1003356 Deals Quarterly v11 - hbcbg.com and researches/Deals Quarterly... · Deals Quarterly Issue...

20

Cautious optimism Analysis of transactions in the global consumer products sector Consumer Products Deals Quarterly Issue 1 September–December 2009

Transcript of 1003356 Deals Quarterly v11 - hbcbg.com and researches/Deals Quarterly... · Deals Quarterly Issue...

Cautious optimismAnalysis of transactions in the global consumer products sector

Consumer Products Deals Quarterly

Issue 1 September–December 2009

Cautious optimism Analysis of transactions in the global consumer products sector

Welcome Welcome to Consumer Products Deals Quarterly — a new report from Ernst & Young that analyzes acquisitions and disposals in the global consumer products sector.

Using data collected by FactSet Mergerstat and insight from our global specialists, we assess what’s driving deals today, which geographies and subsectors are most active and who the key players are.

Building out our analysis of key trends, we also look ahead to consider what may happen in the deal space in the next few months.

We hope that this data and the perspectives we offerwill be of use to the leaders of consumer products companies and to the fi nancial investors who continueto focus on this sector. We are happy to provide further insight on request.

David MurrayGlobal Transactions Leader, Consumer [email protected]

Contents

Overview 1Early 2010 will be the turning point

Top 10 deals 4Analyzing movers and shakers

Geographic focus 7Emerging markets hold the key

China tops the league Brazil attracts foreign investors India is on the up

Sector focus 11HPC bucks the trend

No smoke without fi re

Methodology 15

Contacts 16

1Cautious optimism Analysis of transactions in the global consumer products sector

Lack of confi dence and fi nance have been holding back deal volumes and slowing the rate of progress on deals across the board. However, we believe that the signifi cant deals announced in Q4 09 and at the start of Q1 10 mean we are now at or near the bottom of the market.

The biggest of these by some margin was Kraft’s revised offer for Cadbury, which valued the business at US$18.9b. The takeover will, according to Kraft, create a “global confectionery leader.”

Other signifi cant deals dominating the headlines in early January 2010 include the announcement that Heineken is buying the beer operations of Femsa in Mexico in an all-stock deal valued at US$7.7b. Nestlé too made an active start to the year. It sold its 52% stake in eye-care products maker Alcon to Novartis for US$28b and announced its intention to acquire the US frozen pizza business of Kraft for US$3.7b.

We expect these deals to have a “snowball effect,” encouraging other smaller players to make a move. Deal volumes could start to climb out of the 150 to 250 per quarter range, which has been the norm for the past 12 months. Given Q4 09 volumes were around 55% below the peak seen in Q2 07, there may be a level of pent-up demand to come through in 2010.

This pattern would dovetail with the general view that the worst of the recession ended in August/September 2009, and that we are now in the fi rst phase of a global recovery in which businesses will look to capitalize on opportunities as they become apparent in the marketplace.

Early 2010 will be the turning pointThere is a mood of cautious optimism among deal-makers in the consumer products sector as we move into 2010. Although the last quarter of 2009 saw the lowest volume of deals announced for three years, we are pleased to note that strategic deals are happening, private equity is active and average deal sizes are holding up. We expect confi dence at the top end to encourage greater activity in the middle tier, so that deal volumes should start to recover in early 2010.

Overview

Data highlights Q4 09Volumes are fallingThere were 169 consumer products deals announced in Q4 09, 18% down on Q3 09. This is the lowest number of deals recorded since our records began in Q1 07 and 55% below the deal peak in Q2 07.

Values are holding upDeal values (excluding mega deals of more than US$5b) are holding up, averaging US$140m, a 6% increase on the prior quarter and 116% higher than the low point in Q3 07 when the average deal value was only US$65m.

Private equity is still activePrivate equity (PE) consistently accounts for between 10%–20% of deals by volume and was involved in the 2 largest deals in Q4 09.

Europe dominates in cross-border dealsEurope made the greatest number of cross-border acquisitions in Q4 09 (25) followed by the US (12) and Asia Pacifi c (10). The UK accounted for 46% of the value of businesses acquired, dwarfi ng the US and Asia Pacifi c.

Emerging markets hitting the radarDeal volumes in emerging markets still lag those in more developed economies. However, fast-growing populations and a burgeoning middle class mean they represent a meaningful growth opportunity and will be an increasing driver of future deal activity in the consumer products sector.

2 Cautious optimism Analysis of transactions in the global consumer products sector

Deal volumes fallingOnly household and personal care (HPC) bucked the trend that saw deal volumes decline in every other consumer products subsector between Q3 09 and Q4 09. Lack of activity was most evident in the two subsectors that normally dominate the deal landscape — food and beverages.

Deal volumes Q1 07 to Q4 09

Deal values holding up While deal volumes in Q4 09 were disappointing, particularly in food where we had anticipated a higher level of activity, we are heartened that overall, average deal values are holding up.

At US$140m, the average deal size in Q4 09 was marginally up (6%) on Q3 09 and 116% above the low point in the third quarter of 2007. Although deal values have seen considerable volatility since we began keeping records in Q1 07, the overall trend has been positive, despite the recession.

Value of announced deals by subsector Q1 07 to Q4 091

PE a constant presenceThroughout the highs and lows of the market in the three years to Q4 09, PE has consistently accounted for between 10% and 20% of global consumer products deals by volume. There is no real pattern to investor activity in terms of buy/sell. Instead the common theme is that PE investors always seek to position themselves for an advantageous deal — seizing the opportunity to acquire or dispose of assets at an attractive price.

The two largest deals in Q4 09 both involved PE players. CVC Capital agreed to buy ABInBev’s nine breweries in Eastern Europe for US$2.2b, and Top Frontier Investment acquired a 28% minority stake in brewer San Miguel.

PE vs. corporate deals Q1 07 to Q4 09

%

Q107

Q207

Q307

Q407

Q108

Q208

Q308

Q408

Q109

Q209

Q309

Corporate PE

Q409

0102030405060708090

100

Nu

mb

er

Q107

Q207

Q307

Q407

Q108

Q208

Q308

Q408

Q109

Q209

Q309

Q409

Food TobaccoBeverages HPC

0

50

100

150

200

250

300

350

400360

376358 352

260

302273

216 207237

205169

Strategic deals are happening. While recovery will not be immediate or straight line, the mood is confi dent as we move into 2010.

