1296015303_CA_TM_Chapter_22_Eng

15

28 Chapter 22 Absorption and Marginal Costing Notes to teachers 1 This chapter largely builds on the concepts of fixed costs vs. variable costs, manufacturing overheads vs. non-manufacturing overheads, and product costs vs. period costs introduced in Chapter 20, and the absorption of overheads introduced in Chapter 21. 2 The curriculum only requires the preparation of manufacturing accounts and income statements under absorption costing and marginal costing, respectively. The preparation of other financial statements such as the balance sheet is not required. 3 Note that the manufacturing account is a financial statement and not a ledger account. 4 Teachers should ask students to identify on their own the differences between the financial statements prepared under the two costing methods, instead of just teaching the points stated in Section 22.5. 5 The most difficult part of this chapter is reconciling and explaining the different net profits calculated under the two costing methods. 6 The income statements prepared under marginal costing and the contribution margin concept involved are important for the break-even analysis and business decisions to be made in the subsequent chapters. Q1 Product contribution margin refers to the excess of sales revenue over the variable cost of goods sold. Total contribution margin refers to the excess of sales revenue over all variable costs incurred. Q2 Income Statement for the month $ $ Sales (2,000 × $50) 100,000 Less Variable manufacturing cost of goods sold [2,000 × ($8 + $6 + $5)] (38,000) Product contribution margin (a) 62,000 Less Variable selling overheads (2,000 × $3) (6,000) Total contribution margin (b) 56,000 Less Fixed factory overheads 20,000 Fixed selling overheads 16,000 Administrative overheads 4,000 (40,000) Net profit 16,000 Notes to teachers

Transcript of 1296015303_CA_TM_Chapter_22_Eng

28

Chapter 22 Absorption and Marginal Costing

Notestoteachers

1 This chapter largely builds on the concepts of fixed costs vs. variable costs, manufacturing overheads vs. non-manufacturing overheads, and product costs vs. period costs introduced in Chapter 20, and the absorption of overheads introduced in Chapter 21.

2 The curriculum only requires the preparation of manufacturing accounts and income statements under absorption costing and marginal costing, respectively. The preparation of other financial statements such as the balance sheet is not required.

3 Note that the manufacturing account is a financial statement and not a ledger account.

4 Teachers should ask students to identify on their own the differences between the financial statements prepared under the two costing methods, instead of just teaching the points stated in Section 22.5.

5 The most difficult part of this chapter is reconciling and explaining the different net profits calculated under the two costing methods.

6 The income statements prepared under marginal costing and the contribution margin concept involved are important for the break-even analysis and business decisions to be made in the subsequent chapters.

Q1 Product contribution margin refers to the excess of sales revenue over the variable cost of goods sold. Total contribution margin refers to the excess of sales revenue over all variable costs incurred.

Q2 Income Statement for the month

$ $Sales(2,000×$50) 100,000Less Variablemanufacturingcostofgoodssold[2,000×($8+$6+$5)] (38,000)Productcontributionmargin(a) 62,000Less Variablesellingoverheads(2,000×$3) (6,000)Totalcontributionmargin(b) 56,000Less Fixedfactoryoverheads 20,000 Fixedsellingoverheads 16,000 Administrativeoverheads 4,000 (40,000)Netprofit 16,000

Notestoteachers

29

Q3 The differences between the income statements prepared under absorption and marginal costing include:

• The income statement prepared under absorption costing classifies costs by function: manufacturing and non-manufacturing. In contrast, the income statement prepared under marginal costing classifies costs into fixed and variable costs.

• Under absorption costing, all the manufacturing costs (variable and fixed) are included in the valuation of inventory. Under marginal costing, only variable manufacturing costs are included in the valuation of inventory.

• Under absorption costing, the cost of goods sold includes all the manufacturing costs (variable and fixed). Under marginal costing, only variable manufacturing costs are included in the cost of goods sold.

