11111723 11111858 11113013

34

1 CAPSTONE PROJECT (PART – II) MGT 739 REPORT (Project Term January-April 2013) THE EFFECT OF INTEREST RATE ON HOUSEHOLD CONSUMPTION Submitted by (Nikhil Aggarwal ) Registration Number: 11111723 (Hiralal Kumar) Registrati on Number: 11111858 (Supriya Kumari Bajpayee) Registration Number: 11113013 Project Group Number: F13 Under the Guidance of (Mrs. Neha Tikoo) Lovely faculty of Business and Applied Arts Lovely Professional University, Phagwara January to April, 2013 CERTIFICATION/ THESIS APPROVAL BY FACULTY ADVISOR TO WHOMSOEVER IT MAY CONCERN

-

Upload

nikhil-aggarwal -

Category

Documents

-

view

9 -

download

0

description

investor behaviour in investing equity

Transcript of 11111723 11111858 11113013

7/16/2019 11111723 11111858 11113013

http://slidepdf.com/reader/full/11111723-11111858-11113013 1/34

1

CAPSTONE PROJECT (PART – II) MGT 739 REPORT

(Project Term January-April 2013)

THE EFFECT OF INTEREST RATE ON HOUSEHOLD

CONSUMPTION

Submitted by

(Nikhil Aggarwal ) Registration Number: 11111723

(Hiralal Kumar) Registration Number: 11111858

(Supriya Kumari Bajpayee) Registration Number: 11113013

Project Group Number: F13

Under the Guidance of

(Mrs. Neha Tikoo)

Lovely faculty of Business and Applied Arts

Lovely Professional University, Phagwara

January to April, 2013

CERTIFICATION/ THESIS APPROVAL BY FACULTY ADVISOR

TO WHOMSOEVER IT MAY CONCERN

7/16/2019 11111723 11111858 11113013

http://slidepdf.com/reader/full/11111723-11111858-11113013 2/34

2

Acknowledgements

Many a time we have heard that learning comes from practice. From moving out of classroom

education to the real world during Capstone Project We got an opportunity to experience what

we had heard. We would like to express our gratitude to Mrs. Neha Tikoo for his valuable

guideline, support and encouragement in completing the synopsis.

We are very much thankful to our A.O. and the entire staff of the LFBA for

providing me such a friendly and co-operative environment.

HIRALAL KUMAR (11111858)

NIKHIL AGRAWAL (11111723)

SUPRIYA KUMARI BAJPAYEE (11113013)

7/16/2019 11111723 11111858 11113013

http://slidepdf.com/reader/full/11111723-11111858-11113013 3/34

3

Table of contents:

Chapter 1 Introduction 7-11

Chapter 2 Literature review 12-17

Chapter 3 Research methodology 18-19

Chapter 4 Analysis 20-25

Chapter 5 Findings 26-28

References 29-31

Annexure 32-34

7/16/2019 11111723 11111858 11113013

http://slidepdf.com/reader/full/11111723-11111858-11113013 4/34

4

CERTIFICATE

This is to certify that HIRALAL KUMAR (11111858), NIKHIL AGRAWAL

(11111723) and SUPRIYA KUMARI BAJPAYEE (11113013) has completed objective

formulation of Capstone project titled, “THE EFFECT OF INTEREST RATE ON

HOUSEHOLD CONSUMPTION” under my guidance and supervision. To the best of my

knowledge, the present work is the result of their original investigation and study. No part of

the capstone has ever been submitted for any other degree at any University.

The capstone project is fit for submission and the partial fulfilment of the conditions

for the award of .........................

Signature and Name of the Research Supervisor:

Designation

School

Lovely Professional University

Phagwara, Punjab.

Date :

7/16/2019 11111723 11111858 11113013

http://slidepdf.com/reader/full/11111723-11111858-11113013 5/34

5

DECLARATION

I, HIRALAL KUMAR, NIKHIL AGGARWAL and SUPRIYA KUMARI

BAJPAYEE students of MBA-3501 under Department of LFBAA of Lovely Professional

University, Punjab, hereby declare that all the information furnished in this capstone project

report is based on our own intensive research and is genuine.

This capstone does not, to the best of my knowledge, contain part of my work which

has been submitted for the award of our degree either of this university or any other university

without proper citation.

Date : Signature and Name of the student

Registration No.

11111858

11111723

11113013

7/16/2019 11111723 11111858 11113013

http://slidepdf.com/reader/full/11111723-11111858-11113013 6/34

6

Abstract

In this paper, an attempt has been made to analyse the the effect of real interest rate on

household consumption for which we have taken the data of real interest rate, household

consumption and growth of bank deposits of scheduled commercial bank in India. For

analysis we have used simple regression to know how real interest rate affects household

consumption expenditure. The findings of the study showed that the average real interest rate

was 6.162% and there is long run relationship between real interest rate and household

consumption in India. The estimated coefficients of correlation further indicate that the real

interest rate have a weak correlation with household consumption expenditure. Like wisely

the real interest rate affects the growth of bank deposits positively but negligibly.

