1 THE AMERICAN ADVERTISING FEDERATION MEDIA INVESTMENT SURVEY 2007.

29

1 THE AMERICAN ADVERTISING FEDERATION MEDIA INVESTMENT SURVEY 2007

-

Upload

samantha-porter -

Category

Documents

-

view

223 -

download

0

Transcript of 1 THE AMERICAN ADVERTISING FEDERATION MEDIA INVESTMENT SURVEY 2007.

1

THE AMERICAN ADVERTISING FEDERATION

MEDIA INVESTMENT SURVEY 2007

2

SURVEY OVERVIEW

During a time of unprecedented change, how are marketers navigating the tumultuous media landscape?

To find out, the AAF Media Investment Survey 2007 polled nearly 1,000 advertising industry leaders across agency, media, client and other sectors.

The study revealed that the increasing rate of change is resulting in a commitment to innovation and dedication to a media mix with the proper balance of traditional and emerging media.

3

SURVEY HIGHLIGHTS

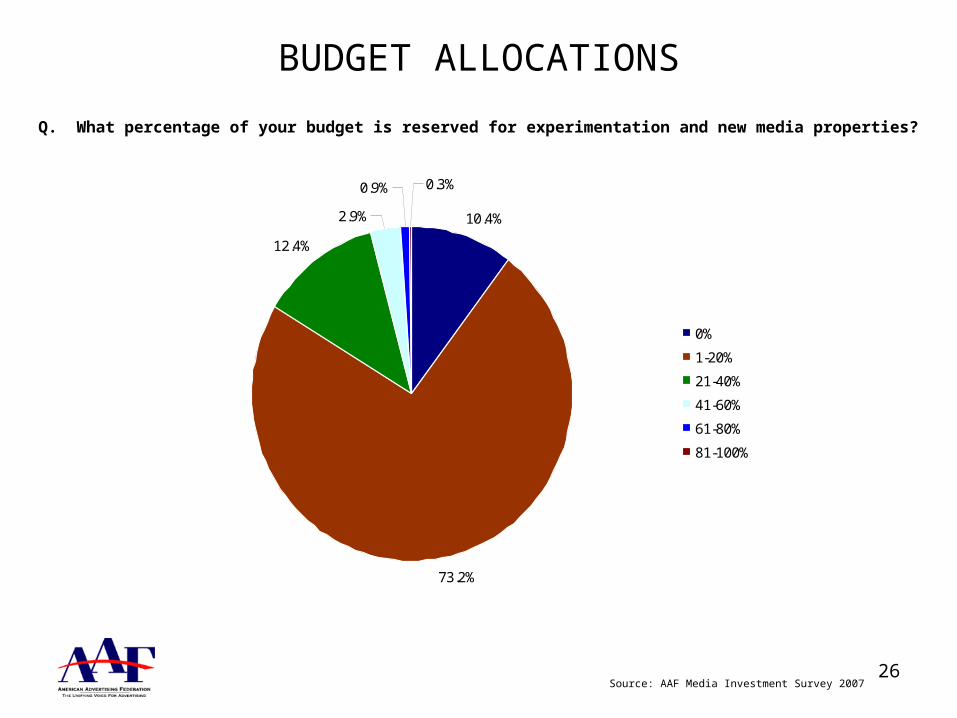

• Three-quarters said that up to 20 percent of their budget is reserved for experimentation and launch vehicles. In addition, 1 in 8 of respondents list 21-40 percent of their budget as reserved for these items.

• When asked about media planning in 2007, respondents ranked “I am open to new ways to use traditional media” highest (78%), with “The right media mix almost always includes a balance of traditional and non-traditional media” (75.5%), and “The search for new properties to grow my brand never stops” (57.7%) right behind.

