1 Statement of Cash Flows Revisited Instructor Adnan Shoaib PART III: Decision Tools Lecture 26.

Upload

elijah-fletcherCategory

view

215download

0

1

Special Accounting Special Accounting Problems Related to Problems Related to

LeasesLeases

InstructorInstructorAdnan ShoaibAdnan Shoaib

PART III: Decision ToolsPART III: Decision Tools

Lecture 29Lecture 29

2

1. Identify special features of lease arrangements that cause unique accounting problems.

2. Describe the effect of residual values, guaranteed and unguaranteed, on lease accounting.

3. Describe the lessor’s accounting for sales-type leases.

4. List the disclosure requirements for leases.

Learning ObjectivesLearning ObjectivesLearning ObjectivesLearning Objectives

3

Leasing Environment

Who are players?

Advantages of leasing

Conceptual nature of a lease

Accounting by Lessee

Accounting by Lessor

Special Accounting Problems

Capitalization criteria

Accounting differences

Capital lease method

Operating method

Comparison

Residual values

Sales-type leases

Bargain-purchase option

Initial direct costs

Current versus noncurrent

Disclosure

Unresolved problems

Economics of leasing

Classification

Direct-financing method

Operating method

Accounting for LeasesAccounting for LeasesAccounting for LeasesAccounting for Leases

4

1. Residual values.

2. Sales-type leases (lessor).

3. Bargain-purchase options.

4. Initial direct costs.

5. Current versus non-current classification.

6. Disclosure.

Special Accounting ProblemsSpecial Accounting ProblemsSpecial Accounting ProblemsSpecial Accounting Problems

LO 1 Identify special features of lease arrangements that cause unique accounting problems.

5

Meaning of Residual Value - Estimated fair value of the

leased asset at the end of the lease term.

Guaranteed Residual Value – Lessee agrees to make up

any deficiency below a stated amount that the lessor

realizes in residual value at the end of the lease term.

Residual Values

Special Accounting ProblemsSpecial Accounting ProblemsSpecial Accounting ProblemsSpecial Accounting Problems

LO 1 Identify special features of lease arrangements that cause unique accounting problems.

6

Lease Payments - Lessor may adjust lease payments

because of the increased certainty of recovery of a

guaranteed residual value.

Lessee Accounting for Residual Value - The minimum

lease payments, include the guaranteed residual value but

excludes the unguaranteed residual value.

Residual Values

Special Accounting ProblemsSpecial Accounting ProblemsSpecial Accounting ProblemsSpecial Accounting Problems

LO 1 Identify special features of lease arrangements that cause unique accounting problems.

7

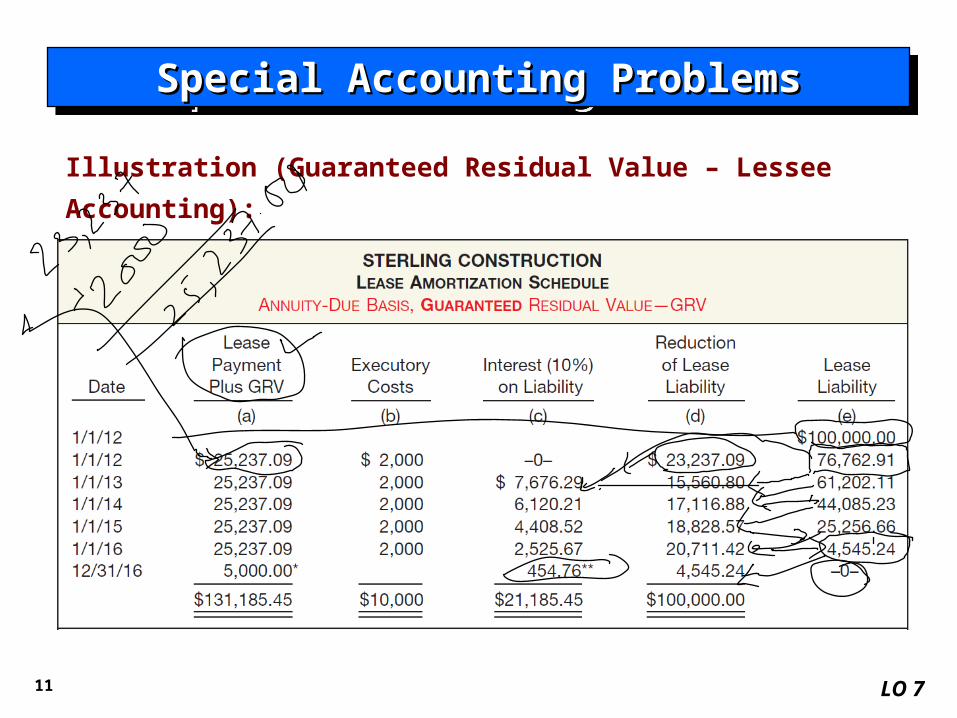

Illustration (Guaranteed Residual Value – Lessee Accounting):

