13-1 CHAPTER 13 McGraw-Hill/Irwin © 2008 The McGraw-Hill Companies, Inc., All Rights Reserved. Cost...

66

13-1 CHAPTER 13 McGraw-Hill/Irwin © 2008 The McGraw-Hill Companies, Inc., All Rights Reserved. Cost Accounting and Reporting Systems

-

Upload

silvester-parsons -

Category

Documents

-

view

217 -

download

0

Transcript of 13-1 CHAPTER 13 McGraw-Hill/Irwin © 2008 The McGraw-Hill Companies, Inc., All Rights Reserved. Cost...

13-1

CHAPTER 13

McGraw-Hill/Irwin © 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Cost Accounting and Reporting Systems

13-2

Decision Making

Strategic, Operational,and Financial (Planning)

Planning and Control Cycle

Executing operational

activities (Managing)

Performance analysis: Plans vs.

actual results (Controlling)

L O 1

Implement Plans

Rev

isit

Pla

ns

Data collection and Performance Feedback

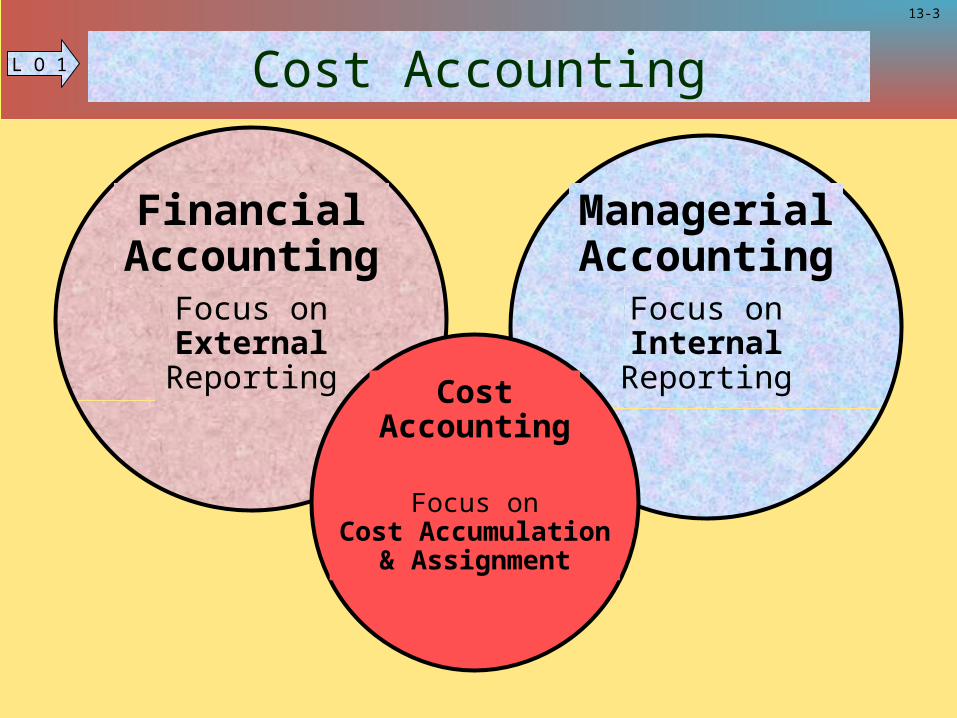

13-3

Cost Accounting

FinancialAccounting

Focus onExternalReporting

ManagerialAccounting

Focus onInternal

ReportingCostAccounting

Focus onCost Accumulation

& Assignment

L O 1

13-4

Costs for Cost Accounting Purposes

Financial Accounting

Cost is a measure of resources used or

given up to achieve a stated purpose.

Financial Accounting

Cost is a measure of resources used or

given up to achieve a stated purpose.

Managerial Accounting

Costs are assigned to products and become

expenses when products are sold.

Managerial Accounting

Costs are assigned to products and become

expenses when products are sold.

L O 1

13-5

Researchand

DevelopmentThe sequence of

functions and activitiesthat, over the lifeof the product or

service, adds valuefor the customer.

Value Chain Functions

Design

Production Marketing Distribution

CustomerService

DesiredROI

L O 2

13-6

Cost Accumulation and Assignment

CostPool

CostObject

Cost Assignment

CostObject

Cost Assignment

CostObject

Cost Assignment

Cost objects are products, jobs, and services.Cost objects are products, jobs, and services.

