10 - Variance Analysis

48

Variance Analysis Variance Analysis Moscow Training September 2008 Moscow Training September 2008

Transcript of 10 - Variance Analysis

Variance AnalysisVariance AnalysisMoscow Training September 2008Moscow Training September 2008

•Overview

•Variances- What do they tell me?

•Ownership

•Variance Release Policy

•Types of VariancesPurchase Price Variance (PPV)

Plant Sourcing Variance (PSV)

Revaluation

Production Order Variance (POV)

Staging Area Variance

Production Activity Variance (PAV)

MOE Variance

Agenda

Overview of TMC Variances*

• TMC Variances represent the difference between actual costs and standard costs and are used to assess performance versus the plan.

• Variance analysis should focus on areas where the costs vary significantly from the annual standard costs.

• The objective of variance analysis is to understand why the costs are different from plan and to determine actions needed to address the variances.

* SAFE standard: COPS 3 Std Costing & Variance Reporting

• Current Operating Conditions different from planned/anticipated

• Physical Count Variations

• Master Data Errors

• Work Process Errors

• It is ok to have variances as long as we understand them

Variances-What do they tell me?

• Plant F&A

• GBU

Ownership

• The variance holding policy will ensure that, on

average across the Company, we are holding

variances on inventory that approximate the

number of days inventory that is on-hand.

*SAFE standard: Inventory 3- Inventory valuation

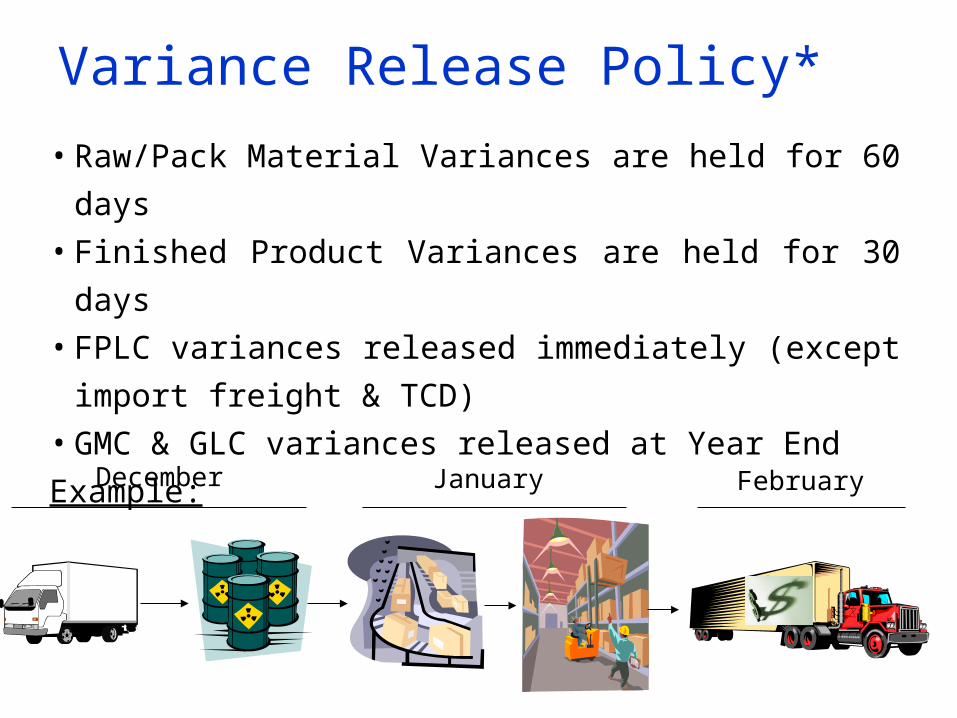

Variance Release Policy*

• Raw/Pack Material Variances are held for 60 days• Finished Product Variances are held for 30 days• FPLC variances released immediately (except

import freight & TCD)• GMC & GLC variances released at Year End

Example:

December January February

Variance Release Policy*

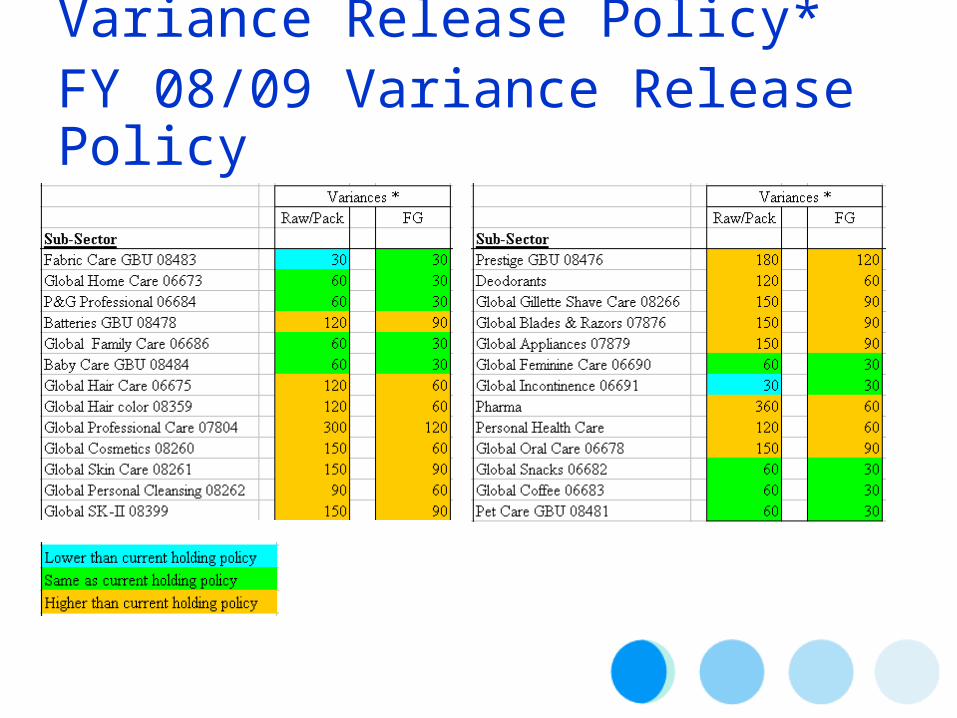

Variance Release Policy*FY 08/09 Variance Release Policy

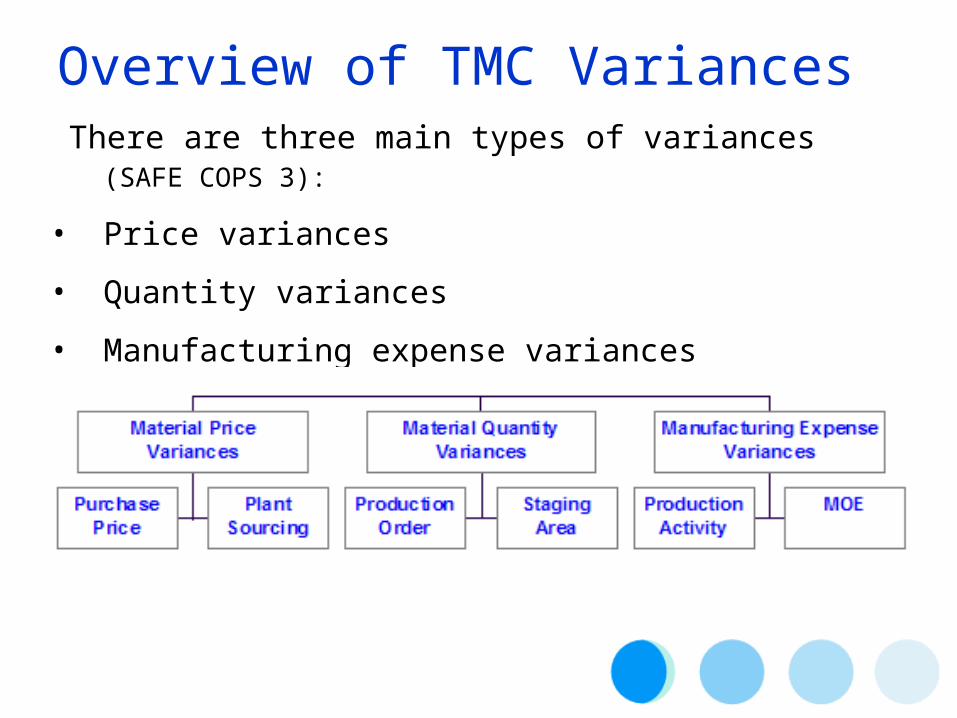

There are three main types of variances (SAFE COPS 3):

