 model

Buses: Boxer, Torino and MBO model

Passenger chassis: 4700, 3000, 3100 and 3300 models

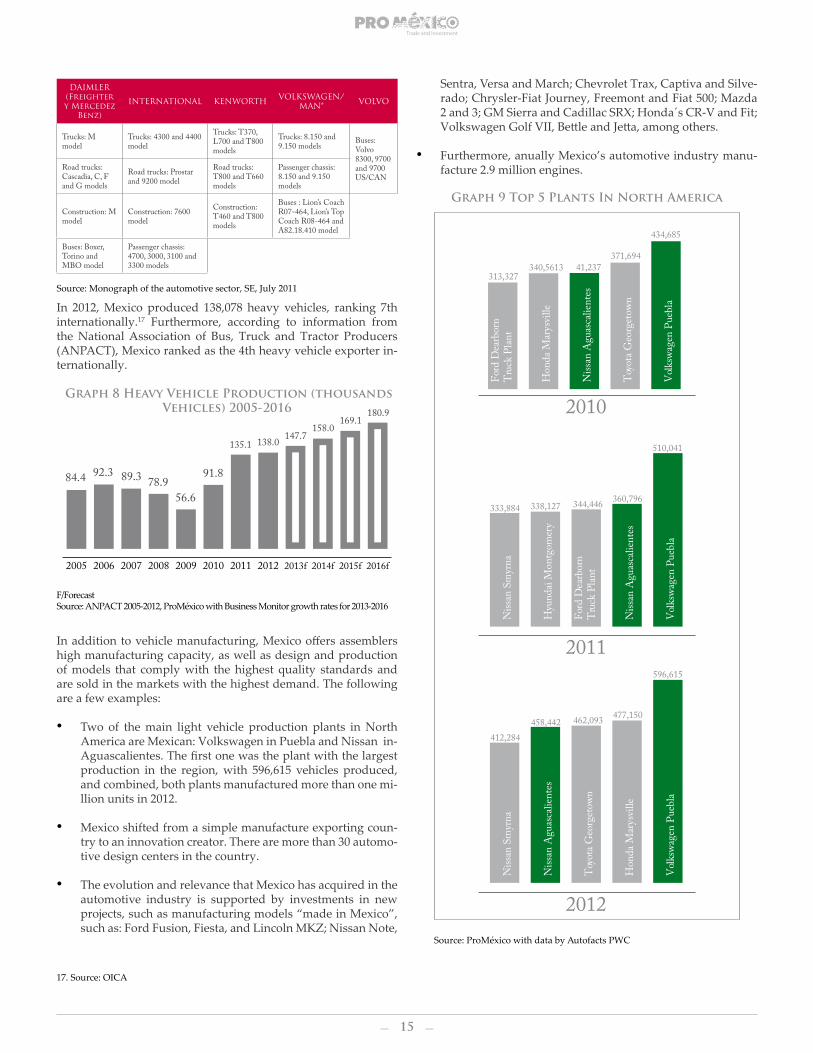

In 2012, Mexico produced 138,078 heavy vehicles, ranking 7th internationally.17 Furthermore, according to information from the National Association of Bus, Truck and Tractor Producers (ANPACT), Mexico ranked as the 4th heavy vehicle exporter in-ternationally.

Graph 8 Heavy Vehicle Production (thousands Vehicles) 2005-2016

F/ForecastSource: ANPACT 2005-2012, ProMéxico with Business Monitor growth rates for 2013-2016

In addition to vehicle manufacturing, Mexico offers assemblers high manufacturing capacity, as well as design and production of models that comply with the highest quality standards and are sold in the markets with the highest demand. The following are a few examples:

• Two of the main light vehicle production plants in North America are Mexican: Volkswagen in Puebla and Nissan in-Aguascalientes. The first one was the plant with the largest production in the region, with 596,615 vehicles produced, and combined, both plants manufactured more than one mi-llion units in 2012.

• Mexico shifted from a simple manufacture exporting coun-try to an innovation creator. There are more than 30 automo-tive design centers in the country.

• The evolution and relevance that Mexico has acquired in the automotive industry is supported by investments in new projects, such as manufacturing models “made in Mexico”, such as: Ford Fusion, Fiesta, and Lincoln MKZ; Nissan Note,

Volk

swag

en P

uebl

a

Toy

ota G

eorg

etow

n

Niss

an A

guas

calie

ntes

Hon

da M

arys

ville

Ford

Dea

rbor

n T

ruck

Pla

nt

313,327340,5613 41,237

371,694

434,685

2010

Volk

swag

en P

uebl

a

Niss

an A

guas

calie

ntes

Ford

Dea

rbor

n T

ruck

Pla

nt

Hyu

ndai

Mon

tgom

ery

Niss

an S

myr

na333,884 338,127 344,446 360,796

510,041

2011V

olksw

agen

Pue

bla

Hon

da M

arys

ville

Toy

ota G

eorg

etow

n

Niss

an A

guas

calie

ntes

Niss

an S

myr

na

412,284458,442 462,093 477,150

596,615

2012

Graph 9 Top 5 Plants In North America

Sentra, Versa and March; Chevrolet Trax, Captiva and Silve-rado; Chrysler-Fiat Journey, Freemont and Fiat 500; Mazda 2 and 3; GM Sierra and Cadillac SRX; Honda´s CR-V and Fit; Volkswagen Golf VII, Bettle and Jetta, among others.

• Furthermore, anually Mexico’s automotive industry manu-facture 2.9 million engines.