Caterpillar Financial Services Corp. (a subsidiary of Caterpillar) and

Sterling Construction Corp. sign a lease agreement dated January 1,

2012, that calls for Caterpillar to lease a front-end loader to Sterling

beginning January 1, 2012. The terms and provisions of the lease

agreement, and other pertinent data, are as follows.

The term of the lease is five years. The lease agreement is

noncancelable, requiring equal rental payments at the beginning of

each year (annuity-due basis).

The loader has a fair value at the inception of the lease of $100,000,

an estimated economic life of five years, and estimated residual

value of $5,000 at the end of the lease.

Special Accounting ProblemsSpecial Accounting ProblemsSpecial Accounting ProblemsSpecial Accounting Problems

LO 2 Describe the effect of residual values, guaranteed and unguaranteed, on lease accounting.

8

Illustration (Guaranteed Residual Value – Lessee Accounting):

Sterling pays all of the executory costs directly to third parties

except for the property taxes of $2,000 per year, which is included

as part of its annual payments to Caterpillar.

The lease contains no renewal options. The loader reverts to

Caterpillar at the termination of the lease.

Sterling’s incremental borrowing rate is 11 percent per year.

Sterling depreciates on a straight-line basis.

Caterpillar sets the annual rental to earn a rate of return on its

investment of 10 percent per year; Sterling knows this fact.

Special Accounting ProblemsSpecial Accounting ProblemsSpecial Accounting ProblemsSpecial Accounting Problems

LO 2 Describe the effect of residual values, guaranteed and unguaranteed, on lease accounting.

9

Illustration (Guaranteed Residual Value – Lessee Accounting):

Special Accounting ProblemsSpecial Accounting ProblemsSpecial Accounting ProblemsSpecial Accounting Problems

LO 2 Describe the effect of residual values, guaranteed and unguaranteed, on lease accounting.

Caterpillar computation of the lease payments:

10

Illustration (Guaranteed Residual Value – Lessee Accounting):

Special Accounting ProblemsSpecial Accounting ProblemsSpecial Accounting ProblemsSpecial Accounting Problems

LO 2 Describe the effect of residual values, guaranteed and unguaranteed, on lease accounting.

Computation of Lessee’s capitalized amount

11

Illustration (Guaranteed Residual Value – Lessee Accounting):

Special Accounting ProblemsSpecial Accounting ProblemsSpecial Accounting ProblemsSpecial Accounting Problems

LO 7

12

Illustration (Guaranteed Residual Value – Lessee Accounting):

Special Accounting ProblemsSpecial Accounting ProblemsSpecial Accounting ProblemsSpecial Accounting Problems

LO 2 Describe the effect of residual values, guaranteed and unguaranteed, on lease accounting.

At the end of the lease term, before the lessee transfers the asset to

Caterpillar, the lease asset and liability accounts have the following

balances.

13

Assume that Sterling depreciated the leased asset down to its residual

value of $5,000 but that the fair market value of the residual value at

December 31, 2016, was $3,000. Sterling would make the following

journal entry.

Special Accounting ProblemsSpecial Accounting ProblemsSpecial Accounting ProblemsSpecial Accounting Problems

LO 2 Describe the effect of residual values, guaranteed and unguaranteed, on lease accounting.

Loss on Capital Lease 2,000.00

Interest Expense (or Interest Payable) 454.76

Lease Liability 4,545.24

Accumulated Depreciation 95,000.00

Leased Equipment (under capital leases) 100,000.00

Cash 2,000.00

Illustration (Guaranteed Residual Value – Lessee Accounting):

14

Assume the same facts as those above except that the $5,000 residual

value is unguaranteed instead of guaranteed. Caterpillar would compute

the amount of the lease payments as follows:

Special Accounting ProblemsSpecial Accounting ProblemsSpecial Accounting ProblemsSpecial Accounting Problems

LO 2 Describe the effect of residual values, guaranteed and unguaranteed, on lease accounting.