• The income statement prepared under absorption costing shows the gross profit, which is the excess of sales revenue over all the manufacturing costs (variable and fixed) of goods sold. The income statement prepared under marginal costing shows the total contribution margin, which is the excess of sales revenue over all the variable costs incurred, regardless of whether they are manufacturing or non-manufacturing.

• Net profit is both defined as the excess of revenues over all costs and expenses incurred in the same period under absorption costing and marginal costing. However, the resulting net profit figures are different. This is due to different costs being absorbed by inventory.

Q4 The net profit reported under absorption costing will be higher when the inventory level increases during the accounting period. Conversely, the net profit reported under absorption costing will be lower when the inventory level decreases during the accounting period.

Q5 Unit contribution margin = Total contribution margin ÷ Sales volume = $52,000 ÷ 800 = $65

Change in net profit = Change in sales volume × Unit contribution margin = –200 × $65 = –$13,000

Net profit will be reduced by $13,000 if the sales volume decreases by 200 units.

Q6 See text, Section 22.6.

A1 Cost of goods sold = $30,500

Gross profit = $49,500

Net profit = $30,500

A2 The statement is incorrect. Under marginal costing, only variable manufacturing costs are absorbed by inventories.

30

A3 Under absorption costing:

Baby Toys Income Statement for the year ended 31 March 2012

$ $Sales 100,000Less Costofgoodssold: Openinginventory 8,000 Add Manufacturingcostofgoodscompleted 40,000 Costofgoodsavailableforsale 48,000 Less Closinginventory($40,000×200÷1,000) (8,000) (40,000)Grossprofit 60,000Less Marketingcosts[(1,000×$5)+$15,000] (20,000)Netprofit 40,000

Under marginal costing:Baby Toys

Income Statement for the year ended 31 March 2012

$ $Sales 100,000Less Variablecostofgoodssold: Openinginventory 6,000 Add Variablemanufacturingcostofgoodscompleted 30,000 Variablecostofgoodsavailableforsale 36,000 Less Closinginventory($30,000×200÷1,000) (6,000) (30,000)Productcontributionmargin 70,000Less Variablemarketingcosts(1,000×$5) (5,000)Totalcontributionmargin 65,000Less Fixedmanufacturingcosts 10,000 Fixedmarketingcosts 15,000 (25,000)Netprofit 40,000

The net profit figures reported by both costing methods are the same.

A4 The net profit reported under absorption and marginal costing will be the same when the inventory level remains unchanged during the accounting period.

A5 Ways to prevent managers from manipulating profits by producing more units of output than needed include:

• Set a target inventory level for managers to achieve.

• Use the profits reported under marginal costing as the basis for performance evaluation.

• Use other criteria (other than reported profits) for performance evaluation.

(Any other reasonable answer)

A6 Net profit under absorption costing − Net profit under marginal costing

= (Fixed manufacturing overheads included in closing inventory of work-in-progress under absorption costing − Fixed manufacturing overheads included in opening inventory of work-in-progress under absorption costing)

+ (Fixed manufacturing overheads included in closing inventory of finished goods under absorption costing − Fixed manufacturing overheads included in opening inventory of finished goods under absorption costing)

= [($4,800 × 100 ÷ 800) − $0] + [($4,200* × 50 ÷ 700) − $0]

= $600 + $300

= $900 (i.e., $11,650 − $10,750)

* $4,800 − ($4,800 × 100 ÷ 800) (fixed manufacturing overheads absorbed by closing inventory of work-in-progress)

31

ASSESSMENT

Short QuestionsShort Questions

22.1(a) Under absorption costing, inventories absorb all the costs of manufacturing, regardless of whether they

are fixed or variable.

Under marginal costing, inventories absorb only variable manufacturing costs.

(b) Reported profits under absorption costing and marginal costing will be the same when production volume equals sales volume.

If production volume exceeds sales volume, reported profits under absorption costing will be higher.

