1 the future is friendly 2005 annual and special meeting Edmonton – May 4, 2005.

47

1 the future is friendl 2005 annual and special meeting Edmonton – May 4, 2005

-

Upload

brent-merritt -

Category

Documents

-

view

214 -

download

0

Transcript of 1 the future is friendly 2005 annual and special meeting Edmonton – May 4, 2005.

1

the future is friendly

2005annual and special meeting

Edmonton – May 4, 2005

2

financial reviewRobert McFarlaneEVP & Chief Financial Officer

3 all dollars in C$ unless otherwise specified3

These CEO & CFO presentations and answers to shareholder questions contain forward-looking statements about expected future events including competition, labour relations developments and financial and operating results that are subject to risks and uncertainties. TELUS’ actual results, performance, or achievement could differ materially from those expressed or implied by such statements. For additional information on potential risk factors, see TELUS’ 2004 Annual Report, and other filings with securities commissions in Canada and the United States.

TELUS disclaims any intention or obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

forward-looking statements

4

Exceeded Original Target?1

Revenue $ 7.6B 6.1%

EBITDA $ 3.1B 9.8%

EPS2 $ 1.58 72%

Free Cash Flow3 $ 1.3B 54%

Net Debt to EBITDA 2.1 times 22%

1 Provided Dec. 18, 2003

3 EBITDA, adding Restructuring and workforce reduction costs, cash interest received and excess of share compensation expense over share compensation payments, subtracting cash interest paid, cash taxes, capital expenditures, and cash restructuring payments

2 EPS included $0.20 in 2003 and $0.21 in 2004 for favourable settlement of tax matters

Change2004

consolidated performance

2004 review

5

2005 – first quarter review

6

2005 – first quarter review

Record first quarter results

1 Including restructuring and workforce reduction costs of $16M in Q1-04 and $9M in Q1-05

TELUS consolidated

Revenue $ 1.80B $ 1.98B 9.5%

EBITDA1 $ 721M $ 856M 19%

Net Income2 $ 101M $ 242M 139%

EPS 2 $ 0.28 $ 0.67 139%

EPS (excl. tax settlements) $ 0.24 $ 0.52 117%

Dividend per share $ 0.15 $ 0.20 33%

Q1-05Q1-04 Change

2 Including favourable impacts for tax settlements on net income of $14M or $0.04 per share in Q1-04, and $54M or $0.15 per share in Q1-05

7 Strong margin expansion across both segments

1 Earnings before interest, taxes, depreciation and amortization divided by total revenue

4042 43

40

2005

2004

39

45

Q1 Q1 Q1 Q1 Q1 Q1 Mobility Communications Consolidated

2005 – first quarter review

EBITDA margin1 (%)

