1130-1215 Robinet North American Light Vehicle … – 25 Growth Volume, CAGR% IHS Automotive |...

34

Michael Robinet Managing Director IHS Automotive

Transcript of 1130-1215 Robinet North American Light Vehicle … – 25 Growth Volume, CAGR% IHS Automotive |...

Michael RobinetManaging Director

IHS Automotive

© 2015 IHS

Presentation

ihs.com

IHS AUTOMOTIVE

Global Light Vehicle Forecast:Readying For The Next StageOctober 15, 2015

Michael Robinet, Managing Director, IHS Automotive Advisory

Contents

© 2015 IHS 3

• Economic Update

• Structural Factors Drive a Next Stage

• Industry Implications

IHS Automotive | October 2015

The “Great Divergence” Emerges

• Over the past four years global growth has been remarkably stable –between 2.5% and 3.0% …

• … Despite “rolling routs” in financial and commodity markets.

• However, the composition of growth has changed fundamentally – with a gradual growth acceleration among the advance economies and a sharp deceleration in the emerging world.

• Four trends have driven this divergence:

• Debt and deleveraging.

• The plunge in the price of oil and other commodities.

• Central banks moving on different paths.

• The rise of the dollar and the fall in other currencies.

4

IHS Automotive | October 2015

© 2015 IHS

-1

0

1

2

3

4

5

6

7

NAFTA OtherAmericas

WesternEurope

EmergingEurope

Mideast-N.Africa

Sub-Saharan

Africa

Japan Other Asia-Pacific

Ann

ual p

erce

nt c

hang

e

2013 2014 2015 2016 2017-21

5

Asia-Pacific (excluding Japan) and Sub-Saharan Africa will achieve the fastest growth in real GDP

IHS Automotive / October 2015

Real GDP

Source: IHS © 2015 IHS

© 2015 IHS 6

US crude oil prices: A big drop – but for how long?IHS Automotive / October 2015

Crude oil and natural gas prices

0

2

4

6

8

10

12

14

0

20

40

60

80

100

120

140

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Dol

lars

/mill

ion

Btu

Dol

lars

/bar

rel

Crude oil, WTI (Left scale) Natural gas, Henry Hub (Right scale)

Source: IHS Energy © 2015 IHS

© 2015 IHS 7

IHS Automotive / October 2015

Exchange rates per US dollar

Quarterly averages

Canadian dollar

Japanese yen

Euro

Chinese renminbi

0.6

0.8

1.0

1.2

1.4

1.6

1998 2001 2004 2007 2010 2013 20160.2

0.4

0.6

0.8

1.0

1.2

1998 2001 2004 2007 2010 2013 2016

4

5

6

7

8

9

1998 2001 2004 2007 2010 2013 201640

60

80

100

120

140

1998 2001 2004 2007 2010 2013 2016

Source: IHS © 2015 IHS Source: IHS © 2015 IHS

Source: IHS © 2015 IHS Source: IHS © 2015 IHS

© 2015 IHS

0

5

10

15

20

1980 1985 1990 1995 2000 2005 2010 2015 2020 2025

Perc

ent c

hang

e

Real GDP Real domestic demand

8

China’s economic growth will downshift in the long runIHS Automotive / October 2015

Real GDP

Source: IHS © 2015 IHS

Contents

© 2015 IHS 9

• Economic Update

• Structural Factors Drive a Next Stage

• Industry Implications

IHS Automotive | October 2015

© 2015 IHS 10

Global Light Vehicle Sales ForecastMarket now flat in 2015, but weakness in emerging markets only temporary

IHS Automotive | October 2015

0

5

10

15

20

25

30

35

40

45

50

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

Mill

ions

Mature Markets China Emerging Markets

Market Growth2009-'12 2012-'15 2015-'22

Mature 10% 12% 1%China 43% 26% 34%

Emerging 39% -12% 48%

Global sales remain at 86 million in 2015, but economic improvement will lift market 2% next year;

long-term prospects unchanged – 100m in 2020.

