1 Stocks (Equity) Characteristics and Valuation What is equity? What factors affect stock prices?...

30

1 Stocks (Equity) Characteristics and Valuation What is equity? What factors affect stock prices? How are stock prices determined? How are stock returns determined? What techniques do investors use to value stocks?

-

Upload

shana-riley -

Category

Documents

-

view

216 -

download

1

Transcript of 1 Stocks (Equity) Characteristics and Valuation What is equity? What factors affect stock prices?...

1

Stocks (Equity)Characteristics and Valuation

What is equity?

What factors affect stock prices?

How are stock prices determined?

How are stock returns determined?

What techniques do investors use to value stocks?

2

Basic Types of Stock

Preferred stock: hybrid

Common stock

3

Preferred Stock FeaturesPar valueThe nominal or face value of a stock or bond

DividendsGenerally fixed, like debt; based on the par value

Cumulative dividendsPreferred dividends not paid in previous periods must

be paid before common dividends can be paid

MaturityNo specific maturity date

Priority to assets and earningsPreferred stockholders are paid before common

stockholders

4

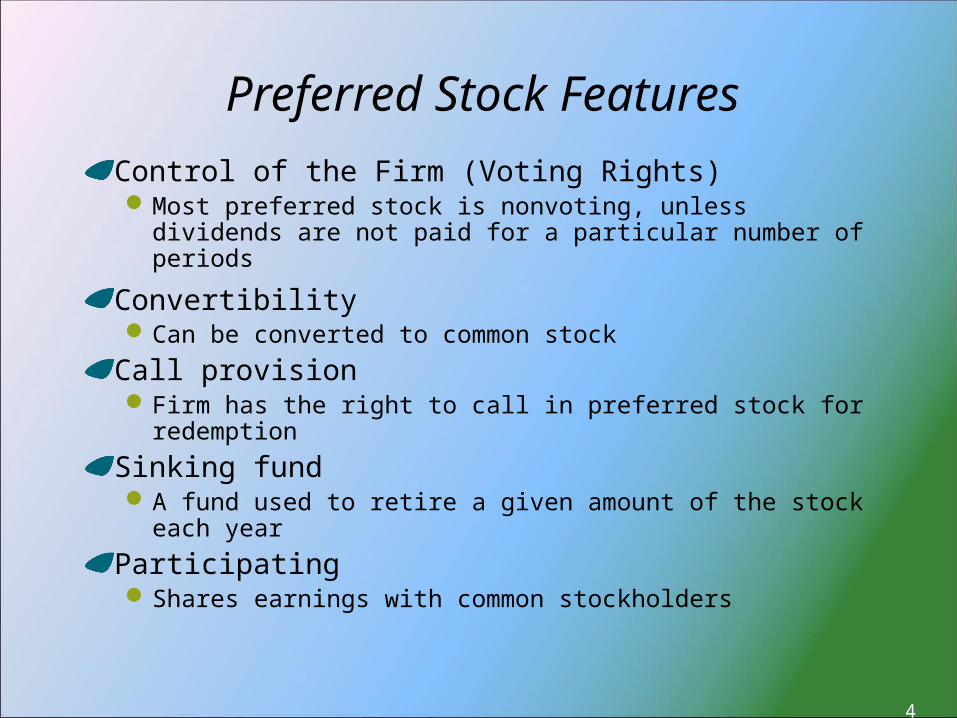

Preferred Stock Features

Control of the Firm (Voting Rights)Most preferred stock is nonvoting, unless dividends

are not paid for a particular number of periods

ConvertibilityCan be converted to common stock

Call provisionFirm has the right to call in preferred stock for

redemption

Sinking fundA fund used to retire a given amount of the stock

each year

ParticipatingShares earnings with common stockholders

5

Common Stock FeaturesPar valueStockholders’ minimum financial obligation

DividendsNo legal obligation to pay dividends

MaturityNo specific maturity date

Priority to assets and earningsReceive distributions last

Preemptive rightRight to buy new issues

Control of the firmVote on board of directors, stockholder proposals,

etc.

6

Types of Common Stock

Classified StockSpecial designations, such as Class A, Class

B, etc., used to meet special needs of the company

Founder’s SharesClassified stock

A class of stock owned by the firm’s founders who have sole voting rights for a particular time period

7

Equity Instruments in International Markets

American Depository ReceiptsCertificates that represent ownership in

stocks of foreign companies

Foreign EquityYankee stock—issued by foreign firm and

traded in the United States

Euro stock—traded outside of “home” country, excluding the United States

8

Stock Valuation

Stock value = Present value of the dividends that the company is expected to pay during its life.

