1 Why India is Important for the European Fine Chemicals Industry Gautam Mahajan Inter-Link Services...

67

1 Why India is Important for the European Fine Chemicals Industry Gautam Mahajan Inter-Link Services Private Limited [email protected] +91 9810060368

-

Upload

polly-lawrence -

Category

Documents

-

view

214 -

download

0

Transcript of 1 Why India is Important for the European Fine Chemicals Industry Gautam Mahajan Inter-Link Services...

1

Why India is Important for the European Fine Chemicals Industry

Gautam MahajanInter-Link Services Private Limited

[email protected]+91 9810060368

2

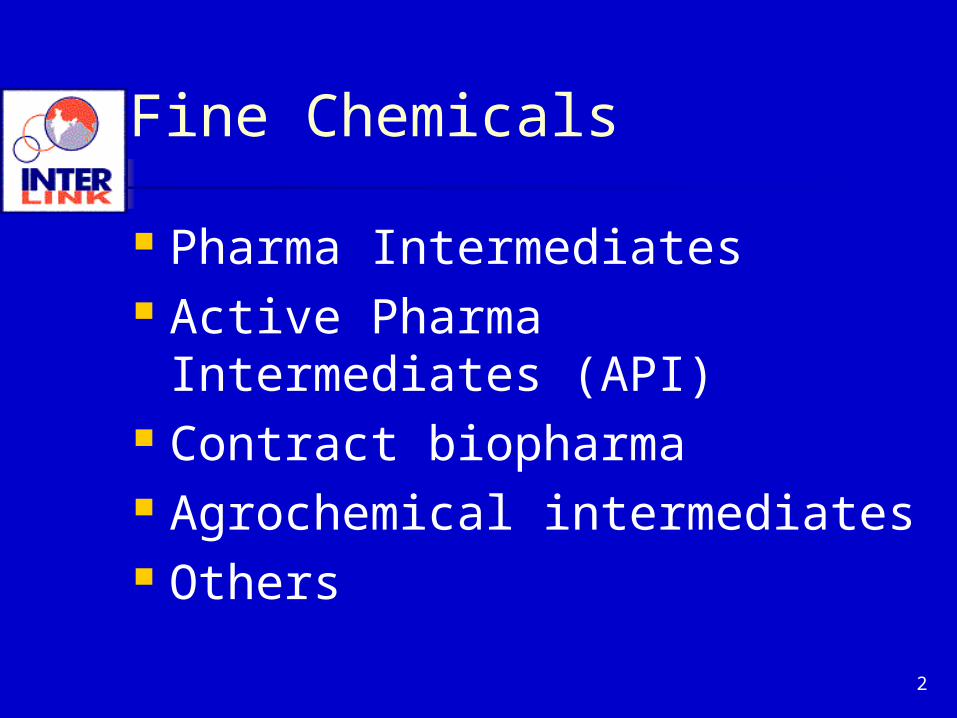

Fine Chemicals

Pharma Intermediates Active Pharma Intermediates

(API) Contract biopharma Agrochemical intermediates Others

3

The changing business dynamics in India• Europe and India: dynamics

• Opportunities to invest in, sell to and buy from in India

• India and China competition• Using India to balance supply constraints

• The changing business dynamics in India

• India Trade• The growth of the chemicals business

and trends in India• Using India as a supply base for other

countries

4

First, we’ll discuss:

• Europe and India: Dynamics

• Opportunities to invest in, sell to and buy from in India

• India and China competition

• Using India to balance supply constraints

5

Fine Chemicals: Market Size

US: €17.18 billion in 2005 €23.10 billion in 2011 est.

Europe: € 8.43 billion in 2005 €10.46 billion in 2009 est.

India: >€ 1 billion

6

EU Chemicals

In 2004, 29% of EU chemicals exported compared to: 19% for the USA and

19% for Japan Only 18% of the EU chemicals demand

was imported from the non-EU regions*

*In 2003, India-China imports were 8%, estimated to increase to 30% in 2008-09

7

European Fine Chemicals profitability under pressure

Profitability eroding: Intense Asian competition New chemical entity (NCE)

approvals rate reduced

8

Threats and Opportunities

Globalisation Higher Exports from Asia India China Symbiosis Asia driven acquisitions could

be exit option offer services across the value

chain

9

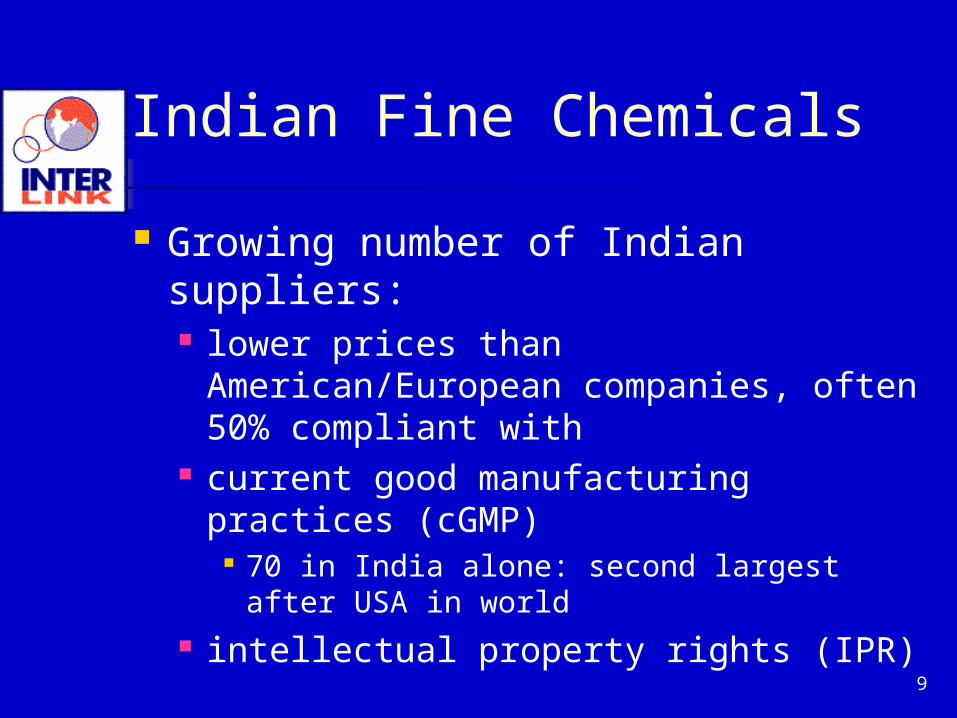

Indian Fine Chemicals

Growing number of Indian suppliers: lower prices than American/European

companies, often 50% compliant with current good manufacturing practices

(cGMP) 70 in India alone: second largest after

USA in world intellectual property rights (IPR)