Source: IHS Automotive

© 2015 IHS 11

Mature Markets LV Sales ForecastReplacement demand is key driver – loyalty critical to OEMs

IHS Automotive | October 2015

6.7

20.3

1.3

14.5

0

2

4

6

8

10

12

14

16

18

20

22

Japan/ Korea North America Oceania West Europe

LV Sales Forecast (millions, 2005 – 2022)

Source: IHS Automotive

© 2015 IHS 12

Emerging Markets LV Sales ForecastRecent declines only temporary – fundamentals remain positive

IHS Automotive | October 2015

2.9

1.1

2.8

3.4

5.2

4.3

0

1

2

3

4

5

6

7

ASEAN Central Europe East Europe IndianSubcontinent

MiddleEast/Africa

South America

LV Sales Forecast (millions, 2005 – 2022)

Source: IHS Automotive

71

60

87

103

113

50

60

70

80

90

100

110

120

2007 2009 2011 2013 2015 2017 2019 2021 2023 2025

Mill

ions

Global Light Vehicle ProductionGlobal Growth Takes a Turn

13

27million

16million

11.3, 3.8%

7.1, 6.1%

3.9, 1.6%

1.7, 0.8%

1.1, 4.1%

1.1, 2.3%

-1.2, -0.8%

-2 0 2 4 6 8 10 12

China

S Asia

EU

NA

MEA

S Amer

Jap/Kor

Millions

2014 – 25 GrowthVolume, CAGR%

IHS Automotive | October 2015

10million

Bodytypes and Segments Shifting Legislation, Global Platforms and Consumer Desires

14

2000

2020

13%

27%

22%

7%

11%

9%

11%25%

28%18%

7%

8%

6%

8% SUV27%

Sedan27%

Hatchback19%

Van7%

MPV7%

Pickup6%

Other7%

6%

18%

26%17%

10%

23%

6%

21%

32%

17%

7%

17%

A6%

B25%

C31%

D16%

E6%

Full-Frame16%

20052015

2025

Global BodyType Share Global Production Segment Share

SUV has doubled since 2005 to be the predominant bodytype – global platforms

• Full-Frame share declines to to NA• B, C & D account for ~72% by 2025

IHS Presentation | October 2015

2005 2015 2025

0

10

20

30

40

50

60

70

80

2005 2010 2015 2020 2025

Global Engine Production by Cylinder Count

0 1-3 4 5-6 8+

4 Cyl.

1-3 Cyl.

8+ Cyl.0 Cyl.

5-6 Cyl.

Global Engine OutputSub 2.0L totals to 66% of the Market

0

20

40

60

80

100

120

2005 2010 2015 2020 2025

Engi

ne P

rodu

ctio

nM

illio

ns

Global Engine Production by Displacement

0L 0.1-0.9L 1-1.9L 2-2.9L 3-3.9L 4-4.9L 5L+

15

2025

52%

66%62%

<2.0L

IHS Presentation | October 2015

By 2025, 71% of powertrains will have some level of electrification

51%44%

.

…

44%

35%

12%

6%

42%

27%

13%

12%

3%

Global Transmission Type by Share

Manual Auto CVT DCTEVT Reduction AMT IVT

TransmissionVolume Stable, Greater Speeds

0

5

10

15

20

25

30

35

40

45

50

2005 2010 2015 2020 2025

Aut

o, D

CT

& A

MT

Tran

smis

sion

sM

illio

ns

Auto, DCT & AMT Trans by Speed

3 4 5 6 7 8 9 10 11

16

20252025

2015

2005

84% 93%

IHS Presentation | October 2015

Global Program Launches by RegionIncreased Launch Activity Raises Risk

© 2015 IHS

17 1825

16

3427

35 40 45 47

26

24 2023

26

3027

2529

28 29

27

2014

2116

14

1621

2019 15

17

21

16

33

31

32

26

32 19

44

28

358

5

817

523

2123

33

36

13

0

20

40

60

80

100

120

140

160

180

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

# of

Lau

nche

s

North America Europe Japan/Korea China Other

17

73

115

169

Increased industry pace places pressure on talent, resources and infrastructure.

IHS Automotive | October 2015

77%17%

3%3% Det 346%

Asian 438%

Germ 311%

Other5%

NAFTA Production Share

NAFTA ProductionCustomer Mix is Changing….