Ave

rag

e d

eal

val

ue

(U

S$

b)

To

tal d

eal

val

ue

(U

S$

b)

Q107

Q207

Q307

Q407

Q108

Q208

Q308

Q408

Q109

Q209

Q309

Average deal value

Q409

Food TobaccoBeverages HPC

0

5

10

15

20

25

0.000.020.040.060.080.100.120.140.160.180.20

1 Excluding deals above US$5b to highlight underlying trend.

3Cautious optimism Analysis of transactions in the global consumer products sector

Europe dominates in cross-border dealsEurope accounted for more deals by volume and value in Q4 09 than any other region.

VolumeCompanies in Europe acquired 25 businesses (37% of deal volume) and sold 24 businesses (35% of deal volume) in Q4 09. The US and Asia Pacifi c bought 12 and 10 businesses respectively in the same period and sold 9 (US) and 12 (Asia Pacifi c).

ValueThe picture in terms of value is not very different, except the role of UK companies as dealmakers comes sharply into focus. At US$2.3b, the UK accounted for almost half (46%) of the value of businesses acquired in Q4 09, dwarfi ng the US and Asia Pacifi c. However, on the sell side, European companies (excluding the UK) were most active in Q4 09, accounting for 64% of total deal value, followed by companies in Asia Pacifi c (16% of the value of deals).

Emerging markets hitting the radarAlthough deal volumes in emerging markets still lag those in developed economies by some margin, in part because much of the activity in these centers concerns privately held or family businesses, Q4 09 saw 10 deals involving China, 8 Brazil and 7 India. Fast-growing populations dominated by a growing number of young, middle-class consumers are an opportunity that no consumer products business can afford to ignore.

Faced with stagnant mature markets (even as the recession recedes), emerging markets undoubtedly represent the most meaningful growth opportunity for all consumer products companies — inevitably they will be an increasing driver of future deal activity.

Canada

Asia Pacific

Japan

US

India

Europe

UK

Other

South Korea

Seller region by volumeQ4 09

Buyer region by volumeQ4 09

37%

18%

15%

13%4%

4%4%

3%1%

35%

13%

18%

16% 9%

1%7%

Canada

Asia Pacific

Japan

US

India

Europe

UK

Other

South Korea

26%46%

9%7%

3%7%

1%1%

64%

16%

7%

10%3%

0% 0%

Seller region by valueQ4 09

Buyer region by valueQ4 09

We expect the strategic deals to have a “snowball effect” encouraging other smaller players to make their move.

4 Cautious optimism Analysis of transactions in the global consumer products sector

Analyzing movers and shakers

Highlights of 2009In 2009, beverages dominated the consumer products deal landscape, accounting for 80% of the top 10 deals. Assessing the drivers behind deals over the year, four broad trends are immediately apparent:

Japanese companies are on the march

PE has staying power

Desire to de-leverage is strong

Companies need to manage risk and their portfolios

In our fi rst issue of Consumer Products Deals Quarterly, we are taking the opportunity to highlight what we believe are the key trends that drove market activity in 2009, focusing on the top 10 deals for the calendar year and the motivation behind those deals. In future issues we will focus on activity and drivers for the quarter.

Buyer nameSeller name/unit name

Disclosed value (US$b) Announced Deal type Sector Synopsis

PepsiCo, Inc. Pepsi Bottling Group, Inc.

5.1 20 Apr 2009 Corporate Beverages PepsiCo, Inc. entered into a defi nitive agreement to acquire the 66.9% stake of Pepsi Bottling Group, Inc. that it does not already own for approximately US$5.1b in cash and stock.

Suntory Holdings Ltd.

Orangina Schweppes SAS

3.8 22 Sep 2009 Corporate Beverages On 22 September 2009, Suntory Holdings Ltd. made a binding offer to acquire Orangina Schweppes SAS from Blackstone Group LP and Lion Capital LLP for EUR2.6b (US$3.8b).

Kirin Holdings Co. Ltd.

Lion Nathan Ltd. 2.5 27 Apr 2009 Corporate Beverages Kirin Holdings Co. Ltd. agreed to acquire the remaining 53.9% majority stake of Australian brewer Lion Nathan Ltd. for approximately AUD3.5b (US$2.5b) by way of a scheme of arrangement in cash.

CVC Capital Partners Ltd.

ABInBev SA 2.2 15 Oct 2009 PE Beverages CVC Capital Partners Ltd. completed its agreement to acquire the business and assets of ABInBev SA’s nine breweries in Eastern European countries for an enterprise value of EUR1.5b (US$2.2b) in cash.

PepsiCo, Inc. PepsiAmericas, Inc.

2.0 20 Apr 2009 Corporate Beverages PepsiCo, Inc. entered into a defi nitive agreement to acquire the 57% stake of PepsiAmericas, Inc. that it does not already own for approximately US$2b in cash and stock.

Perdigao SA Sadia SA 2.0 19 May 2009 Corporate Food Perdigo SA, a Brazilian food manufacturer merged with Sadia SA, a smaller local rival, for BRL4.12b (US$2.01b) in stock.

Unilever Plc Sara Lee Corp. 1.9 25 Sep 2009 Corporate HPC Unilever Plc made a binding offer to acquire the business and assets of the personal care business from Sara Lee Corp. for EUR1.28b (US$1.88b) in cash.

Oriental Brewery Co. Ltd./Private Group 2

ABInBev SA 1.8 7 May 2009 PE Beverages A consortium formed by Kohlberg Kravis Roberts & Co. LP and Affi nity Equity Partners (S) Pte Ltd. acquired South Korean beer maker Oriental Brewery Co. Ltd. from ABInBev SA for KRW2,299 trillion (US$1.8b).

Top Frontier Investment Holdings, Inc.

San Miguel Corp. Retirement Plan

1.4 27 Nov 2009 PE Beverages Top Frontier Investment Holdings, Inc. acquired a 28% minority stake in San Miguel Corp. from San Miguel Corp. Retirement Plan for a consideration of PHP64.3b (US$1.4b) in cash.