Source: ProMéxico with data by Autofacts PWC

17. Source: OICA

2016f2015f2014f2013f20122011201020092008200720062005

84.4 92.3 89.3 78.956.6

91.8

135.1 138.0 147.7158.0

169.1180.9

16

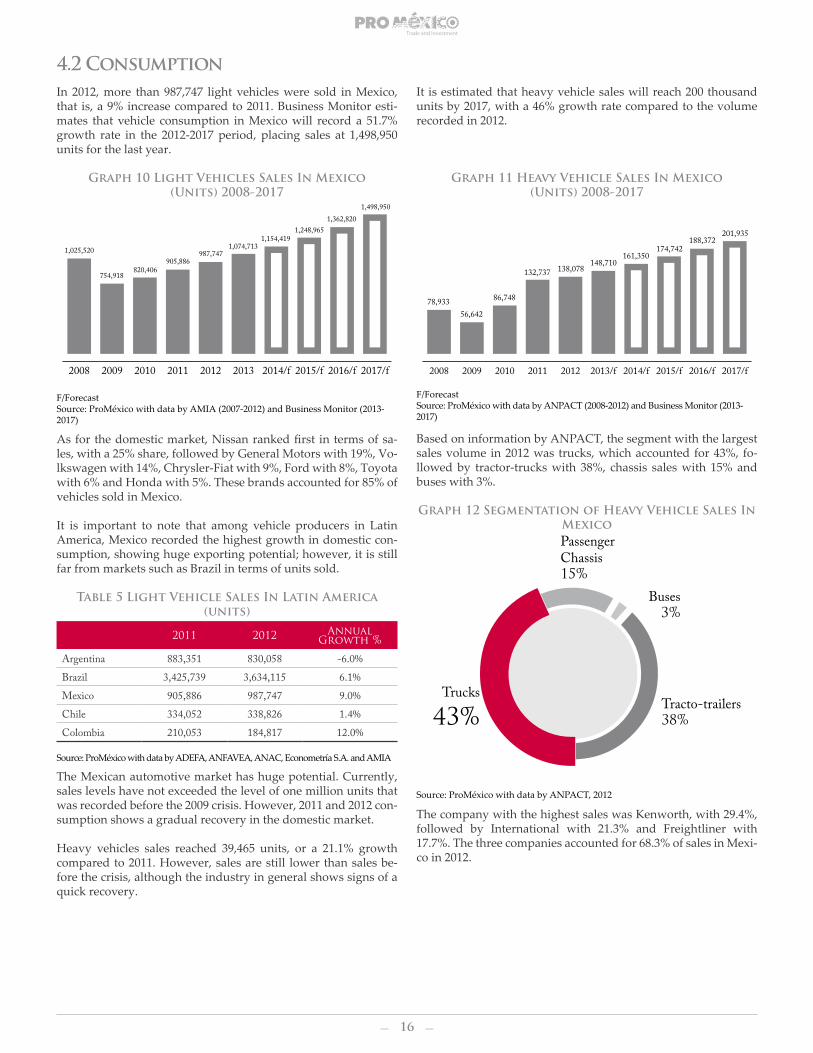

4.2 ConsumptionIn 2012, more than 987,747 light vehicles were sold in Mexico, that is, a 9% increase compared to 2011. Business Monitor esti-mates that vehicle consumption in Mexico will record a 51.7% growth rate in the 2012-2017 period, placing sales at 1,498,950 units for the last year.

Graph 10 Light Vehicles Sales In Mexico (Units) 2008-2017

F/ForecastSource: ProMéxico with data by AMIA (2007-2012) and Business Monitor (2013-2017)

As for the domestic market, Nissan ranked first in terms of sa-les, with a 25% share, followed by General Motors with 19%, Vo-lkswagen with 14%, Chrysler-Fiat with 9%, Ford with 8%, Toyota with 6% and Honda with 5%. These brands accounted for 85% of vehicles sold in Mexico.

It is important to note that among vehicle producers in Latin America, Mexico recorded the highest growth in domestic con-sumption, showing huge exporting potential; however, it is still far from markets such as Brazil in terms of units sold.

Table 5 Light Vehicle Sales In Latin America (units)

2011 2012 Annual Growth %

Argentina 883,351 830,058 -6.0%

Brazil 3,425,739 3,634,115 6.1%

Mexico 905,886 987,747 9.0%

Chile 334,052 338,826 1.4%

Colombia 210,053 184,817 12.0%

Source: ProMéxico with data by ADEFA, ANFAVEA, ANAC, Econometría S.A. and AMIA

The Mexican automotive market has huge potential. Currently, sales levels have not exceeded the level of one million units that was recorded before the 2009 crisis. However, 2011 and 2012 con-sumption shows a gradual recovery in the domestic market.

Heavy vehicles sales reached 39,465 units, or a 21.1% growth compared to 2011. However, sales are still lower than sales be-fore the crisis, although the industry in general shows signs of a quick recovery.

It is estimated that heavy vehicle sales will reach 200 thousand units by 2017, with a 46% growth rate compared to the volume recorded in 2012.

Graph 11 Heavy Vehicle Sales In Mexico (Units) 2008-2017

F/ForecastSource: ProMéxico with data by ANPACT (2008-2012) and Business Monitor (2013-2017)

Based on information by ANPACT, the segment with the largest sales volume in 2012 was trucks, which accounted for 43%, fo-llowed by tractor-trucks with 38%, chassis sales with 15% and buses with 3%.

Graph 12 Segmentation of Heavy Vehicle Sales In Mexico

Source: ProMéxico with data by ANPACT, 2012

The company with the highest sales was Kenworth, with 29.4%, followed by International with 21.3% and Freightliner with 17.7%. The three companies accounted for 68.3% of sales in Mexi-co in 2012.

2017/f2016/f2015/f2014/f2013/f201220112010200920082017/f2016/f2015/f2014/f201320122011201020092008

1,025,520

754,918820,406

905,886987,747

1,074,7131,154,419

1,248,9651,362,820

1,498,950

17

Company Sales (units) % Share

Kenworth 11,585 29.4

International 8,414 21.3

Freightliner 6,973 17.7

Mercedes-Benz 3,477 8.8

Ford 2,135 5.4

Subtotal 32,584 82.6

Total 39,465 100

Destination Units 2012 Share 2012

North America 1,664,450 70.7%

USA 1,504,364 63.9%

Canada 160,086 6.8%

Latin America 366,133 15.5%

Europe 212,792 9.0%

Other 30,815 1.3%

Asia 46,640 2.0%Africa 34,734 1.5%

Total 2,355,564 100%

Origin 2011 (units) % Share

2012 (units)

% Share

Asia 172,837 36 241,441 38

North America 165,945 34 202,165 32

EuropeanUnion 80,040 16 115,748 18

Mercosur 66,800 14 75,099 12

Total 485,622 100 634,453 100Source: ProMéxico with data by ANPACT, 2012

Table 6 Share in sales by heavy vehicle company in Mexico

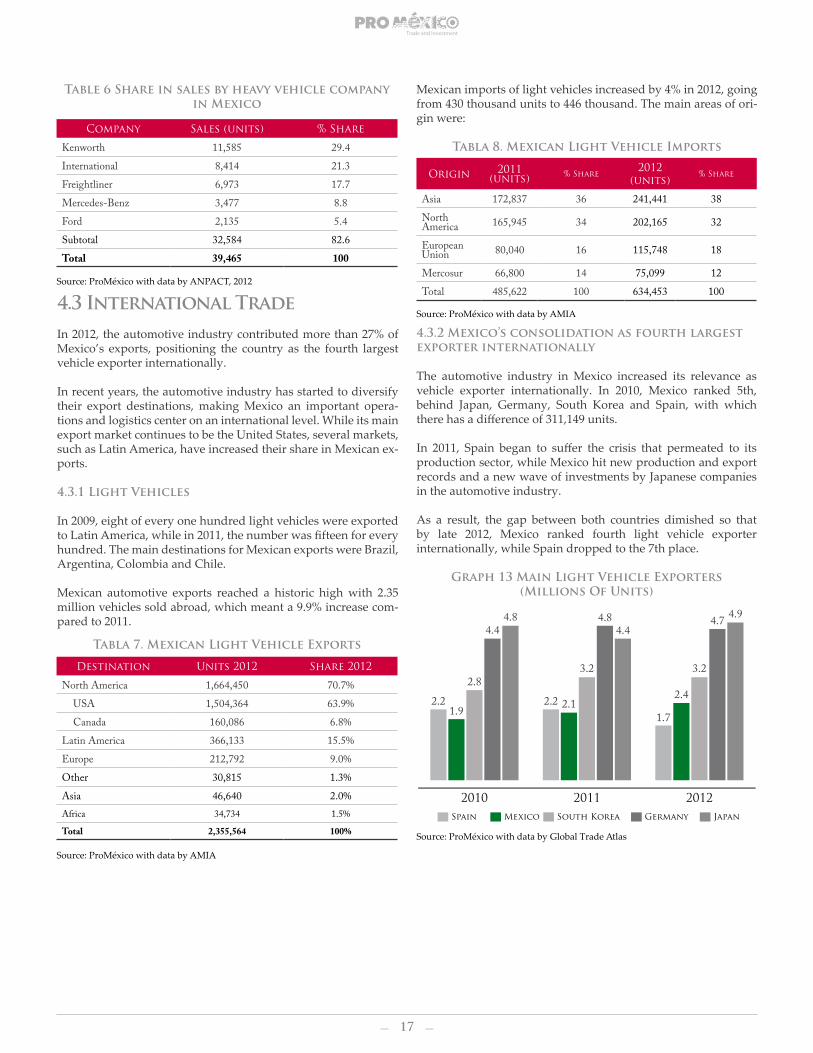

4.3 International TradeIn 2012, the automotive industry contributed more than 27% of Mexico’s exports, positioning the country as the fourth largest vehicle exporter internationally.