• Price variances

• Quantity variances

• Manufacturing expense variances

Overview of TMC Variances

•Purchase Price Variance

PRICE VARIANCES

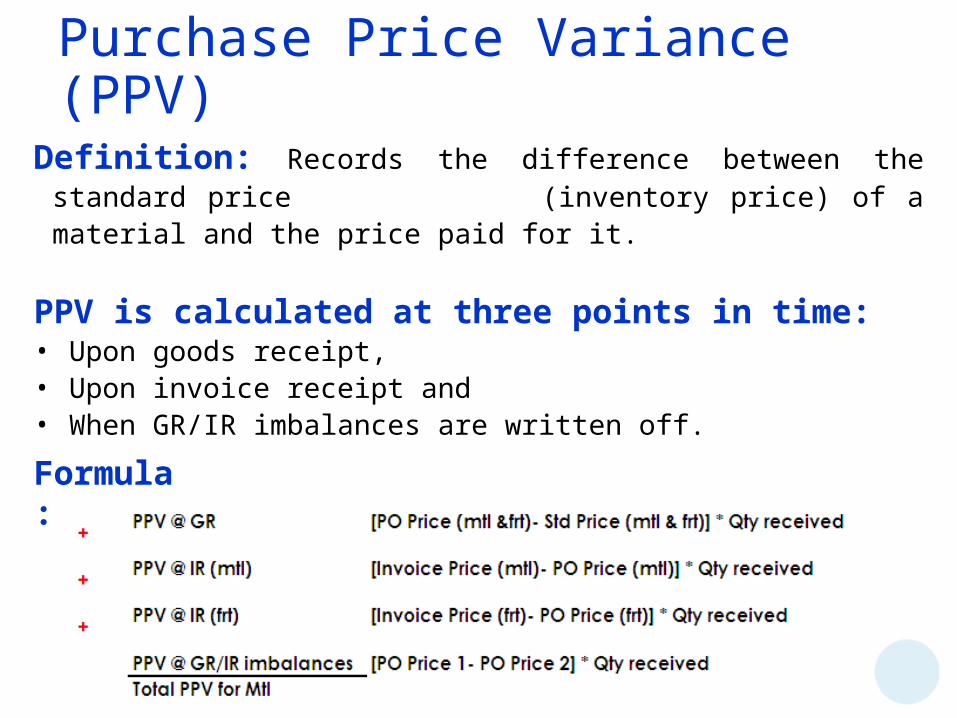

Definition: Records the difference between the standard price (inventory price) of a material and the price paid for it.

PPV is calculated at three points in time: • Upon goods receipt, • Upon invoice receipt and • When GR/IR imbalances are written off.

Formula:

Purchase Price Variance (PPV)

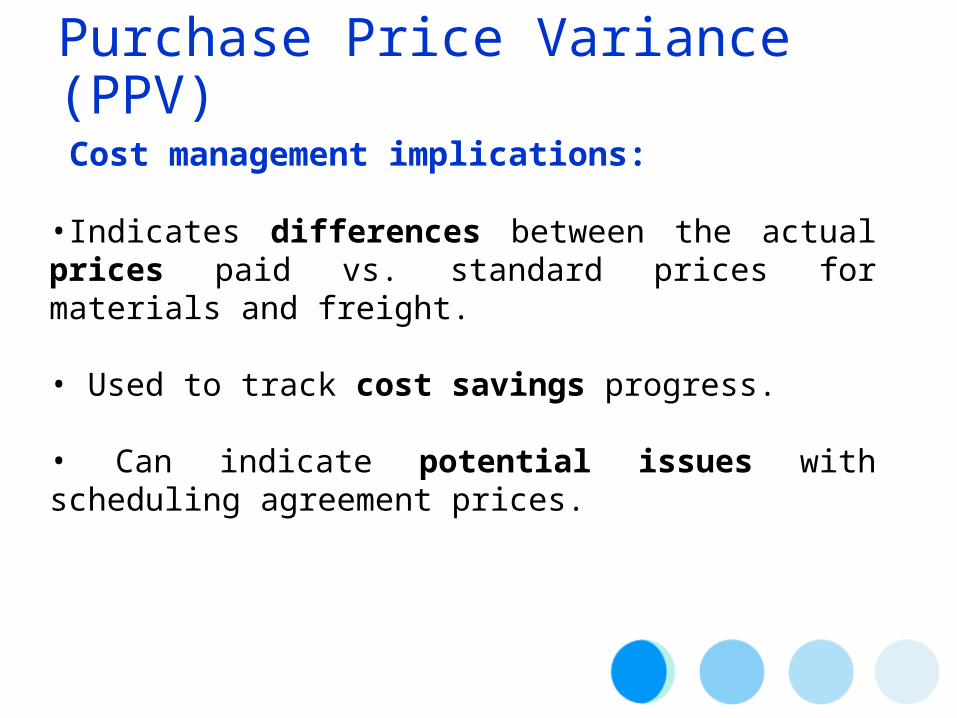

Cost management implications:

•Indicates differences between the actual prices paid vs. standard prices for materials and freight.

• Used to track cost savings progress.

• Can indicate potential issues with scheduling agreement prices.

Purchase Price Variance (PPV)

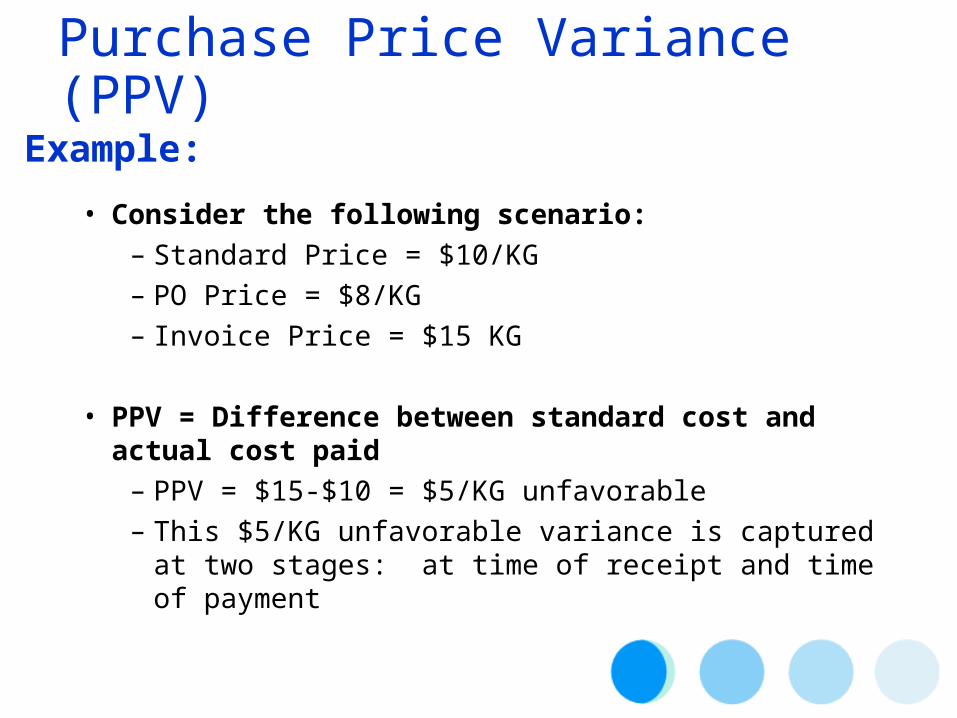

Example:

• Consider the following scenario:– Standard Price = $10/KG– PO Price = $8/KG– Invoice Price = $15 KG

• PPV = Difference between standard cost and actual cost paid

– PPV = $15-$10 = $5/KG unfavorable– This $5/KG unfavorable variance is captured at two

stages: at time of receipt and time of payment

Purchase Price Variance (PPV)

• Overall - (Invoice price for material - Standard price for material)

($15 - $10) = $5

• Calculated in two stages Upon Goods Receipt (Std Price - P.O. Price) ($10 - $ 8) = $2 Inventory GR/IR PPV

Std Price$10

P.O. Price

$8

PPV$2

Upon Invoice Receipt (P.O. Price - Invoice Price) ($8 - $15) = -$7

Vendor A/P GR/IR PPV

Invoice Price$15

P.O. Price

$8

PPV$7

Purchase Price Variance (PPV)

•Purchase Price Variance (PPV)

•Plant Sourcing Variance (PSV)