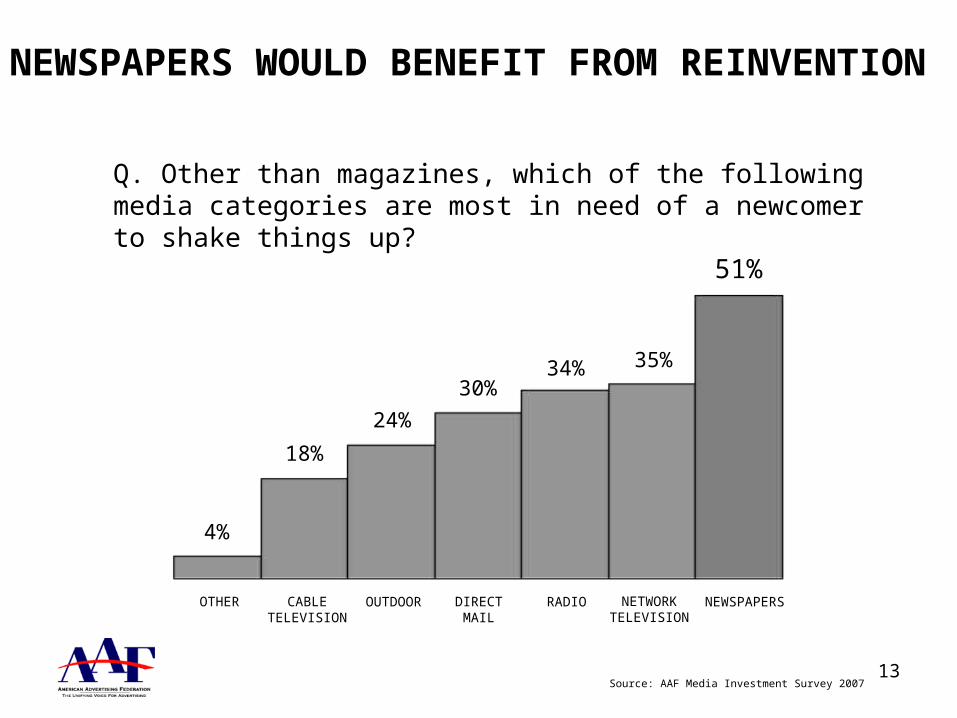

• Newspapers (51.4%) and Network TV (34.5%) are the media categories with the most opportunity for reinvention.

• In the magazine sector, the business category (46%) is seen as “most in need of a newcomer to shake things up.”

Source: AAF Media Investment Survey 2007

4

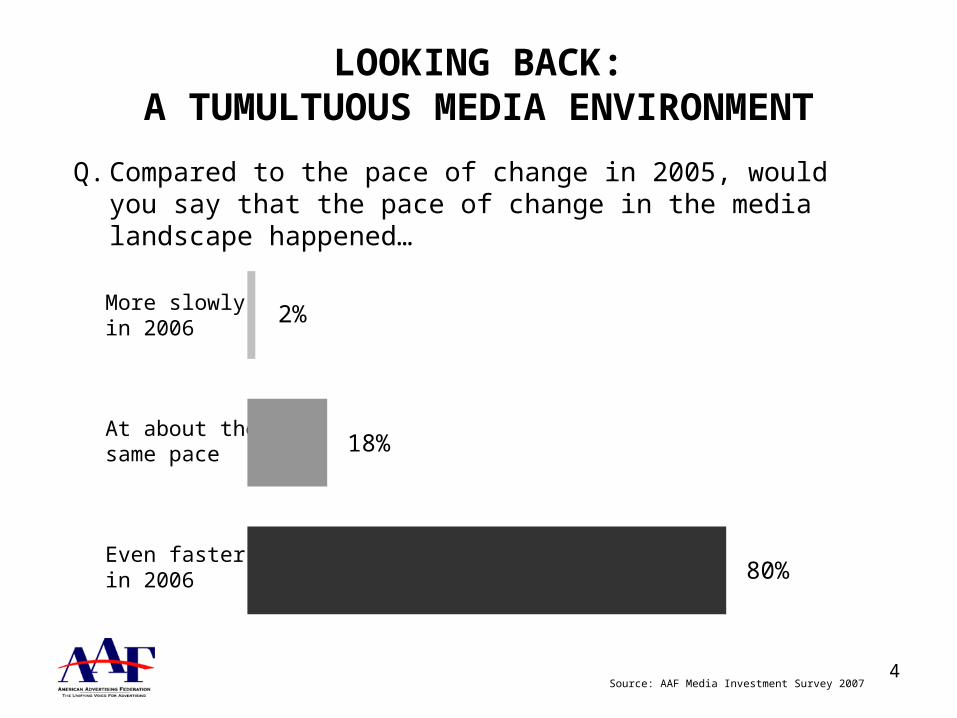

LOOKING BACK:A TUMULTUOUS MEDIA ENVIRONMENT

Q. Compared to the pace of change in 2005, would you say that the pace of change in the media landscape happened…

More slowlyin 2006

At about the same pace

Even fasterin 2006

2%

18%

80%

Source: AAF Media Investment Survey 2007

5

TALE OF TWO WORLDS

1 2 3 4 5

VERYPOORLY

VERYWELL

Source: AAF Media Investment Survey 2007

33% adapt wellto changes

When asked to rate their own performance at managing, adapting to, and getting out in front of significant changes in 2006, 1/3 of marketers give themselves high marks while 1 in 5 admit they have much room for improvement.