Kirin Holdings Co. Ltd.

San Miguel Corp. 1.3 20 Feb 2009 Corporate Beverages Kirin Holdings Co. Ltd. a Tokyo listed beer brewer and distributor, acquired a 43.2% minority stake in San Miguel Brewery Inc. from San Miguel Corp. for PHP58.925b (US$1.3b) in cash.

Top 10 deals based on disclosed value (corporate and PE, full year 2009)

Top 10 deals

5Cautious optimism Analysis of transactions in the global consumer products sector

Japan on the marchEmpowered by the sudden improvement in the value of the Yen as the economy emerged from 20 years of stagnation, Japanese companies were prominent in this year’s statistics as they seized the opportunity to diversify out of a low-growth domestic market characterized by an aging population in which 22.7% of people were over 65 in 20092. This proportion is expected to rise to 35.7% by 20503.

The combination of a strong Yen and the availability of attractive overseas assets meant conditions in 2009 were favorable for Japanese companies. Starved of local corporate development opportunities through the long years of economic stagnation, Japanese buyers were keen to gain exposure to higher-growth markets in developed and emerging economies to balance out over-exposure to their own mature domestic market.

These were the primary drivers behind many of the Japanese deals in the consumer products deal landscape in 2009. These included the purchase by Suntory of soft drink manufacturer Orangina Schweppes in France and Kirin’s acquisition of both a majority stake in Australian brewer Lion Nathan and a signifi cant minority stake in Filipino food, beverage and packaging company San Miguel.

We believe that the Suntory group’s motto “Yatte Minahare” or “Go for it” neatly summarizes the mood of Japanese businesses in 2009.

PE has staying powerPE remained active in the sector throughout the year and was prominent within the top tier of deals on both the buy and sell sides.

The number 2 deal of the year — the sale of Orangina Schweppes for US$3.8b — represented a timely exit at a good return for Blackstone and Lion Capital. Likewise, the cash purchase of ABInBev’s 9 breweries in Eastern Europe for an enterprise value of US$2.2b by CVC Capital demonstrated the PE group’s confi dence in its ability to add further value.

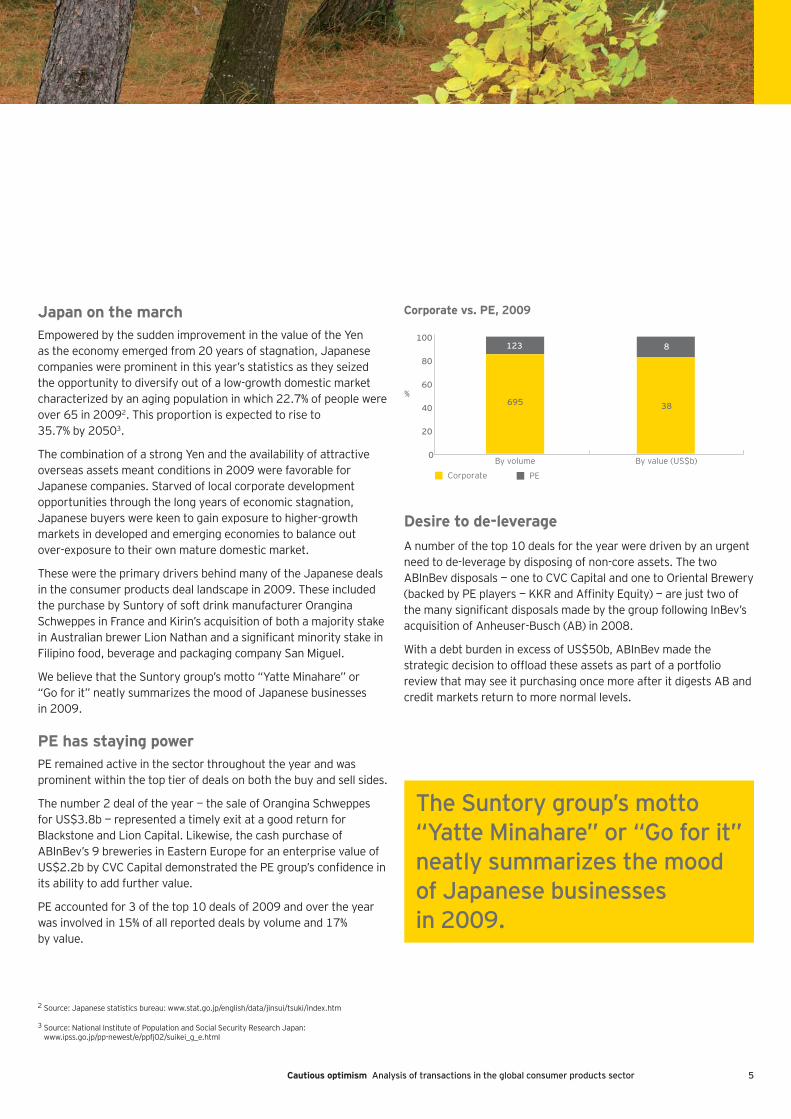

PE accounted for 3 of the top 10 deals of 2009 and over the year was involved in 15% of all reported deals by volume and 17% by value.

Corporate vs. PE, 2009

Desire to de-leverageA number of the top 10 deals for the year were driven by an urgent need to de-leverage by disposing of non-core assets. The two ABInBev disposals — one to CVC Capital and one to Oriental Brewery (backed by PE players — KKR and Affi nity Equity) — are just two of the many signifi cant disposals made by the group following InBev’s acquisition of Anheuser-Busch (AB) in 2008.

With a debt burden in excess of US$50b, ABInBev made the strategic decision to offl oad these assets as part of a portfolio review that may see it purchasing once more after it digests AB and credit markets return to more normal levels.

%

Corporate PE

0

20

40

60

80

100

By volume By value (US$b)

695 38

123 8

2 Source: Japanese statistics bureau: www.stat.go.jp/english/data/jinsui/tsuki/index.htm

3 Source: National Institute of Population and Social Security Research Japan: www.ipss.go.jp/pp-newest/e/ppfj02/suikei_g_e.html

The Suntory group’s motto “Yatte Minahare” or “Go for it” neatly summarizes the mood of Japanese businesses in 2009.