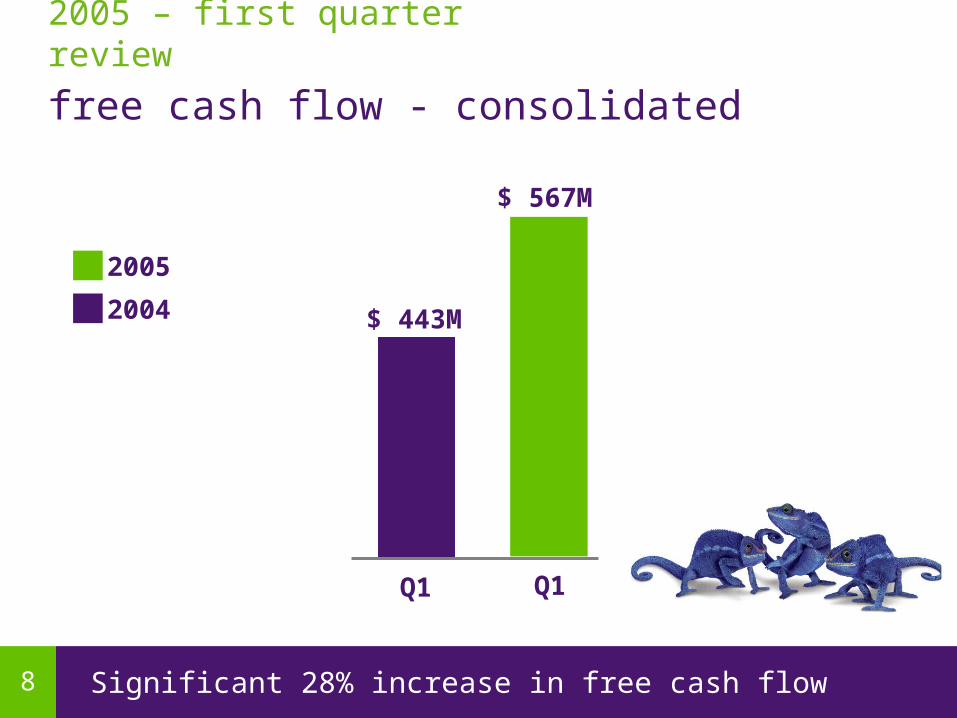

8 Significant 28% increase in free cash flow

$ 443M

2005

2004

$ 567M

Q1Q1

free cash flow - consolidated

2005 – first quarter review

9 Strong gains in wireline profitability and cash flow

43%$ 305M$ 214MCash Flow (EBITDA less capex)

4.5 pts17.2%21.7%Capital Intensity2

9.6%$ 519M$ 474MEBITDA1

4.4%$ 1.22B$ 1.17BExternal Revenue

ChangeQ1-05Q1-04

1 Earnings before interest, taxes, depreciation and amortization

Communications segment

2005 – first quarter review

2 Capital expenditures divided by total revenue

10

8(3)(14) 4(9)

Q1-04 Q2-04 Q3-04 Q4-04 Q1-05

128145

131156 160

Communications segment

Positive trend with record revenue; 2nd quarter of positive EBITDA benefited in part by non-recurring items

Revenue

EBITDA

($M)

review of operations - Communications

non-ILEC revenue & EBITDA

~$3-4M run rate

11High-speed Internet subscriber additions of 22K in quarter; base up 18% year over year in maturing market