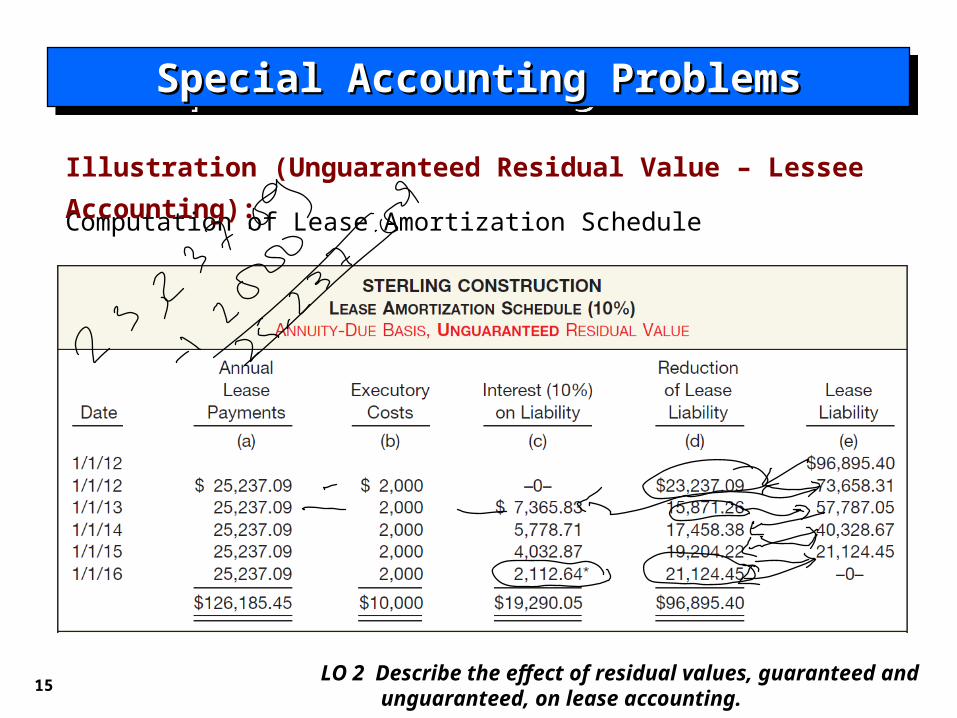

Illustration (Unguaranteed Residual Value – Lessee Accounting):

15

Computation of Lease Amortization Schedule

Special Accounting ProblemsSpecial Accounting ProblemsSpecial Accounting ProblemsSpecial Accounting Problems

LO 2 Describe the effect of residual values, guaranteed and unguaranteed, on lease accounting.

Illustration (Unguaranteed Residual Value – Lessee Accounting):

16

At the end of the lease term, before Sterling transfers the asset to

Caterpillar, the lease asset and liability accounts have the following

balances.

Special Accounting ProblemsSpecial Accounting ProblemsSpecial Accounting ProblemsSpecial Accounting Problems

LO 2 Describe the effect of residual values, guaranteed and unguaranteed, on lease accounting.

Illustration (Unguaranteed Residual Value – Lessee Accounting):

17

Special Accounting ProblemsSpecial Accounting ProblemsSpecial Accounting ProblemsSpecial Accounting Problems

Comparative Entries, Lessee Company

18

Special Accounting ProblemsSpecial Accounting ProblemsSpecial Accounting ProblemsSpecial Accounting Problems