6

Managing risk Risk management was one of the drivers behind PepsiCo’s decision to repurchase two thirds of its bottling group for US$5.1b in a combination of cash and stock. The company was particularly concerned to safeguard its ability to get its product to market — irrespective of economic conditions. Vertical integration ensured the integrity of its value chain from manufacture to shelf.

Other drivers of this transaction included the desire to eliminate costs and to drive growth through a seamless introduction of new products.

The ABInBev deals likewise could be seen as part of the trend to manage risk — in this case the risk of debt default.

Managing the portfolioBy contrast, the sale by Sara Lee of its personal care business to Unilever for US$1.9b in cash is perhaps the most “normal” of the year’s deals in that it was driven by the core strategic agenda rather than external factors such as the recession, pressure to de-leverage or the need to take advantage of currency strength. The brands it sold as part of this deal were no longer core to Sara Lee’s future but complemented Unilever’s offering in this space.

The Japanese deals also could be viewed through the lens of portfolio management, though timing was driven by other factors, as we have outlined.

Cautious optimism Analysis of transactions in the global consumer products sector

Top 10 deals as a percentage of total deals

Q1 07 Q2 07 Q3 07 Q4 07 Q1 08 Q2 08 Q2 08 Q4 08 Q1 09 Q2 09 Q3 09 Q4 09

Value of total top 10 deals (US$b)

7.4 18.1 53.3 13.7 33.9 82.7 20.0 7.7 5.1 16.4 9.0 7.2

Total value of all deals (US$b)

12.5 23.4 58.8 23.1 37.5 88.9 23.0 10.0 6.5 18.5 10.9 10.0

Top 10 as % of total value 59% 77% 91% 59% 90% 93% 87% 77% 79% 89% 83% 72%

The combination of a large (and predominantly young) population base with a growing, increasingly prosperous middle class keen to try new brands is a strong attraction for businesses in every geography, particularly those facing zero or at best incremental growth in their domestic markets. Expansion into emerging markets is made even more attractive when asset values are depressed and exchange rates are favorable.

One potential cloud on the horizon, however, is that some investors are starting to regard emerging market acquisitions with greater caution as they become more expensive and more diffi cult as competition increases.

Brazil top for cross-border deals in Q4 09It is apparent from our data for Q4 09 that companies looking to diversify into emerging markets are focusing on Brazil and Russia. It is also apparent that the impact of the recession has been uneven across markets. Russia saw a much lower level of deal activity in Q4 09 than was apparent in Q4 08.

For Q4 09, Brazil and Russia were the most attractive emerging markets to foreign investors, with a good proportion of deals in those countries involving sales of a domestic company to a foreign buyer (labeled in the charts as foreign sales). In China and India, by contrast, the majority of deal activity during this period was in-border — local companies acquiring or disposing within the country.

Number of deals in Brazil, China, India and Russia, Q4 09

China most active in 2009More deals were concluded in China in 2009 than in any other emerging market. The majority of these (35 out of a total of 60 deals) were in-border. Only 8 of the 60 were acquisitions by Chinese companies of foreign targets, and 17 were sales to foreign buyers. Brazil, by contrast, was the country that acquired the most foreign businesses in 2009, notching up 11 deals over the period. India also was active in the acquisition of foreign companies, with a total of 9 deals.

Number of deals in Brazil, China, India and Russia, 2009

In-border Foreign sale Foreign acquisition

0

5

10

15

20

25

30

35

40

RussiaIndiaChinaBrazil

7Cautious optimism Analysis of transactions in the global consumer products sector

Emerging markets hold the keyProfi table growth is the holy grail for consumer products companies across every subsector. For those with strong balance sheets, that often means expansion into emerging markets.

In-border Foreign sale Foreign acquisition

0123456789

10

RussiaIndiaChinaBrazil

Foreign acquisition — an acquisition by a domestic company of a foreign targetForeign sale — a sale of a domestic company to a foreign buyerIn-border — a sale or acquisition involving companies within the same country

Geographic focus

8 Cautious optimism Analysis of transactions in the global consumer products sector

China tops the leagueWith a population of 1.3 billion, China is a market that no consumer products company can afford to ignore.

Over the calendar year, economic growth accelerated to 8.7%, retail sales of consumer products achieved growth of 16.9% and, signifi cantly, rural retail sales growth outpaced growth in urban sales as a result of a series of government initiatives to boost consumption through the recession.

Central and Western China is home to 60% of the country’s population, so rising sales here — albeit government subsidized — are indicative of even stronger growth potential to come.

We believe that acquisition opportunities are now available at attractive prices as companies experiencing fi nancial diffi culties are keen to fi nd investors. Further industry consolidation is likely to take place this year as companies with strong cash reserves look to acquire assets that are a good strategic fi t for their business.

One potential complication is the enactment of the Anti-Monopoly

Law in August 2008 that introduced a mandatory regime for the oversight of mergers, acquisitions and joint ventures.

Buyer name Seller name/unit name Disclosed value (US$m) Announced Deal type Sector

COFCO Ltd. Maverick Food Co., Ltd. 28.4 24 Dec 2009 Corporate Food

China Kangda Food Co. Ltd. Weifang Zhixing Investment Co. Ltd. / Highway Investment Group Co. Ltd.

19.0 14 Oct 2009 Corporate Food

Tibet Galaxy Science & Technology Development Co. Ltd.

Shenzhen Changhe Yuntong Investment Co. Ltd.

19.0 25 Dec 2009 Corporate Beverages

China Organic Agriculture, Inc. Changbai Eco-Beverage Co. Ltd. 10.3 21 Dec 2009 Corporate Food

Shandong Andre Group Co. Ltd. Yantai North Andre Juice Co. Ltd. 3.7 11 Nov 2009 Corporate Food

Billionlink Holdings Ltd. PME Group Ltd. 0.04 9 Dec 2009 Corporate HCP

Trump Dragon Distillers Holdings Ltd.