In recent years, the automotive industry has started to diversify their export destinations, making Mexico an important opera-tions and logistics center on an international level. While its main export market continues to be the United States, several markets, such as Latin America, have increased their share in Mexican ex-ports.

4.3.1 Light Vehicles

In 2009, eight of every one hundred light vehicles were exported to Latin America, while in 2011, the number was fifteen for every hundred. The main destinations for Mexican exports were Brazil, Argentina, Colombia and Chile.

Mexican automotive exports reached a historic high with 2.35 million vehicles sold abroad, which meant a 9.9% increase com-pared to 2011.

Tabla 7. Mexican Light Vehicle Exports

Source: ProMéxico with data by AMIA

Mexican imports of light vehicles increased by 4% in 2012, going from 430 thousand units to 446 thousand. The main areas of ori-gin were:

Tabla 8. Mexican Light Vehicle Imports

Source: ProMéxico with data by AMIA

4.3.2 Mexico’s consolidation as fourth largest exporter internationally

The automotive industry in Mexico increased its relevance as vehicle exporter internationally. In 2010, Mexico ranked 5th, behind Japan, Germany, South Korea and Spain, with which there has a difference of 311,149 units.

In 2011, Spain began to suffer the crisis that permeated to its production sector, while Mexico hit new production and export records and a new wave of investments by Japanese companies in the automotive industry.

As a result, the gap between both countries dimished so that by late 2012, Mexico ranked fourth light vehicle exporter internationally, while Spain dropped to the 7th place.

Graph 13 Main Light Vehicle Exporters(Millions Of Units)

Source: ProMéxico with data by Global Trade Atlas

18

In terms of the main locations throughout 2011, Japan suffered the effects of the earthquake and tsunami in March, which lar-gely affected its vehicle production and led to Germany beco-ming the leader in light vehicle exports. However, Japan recove-red its lead in 2012.

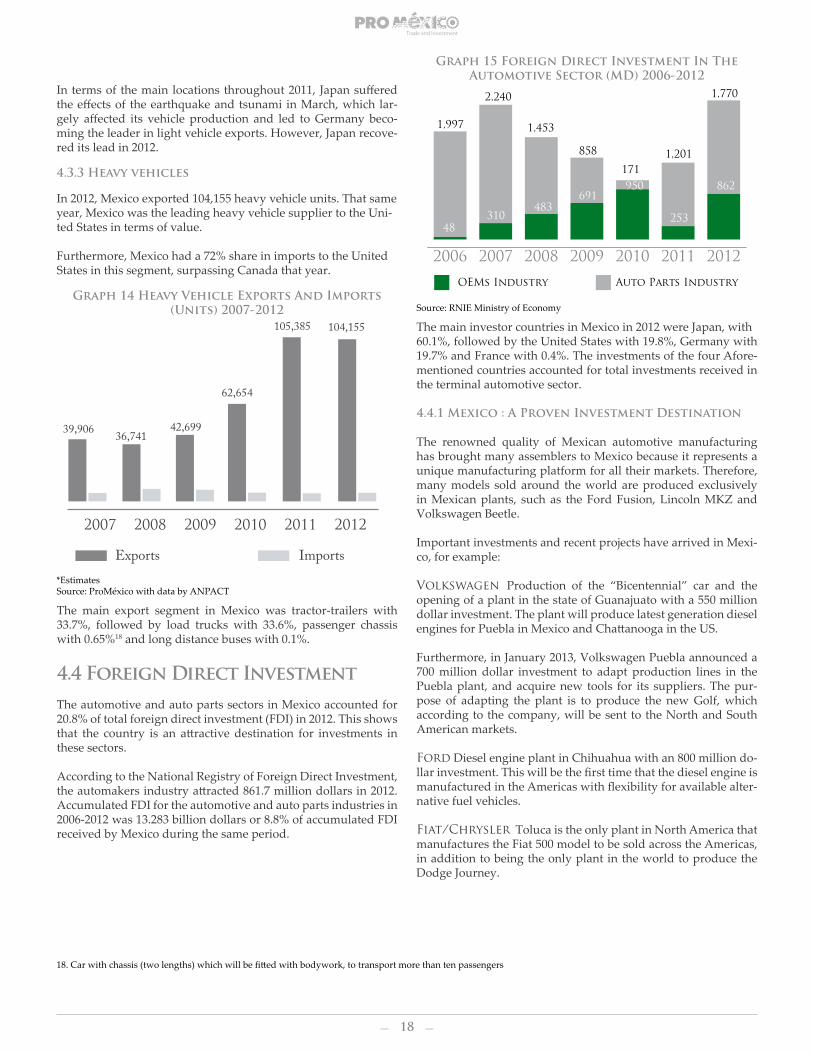

4.3.3 Heavy vehicles

In 2012, Mexico exported 104,155 heavy vehicle units. That same year, Mexico was the leading heavy vehicle supplier to the Uni-ted States in terms of value.

Furthermore, Mexico had a 72% share in imports to the United States in this segment, surpassing Canada that year.

Graph 14 Heavy Vehicle Exports And Imports (Units) 2007-2012

*EstimatesSource: ProMéxico with data by ANPACT

The main export segment in Mexico was tractor-trailers with 33.7%, followed by load trucks with 33.6%, passenger chassis with 0.65%18 and long distance buses with 0.1%.

4.4 Foreign Direct InvestmentThe automotive and auto parts sectors in Mexico accounted for 20.8% of total foreign direct investment (FDI) in 2012. This shows that the country is an attractive destination for investments in these sectors.

According to the National Registry of Foreign Direct Investment, the automakers industry attracted 861.7 million dollars in 2012. Accumulated FDI for the automotive and auto parts industries in 2006-2012 was 13.283 billion dollars or 8.8% of accumulated FDI received by Mexico during the same period.

18. Car with chassis (two lengths) which will be fitted with bodywork, to transport more than ten passengers

Graph 15 Foreign Direct Investment In The Automotive Sector (MD) 2006-2012

Source: RNIE Ministry of Economy

The main investor countries in Mexico in 2012 were Japan, with60.1%, followed by the United States with 19.8%, Germany with 19.7% and France with 0.4%. The investments of the four Afore-mentioned countries accounted for total investments received in the terminal automotive sector.