605K

712K

2004

high-speed Internet982K

total Internet subscribers

2005

high-speed 72%

dial-up28%

712K

270K

high-speed Internet subscriber growth

review of operations - Communications

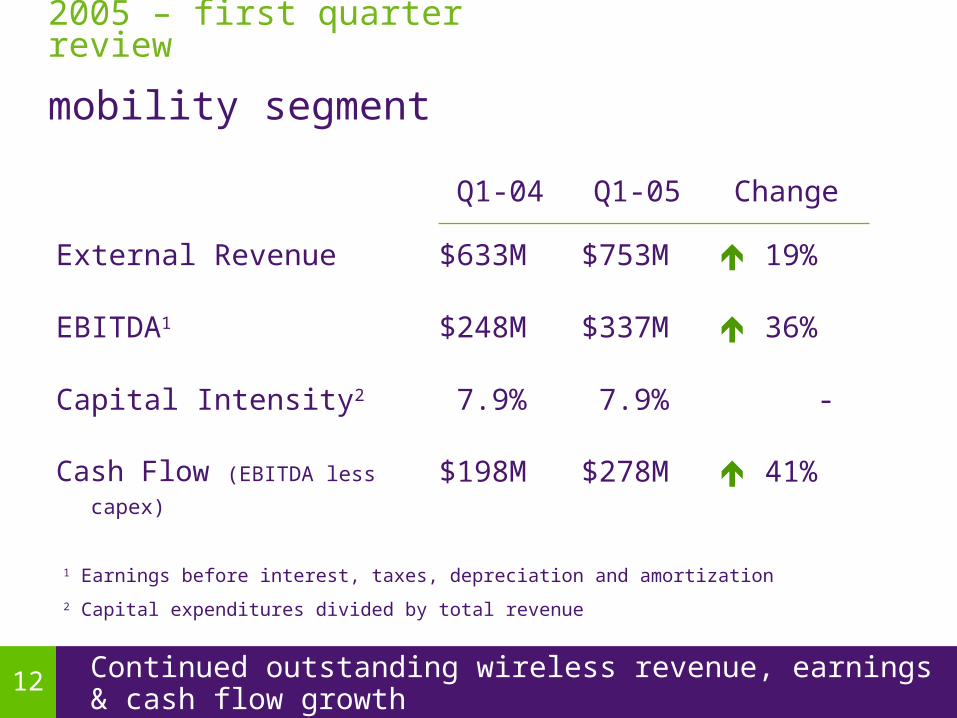

12Continued outstanding wireless revenue, earnings & cash flow growth

41%$278M$198MCash Flow (EBITDA less capex)

-7.9%7.9%Capital Intensity2

36%$337M$248MEBITDA1

19%$753M$633MExternal Revenue

Change Q1-05 Q1-04

1 Earnings before interest, taxes, depreciation and amortization

2 Capital expenditures divided by total revenue

2005 – first quarter review

mobility segment

13 Strong subscriber economics lead the Canadian industry

4 bps1.45%1.49%Churn

1.8%$58$57Avg. Revenue Per Unit (ARPU)

5.4%8076Net Adds (thousands)

15%4.0M3.5MSubscribers

ChangeQ1-05Q1-04

2005 – first quarter review

mobility segment

14 TELUS Mobility generates nearly half of consolidated cash flow

Revenue EBITDA

Mobility 39%

Communications 61%

Cash Flow

Mobility 38%

Communications 62%

Mobility 48%

Communications 52%

2005 – first quarter review

mobility’s share of TELUS corporate

15 Positive revisions to guidance

current2previous1

Communications

Revenue $ 4.7 to 4.75B $ 4.75 to 4.8B

EBITDA3 $1.85 to 1.9B $1.875 to 1.925B

Capex $ 950M to 1B approx. $ 1B

Mobility

EBITDA $ 1.35 to 1.4B $ 1.375 to 1.4B

Capex $ 350 to 400M approx. $ 400M

Wireless net adds 425 to 475K 475 to 525K

1 Provided on December 17, 2004 2 Updated May 4, 20053 Includes ~$100M in restructuring & workforce reduction costs

2005 guidance changes made today

16 Positive revisions to consolidated guidance

current2previous1

Consolidated

Revenue $ 7.9 to 8.0B $ 7.95 to 8.05B

EBITDA3 $ 3.2 to 3.3B $ 3.25 to 3.325B

EPS $ 1.65 to 1.85 $ 1.85 to 2.05

Capex $ 1.3 to 1.4B approx. $ 1.4B

Free cash flow $ 1.2 to 1.3B $ 1.25 to 1.35B

1 Provided on December 17, 2004 2 Updated May 4, 20053 Includes ~$100M in restructuring & workforce reduction costs

2005 guidance changes made today

17

$7.95 to 8.05B

$3.25 to 3.325B

$1.85 to 2.05

approx. $1.4B

$1.25 to 1.35B

Current outlook reflects strong expected growth

5 to 6%

1 2005 Includes ~$100M in restructuring & workforce reduction costs2 Includes $0.21 in 2004 and $0.15 in 2005 guidance for favourable settlement of tax matters Normalized EPS growth would be 24 to 39%

flatFree Cash Flow

6%Capex

17 to 30%EPS2

5 to 8%

annual change

EBITDA1

Revenue

2005E

2005 consolidated guidance summary

18

Renewed bank credit facilities totaling $1.6B$800M five-year term & $800M three-year termWill replace TELUS’ existing $1.6B facilitiesFavourable changes & extended term support

strong liquidity position

Normal Course Issuer Bid for 25.5M sharesRepurchased 4.1M shares in Q1, for a total of 6.3M