L O 2

13-7

Direct Costs and Indirect Costs

Direct costs Can be easily and

conveniently traced to a unit of product or other cost objective.

Would not be incurred if the product or activity was discontinued.

Indirect costs Cannot be easily and

conveniently traced to a unit of product or other cost object.

Would be incurred even if the product or activity was discontinued.

L O 3

13-8

Manufacturers . . .Buy raw materials.

Produce and sell finished goods.

Merchandisers . . .Buy finished goods.

Sell finished goods.

MegaLoMart

Costs for Cost Accounting PurposesL O 4

13-9

Merchandiser Current Assets

Cash

Receivables

Prepaid Expenses

Merchandise Inventory

Manufacturer Current Assets

• Cash

• Receivables

• Prepaid Expenses

• InventoriesRaw Materials

Work in Process

Finished Goods

Costs for Cost Accounting PurposesL O 4

13-10

Costs for Cost Accounting Purposes

ManufacturerManufacturer

MerchandiserMerchandiser

Ingredients

Human effort

Machine support

+

+

Balance SheetInventory

Income StatementCost of Goods Sold

= Manufacturedproduct

Purchasedproduct

Sold toCustomers

Sold toCustomers

L O 4

13-11

The ProductThe Product

RawMaterials

RawMaterials

DirectLaborDirectLabor

ManufacturingOverhead

ManufacturingOverhead

Product Costs L O 4

13-12

Raw materials are theingredients of the product.

Example: A radio installed in an automobileExample: A radio installed in an automobile

Product Costs L O 4

13-13

Direct labor is the effort provided by workers who are directly involved with

the manufacture of the product.

Example: Wages paid to automobile assembly workersExample: Wages paid to automobile assembly workers

Product Costs L O 4

13-14

Manufacturing overhead includes all manufacturing costs except raw materials

and direct labor.

Examples

• Wages of maintenance workers, janitors,security guards.

• Production supervision salaries.

• Factory utilities, property taxes, and insurance.

• Depreciation for factory buildings and equipment.

Examples

• Wages of maintenance workers, janitors,security guards.

• Production supervision salaries.

• Factory utilities, property taxes, and insurance.

• Depreciation for factory buildings and equipment.

Product CostsL O 4

13-15

FinishedGoods

Work in Process

Cost of GoodsSold

Direct Labor

Balance Sheet Costs Inventories

Income StatementExpenses

Selling andAdministrative

Period Costs

Raw MaterialsMaterial Purchases

ManufacturingOverhead

Selling andAdministrative

Product Costs and Period Costs L O 4

13-16

Planning andcontrol

functions.

Providingproducts or services tocustomers.

Assessing theefficiency andeffectivenessof operations.

Determining unitmanufacturing

costs.

Cost accounting systems provide the

INFORMATIONthat supports successful decision-making.

Cost Accounting SystemsL O 5

13-17

Discloseinventoriesand cost ofgoods sold.

Track resourcesconsumed byproducts and

services.

Manage activitiesthat consume

resources.

Evaluate andreward

employeeperformance.

Cost accounting systems are the proceduresand techniques used by management.

Cost Accounting SystemsL O 5

13-18

THE JOB

Rawmaterial

Direct labor

Traced directly to each job

Traced directly

to each job

Manufacturingoverhead (OH)

Applied to eachjob using a

predeterminedrate

Cost Accounting SystemsL O 5

13-19

Estimated total manufacturingoverhead cost for the coming period

Estimated total units in theallocation base for the coming period

POHR =

The predetermined overhead rate (POHR) used to apply overhead to jobs is

determined before the period begins.

Ideally, the allocation base is a cost driver that causes overhead.

Cost Accounting SystemsL O 6

13-20

Overhead applied = POHR × Actual activity

Actual amount of the cost driver such as units produced, direct labor hours, or machine hours

incurred during the period.

Based on estimates, and determined before

the period begins.

Cost Accounting SystemsL O 6

13-21

Cruisers, Inc., applies overhead based on direct labor hours. Total estimated

overhead for the year is $4,200,000. Total estimated labor hours are 300,000.