4.4.1 Mexico : A Proven Investment Destination

The renowned quality of Mexican automotive manufacturing has brought many assemblers to Mexico because it represents a unique manufacturing platform for all their markets. Therefore, many models sold around the world are produced exclusively in Mexican plants, such as the Ford Fusion, Lincoln MKZ and Volkswagen Beetle.

Important investments and recent projects have arrived in Mexi-co, for example:

Volkswagen Production of the “Bicentennial” car and the opening of a plant in the state of Guanajuato with a 550 million dollar investment. The plant will produce latest generation diesel engines for Puebla in Mexico and Chattanooga in the US.

Furthermore, in January 2013, Volkswagen Puebla announced a 700 million dollar investment to adapt production lines in the Puebla plant, and acquire new tools for its suppliers. The pur-pose of adapting the plant is to produce the new Golf, which according to the company, will be sent to the North and South American markets.

Ford Diesel engine plant in Chihuahua with an 800 million do-llar investment. This will be the first time that the diesel engine is manufactured in the Americas with flexibility for available alter-native fuel vehicles.

Fiat/Chrysler Toluca is the only plant in North America that manufactures the Fiat 500 model to be sold across the Americas, in addition to being the only plant in the world to produce the Dodge Journey.

201220112010200920082007

OEMs Industry Auto Parts Industry

19

Mazda Construction of a plant to manufacture vehicles and en-gines in the state of Guanajuato, with an investment of approxi-mately 500 million dollars.

Audi In 2012, this luxury assembler revealed its plans to build a new plant in San José, Chiapa, Puebla, which will produce the Q5 model as of 2016.

In addition, Mexico is the leader in systems manufacturing, na-mely: electric parts, transmissions, clutches, engine parts and ve-hicle parts. For example:

Pirelli Tire plant pioneer for the production of the Fiat Tyre in Silao, Guanajuato, with a 210 million dollar investment.

Nissan-Jatco will invest 220 million dollars in a plant to ma-nufacture continuous variable transmissions (CVT) for several car models, creating 200 new jobs in the state of Aguascalientes.

Honda de Mexico announced in May 2013 an investment for a new plant in Celaya, Guanajuato, which will focus on trans-mission manufacturing. The plant will have an annual capacity of 350 thousand units with a plan to double its capacity in the future.

Likewise, in recent years several large investments have been announced to develop larger capacities for the heavy vehicle in-dustry.

A few examples that have been gathered in this document are:

Usui International Manufacturing, announced in 2012 a 10 million dollar investment in a plant in Guanajuato, to produce steel pipes for fuel, brake and general fluid systems for commercial and load vehicles and tractors. The plant will begin operating in late 2014.

Daimler Vehículos Comerciales announced a 19.5 million dollar investment for 2013 to expand its plant in García, Nue-vo León. The investment will serve to expand its facilities and acquire devices, chassis and bodywork assembly tools for long-distance buses.

Navistar-International announced in late 2012 that it would transfer its truck production operations from its plant in Garland, Texas, to its plant in Escobedo, Nuevo León. According to information from the Heavy Duty Manufacturers Association (HDMA), the models manufactured in the Texas plant were the LoneStar, TranStar, WorkStar and PayStar, as well as other vehi-cles that will be produced in Springfield, Ohio.

4.5 International Companies in MexicoThe automotive and auto parts industry in Mexico has been dri-ven by the productive presence of the top ten (light and heavy) vehicle assembly companies in the world, such as General Mo-tors, Ford, Chrysler, Volkswagen, Nissan, Honda, BMW, Toyota, Volvo and Mercedes-Benz. Audi announced recently an inves-tment in Mexico to produce the Q5, joining light vehicle assem-blers in Mexico.

Light vehicles

Commercial vehicles

Engines Autoparts

General Motors Daimler*

CumminsSlightly over one thousand companies

Ford Scania

Chrysler/Fiat Volvo

Nissan DINA

Honda Kenworth

Toyota International

Detroit Diesel

345 companies are Tier 1 suppliers

Volkswagen Volkswagen/MAN

BMW GIANT

Mazda Hino Motors

Isuzu

* Freightliner and Mercedes Benz

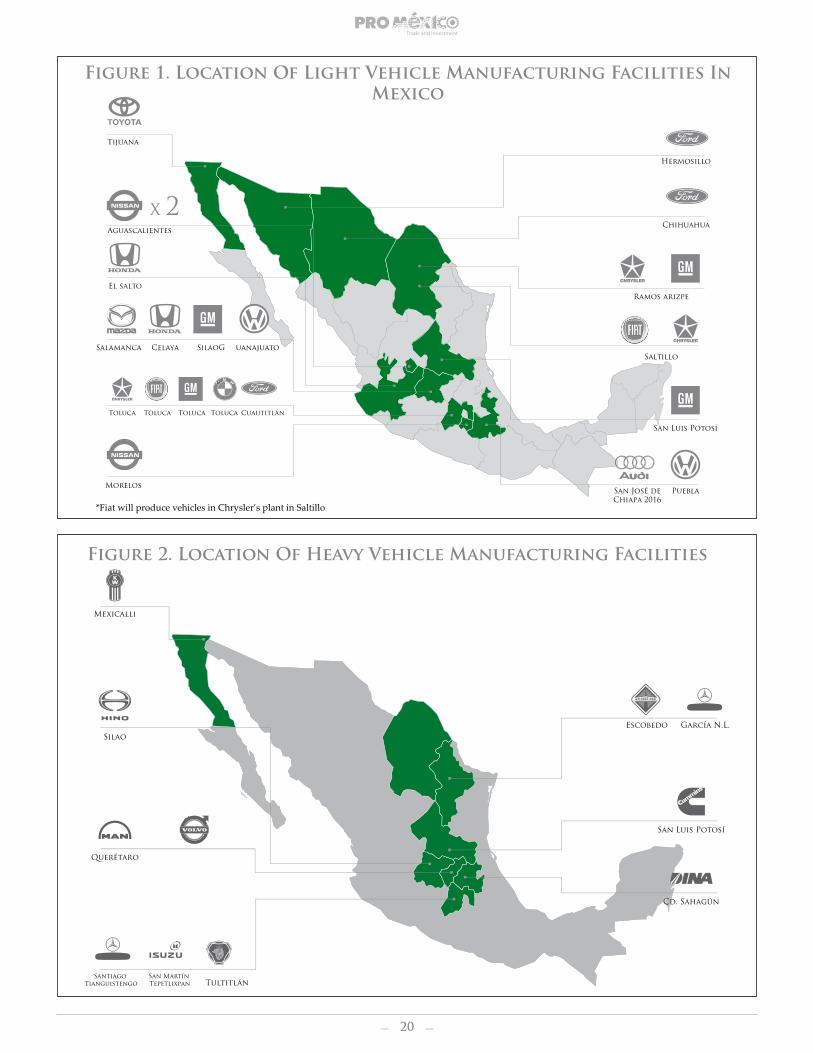

Most of the assembly companies in Mexico have auto parts com-panies located around their vehicle plants to comply with su-pply and delivery deadlines. The leading assemblers of light and heavy vehicles are identified in the following maps.