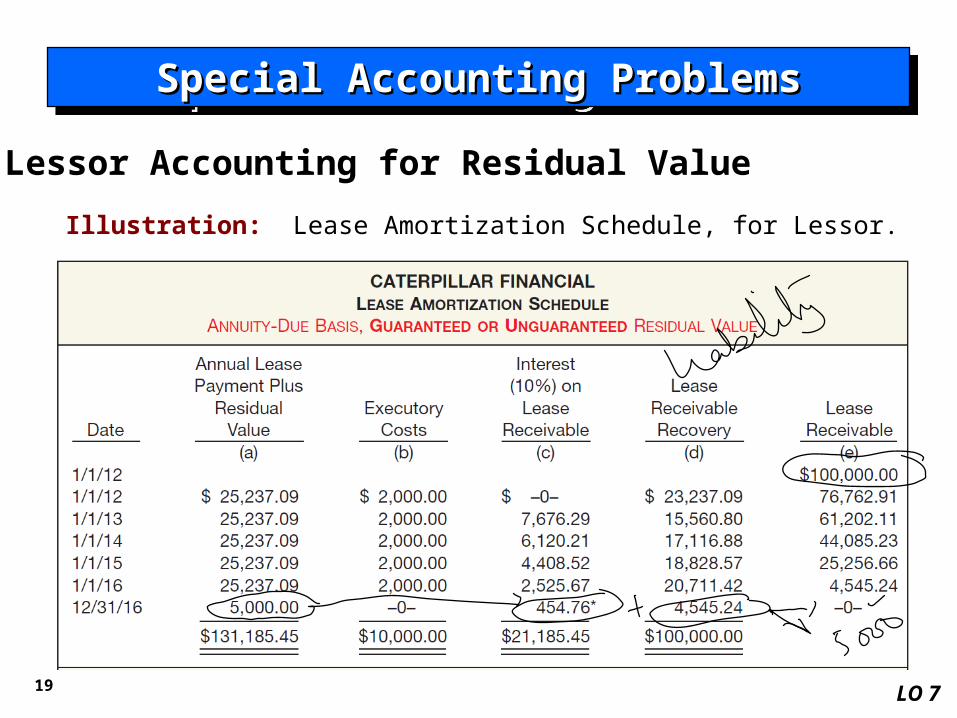

Illustration: Assume a direct-financing lease with a residual value (either

guaranteed or unguaranteed) of $5,000. Caterpillar determines the

payments as follows.

LO 2 Describe the effect of residual values, guaranteed and unguaranteed, on lease accounting.

Lessor Accounting for Residual Value

The lessor works on the assumption that it will realize the residual value at

the end of the lease term whether guaranteed or unguaranteed.

19

Special Accounting ProblemsSpecial Accounting ProblemsSpecial Accounting ProblemsSpecial Accounting Problems

Illustration: Lease Amortization Schedule, for Lessor.

Lessor Accounting for Residual Value

LO 7

20LO 2 Describe the effect of residual values, guaranteed and

unguaranteed, on lease accounting.

Special Accounting ProblemsSpecial Accounting ProblemsSpecial Accounting ProblemsSpecial Accounting Problems

Illustration: Caterpillar would make the following entries for this direct-

financing lease in the first year.

Lessor Accounting for Residual Value

21

Primary difference between a direct-financing lease and

a sales-type lease is the manufacturer’s or dealer’s gross

profit (or loss).

Lessor records the sale price of the asset, the cost of

goods sold and related inventory reduction, and the

lease receivable.

Difference in accounting for guaranteed and

unguaranteed residual values.

Sales-Type Leases (Lessor)

Special Accounting ProblemsSpecial Accounting ProblemsSpecial Accounting ProblemsSpecial Accounting Problems

LO 3 Describe the lessor’s accounting for sales-type leases.

22

Sales-Type Leases (Lessor)

Special Accounting ProblemsSpecial Accounting ProblemsSpecial Accounting ProblemsSpecial Accounting Problems

LO 3 Describe the lessor’s accounting for sales-type leases.

23

Sales-Type Leases (Lessor)

Special Accounting ProblemsSpecial Accounting ProblemsSpecial Accounting ProblemsSpecial Accounting Problems

LO 3 Describe the lessor’s accounting for sales-type leases.