Dukang Investment Group Ltd./Yichuan Dukang Distillers Asset Management Ltd.

NA 1 Oct 2009 Corporate Beverages

Trump Dragon Distillers Holdings Ltd.

Dukang Investment Group Ltd./Henan Dukang Distillers Co. Ltd.

NA 1 Oct 2009 Corporate Beverages

Trump Dragon Distillers Holdings Ltd.

Bai Rui Trust Ltd./Ruyang Siji Trading Co. Ltd.

NA 1 Oct 2009 Corporate Beverages

Trump Dragon Distillers Holdings Ltd.

Bai Rui Trust Ltd./Ruyang Dukang Distillers Co. Ltd.

NA 1 Oct 2009 Corporate Beverages

NA: information was not available as no values were disclosed for these deals.

Deal summaryTen deals were announced in China in Q4 09, 9 of which were in-border and 1 of which was cross-border. Nine of the deals were corporate (5 in beverages, 4 in food).

Over 2009 as a whole, 60 deals were disclosed involving Chinese companies, compared with 71 in 2008 and 94 in 2007. For each of these years, the number of in-border deals has always accounted for the lion’s share of transactions, and acquisitions of foreign assets are always the smallest proportion of deals overall.

4 Billionlink Holdings paid a nominal US$1.30 for the acquisition of PME.

Deals in Q4 09

9Cautious optimism Analysis of transactions in the global consumer products sector

Buyer name Seller name/unit name Disclosed value (US$m) Announced Deal type Sector

Shree Renuka Sugars Ltd. Vale do Ivai SA Açucar e Álcool 81.6 11 Nov 2009 Corporate Food

Bom Gosto Laticinios SA LAEP Capital LLC 36.9 25 Nov 2009 Corporate Food

Sao Martinho SA Mitsubishi Corp. 14.0 30 Nov 2009 Corporate Food

Cosan SA Industria e Comercio Petrosul Distribuidora Transp Com Combustivel Ltda.

NA 14 Dec 2009 Corporate Food

Louis Dreyfus et Cie SA Santelisa Vale SA NA 26 Oct 2009 Corporate Food

Illinois Tool Works, Inc. Luvex - Industria de Equipamentos de Proteçao Ltda.

NA 3 Nov 2009 Corporate HCP

Arfei Comercio e Participaçoes Ltda.

Grupo Aresti NA 17 Dec 2009 Corporate Food

JBS SA Vion Holding NV NA 15 Dec 2009 Corporate Food

NA: information was not available as no values were disclosed for these deals.

Brazil attracts foreign investorsBrazil has certainly benefi ted from the BRIC “brand” coined by Goldman Sachs Chief Economist Jim O’Neill in 2001. It raised the country’s profi le and put Brazil on the business radar in a way it might never have achieved independently. But there is more to Brazil than a handy acronym.

Brazil is the largest consumer products market in Latin America. With a domestic population of 180 million, it dwarfs its nearest rival Mexico (100 million) and is far larger than its neighbors Venezuela, Colombia, Peru and Argentina where populations range from 25 million to 40 million. It also has the advantage that the consumer base is homogenous — the single language and common culture make the market relatively easy, and economic, to access.

Stability is another feature in Brazil’s favor. Over the past 10 years it appears to have kicked the boom-bust cycle that had characterized its economy previously. Increased stability has been accompanied by rising prosperity — 52% of the population has enjoyed annual income levels greater than US$4,000 since 2008 (compared to 42% in 2004) and the formal employment index has marked a steady ascent since 2000. With the Brazilian Real appreciating against the US Dollar, more local consumers than ever have both the appetite and the cash to experiment with foreign brands.

Brazil is also rated highly in the region for PE and venture capital opportunities, according to the Latin America Venture Capital Association. It has favorable laws in terms of fund start-up and operation, protection of minority shareholder rights and bankruptcy

protection. It also has a relatively mature fi nancial services industry and capital markets — facilitating leverage and IPO exits — and is moving toward convergence with IFRS accounting standards.

Although the World Bank rates Brazil in the bottom quartile in the region in terms of the ease of starting a business and the amount of operational red-tape, and close to the worst from a tax burden standpoint, investors continue to favor Brazil over its neighbors.

Looking further ahead, the World Cup in 2014 and the Olympics in 2016 will encourage investment in infrastructure and prove a signifi cant boost to the domestic economy, extending the party for some time to come.

* Foreign acquisition — an acquisition by a domestic company of a foreign target.

Deal summaryEight deals were announced in Brazil in Q4 09, six of which were cross-border. All deals were in food bar one — the acquisition of HPC company Luvex by Illinois Tool Works.

Over the year as a whole, 28 deals were disclosed involving Brazilian companies, compared with 48 in 2008 and 54 in 2007. In 2009, the greatest proportion of deals (11) were foreign acquisitions*. In 2007 and 2008, by contrast, the greatest proportion of deals were in-border.

Deals in Q4 09

10

India is on the upAlthough India was affected by the recession, the impact was not as deep or as long-lasting as in the developed economies. The consumer products market is valued at US$240b5, GDP per capita is rising fast and the proportion of the population earning US$5,000-plus is increasing. One key factor driving growth is the consistent increase in demand for products among rural Indians.

Driven by India’s buoyant domestic economy, in which around 90%6 of the population is under 60, demand for consumer goods held up through 2009. Indian consumer goods companies continued to trade at a 50%7 premium to their foreign counterparts operating in developed economies. Refl ecting the confi dent mood of domestic business, the Sensex has risen by 90% since February 2009.

Companies have established a good track record of creating shareholder value, and it is not uncommon to fi nd companies in this sector generating a high return on capital employed. Strong earnings, healthy balance sheets and a rising stock market have combined to put Indian companies in a good position to initiate deals, particularly outbound where they can take advantage of attractively priced and complementary assets in countries with a complementary consumer base.

Target markets include Africa, South Africa, Indonesia, Malaysia and the Middle East — where similar tastes and skin tones create a ready market for goods produced in India. Such regions are a good strategic fi t, entry barriers are relatively low and there is less competition than in the US or Europe.