shares since inception Dividend declared - $0.20 per share

Represents 33% over last year

Strong financial position enables attractive return of capital to shareholders

2005 highlights

financial highlights

19

2005annual & special meeting

20

the future is friendly

2005first quarter review & conference call

May 5, 2005

Robert McFarlaneEVP & Chief Financial Officer

21 Strong increases in revenue and profitability

12%$273M$310MCapex

139%$0.67$0.28EPS2

19%$856M$721MEBITDA1

9.5%$1.98B$1.80BRevenue

ChangeQ1-05Q1-04

1 Earnings before interest, taxes, depreciation and amortization

financial results

Free Cash Flow3 $443M $567M 28%

3 EBITDA, adding Restructuring and workforce reduction costs, cash interest received and excess of share compensation expense over share compensation payments, subtracting cash interest paid, cash taxes, capital expenditures, and cash restructuring payments

2 Including favourable impacts for tax settlements on EPS of $0.04 in Q1-04 & $0.15 in Q1-05

TELUS consolidated

4

22

15 cent impact on EPS in Q1-05 versus 4 cents in Q1-04

reflects change in tax estimates for available temporary differences, other tax adjustments, and related interest income on settlements

tax normalization

TELUS consolidated

5

23

CDNS

35% of TELUS ILEC local voice revenue regulated

Feb-05, Competitive digital network services (CDNS) decision

Positive consolidated impact of $25M in 2005

unfavourable ILEC impacts effectively offset by mandated price reductions accrued in deferral account

expense reductions for non-ILEC & Mobility

Portable Subsidy

TELUS Quebec benefited from decision on portable subsidy retroactive to 2003 & 2004

positive impact of $10M in 2005

regulatory update

TELUS consolidated

positive regulatory impacts6

24 Normalized quarterly EPS increase of $0.27

EPS continuity

($0.01)- Retroactive impacts of TQ, CDNS regulatory decisions

($0.15)($0.04) Income tax settlement

139%$0.67$0.28EPS reported

ChangeQ1-05Q1-04

EPS normalized $0.24 $0.51 113%

TELUS consolidated

7

25

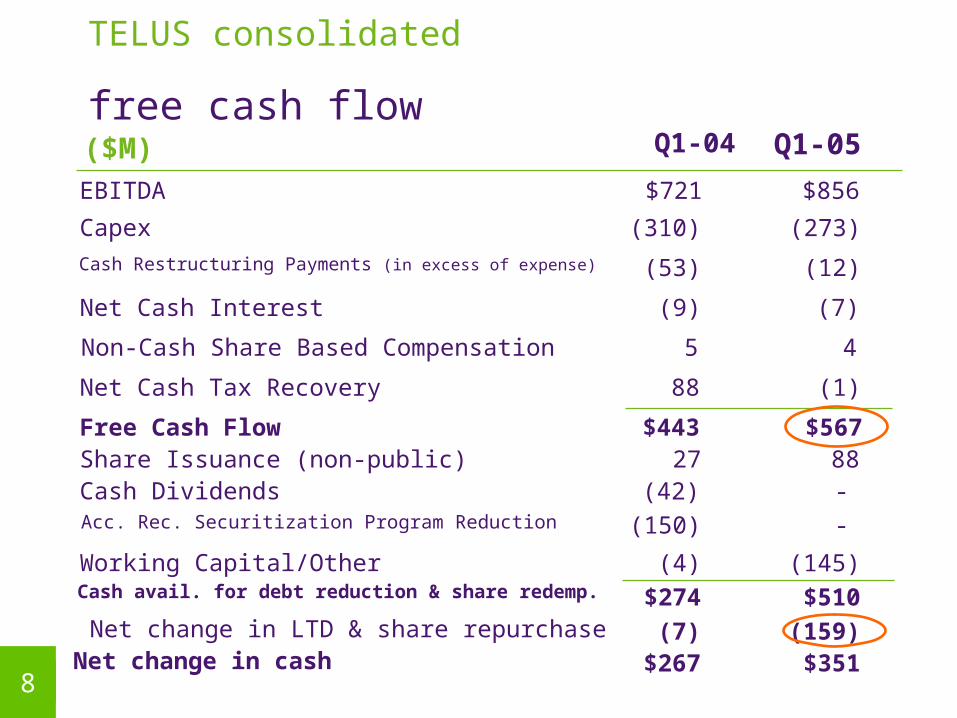

$274

(4)