10

Active Pharma Intermediates

Indian API 3rd largest in world (€1.6 bn in 2005) and will

grow to €3.63 bn by 2010, CAGR 19.3 %

India will become second largest API manufacturer (overtake Italy) by 2010*

* Italy's Chemical Pharmaceutical Generic Association (CPA)

report

11

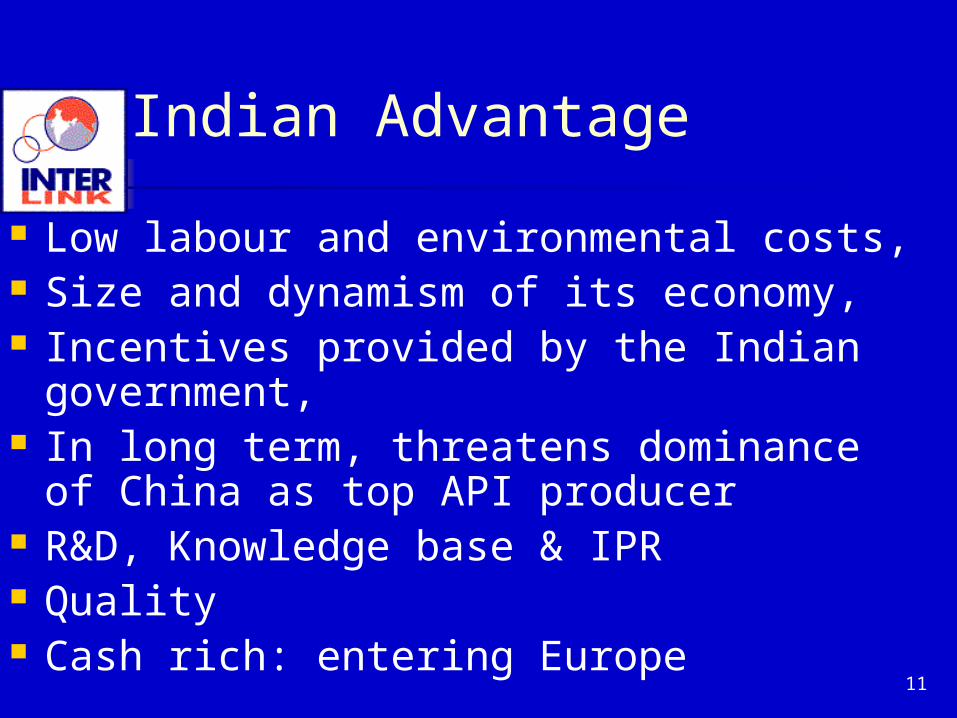

Indian Advantage

Low labour and environmental costs, Size and dynamism of its economy, Incentives provided by the Indian

government, In long term, threatens dominance of

China as top API producer R&D, Knowledge base & IPR Quality Cash rich: entering Europe

12

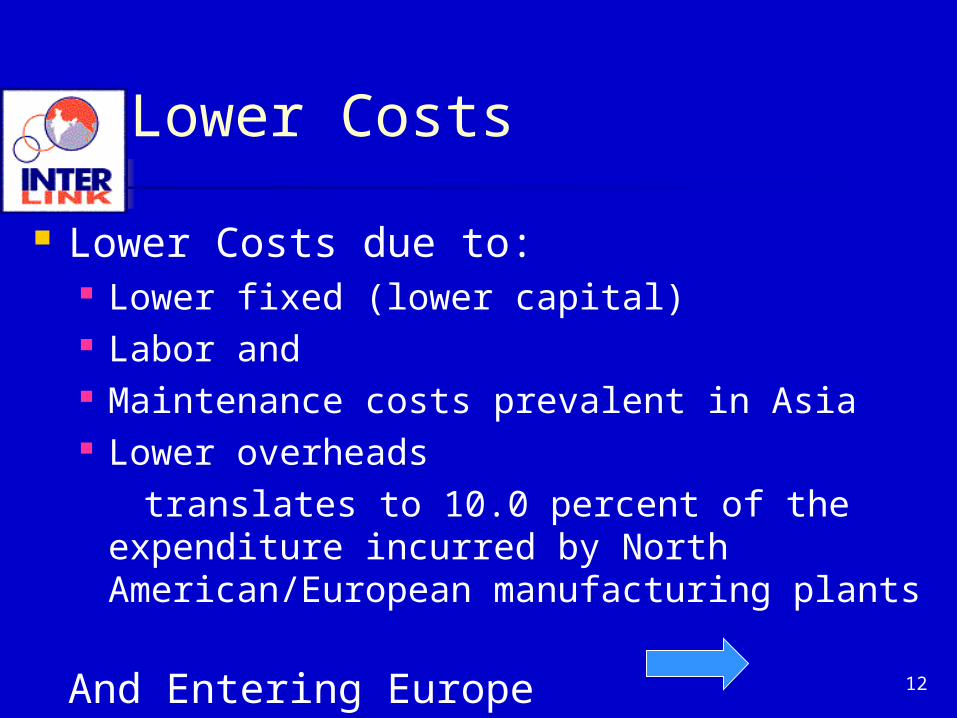

Lower Costs

Lower Costs due to: Lower fixed (lower capital) Labor and Maintenance costs prevalent in Asia Lower overheads translates to 10.0 percent of the

expenditure incurred by North American/European manufacturing plants

And Entering Europe

13

Examples of Indian Acquisitions

Nicholas Piramal Avecia Pharmaceutical Pfizer, Inc. (Morpeth, UK)