Conversely, if production volume is lower than sales volume, reported profits under marginal costing will be higher.

22.2XAbsorption costing. Under absorption costing, all manufacturing costs (fixed or variable) that are incurred to bring the goods into saleable condition are treated as product costs. They are written off to the profit and loss account when the goods are sold. If the goods remain unsold at the end of an accounting period, their product costs will be carried forward to the next period as inventories. However, under marginal costing, all fixed manufacturing costs are written off to the profit and loss account as they are incurred, regardless of whether the goods are sold or not.

Application Problems

22.3 Global Manufacturing Co Manufacturing Account for the year ended 31 March 2011

$ $Openinginventoryofrawmaterials 24,000Add Purchases 213,400 Carriageinwards 3,210 216,610 240,610Less Closinginventoryofrawmaterials (26,200)Costofrawmaterialsconsumed 214,410Manufacturingwages 132,800Primecost 347,210Factoryoverheads:Factorywaterandelectricity 23,000 Factoryrent 62,200 Othermanufacturingexpenses 14,300 99,500 446,710Add Openingwork-in-progress 9,550 456,260Less Closingwork-in-progress (8,700)Manufacturingcostofgoodscompleted 447,560

32

22.4X Best Toys Co Manufacturing Account for the year ended 31 August 2011

$ $Openinginventoryofrawmaterials 56,200Add Purchases 222,000 Carriageinwards 6,100 228,100 284,300Less Closinginventoryofrawmaterials (84,100)Costofrawmaterialsconsumed 200,200Manufacturingwages 145,220Primecost 345,420Factoryoverheads:Factoryrent($80,000×70%) 56,000 Factoryutilities($35,000×70%) 24,500 Generalmanufacturingexpenses 38,790 119,290 464,710Add Openingwork-in-progress 8,110 472,820Less Closingwork-in-progress (10,330)Manufacturingcostofgoodscompleted 462,490

22.5 ProductA ProductB TotalBudgeteddirectlabourhoursperunit 1.5 2Totalbudgeteddirectlabourhours 15,000 16,000 31,000Fixedproductionoverheads $124,000Fixedproductionoverheadsperdirectlabourhour $4

Productioncostsperunit: $ $ Directmaterialscost 8 10 Directlabourcost 9 12 Variableproductionoverheads 5 6 Fixedproductionoverheads 6 8 28 36

(a) (i) Under absorption costing:

Budgeted Income Statement for the year ended 31 December 2010

ProductA ProductB Total $ $ $Sales(W1) 332,500 300,000 632,500Less Costofgoodssold: Manufacturingcostofgoodscompleted(W2) 280,000 288,000 568,000 Less Closinginventory(W3) (14,000) (18,000) (32,000) 266,000 270,000 536,000

Grossprofit 66,500 30,000 96,500Less Fixedadministrativeoverheads (95,000)Netprofit 1,500

Workings:

(W1) Product A = 9,500 × $35 = $332,500 Product B = 7,500 × $40 = $300,000

(W2) Product A = 10,000 × $28 = $280,000 Product B = 8,000 × $36 = $288,000

(W3) Product A = $280,000 × [(10,000 − 9,500) ÷ 10,000] = $14,000

Product B = $288,000 × [(8,000 − 7,500) ÷ 8,000] = $18,000

33

(ii) Under marginal costing:

Budgeted Income Statement for the year ended 31 December 2010

ProductA ProductB Total $ $ $Sales 332,500 300,000 632,500Less Variablecostofgoodssold: Variablemanufacturingcostofgoodscompleted(W4) 220,000 224,000 444,000 Less Closinginventory(W5) (11,000) (14,000) (25,000) 209,000 210,000 419,000

Contributionmargin 123,500 90,000 213,500Less Fixedproductionoverheads (124,000) Fixedadministrativeoverheads (95,000)Netloss (5,500)