7/16/2019 11111723 11111858 11113013

http://slidepdf.com/reader/full/11111723-11111858-11113013 7/34

7

Chapter1

Introduction

7/16/2019 11111723 11111858 11113013

http://slidepdf.com/reader/full/11111723-11111858-11113013 8/34

8

Interest rates are the most closely watched element in the financial market. It drives the

decision, whether to lend or borrow, save or invest or choose the available alternative

investment opportunities. Interest rates are the primary tool to consider while making

investments. “Interest rates are the most pervasive elements in the financial world. They affect

every nook and cranny of financial markets” (Ritter, Silber et al. 1991).

The effect of fluctuation in interest rate in the saving or consumption can be

represented by a variable. This variable can be either in the form of saving or in the form of

consumption. The variable in the form of saving is called interest elasticity of saving. This

represents the change in saving by one percent change in interest. The variable in the form of

consumption is called interest elasticity of consumption. This interest elasticity of

consumption is reciprocal of interest elasticity of saving. There have been a large number in

of empirical studies in this topic. However, most of the results do not coincide at a single

point. Moreover, in developing countries the result is more contradictory.

It is an undeniable truth that the development of an individual economy passes

through different economic phases. Sometimes it is booming and sometimes it suffers from

recession. In the theories, it may be possible to have only the booming economy but the truth

is truth. Theories are based on the assumptions but the practical life has to move with time, in

complex environment, and the time is never static. The effect of interest rate on

consumption is a central concern in macroeconomics. Among many issues that are

related to inter-temporal substitution, one of the most relevant from today's perspective

is whether consumers can be induced to increase consumption by a reduction in interest

rate paid on deposits. In this paper we measure the causal effect of interest rate on

consumption. This has crucial implications for understanding the timing and effectiveness of

the interest rate as a policy instrument that affects consumption, savings and ultimately the

growth rate of an economy. Our paper estimates the causal effect of a higher interest

rate on household consumption expenditure by exploiting a unique Indian banking

legislation and using detailed household consumption expenditure data from the RBI.

As of April 2001, the Reserve Bank of India permitted and actively encouraged banks to

offer higher interest rates on deposits of senior citizens, We use the regression discontinuity

approach to estimate the precise causal effect that the interest rate has on consumption

of households.

To achieve a higher economic growth there has to be an increased investment

both from the public and the private sector. Increased investment both from the public and private sector can take place only when savings are mobilized sufficiently. Savings can be

7/16/2019 11111723 11111858 11113013

http://slidepdf.com/reader/full/11111723-11111858-11113013 9/34

9

increased if real interest rates are positive. In this respect, RBI has adopted interest rate policy

for the (i) Mobilization of higher level of savings in the form of bank deposits (ii)Prevention

of capital flight to foreign countries (iii) Allocation of resources to productive sectors of the

economy, and (iv) Promotion of economic activities particularly industry and trade. For those

purpose, interest rates were regulated.

In the past when interest rates were controlled, RBI attempted to keep real

interest rates positive by making frequent revisions in nominal rates whenever inflation rates

were changing. But RBI was unable to appropriately monitor the movements and the real

interest rate was moving up and down over time. With this background, the objective of this

research is to find out the real interest rate and analyze its movements, find possible factors

for these movements, and find the correlation between real interest rates and other important

variables.

Terminology:

Interest rate is the rate at which interest is paid by a borrower for the use of money that they

borrow from a lender. Interest rates are fundamental to a capitalist society. Interest rates are

normally expressed as a percentage rate over the period of one year.

Real Interest rate is approximately the nominal interest rate minus the inflation rate

(Fisher,1911). It is the rate of interest an investor expect to receive after subtracting inflation.

Income is the consumption and savings opportunity gained by an entity within a specified

time frame, which is generally expressed in monetary terms. For firms, income generally

refers to net-profit: what remains of revenue after expenses have been subtracted. In the field

of public economics, it may refer to the accumulation of both monetary and non-monetary

consumption ability, the former being used as a proxy for total income.

Household final consumption expenditure (HFCE) is a transaction of the national account's

use of income account representing consumer spending. It consists of

the expenditure incurred by resident households on individual consumption goods and

services, including those sold at prices that are not economically significant. It also includes

various kinds of imputed expenditure of which the imputed rent for services of owner-

occupied housing (imputed rents) is generally the most important one. The household sector

7/16/2019 11111723 11111858 11113013

http://slidepdf.com/reader/full/11111723-11111858-11113013 10/34

10

covers not only those living in traditional households, but also those people living in

communal establishments, such as retirement homes, boarding houses and prisons.

The above given definition of HFCE includes expenditure by resident households on the

domestic territory and expenditure by resident households abroad (outbound tourists), butexcludes any non-resident households' expenditure on the domestic territory (inbound

tourists). From this national definition of consumption expenditure may be distinguished the

household final consumption expenditure according to the domestic concept which includes

household expenditure made on the domestic territory by residents and inbound tourists, but

excludes residents' expenditure made abroad.