What is Cruisers’ predeterminedoverhead rate?

Cost Accounting SystemsL O 6

13-22

For each direct labor hour worked on a job, $14.00 of factory overhead will be

applied to the job.

POHR = $14.00 per DLH

$4,200,000

300,000 direct labor hours (DLH)POHR =

Estimated total manufacturingoverhead cost for the coming period

Estimated total units in theallocation base for the coming period

POHR =

Cost Accounting SystemsL O 6

13-23

Cost Accounting Systems

Cruisers, Inc., produced 86 SeaCruiser sailboats during the month working a total of 20,640 labor hours and incurring these costs: raw materials $368,510; and direct

labor $330,240.

What is the cost per SeaCruiser sailboat?

L O 6

13-24

Cost Accounting Systems

Raw Materials 368,510$ Direct Labor 330,240 Overhead 20,640 DLH × $14 per DLH 288,960 Total manufacturing cost incurred 987,710$

Cost per boat $987,710 ÷ 86 boats 11,485$

Raw Materials 368,510$ Direct Labor 330,240 Overhead 20,640 DLH × $14 per DLH 288,960 Total manufacturing cost incurred 987,710$

Cost per boat $987,710 ÷ 86 boats 11,485$

L O 6

13-25

What will Cruisers do if

actual and applied overhead

are not equal?

Cost Accounting SystemsL O 6

13-26

Cost Accounting Systems

Cruisers’ actual overhead for the year was $4,250,000 for a total of 310,000 direct labor hours.

How much total overhead was applied to Cruisers’ jobs during the year? Use Cruisers’ predetermined

overhead rate of $14.00 per direct labor hour.

L O 6

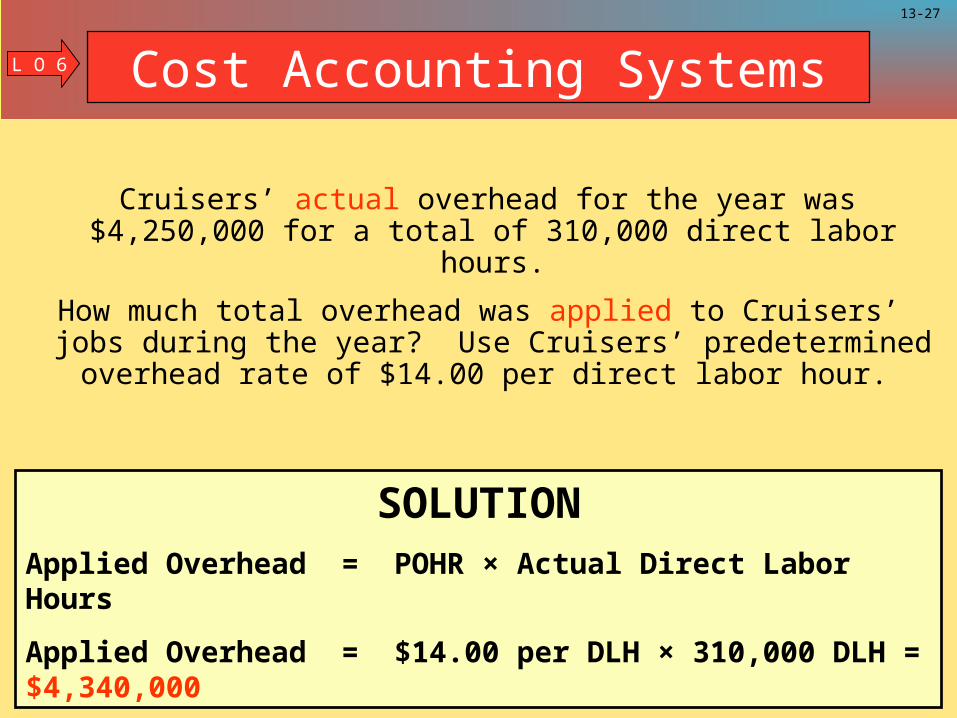

13-27

Cruisers’ actual overhead for the year was $4,250,000 for a total of 310,000 direct labor hours.

How much total overhead was applied to Cruisers’ jobs during the year? Use Cruisers’ predetermined

overhead rate of $14.00 per direct labor hour.