(W4) Product A = 10,000 × $22 = $220,000

Product B = 8,000 × $28 = $224,000

(W5) Product A = $220,000 × [(10,000 − 9,500) ÷ 10,000] = $11,000

Product B = $224,000 × [(8,000 − 7,500) ÷ 8,000] = $14,000

(b) Net profit under absorption costing − Net profit under marginal costing

= Fixed production overheads included in closing inventory under absorption costing

− Fixed production costs included in opening inventory under absorption costing

= [(500 × $6) − $0] + [(500 × $8) − $0]

= $7,000 [$1,500 − (–$5,500)]

22.6XProduction costs per unit: $Variablemanufacturingcosts 18Fixedmanufacturingcosts($168,000÷12,000) 14 32

(a) (i) Under absorption costing:

Budgeted Income Statement for the year ended 31 December 2010

$ $Sales (12,600×$38) 478,800Less Costofgoodssold: Openinginventory(1,000×$32) 32,000 Add Manufacturingcostofgoodscompleted(12,000×$32) 384,000 416,000 Less Closinginventory[$384,000×(1,000+12,000–12,600)÷12,000] (12,800) (403,200)Grossprofit 75,600Less Fixedsellinganddistributionoverheads (78,000)Netloss (2,400)

34

(ii) Under marginal costing:

Budgeted Income Statement for the year ended 31 December 2010

$ $Sales 478,800Less Costofgoodssold: Openinginventory(1,000×$18) 18,000 Add Variablemanufacturingcostofgoodscompleted(12,000×$18) 216,000 234,000 Less Closinginventory[$216,000×(1,000+12,000–12,600)÷12,000] (7,200) (226,800)Contributionmargin 252,000Less Fixedmanufacturingcosts 168,000 Fixedsellinganddistributionoverheads 78,000 (246,000)Netprofit 6,000

(b) Net profit under absorption costing − Net profit under marginal costing

= Fixed manufacturing costs included in closing inventory under absorption costing − Fixed manufacturing costs included in opening inventory under absorption costing

= (400 × $14) − (1,000 × $14)

= –$8,400 (i.e., –$2,400 − $6,000)

22.7 In Question 22.5, marginal costing reports a lower net profit because of an increase in inventory. Under absorption costing, some fixed manufacturing costs are absorbed into the closing inventory. As a result, the net profit reported under absorption costing is higher.

In Question 22.6X, marginal costing reports a higher net profit because of a decrease in inventory. Under absorption costing, some fixed manufacturing costs of the previous year are released from the opening inventory while a portion of fixed manufacturing costs incurred in the current year are absorbed by the closing inventory. When the inventory level falls, the amount of fixed manufacturing costs released exceeds the amount absorbed (assuming fixed manufacturing costs per unit remain the same). As a result, the net profit reported under absorption costing is lower.

22.8X(a) Under marginal costing:

Budgeted Income Statement for the year ended 31 December 2011

$ $Sales(38,000×$45) 1,710,000Less Variablecostofgoodssold: Variablemanufacturingcostofgoodscompleted[40,000×($8+$10+$6)] 960,000 Less Closinginventory[$960,000×(40,000–38,000)÷40,000] (48,000) (912,000)Contributionmargin 798,000Less Fixedmanufacturingoverheads 120,000 Non-manufacturingoverheads 80,000 (200,000)Netprofit 598,000

35

Budgeted Income Statement for the year ended 31 December 2012

$ $Sales(42,000×$45) 1,890,000Less Variablecostofgoodssold: Openinginventory 48,000 Add Variablemanufacturingcostofgoodscompleted(40,000×$24) 960,000 (1,008,000)Contributionmargin 882,000Less Fixedmanufacturingoverheads 120,000 Non-manufacturingoverheads 80,000 (200,000)Netprofit 682,000

(b) Under absorption costing:

Budgeted Income Statement for the year ended 31 December 2011

$ $Sales 1,710,000Less Costofgoodssold: Manufacturingcostofgoodscompleted{40,000×[$24+($120,000÷40,000)]} 1,080,000 Less Closinginventory[$1,080,000×(40,000–38,000)÷40,000] (54,000) (1,026,000)Grossprofit 684,000Less Non-manufacturingoverheads (80,000)Netprofit 604,000

Budgeted Income Statement for the year ended 31 December 2012

$ $Sales 1,890,000Less Costofgoodssold: Openinginventory 54,000 Add Manufacturingcostofgoodscompleted(40,000×$27) 1,080,000 (1,134,000)Grossprofit 756,000Less Non-manufacturingoverheads (80,000)Netprofit 676,000

22.9 $ per unitSelling price ($1,200,000 ÷ 40,000) 30Direct materials ($600,000 ÷ 40,000) 15 Direct labour ($240,000 ÷ 40,000) 6Variable factory overheads ($120,000 ÷ 40,000) 3Fixed factory overheads ($100,000 ÷ 40,000) 2.5

(a) (i) Under absorption costing:

Income Statement for the year ended 31 March 2011

$ $Sales(35,000×$30) 1,050,000Less Costofgoodssold: Manufacturingcostofgoodscompleted(W1) 1,007,000 Less Closinginventory(W2) (79,500) 927,500 Add Under-absorptionoffixedfactoryoverheads(W3) 5,000 (932,500)Grossprofit 117,500Less Fixedadministrativeoverheads (60,000)Netprofit 57,500

36

Workings:

(W1) 38,000 × ($15 + $6 + $3 + $2.5) = $1,007,000

(W2) (38,000 − 35,000) × $26.5 = $79,500

(W3) $100,000 − (38,000 × $2.5) = $5,000

(ii) Under marginal costing:

Income Statement for the year ended 31 March 2011

$ $Sales 1,050,000Less Variablecostofgoodssold: Variablemanufacturingcostofgoodscompleted(W4) 912,000 Less Closinginventory(W5) (72,000) (840,000)Contributionmargin 210,000Less Fixedfactoryoverheads 100,000 Fixedadministrativeoverheads 60,000 (160,000)Netprofit 50,000

(W4) 38,000 × ($15 + $6 + $3) = $912,000

(W5) (38,000 − 35,000) × $24 = $72,000

(b) Difference in net profit = $80,000 − $50,000 = $30,000 lower

This is due to:

5,000 (Budgeted 40,000 − Actual 35,000) units × Contribution of $6 ($30 − $24) per unit = $30,000

22.10X(a) Absorption costing.

When the inventory level increases during the year, a higher net profit figure would be reported under absorption costing than under marginal costing. This is because with absorption costing, some of the fixed manufacturing costs of the previous year are released from the opening inventory while a portion of fixed manufacturing costs incurred during the current year are absorbed by the closing inventory. In our case, the amount of fixed manufacturing costs released is lower than the amount absorbed. This leads to a higher net profit figure.

(b) Net profit under absorption costing − Net profit under marginal costing

= Fixed manufacturing costs included in closing inventory under absorption costing − Fixed manufacturing costs included in opening inventory under absorption costing

= ($240,000 × 5,800 ÷ 50,000) − ($240,000 × 4,600 ÷ 50,000)

= $27,840 − $22,080

= $5,760

Net profit reported under marginal costing

= $66,000 − $5,760

= $60,240

(c) Under absorption costing, the net profit figure can be manipulated by changing the inventory level. Managers who are evaluated on the basis of profits earned using the absorption cost approach may be tempted to produce more units of output than needed. This will result in an undesirable buildup of inventories, which will in turn hurt a company’s profitability and liquidity in the long term.