Household consumer expenditure: The expenditure incurred by a household on domestic

consumption during the reference period is the household's consumer expenditure.

Expenditure incurred towards productive enterprises of households is excluded from

household consumer expenditure. Also excluded are expenditure on purchase and

construction of residential land and building, interest payments, insurance premium

payments, payments of fines and penalties, and expenditure on gambling including lottery

tickets. Money given as remittance, charity, gift, etc. is not consumer expenditure. However,

self-consumed produce of own farm or other household enterprise is valued and included in

household consumer expenditure. So are goods and services received as payment in kind or

free from employer, such as accommodation and medical care, and travelling allowance

excluding allowance for business trips.

Household size: The size of a household is the total number of persons in the household.

Purpose of study

There are hardly any economic papers which do not talk about the interest rates. Perhaps,

interest rates are the most closely watched element in the financial market. “Interest rates are

the most pervasive elements in the financial world. They affect every nook and cranny of

financial markets.” (Ritter, Silber et al. 1991). From this citation we can say that how

7/16/2019 11111723 11111858 11113013

http://slidepdf.com/reader/full/11111723-11111858-11113013 11/34

11

important is interest rate in an economy and how it impact on Household consumption when

it changes.

Objective1. To know the effect of change of interest rate on household consumption.

2. To know how consumption and savings are related to interest rate.

Limitations

1. Data taken is for scheduled commercial banks non schedule data is not properly available.

2. Data is taken for 1990 -2010 only recent data of 2011 and 2012 is not available on RBI site.

3. There is lack of time, classes, busy schedule and less members in our group.

4. We depend on the data given by RBI or NSSO and world bank.

5. Exact deposits of all accounts and transactions are not given anywhere.

7/16/2019 11111723 11111858 11113013

http://slidepdf.com/reader/full/11111723-11111858-11113013 12/34

12

Chapter 2

Literature Review

7/16/2019 11111723 11111858 11113013

http://slidepdf.com/reader/full/11111723-11111858-11113013 13/34

13

1. Attanasio and Weber (1993), investigate the effects of aggregation on consumption Euler

equations, with particular emphasis on the inter temporal elasticity of substitution. Using

British National Accounts data, they estimate an elasticity around 1/3, which is somewhat

larger and has a smaller standard error than the Campbell-Mankiw estimate for the U.S. Then

AW turn to the British Family Expenditure Survey (FES), which provides a long time series

of household-level data. They construct separate time series for the average consumption of

all households and of households in three different age cohorts. For all households, the

estimated inter temporal elasticity of substitution is around 1/3, as in the aggregate British

data. For the young and middle-aged cohorts, the estimated elasticity is roughly twice as

large, and for the older cohort, it is fairly small (although not statistically different from the

other estimates).

2. Campbell and Mankiw (1989), examined aggregate consumption data, extending Hall's

framework to allow for some households who choose consumption based on a "rule of

thumb" rather than the lifecycle model. They estimate that these households receive almost

half of total income, suggesting that their presence significantly alters the expected dynamics

of aggregate consumption. For the traditional lifecycle consumers, Campbell and Mankiw

estimate elasticity of substitution between 0 and 0.2. Estimates derived from household data.

One of the earliest papers to use cross-sectional variation in interest rates to estimate the inter

temporal elasticity of substitution is Shapiro (1984). His estimates are very large, but they

have enormous standard errors, so they are simply not informative.

3. Avery and Kennickell's (1991), exploration of the Survey of Consumer Finances shows

that among people over age 70, median saving is less than zero (the average person is dis-

saving) but mean saving is greater than zero (the group as a whole is still accumulating

wealth). Bequests may be important for aggregate saving even if most people do not leave

significant bequests.

4. Cantor (1989) and Goodman, Luckett and Wilcox (1988),conclude that household likelyto experience positive changes in cash flow when interest rates rise. These papers carefully

7/16/2019 11111723 11111858 11113013

http://slidepdf.com/reader/full/11111723-11111858-11113013 14/34

14

examine the responsiveness of different categories of interest payments and receipts to

changes in market interest rates.

5. Deaton (1992), argues that if consumption is always close to income for many people,

then"the prima facie supposition must be that interest rates are not very important" in

determining consumption and saving. But consumption is not that close to income for people

who are doing the saving in the economy, so there is no reason to presume that the savers'

decisions are unaffected by interest rates or other factors.

6. Hall (1988), examines the behaviour of aggregate consumer spending, using different time

periods and different measures of the expected rate of return. He finds no evidence of a

significant positive elasticity of substitution. Hall notes that his results are not surprising

given that the U.S. has experienced large changes in the interest rate over time but only small

changes in the growth rate of aggregate consumption. Together, these facts suggest that

consumption is not very responsive to changes in the interest rate and thus that

the inter temporal elasticity of substitution is small.

7. Feldstein (1994), argues that Income may also be correlated with pre-tax rates of

return,high-income households may earn a higher pre-tax return on their investments than

other households, and thus may have a higher after-tax return despite their higher tax rates.

