1 The long and winding road The world economy, the Arab Spring, and what it means for you Robin Bew,...

30

1 he long and winding road he world economy, the Arab Spring, nd what it means for you bin Bew, Managing Director bai, October 2013

-

Upload

letitia-chandler -

Category

Documents

-

view

215 -

download

0

Transcript of 1 The long and winding road The world economy, the Arab Spring, and what it means for you Robin Bew,...

1

The long and winding road

The world economy, the Arab Spring, and what it means for you

Robin Bew, Managing DirectorDubai, October 2013

Risk, recovery, rebalancing

• A gradual end to the Fed’s money-printing will raise US interest rates and draw capital from emerging markets.

• Rich economies are gradually rebounding from long slumps. Even Europe and Japan are making progress.

• Many developing economies, especially the BRICs, are suffering. Is the emerging market growth story over or just evolving?

Risk

Time to taper? The Fed will buy fewer bonds

• Bernanke says the Fed will reduce bondbuying if the jobs market continues to improve US jobless rate down to 7.3% from 10%

• Fed was increasingly concerned about instability in asset markets

• Exit strategy was always going to be complicated Search for yield pushed capital into emerging markets Markets became addicted to QE

• So Bernanke was cautious; so far, nothing has happened Global sell-off, especially in emerging markets, probably overdone

