Challenging Globalization – The Contemporary Sociological - IEEI

1

The Parmalat case and the recent bankruptcy reform

Lorenzo StanghelliniFacoltà di Giurisprudenza dell’Università di Firenze (*)

Colloquium IEEI, Rome, 19 maggio 2006

2

Part 1

The Collapse of Parmalat

3

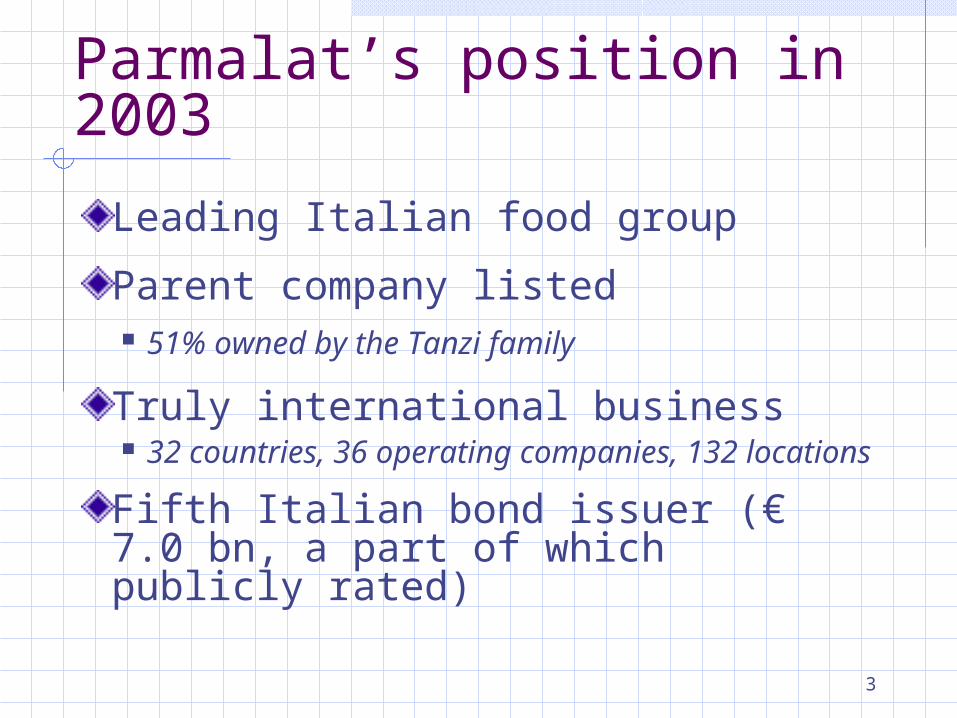

Parmalat’s position in 2003

Leading Italian food group

Parent company listed 51% owned by the Tanzi family

Truly international business 32 countries, 36 operating companies, 132

locations

Fifth Italian bond issuer (€ 7.0 bn, a part of which publicly rated)

