WINTER FEEDING OF BEEF COWS By Tom Hoagland University of Connecticut.

Upload

bertram-johnstonCategory

view

212download

0

1

The Federal BudgetPast – Present – Uncertain Future

Stanford Institute for Economic Policy Research

G. William Hoagland

March 9, 2012

2

Recession as announced by National Bureau of EconomicResearch

Surplus

Deficit

Trend

Actual Alternative Projections

Source: Congressional Budget Office; The Budget and Economic Outlook: Fiscal Years 2012 to 2022. January 2012.Office of Management and Budget: FY 2013 Budget of the United States. February 2012.

“The Past, Present & Future”

Total Budget Surplus/Deficit

CBO Baseline. Alternative Baseline & The President’s Projections: January 2012 FY 1965 - 2022

22

3

“The Past”Changes in Projections of Surplus Since January 2001

($ in billions)

2001-2011 % of Swing

Surplus Projected in January 2001:

$ 5,610 NA

Legislative Changes:

•Revenues

•Outlays (Afghan/Iraq/Related Activities)

Total

- 2,808

+ 5,712(+ 1,263)

- 8,520

23%

48%(11%)

(71%)

Economic/Technical Changes:

•Revenues

•Outlays

•Total

- 3,412

-83

- 3,329

28%

1%

(29%)

Total Swing

Actual Deficit

$11,849

- $ 6,239

100%NA

Source: Congressional Budget Office; Joint Committee on Taxation

4

“The Future” Budget Outlook FY 2011 – 2017

(In Billions of Dollars – % of GDP)President’s FY 2013 Budget

2011Actual

2012Est

2013Proj →

2014 2015 2016 2017% ∆ annual

2012-2017

Receipts 2,302 2,469 2,902 3,215 3,450 3,680 3,919 + 9.6%

Spending 3,603 3,796 3,803 3,883 4,060 4,329 4,532 + 3.6%

Deficits

% of GDP

1,300

8.7%

1,327

8.5%

901

5.5%

668

3.9%

610

3.4%

649

3.4%

612

3.0%

NA

NA

Public Debt

% GDP

Debt Subject Limit*

% GDP

10,128

68%

14,747

98%

11,578

74%

16,334

104%

12,637

77%

17,532

106%

13,445

78%

18,485

106%

14,198

78%

19,412

105%

14,980

78%

20,379

104%

15,713

77%

21,315

103%

+ 9.1%

+5.4%

Source: Office of Management and Budget, Fiscal Year 2013 Budget of the U.S. Government. February 2012.

Nominal GDP estimated to increase 5.5 % annually 2012-2017: Real GDP estimated to increase 4.3% annually 2012-

2017.

5

Federal Debt Held by the Public Baseline, Alternative Fiscal Scenario, President’s Budget

% of GDP

CBO’s Alternative Fiscal Scenario assumes expiring tax provisions (other than the payroll tax reduction) are extended, the AMT is indexed for inflation after 2011, Medicare’s payment rates for physicians’ services are held constant at their current level, and automatic spending reductions required by the Budget Control Act do not take effect. CBO January 2012. President’s Budget estimates from FY 2013 Federal Budget, OMB, February 2012.

%

President’s BudgetAvg. 2012-22: 77%Avg. 2012-22:

84.4%Avg. 2012-22:

68.6%

62.0%

94.2%

76.5%

72.5%

6

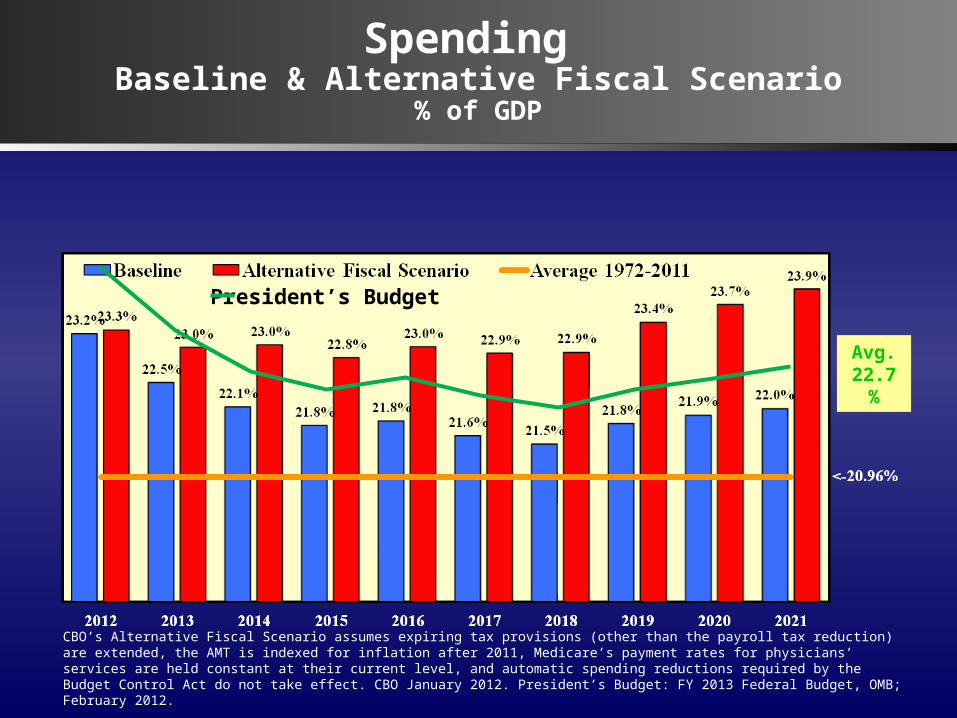

Spending Baseline & Alternative Fiscal Scenario

% of GDP

CBO’s Alternative Fiscal Scenario assumes expiring tax provisions (other than the payroll tax reduction) are extended, the AMT is indexed for inflation after 2011, Medicare’s payment rates for physicians’ services are held constant at their current level, and automatic spending reductions required by the Budget Control Act do not take effect. CBO January 2012. President’s Budget: FY 2013 Federal Budget, OMB; February 2012.

President’s Budget

Avg. 22.7

%

7

Revenues Baseline & Alternative Fiscal Scenario

% of GDP

CBO’s Alternative Fiscal Scenario assumes expiring tax provisions (other than the payroll tax reduction) are extended, the AMT is indexed for inflation after 2011, Medicare’s payment rates for physicians’ services are held constant at their current level, and automatic spending reductions required by the Budget Control Act do not take effect. CBO January 2012. President’s Budget: FY 2013 Federal Budget, OMB; February 2012.

President’s Budget

Avg. 20.8%

8

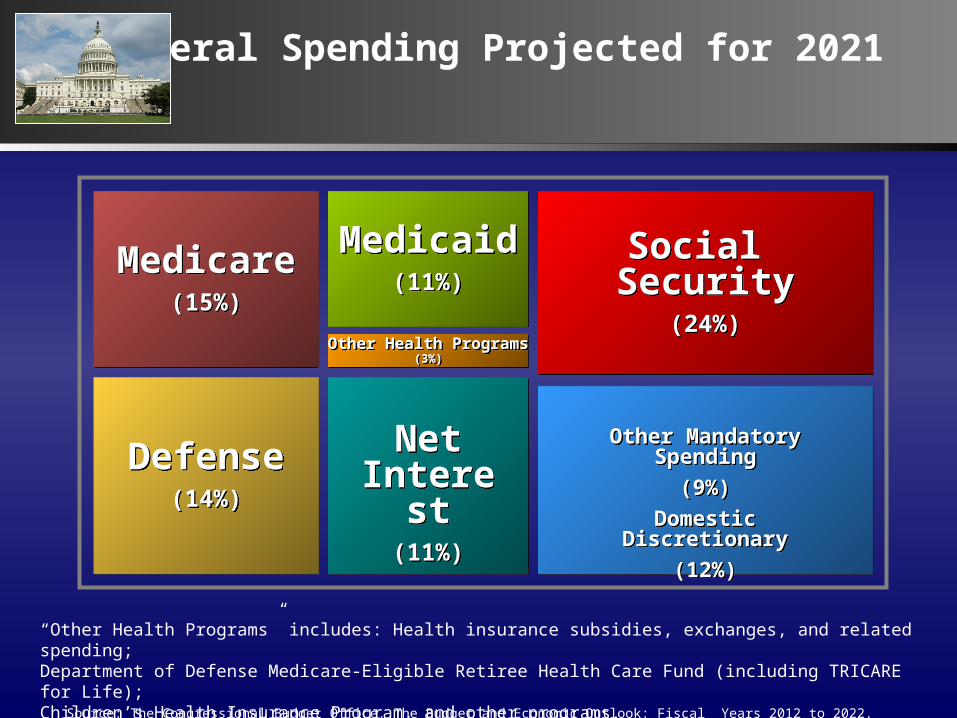

Federal Spending Projected for 2021

“Other Health Programs” includes: Health insurance subsidies, exchanges, and related spending;Department of Defense Medicare-Eligible Retiree Health Care Fund (including TRICARE for Life);Children’s Health Insurance Program, and other programs.

Medicare(15%)

Medicare(15%)

Defense(14%)

Defense(14%)

Medicaid(11%)

Medicaid(11%)

Social Security

(24%)

Social Security

(24%)

Other Mandatory Spending

(9%)

Domestic Discretionary

(12%)

Other Mandatory Spending

(9%)

Domestic Discretionary

(12%)

NetInterest

(11%)

NetInterest

(11%)

Other Health Programs(3%)

Other Health Programs(3%)

Source: The Congressional Budget Office. The Budget and Economic Outlook: Fiscal Years 2012 to 2022. January 2012.