Conversely, inbound investment is unlikely to pick up signifi cantly while the pricing of Indian assets remains so buoyant. While deal volumes were depressed in 2009, there is a strong expectation that transactions will take off again in 2010.

Cautious optimism Analysis of transactions in the global consumer products sector

Deal summaryQ4 09 saw seven deals announced in India, of which three were cross-border. Most notable were Wipro’s acquisition of Yardley from UK-based Lornamead Group and Shree Renuka Sugars’ acquisition of Brazil-based sugar and ethanol manufacturer Vale do Ivai SA Açucar e Álcool.

Four deals were in the tea sector*, where companies are looking to strengthen their positioning in local markets. The acquisition by McLeod Russell subsidiary Borelli Teas of Rwenzori Tea from James Finlay in Uganda had been planned for some time and gives Borelli a base from which to build in Africa.

Over the year as a whole, 18 deals were disclosed involving Indian companies, compared with 35 in 2008 and 51 in 2007. In 2009, the greatest proportion of deals (nine) were foreign acquisitions**. In 2007 and 2008, by contrast, the greatest proportion of deals were in-border.

Buyer name Seller name/unit name Disclosed value (US$m) Announced Deal type Sector

Shree Renuka Sugars Ltd. Vale do Ivai SA Açucar e Álcool 81.6 11 Nov 2009 Corporate Food

Wipro Ltd. Lornamead Group 45.5 5 Nov 2009 Corporate HCP

McLeod Russel India Ltd. James Finlay Ltd./James Finlay International Holding Ltd.

25.1 23 Dec 2009 Corporate Food

United Spirits Ltd. Tern Distilleries Pvt Ltd. 2.9 23 Nov 2009 Corporate Beverages

Barak Valley Cements Ltd. Goombira Tea Estates Pvt Ltd. NA 7 Dec 2009 Corporate Food

Barak Valley Cements Ltd. Chargola Tea Co. Pvt Ltd. NA 7 Dec 2009 Corporate Food

Barak Valley Cements Ltd. Singlacherra Tea Co. Pvt Ltd. NA 7 Dec 2009 Corporate Food

NA: information was not available as no values were disclosed for these deals.

5 An appetite for growth — Opportunities in the Indian food industry, FICCI-Ernst & Young Food Report, November 2009.

6 Population Division of the Department of Economic and Social Affairs of the United Nations.

7 Ernst & Young internal analysis.

* Transactions in the tea sector are classifi ed as food.

** Foreign acquisition — an acquisition by a domestic company of a foreign target.

Deals in Q4 09

11Cautious optimism Analysis of transactions in the global consumer products sector

HPC bucks the trend

There were 36 fewer deals in Q4 09 compared to Q3 09, a drop of 18%. In large part this was due to the decline in volume of deals in the food subsector, which historically accounts for the greatest number of deals in the sector as a whole. Only the HPC subsector recorded an increase in the volume of deals (from 23 to 28).

Deal volume in Q4 09 for the sector as a whole was 22% down on the comparable quarter in 2008.

Volume of announced deals by subsector Q1 07 to Q4 09

In line with the historical trend, the subsector generating the greatest value this quarter was beverages. However, deal value fell in this subsector from US$4.7b in Q3 09 to US$4.3b in Q4 09.

Deal values Q1 07 to Q4 098

The only subsector to achieve an increase in deal volume in Q4 09 was HPC. Deal stalwarts, food and beverages, both suffered a lacklustre quarter.

Vo

lum

e o

f d

eal

s

Q107

Q207

Q307

Q407

Q108

Q208

Q308

Q408

Q109

Q209

Q309

Food TobaccoBeverages HPC

Q409

0

50

100

150

200

250

300

350

400

235259 239

222169 178 176

143 124 136 122 103

47

7 7

7

28

4 110

6

1

79

42

82

28

78

34

81

42

67

1785

37

56

33

43

26

61

2161

30

54

23

37

28

Sector focus

8 All deals including those over US$5b.

Ave

rag

e d

eal

val

ue

(U

S$

b)

To

tal d

eal

val

ue

(U

S$

b)