$350 mn supply agreement with Pfizer 7 year agreement for process development

and scale-up services to Pfizer Rhodia's (Paris) inhalation anesthetics

business

14

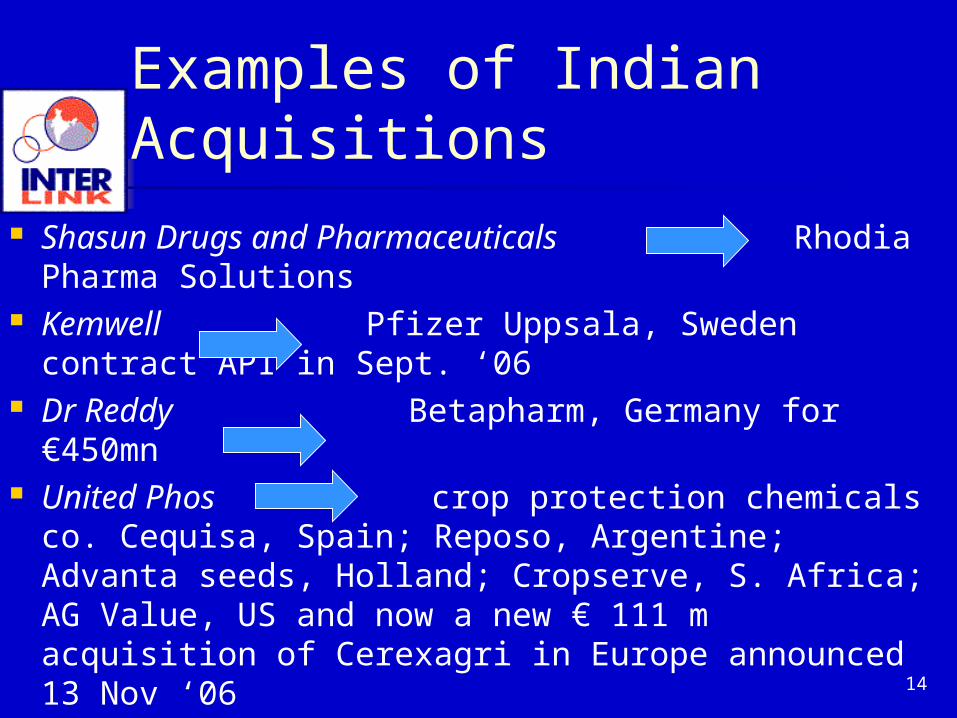

Examples of Indian Acquisitions

Shasun Drugs and Pharmaceuticals Rhodia Pharma Solutions

Kemwell Pfizer Uppsala, Sweden contract API in Sept. ‘06

Dr Reddy Betapharm, Germany for €450mn

United Phos crop protection chemicals co. Cequisa, Spain; Reposo, Argentine; Advanta seeds, Holland; Cropserve, S. Africa; AG Value, US and now a new € 111 m acquisition of Cerexagri in Europe announced 13 Nov ‘06

15

Examples of Indian Acquisitions

Dishman Pharmaceuticals and Chemicals

CarbonGen and AMCIS, Switzerland for high-potency actives

I03S, Ltd. ( ozone chemistry), Synprotec, a contract research company

16

Backward Integration in China

Indian producers backward–integrating in China Example: Dishman has two projects:

a $10-million investment for producing quaternary compounds and intermediates and

an API plant

17

Example: Matrix Labs

Matrix Laboratories Concord Biotech specializing in fermentation and biocatalytic

backward-integrate into China, acquired a 58% stake in Mchem Group

43% stake in Swiss API technology firm Explora Laboratories

Ventures with South Africa's Aspen Pharmacare Belgium generics company Docpharma NVBUT US generic drugmaker Mylan: €573.4mn to

acquire a controlling stake in Matrix

18

Indian Companies setting up in Europe/America

Denisco Nancy, France, API Dallas, Texas customer support office

“Customers in North America face tight margins and fierce competitive pressure for time-to-market. Our ability to quickly, safely and efficiently produce pharmaceutical lab samples, and then rapidly ramp up for commercial-level volumes, will help lighten these pressures,” said Venkat Ram, president of Denisco Chemicals.

19

Indian Companies setting up in Europe/America

G Amphray in Holland and now in Mexico

Bilcare, India's largest research-based pharmaceuticals packaging company, has bought UK-based clinical trials services provider DHP in Sept. 2006

20

Other Indian Companies

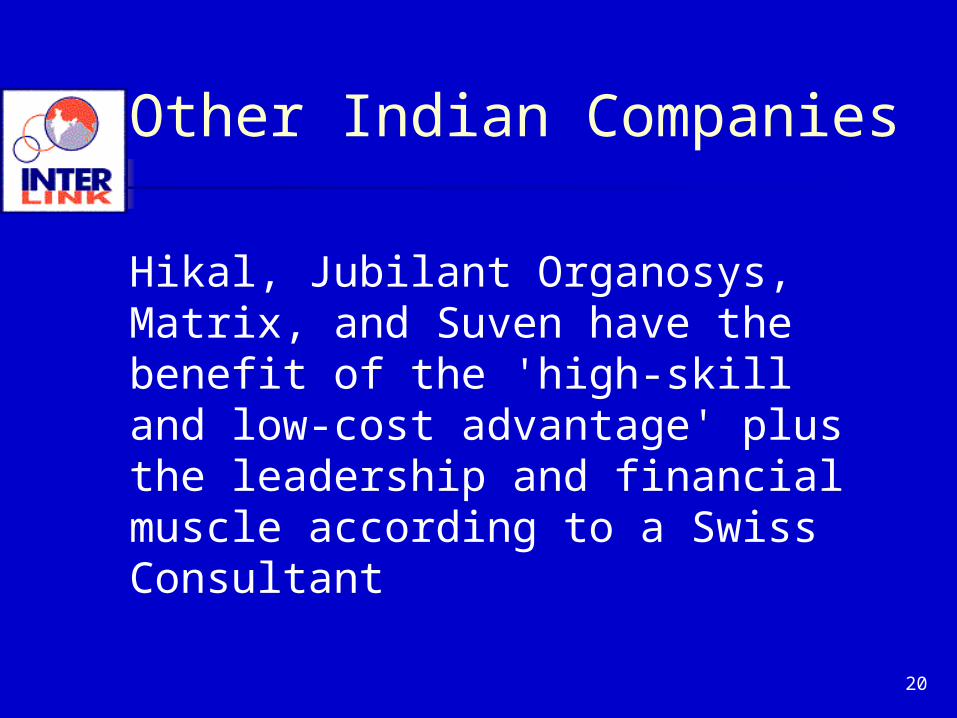

Hikal, Jubilant Organosys, Matrix, and Suven have the benefit of the 'high-skill and low-cost advantage' plus the leadership and financial muscle according to a Swiss Consultant