4

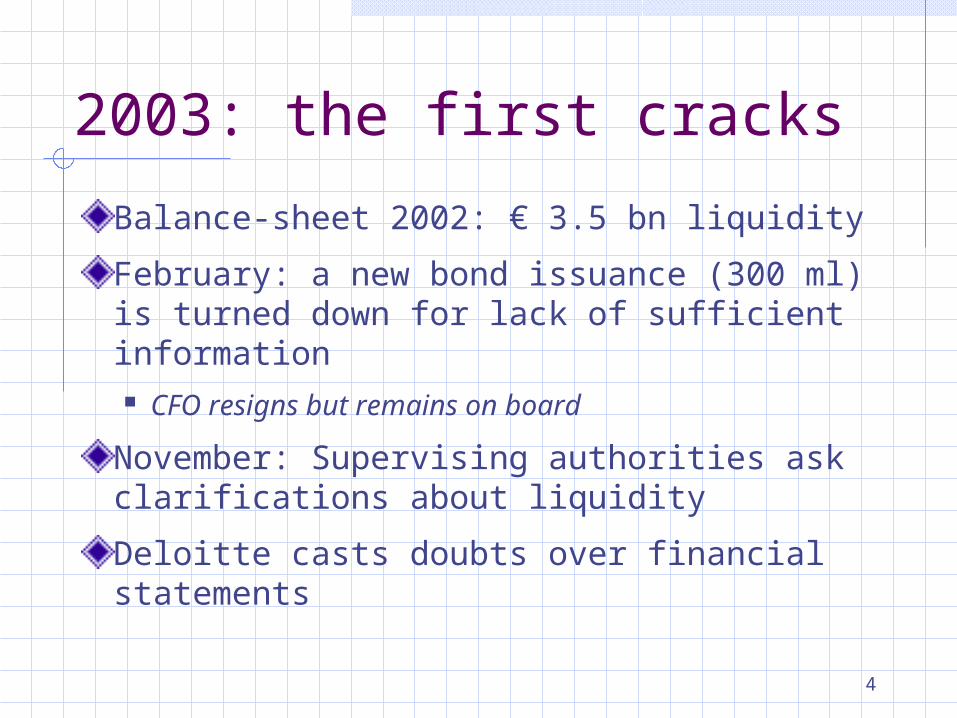

2003: the first cracks

Balance-sheet 2002: € 3.5 bn liquidity

February: a new bond issuance (300 ml) is turned down for lack of sufficient information CFO resigns but remains on board

November: Supervising authorities ask clarifications about liquidity

Deloitte casts doubts over financial statements

5

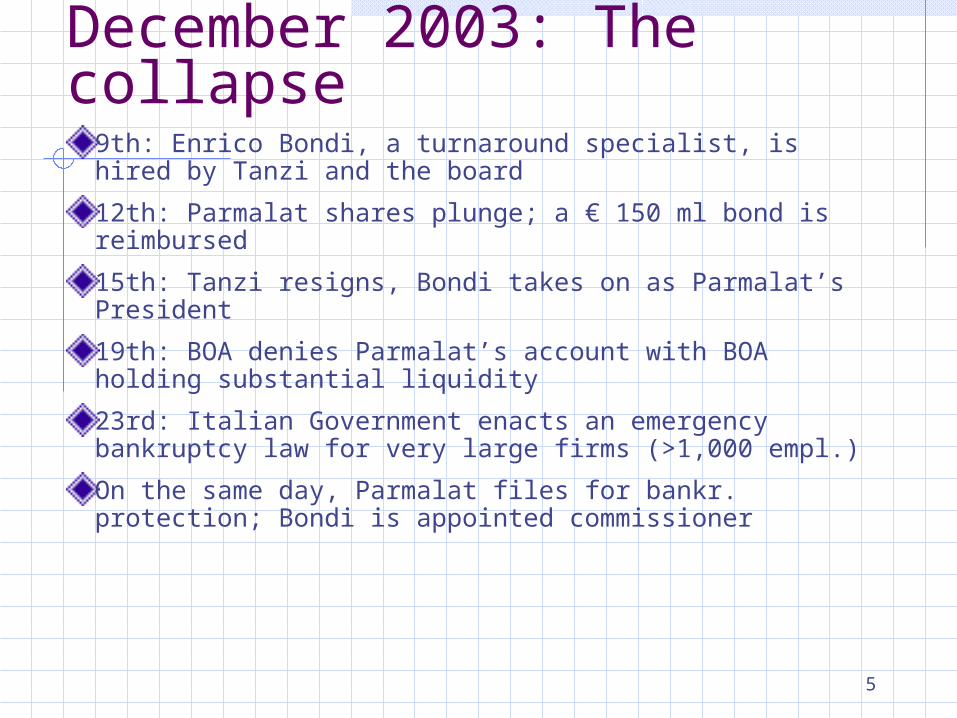

December 2003: The collapse

9th: Enrico Bondi, a turnaround specialist, is hired by Tanzi and the board

12th: Parmalat shares plunge; a € 150 ml bond is reimbursed

15th: Tanzi resigns, Bondi takes on as Parmalat’s President

19th: BOA denies Parmalat’s account with BOA holding substantial liquidity

23rd: Italian Government enacts an emergency bankruptcy law for very large firms (>1,000 empl.)

On the same day, Parmalat files for bankr. protection; Bondi is appointed commissioner