Q107

Q207

Q307

Q407

Q108

Q208

Q308

Q408

Q109

Q209

Q309

Average deal value

Q409

Food TobaccoBeverages HPC

0102030405060708090

100

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

12 Cautious optimism Analysis of transactions in the global consumer products sector

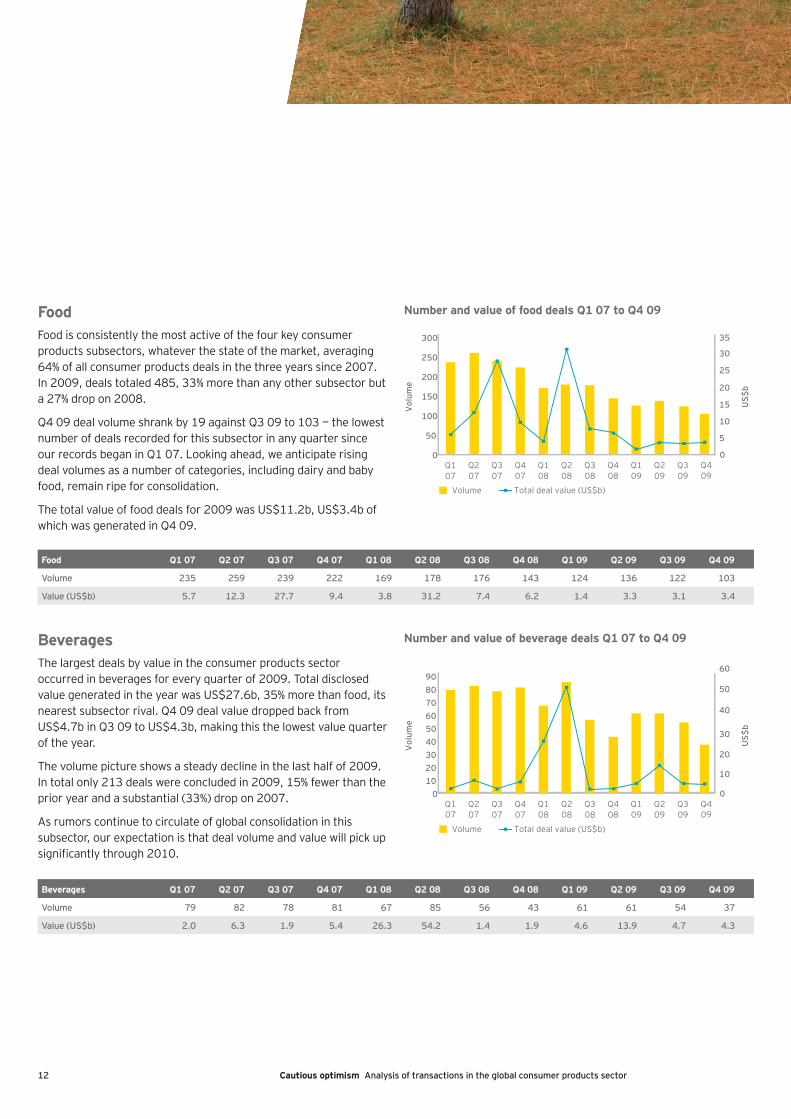

BeveragesThe largest deals by value in the consumer products sector occurred in beverages for every quarter of 2009. Total disclosed value generated in the year was US$27.6b, 35% more than food, its nearest subsector rival. Q4 09 deal value dropped back from US$4.7b in Q3 09 to US$4.3b, making this the lowest value quarter of the year.

The volume picture shows a steady decline in the last half of 2009. In total only 213 deals were concluded in 2009, 15% fewer than the prior year and a substantial (33%) drop on 2007.

As rumors continue to circulate of global consolidation in this subsector, our expectation is that deal volume and value will pick up signifi cantly through 2010.

Number and value of beverage deals Q1 07 to Q4 09

FoodFood is consistently the most active of the four key consumer products subsectors, whatever the state of the market, averaging 64% of all consumer products deals in the three years since 2007. In 2009, deals totaled 485, 33% more than any other subsector but a 27% drop on 2008.

Q4 09 deal volume shrank by 19 against Q3 09 to 103 — the lowest number of deals recorded for this subsector in any quarter since our records began in Q1 07. Looking ahead, we anticipate rising deal volumes as a number of categories, including dairy and baby food, remain ripe for consolidation.

The total value of food deals for 2009 was US$11.2b, US$3.4b of which was generated in Q4 09.

Number and value of food deals Q1 07 to Q4 09

US

$b

Vo

lum

e

Q107

Q207

Q307

Q407

Q108

Q208

Q308

Q408

Q109

Q209

Q309

Q409

Volume Total deal value (US$b)

0

50

100

150

200

250

300

0

5

10

15

20

25

30

35

Food Q1 07 Q2 07 Q3 07 Q4 07 Q1 08 Q2 08 Q3 08 Q4 08 Q1 09 Q2 09 Q3 09 Q4 09

Volume 235 259 239 222 169 178 176 143 124 136 122 103

Value (US$b) 5.7 12.3 27.7 9.4 3.8 31.2 7.4 6.2 1.4 3.3 3.1 3.4

US

$b

Vo

lum

e

Q107

Q207

Q307

Q407

Q108

Q208

Q308

Q408

Q109

Q209

Q309

Q409

Volume Total deal value (US$b)

0

10

20

30

40

50

60

70

80

90

0

10

20

30

40

50

60

Beverages Q1 07 Q2 07 Q3 07 Q4 07 Q1 08 Q2 08 Q3 08 Q4 08 Q1 09 Q2 09 Q3 09 Q4 09

Volume 79 82 78 81 67 85 56 43 61 61 54 37

Value (US$b) 2.0 6.3 1.9 5.4 26.3 54.2 1.4 1.9 4.6 13.9 4.7 4.3

13Cautious optimism Analysis of transactions in the global consumer products sector

TobaccoThe tobacco subsector is now largely consolidated with the expectation that going forward, the major global players will concentrate on smaller deals to build local scale. Only one deal was announced in Q4 09 at a value of US$45m. The total number of deals for the year was 18 at an aggregate value of US$1.6b.

Number and value of tobacco deals Q107 to Q409

HPCSince Q1 07, the HPC subsector has consistently been the third largest generator of consumer products deals by volume. In Q4 09, however, HPC was the only subsector to record an increase in the number of deals compared with the prior quarter. Deal volumes were up by 5, taking the total for the quarter to 28 and the aggregate value to US$2.3b for the quarter and US$5.3b for the calendar year.

Number and value of HPC deals Q1 07 to Q4 09

US

$b

Vo

lum

e

Q107

Q207

Q307

Q407

Q108

Q208

Q308

Q408

Q109

Q209

Q309

Q409

Volume Total deal value (US$b)

0

2

4

6

8

10

12

02468101214161820

Tobacco Q1 07 Q2 07 Q3 07 Q4 07 Q1 08 Q2 08 Q3 08 Q4 08 Q1 09 Q2 09 Q3 09 Q4 09

Volume 4 7 7 7 7 2 8 4 1 10 6 1

Value (US$b) 2.2 0.0* 17.9 4.2 7.3 NA 12.3 NA NA 0.8 0.8 0.0*

NA: information was not available as no values were disclosed for these deals.* Total deal value is less than US$0.05b.

US

$b

Vo

lum

e

Q107

Q207

Q307

Q407

Q108

Q208

Q308

Q408

Q109

Q209

Q309

Q409

Volume Total deal value (US$b)

0

5

10

15

20

25

30

35

40

45

0

2

4

6

8

10

12

HPC Q1 07 Q2 07 Q3 07 Q4 07 Q1 08 Q2 08 Q3 08 Q4 08 Q1 09 Q2 09 Q3 09 Q4 09

Volume 42 28 34 42 17 37 33 26 21 30 23 28

Value (US$b) 2.6 4.8 11.3 4.1 0.2 3.6 1.8 1.9 0.4 0.4 2.3 2.3

14 Cautious optimism Analysis of transactions in the global consumer products sector

No smoke without fi reAfter an active Q3 09 in which the tobacco subsector announced 6 deals, 2 of which were in the top 10 for the quarter, Q4 09 was very quiet with only one deal announced at a value of US$45m. The total number of deals for the year was 18 at an aggregate value of US$1.6b. Most deal activity was focused on diversifi cation away from conventional cigarette products, refl ecting increasing regulatory pressure. An example of this was the comparatively small Q4 09 acquisition of Swedish smoking cessation company Niconovum by Reynolds American. Of great interest to industry watchers, the deal marked the fi rst move by a tobacco company into nicotine replacement, a segment dominated by the pharmaceutical industry.