8. Bernheim and Scholz (1993), suggest an alternative utility function for which the interest

elasticity of saving is positively correlated with income. They show that if utility is a function

of actual consumption less some subsistence level of consumption, the "effective" interest

elasticity of saving increases with consumption.

9. Fry (1995) The Economic literature on savings provides a long list of factors affecting the

saving rates. Study have found ambiguous effect of increase in real interest rate on savings

because of a positive substitution effect towards future consumption and a negative income

effect due to increased real returns on saved wealth. has found small but positive interest rate

elasticity of savings to be insignificantly related to real interest rates.

7/16/2019 11111723 11111858 11113013

http://slidepdf.com/reader/full/11111723-11111858-11113013 15/34

15

10. Bhattarai and kafle,(2011).The influence of real interest rate on savings depends on the

relative strength of the offsetting substitution and income effect A rise in the interest rate of

return may increase savings by making future consumption cheaper relative to current

consumption (substitution effect).At the same time higher real interest rate may reduce the

savings necessary to purchase a given amount of future consumption (income effect). Given

the theoretical ambiguities, whether or not saving behaviour is interest elastic is a matter of

country specific empirical analysis

11. Shrestha,(2010).there are number of studies which suggested for significantly positive to

significantly negative coefficients of real interest rate. It is also important to note that the real

interest rate have a positive influence on the private savings and can be taken as an important

policy variable in Nepal.

12. Arrieta,(1988) identified activities variable such as the real interest rates and some

measures of capital inflows ( or foreign savings) as the important variables determining

domestic savings in developing countries. though, some of the studies also included

demographic variables, government savings and labour market constraints in to the model to

investigate their influence on private savings, the interest rate are sensitivity of savings has

been the subject of literature relating to LDCs. Many economist remain doubtful that interest

rates whether real or nominal, have any significant impact on private sector saving behaviour

in developed or developing countries, since saving is defined as not consuming, economist

who do not believe on the role of interest rates conclude that the interest rates have little

impact on private savings decision to allocate income between consumption and savings: the

interest rate of elasticity is held to be zero or insignificantly small.

7/16/2019 11111723 11111858 11113013

http://slidepdf.com/reader/full/11111723-11111858-11113013 16/34

16

13. Agrawal, P., P. Sahoo, and R.K.Das.,(2007). The Real interest rate affects the savings

rate positively in Bangladesh and Nepal but negatively in India, Pakistan and Sri Lanka Their

analysis suggests that trying to influence the savings rate by manipulating interest rate is not

likely to be practical policy option in these countries as interest rate changes have only a

minor impact on savings rate.

14. Arron and Meulbauer (1999) present the determinants of private savings in south

Africa, Separately examining personal and corporate sector saving behaviour over nearly

three decades, from the late 1960s to 1997. This paper confirms that the main factors behind

personal saving in South Africa include direct negative effects of wealth and financial

liberalization and the direct positive effects of real interest rates and uncertainty. Moreover,

corporations save more when dividend tax rates rise, while in the absence of the capital gains

tax, higher inflation encourages corporate saving.

15. Mudit Kapoor and Shamika Ravi (2009), A recent study that is close to this research is

the empirical test of the effect of interest rate on household consumption under taken by

Mudit Kapoor and Shamika Ravi in 2009.This research was carried out after the change in

Indian banking legislation that offered higher interest rate on the deposits of senior citizens

(above sixty years). The banking legislation was established in the year 2001. This change in

banking legislation in Indian provided an opportunity to find the relationship between interest

rate and consumption more accurately. The author used the household consumption

expenditure data from the National Sample Survey (NSS). The estimation of effect of change

in interest rate on consumption was done through comparing the expenditures of households

that are not eligible for the higher interest earnings on their deposits to households that are

eligible. The eligibility criteria were based upon the age of the household members. When

7/16/2019 11111723 11111858 11113013

http://slidepdf.com/reader/full/11111723-11111858-11113013 17/34

17

there is at least one member who is sixty years or above was eligible for the higher interest

rate. The study has found a strong and significant short run impact on saving and consumption

of households. But it failed to explain the long term effect due to the lack of sufficient data to

explain the long term effect of interest rate. They found an immediate 12 percent decline in

household consumption when the interest rates on deposits were increased by 50 basis points.

The effect was primarily in non-food, non-essential items which were declined by 17 percent.

The analysis was performed with the 2005-06 data. And to compare the results with prior to

banking legislation, 2000-01 data was used.

The reviews of all these literatures have given a platform to do this dissertation. The reviews

have given an experience of dependency of different variables in different situation and time

frame. The review of the literatures has shown that the parameter of consideration and

assumptions in the research significantly influences the conclusion.

7/16/2019 11111723 11111858 11113013

http://slidepdf.com/reader/full/11111723-11111858-11113013 18/34

18

Chapter 3

Research

methodology

7/16/2019 11111723 11111858 11113013

http://slidepdf.com/reader/full/11111723-11111858-11113013 19/34

19

Research methodology means the method of preparing project. In other words project

methodology is the way of preparing the project, and presenting the project report, the work is

systematic and done in proper order as good work gives good results. Further the data

collected to prepare the project must be relevant.