0

2

4

6

8

10

12

14

16

18

20

2000 2003 2006 2009 2012 2015 2018 2021 2024

NA

LV P

rodu

ctio

nM

illio

ns

Detroit 3 Asian 4 German 3 Other

18

2000 2025

• German OEMs growing faster than Asian 4 and ‘Other’ OEMs.

• Detroit 3 may actually decline due to lack of capacity and competitors shifting of imported offerings to NA output.

IHS Automotive | October 2015

-53%

51%

69%

33%

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

140%

160%

2015-25 CTG

US LV SalesPent-Up Demand Declines and Affordability Impacts Towards 2020

19

17.016.616.2

13.210.4

11.612.8

14.515.6

16.517.117.3

17.717.517.317.117.1

0

4

8

12

16

20

2005 2010 2015 2020

Mill

ions

IHS Presentation | October 2015

• Affordability crests with wealth effect• Credit availability at a peak• Legislation drives increased cost into the fleet• Employment growth and vehicle age supports

NA Light Vehicle Production

20

15.815.315.1 12.6

8.611.9

13.115.4

16.217.0

17.517.9

18.318.518.818.918.9

0%

20%

40%

60%

80%

100%

0

4

8

12

16

20

2005 2010 2015 2020

Mill

ions

NA Production Underutilized Capacity % Utilization

IHS Presentation | October 2015

• Production Co-Location• Exports• Global Production Flexibility

Bodytypes and Segments Shifting to Legislation and Consumers

21

2000

2020

17%

36%22%

2%

10%

7%6% 31%

35%

18%

1%

6%

4%5%

SUV36%

Sedan34%

Pickup15%

Hatchback6%

MPV3%

Coupe2%

Other4%

2%18%

22%

17%

41%

2%

24%

32%

16%

26%

B-Segment7%

C-Segment27%

D-Segment34%

E-Segment12%

Full Frame20%

2000 2010 2020

20002010

2020

NA BodyType Share NA Production Segment Share

SUV has doubled since 2000 to be the predominant bodytype – global platforms

• Full-Frame share is cut in half• B, C & D account for ~70% by 2020

IHS Presentation | October 2015

Three Distinct NA Production Clusters Coexist

0

1

2

3

4

5

6

7

8

9

10

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

Mill

ions

Great Lakes

Mid-Mexico

Southeast

22

• Great Lakes driven by installed capacity shifting to 3 crew/3 shift structures to reach +7 million units

• Southeast reaching a formidable level of +5 million units by 2017 with virtually every NA OEM resident

• Mid-Mexico rises to ~4 million units by 2022 as new capacity, diversified demand and supplier investment act as enablers

© 2015 IHS

IHS Presentation | October 2015

NAFTA Program Launches by Country

© 2015 IHS

25 3 2 1

4 2 15 3 2

3

67

6 9 3 814

11 138

17

13

25

15

27

1917

2526

37

12

14%

26%

35%36%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0

10

20

30

40

50

60

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Laun

ch S

hare

in M

exic

o (L

ine)

# of

Lau

nche

s by

Cou

ntry

(Bar

)