(42)

$443

88

(9)

(310)

$721

Q1-04

$510

(145)

-

$567

(1)

(7)

(273)

$856

Q1-05

Cash avail. for debt reduction & share redemp.Working Capital/Other

Cash Dividends

Free Cash Flow

Net Cash Tax Recovery

Net Cash Interest

Capex

EBITDA

($M)

(53) (12)Cash Restructuring Payments (in excess of expense)

5 4Non-Cash Share Based Compensation

(150) -Acc. Rec. Securitization Program Reduction

27 88Share Issuance (non-public)

$267 $351Net change in cash(7) (159)Net change in LTD & share repurchase

free cash flow

TELUS consolidated

8

26 Continued strong revenue, earnings & cash flow growth

41%278198Cash Flow (EBITDA less capex)

19%6050Capex

36%337248EBITDA1

19%753633External Revenue

ChangeQ1-05Q1-04

1 Earnings before interest, taxes, depreciation and amortization

($M)

Mobility segment

financial results

9

27

subscriber results

Continued strong postpaid mix

net additions

Q1-04 Q1-05

76K80K

4.0M

total wireless subscribers

postpaid83%

prepaid17%

3.3M

0.7M

Mobility segment

10

28

Source: Company reports

TELUS Mobility Rogers Wireless1BCE Wireless

$57

$44$47

$58

$48$46

Q1-04

Q1-05

1 Pro forma Microcell

TELUS maintaining ~20% premium to competitors

ARPU comparison

Mobility segment

11

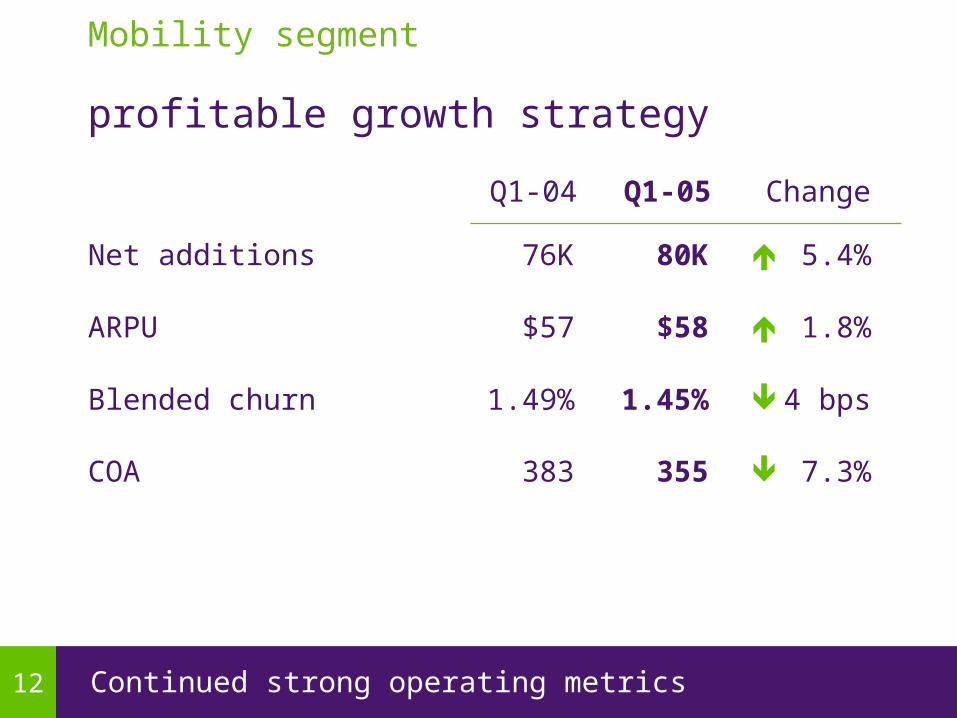

29 Continued strong operating metrics

7.3%355383COA

4 bps1.45%1.49%Blended churn

1.8%$58$57ARPU

5.4%80K76KNet additions

ChangeQ1-05Q1-04

profitable growth strategy

Mobility segment

12

30 Achieving profitable subscriber growth

Mobility segment

TELUS achieving profitable subscriber growth

$936M182K

EBITDA

net adds

TELUSMobility

36%44%

TELUSMobility

$693M

cash flow1

40%

TELUSMobility

1 EBITDA - Capex

Canadian national wireless carriers in Q1-05

44%

TELUSMobility

40%

TELUSMobility

Source: Company reports. Sum of reported results for BCE, Rogers Wireless pro forma Microcell, & TELUS Mobility

13

31 Positive revisions to guidance

2005 guidance summary

1 Provided on December 17, 20042 Updated May 4, 2005

425 to 475KWireless Net Adds

$350 to 400MCapex

updated 2005 guidance2

EBITDA

Revenue

original 2005 targets1

$1.35 to 1.4B

$3.2 to 3.25B

475 to 525K

approx. $400M

$1.375 to 1.4B

no change

Mobility segment

14

32 Strong gains in profitability & cash flow

43%$305M$214MCash Flow (EBITDA less capex)

18%$214M$259MCapex

9.6%$519M$474MEBITDA1

4.4%$1.22B$1.17BExternal Revenue

ChangeQ1-05Q1-04

1 Earnings before interest, taxes, depreciation and amortization