If the stock never pays a dividend—whether a regular dividend or a liquidating dividend—then its value is $0.

9

Stock Valuation—Terms

tD̂ = dividend expected in Period t, such that

1D̂ = the dividend expected in Period 1

D0 = the most recently paid dividend

tP̂ = stock price expected in Period t, such that

1P̂ = the price expected in Period 1P0 = current market price

g = growth rate

rs = the rate of return investors require to purchase the firm’s common stock

^ (hat) = an expected value—that is, a value that is forecasted to occur in the future.

10

Stock ValuationStock ownership entitles the investor to the future cash flows, called dividends, that are paid by the firm 1

…0 2 3 ∞

1D̂ 2D̂ 3D̂ D̂

1D ofPV ˆ

2D ofPV ˆ

3D ofPV ˆ

D ofPV ˆ

...

0t P ValueStock D ofPV ˆˆ

11

Stock Valuation

dividends future expected ofPV P V valueStock 0s ˆ

)r (1

D

)r (1

D

)r (1

D P

s2

s

21

s

10

ˆˆˆˆ

)r (1

D

1tt

s

t

ˆ

rs = required return on stock

12

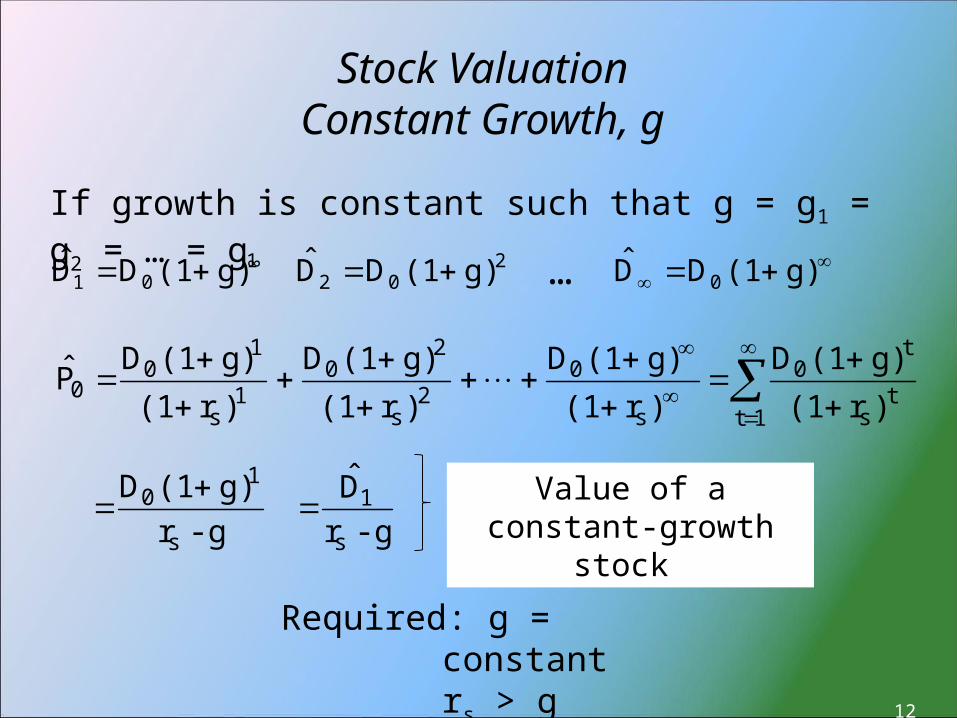

Stock ValuationConstant Growth, g

Required: g = constant rs > g

1t

ˆt

s

t0

s

02

s

20

1s

10

0)r (1

g) (1D

)r (1

g) (1D

)r (1

g) (1D

)r (1

g) (1D P

If growth is constant such that g = g1 = g2 = … = g∞ 1