6

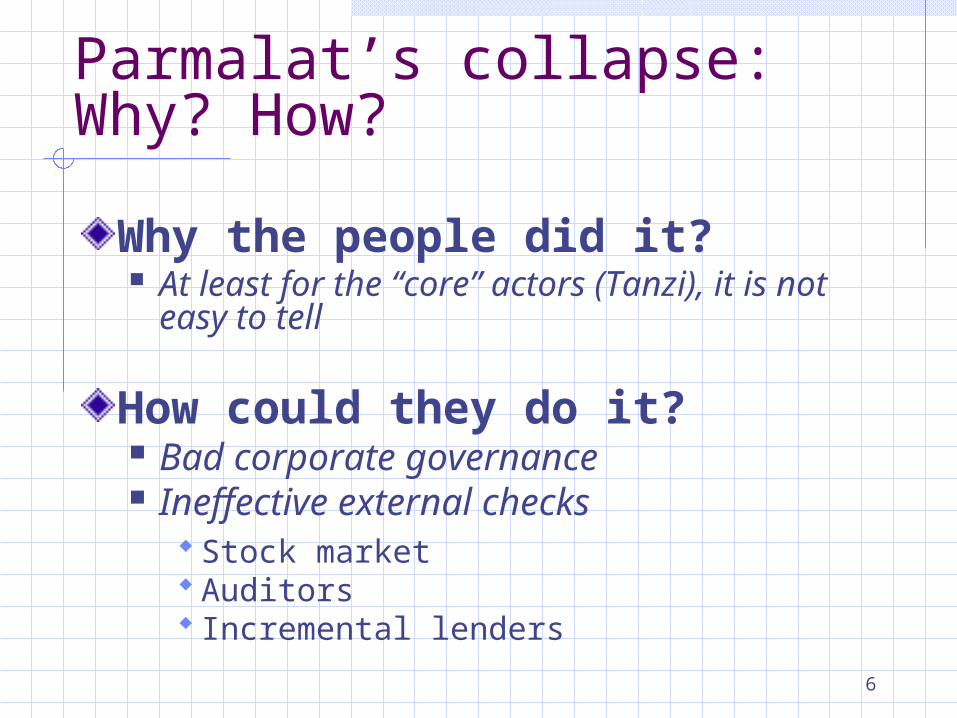

Parmalat’s collapse:Why? How?

Why the people did it? At least for the “core” actors (Tanzi), it is

not easy to tell

How could they do it? Bad corporate governance Ineffective external checks

Stock market Auditors Incremental lenders

7

Part 2

The Rescue of Parmalat

8

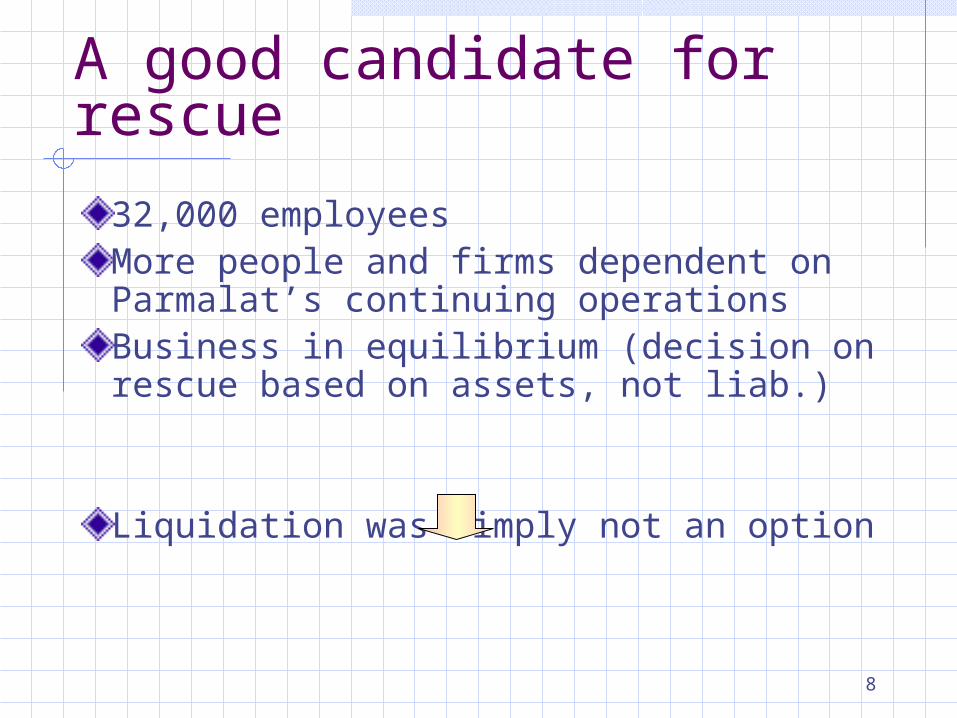

A good candidate for rescue

32,000 employeesMore people and firms dependent on Parmalat’s continuing operationsBusiness in equilibrium (decision on rescue based on assets, not liab.)