19% adapt poorlyto changes

6

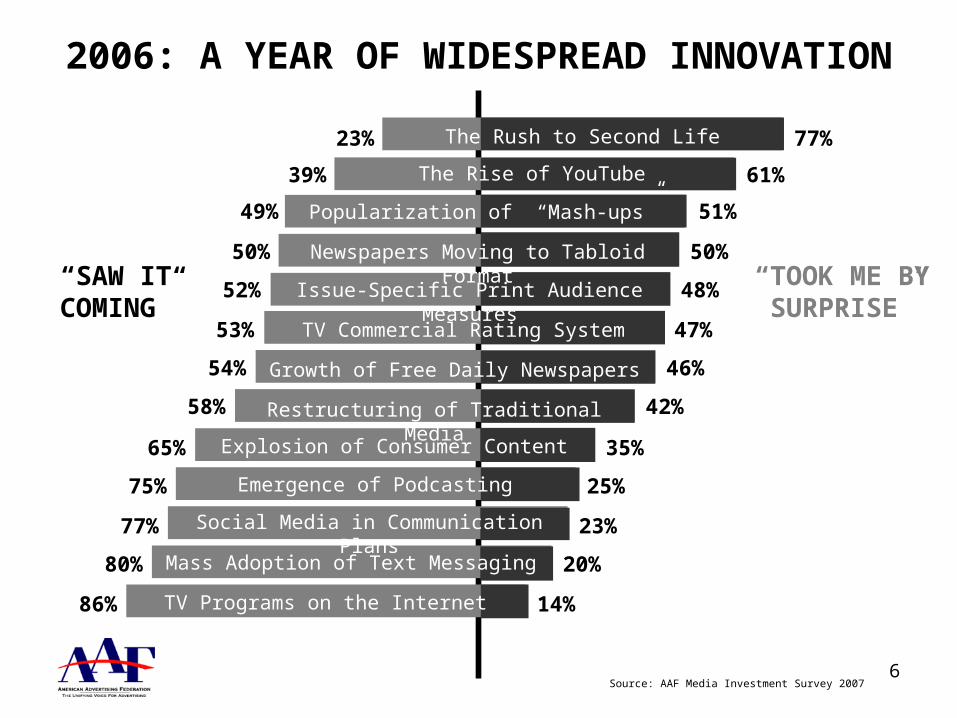

2006: A YEAR OF WIDESPREAD INNOVATION

Source: AAF Media Investment Survey 2007

“SAW IT COMING”

“TOOK ME BY SURPRISE”

77%23%

61%39%

51%49%

50%50%

48%52%

47%53%

46%54%

42%58%

35%65%

25%75%

23%77%

20%80%

14%86%

The Rush to Second Life

The Rise of YouTube

Popularization of “Mash-ups”

Newspapers Moving to Tabloid Format

Issue-Specific Print Audience Measures

TV Commercial Rating System

Growth of Free Daily Newspapers

Restructuring of Traditional Media

Explosion of Consumer Content

Emergence of Podcasting

Social Media in Communication Plans

Mass Adoption of Text Messaging

TV Programs on the Internet

7

LOOKING FORWARDHOW MUCH FASTER CAN IT GET?

Q. Looking forward to 2007, do you expect significant changes in the media landscape to happen…

More slowlythan in 2006

At about the same pace

Even fasterthan in 2006

3%

39%

58%

Source: AAF Media Investment Survey 2007

8

EMBRACING CHANGE IN 2007

52% say…

“I am more likely to anticipate, prepare for, and get out in front of changes in the media landscape in 2007.”

46%

Source: AAF Media Investment Survey 2007

9

CHANGE CHAMPION = INNOVATION INVESTOR

• Change Champions reserve 18% of their media budget for experimentation, while Change Acceptors only set aside 12%.

• Not surprisingly, Change Champions are also more aggressive with their investment strategy, with 1 in 4 budgeting over 20% for new opportunities.

• Conversely, only 6% of Change Avoiders reserve that level of investment for experimentation.

The degree to which an individual embraces change has a significant effect on their innovation investment strategy.

Average % of budget

reserved for innovation

Source: AAF Media Investment Survey 2007

10

MAKING A FINANCIAL COMMITMENT TO INNOVATION

And of the overall respondent base, 73% say…

“Up to 20 percent of my budget is reserved for experimentation and new properties.”

On average, respondents will devote 15% of their overall media spending to innovation.

Source: AAF Media Investment Survey 2007

11

NEW YEAR, FRESH APPROACHES

• 4 in 5 say “I am open to new ways to use traditional media.”

• 4 in 5 say “The right mix almost always includes a balance of traditional and non-traditional media.”

• 3 in 5 say “The search for new properties to grow my brand never stops.”

• The majority say that staid media categories are in need of innovation if they are to remain competitive….