Data collection will be done from following sources:-

1. Secondary Data

Secondary data will be collected through:-

1. RBI

2. World Bank

The data of 1990-2010 of household consumption expenditure, real interest rates and growth

of bank deposits in India has been taken.

Research Design:

Descriptive Research Design has been used in the research work.

Tools and Techniques:

Regression Analysis is used to determine the impacts of determinants on interest rate with

respect to household consumption rate in India

To make use of these variables, we sort them by year wise data of household

consumption and interest rates, then calculated the mean, maximum, minimum, and standard

deviation for each variable. We create a correlation matrix between all the variables and then

run regressions to determine which variables are significant, at what level, and what optimal

rates we might find.

7/16/2019 11111723 11111858 11113013

http://slidepdf.com/reader/full/11111723-11111858-11113013 20/34

20

Chapter4

Analysis

7/16/2019 11111723 11111858 11113013

http://slidepdf.com/reader/full/11111723-11111858-11113013 21/34

21

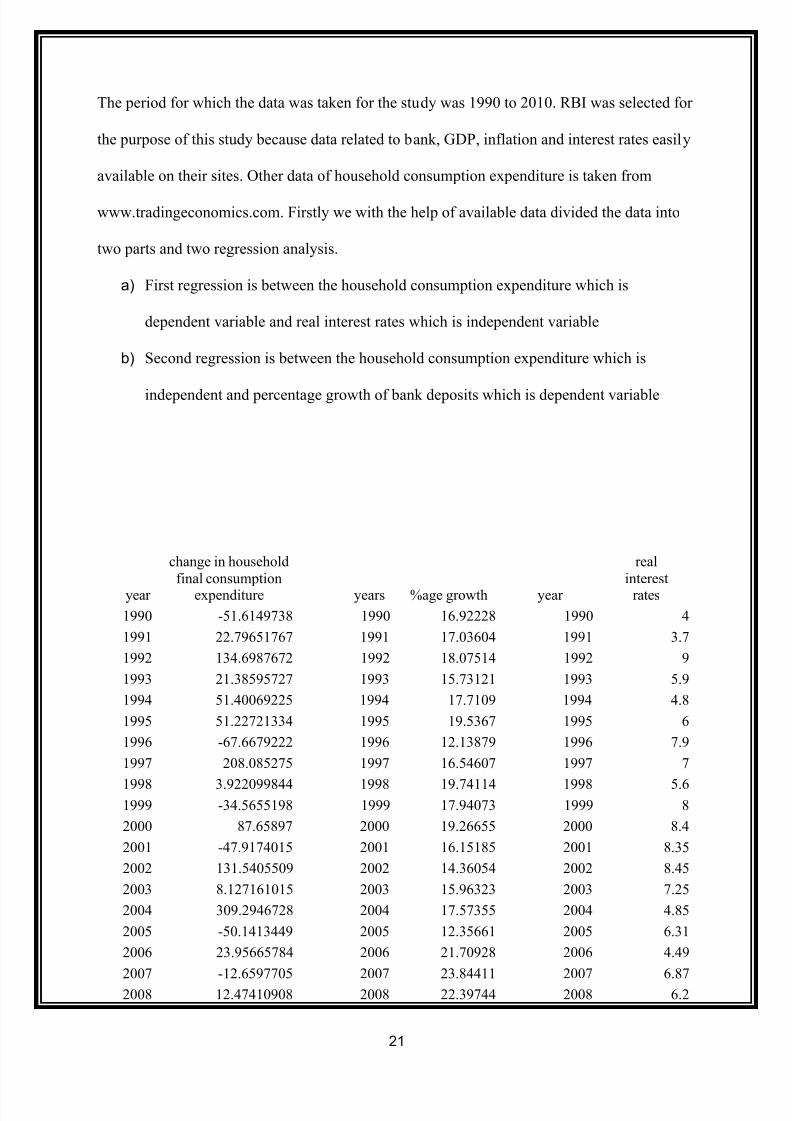

The period for which the data was taken for the study was 1990 to 2010. RBI was selected for

the purpose of this study because data related to bank, GDP, inflation and interest rates easily

available on their sites. Other data of household consumption expenditure is taken from

www.tradingeconomics.com. Firstly we with the help of available data divided the data into

two parts and two regression analysis.