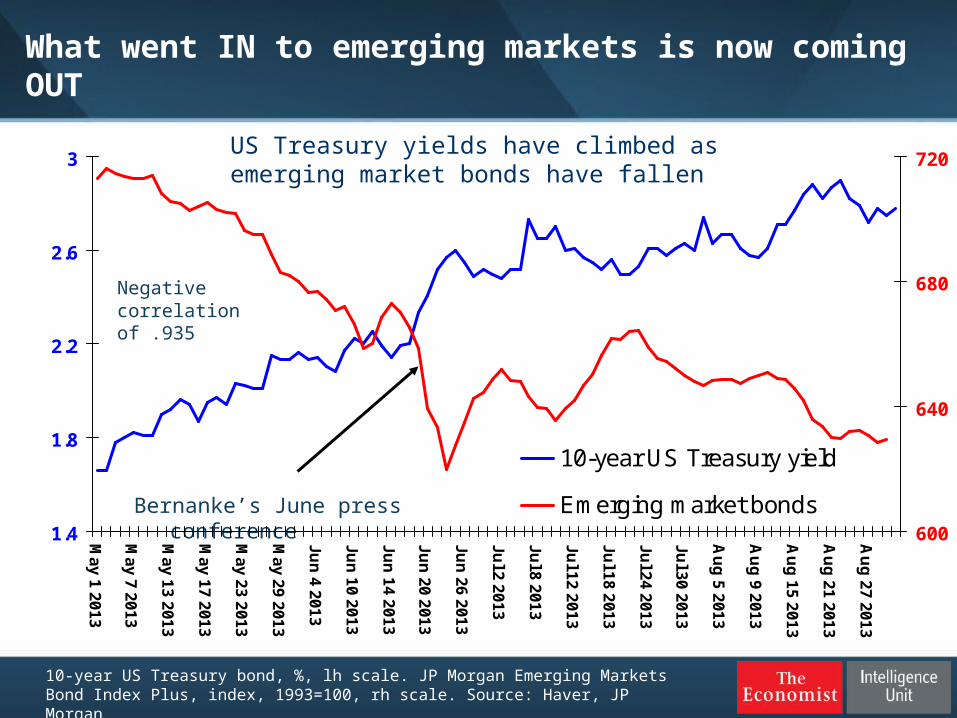

What went IN to emerging markets is now coming OUT

1.4

1.8

2.2

2.6

3

Ma

y 1

20

13

Ma

y 7

20

13

Ma

y 1

3 2

01

3

Ma

y 1

7 2

01

3

Ma

y 2

3 2

01

3

Ma

y 2

9 2

01

3

Ju

n 4

20

13

Ju

n 1

0 2

01

3

Ju

n 1

4 2

01

3

Ju

n 2

0 2

01

3

Ju

n 2

6 2

01

3

Ju

l 2 2

01

3

Ju

l 8 2

01

3

Ju

l 12

20

13

Ju

l 18

20

13

Ju

l 24

20

13

Ju

l 30

20

13

Au

g 5

20

13

Au

g 9

20

13

Au

g 1

5 2

01

3

Au

g 2

1 2

01

3

Au

g 2

7 2

01

3

600

640

680

720

10-year US Treasury yield

Emerging market bonds

10-year US Treasury bond, %, lh scale. JP Morgan Emerging Markets Bond Index Plus, index, 1993=100, rh scale. Source: Haver, JP Morgan

Bernanke’s June press conference

Negative correlation of .935

US Treasuries soar, emerging market bonds plunge

US Treasury yields have climbed as emerging market bonds have fallen

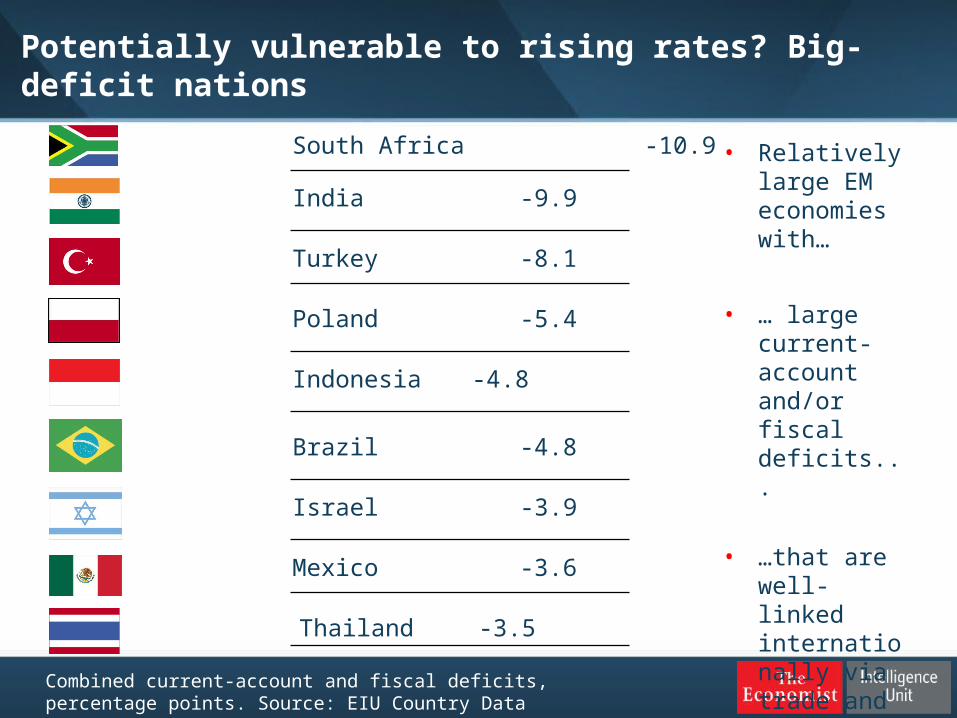

Potentially vulnerable to rising rates? Big-deficit nations

South Africa -10.9

India -9.9

Turkey -8.1

Poland -5.4

Indonesia -4.8

Brazil -4.8

Israel -3.9

Mexico -3.6

Thailand -3.5

Combined current-account and fiscal deficits, percentage points. Source: EIU Country Data

• Relatively large EM economies with…

• … large current-account and/or fiscal deficits...

• …that are well-linked internationally via trade and investment

Recovery

Manufacturing is expanding in the US, China and…

30

35

40

45

50

55

60

65

12/31/2007

3/31/2008

6/30/2008

9/30/2008

12/31/2008

3/31/2009

6/30/2009

9/30/2009

12/31/2009

3/31/2010

6/30/2010

9/30/2010

12/31/2010

3/31/2011

6/30/2011

9/30/2011

12/31/2011

3/31/2012

6/30/2012

9/30/2012

12/31/2012

3/31/2013

6/30/2013

US

China

Euro zone

Diffusion index; 50 is dividing line between expansion and contraction. Source: Bloomberg

Purchasing managers’ indices

…yes, EVEN IN EUROPE, where industry is growing for the first time in two years.