Liquidation was simply not an option

9

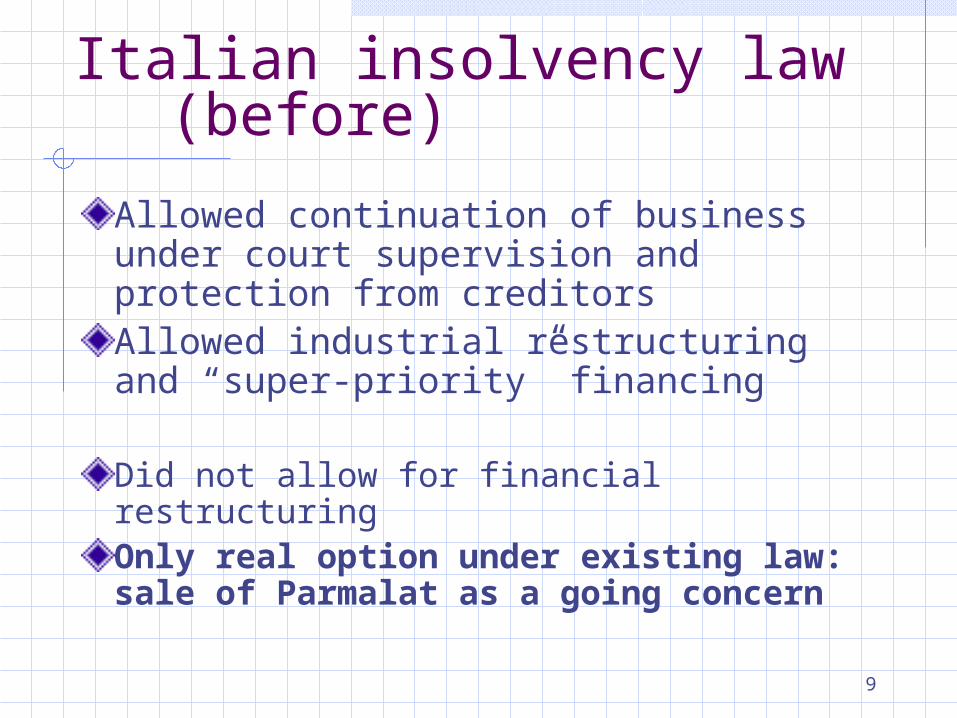

Italian insolvency law(before)

Allowed continuation of business under court supervision and protection from creditorsAllowed industrial restructuring and “super-priority” financing

Did not allow for financial restructuringOnly real option under existing law: sale of Parmalat as a going concern

10

Italian insolvency law (after): d.l. 347/2003 and Law 39/2004

But:

Selling large businesses is difficult Often yields fire-sale prices

Law amended to allow financial restructuring, including debt-equity swap (Law No. 39-2004)Debt-equity swap proposed to creditors: Parmalat would be “sold” to its creditors

11

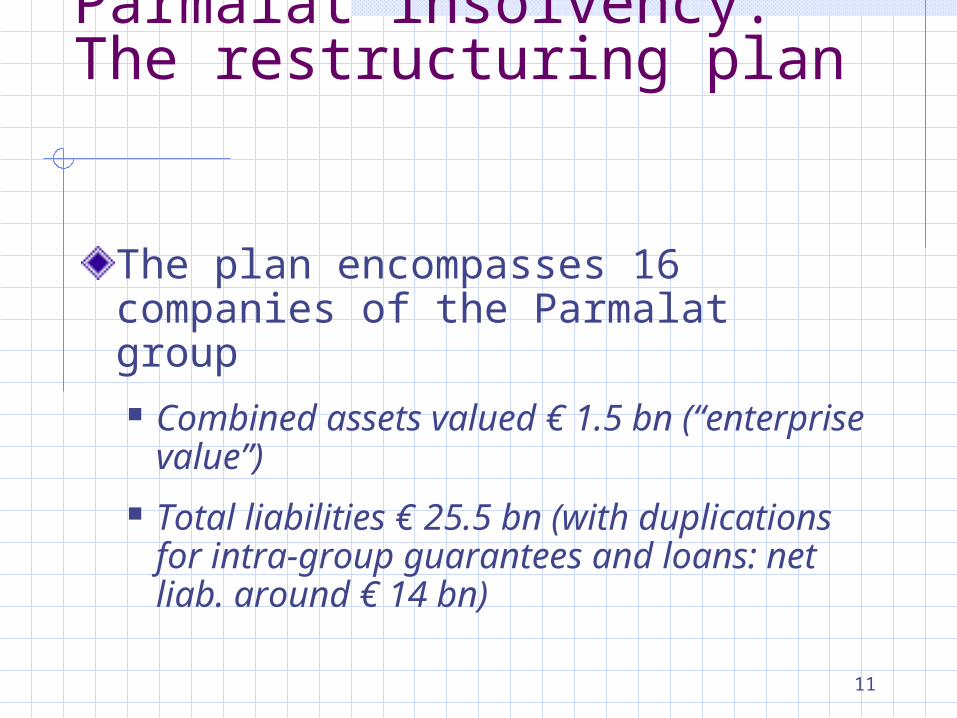

Parmalat insolvency:The restructuring plan

The plan encompasses 16 companies of the Parmalat group Combined assets valued € 1.5 bn