24

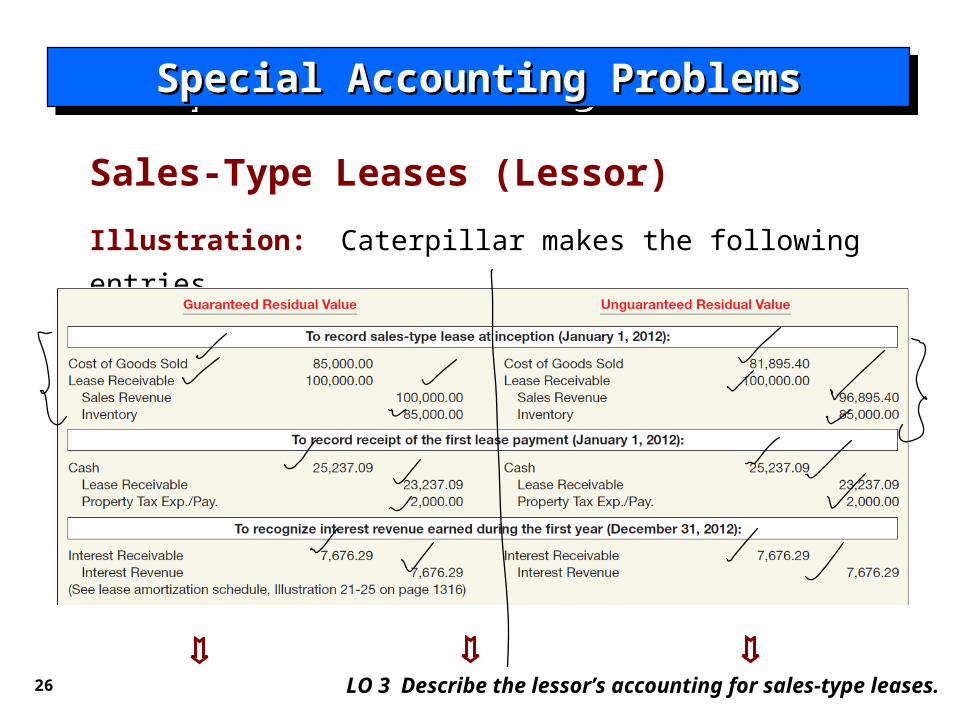

Special Accounting ProblemsSpecial Accounting ProblemsSpecial Accounting ProblemsSpecial Accounting Problems

LO 3 Describe the lessor’s accounting for sales-type leases.

Illustration: To illustrate a sales-type lease with a guaranteed

residual value and with an unguaranteed residual value, assume

the same facts as in the preceding direct-financing lease

situation. The estimated residual value is $5,000 (the present

value of which is $3,104.60), and the leased equipment has an

$85,000 cost to the dealer, Caterpillar. Assume that the fair

market value of the residual value is $3,000 at the end of the

lease term.

Sales-Type Leases (Lessor)

25

Special Accounting ProblemsSpecial Accounting ProblemsSpecial Accounting ProblemsSpecial Accounting Problems

LO 3 Describe the lessor’s accounting for sales-type leases.

Illustration: Computation of Lease Amounts by Caterpillar

Financial—Sales-Type Lease

Sales-Type Leases (Lessor)

26

Special Accounting ProblemsSpecial Accounting ProblemsSpecial Accounting ProblemsSpecial Accounting Problems

LO 3 Describe the lessor’s accounting for sales-type leases.

Illustration: Caterpillar makes the following entries.

Sales-Type Leases (Lessor)