PRICE VARIANCES

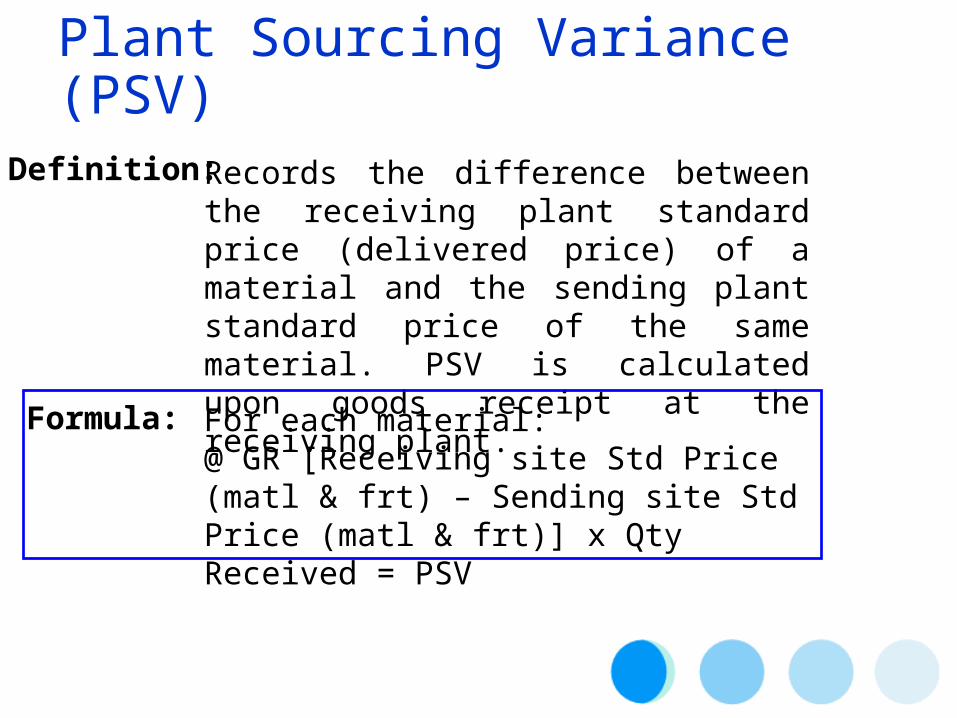

Definition:

Formula:

Records the difference between the receiving plant standard price (delivered price) of a material and the sending plant standard price of the same material. PSV is calculated upon goods receipt at the receiving plant.For each material:@ GR [Receiving site Std Price (matl & frt) – Sending site Std Price (matl & frt)] x Qty Received = PSV

Plant Sourcing Variance (PSV)

• Plant sourcing variance also occurs when a plant ships finished goods to the Distributing Company Control Plant and the sending plant standard price is different

• The receiving plant (DC Control plant) books the variance.

• Intersite freight for anything but FP is mapped to PSV.

Plant Sourcing Variance (PSV)

Cost management implications:

•Indicates a difference in price between one site and another.

•Can indicate costing issues.

Plant Sourcing Variance (PSV)

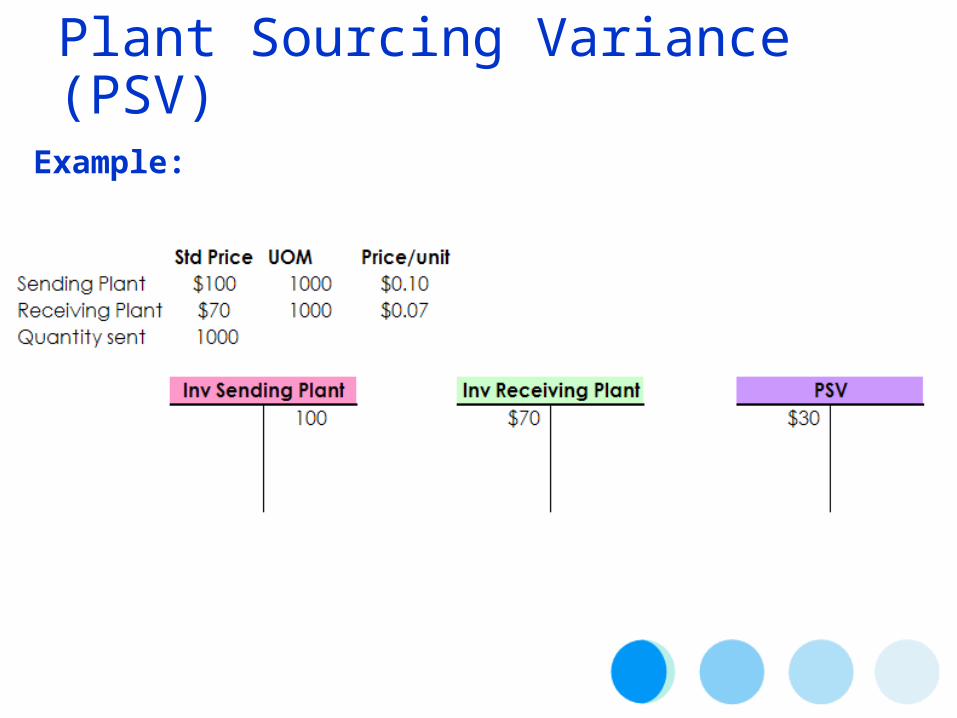

Example:

Plant Sourcing Variance (PSV)

•Purchase Price Variance (PPV)

•Plant Sourcing Variance (PSV)

•Revaluation

PRICE VARIANCES

Formula:

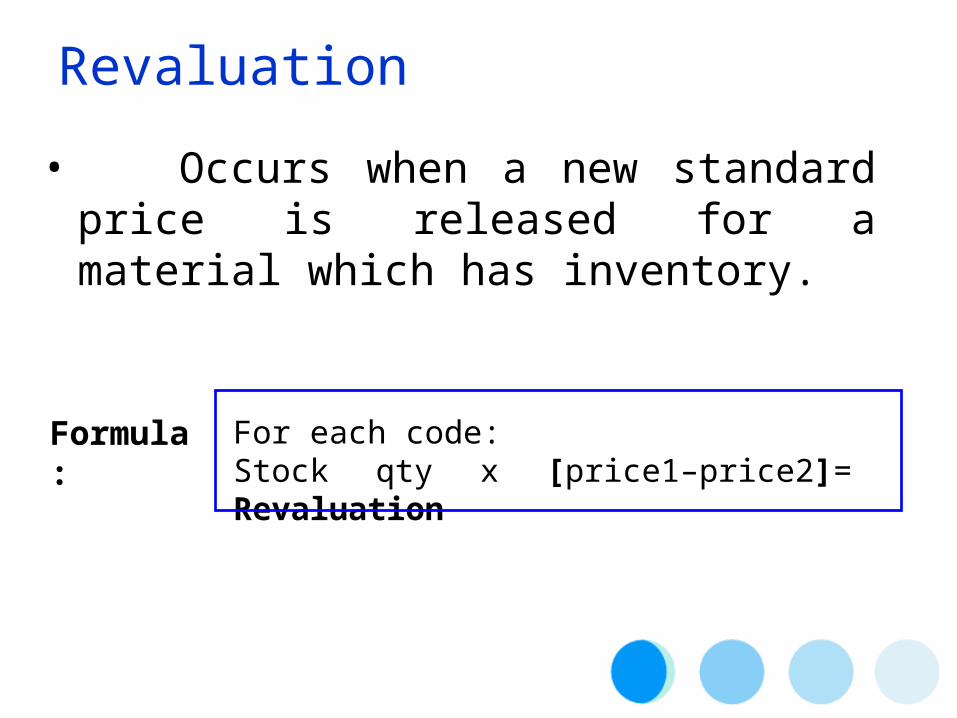

For each code:Stock qty x [price1–price2]= Revaluation

Revaluation

• Occurs when a new standard price is released for a material which has inventory.

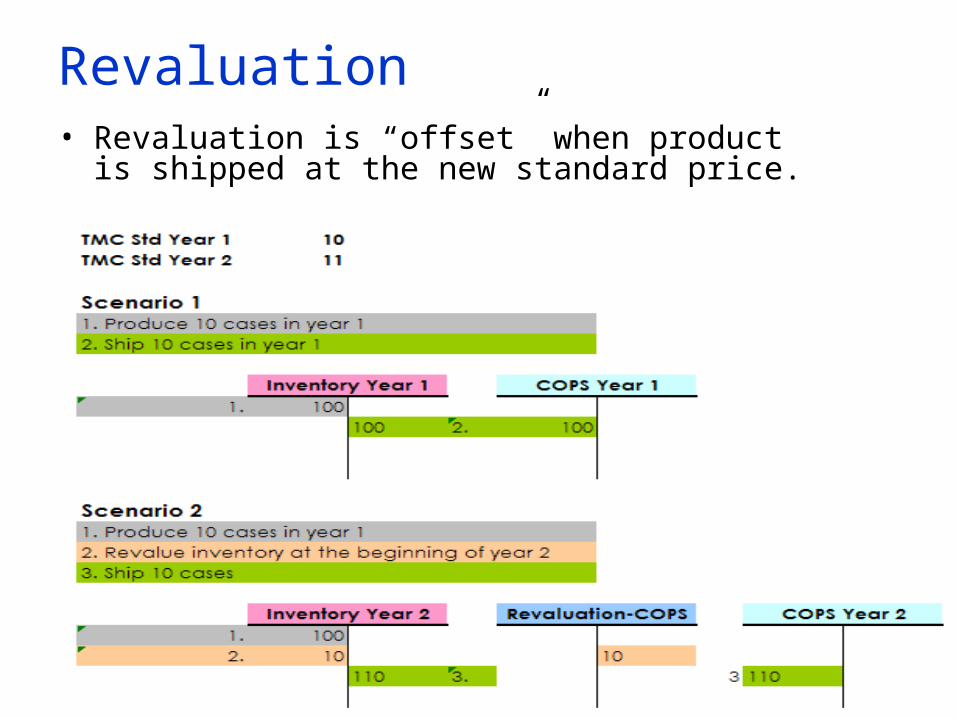

• Revaluation is “offset” when product is shipped at the new standard price.