In the area of commercial vehicles, several companies have pro-duction facilities in Mexico, such as Daimler, Kenworth, Hino, Isuzu, Mercedes-Benz, Volvo, Man, etc.

Table 9 Producing Companies Established In Mexico

Mexico shifted from a simple manufacture

exporting country to an innovation

creator. There are more than 30

automotive design centers in the

country.

20

Figure 1. Location Of Light Vehicle Manufacturing Facilities In Mexico

Figure 2. Location Of Heavy Vehicle Manufacturing Facilities

*Fiat will produce vehicles in Chrysler’s plant in Saltillo

Tijuana

Aguascalientes

El salto

Salamanca

Toluca

Morelos

Toluca Toluca Toluca

Celaya SilaoG uanajuato

Cuautitlán

Puebla

San Luis Potosí

Saltillo

Ramos arizpe

Hermosillo

Chihuahua

San José deChiapa 2016

21

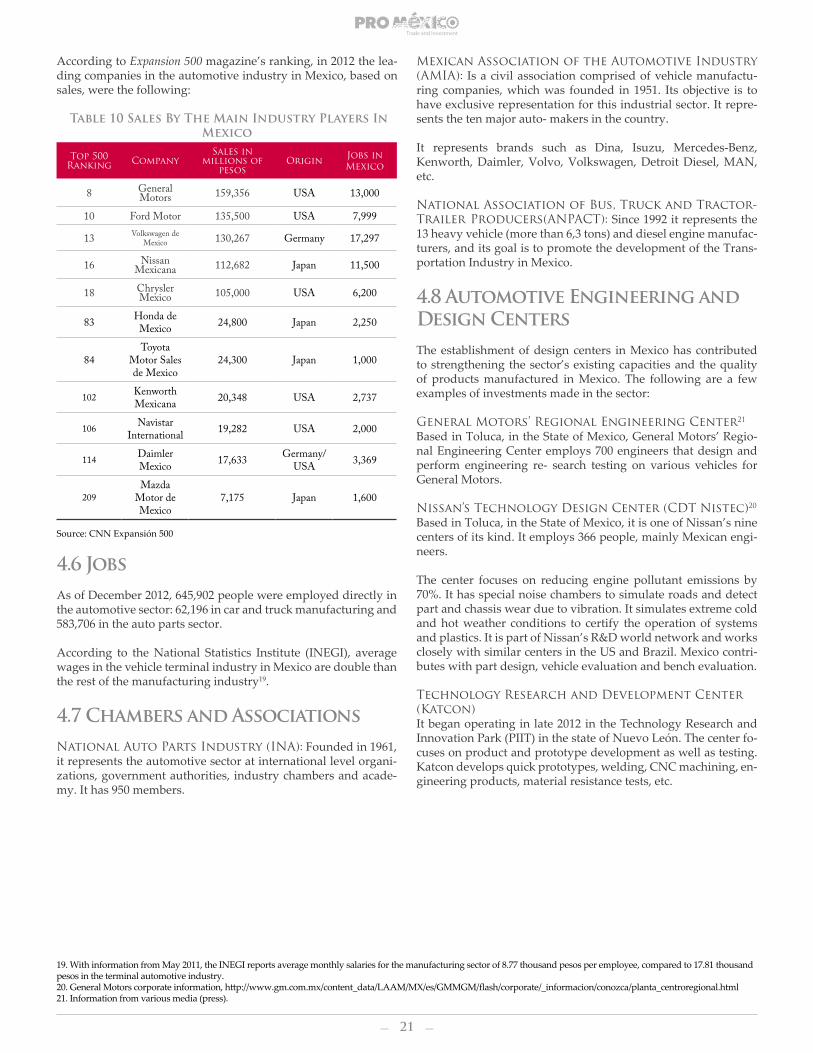

According to Expansion 500 magazine’s ranking, in 2012 the lea-ding companies in the automotive industry in Mexico, based on sales, were the following:

Table 10 Sales By The Main Industry Players In Mexico

Top 500 Ranking Company

Sales in millions of

pesosOrigin Jobs in

Mexico

8 General Motors 159,356 USA 13,000

10 Ford Motor 135,500 USA 7,999

13 Volkswagen de Mexico 130,267 Germany 17,297

16 Nissan Mexicana 112,682 Japan 11,500

18 Chrysler Mexico 105,000 USA 6,200

83 Honda de Mexico 24,800 Japan 2,250

84Toyota

Motor Sales de Mexico

24,300 Japan 1,000

102 Kenworth Mexicana 20,348 USA 2,737

106 Navistar International 19,282 USA 2,000

114 Daimler Mexico 17,633 Germany/

USA 3,369

209Mazda

Motor de Mexico

7,175 Japan 1,600

Source: CNN Expansión 500

4.6 JobsAs of December 2012, 645,902 people were employed directly in the automotive sector: 62,196 in car and truck manufacturing and 583,706 in the auto parts sector.

According to the National Statistics Institute (INEGI), average wages in the vehicle terminal industry in Mexico are double than the rest of the manufacturing industry19.

4.7 Chambers and AssociationsNational Auto Parts Industry (INA): Founded in 1961, it represents the automotive sector at international level organi-zations, government authorities, industry chambers and acade-my. It has 950 members.

19. With information from May 2011, the INEGI reports average monthly salaries for the manufacturing sector of 8.77 thousand pesos per employee, compared to 17.81 thousand pesos in the terminal automotive industry.20. General Motors corporate information, http://www.gm.com.mx/content_data/LAAM/MX/es/GMMGM/flash/corporate/_informacion/conozca/planta_centroregional.html21. Information from various media (press).

Mexican Association of the Automotive Industry (AMIA): Is a civil association comprised of vehicle manufactu-ring companies, which was founded in 1951. Its objective is to have exclusive representation for this industrial sector. It repre-sents the ten major auto- makers in the country.

It represents brands such as Dina, Isuzu, Mercedes-Benz, Kenworth, Daimler, Volvo, Volkswagen, Detroit Diesel, MAN, etc.

National Association of Bus, Truck and Tractor-Trailer Producers(ANPACT): Since 1992 it represents the 13 heavy vehicle (more than 6,3 tons) and diesel engine manufac-turers, and its goal is to promote the development of the Trans-portation Industry in Mexico.

4.8 Automotive Engineering and Design CentersThe establishment of design centers in Mexico has contributed to strengthening the sector’s existing capacities and the quality of products manufactured in Mexico. The following are a few examples of investments made in the sector:

General Motors’ Regional Engineering Center21

Based in Toluca, in the State of Mexico, General Motors’ Regio-nal Engineering Center employs 700 engineers that design and perform engineering re- search testing on various vehicles for General Motors.

Nissan’s Technology Design Center (CDT Nistec)20 Based in Toluca, in the State of Mexico, it is one of Nissan’s nine centers of its kind. It employs 366 people, mainly Mexican engi-neers.

The center focuses on reducing engine pollutant emissions by 70%. It has special noise chambers to simulate roads and detect part and chassis wear due to vibration. It simulates extreme cold and hot weather conditions to certify the operation of systems and plastics. It is part of Nissan’s R&D world network and works closely with similar centers in the US and Brazil. Mexico contri-butes with part design, vehicle evaluation and bench evaluation.