a) First regression is between the household consumption expenditure which is

dependent variable and real interest rates which is independent variable

b) Second regression is between the household consumption expenditure which is

independent and percentage growth of bank deposits which is dependent variable

year

change in household

final consumptionexpenditure years %age growth year

real

interestrates

1990 -51.6149738 1990 16.92228 1990 4

1991 22.79651767 1991 17.03604 1991 3.7

1992 134.6987672 1992 18.07514 1992 9

1993 21.38595727 1993 15.73121 1993 5.9

1994 51.40069225 1994 17.7109 1994 4.8

1995 51.22721334 1995 19.5367 1995 6

1996 -67.6679222 1996 12.13879 1996 7.9

1997 208.085275 1997 16.54607 1997 7

1998 3.922099844 1998 19.74114 1998 5.61999 -34.5655198 1999 17.94073 1999 8

2000 87.65897 2000 19.26655 2000 8.4

2001 -47.9174015 2001 16.15185 2001 8.35

2002 131.5405509 2002 14.36054 2002 8.45

2003 8.127161015 2003 15.96323 2003 7.25

2004 309.2946728 2004 17.57355 2004 4.85

2005 -50.1413449 2005 12.35661 2005 6.31

2006 23.95665784 2006 21.70928 2006 4.49

2007 -12.6597705 2007 23.84411 2007 6.87

2008 12.47410908 2008 22.39744 2008 6.2

7/16/2019 11111723 11111858 11113013

http://slidepdf.com/reader/full/11111723-11111858-11113013 22/34

22

2009 39.36931973 2009 19.93066 2009 4.32

2010 -100 2010 17.18041 2010 2.01

Data interpretation

The period for which the data was taken for the study was 1990 to 2010. RBI was selected for

the purpose of this study because data related to bank, GDP inflation and interest rates are

easily available on their sites. Other data of household consumption expenditure is taken from

www.tradingeconomics.com. Firstly we with the help of available data divided the data into

two parts and applied regression analysis.

a) First regression is between the household consumption expenditure which is

dependent variable and real interest rates which is independent variable

b) Second regression is between the household consumption expenditure which is

independent and percentage growth of bank deposits which is dependent variable

7/16/2019 11111723 11111858 11113013

http://slidepdf.com/reader/full/11111723-11111858-11113013 23/34

23

Regression model 1

Degree of percentage change in household consumption = ß0 + ß1 (Real interest rate) + ε

Where ε is the error term with the distribution N (0,1)

Correlations

change_in_household

__final_consumption_

expenditure real_interest_rates

Pearson Correlation change_in_household__final_consum

ption_expenditure1.000 .173

real_interest_rates .173 1.000

Above table shows the correlation between the change household final consumption

expenditure and the change in the real interest. It clearly depicts that correlation between the

two variables in very less, i.e. 0.173 and the level of significance is weak, i.e. 0.227. This

shows that there is least relation between the two variables.

Regression model analysis

Degree of percentage change in household consumption

= -19.854 +8.951 (real interest rate)

(75.223) (11.704)

[-.264] [.764]

(.795*) (.454*)

{0.173}

F = 0.585R2 = 0.030

R = 00.173

7/16/2019 11111723 11111858 11113013

http://slidepdf.com/reader/full/11111723-11111858-11113013 24/34

24

Figures in round brackets shows Standard Errors

Figures in square brackets shows t-values

(*) Two tailed 0.05 level of significance

Figures in curly brackets shows beta values

It shows that the high R value (0.173), indicates a very weak relationship b/w the independent

variables (real interest rates) and its square (0.030) and the dependent variable percentage

change in growth of bank deposits). The R-square for said variables is coming 0.030. It means

that there is no significant relationship between the independent predictors & dependent

variable. The value of beta for demand is the highest (0.173), this shows that it has a

positively influence on the % change in real interest rates.