Revaluation

•Purchase Price Variance (PPV)

•Plant Sourcing Variance (PSV)

•Revaluation

•Production Order Variance (POV)

PRICE VARIANCES

QUANTITY VARIANCES

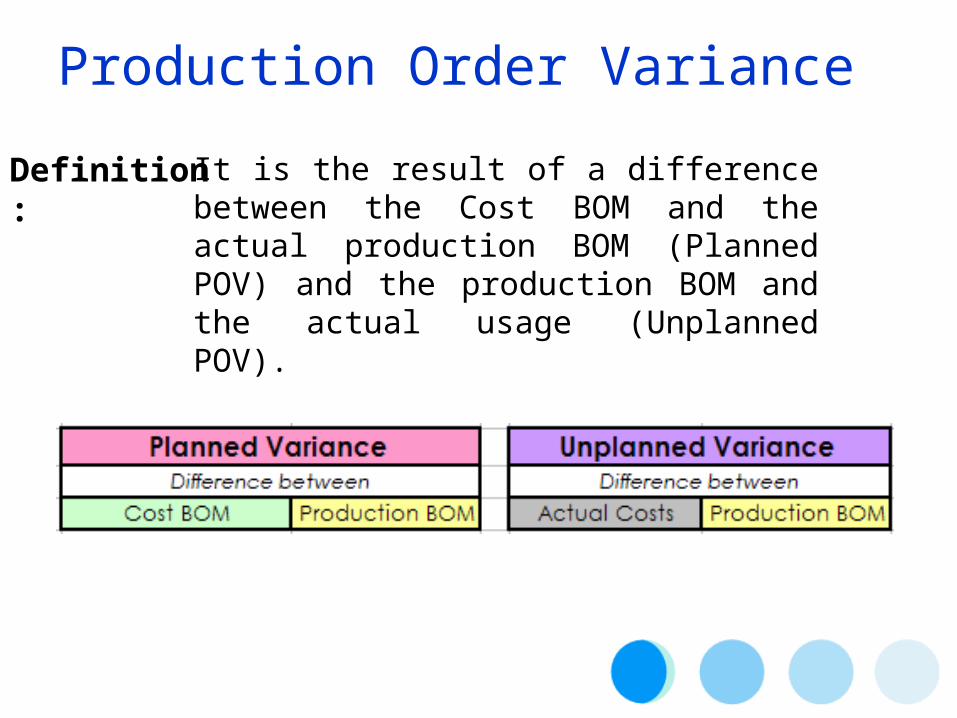

Definition:It is the result of a difference between the Cost BOM and the actual production BOM (Planned POV) and the production BOM and the actual usage (Unplanned POV).

Production Order Variance

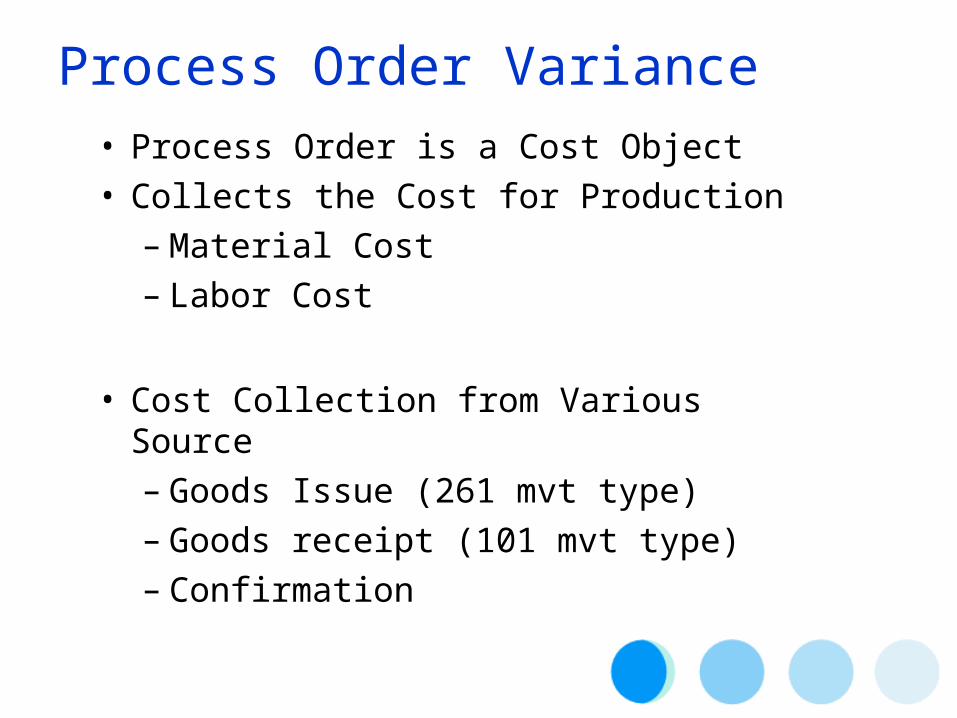

• Process Order is a Cost Object• Collects the Cost for Production

– Material Cost– Labor Cost

• Cost Collection from Various Source– Goods Issue (261 mvt type)– Goods receipt (101 mvt type)– Confirmation

Process Order Variance

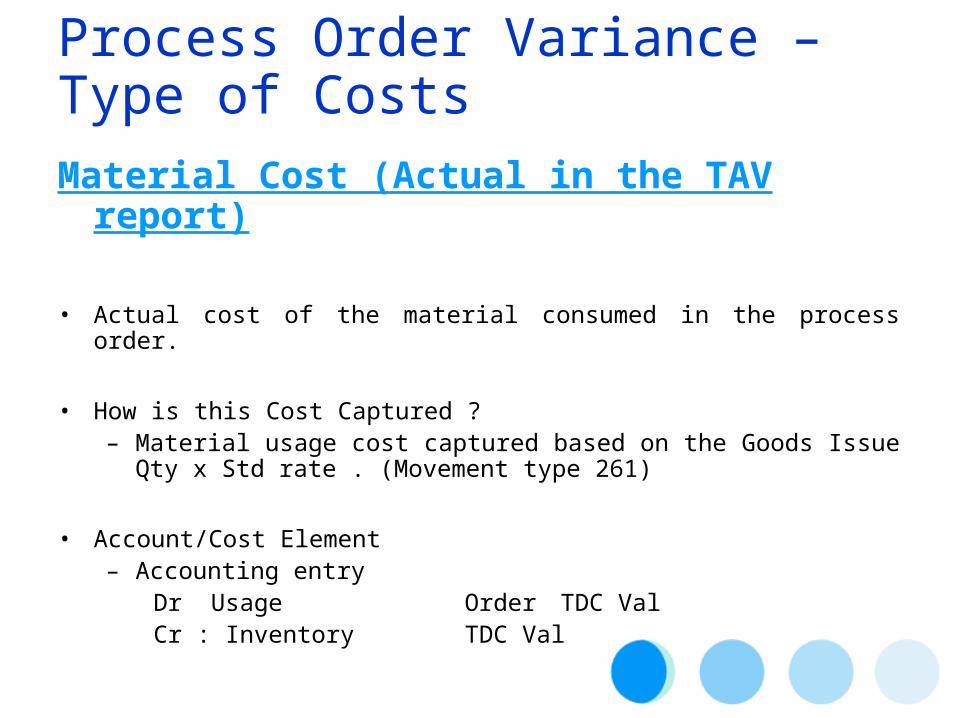

Material Cost (Actual in the TAV report)

• Actual cost of the material consumed in the process order.

• How is this Cost Captured ?– Material usage cost captured based on the Goods Issue Qty x

Std rate . (Movement type 261)

• Account/Cost Element – Accounting entry

Dr Usage Order TDC ValCr : Inventory TDC Val

Process Order Variance – Type of Costs

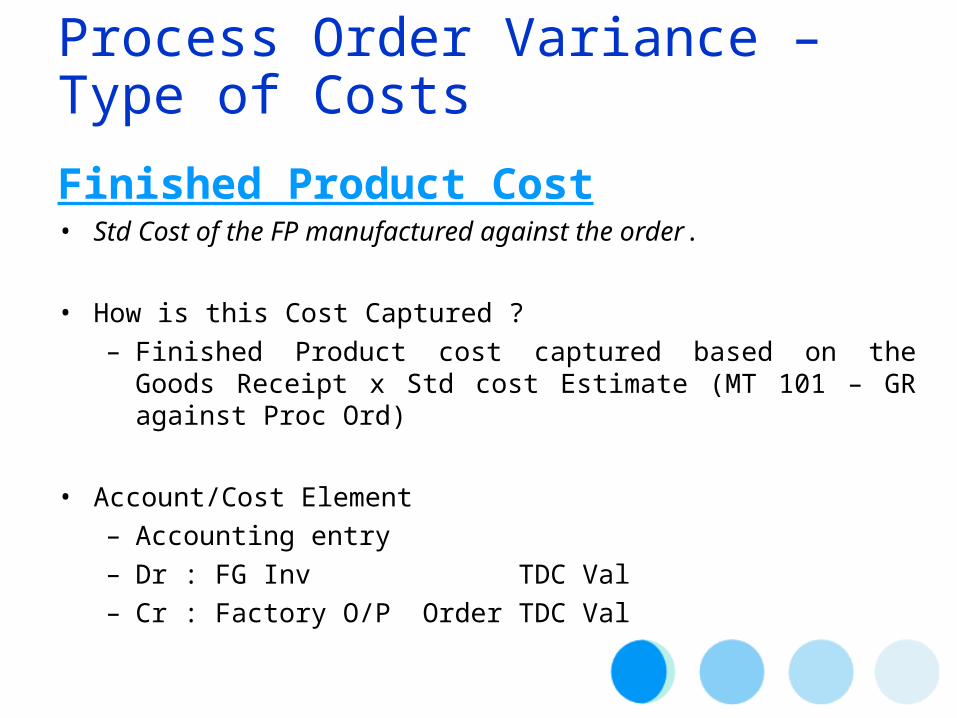

Finished Product Cost• Std Cost of the FP manufactured against the order.