27

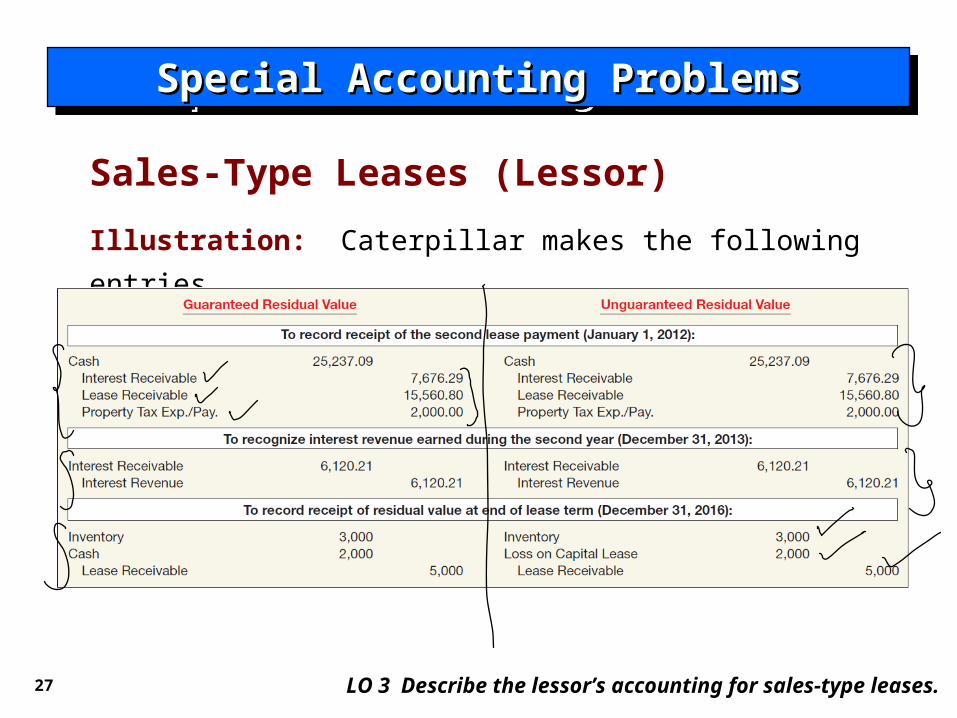

Special Accounting ProblemsSpecial Accounting ProblemsSpecial Accounting ProblemsSpecial Accounting Problems

LO 3 Describe the lessor’s accounting for sales-type leases.

Illustration: Caterpillar makes the following entries.

Sales-Type Leases (Lessor)

28

Present value of the minimum lease payments must

include the present value of the option.

Only difference between the accounting treatment for a

bargain-purchase option and a guaranteed residual value

of identical amounts is in the computation of the annual

depreciation.

Bargain Purchase Option (Lessee)

Special Accounting ProblemsSpecial Accounting ProblemsSpecial Accounting ProblemsSpecial Accounting Problems

LO 3 Describe the lessor’s accounting for sales-type leases.

29

Bargain Purchase OptionsBargain Purchase Optionsand Residual Valueand Residual Value

Bargain Purchase OptionsBargain Purchase Optionsand Residual Valueand Residual Value

A bargain purchase option (BPO) is a provision of some lease contracts that gives the lessee the option of

purchasing the leased property at a bargain price. The expectation that the option price will be paid effectively adds an additional cash flow to the lease for both the

lessee and the lessor. As a result:

LESSEE adds the present value of the BPO price to the present value of periodic rental payments when computing the amount to be recorded a

leased asset and a lease liability.

LESSOR, when computing periodic rental payments, subtracts the present value of the BPO price from the amount to be recovered (fair value) to

determine the amount that must be recovered from the lessee through the periodic rental payments.

LESSEE adds the present value of the BPO price to the present value of periodic rental payments when computing the amount to be recorded a

leased asset and a lease liability.

LESSOR, when computing periodic rental payments, subtracts the present value of the BPO price from the amount to be recovered (fair value) to

determine the amount that must be recovered from the lessee through the periodic rental payments.