Cost Accounting Systems

SOLUTIONApplied Overhead = POHR × Actual Direct Labor Hours

Applied Overhead = $14.00 per DLH × 310,000 DLH = $4,340,000

L O 6

13-28

Cruisers’ actual overhead for the year was $4,250,000 for a total of 310,000 direct labor hours.

How much total overhead was applied to Cruisers’ jobs during the year? Use Cruisers’ predetermined

overhead rate of $13.00 per direct labor hour.

Cost Accounting Systems

SOLUTIONApplied Overhead = POHR × Actual Direct Labor Hours

Applied Overhead = $14.00 per DLH × 310,000 DLH = $4,340,000

Applied Overhead $4,340,000Actual Overhead $4,250,000Overapplied by $90,000

Overhead has been overapplied for the year. What will Cruisers do?

L O 6

13-29

Work inProcess

FinishedGoods

Cost of Goods Sold

$90,000may be allocated

to these accounts.

$90,000 may beclosed directly to

cost of goods sold.

Cost of Goods Sold

Smaller amounts

OR

Cost Accounting SystemsL O 6

13-30

Alternative 1 Alternative 2If Manufacturing Close to Cost Overhead is . . . of Goods Sold Allocation

UNDERAPPLIED INCREASE INCREASECost of Goods Sold Work in Process

(Applied OH is less Finished Goodsthan actual OH) Cost of Goods Sold

OVERAPPLIED DECREASE DECREASECost of Goods Sold Work in Process

(Applied OH is greater Finished Goodsthan actual OH) Cost of Goods Sold

Smaller amounts

Cost Accounting SystemsL O 6

13-31

Let’s examine the cost flows in a

product costing system. We will use T-accounts and start with

materials.

Cost Accounting SystemsL O 6

13-32

Raw MaterialsMaterial

PurchasesDirect

Materials

Direct Materials

Mfg. Overhead

Indirect Materials

Work in Process

Indirect Materials

Actual Applied

Cost Accounting SystemsL O 6

13-33

Next let’s add labor costs and

applied manufacturing overhead to the cost flows. Are you with me?

Cost Accounting SystemsL O 6

13-34

Direct Labor

Mfg. Overhead

Salaries and Wages Payable Work in Process

Direct

Materials

OverheadApplied to

Work inProcess

IndirectLabor

Direct Labor

Overhead Applied

IndirectLabor

Indirect Materials

Actual AppliedIf actual and applied

manufacturing overheadare not equal, a year-end adjustment is required.

If actual and applied manufacturing overheadare not equal, a year-end adjustment is required.

Cost Accounting SystemsL O 6

13-35

Now let’s complete the

goods and sell them. Still with

me?

Cost Accounting SystemsL O 6

13-36

Cost ofGoodsMfd.

Finished Goods

Cost ofGoodsSold

Cost ofGoodsMfd.

Cost of Goods Sold

Cost ofGoodsSold

Work in ProcessDirect

MaterialsDirect

LaborOverhead

Applied

Cost Accounting SystemsL O 6

13-37

A schedule of cost of goods manufactured is prepared to assist

managers in understanding and

evaluating the overall cost of manufacturing

products.

A schedule of cost of goods manufactured is prepared to assist

managers in understanding and

evaluating the overall cost of manufacturing

products.

Cost Accounting SystemsL O 7

13-38

Use the following informationto prepare a statement of cost

of goods manufactured for Cruisers, Inc. for the month of April:

Raw materials inventory:

March 31 $126,900

April 30 $106,250

Raw materials purchases:

April $347,860

Direct labor costs: $330,240

MOH Applied: $288,960

Assume no WIP inventories

Use the following informationto prepare a statement of cost

of goods manufactured for Cruisers, Inc. for the month of April:

Raw materials inventory:

March 31 $126,900

April 30 $106,250

Raw materials purchases:

April $347,860

Direct labor costs: $330,240

MOH Applied: $288,960

Assume no WIP inventories

Cost Accounting SystemsL O 7

13-39

Cost Accounting SystemsL O 7

13-40

The cost of goods manufactured

during the period is used to compute

cost of goods sold for the period.

The cost of goods manufactured

during the period is used to compute

cost of goods sold for the period.

Beginning and ending

finished goods

inventory amounts

are assumed values.

Beginning and ending

finished goods

inventory amounts

are assumed values.