Source: AAF Media Investment Survey 2007

When asked about their approaches to media planning in 2007…

12

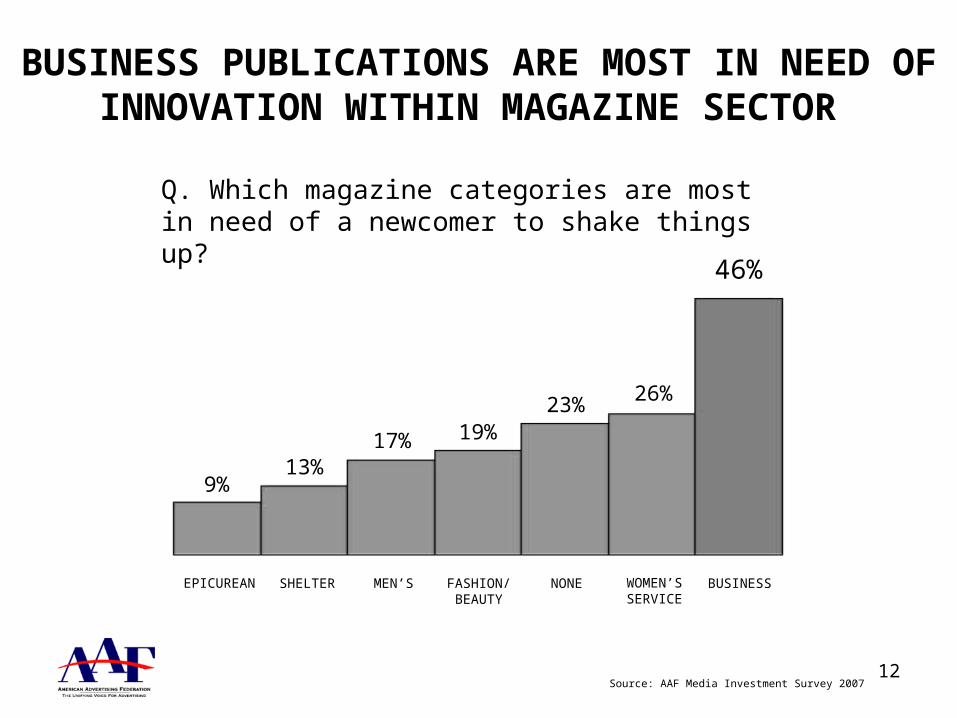

BUSINESS PUBLICATIONS ARE MOST IN NEED OF INNOVATION WITHIN MAGAZINE SECTOR

9%13%

17% 19%23% 26%

46%

Q. Which magazine categories are most in need of a newcomer to shake things up?

Source: AAF Media Investment Survey 2007

EPICUREAN SHELTER MEN’S FASHION/BEAUTY

NONE WOMEN’S SERVICE

BUSINESS

13

NEWSPAPERS WOULD BENEFIT FROM REINVENTION

4%

18%

24%

30%34% 35%

51%

Q. Other than magazines, which of the following media categories are most in need of a newcomer to shake things up?

Source: AAF Media Investment Survey 2007

OTHER CABLETELEVISION

OUTDOOR DIRECTMAIL

RADIO NETWORKTELEVISION

NEWSPAPERS

14

APPENDIX

15

38.1%

26.9%

13.6%

12.6%

4.3%3.7% 0.8%

Agency

Media

Advertiser/client

Other (specify)

Supplier

Academia

Club membership

Q. Please indicate the industry sector in which you work.

RESPONDENT INDUSTRIES

16

5.7%

7.4%

8.5%

8.7%

15.1%

17.6%

18.0%

19.1%

Q. What is your title?

Account Exec/Coordinator

Vice President

Other

Manager

Owner

Director

President

Managing Director/Partner

RESPONDENT TITLES

17

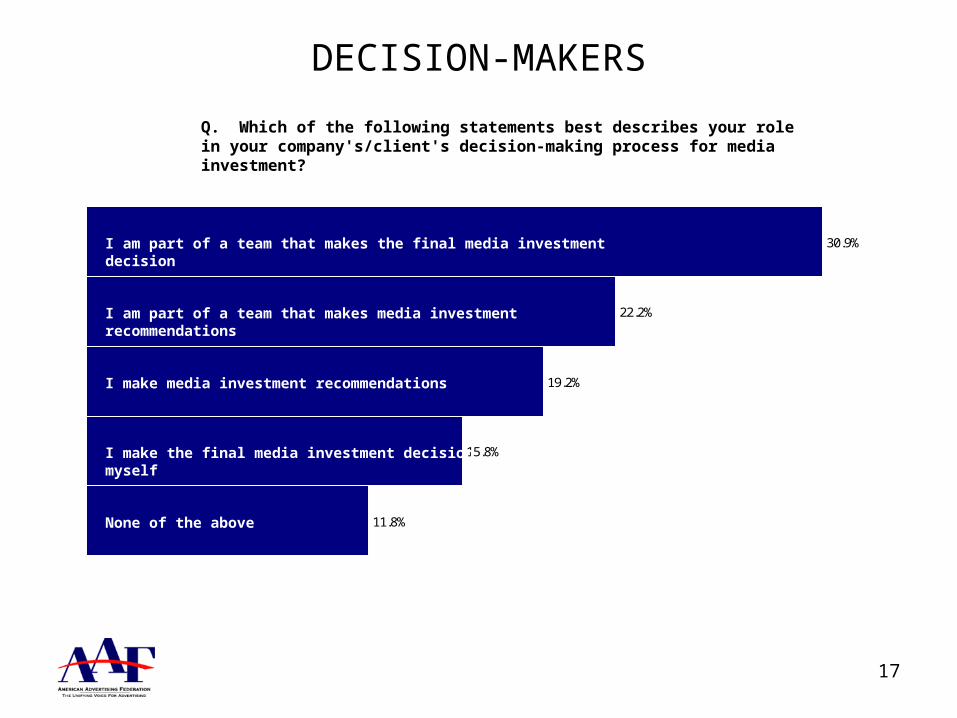

Q. Which of the following statements best describes your role in your company's/client's decision-making process for media investment?