• How is this Cost Captured ?– Finished Product cost captured based on the Goods

Receipt x Std cost Estimate (MT 101 – GR against Proc Ord)

• Account/Cost Element – Accounting entry– Dr : FG Inv TDC Val– Cr : Factory O/P Order TDC Val

Process Order Variance – Type of Costs

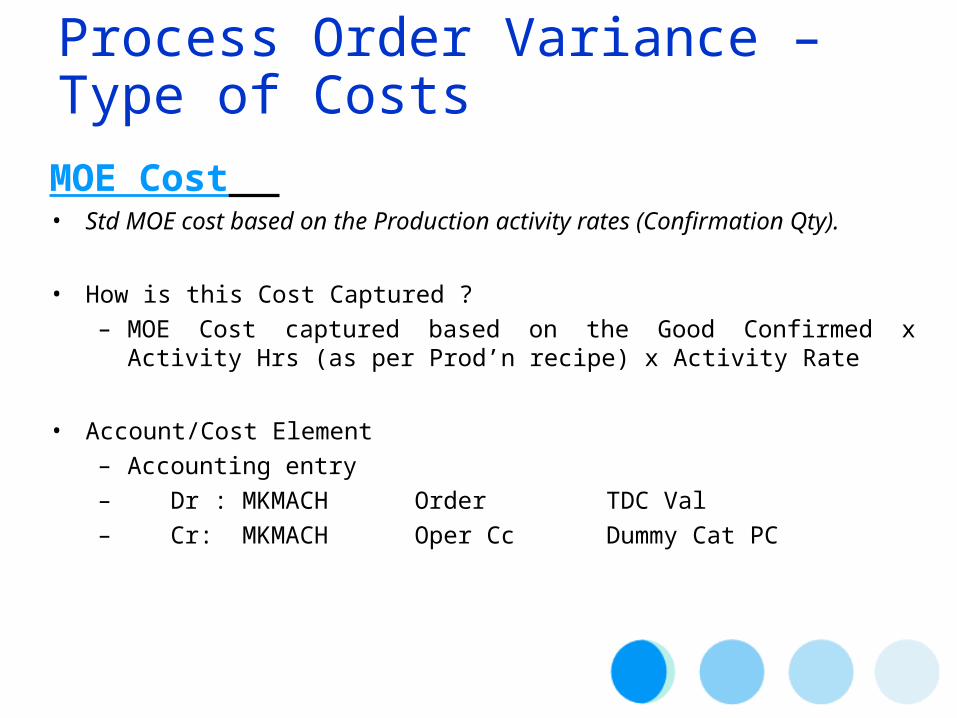

MOE Cost • Std MOE cost based on the Production activity rates (Confirmation

Qty).

• How is this Cost Captured ?– MOE Cost captured based on the Good Confirmed x Activity Hrs

(as per Prod’n recipe) x Activity Rate

• Account/Cost Element – Accounting entry– Dr : MKMACH Order TDC Val– Cr: MKMACH Oper Cc Dummy Cat PC

Process Order Variance – Type of Costs

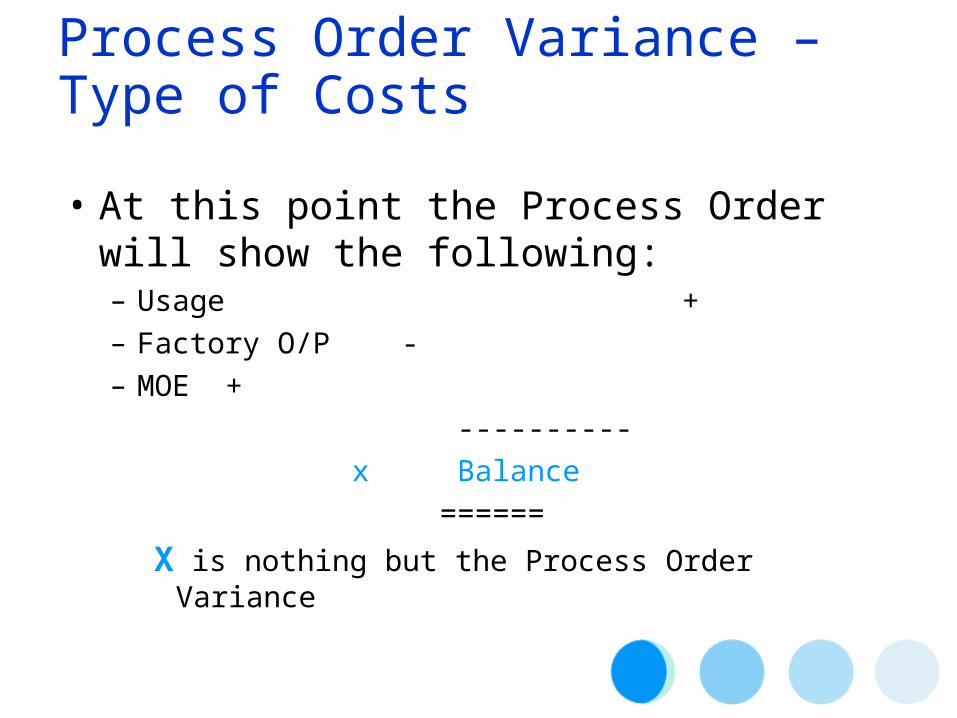

• At this point the Process Order will show the following:– Usage +– Factory O/P -– MOE +