21

Example: SST USA

SST USA: “..European-based producers still account for the majority of supplier base, producers from India and Japan now represent an important minority of the company's suppliers," says Gary Vassallo, president of SST, who took over in March

India makes up one-quarter of the 23 manufacturers represented by SST.

22

Therefore,

Supplies from India and China forcing US and European companies to redefine their business models:"Apart from the issues of quality, speed, and value, the two key requisites for success are a position in India or China (a manufacturing subcontracting arrangement is good and an affiliate company is better) and an attractive toolbox of technologies,"

Degussa custom manufacturing j. v. with Lynchem in China

*says Pollak.

23

Fine Chemicals Economics

Fine chemicals production economics favor China and India based operations. Annual unit labor costs are a fraction of the

West’s: €3,000 in India €4,000-€6,100 China versus €40,400 in West Europe or €15,300 in Poland, a good proxy for the

Central and Eastern European region

24

Unit Labor Costs¹*

0

10

20

30

40

50

60

70

Swiss. Italy Poland India ChinaCoastal

ChinaInner

K Euro/ p/y

65

42

15

2.5 4.5 3

¹Includes fringe/other benefits

*Source: Arthur D. Little

25

Productivity Ratio*

0

1

2

3

4

5

6

7

8

West India China

This ratio is calculated dividing value added – (net sales less raw material costs )-- by total direct labor wage costs. Note that even with lower labor costs, productivity is higher in Asia *Source: Arthur D. Little

2.5 - 4

7-9

6-8

26

Transformation Costs*

02468

101214161820

Swiss Italy Poland India ChinaCoastal

ChinaInner

~20 ~1

8 ~15

~7 ~8 ~6.5

Euro/Kg

*Source: Arthur D. Little

27

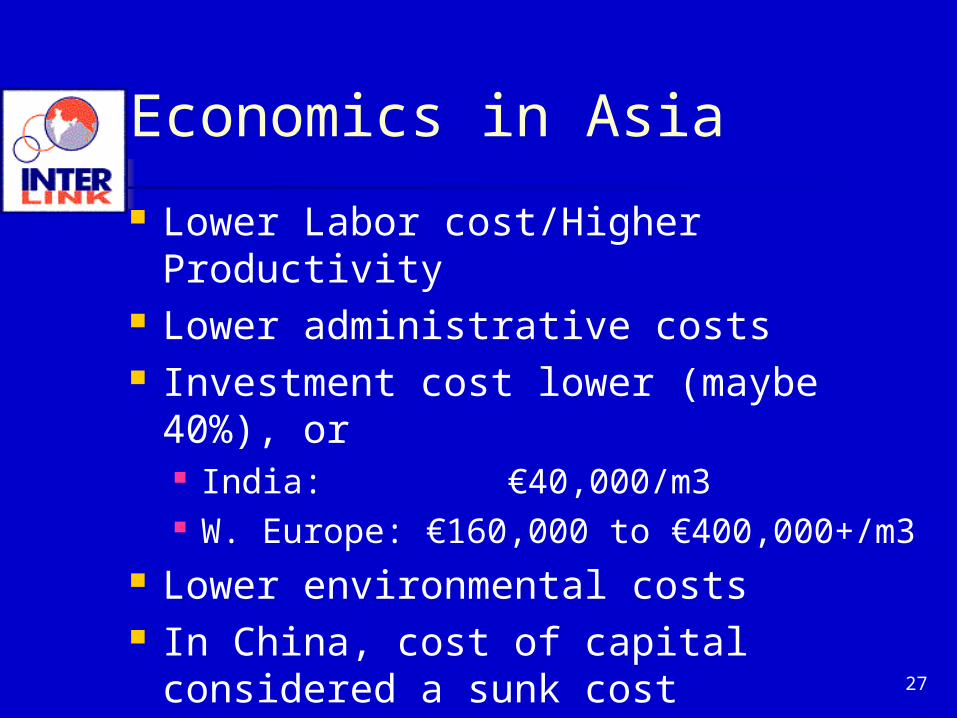

Economics in Asia

Lower Labor cost/Higher Productivity Lower administrative costs Investment cost lower (maybe 40%),

or India: €40,000/m3 W. Europe: €160,000 to €400,000+/m3

Lower environmental costs In China, cost of capital considered a

sunk cost

28

Economics in Asia

Raw materials maybe higher in India and China Higher solvent loss due to climate Higher energy costs Higher costs due to logistics, infrastructure and

other inefficiencies

Overall: Cost advantage of Asian suppliers increases with the complexity of the molecule, the longer and more complex the synthesis, and the higher the manpower and reactor volume

requirements.