11.8%

15.8%

19.2%

22.2%

30.9%

I make the final media investment decision myself

I make media investment recommendations

I am part of a team that makes media investment recommendations

I am part of a team that makes the final media investment decision

None of the above

DECISION-MAKERS

18

20.4%

39.7%

47.7%

47.9%

48.8%

51.9%

53.7%

57.8%

65.9%

74.8%

75.7%

80.3%

85.9%

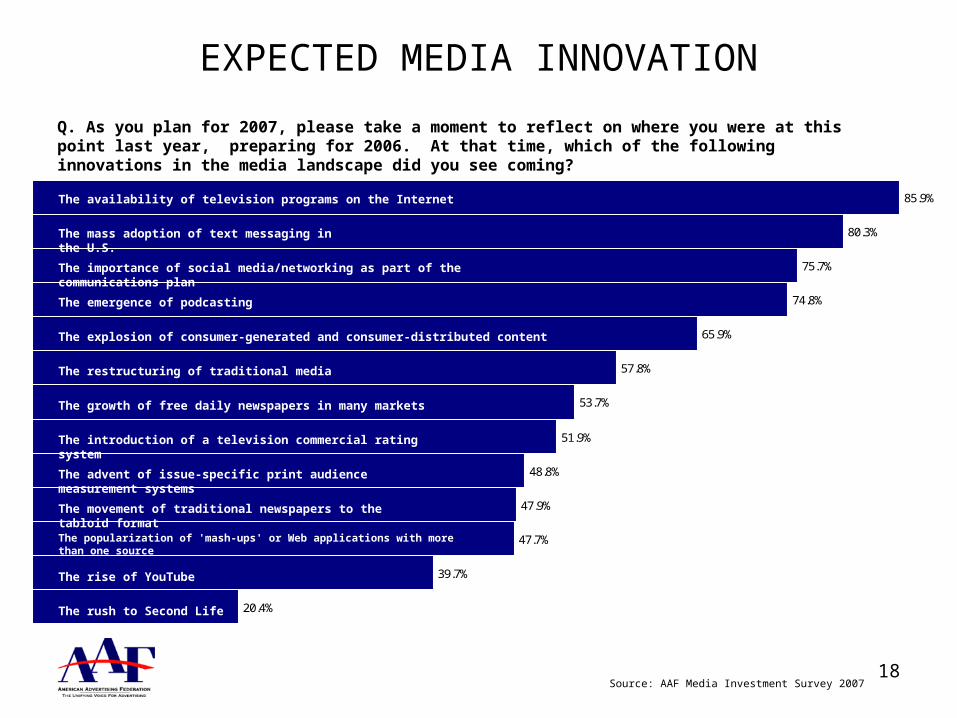

Q. As you plan for 2007, please take a moment to reflect on where you were at this point last year, preparing for 2006. At that time, which of the following innovations in the media landscape did you see coming?

Source: AAF Media Investment Survey 2007

The availability of television programs on the Internet

The mass adoption of text messaging in the U.S.