----------x Balance

======

X is nothing but the Process Order Variance

Process Order Variance – Type of Costs

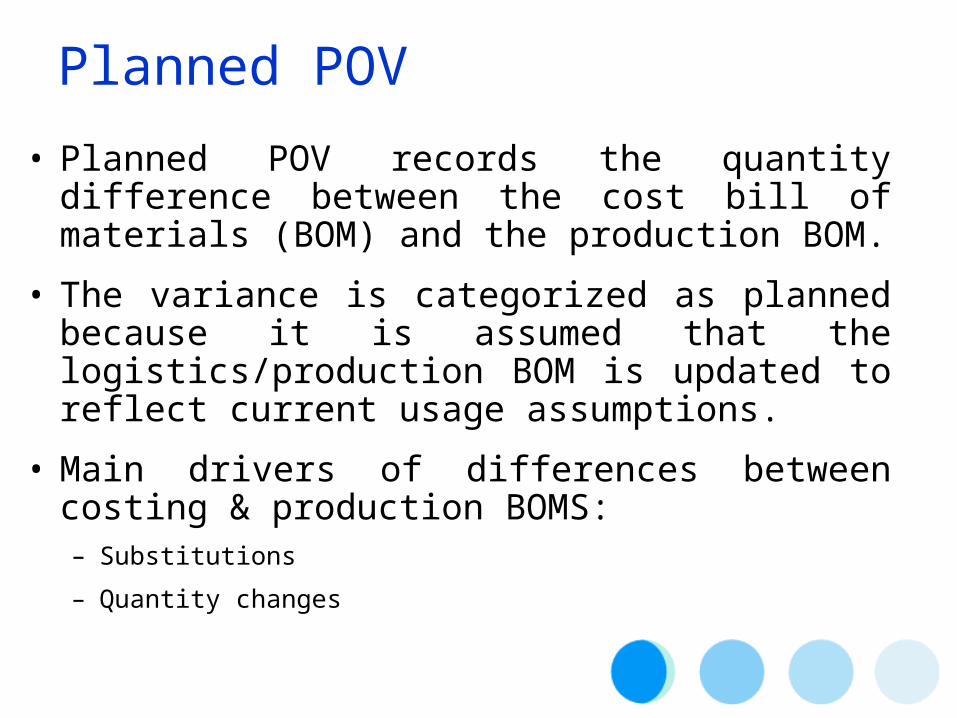

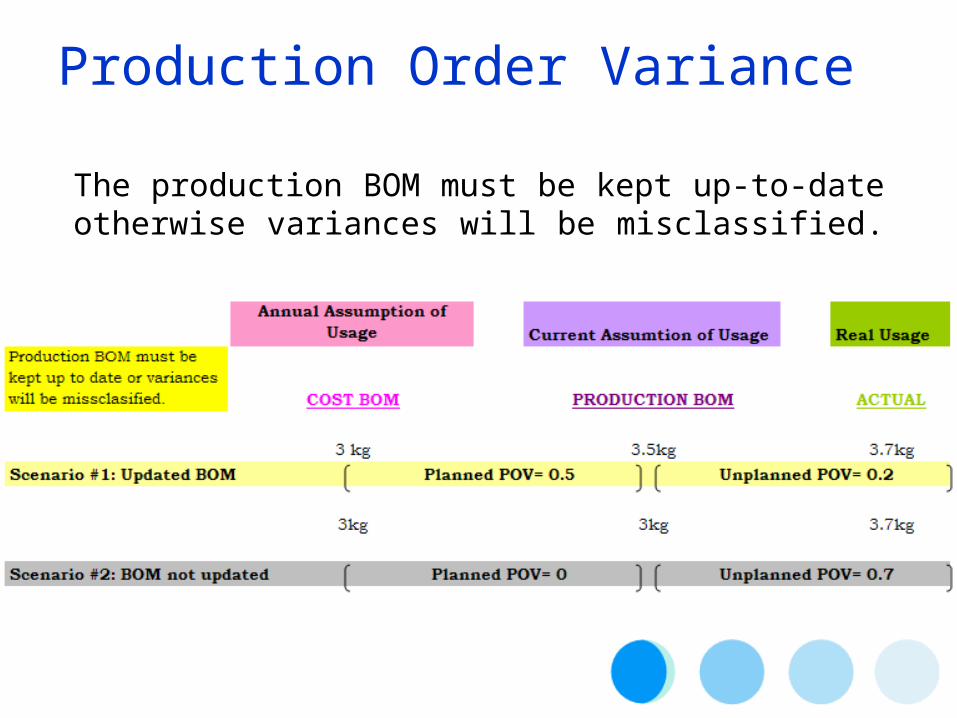

• Planned POV records the quantity difference between the cost bill of materials (BOM) and the production BOM.

• The variance is categorized as planned because it is assumed that the logistics/production BOM is updated to reflect current usage assumptions.

• Main drivers of differences between costing & production BOMS:– Substitutions

– Quantity changes

Planned POV

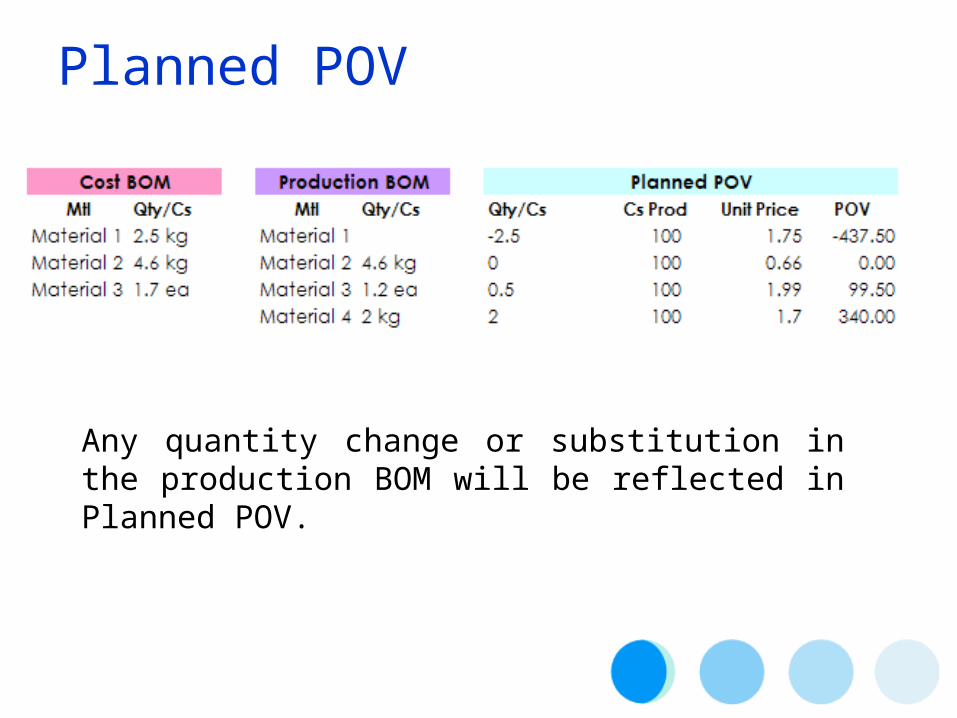

• Example: •

Any quantity change or substitution in the production BOM will be reflected in Planned POV.

Planned POV

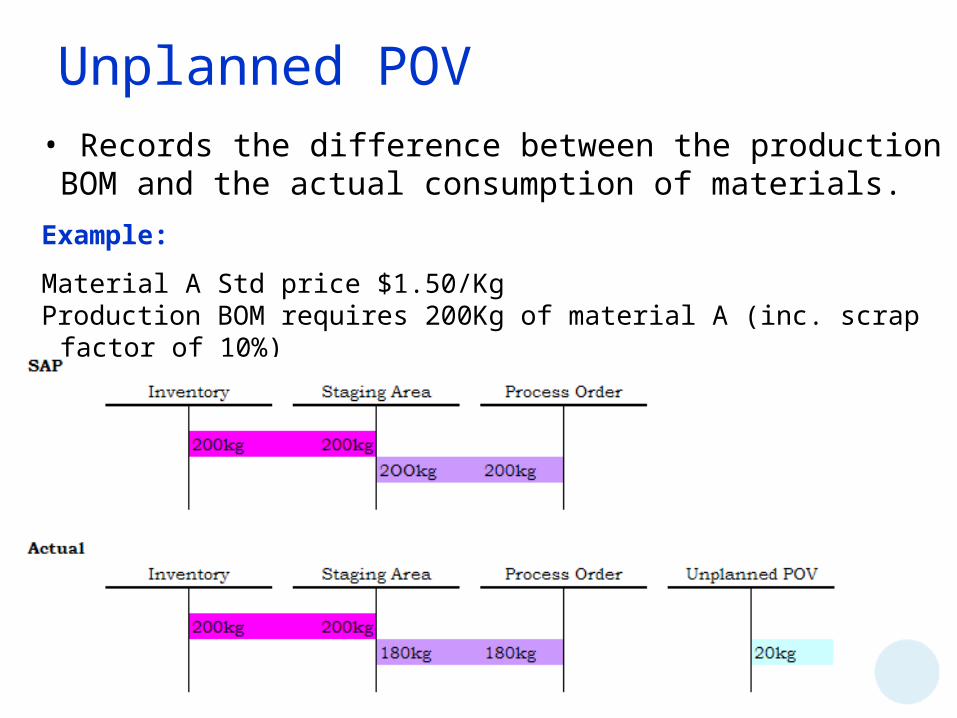

Unplanned POV• Records the difference between the production BOM and the actual consumption of materials.

Example:

Material A Std price $1.50/KgProduction BOM requires 200Kg of material A (inc. scrap factor of

10%)Actual usage on order 180Kg

The production BOM must be kept up-to-date otherwise variances will be misclassified.

Production Order Variance

Cost management implications:

•Indicates change in usage quantity of a material.

• Indicates changes in scrap rate assumptions.

• Can highlight impact of producing on efficient lines vs. less efficient ones (I.e. lines with different scrap rates)

• Indicates substitutions of materials which may be part of cost savings work.