37

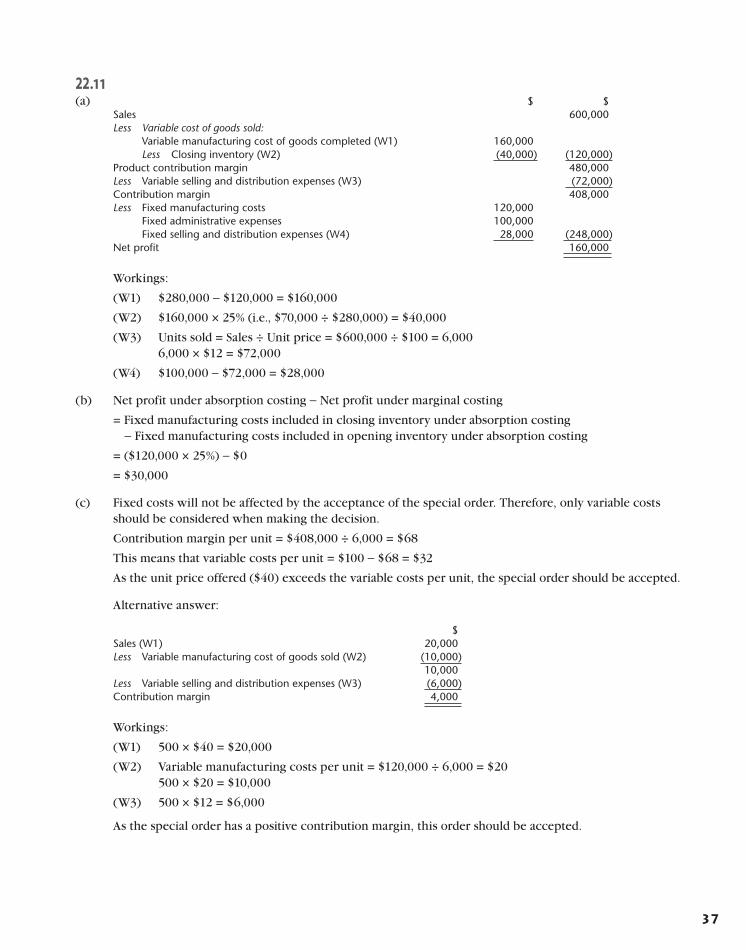

22.11(a) $ $

Sales 600,000Less Variablecostofgoodssold: Variablemanufacturingcostofgoodscompleted(W1) 160,000 Less Closinginventory(W2) (40,000) (120,000)Productcontributionmargin 480,000Less Variablesellinganddistributionexpenses(W3) (72,000)Contributionmargin 408,000Less Fixedmanufacturingcosts 120,000 Fixedadministrativeexpenses 100,000 Fixedsellinganddistributionexpenses(W4) 28,000 (248,000)Netprofit 160,000

Workings:

(W1) $280,000 − $120,000 = $160,000

(W2) $160,000 × 25% (i.e., $70,000 ÷ $280,000) = $40,000

(W3) Units sold = Sales ÷ Unit price = $600,000 ÷ $100 = 6,000 6,000 × $12 = $72,000

(W4) $100,000 − $72,000 = $28,000

(b) Net profit under absorption costing − Net profit under marginal costing

= Fixed manufacturing costs included in closing inventory under absorption costing − Fixed manufacturing costs included in opening inventory under absorption costing

= ($120,000 × 25%) − $0

= $30,000

(c) Fixed costs will not be affected by the acceptance of the special order. Therefore, only variable costs should be considered when making the decision.

Contribution margin per unit = $408,000 ÷ 6,000 = $68

This means that variable costs per unit = $100 − $68 = $32

As the unit price offered ($40) exceeds the variable costs per unit, the special order should be accepted.

Alternative answer:

$Sales(W1) 20,000Less Variablemanufacturingcostofgoodssold(W2) (10,000) 10,000Less Variablesellinganddistributionexpenses(W3) (6,000)Contributionmargin 4,000

Workings:

(W1) 500 × $40 = $20,000

(W2) Variable manufacturing costs per unit = $120,000 ÷ 6,000 = $20 500 × $20 = $10,000

(W3) 500 × $12 = $6,000

As the special order has a positive contribution margin, this order should be accepted.