29

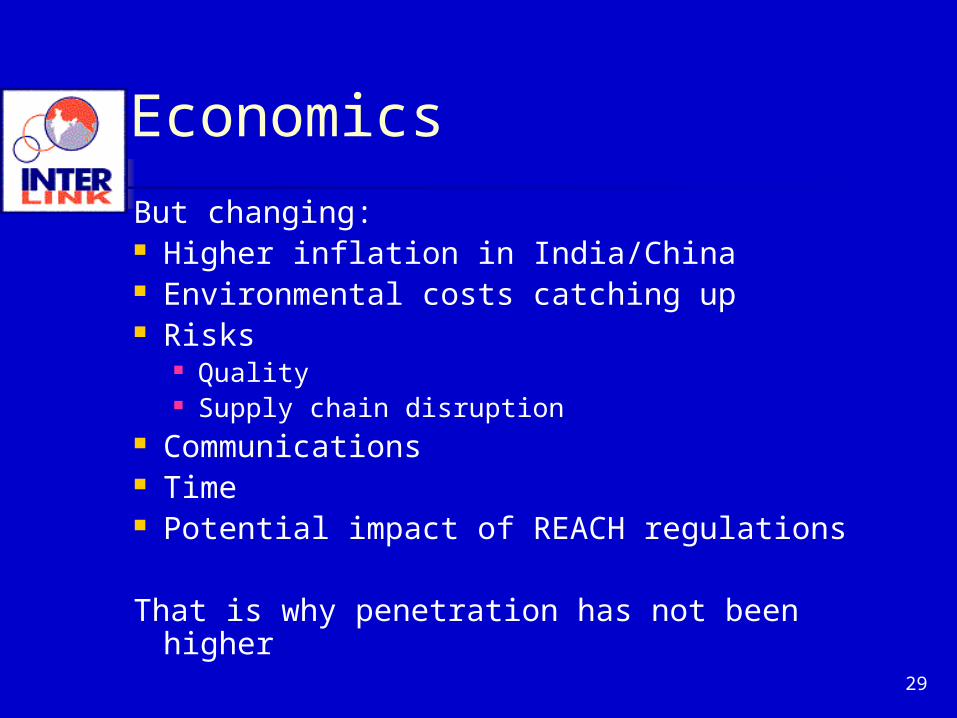

Economics

But changing: Higher inflation in India/China Environmental costs catching up Risks

Quality Supply chain disruption

Communications Time Potential impact of REACH regulations

That is why penetration has not been higher

30

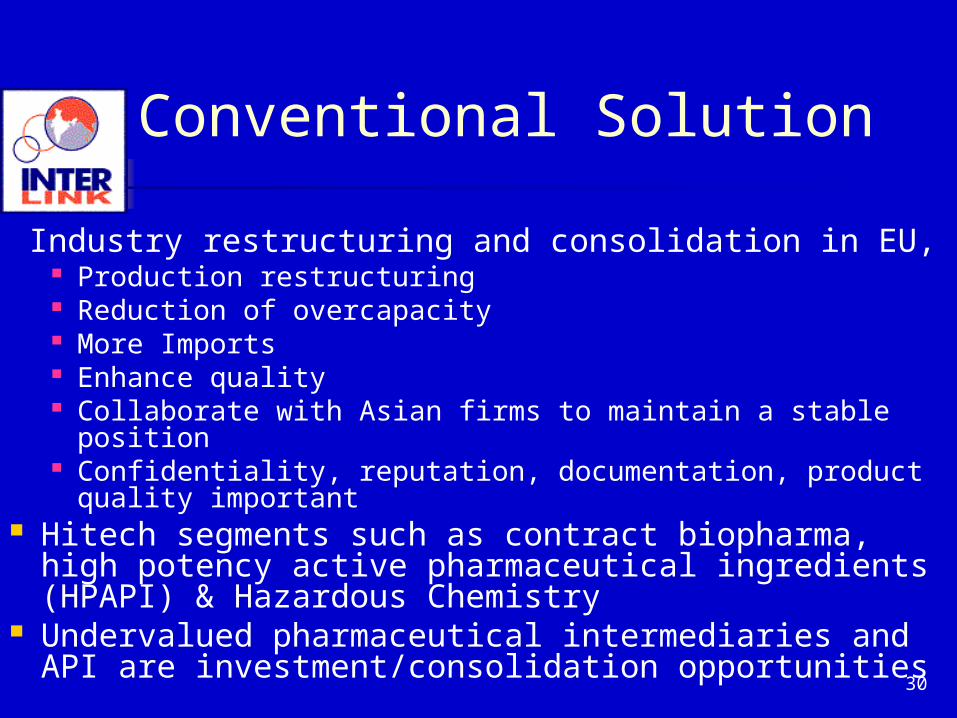

Conventional Solution

Industry restructuring and consolidation in EU, Production restructuring Reduction of overcapacity More Imports Enhance quality Collaborate with Asian firms to maintain a stable

position Confidentiality, reputation, documentation, product

quality important Hitech segments such as contract biopharma, high

potency active pharmaceutical ingredients (HPAPI) & Hazardous Chemistry

Undervalued pharmaceutical intermediaries and API are investment/consolidation opportunities

31

Opportunities for European Companies

Take advantage of Globalisation Acquire/update Asian companies Import from/Export to Asia Distribute in Europe, Asia and

North America Use REACH regulations to

advantage To import To buy time to restructure

32

Acquire/Update Indian Companies

Degussa long-term agreement Hikal

Solvay Pharma got FDA approval for Bavla facility Expanded its facilities in Naroda, India, for

cGMP manufacture of quaternary ammonium and phosphonium compounds and certain bulk drugs.

33

Acquire/Update Indian Companies

Albany Molecular Research USA expanding Indian R&D center, + scale-up lab for APIs and intermediates.

Aceto Corporation USA (a distributor) to buy or build its pharma quality assurance, and analytical labs, and to be Indian logistics center.

Sigma-Aldrich Corporation USA building a manufacturing plant in Bangalore

34

Galaxy Surfactants Ltd.

35

The changing business dynamics in India• Europe and India: dynamics

• Opportunities to invest in, sell to and buy from in India

• India and China competition• Using India to balance supply constraints

• The changing business dynamics in India• India Trade

• The growth of the chemicals businessand trends in India

• Using India as a supply base for other countries

36

India

Purchasing power parity 3rd largest in world of €3 trillion

10th largest GDP at > €600 bn (2006)

2nd fastest growing major economy, with a GDP growth rate of 8.9% (1st quarter 2006–2007)

Growth in industrial output of 11.4% for September 2006 and 12.7% for the year

37

Growth in other Industries

Car sales up 22% in September Indian Engineering & Construction

industry 8.5% CAGR in 5 years, increasing rapidly

Manufacturing to grow from €39 bn in 2003 to €242 bn in 2015

Telephones grew from 14.5 million in 1997 to 120 million in 2006

IT industry has had 29% CAGR in 5 years

38

India

India:FTA with ThailandTrading partner status AseanWorking on EU special relationNAFTA?