financial results

Communications segment

15

333rd straight quarter of year over year wireline revenue growth driven by data

10%6573Other

11%378340Data

1.4%226230Voice – Long Distance

4.5%553529Voice – Local

ChangeQ1-05Q1-04

External Revenue $1,171 $1,222

($M)

Communications segment

revenue profile

4.4%

16

34 Normalized revenue growth 3.8%, organic revenue growth 2.2%

revenue - normalized

Q1-04 Q1-05 Change

Reported external revenue 1,171 1,222 4.4%

TQ portable subsidy - (7)

External revenue (normalized) 1,171 1,216 3.8%

Acquisitions - (19)

External revenue (organic) 1,171 1,197 2.2%

($M)

Communications segment

17

35 Normalized local revenue flat & data growth of 11%

Q1-04 Q1-05 Change

Local revenue (reported) 529 553 4.5%

TQ portable subsidy - (7)

CDNS - def. account - (18)

Local revenue (normalized) 529 528 0.2%

Data revenue (reported) 340 378 11%

Acquisitions - (19)

CDNS impact - data - 18

Data revenue (normalized) 340 377 11%

($M)

Communications segment

local and data revenue - normalized

18

36

Q1-04 Q2-04 Q3-04 Q4-04 Q1-05

-1.3% -1.4%-1.2% -1.3% -1.1%

Strongest NAL result in 5 quarters despite growing competition

% of network access lines lost, YoY

network access line results

Q4-03

-0.8%

Communications segment

19

37 Normalized Communications EBITDA growth of 5.7%

EBITDA - normalized

Q1-04 Q1-05 Change

Comm. EBITDA (reported) 474 519 9.6%

Restruc. & w. r. costs 16 9

Comm. EBITDA (bef. restruc.) 490 528 7.8%

Regulatory impacts (retroactive)1 - (7)

Comm. EBITDA (normalized) 490 521 6.3%

Acquisitions - (3)

Comm. EBITDA (organic) $490M $518M 5.7%

($M)

Communications segment

1 Retroactive regulatory impacts include TQ portable subsidy and CDNS

20

38

8(3)(14) 4(9)

Q1-04 Q2-04 Q3-04 Q4-04 Q1-05

128145

131156 160

Positive trend with record revenue; 2nd quarter of positive EBITDA benefited in part from non-recurring items

Revenue

EBITDA

non-ILEC revenue & EBITDA ($M)

~$3-4M run rate

Communications segment

21

39

high-speed Internet subscriber growth

High-speed Internet base up 18% in maturing market

high-speed Internet net additions

Q1-04 Q1-05

44K

22K

982K

total Internet subscribers

high-speed 72%

dial-up28%

712K

270K

Communications segment

22

40

Business

Geographic expansion building high quality, recurring revenues in non-ILEC leveraging

IP network & application leadership

$245M long-term contract with Gov’t of B.C.