38

(d) Non-financial factors that should be considered include:

• Relationship with the customer

• Pressure from other customers to cut prices

(Any other reasonable answer)

22.12X(a) $ $

Sales(W1) 60,000Less Variablecostofgoodssold: Variablemanufacturingcostofgoodscompleted(W4) 10,000 Less Closinginventory(balancingfigure) (1,000) 9,000 Variablemarketingcosts(W3) 11,000 (20,000)Contributionmargin(W2) 40,000Less Fixedmanufacturingcosts 12,000 Fixedmarketingcosts 10,000 (22,000)Netprofit(balancingfigure) 18,000

Workings:

(W1) Total Accounts Receivable

$ $Balanceb/f 8,000 Cash/Bank 58,000Sales(balancingfigure) 60,000 Balancec/f 10,000 68,000 68,000

(W2) $60,000 × 2 ÷ 3 = $40,000

(W3) $21,000 − $10,000 = $11,000

(W4) $22,000 − $12,000 = $10,000

(b) Break-even point in sales revenue

= Fixed costs ÷ Contribution margin ratio

= $22,000 ÷ 2/3

= $33,000

(c) Net profit under absorption costing − Net profit under marginal costing

= Fixed manufacturing costs included in closing inventory under absorption costing − Fixed manufacturing costs included in opening inventory under absorption costing

= ($12,000 × 1,000 ÷ 10,000) − $0

= $1,200

Net profit under absorption costing = $18,000 + $1,200 = $19,200

Alternative answer: $ $Sales 60,000Less Costofgoodssold: Manufacturingcostofgoodscompleted($10,000+$12,000) 22,000 Less Closinginventory(Workings) (2,200) (19,800)Grossprofit 40,200Less Marketingcosts($11,000+$10,000) (21,000)Netprofit 19,200

39

Workings: $22,000 × 10% (i.e., $1,000 ÷ $10,000) = $2,200

(d) Net profit would increase by $4,000 (Contribution margin $40,000 × 10%), assuming the unit price and existing cost behaviour remain unchanged.

(e) The net profit would be reduced, but not as much as $100,000. Investment in plant and equipment is a capital expenditure and should not be wholly written off in the period in which it is incurred. Only a portion, known as depreciation, is to be written off in each period the plant and equipment is in use.

Past Exam QuestionsPast Exam Questions

22.14(a) Absorption Marginal

$ $Directmanufacturinglabour($20×1.5hrs) 30.00 30.00Directmaterials 13.25 13.25Variablemanufacturingoverhead 10.50 10.50Fixedmanufacturingoverhead($176,000÷12,800) 13.75 —Totalcostperunit 67.50 53.75

(b) Absorption Marginal $ $Openinginventory — —Costofgoodsmanufactured: 12,800×$67.5 864,000 — 12,800×$53.75 — 688,000Costofgoodsavailableforsale 864,000 688,000Costofgoodssold: 9,600×$67.5 (648,000) — 9,600×$53.75 — (516,000)Closinginventory 216,000 172,000

(c) Absorption costing income statement: $ $Sales(9,600×$85.5) 820,800Costofgoodssold(9,600×$67.5) (648,000)Grossmargin 172,800Less Variablesellingexpenses(9,600×$4.8) 46,080 Fixedsellingandadministrativecosts 86,500 (132,580)Operatingincome 40,220

Marginal costing income statement: $ $Sales(9,600×$85.5) 820,800Variablecostofgoodssold(9,600×$53.75) 516,000Variablesellingexpenses(9,600×$4.8) 46,080 (562,080)Contributionmargin 258,720Fixedcosts:Manufacturingoverhead 176,000 Sellingandadministrativecosts 86,500 (262,500)Operatingincome (3,780)

40

(d) (i) When sales are equal to production, net income will be the same in both the absorption costing and marginal costing systems.

(ii) When production exceeds sales, the absorption costing system will show a higher profit than the marginal costing system.