01 g) (1D D ˆ 202 g) (1D D ˆ …

g) (1D D 0ˆ

g - rg) (1D

s

10

g - r

D

s

1ˆ

Value of a constant-growth stock

13

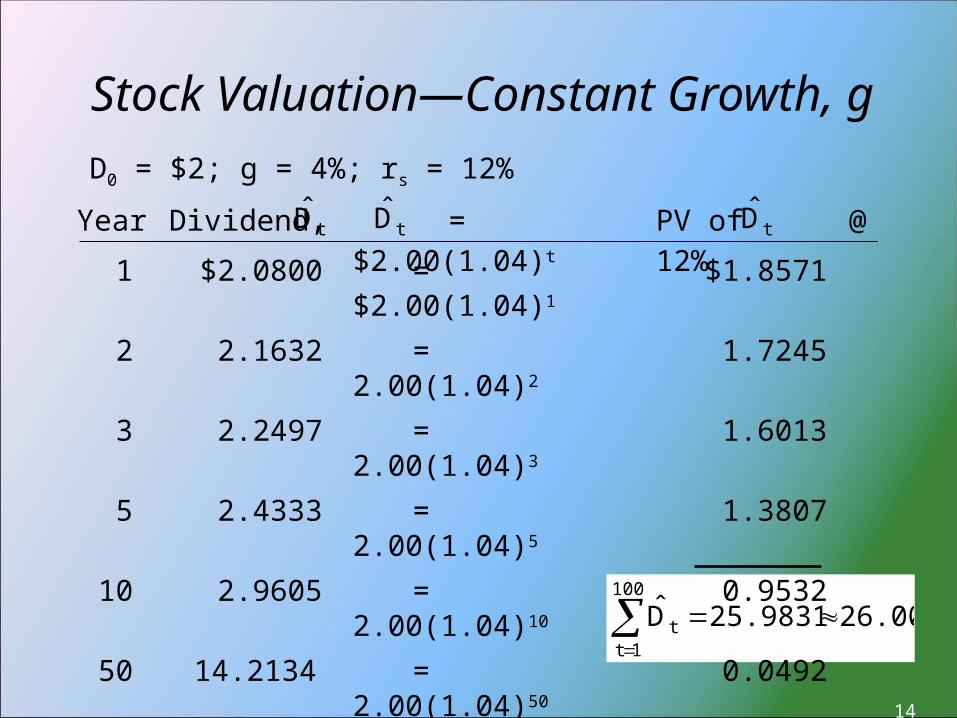

Stock Valuation—Constant Growth, g

The most recent dividend paid (D0) by a firm was $2;

the firm is expected to grow at a constant rate (g) equal to 4 percent; and the required rate of return (rs)

on similar risk investments is 12 percent.

g - rg) (1D

Ps

10

0

ˆ0.04 - 0.12

$2(1.04)

1

$26.00 0.08$2.08

14

Stock Valuation—Constant Growth, gD0 = $2; g = 4%; rs = 12%

26.00 25.9831 D100

1tt

ˆ

PV of @ 12%

= $2.00(1.04)tDividend, Year tD̂tD̂ tD̂

1 $2.0800 = $2.00(1.04)1 $1.8571

2 2.1632 = 2.00(1.04)2 1.7245

3 2.2497 = 2.00(1.04)3 1.6013

5 2.4333 = 2.00(1.04)5 1.3807

10 2.9605 = 2.00(1.04)10

0.9532

50 14.2134 = 2.00(1.04)50

0.0492

100 101.0099 = 2.00(1.04)100

0.0012

15

Stock Valuation—Constant Growth, g=0

)r(1

D

)r(1

D

)r(1

DP

s2

s

21

s

10

ˆˆˆˆ

DDDD 21 ˆˆˆ

g = 0

srD

s

2s

1s

0 )r(1D

)r(1D

)r(1D

P

ˆ

16

Stock Valuation—Constant Growth, g=0

s0 r

D P ˆ

The preferred stock of a company pays a constant dollar dividend equal to $4 per share. The required rate of return on similar risk investments is 8 percent.