(“enterprise value”)

Total liabilities € 25.5 bn (with duplications for intra-group guarantees and loans: net liab. around € 14 bn)

12

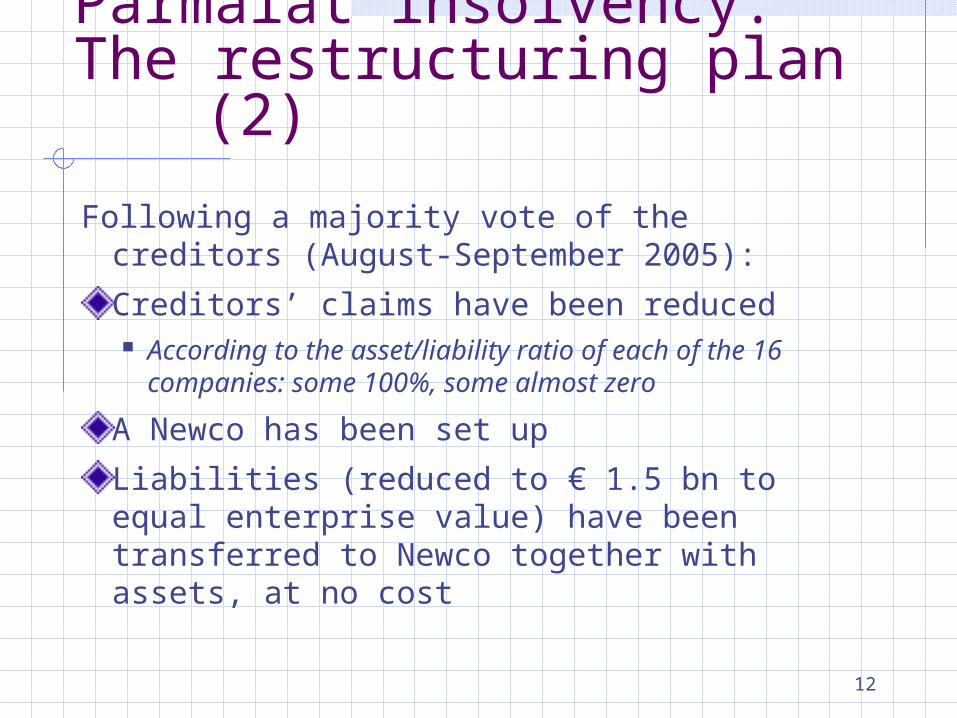

Parmalat insolvency:The restructuring plan (2)

Following a majority vote of the creditors (August-September 2005):

Creditors’ claims have been reduced According to the asset/liability ratio of each of the

16 companies: some 100%, some almost zero

A Newco has been set up

Liabilities (reduced to € 1.5 bn to equal enterprise value) have been transferred to Newco together with assets, at no cost

13

Parmalat insolvency:The restructuring plan (3)