9

Major Components of Federal Expenditures% of GDP 2011-2051

Source: Congressional Budget Office.

Other Mandatory Spending

Healthcare

Social SecurityDiscretionary Spending

0%

2%

4%

6%

8%

10%

12%

14%

2011 2021 2031 2041 2051

% of GDP

10

Alternative Medicare Spending PathsSpending Relative to GDP

8

14

12

10

The unstainable pathwe are on

6

2

0

4

2010 2015 2020 2025 2030 2035 2040 2045 2050 2055 2060 2065 2070 2075 2080

GDP+2%

Goal of:Bowles/Simpson, Rivlin/Ryan, Domenici/Rivlin, Ryan/Wyden,and Obama/CBO

GDP+1%

Medicare Trustees Report Estimate of PPACA

Ryan (House Republican)

GDP+0%

Year

% G

DP

11

Health Benefit Costs as a Share of Wages forFull-Time, Full-Year Workers Receiving

Health Care Benefits through Their Own Employer

Deciles 1980 1990 2000 2009

1 15.4% 30.9% 38.1%

2 9.5 18.7 22.9 30.9

3 8.0 15.3 18.6 25.5

4 7.2 13.3 16.0 22.3

5 6.3 11.6 14.0 19.4

6 5.8 9.9 12.1 16.8

7 5.4 9.2 10.8 14.8

8 4.9 8.2 9.2 12.5

9 4.3 6.9 7.8 10.2

10 3.2 4.9 4.7 6.3

Source: Steven A. Nyce and Sylvester Schieber, “Treating Our Ills and Killing Our Prospects” paper prepared for the Coalition for Affordable Health Care, July 2011.

49.5%

12

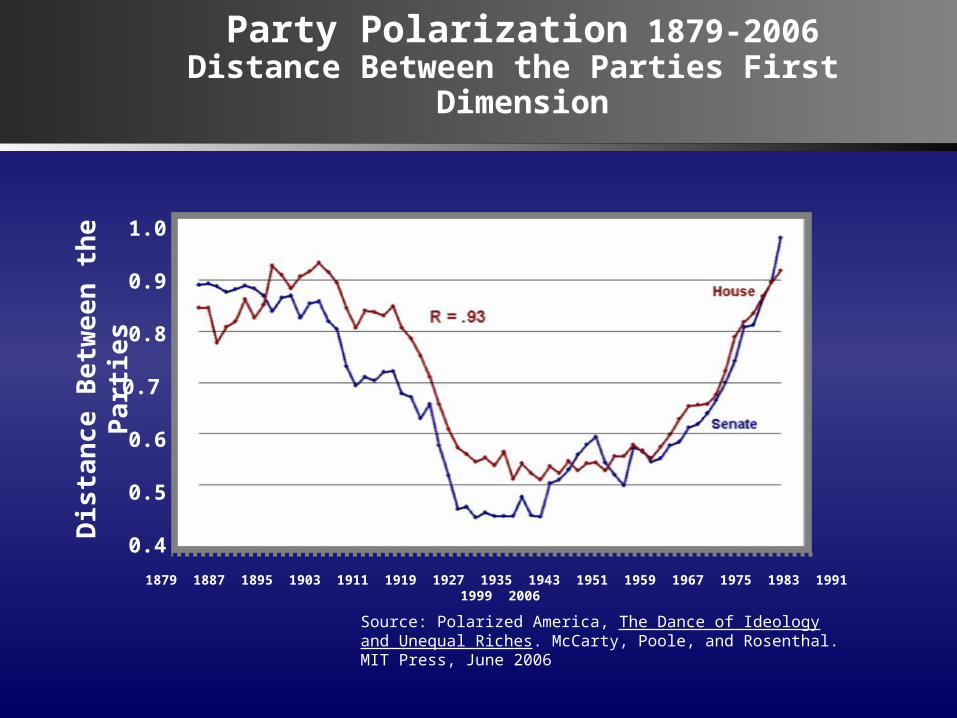

1879 1887 1895 1903 1911 1919 1927 1935 1943 1951 1959 1967 1975 1983 1991 1999 2006

Party Polarization 1879-2006Distance Between the Parties First

Dimension

1.0

0.9

0.8

0.7

0.6

0.5

0.4Dis

tan

ce B

etw

een

th

e

Part

ies

Source: Polarized America, The Dance of Ideology and Unequal Riches. McCarty, Poole, and Rosenthal. MIT Press, June 2006

13

It could be worse.

![Hoagland long c.v. - Woods Hole Oceanographic Institution082316]_237864.pdf · Hoagland P, Kite-Powell HL, Jin D, Solow AR. 2013. Supply-side approaches to the economic valuation](https://static.fdocuments.us/doc/165x107/5ec40dc68f881e5c8033479d/hoagland-long-cv-woods-hole-oceanographic-institution-082316-hoagland-p.jpg)