$50 0.08$4

Relationship between value and rs

Required Return, rs Stock Value

5.0%

8.0

12.0

Relationship between value and rs

Required Return, rs Stock Value

5.0% $80.00

Relationship between value and rs

Required Return, rs Stock Value

5.0% $80.00

8.0 50.00

Relationship between value and rs

Required Return, rs Stock Value

5.0% $80.00

8.0 50.00

12.0 33.33

17

Stock Valuation—Nonconstant Growth

)r (1

D

)r (1

D

)r (1

D P

s2

s

21

s

10

ˆˆˆˆ

)r (1

)g (1D

)r (1

)g (1D

)r (1

)g (1D

s

12

s

211

s

10ˆˆ

N

s

NN1N2

s

211

s

10

)r (1

P )g (1D

)r (1

)g (1D

)r (1

)g (1D

ˆˆˆ

norms

1N

norms

normNN g - r

D

g - r)g (1D

P

ˆˆ

ˆ gnorm = constant, or normal, growth

NP ˆ

18

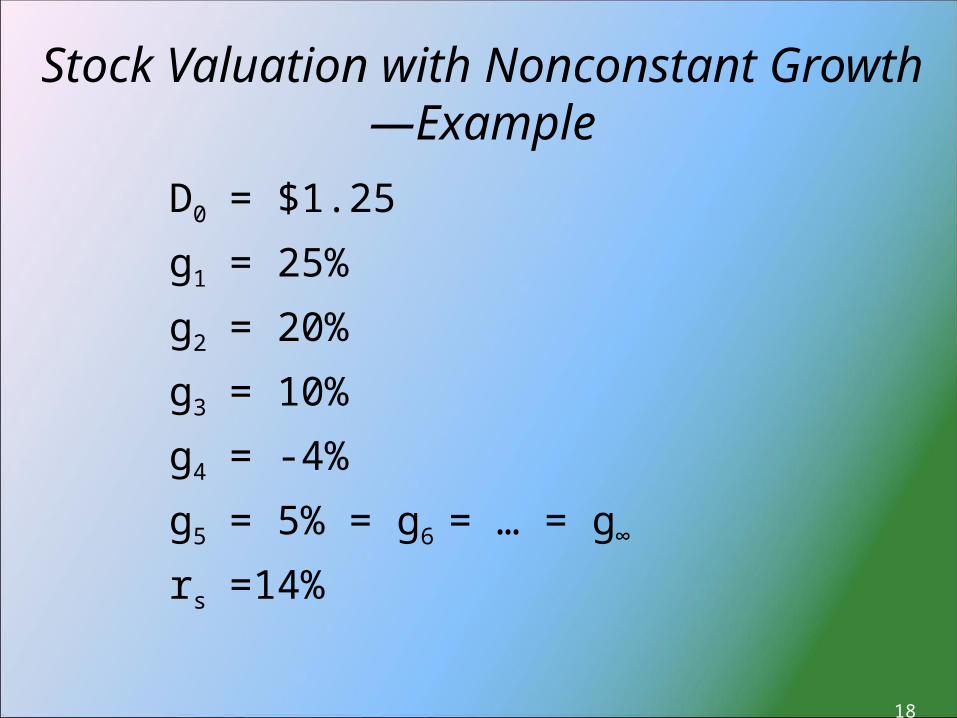

Stock Valuation with Nonconstant Growth—Example

D0 = $1.25

g1 = 25%

g2 = 20%

g3 = 10%

g4 = -4%

g5 = 5% = g6 = … = g∞

rs =14%

19

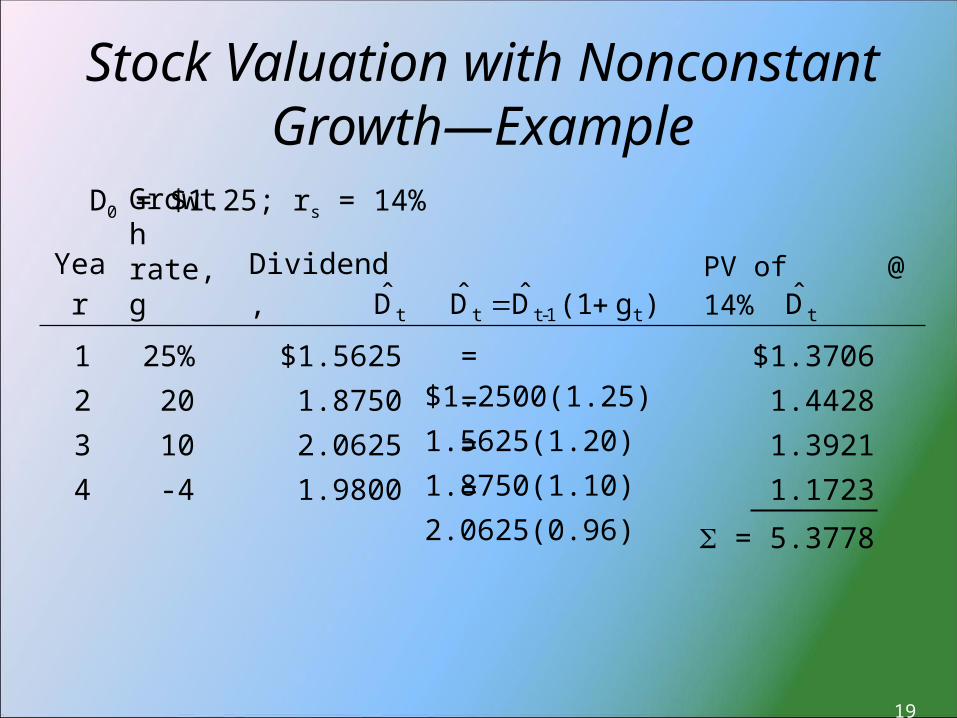

D0 = $1.25; rs = 14%

25%

-4 1.1723= 2.0625(0.96)

1.98004

10 1.3921= 1.8750(1.10)

2.06253

20 1.4428= 1.5625(1.20)

1.87502

$1.3706= $1.2500(1.25)

$1.56251

Growth rate, g

PV of @ 14% Dividend,

Year tD̂tD̂ )g (1D D t1-tt ˆˆ

= 5.3778

Stock Valuation with Nonconstant Growth—Example

20

Because the dividends grow at a constant rate after Year 4, we can apply the constant growth model such that:

ns

n4

ns

54 g - r

)g (1D

g - rD

P

ˆˆ

ˆ

$23.10 0.09

$2.0790

0.05 - 0.14)$1.98(1.05

Stock Valuation with Nonconstant Growth—Example

21

Valuation—Cash Flow Time Line

10 2 3 414%

1.5625 1.8750 2.0625 1.9800

5.3778

tD̂

23.10 4P̂13.6771

19.0549

$19.05P0 ˆ

22

Stock Valuation—Nonconstant Growth

The key to computing the value of a stock that exhibits nonconstant growth is to assume constant growth occurs at some point in the future—it might start in five years, 50 years, or 100 years:Apply the constant growth model to compute the value of

the expected dividends from that point forward. Compute the present value of the stock’s value at the

point where you assume constant growth begins.