Rebalancing:

Is the EM growth story over?

Many people think so; look at the headlines

Source: Financial Times

Main reasons for “death of emerging markets” story

• Weak demand from chronically struggling rich countries So fewer EM exports

• China’s growth has slowed China is huge draw for EMs

• End of credit, liquidity boom Monetary policy has tightened

• Hubris caused EM reforms to lag Weaknesses never addressed

• Commodity supercycle is over Weaker terms of trade for commodity exporters

• US Federal Reserve liquidity tightening

Conclusion: Emerging markets rebalancing, not retreating

• Yes, China won’t grow as fast now that it’s middle-income; no surprise In absolute US$, China will add more to GDP now than when it grew

by 14%

• Many EMs, like India, are still under-developed, have young populations and have good growth potential, if they reform Infrastructure need in India, Brazil, Africa, etc is huge

• Recovery in rich countries will boost emerging markets in medium term

• Emerging markets struggling with credit-boom fallout, but this is cyclical

• Shifting to more balanced growth (more consumer spending, less exports) is good thing and should re-set the foundation for better growth

The Middle East outlook

14

The Arab spring: Where did it go wrong?

A lack of experienced leaders and parties• Experienced politicians and bureaucrats often tainted by association

Muslim Brotherhood only show in town most of the time

Mistakes• New leaders have taken on some of the facets of their predecessors• Transitions often poorly planned (Egypt in particular)

Incumbents dug in• Libya, Bahrain and now Syria• Saudi and the rest of the GCC

Impatient populations• Instability has stymied investment and job-creation, creating a backlash against

barely-installed incumbents (weak global economy not helped either) “Economically considered, war and revolution are always bad business” - Ludwig von Mises

But above all….

The sheer scale of the challenge• Decades of oppression have allowed underlying economic, societal and sectarian

tensions to fester

15

Political stability risk, June 2010

Uncertainty breeds instability

Source: EIU Risk Briefing.

16

Uncertainty breeds instability

Source: EIU Risk Briefing.

Political stability risk, December 2012

17

...which in turn depresses growth

Real GDP growth(%)

2006-10 2011-13

Egypt 6.2 1.9

Tunisia 4.6 1.5

Yemen 4.0 -1.4

Syria 4.9 -11.8

Libya 3.2 13.7

Saudi Arabia 2.8 5.7

UAE 3.2 4.1

-61% in 2011

18

RESULT: An uneven regional picture

Liby

a

Tuni

sia

Egyp

tIra

qUAE

Saud

i02468

101214

FDI inflows, 2012 (US$ bn)

The haves• Stability will continue to drive prosperity• But so will oil!

• Risk premium hugely beneficial to the GCC states (as well as Algeria & Iraq)

• Policy helping• Expansionary fiscal policy will remain• Bloated bureaucracies, but implementation improving

• External consultants increasingly in vogue• But policies to nationalise workforce can be a headache

The have nots• Most affected by the Arab Spring and its fallout

• Levant & North Africa • Typically both non-oil & poorer

• Waxing and waning of the Muslim Brotherhood• Will be far less electorally dominant

• But in long run may have the better potential• Larger populations, cheap labour, export-oriented

19

A few to keep you up at night

Egypt• A little bit of history repeating….

• Military to all intents and purposes now in charge• Unrest will persist, deterring foreign investment• Massive GCC aid, but won’t be enough• Similarities with Algeria, but economy will make it harder for military

• Economic restructuring programme inevitable, probably with IMF

Tunisia• Post-revolutionary pains

• Tunisia rocked by political assassinations…• Salafis out the bottle

• …but best chance of completing a successful transition• Al-Nahda conciliatory compared with its MB peers

Syria• No good options….