L O 7 Cost Accounting Systems

13-41

The income statement is

prepared using

established financial

accounting procedures.

Sales andexpense numbers

are assumed amounts.

Sales andexpense numbers

are assumed amounts.

L O 7 Cost Accounting Systems

13-42

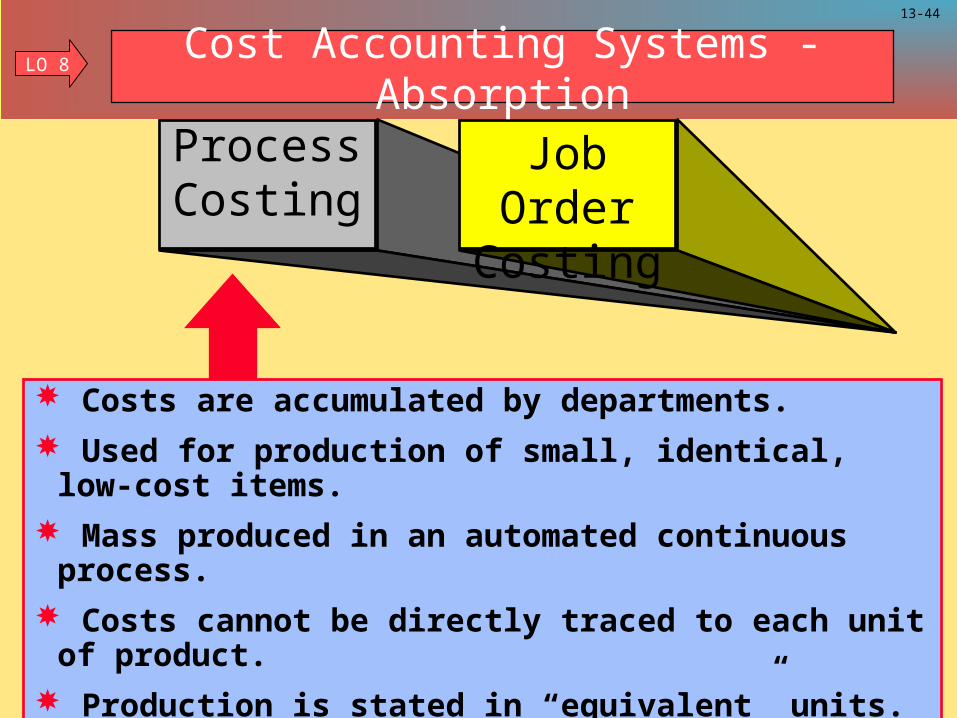

ProcessCosting

Job OrderCosting

Costs are accumulated by job.

Used for production of large, unique, high-cost items.

Built to order rather than mass produced.

Many costs can be directly traced to each job.

Cost Accounting Systems - AbsorptionL O 8

13-43

Typical job order cost applications: Special-order printing Building construction

Also used in service industries Hospitals Law firms

ProcessCosting

Job OrderCosting

LO 8 Cost Accounting Systems - Absorption

13-44

Costs are accumulated by departments.

Used for production of small, identical, low-cost items.

Mass produced in an automated continuous process.

Costs cannot be directly traced to each unit of product.

Production is stated in “equivalent” units.

ProcessCosting

Job OrderCosting

LO 8 Cost Accounting Systems - Absorption

13-45

Typical process cost applications:

Petrochemical refinery

Paint manufacturer

Paper mill

ProcessCosting

Job OrderCosting

L O 8 Cost Accounting Systems - Absorption

13-46

Direct Materials

Direct Labor

Variable Manufacturing Overhead

Fixed Manufacturing Overhead

Variable Selling and Administrative Expenses

Fixed Selling and Administrative Expenses

VariableCosting

AbsorptionCosting

ProductCosts

PeriodCosts

ProductCosts

PeriodCosts

Cost Accounting SystemsL O 8

Absorption Costing and Variable Costing

13-47

Variable costing

Balance Sheet Costs Inventories

Income StatementExpenses

Cost of GoodsSold

Selling andAdministrativePeriod Costs

Work in Process

FinishedGoods

Raw Materials

VariableManufacturing

Overhead

Material Purchases

Direct Labor

Selling andAdministrative

FixedManufacturing

Overhead

Absorption costin

g

Absorption and Variable CostingL O 8

13-48

Fixed costs arenot really the costs

of any particularproduct.