Prior to the point where constant growth begins:Compute the dividend for each yearFind the present value of each dividend

Sum the PV results.

23

Stock Return

g P

D̂ r̂

0

1s

Expected rateof return

Expecteddividend

yield= +

Expected growthrate (capital gains yield)

24

Stock Return

P0 = $30.00; D0 = $1.50; g = 6.0%

g P

D r

0

1s

ˆ

ˆˆ 0.06

$30)$1.50(1.06

11.3% 0.06 0.053 0.06 $30

$1.59

g - rD

g - rg) (1D

Ps

1

s

00

ˆˆ

25

Stock Return

In one year, the price of the stock is expected to be:

g - rD

)r (1

D

)r (1

D

)r (1

D P

s

21-

s2

s

31

s

21

ˆˆˆˆˆ

$31.80 0.053

$1.6854

0.06 - 0.113)$1.59(1.06

26

Stock Return

Because the value of the stock is expected to increase from $30.00 to $31.80 during the year,

g P

PP

valueBeginning valueBeginning - valueEnding

yieldgains

Capital

0

01

ˆ

0

1

P

Dyield

Dividend ˆ

6.0% 0.06 $30.00

$30.00 $31.80

5.3% 0.053 $30.00$1.59

rs = 11.3%^

27

Valuation Using P/E Ratios

P/E ratio = Price ÷ EPS = price multiple

“Normal” P/E

Example: A firm’s P/E is normally 8.0x. If its EPS = $7, then the value of its stock should be $56 = $7 x 8

28

Valuation Using EVA

Economic Value Added = EVA

Earnings must be sufficient to pay those who provide funds to the firm; otherwise the value of the firm should decrease.

funds) of cost (Dollarrate)Tax EBIT(1

funds

of Cost

income operating

taxAfterEVA

29

What is equity?Stock/ownership.

What factors affect stock prices? Investors change their expectations about the

returns the firm will generate in the future.

How are stock prices determined?The price is equal to the present value of the

dividends stockholders expect to receive during the company’s life.

Stocks (Equity)Characteristics and Valuation

30

How are stock returns determined?Returns are based on the dividend the

company pays and the change in the market value of the stock during the year

What techniques do investors use to value stocks?P/E Ratio

Economic Value Added (EVA)

Stocks (Equity)Characteristics and Valuation