Consumer

“Future Friendly” home continued high-speed Internet growth launched suite of IP applications

Home Networking, HomeSitterTM launched in 2004 IPTV employee trials continue

Bundling bundling strategy protects legacy revenues

revitalizing wireline growth

Communications segment

23

41 Expected additional restructuring costs of $91M for Q2 to Q4-05

restructuring and workforce reduction costs

Programs

initiated in 2005

Programs prior

to 2005 Total

Beginning period liability - $70.7 $70.7

Restructuring and workforce reduction costs

7.9

1.5

9.4

Cash payments (0.6) (21.1) (21.7)

Total liability $7.3 $51.1 $58.4

($M)

Communications segment

24

42 Positive revisions to guidance

2005 guidance summary

1 Provided on December 17, 20042 Updated May 4, 20053 Includes ~$100M in restructuring & workforce reduction costs

approx. 100,000High-Speed Net Adds

$950M to 1BCapex

updated 2005 guidance2

EBITDA3

Revenue

original 2005 targets1

$1.85 to 1.9B

$4.7 to 4.75B

no change

approx. $1B

$1.875 to 1.925B

$4.75 to 4.8B Non-ILEC Revenue $600 to 650M $625 to 650M

Non-ILEC EBITDA $0 to 10M $15 to 20M

Communications segment

25

43

collective bargaining with TWU resumed, Feb. 16 tabled comprehensive offer to TWU, Apr. 13 declared impasse and delivered notice of lockout measures,

Apr. 18 presented the comprehensive offer to employees, Apr. 21

cash impact of offer would be up to approx. $200M Federal Court of Appeal denied TWU application challenging

TELUS, Apr. 21 CIRB dismissed application by TWU for interim relief, Apr. 25 lock-out measures implemented, Apr. 25 business remains as usual

Negotiations continue

labour relations update

26

44 TELUS has repurchased 25% of shares permitted under NCIB

share buy back updateNo. of Shares

Repurchased

This Quarter

No. of Shares

Repurchased

Since

Inception

Total

Authorized

% of Auth.

Repurchased

Since

Inception

Common 2.1M 2.8M 14.0M 20%

Non-Voting 2.0M 3.5M 11.5M 30%

Total 4.1M 6.3M 25.5M 25%

Total cost $158M $236M

27

45

Effective May 4, 2005, TELUS entered into new credit facilities totaling $1.6 billion $800M five-year revolving term expiring May 2010$800M three-year revolving term expiring May 2008Facilities mature subsequent to 06/07 debt

maturities Will replace TELUS’ existing $1.6B committed facilities Favourable changes to pricing & extended terms

reinforce strong liquidity position

Renewal of credit facilities reflect strong financial position

renewed bank credit facilities

28

46 Positive changes reflect Q1 momentum and tax settlement

2005 consolidated guidance summary

1 Provided on December 17, 20042 Updated May 4, 20053 Includes ~$100M in restructuring & workforce reduction costs4 Updated guidance includes $0.15 in 2005 for favourable settlement of tax matters

$1.2 to $1.3BFree Cash Flow

$1.3 to $1.4BCapex

$1.65 to $1.85EPS4

updated 2005 guidance2

EBITDA3

Revenue

original 2005 targets1

$3.2 to $3.3B

$7.9 to $8.0 B

$1.25 to $1.35B

approx. $1.4B

$1.85 to $2.05

$3.25 to $3.325B

$7.95 to $8.05B

29

47

2005first quarter review

questions?