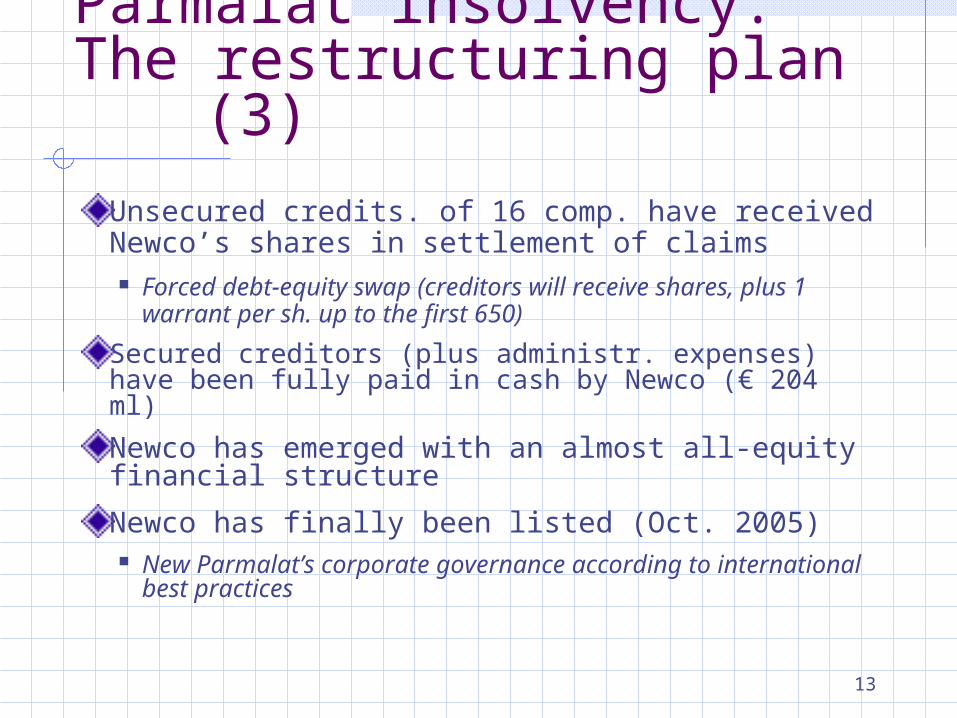

Unsecured credits. of 16 comp. have received Newco’s shares in settlement of claims Forced debt-equity swap (creditors will receive

shares, plus 1 warrant per sh. up to the first 650)

Secured creditors (plus administr. expenses) have been fully paid in cash by Newco (€ 204 ml)

Newco has emerged with an almost all-equity financial structure

Newco has finally been listed (Oct. 2005) New Parmalat’s corporate governance according to

international best practices

14

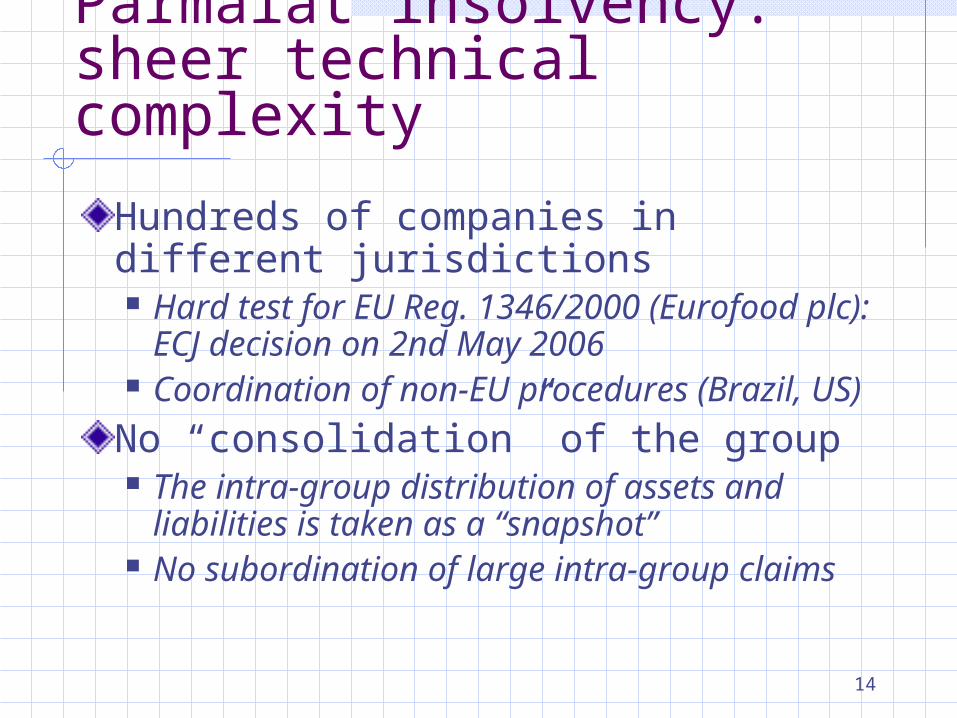

Parmalat insolvency:sheer technical complexity

Hundreds of companies in different jurisdictions Hard test for EU Reg. 1346/2000 (Eurofood

plc): ECJ decision on 2nd May 2006 Coordination of non-EU procedures (Brazil,

US)

No “consolidation” of the group The intra-group distribution of assets and

liabilities is taken as a “snapshot” No subordination of large intra-group claims

15

Parmalat insolvency:sheer technical complexity (2)