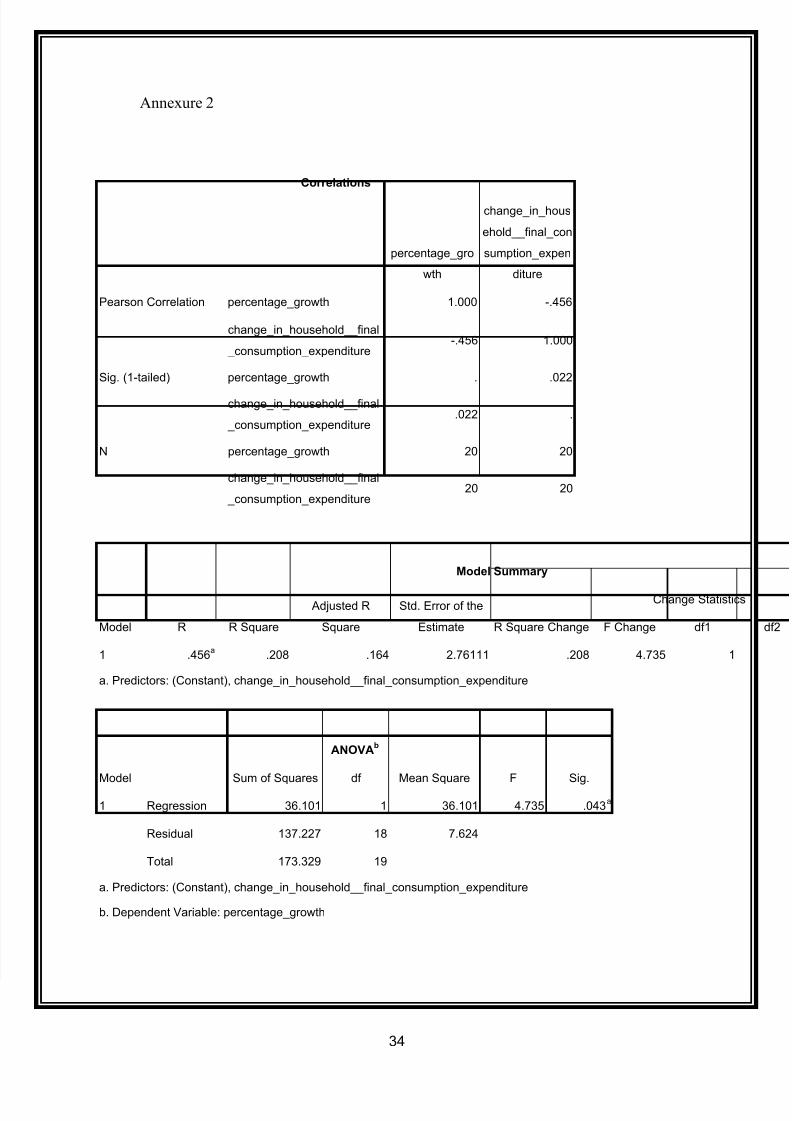

Regression model 2

Degree of percentage growth of bank deposits= ß0 + ß1 (percentage change in final

consumption expenditure) + ε

where ε is the error term with the distribution N (0,1)

Correlations

percentage_growth

change_in_househ

old__final_consu

mption_expenditur

e

Pearson Correlation percentage_growth 1.000 -.456

change_in_household__final_co

nsumption_expenditure

-.456 1.000

7/16/2019 11111723 11111858 11113013

http://slidepdf.com/reader/full/11111723-11111858-11113013 25/34

25

Above Table shows the correlation between the change in percentage growth of bank deposit

with the percentage change in household final consumption. It clearly depicts that correlation

between the two variables in very negatively correlated , i.e. -0.456. and the level of

significance is weak, i.e. 0.22. This shows that there is least relation between the two variable.

Regression model analysis

Degree of percentage growth of bank deposits

= 18.308 -0.014(change in final household consumption)

(.669) (0.007)

[27.360] [-.2.176]

(0.000*) (.043*)

{-.456}

F = 4.735

R2 = 0.208R = 0.456

Figures in round brackets shows Standard Errors

Figures in square brackets shows t-values

(*) Two tailed 0.05 level of significance

Figures in curly brackets shows beta values

It shows that the high multiple R value (.456), indicates a very strong relationship b/w the

independent variables (%change in final household consumption) and its square (.208) and

the dependent variable percentage growth of bank deposits). The R-square for said variables

is coming 0.208. It means that there is little significant relationship between the independent

predictors & dependent variable. The value of beta for demand is the highest (-.456), this

shows that it has a negatively influence on the % change in final household consumption.

7/16/2019 11111723 11111858 11113013

http://slidepdf.com/reader/full/11111723-11111858-11113013 26/34

26

Chapter 5

Findings and conclusion

7/16/2019 11111723 11111858 11113013

http://slidepdf.com/reader/full/11111723-11111858-11113013 27/34

27

Our result shows that:

1) a The correlation between the change household final consumption expenditure and the

change in the real interest. It clearly depicts that correlation between the two variables in very

less, i.e. 0.173 and the level of significance is weak, i.e. 0.227. This shows that there is least

relation between the two variables.

b) The high R value (0.173), indicates a very weak relationship b/w the independent variables

(real interest rates) and its square (0.030) and the dependent variable percentage change in

growth of bank deposits). The R-square for said variables is coming 0.030. It means that

there is no significant relationship between the independent predictors & dependent variable.

The value of beta for demand is the highest (0.173), this shows that it has a positively

influence on the percentage change in real interest rates.

2) a) The correlation between the changes in percentage growth of bank deposit with the

percentage change in household final consumption. It clearly depicts that correlation between

the two variables in very negatively correlated, i.e. -0.456. And the level of significance is

weak, i.e. 0.22. This shows that there is least relation between the two variables.

b) It shows that the high multiple R value (.456), indicates a very strong relationship b/w the

independent variables (%change in final household consumption) and its square (.208) and

the dependent variable percentage growth of bank deposits). The R-square for said variables

is coming 0.208. It means that there is little significant relationship between the independent

predictors & dependent variable. The value of beta for demand is the highest (-.456), this

shows that it has a negatively influence on the % change in final household consumption.

7/16/2019 11111723 11111858 11113013

http://slidepdf.com/reader/full/11111723-11111858-11113013 28/34

28

From the study we conclude that relationship between the household consumption, real

interest rate and bank deposits are interrelated in long run but real interest rates impact to

consumption is very less and consumption impact to saving or bank deposits is there.

Second we find that household final consumption expenditure is negatively correlated to

growth of bank deposits.

7/16/2019 11111723 11111858 11113013

http://slidepdf.com/reader/full/11111723-11111858-11113013 29/34

29

References

7/16/2019 11111723 11111858 11113013

http://slidepdf.com/reader/full/11111723-11111858-11113013 30/34

30

1. Arrieta,E.1988.Saving and growth: A Reinterpretation Carnegie-Rochester series on

public policy,Vol,40. pp.133-92.