Canada Mexico United States Share in Mexico

23

IHS Presentation | October 2015

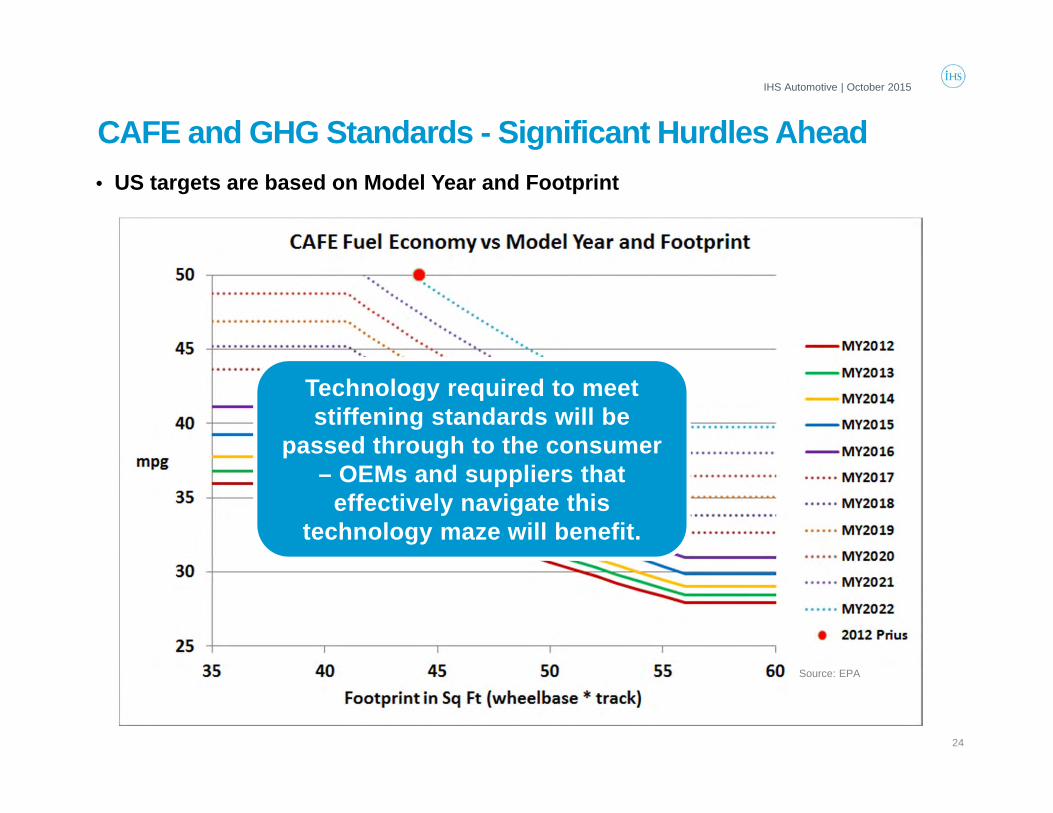

CAFE and GHG Standards - Significant Hurdles Ahead• US targets are based on Model Year and Footprint

24

Source: EPA

Technology required to meet stiffening standards will be

passed through to the consumer – OEMs and suppliers that

effectively navigate this technology maze will benefit.

IHS Automotive | October 2015

25

10987654321

Build Process Change /All-New Architecture

Integrate new build processes due to platform consolidation, increased flexibility and need to integrate new materials.

All-New/ Major Platform, Powertrain Packaging

All-new dimensions, locations points, powertrain packaging/fitments & suspension/ chassis structures.

Moderate Revision/Mid-cycle Enhancement

New interior/exterior styling, add bodystyles, significant trim levels and new/major powerteams changes.

Exterior Modifications & Electronic Changes

Exterior lighting, front/rear fascia trim, interior electronic content, software revisions, incremental electronic content.

The New Cadence 10 – 5 – 2.5 – 1 Increased Speed & Intensity Impacts Launch Requirements

10

5

2.5

1

IHS Automotive | October 2015

Material Forecast AnalysisTotal NA LV Industry By Pounds

• Growing total volume in NA 17.0 Mil to 19.0 Mil +12%• Aluminum with a scrap allowance rises to ~1.6 Bil lbs• Steel declines in larger segments – shift to Al

Pounds

IHS Automotive | October 2015

27

Material Forecast AnalysisFull-Size Full Frame Industry By Pounds

Pounds

IHS Automotive | October 2015

Launch Performance in the Spotlight

• Cadence is over 25% faster and competition more intense

• Highest content and most profitable versions are earliest in the cycle

• Integration of new materials/systems into the build process

• Launches curves need to improve:

• 7-year cycle – loss of ~2.0% of total cycle volume

• 5-year cycle – same launch curve – loss of ~3.5% of volume

• Quantifiable capacity & tier 2 & 3 readiness is critical

28

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

Volume Gross Profit

Bill

ions

Major Program Launch Loss

No Launch LossIdeal Launch LossActual Launch Loss

OEM should have lost

~several mil during the launch, it

instead lost ~ 2X the

expected

Inst

ead

of lo

sing

1.9

% o

f tot

al

cycl

e vo

lum

e, O

EM lo

st 3

.9%

IHS Automotive | October 2015

© 2015 IHS 29

Worldwide V2X market forecast – Expected Scenario

Worldwide V2X Regional Share Forecast – Expected Scenario

© 2015 IHSSource: IHS

0

20

40

60

80

100

120

140

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027

#M

USA Western Europe Japan South Korea Rest of World

IHS Automotive | October 2015

Level 0-5 Driving automation expands with technology, legislation and

consumers demands. V2V & V2I rise exponentially after 2020.