In the tobacco subsector, the Big 4 companies — British American Tobacco, Japan Tobacco, Philip Morris International and Imperial Tobacco — have emerged as the victors in what is now a highly consolidated industry. These key players have plenty of fi repower and are actively seeking to build scale through further local acquisitions. This suggests there will be a high level of competition for quality local assets.

In Q3 09, Philip Morris International announced plans to acquire Protabaco (La Productora Tabacalera) in Colombia for US$452m and Swedish Match in South Africa for US$223m. Both of these acquisitions serve to enhance access to fast-growth markets and, in the case of the Swedish Match acquisition, facilitate the expansion into smokeless products.

Meanwhile, the decision by Japan Tobacco to acquire two Kannenberg leaf tobacco and processing businesses in Brazil, was interpreted as part of wider moves to secure quality leaf supply and reduce cost volatility.

What drove deals in the sector?Reopening debt markets, valuations at all-time lows, declining costs and sturdy balance sheets have been the key deal drivers in the tobacco subsector, along with the continuing need for major players to look for growth outside declining developed markets.

In general, businesses in this sector are not highly leveraged and enjoy a substantial cash fl ow that has proved to be reasonably recession-proof. Combine this with an improving outlook and the sense that further consolidation in this subsector would be value-creating at reasonable multiples, and there is a clear case for more deal activity to follow into 2010.

Emerging markets and innovative productsAccess to emerging markets and non-conventional products will be key drivers of deal activity.

State privatizations are likely to be one source of appreciable new value. Egypt, Iran, Macedonia, Thailand and Vietnam are among those markets where a full privatization, or the sale of a sizeable government stake, are expected in the short to medium term. All of the international players are trying to rationalize their global portfolio and see the acquisition of state monopolies or privately held businesses in emerging markets as an opportunity to acquire a platform from which they can introduce their global brands to large local markets.

Companies are keen to make the move because of the signifi cant opportunities to eliminate manufacturing overlap, combine sales and distribution efforts and increase purchasing and manufacturing scale.

In terms of alternative products, players specializing in smokeless products, including snus and other innovations, will be high on the target list.

All of the international players are trying to rationalize their global portfolio and see the acquisition of state monopolies or privately held businesses in emerging markets as an opportunity.

15Cautious optimism Analysis of transactions in the global consumer products sector

MethodologyData source and industry scopeConsumer Products Deals Quarterly is based on Ernst & Young’s analysis of FactSet Mergerstat data from Q1 07 to Q4 09. Data was pulled from the FactSet Mergerstat database using standard industrial classifi cation codes.

For the purposes of this publication, our defi nition of consumer products is only those companies in the food, beverages, tobacco and HPC subsectors.

Deal activity and valuations may fl uctuate slightly based on the date that the Factset Mergerstat database is accessed.

Qualifying dealsDeals include:

Deal transactions between companies in the four consumer products subsectors

Consumer products companies acquiring businesses in other subsectors

Non-consumer products companies acquiring consumer products companies

PE deal activity includes both full- and partial-stake transactions and was analyzed based on acquisitions by fi rms classifi ed as PE, alternative investment management groups, certain commercial banks, investment banks, venture capital and other similar entities

For non-consumer products acquirers, deals were classifi ed based on the consumer products sector of the seller

Equity investments were included (corporate and PE)

Joint ventures were not included

The value and status of all deals highlighted in this report are as at 31 December 2009

All dollar amounts are in US$ unless otherwise indicated

There is no minimum US$ deal threshold

Unsolicited consumer products deal values were not included in the dataset unless the proposed bid was accepted and the deal closed based on FactSet Mergerstat data available at the time of analysis

Only disclosed deal values (as per FactSet Mergerstat) are used in all value analyses

As used in this report, “total value” refers to the aggregate value of deals with disclosed values for the period under discussion

16 Cautious optimism Analysis of transactions in the global consumer products sector

ContactsCountry Local contact Email/telephone

Global/EMEIA David MurrayPartnerGlobal Transactions Leader, Consumer Products

[email protected] +44 (0)158 264 3248

Far East Robert PartridgePartnerTransaction Advisory Services Leader

[email protected] +852 2846 9973

India Pinakiranjan MishraPartnerIndia Retail & Consumer Products

[email protected]+91 22 4035 6300

Japan Michael BuxtonPartnerTransaction Advisory Services Leader

[email protected] +81 3 5401 7100

Latin America Jeremy BarnesPrincipalTransaction Advisory Services

[email protected] +1 305 415 1379

USA Gregory StemlerPartnerTransaction Advisory Services

[email protected] +1 312 879 3351

17Cautious optimism Analysis of transactions in the global consumer products sector

About Ernst & YoungErnst & Young is a global leader in assurance, tax, transaction and advisory services. Worldwide, our 144,000 people are united by our shared values and an unwavering commitment to quality. We make a difference by helping our people, our clients and our wider communities achieve their potential.

For more information, please visit www.ey.com.

Ernst & Young refers to the global organization of member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

EYG no. XX0000

© 2010 EYGM Limited.All Rights Reserved.

In line with Ernst & Young’s commitment to minimize its impact on the environment, this document has been printed on paper with a high recycled content.

This publication contains information in summary form and is therefore intended for general guidance only. It is not intended to be a substitute for detailed research or the exercise of professional judgment. Neither EYGM Limited nor any other member of the global Ernst & Young organization can accept any responsibility for loss occasioned to any person acting or refraining from action as a result of any material in this publication. On any specific matter, reference should be made to the appropriate advisor.

1003356.indd (UK) 02/2010. Creative Services Group.

Assurance | Tax | Transactions | Advisory

Ernst & Young