Technology Research and Development Center (Katcon)It began operating in late 2012 in the Technology Research and Innovation Park (PIIT) in the state of Nuevo León. The center fo-cuses on product and prototype development as well as testing. Katcon develops quick prototypes, welding, CNC machining, en-gineering products, material resistance tests, etc.

22

Competitive Advantage Innovation and Develop-ment Center (CiDeVeC)The center belongs to Metalsa, a subsidiary of Grupo Proeza, a chassis manufacturer. The center is constituted by three areas. The first one focuses on designing new products and virtual tes-ting to save costs.

The second area performs material, resistance, wear, lightness and elasticity testing. The third area carries out tests on chassis. The center is located in the PIIT in Nuevo León.

Strategic Product Innovation and Development Center of the Tecnológico de Monterrey (CIDEP)

Its goal is to support new companies and develop prototypes of technology products, as well as to carry out the relevant tests that justify and determine their viability.

The center has labs for reliability, metrology, anechoic chamber, exterior design prototyping, and other tests, and can develop ma-nufacturing processes and numeric design simulations. It serves high technology companies in the micro-electronics, telecom-munications and industrial design sectors in the state of Nuevo León.

Chrysler’s Automotive Research, Development and Engineering Testing Center22

Based in Mexico City, the purpose of this center is to develop and evaluate the new Dodge, Chrysler, Jeep, Mitsubishi and Hyundai vehicles. The center includes the following areas: Vehicle Testing, Labs to measure Pollutant Emissions, Materials and Metrology Engineering Labs, Engine and Transmission dynamometers. It provides direct jobs to 30 engineers specialized in process deve-lopment and validation, in addition to any indirect jobs required by each project.

At the center, world-class engineering tests are preformed, as well as studies of environmentally friendly raw materials and alternative fuel technologies, emission reduction and petroleum derived fuel consumption.

The vehicle testing, research and development area occupies the largest space in the facilities. Its activities include processes to develop, review and test any type of operation: from changes to a part, to partial or total changes to chassis, engine, trans- mission, etc. The center uses up-to-date models, as well as potential vehi-cle concepts for launch in the future.

Center for Research and Technical Assistance of the State of Queretaro (CIATEQ)23 Based in the city of Queretaro, this center was built with the par-ticipation of the federal government represented by Conacyt and LANFI, the government of the state of Queretaro and industrials from the state, headed by executives of Grupo ICA and Grupo SPICER.

CIATEQ performs technology development projects for the au-tomotive and autoparts industry, from basic engineering to the manufacture of purpose machinery and equipment, tools, test benches, control and measurement systems, manufacturing of prototypes and development of specialized vehicles for airports:

Vehicle Electronic Technology Center24

This is an initiative in Guadalajara that results from the agree-ment between the Technological Institute of Occident (ITESO) and the private company Soluciones Tecnológicas. The center develops and integrates electronic systems for automotive appli-cations, in the following areas:

• Testing and systems integration services for testing modules and systems for assembly companies and their suppliers.

• Engineering, design and electronic systems integration ser-vices.

• Technology research and development in electronic systems.

The main users are OEMs and their suppliers that export pro-ducts to North America and Europe; further users are the elec-tronic component and automotive systems software developers and designers as well as universities and other research institutes related to cars, airplanes, boats, electronics and software, especia-lly firmware.

22. Información corporativa Chrysler, http://www.chryslerdemexicoonline.com/company/ingenieria/index.htm23. CONACYT, http://www.ciateq.mx/24. ITESO, http://portal.iteso.mx/portal/page/portal/ITESO/Informacion_Institucional/ITESO_Empresa/Centro_de_tecnologia_electronica_vehicular25. Infomaquila, http://www.youtube.com/watch?v=-yy3kHIhbOM

• Wind tunnel for car radia-tor testing

• Design and manufacture of thermo cycle test bench for the evaluation of charged-air coolers

• Mechanical design of the new ranges of seven models of agricultural tractors

• Design and manufacture of an aluminum mold for tractors

• Angle cutting machine for rubber profile

• Machine to inspect and laser mark engine rings

• Machine for car radiator thermo cycle testing

• Device to inspect the position of headlights

• Machine to test car tires• Crane to assemble power-

train• Machines for secondary

operations in the produc-tion of door seals

• Drill for rubber extruding line

• Zero gravity arm for sus-pension assembly line

• Analysis and simulation of automotive structures

• Machines to test truck dashboards (cluster)

• Template for welding the structure of car seats

• Assembly table for seat frames

• Measurement and veri-fication devices for car window raisers

• Redesign of cooling sys-tems, molds and auxiliary elements for the manu-facture of aluminum auto parts

• Design and manufacture of cabin to apply water-based paint

• Design and construction of a set of machines for secondary operations in the production of seals for car doors.

23

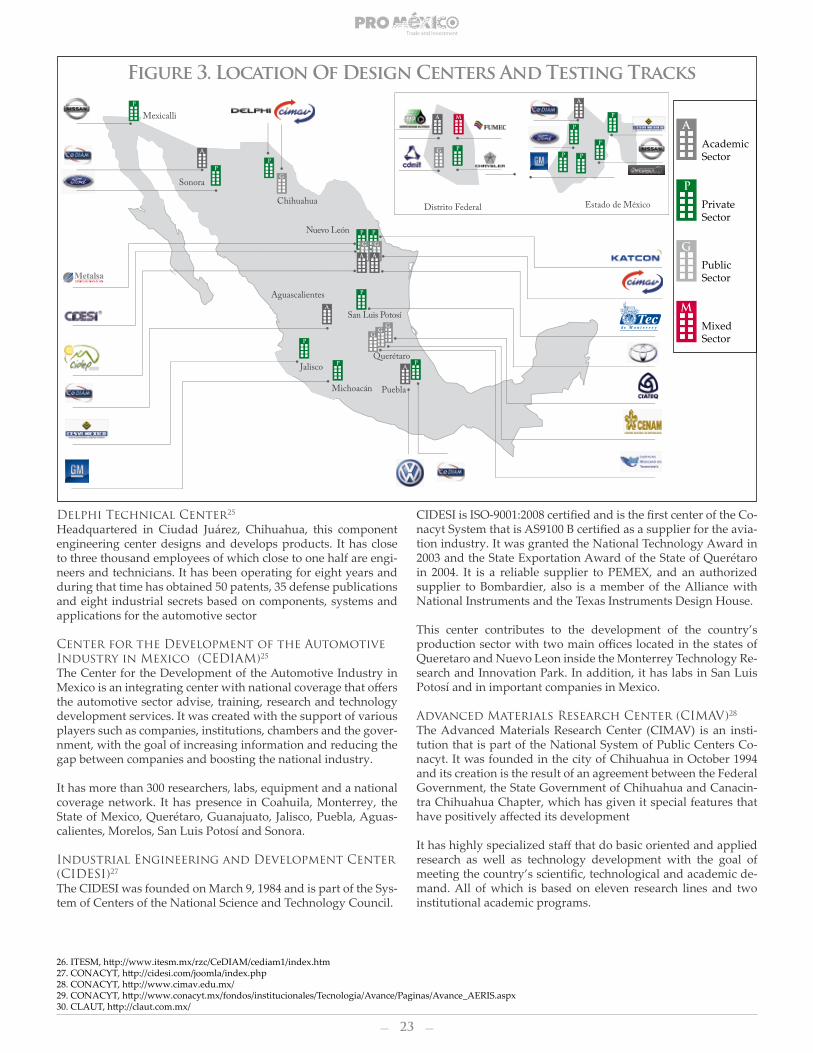

Delphi Technical Center25 Headquartered in Ciudad Juárez, Chihuahua, this component engineering center designs and develops products. It has close to three thousand employees of which close to one half are engi-neers and technicians. It has been operating for eight years and during that time has obtained 50 patents, 35 defense publications and eight industrial secrets based on components, systems and applications for the automotive sector

Center for the Development of the Automotive Industry in Mexico (CEDIAM)25 The Center for the Development of the Automotive Industry in Mexico is an integrating center with national coverage that offers the automotive sector advise, training, research and technology development services. It was created with the support of various players such as companies, institutions, chambers and the gover-nment, with the goal of increasing information and reducing the gap between companies and boosting the national industry.