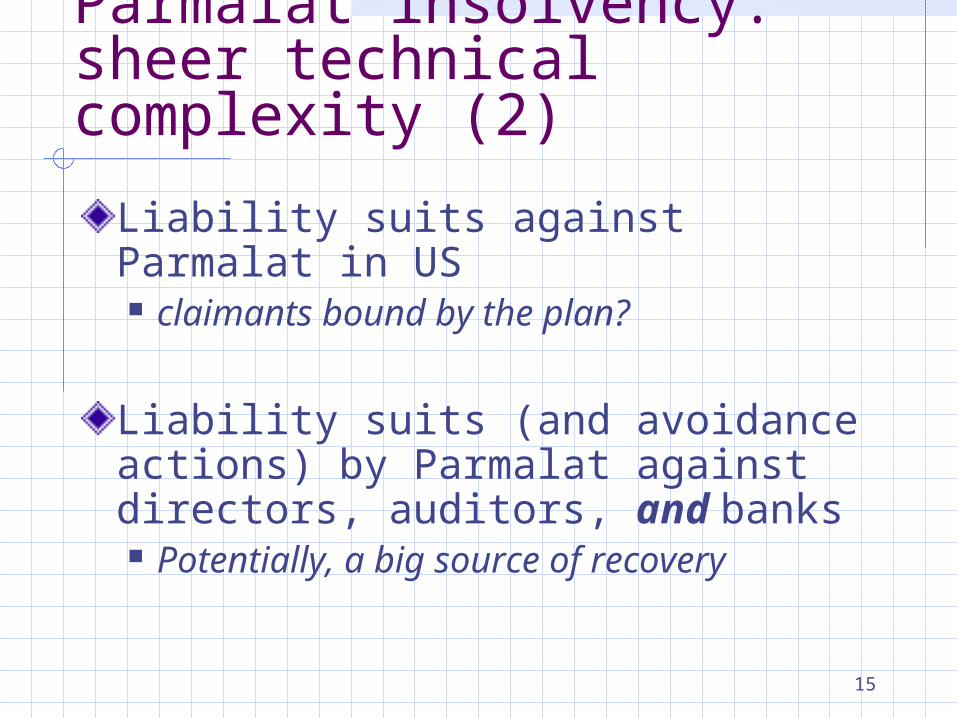

Liability suits against Parmalat in US claimants bound by the plan?

Liability suits (and avoidance actions) by Parmalat against directors, auditors, and banks Potentially, a big source of recovery

16

Part 3

Italian Law after Parmalat

17

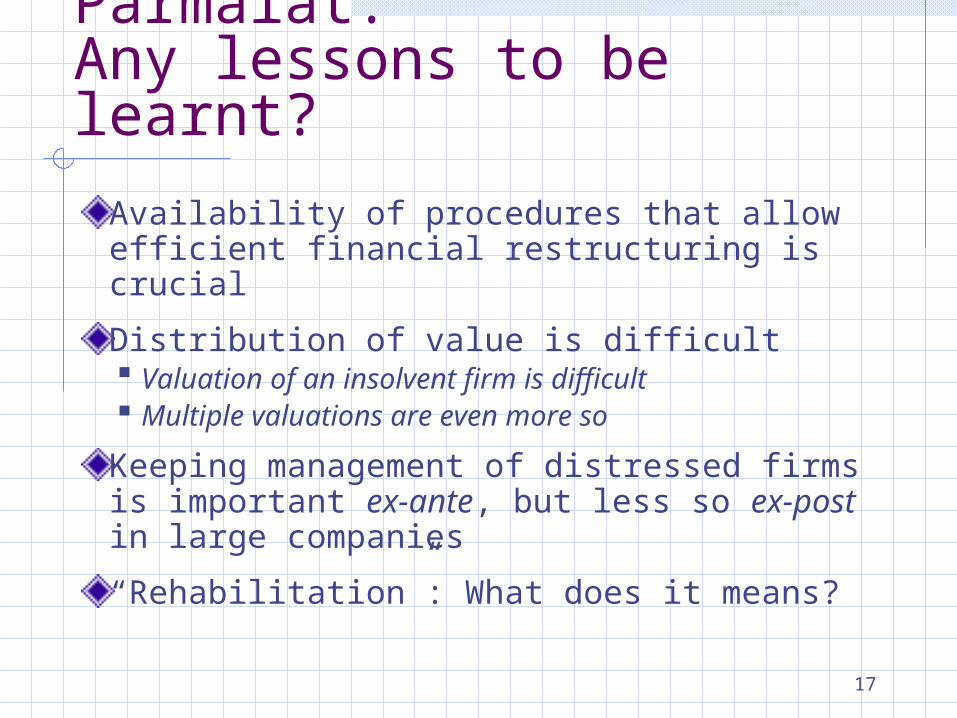

Parmalat: Any lessons to be learnt?

Availability of procedures that allow efficient financial restructuring is crucial

Distribution of value is difficult Valuation of an insolvent firm is difficult Multiple valuations are even more so

Keeping management of distressed firms is important ex-ante, but less so ex-post in large companies

“Rehabilitation”: What does it means?