India as a base for value added marketing into Asia and Middle East/Africa

India as a source of manufactured goods, not just services and knowledge (and R&D)

39

India – Sustained High Growth India adds:

€36 billion in incremental output (around a tenth of the levels of the US) to world

Annual contribution will rise to €282 billion by 2025 and €1.8 trillion by 2050

By 2050, 1/3 of global economic growth from India

India and China together will account for 2/3

India's economic growth will bring several benefits to Western economies

R&D facilities in India will help reduce costs and improve productivity

Low cost geography and its scientific talent pool, India will provide value added services, globally

Special Economic Zones to give distinct thrust to exports – Tax benefits, export incentives etc.

40

India Merchandise Trade with World

41

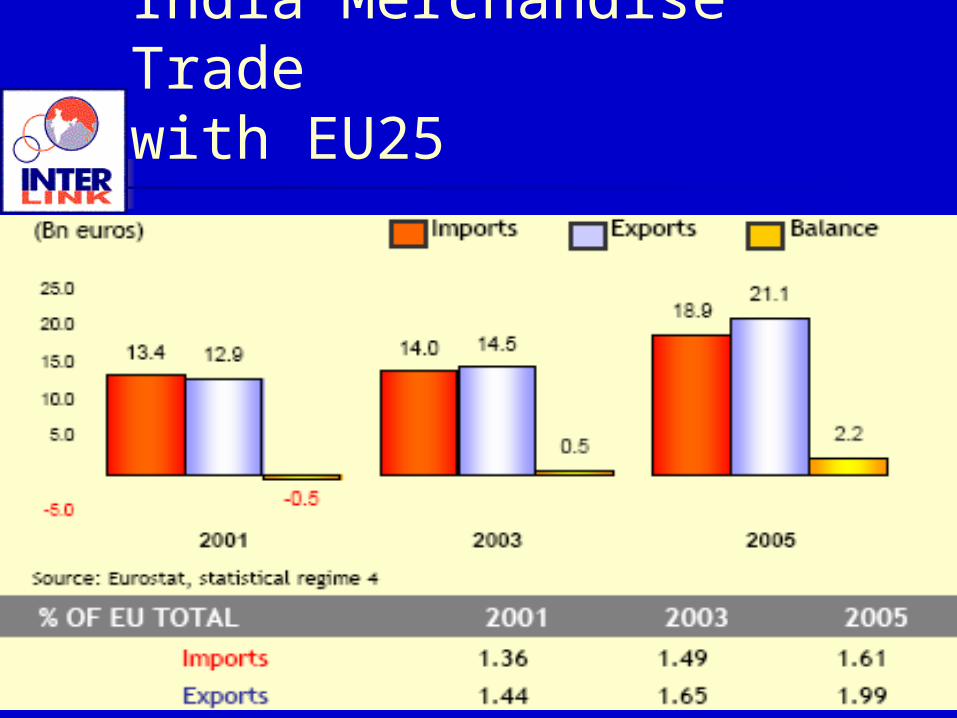

India Merchandise Trade with EU25

42

Indo EU Trade

Total 2 way trade expected to be €80BN in 2011 EU-India trade has grown from €4.4 billion in

1980 to €40 billion in 2005 Trade with the EU represents more than 20% of

Indian's exports and import and EU is India's largest trading partner The EU is also India's largest source of foreign