• US attack still on the table; outcome massively uncertain• Spillover (ISIS; Kurds; Lebanon; Israel)• Outcome: Assad eventually falls, but the country could take decades to recover

So where is the opportunity?

21

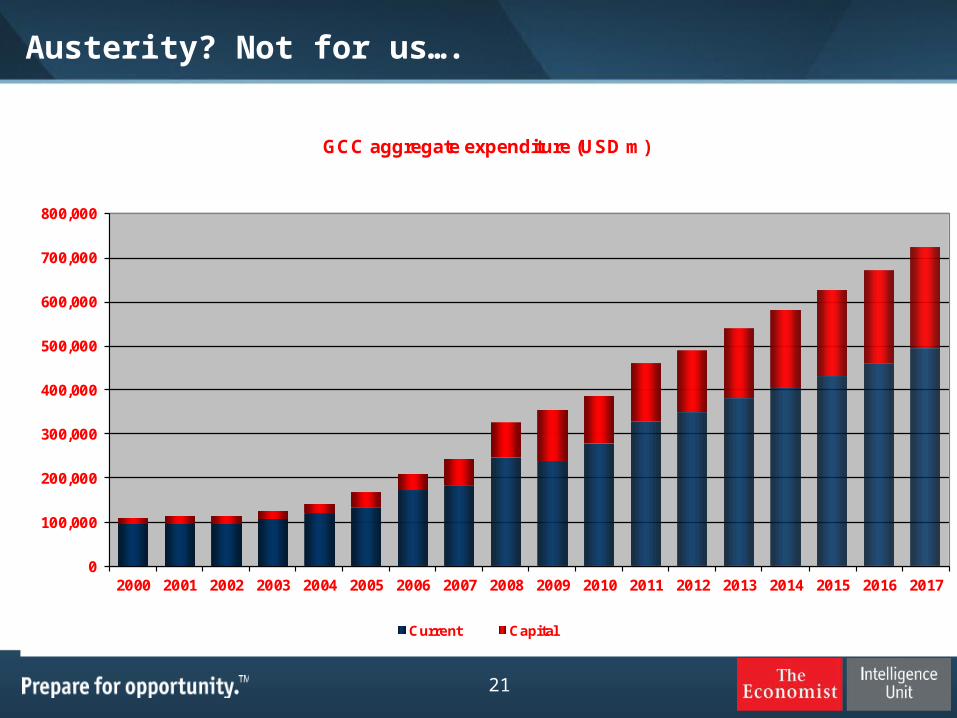

Austerity? Not for us….

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

GCC aggregate expenditure (USD m)

Current Capital

22

Rising affluence

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

GDP/capita ($)

GCC MENA Levant Iraq N Africa

23

Spend, spend, spend

Build the infrastructureAll aboard the GCC train• Massive rail projects in Saudi, Qatar, Oman, and the UAE

Riyadh Metro’s budget alone is US$28.7bn

Keep taxes low• Low corporation tax; no income tax; no VAT• Free zones in UAE (tax-free and 100% ownership)

And watch them come!• Services hubs

Financial services: Bahrain, Dubai, Doha Dubai Media City; Tourism

• Manufacturing hubs King Abdullah Economic City, Yanbu Economic City (Saudi)