It has more than 300 researchers, labs, equipment and a national coverage network. It has presence in Coahuila, Monterrey, the State of Mexico, Querétaro, Guanajuato, Jalisco, Puebla, Aguas-calientes, Morelos, San Luis Potosí and Sonora.

Industrial Engineering and Development Center (CIDESI)27 The CIDESI was founded on March 9, 1984 and is part of the Sys-tem of Centers of the National Science and Technology Council.

CIDESI is ISO-9001:2008 certified and is the first center of the Co-nacyt System that is AS9100 B certified as a supplier for the avia-tion industry. It was granted the National Technology Award in 2003 and the State Exportation Award of the State of Querétaro in 2004. It is a reliable supplier to PEMEX, and an authorized supplier to Bombardier, also is a member of the Alliance with National Instruments and the Texas Instruments Design House.

This center contributes to the development of the country’s production sector with two main offices located in the states of Queretaro and Nuevo Leon inside the Monterrey Technology Re-search and Innovation Park. In addition, it has labs in San Luis Potosí and in important companies in Mexico.

Advanced Materials Research Center (CIMAV)28 The Advanced Materials Research Center (CIMAV) is an insti-tution that is part of the National System of Public Centers Co-nacyt. It was founded in the city of Chihuahua in October 1994 and its creation is the result of an agreement between the Federal Government, the State Government of Chihuahua and Canacin-tra Chihuahua Chapter, which has given it special features that have positively affected its development

It has highly specialized staff that do basic oriented and applied research as well as technology development with the goal of meeting the country’s scientific, technological and academic de-mand. All of which is based on eleven research lines and two institutional academic programs.

26. ITESM, http://www.itesm.mx/rzc/CeDIAM/cediam1/index.htm27. CONACYT, http://cidesi.com/joomla/index.php28. CONACYT, http://www.cimav.edu.mx/29. CONACYT, http://www.conacyt.mx/fondos/institucionales/Tecnologia/Avance/Paginas/Avance_AERIS.aspx30. CLAUT, http://claut.com.mx/

A

P

G

M

AcademicSector

PrivateSector

PublicSector

MixedSector

Figure 3. Location Of Design Centers And Testing Tracks

Chihuahua

Sonora

Mexicalli

San Luis Potosí

Nuevo León

Aguascalientes

Michoacán

Jalisco

Puebla

Querétaro

P

P

P

PP

P

P

P

G

G

GG

A

A

A

PA

A

GG

Distrito Federal Estado de México

G P

P

P

P

P P

A

A

M

24

4.9 Other Relevant Initiatives in Automotive Engineering and Design

Strategic Alliances and Innovation Networks (AERIS)29 AERIS is a mechanism promoted by Conacyt that supports com-panies in the planning and constitution of alliances and innova-tion networks with other companies and academic institutions.

Their objective is to position Mexico as a viable global option for automotive R&D, and to promote the development and applica-tion of new technologies in the industry which increase the te-chnical capacity of Mexicans for the creation of new automotive products.

The network’s strategic lines are:• New materials: ultra-light plastics. • Nanotechnology applied to automotive systems.• Development of mathematical simulation models (CAD, CAE,CAM)• Innovation in fuel performance and alternative fuels (electric hybrid)• Vehicle adaptation to Mexico’s specific features

• R&D in electric systems and components• Technology development for HVAC• New technologies applied to manufacturing

Nuevo León Automotive Cluster (CLAUT)30 The Nuevo León Automotive Cluster is a civil association com-prising tier 1 manufacturers of the automotive industry and rela-ted academic and government institutions.

CLAUT seeks the development of the integrated chain from OEMs to tier 1, 2 and 3 suppliers, as well as others that support the automotive industry, such as logistics and consulting service companies, among others.

4.10 Mexico: Consolidation in the International Automotive Industry

The recognized quality of Mexico’s automotive manufacturing has enabled several OEMs to choose Mexico as a unique ma-nufacturing platform for all their destinations. This creates the appropriate industrial environment to manufacture luxury vehi-cles, boosting Mexico as an exclusive platform for OEMs.

25

In recent years, the Mexican industry has shown a shift in trends, going from the maquila of automobiles towards the development of capacities for the integral production of vehicles for specific niches, such as Vehizero and Mastretta.

VehizeroThe company was created in July 1999 by Sean O’Hea, an engi-neer who worked on the project to assemble zero emission units, supported by the National Autonomous University of Mexico (UNAM), the Universidad Iberoamericana and advice from Har-vard experts. Since 2006, the company manufactures, designs, develops and assembles prototypes of hybrid units and vehicles

In early 2008, the Aguascalientes government granted five hecta-res of land for the assembly facilities, with an option to expand to seven additional adjacent hectares. The construction of the plant was supported by Conacyt, Nafin, the Aguascalientes govern-ment and his own resources. Currently, the company manufac-tures and sells the Ecco-C1, Ecco-C2 and Ecco-C3 models.

MastrettaIn November 2007, Mastretta Design built the commercial ver-sion of the first sports car designed and produced by national technicians. The design and creation of the prototype received 2.5 million dollars in investment, of which 15% were contributed by Conacyt. Recently, the Mexican sports car Mastretta MXT was exhibited in the Paris Showroom.