Production Order Variance

•Purchase Price Variance (PPV)

•Plant Sourcing Variance (PSV)

•Revaluation

•Production Order Variance (POV)

•Staging Area Variance

PRICE VARIANCES

QUANTITY VARIANCES

Definition:

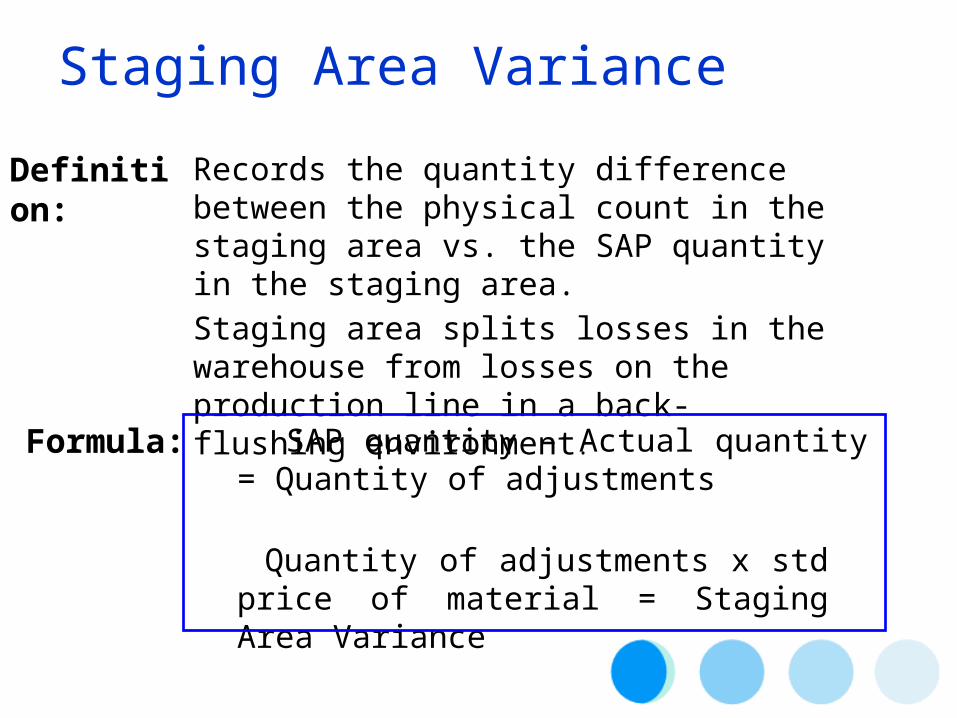

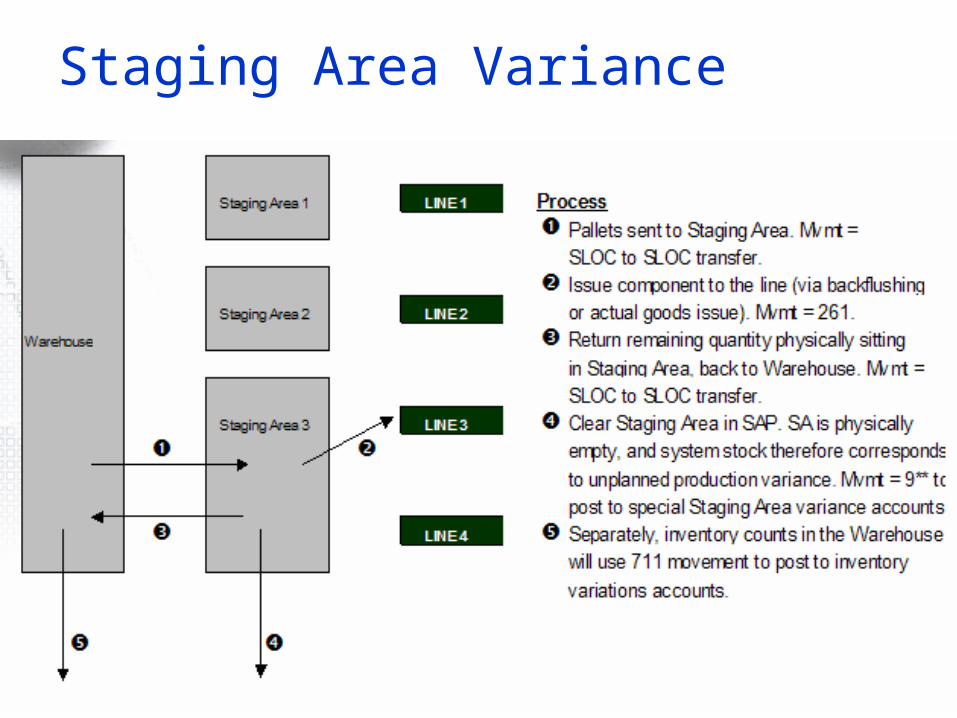

Records the quantity difference between the physical count in the staging area vs. the SAP quantity in the staging area.Staging area splits losses in the warehouse from losses on the production line in a back-flushing environment.Formula: SAP quantity – Actual quantity =

Quantity of adjustments

Quantity of adjustments x std price of material = Staging Area Variance

Staging Area Variance

Staging Area Variance

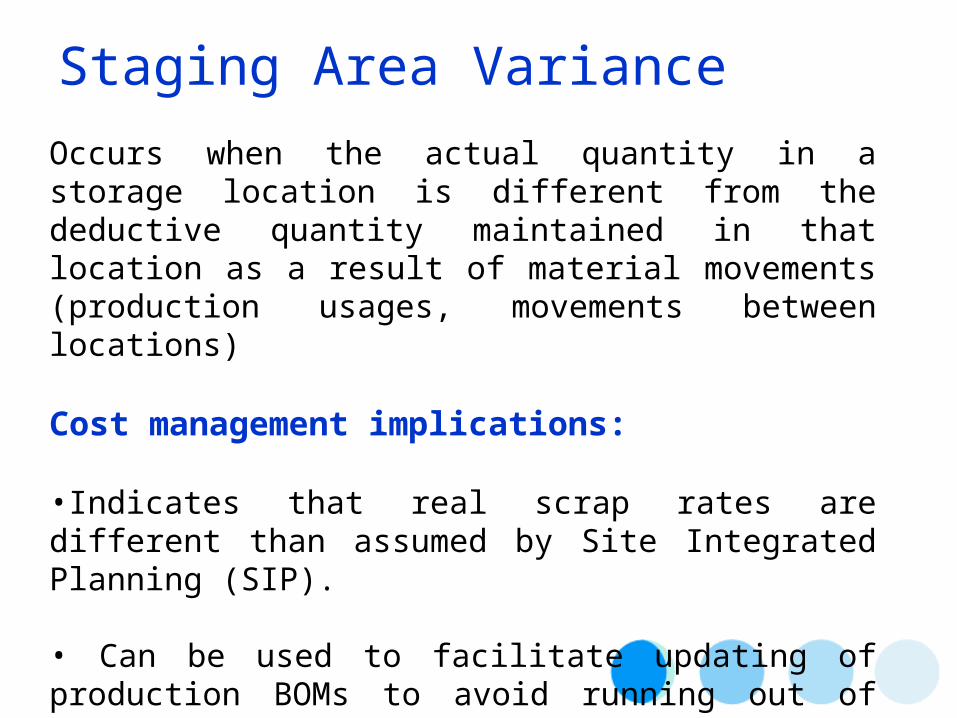

Occurs when the actual quantity in a storage location is different from the deductive quantity maintained in that location as a result of material movements (production usages, movements between locations)

Cost management implications:

•Indicates that real scrap rates are different than assumed by Site Integrated Planning (SIP).

• Can be used to facilitate updating of production BOMs to avoid running out of materials

Staging Area Variance

•Purchase Price Variance (PPV)

•Plant Sourcing Variance (PSV)

•Revaluation

•Production Order Variance (POV)

•Staging Area Variance

•Production Activity Variance

PRICE VARIANCES

EXPENSE VARIANCES

QUANTITY VARIANCES

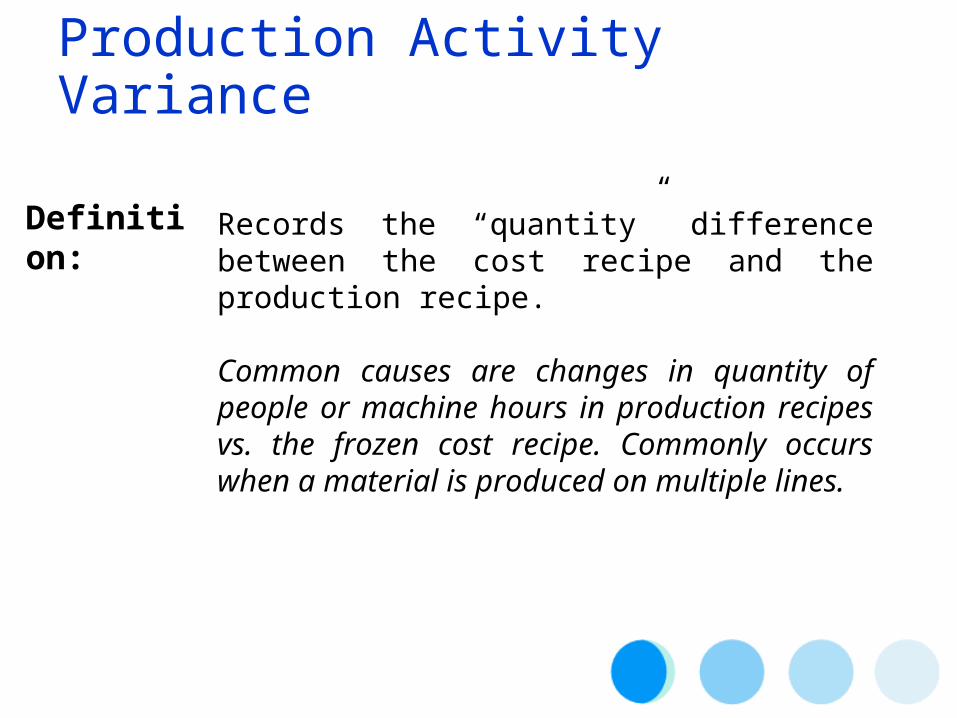

Definition:

Records the “quantity” difference between the cost recipe and the production recipe.