• Jebel Ali Free Zone; Khalifa Industrial Zone Abu Dhabi

24

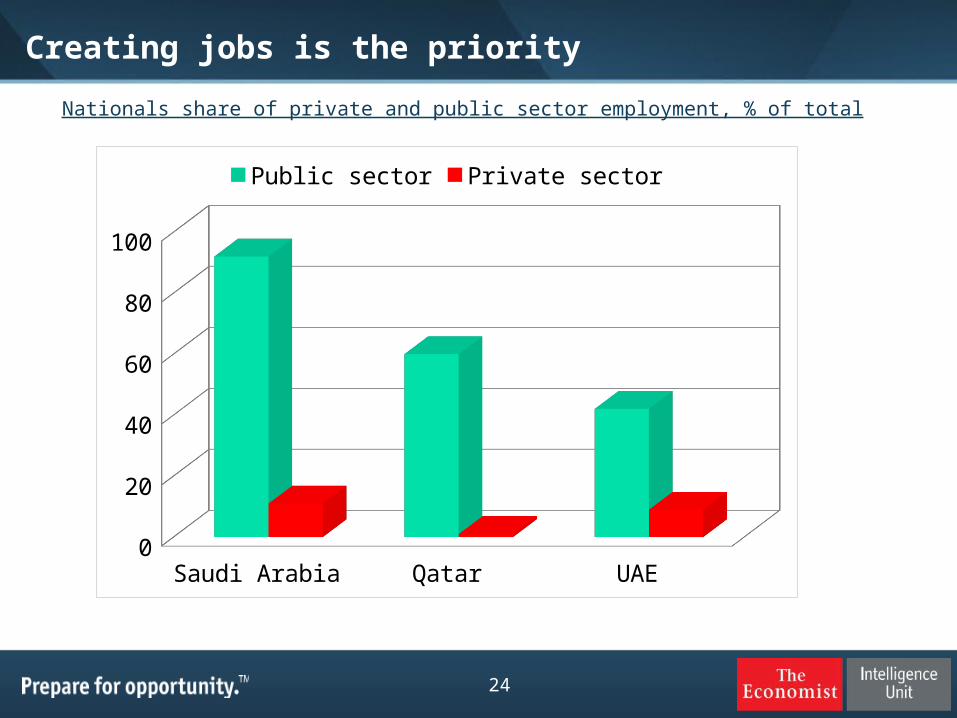

Creating jobs is the priority

Nationals share of private and public sector employment, % of total

Saudi Arabia Qatar UAE0

102030405060708090

100

Public sector Private sector

25

Give ‘em what they want

• Finding the right kind of jobs EIU expects IT & communication and financial services

to be fastest-growing sectors in Gulf in 2013-17

• But will need investment in R&D… Qatar seeking to boost R&D to 2.8% of GDP Abu Dhabi Vision 2030

◦ Public spending on research to exceed 0.75% of GDP by 2018

• …and education Dubai International Academic City Qatar Education City King Abdullah University of Science and Technology

◦ First-mixed campus university in Saudi Arabia

• Masdar City breaks new ground Low-carbon city Hub for renewables technology

• More tech entrepreneurs needed Maktoob takeover by Yahoo points the way

2626

Macro risks & business challenges

• GCC Oil price Domestic political instability Domestic energy

consumption Iran Global economic contagion

◦ Financial◦ Trade

• North Africa Revolutionary transitions Insecurity in Sahel Euro zone slowdown

• Levant Syria overspill

• Political risk Instability engaging with governments

• Talent Good talent: rare or expensive Nationalisation

• Regulation lags vision and growth

• Price pressures Inflation Drive for value

• Payment risk Cashflow pressures

• Supply chain cross border trade: bureaucratic

and subject to political interference

What does it mean for you?

28

• What does the EIU see? Granularity

◦ increased demand for emerging and pre-emerging market information

◦ demand for industry information

◦ demand for risk analysis

• Understanding the customer need need for customisation

• Flexible delivery mechanisms• Demand for ever higher

quality relevance, accuracy and speed

• The librarian’s reality more demanding internal

clients evolving offering from your

suppliers

• The challenges (as we see them) match information to the need ever greater understanding of

your users needs ever greater understanding of

the strengths and weaknesses of your sources

• The result a significant source of value to

your institution

Librarians and the knowledge economy

29

The impact

• Tremendous economic opportunity across the region Tangible in GCC Potential in Levant and North Africa

• But need to operate at mid to high end of value curve Manufacturing, financial services etc

• Need to bring local population into workforce• Need to design policies and institutions

All creates need for education and research◦ Places great emphasis on educational institutions

► To enhance local talent► As an export in it’s own right

30

Questions?