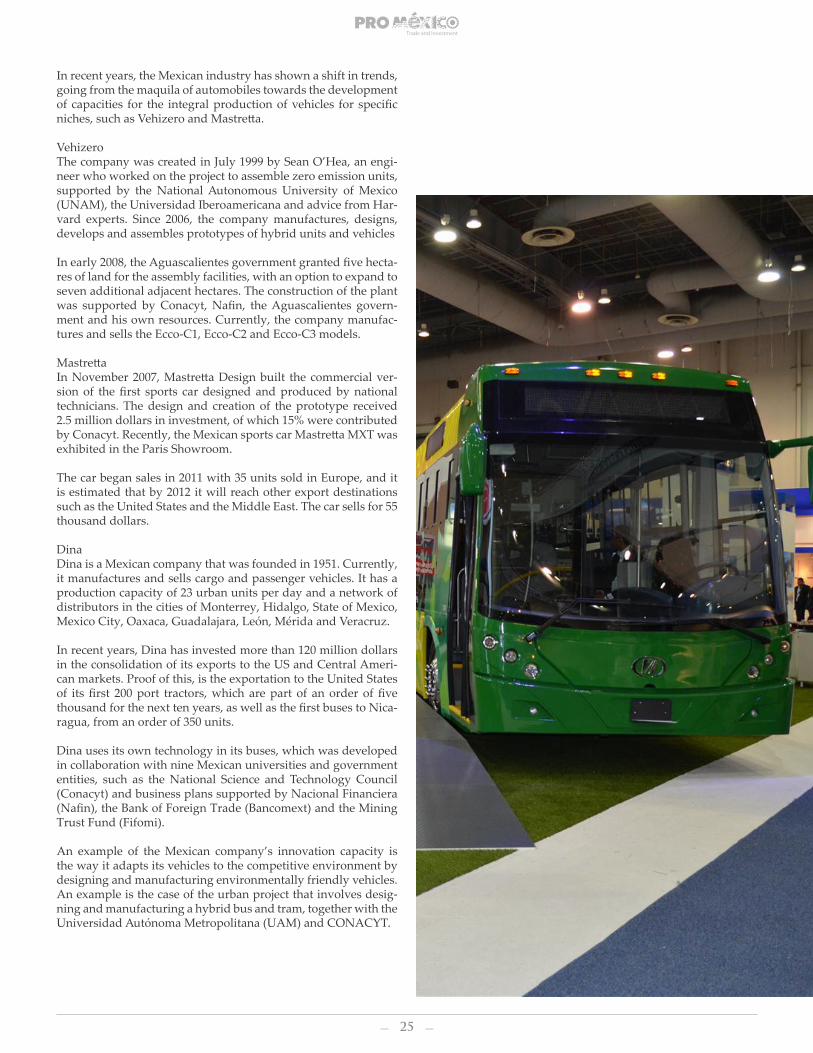

The car began sales in 2011 with 35 units sold in Europe, and it is estimated that by 2012 it will reach other export destinations such as the United States and the Middle East. The car sells for 55 thousand dollars.

DinaDina is a Mexican company that was founded in 1951. Currently, it manufactures and sells cargo and passenger vehicles. It has a production capacity of 23 urban units per day and a network of distributors in the cities of Monterrey, Hidalgo, State of Mexico, Mexico City, Oaxaca, Guadalajara, León, Mérida and Veracruz.

In recent years, Dina has invested more than 120 million dollars in the consolidation of its exports to the US and Central Ameri-can markets. Proof of this, is the exportation to the United States of its first 200 port tractors, which are part of an order of five thousand for the next ten years, as well as the first buses to Nica-ragua, from an order of 350 units.

Dina uses its own technology in its buses, which was developed in collaboration with nine Mexican universities and government entities, such as the National Science and Technology Council (Conacyt) and business plans supported by Nacional Financiera (Nafin), the Bank of Foreign Trade (Bancomext) and the Mining Trust Fund (Fifomi).

An example of the Mexican company’s innovation capacity is the way it adapts its vehicles to the competitive environment by designing and manufacturing environmentally friendly vehicles. An example is the case of the urban project that involves desig-ning and manufacturing a hybrid bus and tram, together with the Universidad Autónoma Metropolitana (UAM) and CONACYT.

26

V Export Business

Case

27

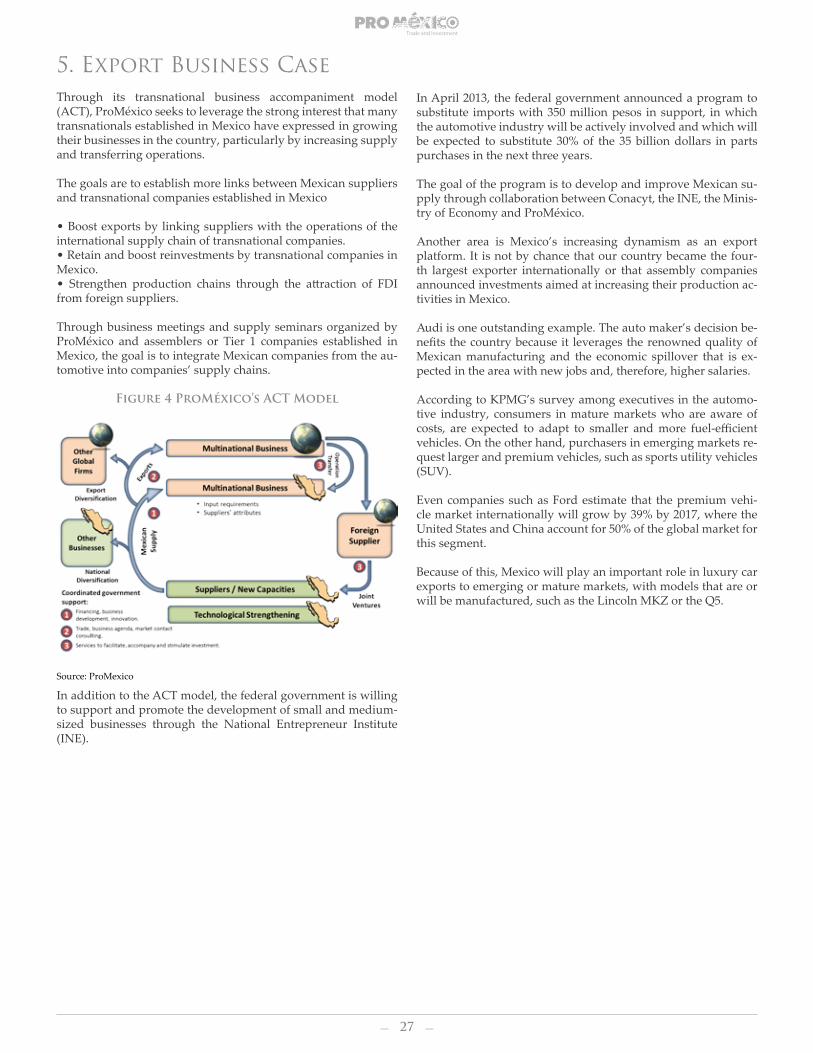

5. Export Business CaseThrough its transnational business accompaniment model (ACT), ProMéxico seeks to leverage the strong interest that many transnationals established in Mexico have expressed in growing their businesses in the country, particularly by increasing supply and transferring operations.

The goals are to establish more links between Mexican suppliers and transnational companies established in Mexico

• Boost exports by linking suppliers with the operations of the international supply chain of transnational companies.• Retain and boost reinvestments by transnational companies in Mexico.• Strengthen production chains through the attraction of FDI from foreign suppliers.

Through business meetings and supply seminars organized by ProMéxico and assemblers or Tier 1 companies established in Mexico, the goal is to integrate Mexican companies from the au-tomotive into companies’ supply chains.

Figure 4 ProMéxico’s ACT Model

Source: ProMexico

In addition to the ACT model, the federal government is willing to support and promote the development of small and medium-sized businesses through the National Entrepreneur Institute (INE).

In April 2013, the federal government announced a program to substitute imports with 350 million pesos in support, in which the automotive industry will be actively involved and which will be expected to substitute 30% of the 35 billion dollars in parts purchases in the next three years.