122 October 2009CER The Voice of European Railways The future of railways in Europe What shall we...

17

1 22 October 2009 CER The Voice of European Railways The future of railways in Europe What shall we do? International Conference on the Future of Railway Transport in Europe October 29th, Budapest Dr Libor Lochman

-

Upload

magdalene-reed -

Category

Documents

-

view

216 -

download

0

Transcript of 122 October 2009CER The Voice of European Railways The future of railways in Europe What shall we...

122 October 2009 CER

The Voice of European Railways

The future of railways in EuropeWhat shall we do?

International Conference on the Future of Railway Transport in Europe

October 29th, Budapest

Dr Libor Lochman

222 October 2009 CER

The Voice of European Railways

CER – representing the railway sector in Brussels

CER stands for…

The Community of European Railway and Infrastructure Companies (CER) brings together 75 railway undertakings and infrastructure companies from the European Union, the accession countries (Croatia, Macedonia and Turkey) as well as from the Western Balkan countries, Norway, and Switzerland

CER is based in Brussels and represents the interests of its members to the European Parliament, Commission and Council of Ministers as well as other policymakers and transport actors

CER`s main focus is to promote a strong rail industry that is essential to the creation of a sustainable transport system which is efficient, effective and environmentally sound.

...therefore, we are the Voice of European Railways

322 October 2009 CER

The Voice of European Railways

Future? Clear government objective needed:RAIL or NO RAIL

Upward spiral Downward spiral- Government takes responsibility for infrastructure provision (as for road infrastructure) - public authorities – cities, regions, state – take responsibility for public service (as for busses)

1. rail freight companies able to

compete with road on equal par2. revenues can be reinvested in business 3. rail competitiveness increases4. fair chance for incumbent to compete with other companies

- rail infrastructure paid by tolls from rail operators OR infrastructure ill-maintained - freight services pay for passen- ger public services OR public

services close

1. rail freight competitiveness

decreases against road freight2. rail freight volumes shift to

road3. rail freight revenues decrease4. Market unattractive to outside investments

422 October 2009 CER

The Voice of European Railways

Target: An efficient and successful railway system

BUT

Three commonly held (mis)beliefs:

A. Competition on its own will lead to the self-regulating power of the market and lead to the revitalisation of rail mode

B. As soon as incumbent railway companies are organisationally restructured and infrastructure is split off from railway service providers, competition will automatically start working and solve the problems of the rail market

C. Charges for the use of railway infrastructure can to a large extend replace investments from the state

522 October 2009 CER

The Voice of European Railways

0

20000

40000

60000

80000

100000

Year

thou

sand

s to

ns

CFR Marfa

Private rail operators

Total

Example: Romania – freight volumes versus

market share of new entrants

MISBELIEF A: ‘Competition on its own will lead to the self-regulating to the revitalisation of rail mode’

622 October 2009 CER

The Voice of European Railways

Separation

- infrastructure is less market driven

- complicated regulation of interface between infra-structure and operations

- high transaction costs

- non-discriminatory access is more obvious

- clearer use of public money

- market / client driven

- integrated system that takes account of inter-dependencies

- no transaction costs

- returns-to-scale technology (especially in uncertain world)

- incentives for IMs

- Competent cooperation partner for other railways

Integration

MISBELIEF B: ‘Infrastructure separation from railway brings competition and solves problems of the rail market

722 October 2009 CER

The Voice of European Railways

Direct loss from rail PSO transport increases every year

Cross- subsidisation from freight and

low passenger infrastructure

charges

Less income for network

maintenance, renewal,

investment and rolling stock

Rail freight

becomes less

attractivefor customers

Deterioration of the quality of public service transport

Downward spiral of indebtedness /

competitiveness…

MISBELIEF C: ‘Track access charges can replace investments from the state’

BUT:

Rail services will continue to deteriorate because it cannot compete with road if road users do not pay similar road tolls

822 October 2009 CER

The Voice of European Railways

Reversing the downward spiralling trend…what to do about it?