Contents

© 2015 IHS 30

• Economic Update

• Structural Factors Drive a Next Stage

• Industry Implications

IHS Automotive | October 2015

© 2015 IHS

• OEM Consolidation Drivers• Scale economies

• Legislative compliance

• Tariff and non-tariff protections eliminated

• Lack of demand diversification, capital, supplier alliances and technical capability

• Capital (ROE) and production utilization is below average

• Candidates: • Most Chinese OEMs with SOE ownership

• Regional’ OEMs without appreciable volume in major segments or under intense

competitive pressures from larger players

• Regional OEMs serving divergent markets – lacking the ability to consolidate platforms,

build processes

• OEMs with ownership lacking a viable long-term vision

OEM & Supplier ConsolidationThe Post-2009 Free Ride is Over – The Next Stage Has Arrived

31

IHS Automotive | October 2015

© 2015 IHS

• Supplier Consolidation Drivers• Lack of global production or R/D scale to match platform footprints

• Lagging technology amidst a faster cadence

• Lack of a liable supply base

• Risk aversion – HR, capital & technology (I/P)

• Inability to achieve adequate ROE levels, ownership motivations

• Sector Candidates: • Regional tier 1 and tier 2 players focused on global platforms

• Those without appropriate global capabilities and relationships

• Areas under intense competition with high process turnover and shorter lifecycles

• Those focused on few customers with high demand variability

• Suppliers with ownership structures with shorter horizons/goals (PE/Family)

OEM & Supplier ConsolidationThe Post-2009 Free Ride is Over – The Next Stage Has Arrived

32

IHS Automotive | October 2015

© 2015 IHS

• Volumes flattening in several markets• Japan/Korea, North America and Europe grow below global trend

• Cadence is faster – challenging for Tier 2 & 3 regional suppliers• Increased complexity coupled with shorter cycles

• Launch readiness is critical• OEMs focus on optimization of early cycle volume

• Increased NA non-D3 capacity – new suppliers emerge• Global platforms, architectures increasing

• Ability to design and manufacture in key markets differentiates

• OEMs increasing pressure on suppliers for cost control• ‘One Cost’ models, APRs and enhanced oversight of purchased materials

• Exposure to China, South America and Russia raises pressure on other markets

An Inflection PointThe New Mantra ‘Launches, Logistics & Capacity’

33

IHS Automotive | October 2015

IHSTM AUTOMOTIVE

COPYRIGHT NOTICE AND DISCLAIMER © 2015 IHS. For internal use of IHS clients only.No portion of this report may be reproduced, reused, or otherwise distributed in any form without prior written consent, with the exception of any internal client distribution as may be permitted in the license agreement between client and IHS. Contentreproduced or redistributed with IHS permission must display IHS legal notices and attributions of authorship. The information contained herein is from sources considered reliable, but its accuracy and completeness are not warranted, nor are theopinions and analyses that are based upon it, and to the extent permitted by law, IHS shall not be liable for any errors or omissions or any loss, damage, or expense incurred by reliance on information or any statement contained herein. In particular,please note that no representation or warranty is given as to the achievement or reasonableness of, and no reliance should be placed on, any projections, forecasts, estimates, or assumptions, and, due to various risks and uncertainties, actual eventsand results may differ materially from forecasts and statements of belief noted herein. This report is not to be construed as legal or financial advice, and use of or reliance on any information in this publication is entirely at client’s own risk. IHS and theIHS logo are trademarks of IHS.

IHS Customer Care:Americas: +1 800 IHS CARE (+1 800 447 2273); [email protected] Europe, Middle East, and Africa: +44 (0) 1344 328 300; [email protected] Asia and the Pacific Rim: +604 291 3600; [email protected]

Thank You

Michael RobinetManaging Director, IHS Automotive Advisory [email protected]