18

Parmalat: Any lessons to be learnt? (2)

Creditors’ committee necessary to achieve consensus Unfavourable international press (see,

e.g.,“Global Turnaround” March 2004)

A Newco necessary to get around the necessary shareholder’s vote ECJ Pafitis v. Banca Trapeza (1993)

19

Parmalat case: What it does NOT tell

Parmalat needed “pruning” and turnaround

Business was profitable (albeit much less than told)

Therefore: no “tragic choice” (creditors vs. employees/suppliers) has been necessary Alitalia (more than 20.000 employees and

significant operating losses) would be a much more problematic case…

20

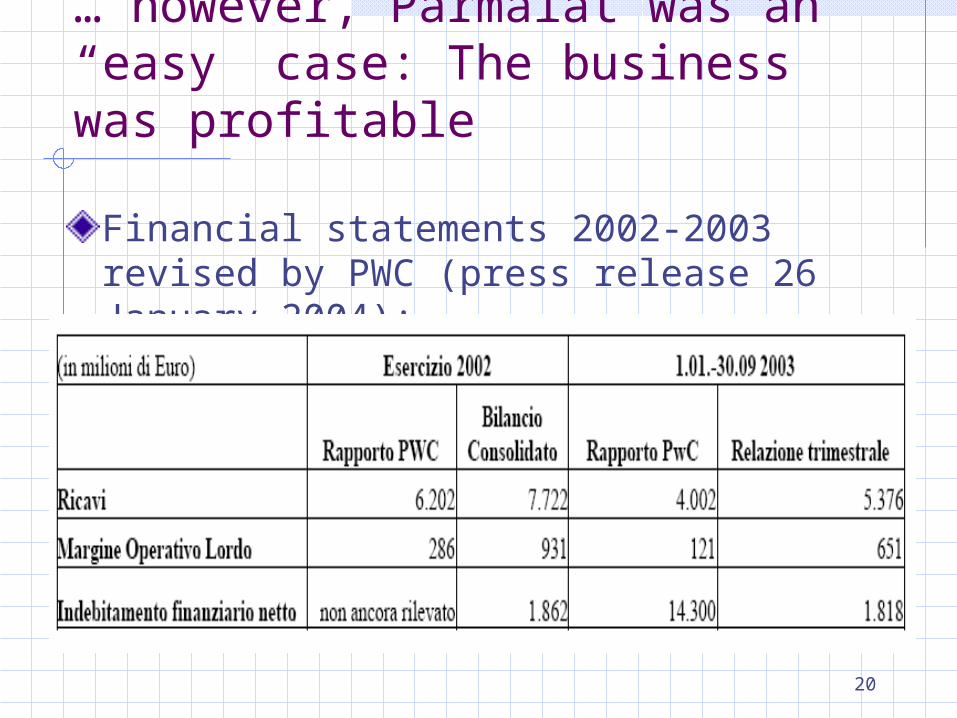

… however, Parmalat was an “easy” case: The business was profitable

Financial statements 2002-2003 revised by PWC (press release 26 January 2004):

21

The new composition procedures: (a) The “Concordato preventivo”

Decree-Law 14 March 2005, n. 35: New “concordato preventivo” Plan by the debtor to avoid the bankruptcy procedure

(“Fallimento”) through a composition with the creditors

High degree of flexibility, classes of creditors No constraints on financial restructuring proposals by

the debtor Debt for equity swap possible pursuant to a majority

vote

New Art. 160 of bankruptcy is taken almost literally from Art. 4-bis l. 39/2004 (Parmalat law)

22

The new composition procedures: (b) The “Concordato fallimentare”

D.lgs. 9 January 2006, n. 5: the new “concordato fallimentare” Plan by the debtor, any creditor or third

party, to close the bankruptcy procedure (“Fallimento”)

Same potential for restructuring of the new “concordato preventivo”

New concept of “concordato”

23

The legacy of ParmalatA “giant leap forward”. Now let us consolidate Reform of general bankruptcy law by

d.lgs. 9 January 2006, n. 5: an important work in progress

Generalize Parmalat: NO, thanks Creditors have been kept out of the door

Called upon at the end for a vote on a plan “take it or leave it”

The success of Parmalat turnaround is due to the business and the people who worked on it. Now it’s enough…

![UNCLASSIFIED ,,4E IEEI MINE DEC HOIST OPERATOR TRAINING ... · Training Program Instruction Manual DTIC ELECTE f I LI] ...](https://static.fdocuments.us/doc/165x107/5b6d012d7f8b9a0b558c5987/unclassified-4e-ieei-mine-dec-hoist-operator-training-training-program.jpg)

![Diploma Supplement Giurisprudenza Universita Cattolica[2305843009213743626]](https://static.fdocuments.us/doc/165x107/589a21561a28ab2a678b6b51/diploma-supplement-giurisprudenza-universita-cattolica2305843009213743626.jpg)