VariableCosting

AbsorptionCosting

All manufacturingAll manufacturingcosts must be assignedcosts must be assignedto products to properlyto products to properlymatch revenues andmatch revenues and

costs.costs.

Absorption and Variable CostingL O 8

13-49

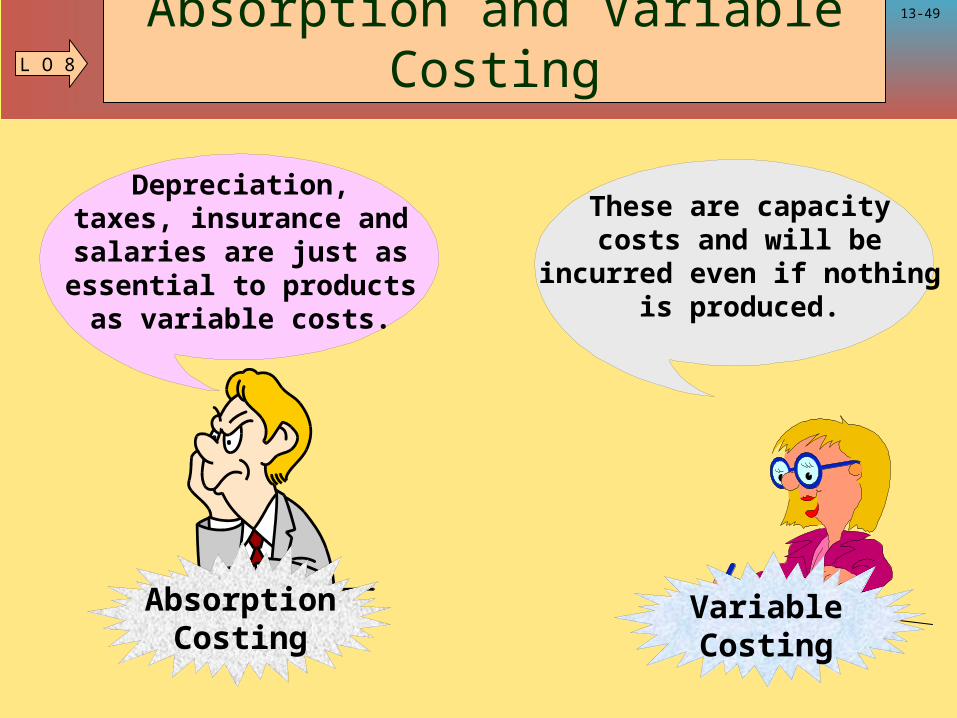

AbsorptionCosting

These are capacitycosts and will be

incurred even if nothingis produced.

VariableCosting

Depreciation,taxes, insurance andsalaries are just as

essential to productsas variable costs.

Absorption and Variable CostingL O 8

13-50

VariableCosting

Absorptioncosting product costs

are misleading fordecision making.

They are the numbers that appear on our

external reports.

AbsorptionCosting

Absorption and Variable CostingL O 8

13-51

A

B CA

CB

Activity-Based Costing (ABC)L O 9

13-52

One of the most difficult tasks in

computing accurate unit costs lies in determining the

proper amount of overhead cost that should be assigned

to each job.

Assigningoverhead is

difficult. I agree!

Activity-Based Costing (ABC)L O 9

13-53

Level of C

omplexity

Overhead Allocation

Traditional Plantwide Overhead

Rate

Activity-Based Costing (ABC)L O 9

AA

CB

13-54

In the ABC method, we recognize that many

activities within a department drive overhead costs.

In the ABC method, we recognize that many

activities within a department drive overhead costs.A

B CA

CB

Activity-Based Costing (ABC)L O 9

13-55

Identify activities and assign costs to those activities.

Central idea . . .

Products require activities.

Activities consume resources.

Activity-Based Costing (ABC)

A

B CA

CB

L O 9

13-56

More detailed measures of costs. Better understanding of activities. More accurate product costs for . . .

– Pricing decisions.– Product elimination decisions.– Managing activities that cause costs.

Benefits should always be compared tocosts of implementation.