(iii) When sales exceed production, the marginal costing system will show a higher profit than the absorption costing system.

22.15X(a) Jimmy Company Profit and Loss Account for the year ended 30 June 2005

$ $Sales(18,750units) 1,875,000Less Costofsales: Variablecosts($575,000×30,000÷15,000) 1,150,000 Fixedcosts 700,000 1,850,000 Less Closingstock($1,850,000×11,250÷30,000) (693,750) (1,156,250)Grossprofit 718,750Sellingandadministration($325,000+$100,000) (425,000)SalarypackageofBennyTunner {$200,000+[($718,750–$425,000–$200,000)×20%]} (218,750)Netprofit 75,000

(b) Change in profitability: Lossin2003/04 ($100,000) Profitin2004/05 $75,000 Increaseinprofit $175,000

The main causes for the changes are:

(i) Deferring fixed costs through accumulation of stock ($700,000 × 11,250 ÷ 30,000) $262,500

(ii) Increase in contribution from sales increase {3,750 × [($1,500,000 − $575,000) ÷ 15,000]} $231,250

Offset by:

(i) Increase in fixed costs ($100,000)

(ii) Salary package of Benny Tunner ($218,750)

(c) No.

Fixed costs and salary package increased by $318,750.

Increase in amount of closing stock.

(d) Key features of marginal costing:

(i) Variable production costs are charged to cost units.

(ii) All fixed costs of the period are written off in full against the aggregate contribution.

Key features of absorption costing:

(i) All manufacturing costs, variable or fixed, are considered as costs of production and inventories.

(ii) Fixed manufacturing costs are charged to the units produced on the basis of the per unit fixed manufacturing overhead rate.

41

22.16(a) Operating Statement (Using Absorption Costing) for the year ended 31 December

2006 2007 $000 $000Sales 6,300 8,100Less Productioncostsofsales: Openinginventory — 700 Add Variableproductioncostsandoverheadcosts 3,360 3,040 Fixedproductionoverheadcosts 840 760 4,200 4,500 Less Closinginventory($4,200,000×7,000÷42,000) (700) — 3,500 4,500Under-/(Over-)absorbedfixedproductioncosts (40) 40 3,460 4,540

Grossprofit 2,840 3,560

Less Variablenon-productionoverheadcosts 280 360 Fixednon-productionoverheadcosts 150 150 430 510

Netprofit 2,410 3,050

Operating Statement (Using Marginal Costing) for the year ended 31 December

2006 2007 $000 $000Sales 6,300 8,100Less Variableproductioncostsofsales: Openinginventory — 560 Add Variableproductioncostsandoverheadcosts 3,360 3,040 3,360 3,600 Less Closinginventory($3,360,000×7,000÷42,000) (560) — 2,800 3,600 Variablenon-productionoverheadcosts 280 360 3,080 3,960

Contribution 3,220 4,140

Less Fixedproductionoverheadcosts 800 800 Fixednon-productionoverheadcosts 150 150 950 950

Netprofit 2,270 3,190

(b) The profits reported for 2006 and 2007 are reconciled as follows: 2006 2007 $000 $000Absorptioncostingprofit 2,410 3,0502006—Decreaseinclosinginventoryvaluation(7,000units×$20) (140) —2007—Decreaseinopeninginventoryvaluation(7,000units×$20) — 140Marginalcostingprofit 2,270 3,190

42

(c) The reasons for using marginal costing system in preparing management accounts include:

• Marginal costing is simple to operate as it does not require complex apportionments and calculation of overhead absorption rates.

• Fixed costs are incurred on a time basis and are thus charged wholly as expenses in the period they occur rather than as part of the product cost.

• Changes in production volume do not affect the unit cost of inventory which comprises only variable production costs.

• Marginal costing operating statements are more useful for making short-term decisions as they provide better information about expected profit which is obtained from the use of contribution margin.

(Any two)