2. Agrawal, P., P.Sahoo, and R.K.Das.,2007. Saving Behaviour in South Asia.University

of Delhi Enclave Working Paper series No. E/289/2008.

3. Aron ,Janine and J.Meullbauer.1999. Estimates of personal sector wealth for south

Africa. CSAE working paper series 1999-17.

4. Bhattarai,R and L. Kafle.2011 saving behaviour in developing country:an empirical

Analysis. Nepal Rastra Bank, Kathmandu, Nepal.

5. Deaton, Angus. 1992. Understanding Consumption . Oxford: Clarendon Press.

6. Douglas Bernheim.B and John Karl Scholz, "Private Saving and Public Policy," Tax

Policy andthe Economy, vol. 7 (Cambridge, Mass.: MIT Press, 1993).

7. Fry,S.1995. Saving Mobilization in Developing Countries: Bottleness and Reform

Proposal. Saving and Development, Vol. 14,Pp. 117-131.

8. Hall, Robert E. 1988. “Intertemporal Substitution in Consumption.” Journal of Political

Economy.

9. John Y. Campbell and N. Gregory Mankiw (1989), "Consumption, Income and Interest

Rates:Reinterpreting the Time Series Evidence," in Olivier Jean Blanchard and Stanley

Fischer,eds., NBER Macroeconomics Annual: (Cambridge, Mass.: MIT Press, 1989).

10. Martin Feldstein .1994, "Fiscal Policies, Capital Formation, and Capitalism," Working

Paper (National Bureau of Economic Research, Cambridge, Mass., October 1994).

11. Mudit Kapoor and Shamika Ravi. 1999, “The Effect of Interest Rate on Household

Consumption: Evidence from a Natural Experiment in India,” American EconomicAssociation.

7/16/2019 11111723 11111858 11113013

http://slidepdf.com/reader/full/11111723-11111858-11113013 31/34

31

12. Orazio P. Attanasio and Guglielmo Weber (July 1993), "Consumption Growth, the

Interest Rate, and Aggregation," Review of Economic Studies.

13. Robert B. Avery and Arthur B. Kennickell (December 1991), "Household Saving in the

U.S.," Review of Income and Wealth, vol. 37, no. 4

14. Richard Cantor.1989, "Interest Rates, Household Cash Flow, and Consumer

Expenditures," Quarterly Review, Federal Reserve Bank of New York, Summer.

15. Shrestha. R..P. 2010. Private Savings Behaviour in Nepal: Long-term Determinants

and short run Dynamics. Economic Review, occasional paper, Nepal Rastra Bank,

Kathmandu, Nepal.

7/16/2019 11111723 11111858 11113013

http://slidepdf.com/reader/full/11111723-11111858-11113013 32/34

32

Annexure

7/16/2019 11111723 11111858 11113013

http://slidepdf.com/reader/full/11111723-11111858-11113013 33/34

33

Annexure 1

Correlations

change_in_hous

ehold__final_con

sumption_expen

diture

real_interest_rat

es

Pearson Correlation change_in_household__final

_consumption_expenditure1.000 .173

real_interest_rates .173 1.000

Sig. (1-tailed) change_in_household__final

_consumption_expenditure. .227

real_interest_rates .227 .

N change_in_household__final

_consumption_expenditure21 21

real_interest_rates 21 21

Model Summary

Model R R Square

Adjusted R

Square

Std. Error of the

Estimate

Change Statistics

R Square Change F Change df1 df2

1 .173a

.030 -.021 97.95824 .030 .585 1

a. Predictors: (Constant), real_interest_rates

ANOVAb

Model Sum of Squares df Mean Square F Sig.

1 Regression 5612.542 1 5612.542 .585 .454a

Residual 182320.530 19 9595.817

Total 187933.071 20

a. Predictors: (Constant), real_interest_rates

b. Dependent Variable: change_in_household__final_consumption_expenditure

7/16/2019 11111723 11111858 11113013

http://slidepdf.com/reader/full/11111723-11111858-11113013 34/34

Annexure 2

Correlations

percentage_gro

wth

change_in_hous

ehold__final_con

sumption_expen

diture

Pearson Correlation percentage_growth 1.000 -.456

change_in_household__final

_consumption_expenditure-.456 1.000

Sig. (1-tailed) percentage_growth . .022

change_in_household__final

_consumption_expenditure.022 .

N percentage_growth 20 20

change_in_household__final

_consumption_expenditure20 20

Model Summary

Model R R Square

Adjusted R

Square

Std. Error of the

Estimate

Change Statistics

R Square Change F Change df1 df2

1 .456a

.208 .164 2.76111 .208 4.735 1

a. Predictors: (Constant), change_in_household__final_consumption_expenditure

ANOVAb

Model Sum of Squares df Mean Square F Sig.

1 Regression 36.101 1 36.101 4.735 .043a

Residual 137.227 18 7.624

Total 173.329 19

a. Predictors: (Constant), change_in_household__final_consumption_expenditure

b. Dependent Variable: percentage_growth