The Benefits of ABCL O 9

13-57

Most cost drivers are related to either volume or complexity of production.

Examples: machine time, machine setups, purchase orders, production orders.

Three factors are considered in choosing a cost driver:

Causal relationship.

Benefits received.

Reasonableness.

Identifying Cost Drivers L O 9

13-58

Overhead Actual Rate Activity×

Rate = Estimated overhead costs in activity cost pool

Estimated number of activity units

1. Identify activities that consume resources.

2. Assign costs to a cost pool for each activity.

3. Identify cost drivers associated with each activity.

4. Compute overhead rate for each cost pool:

5. Assign costs to products:

Activity-Based Costing ProceduresL O 9

13-59

Let’s look at anexample comparingtraditional costing

with ABC. We will start with

traditional costing.

Activity-Based CostingL O 9

13-60

Cruisers, Inc. manufactures sailboats and canoes. Overhead is applied at the rate of $14 per direct

labor hour. Production for May was 100 sailboats requiring 24,000 hours, and 1,000 canoes requiring

13,000 hours.

Overhead applied using traditional costing is:

Sailboats CanoesDirect labor hours (DLH) 24,000 13,000 Overhead rate per DLH 14$ 14$ Overhead applied 336,000$ 182,000$

Traditional Costing vs. ABCL O 9

13-61

Estimated Annual

Activity CostProduction orders 135,000$ 180 orders 750$ per orderHull & deck setup 2,140,000 1,000 setups 2,140 per setupRaw material acquisition 650,000 26,000 receipts 25 per receiptMaterial handling 450,000 9,000 moves 50 per moveQuality inspection 750,000 6,000 inspections 125 per inspectionCleanup & waste disposal 75,000 250 loads 300 per loadTotal Overhead 4,200,000$

Estimated TotalActivity

Predetermined rateper unit of activity

Activity-Based Costing

Same amount of annual total overhead used earlier in the chapter.Same amount of annual total overhead used earlier in the chapter.

Cruisers plans to adopt activity-based costing and identifies these activities and costs for computing overhead rates.

L O 9

13-62

Using the following activity center data, determine the amount of overhead applied to the two

products using activity-based costing.

ActivityProduction orders 13 orders 1 orderHull & deck setup 103 setups 1 setupRaw material acquisition 222 receipts 10 receiptsMaterial handling 732 moves 50 movesQuality inspection 408 inspections 1,000 inspectionsCleanup & waste disposal 20 loads 20 loads

Sailboats CanoesActivity Required

Activity-Based CostingL O 9

13-63

Activity-Based Costing

Let’s complete the table.

Actual Cost Actual Cost Units of Allocated Units of Allocated

Activity Rate Activity to Product Activity to ProductProduction orders 750$ per order 13 9,750$ 1 750$ Hull & deck setup 2,140 per setup 103 ? 1 ?Raw material acquisition 250 per receipt 222 ? 10 ?Material handling 50 per move 732 ? 50 ?Quality inspection 125 per inspection 408 ? 1,000 ?Cleanup & waste disposal 300 per load 20 ? 20 ?Total Overhead ? ?

Cost Allocated to Product = Actual Units of Activity × Rate

Sailboats Canoes

L O 9

13-64

Activity-Based Costing

Actual Cost Actual Cost Units of Allocated Units of Allocated

Activity Rate Activity to Product Activity to ProductProduction orders 750$ per order 13 9,750$ 1 750$ Hull & deck setup 2,140 per setup 103 220,420 1 2,140 Raw material acquisition 250 per receipt 222 55,500 10 2,500 Material handling 50 per move 732 36,600 50 2,500 Quality inspection 125 per inspection 408 51,000 1,000 125,000 Cleanup & waste disposal 300 per load 20 6,000 20 6,000 Total Overhead 379,270$ 138,890$

Cost Allocated to Product = Actual Units of Activity × Rate

Sailboats Canoes

L O 9

13-65

This result is not uncommon when activity-based costing is used. Many companies have found that lower volume, more complex products have greater overhead

costs than previously realized.

Traditional Costing ABCSailboats Canoes Sailboats Canoes

Overhead applied 336,000$ 182,000$ 379,270$ 138,890$

Comparison of Overhead Applied

Activity-Based CostingL O 9

13-66

End of Chapter 13