The importance of social media/networking as part of the communications plan

The emergence of podcasting

The explosion of consumer-generated and consumer-distributed content

The restructuring of traditional media

The growth of free daily newspapers in many markets

The introduction of a television commercial rating system

The advent of issue-specific print audience measurement systems

The movement of traditional newspapers to the tabloid format

The popularization of 'mash-ups' or Web applications with more than one source

The rise of YouTube

The rush to Second Life

EXPECTED MEDIA INNOVATION

19

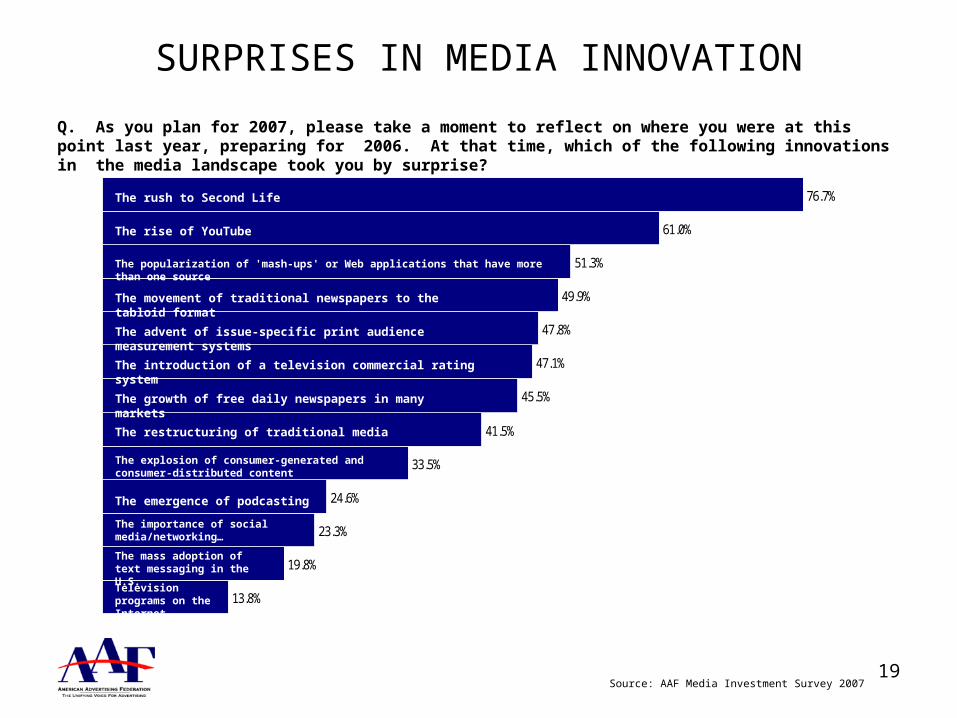

Q. As you plan for 2007, please take a moment to reflect on where you were at this point last year, preparing for 2006. At that time, which of the following innovations in the media landscape took you by surprise?

Source: AAF Media Investment Survey 2007

13.8%

19.8%

23.3%

24.6%

33.5%

41.5%

45.5%

47.1%

47.8%

49.9%

51.3%

61.0%

76.7%

The importance of social media/networking…

The emergence of podcasting

The explosion of consumer-generated and consumer-distributed content

The restructuring of traditional media

The growth of free daily newspapers in many markets

The advent of issue-specific print audience measurement systems

The movement of traditional newspapers to the tabloid format

The popularization of 'mash-ups' or Web applications that have more than one source

The rise of YouTube

The rush to Second Life

Television programs on the Internet

The mass adoption of text messaging in the U.S.

The introduction of a television commercial rating system

SURPRISES IN MEDIA INNOVATION

20Source: AAF Media Investment Survey 2007

79.9%

18.5%

1.6%

Even faster in 2006At about the same pace in 2006 as in 2005More slowly in 2006 than in 2005

Q. Compared to the pace of change in 2005, would you say that the pace of change in the media landscape happened…

2006 PACE OF CHANGE

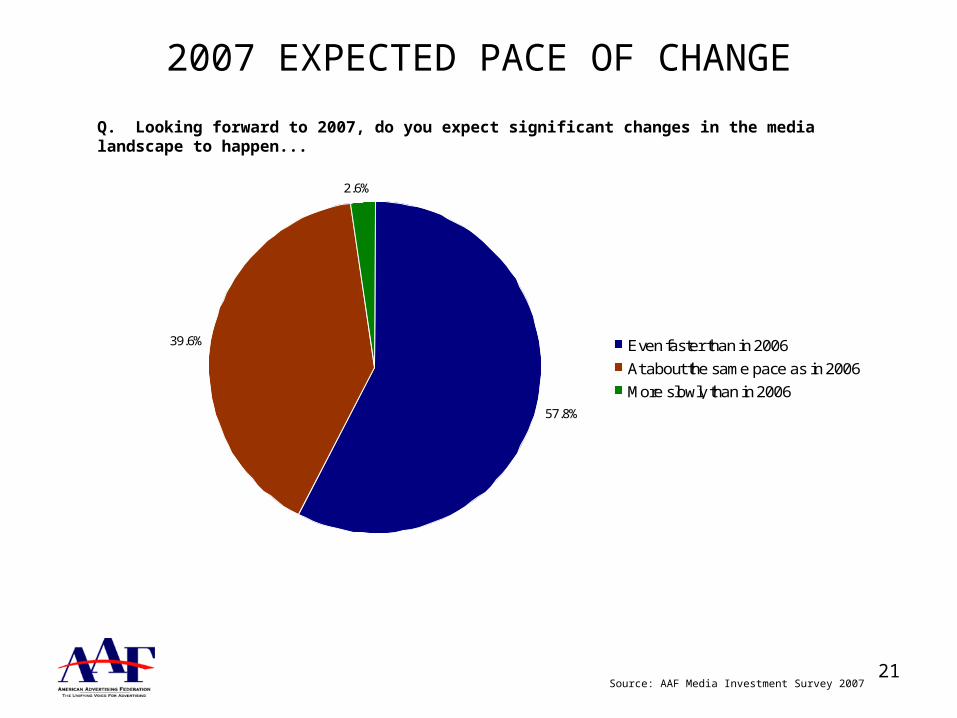

21

Q. Looking forward to 2007, do you expect significant changes in the media landscape to happen...

Source: AAF Media Investment Survey 2007

57.8%

39.6%

2.6%

Even faster than in 2006

At about the same pace as in 2006

More slowly than in 2006

2007 EXPECTED PACE OF CHANGE

22

Q. On a scale of 1 to 5 with 1 meaning 'very poorly' and 5 meaning 'very well,' please rate your own performance at managing, adapting to, and getting out in front of significant changes in 2006.

Source: AAF Media Investment Survey 2007

3.7%

14.8%

48.0%

28.3%

5.3%5

4

3

2

1

2007 EXPECTED PACE OF CHANGE

23

Q. Given your experience with managing the pace of change in 2006, are you more or less likely to anticipate, prepare for, and get out in front of changes in the media landscape in 2007?