Common causes are changes in quantity of people or machine hours in production recipes vs. the frozen cost recipe. Commonly occurs when a material is produced on multiple lines.

Production Activity Variance

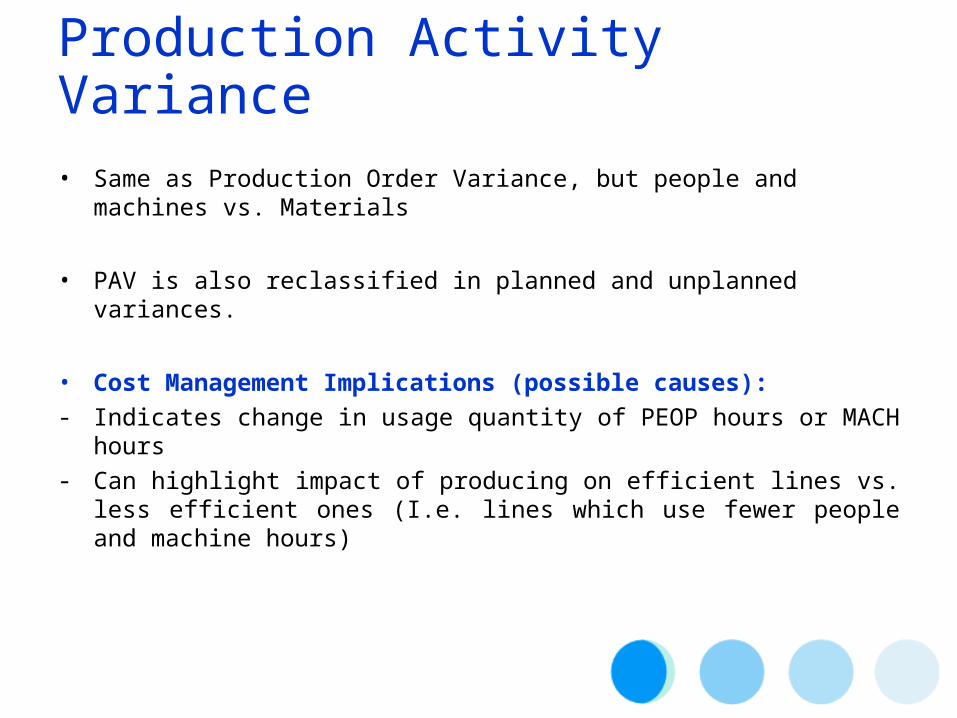

• Same as Production Order Variance, but people and machines vs. Materials

• PAV is also reclassified in planned and unplanned variances.

• Cost Management Implications (possible causes):- Indicates change in usage quantity of PEOP hours or MACH hours- Can highlight impact of producing on efficient lines vs. less

efficient ones (I.e. lines which use fewer people and machine hours)

Production Activity Variance

•Purchase Price Variance (PPV)

•Plant Sourcing Variance (PSV)

•Revaluation

•Production Order Variance (POV)

•Staging Area Variance

•Production Activity Variance

•MOE variance

PRICE VARIANCES

EXPENSE VARIANCES

QUANTITY VARIANCES

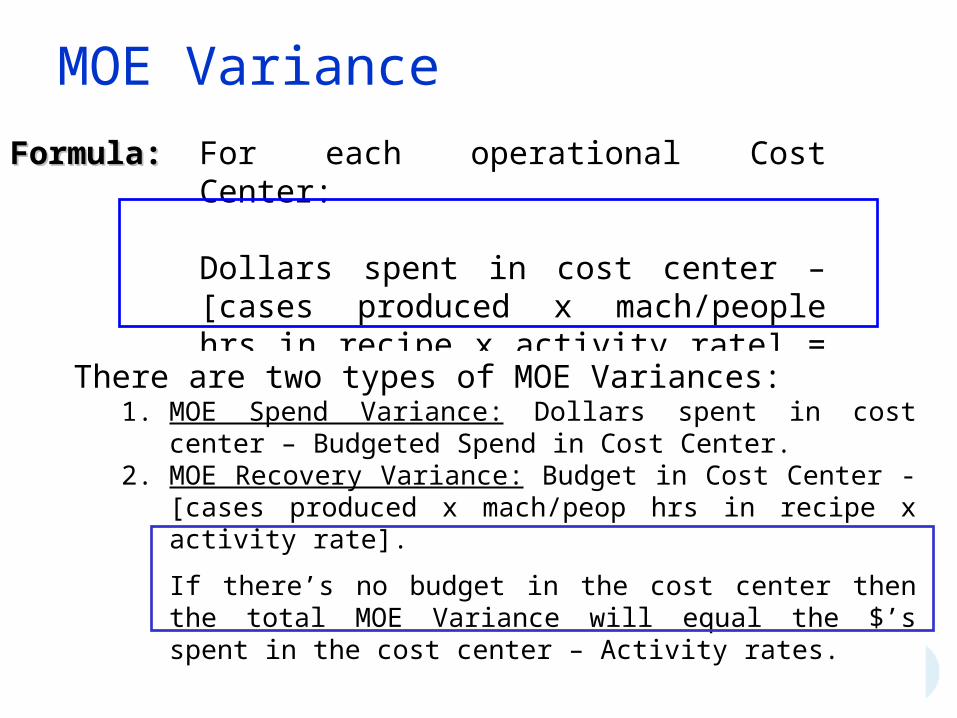

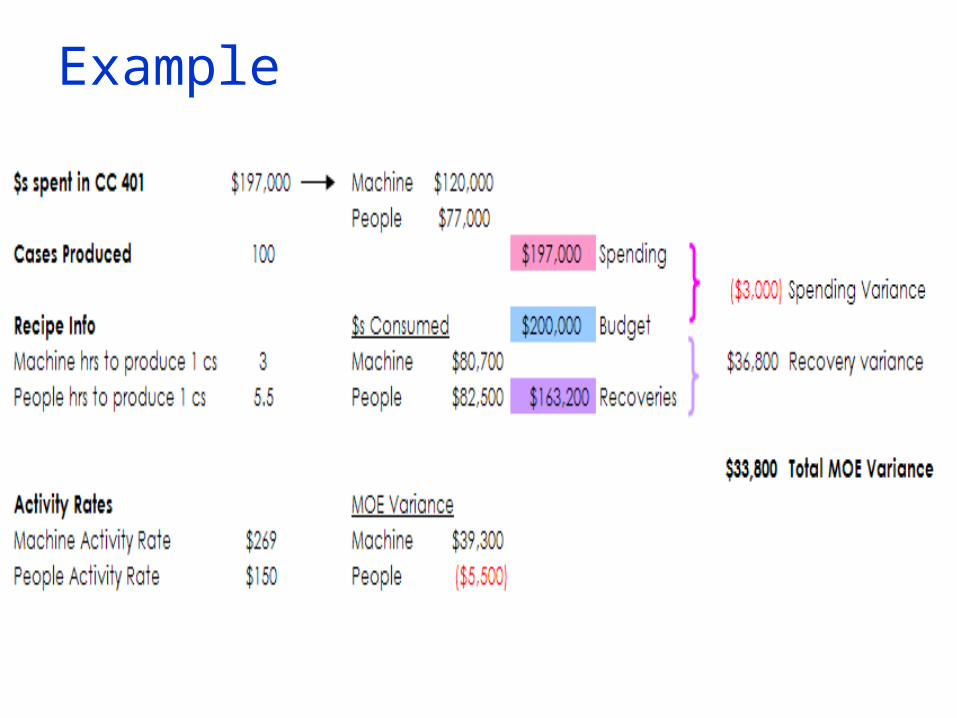

There are two main factors that influence MOE variance:

Spending: captures differences between planned and actual spending against a cost center. The level of spending for the month will determine the MOE variance.

Production volume: MOE variance also captures over or under consumption of costs out of the cost center (based on the volume more or less dollars will be consumed out the cost center).

MOE Variance

FormulaFormula::

For each operational Cost Center:

Dollars spent in cost center – [cases produced x mach/people hrs in recipe x activity rate] = MOEV

There are two types of MOE Variances:1. MOE Spend Variance: Dollars spent in cost center –

Budgeted Spend in Cost Center. 2. MOE Recovery Variance: Budget in Cost Center - [cases

produced x mach/peop hrs in recipe x activity rate].

If there’s no budget in the cost center then the total MOE Variance will equal the $’s spent in the cost center – Activity rates.

MOE Variance

MOE VarianceExample

MOE variance can indicate:

• Overspending i.e. there was the need to hire 3 more technicians and it was not considered at the time of the firm.

• Under spending i.e. invoices not received on time.

• Over/Under production (you spent the budgeted $, but produced more or less than planned)

• Wrong activity rates.

MOE Variance

•Purchase Price Variance (PPV)

•Plant Sourcing Variance (PSV)

•Revaluation

•Production Order Variance (POV)

•Staging Area Variance

•Production Activity Variance

•MOE Variance

PRICE VARIANCES

QUANTITY VARIANCES

EXPENSE VARIANCES

Questions?Questions?