direct investment. However, India accounts for just 1.8% of total EU

trade. India attracts only 0.3% of the EU's world-wide investments

43

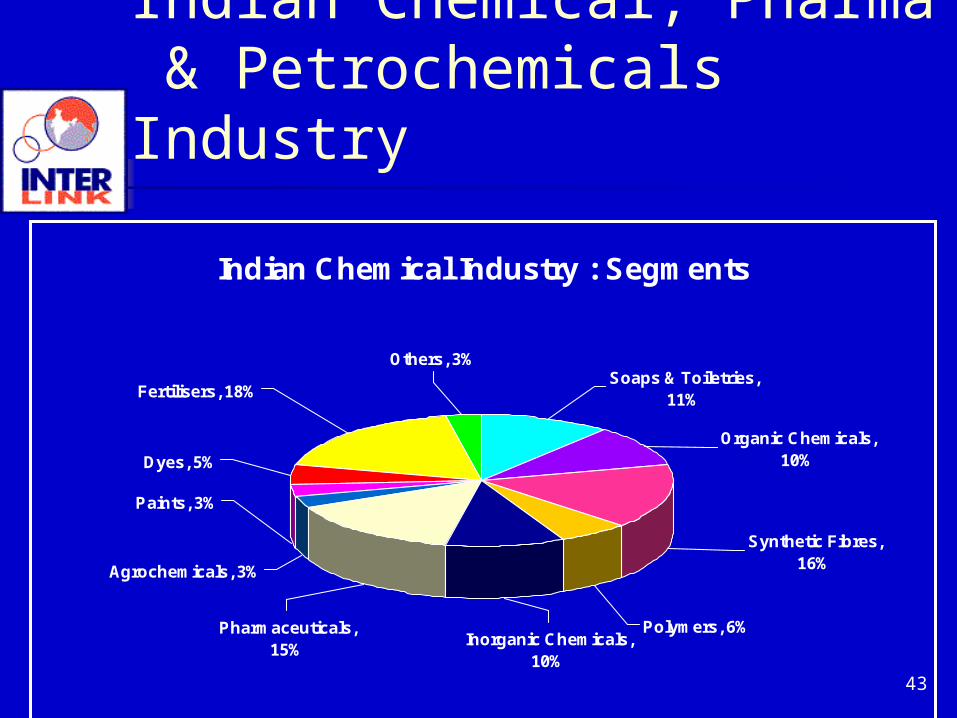

Indian Chemical, Pharma & Petrochemicals Industry

Indian Chemical Industry : Segments

Others, 3%Soaps & Toiletries,

11%

Organic Chemicals, 10%

Synthetic Fibres, 16%

Polymers, 6%Inorganic Chemicals,

10%

Pharmaceuticals, 15%

Agrochemicals, 3%

Paints, 3%

Dyes, 5%

Fertilisers, 18%

44

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

1999-00 2000-01 2001-02 2002-03 2003-04 2005-06

ExportsImports

In Million Euros

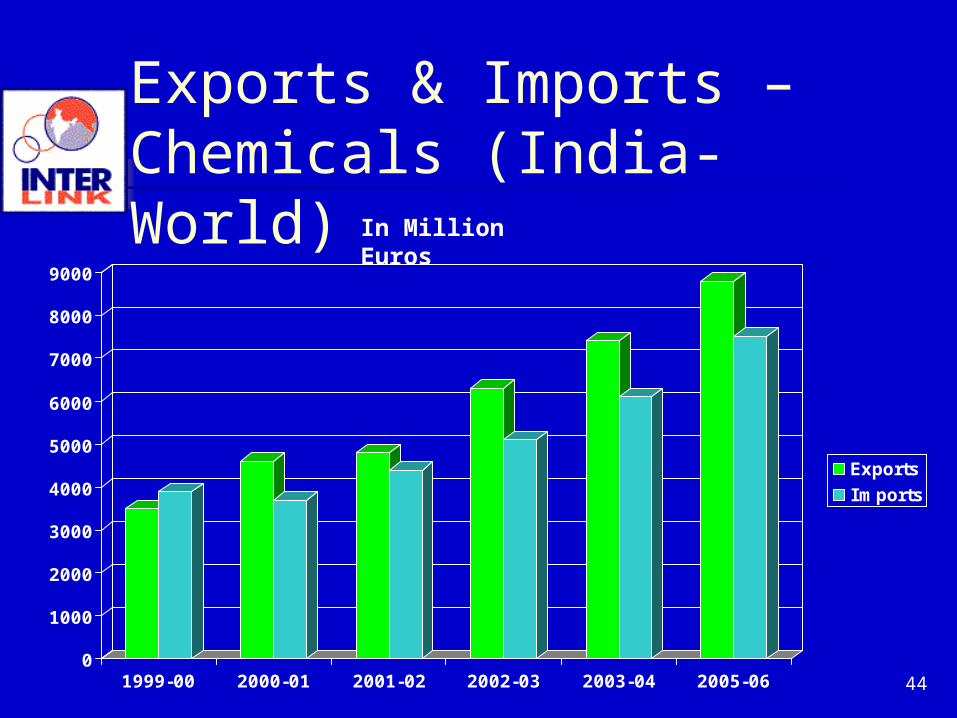

Exports & Imports – Chemicals (India-World)

45

India: Chemicals

Organic Chemicals: 1.53% of EU organic chemicals exported to India

which are 18.63% of India’s needs China, EU are top suppliers to India. India is 11th ranked importer from EU

Inorganic Chemicals: 1.54% of EU inorganic chemicals exported to

India which are 6.26% of India’s needs Inorganic Chemicals suppliers Morocco, South

Africa India ranks 11th as importer from EU

46* These figures include production from unorganized sector, which is estimated at 26% of the production.

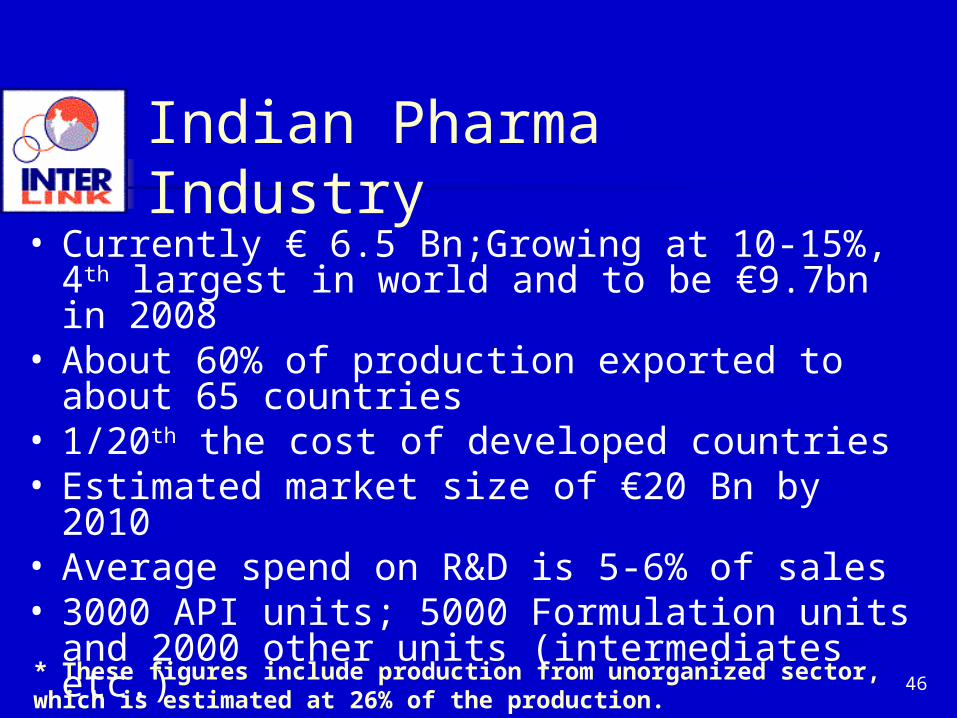

• Currently € 6.5 Bn;Growing at 10-15%, 4th largest in world and to be €9.7bn in 2008

• About 60% of production exported to about 65 countries

• 1/20th the cost of developed countries• Estimated market size of €20 Bn by 2010• Average spend on R&D is 5-6% of sales• 3000 API units; 5000 Formulation units and 2000

other units (intermediates etc.)

Indian Pharma Industry

47

Indian Pharma Industry

Exports are over €3.8 billion. India among top five bulk drug makers. Indian owned companies are 65% increased

from 25% Exports growing by 20% Medicinal plants trade > €725M. 170 biotechnology companies in R&D and

manufacture of genomic drugs, business growing exponentially.