Source: AAF Media Investment Survey 2007

51.5%46.2%

2.3%

More likely

About the same

Less likely

MANAGING MEDIA CHANGES IN 2007

24

3.0%

21.9%

26.6%

31.4%

31.7%

38.5%

43.3%

57.7%

75.5%

78.0%

Q. Given the current media climate and your expectations for 2007, please indicate which of the following describe your approach to media planning in the coming year.

Source: AAF Media Investment Survey 2007; *None of the above

*

The tumultuous nature of the media climate requires the assumption of more risk in order to reap the big rewards and avoid +missing the boat

I am willing to spend more and/or assume more risk to reach word-of-mouth generators

Partnering with a new media launch that has a significant +buzz+ factor mitigates some of the risk associated with new media launches

Partnering with innovative media brands is an important way to convey the image of my brand as fresh and innovative

The search for new media properties to grow my brand never stops

The right media mix almost always includes a balance of traditional and non-traditional media

I am always open to new ways to use traditional media

The rush to Second Life

Partnering with new media launches is an important way to convey the image of my brand as influential and ahead of the curve

I am willing to spend more and/or assume more risk to reach early adopters

2007 APPROACH TO MEDIA PLANNING

25

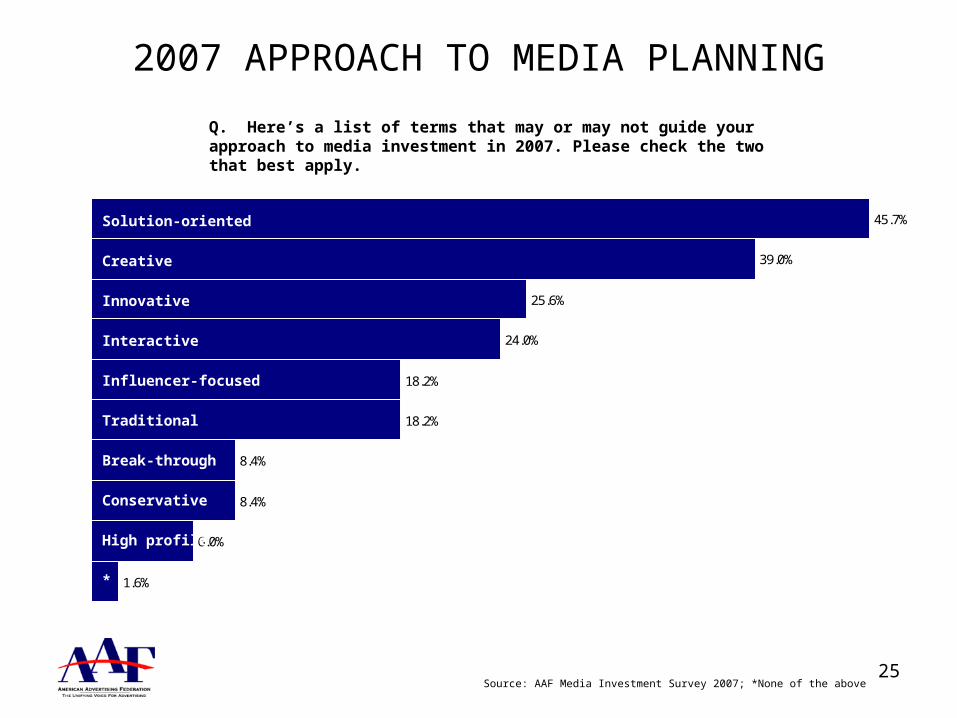

Q. Here’s a list of terms that may or may not guide your approach to media investment in 2007. Please check the two that best apply.