Raising track access charges further not an option: already at the maximum of what the market can bear in most CEE countries

Capitalize on best practices from abroad to enhance railways competitiveness– Dutch and Swedish model

– High level of investments in the rail infrastructure– Adequate financing of Public Service Obligations (for

passenger services)– Low rail infrastructure charges (almost equal to those

applied to road)– Swiss model

– Mobilize revenues through progressive implementation of ‘polluter pays’ principles for all modes

– Infrastructure fund to allocate these revenues to most sustainable transport options

922 October 2009 CER

The Voice of European Railways

Thus: Stable financial architecture necessarytoday: a vicious circle that matters to all

*TAC= track access charges Source: CER, 2009

Insufficient finances for infrastructure

Insufficient government funding for rail infrastructure

Regulated industry with limited commercial freedom

Accumulation of debt and debt

service payments

High TAC* for rail freight (cross-

subsidization of PSO traffic)

Decline in rail infrastructure quality

Loss of rail freight and passenger traffic

Loss of income and ability to invest

Unfair conditions for

inter-modal competition

(road undercharged)

Historic Debt

Insufficient revenue from rail passenger services leads to low

passenger TAC* (PSO under-compensation)

1022 October 2009 CER

The Voice of European Railways

Rail ‘financial architecture’: a clear legal requirement in EU law!

financing infrastructure adequate compensation of PSO

(and rolling stock)

treatment of historical debt

Art. 6 (1) Dir 2001/14

MS shall ensure the accounts of an IM shall at least balance income from infrastructure charges, surpluses from other commercial activities and State funding on the one hand, and infrastructure expenditure on the other

Art. 1 (1) Reg. 1370/2007competent authorities to compensate public service operators for costs incurred in return for the discharge of public service obligationsParag.6 third indent of Annexthe costs of the public service must be balanced by operating revenues and payments from public authorities

Art. 9 Dir. 91/440MS shall set up appropriate mechanisms to help reduce the indebtedness of such undertakings to a level which does not impede sound financial management and improve their financial situation

1122 October 2009 CER

The Voice of European Railways

A successful railway system in future?

… the RAILWAYS make efforts to achieve better quality, productivity and efficiency and are vitally supported in their efforts by politics…

Market Opening / Competition

Fair Competition between modes

Modern railInfrastructure

Introduce market ope-ning and competition but

in the context of

Equal treatment in taxation and charging between all modes of

transport

Provision of adequate infrastructure is the responsibility of the

national state

Integrated policy concept

1222 October 2009 CER

The Voice of European Railways

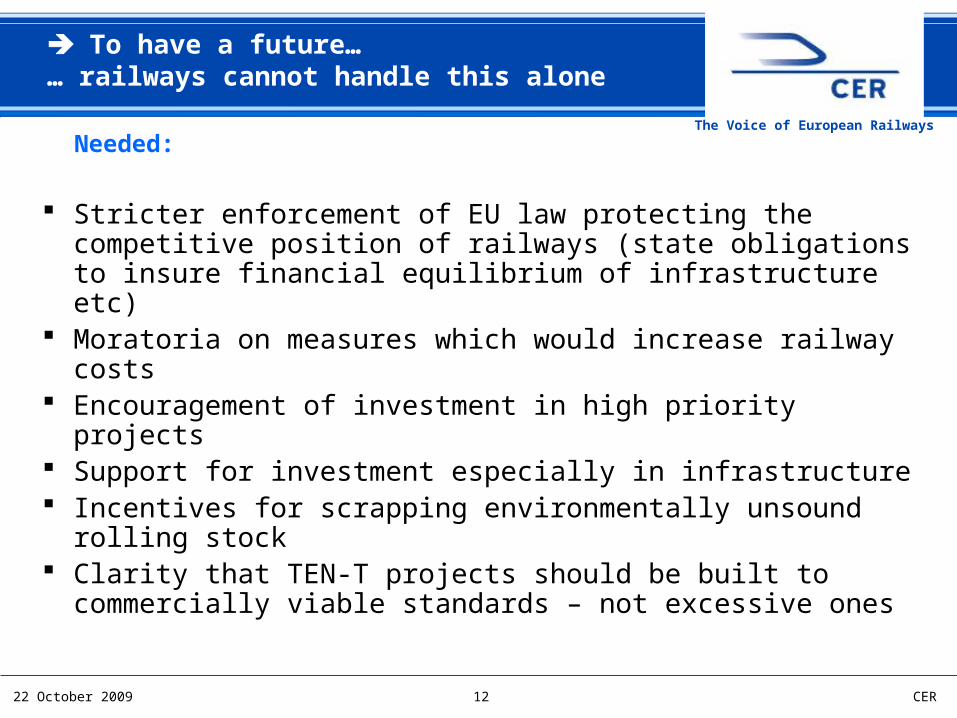

To have a future…… railways cannot handle this alone

Stricter enforcement of EU law protecting the competitive position of railways (state obligations to insure financial equilibrium of infrastructure etc)

Moratoria on measures which would increase railway costs

Encouragement of investment in high priority projects

Support for investment especially in infrastructure Incentives for scrapping environmentally unsound

rolling stock Clarity that TEN-T projects should be built to

commercially viable standards – not excessive ones

Needed:

1322 October 2009 CER

The Voice of European Railways

… or maybe not?Option unacceptable to Europe’s ambitions

Unacceptable political cost:> in contradiction to the EU transport policy of the last 20 years

Unacceptable economic cost:> medium and long distance rail services would go to air and road = massive congestion of airports and roads = enormous (road) infrastructure costs (road congestion costs now already 3% of EU GDP)> sprawling cities throughout Europe = not enough road infrastructure capacity = migration of work force (incl. related costs)

Unacceptable social cost:> ca. 1 million of direct employment from rail in Europe > greater social inequality (less public transport)

Unacceptable environmental cost:> more polluting modes take over market = increasingly impossible to reach CO2 reduction targets > increased transport accidents, noise, air pollution…

1422 October 2009 CER

The Voice of European Railways

CER’s input to the next White Paper

The Commission should develop a plan for reducing CO2 emissions from transport

The plan needs to be ambitious and to be based on a consideration of all possible instruments

In order to provide incentives for innovation, appropriate investment and demand management, prices for all modes should be adjusted to adequately reflect the costs of transport to society

full internalisation of external costs should be introduced for all modes of transport and not be limited largely to rail (e.g. ETS)

1522 October 2009 CER

The Voice of European Railways

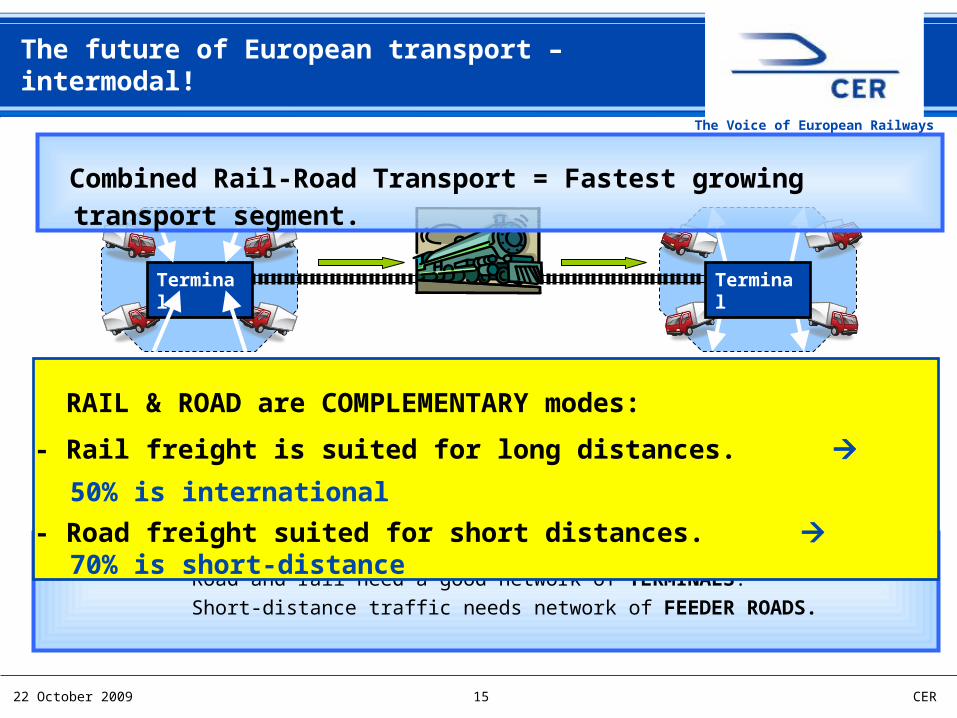

Conclusion: Long-distance traffic needs network of RAIL CORRIDORS. Road and rail need a good network of TERMINALS. Short-distance traffic needs network of FEEDER ROADS.

Terminal Terminal

RAIL & ROAD are COMPLEMENTARY modes:

- Rail freight is suited for long distances. 50% is international - Road freight suited for short distances. 70% is short-distance

Combined Rail-Road Transport = Fastest growing transport segment.

The future of European transport – intermodal!

1622 October 2009 CER

The Voice of European Railways

The future: no alternative to rail as the backbone!

+25%

Source: EEA 2007

Development of GHG emissions in different sectors (1990 – 2010)

Development of GHG emissions in different sectors (1990 – 2010)

GHG emissions in Transport sector

(1990 – 2010)

GHG emissions in Transport sector

(1990 – 2010)

!

It is time to act now!!!

1722 October 2009 CER

The Voice of European Railways

Thank you for your attention!

For further information, visit our website: www.cer.be

Libor Lochman

CER Deputy Executive Director

Tel: +32 2 213 08 82Email: [email protected]