Sequencing genes and delivering genomic information for big Pharmaceutical companies is the next boom industry in India.

48

Indian Pharma Industry

India's bulk drug and pharmaceutical industry grown into a highly sophisticated one, meeting the International standards of Production, Technology and Quality Control

The progress of the Drug industry has rendered the country self-sufficient in National Health Care, has reversed the trend of Indian foreign trade profile from a predominantly importing country to a highly visible exporter to global marketing

49

Indian Pharma Industry

Indian pharmaceutical companies: filed 104 out of 251 new Drug Master Filings made in the US in April- June 2006, largest number of DMFs by any country

India has largest contract research business in pharma industry (2005: $100-120 Mn) and growing at 20-25 per cent per year. About 35 per cent is new drug discovery and 65 per cent is in clinical trials.

Cost saving for a multinational company moving R&D to India is 30-50%

Indian domestic Pharma companies are going global with a direct presence in multinational locations in the world.

50

Pharma Industry

Bulk Drugs, € 1.6 bn, growing at 20%

Formulations, € 5.5 bn, growing at 15%

Imports > € 1.4 bn

Exports € 2.5 bn in 2003, 40% of India’s pharma manufacturing Now € 3.8 bn

51

India’s Pharma Intermediates

Distinctive focus on: Late stage Intermediates Complex Synthetic APIs

Move Towards: Custom Synthesis Low delivered prices Increasing technical & managerial

sophistication

52

Performance of Chemicals during 2001-02 to 2004-05 (000 MT)

Group2001-02

2002-03

2003-04

2004-05

Growth(%) CAGR

Total major Chemicals

Capacity 8012 8334 8750 8933 3.69

Production 5963 6612 7066 7375 7.34

Capacity Utilisation (%) 74.4 79.3 80.8 82.6

Imports 743 724.6 930 914 7.15

Exports 277 435 478 721 37.56

Consumption 6429 6902 7518 7568 5,59

Source: Report 2005-06 Ministry of Chemicals & Fertilizers Govt. of India

Chemicals Industry

53

2001-02 to 2004-05(000 MT)

Group 2001-02 2002-03 2003-04 2004-05 Growth(%) CAGR

Total major Petrochemicals

Capacity 7017 7162 7423 7915 4.1

Production 6235 6553 7006 7348 5.63

Capacity Utilisation (%) 88.9 9 1.5 94.4 92.8

Imports 669 691 830 841 7.93

Exports 698 969 1039 1257 21.66

Consumption 6206 6275 6797 6932 3.76 Source: Annual Report 2005-06 Ministry of Chemicals & Fertilizers (Govt. of India)

Indian Petrochemicals

54

Year Production Imports Exports Demand

2001-02 9,808 1,157 1,150 9,815

2002-03 10,932 997 871 11,058

2003-04 11,269 875 918 11,226

2004-05 13,546 728 844 13,430

2005-06 13,574 - - -

Organic Pigments ‘000 Tons

55

Indian Specialty & Fine Chemicals Industry > €4 Billion/Year Will be one of top-two exporters in low cost countries 2002: Exports valued at €1.6 Billion Growing @15%-20% annually Manufacturing hub for technology – intensive production Better than China in product quality & R&D facilities Specialty chemicals as antioxidants, food additives, and

pigments Pharmaceutical and Agrochemical Industries consume more

than 70% of the fine chemicals produced Performance chemicals being developed in India. Growing

demand from manufacturers of products such as sunscreens and Biocides

Manufacturing for Fine & Specialty chemicals shifting from developed countries to developing countries such as India.

Indian Specialty & Fine Chemicals Market

56

Why India is Important for the European Fine Chemicals IndustryThe changing business dynamics in India

The growth of the fine chemicals businessand trends in India: Knowledge and R&D base

Opportunities to invest in, sell to and buy from in India

India and China competition

Using India to balance supply constraints

Using India as a supply base for other countries

57

Confused European Dynamics* Some European Companies:

GrowingGrowing Others: On the FenceOn the Fence And Some: ExitingExiting

Understand and React to Change

Cos. Trading at Low MultiplesFew Customers for Used Plants

* Marc Hannebert

58

European Growth Drivers

Generics New Molecules (R&D) Speed of Generisation

India is great at these

59

Who is your Customer?

Taking Pharma Intermediate Cos. as an example:

Consumer Final Drug Producer Some one else Insurance Companies?Provide Value Added solution to end

CustomerMove down and up Value Chain, convert

commodities to specialties through soft factors (Roger LaForce)

60

Lessons

European Fine Chemicals Cos. have Customer Base

Change Production Base to India Source Contract Buy someone Use India for R&D: REACH labs in

India

61

Lessons

Build Global Strategy: USA, Asia, and the world

Understand and react to change Try to Europeanise India

Upgrade As economy grows

Insurance companies

62

Lessons

Indian Companies Use Production & R&D base to your

advantage Get closer to Customer

Buy someone close to the customer, or with a customer base

Buy a distribution co. Manage expensive European logistics

Globalise: Backward/Forward Integration Indianise Europe

63

Drivers in India

India low Cost Driven by Government to deliver

low cost health care solutions to the poor Low cost/affordable drugs

Avoid Insurance company syndrome Lobby of people vs. Lobby of insurance companies/drug

companies Example: AIDS drugs

64

India and Specialties

Opportunity for European companies to sell

For Indian companies to develop low cost alternatives

65

We conclude, India is important:

Very cheap source of fine chemicals Growing & important R&D centre Growing market for European companies to tap India is Entering Europe Growing competitor Opportunity for European manufacturers to re-

locate and source from India and to sell in India Sub contract Or source and sell through specialists like Azelis

66

Therefore, understanding India, build a Global Strategy

Used to be in many industries:“What is your China Strategy?”

It is not only that but your Indian and Asian strategy, and your Global strategy

Ignore India at your own risk!

67

THANK YOU

Gautam MahajanInter-Link Services Pvt. Ltd.K 185 Sarai Jullena New Delhi [email protected]+91 98100 60368, Fax +91 11 26929055