Source: AAF Media Investment Survey 2007; *None of the above

1.6%

6.0%

8.4%

8.4%

18.2%

18.2%

24.0%

25.6%

39.0%

45.7%

*

Conservative

Break-through

Traditional

Interactive

Innovative

Creative

Solution-oriented

Influencer-focused

High profile

2007 APPROACH TO MEDIA PLANNING

26

Q. What percentage of your budget is reserved for experimentation and new media properties?

Source: AAF Media Investment Survey 2007

10.4%

73.2%

12.4%

2.9%

0.9% 0.3%

0%

1-20%

21-40%

41-60%

61-80%

81-100%

BUDGET ALLOCATIONS

27

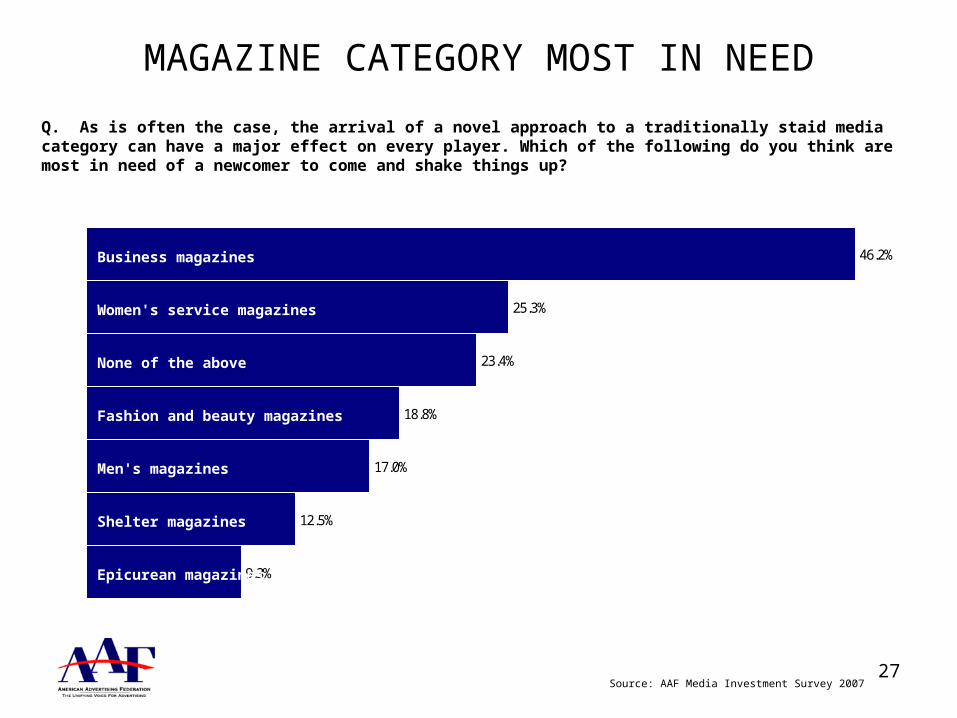

Q. As is often the case, the arrival of a novel approach to a traditionally staid media category can have a major effect on every player. Which of the following do you think are most in need of a newcomer to come and shake things up?

Source: AAF Media Investment Survey 2007

9.3%

12.5%

17.0%

18.8%

23.4%

25.3%

46.2%

Epicurean magazines

Shelter magazines

Fashion and beauty magazines

None of the above

Women's service magazines

Business magazines

Men's magazines

MAGAZINE CATEGORY MOST IN NEED

28

Q. Beyond magazines, which of the following media categories do you think are most in need of a newcomer to come and shake things up?

Source: AAF Media Investment Survey 2007

3.5%

18.3%

23.7%

33.8%

34.5%

51.4%

30.2%

Other

Cable television

Direct mail

Radio

Network television

Newspapers

Outdoor

MEDIA MOST IN NEED

29

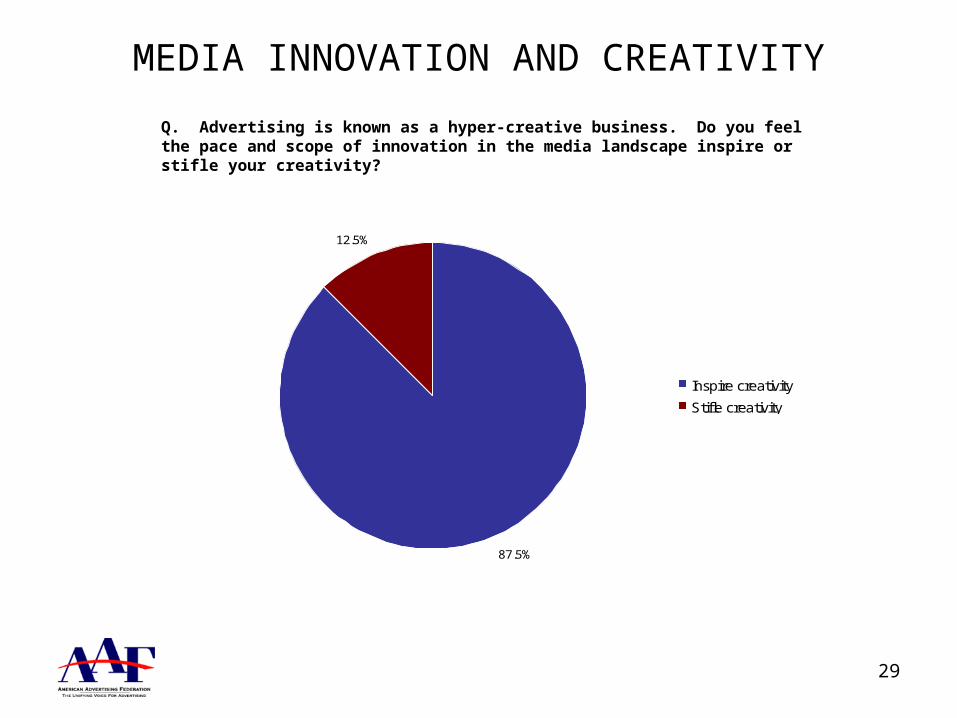

Q. Advertising is known as a hyper-creative business. Do you feel the pace and scope of innovation in the media landscape inspire or stifle your creativity?

87.5%

12.5%

Inspire creativity

Stifle creativity

MEDIA INNOVATION AND CREATIVITY