30

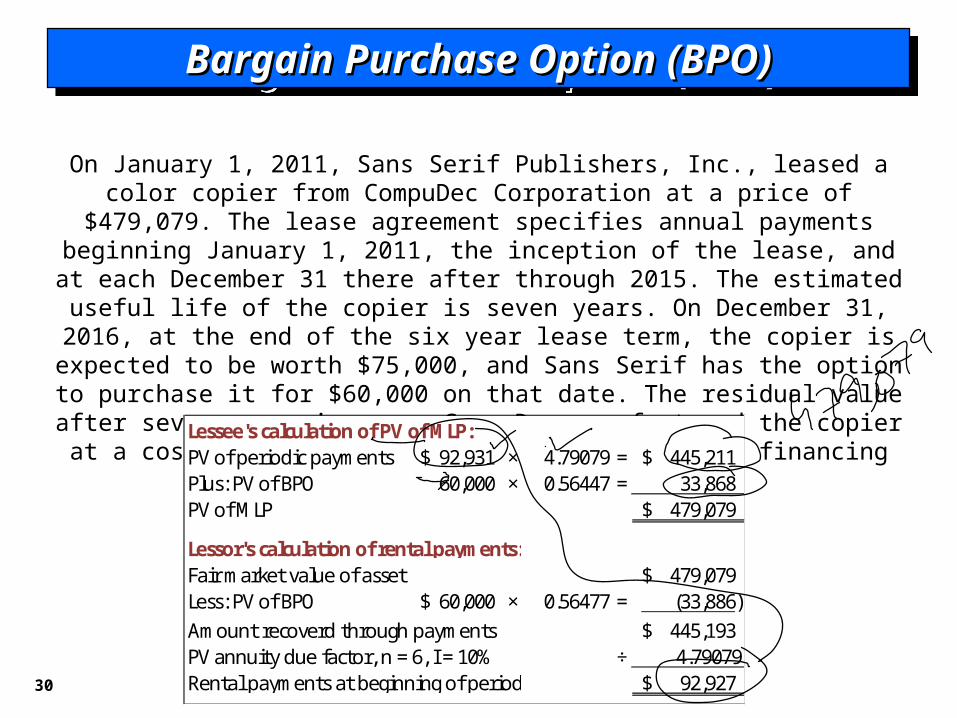

Bargain Purchase Option (BPO)Bargain Purchase Option (BPO)Bargain Purchase Option (BPO)Bargain Purchase Option (BPO)

On January 1, 2011, Sans Serif Publishers, Inc., leased a color copier from CompuDec Corporation at a price of $479,079. The lease agreement specifies annual payments beginning January 1, 2011, the inception of the lease, and at each December 31 there after through 2015. The estimated useful life of the

copier is seven years. On December 31, 2016, at the end of the six year lease term, the copier is expected to be worth $75,000, and Sans Serif has the option to purchase it for $60,000 on that date. The residual value after seven years is zero. CompuDec manufactured the copier at a cost of $300,000 and its interest rate for

financing the transaction is10%.Lessee's calculation of PV of MLP:PV of periodic payments 92,931$ × 4.79079 = 445,211$ Plus: PV of BPO 60,000 × 0.56447 = 33,868 PV of MLP 479,079$

Lessor's calculation of rental payments:Fair market value of asset 479,079$ Less: PV of BPO 60,000$ × 0.56477 = (33,886) Amount recoverd through payments 445,193$ PV annuity due factor, n = 6, I = 10% ÷ 4.79079Rental payments at beginning of period 92,927$

31

Bargain Purchase Option (BPO)Bargain Purchase Option (BPO)Bargain Purchase Option (BPO)Bargain Purchase Option (BPO)

Effective Decrease in OutstandingDate Payment Interest Balance Balance

1/1/11 479,079$ 1/1/11 92,931$ -$ 92,931$ 386,148

12/31/11 92,931 38,615 54,316 331,832 12/31/12 92,931 33,183 59,748 272,084 12/31/13 92,931 27,208 65,723 206,361 12/31/14 92,931 20,636 72,295 134,067 12/31/15 92,931 13,407 79,524 54,542

557,586$ 133,049$ 424,537$

Exercise of BPO at the end of the lease term:$54,542 × 10% = $5,458*

$60,000 BPO payment - $5,458 = $54,542$54,542

32

Bargain Purchase Option (BPO)Bargain Purchase Option (BPO)Bargain Purchase Option (BPO)Bargain Purchase Option (BPO)

End of Lease – December 31, 2016

Sans Serif Publishers, Inc. (Lessee)Depreciation expense ($479,079 ÷ 7) 68,440

Accumulated depreciation 68,440

Interest expense 5,458Lease payable 54,542

Cash (BPO payment) 60,000

CompDec Corporation(Lessor)Cash 60,000

Lease receivable 54,582Interest revenue 5,458

End of Lease – December 31, 2016

Sans Serif Publishers, Inc. (Lessee)Depreciation expense ($479,079 ÷ 7) 68,440

Accumulated depreciation 68,440

Interest expense 5,458Lease payable 54,542

Cash (BPO payment) 60,000

CompDec Corporation(Lessor)Cash 60,000

Lease receivable 54,582Interest revenue 5,458

Refer the amortization schedule and computations on the previous screenRefer the amortization schedule and computations on the previous screen

33

Accounting for initial direct costs:

Operating leases, the lessor should defer initial direct

costs.

Sales-type leases, the lessor expenses the initial direct

costs.

Direct-financing lease, the lessor adds initial direct

costs to the net investment.

Initial Direct Costs (Lessor)

Special Accounting ProblemsSpecial Accounting ProblemsSpecial Accounting ProblemsSpecial Accounting Problems

LO 3 Describe the lessor’s accounting for sales-type leases.

34

GAAP does not indicate how to measure the current and

noncurrent amounts.

For both the annuity-due and the ordinary-annuity situations

report the reduction of principal for the next period as a current

liability/current asset.

Current versus Noncurrent

Special Accounting ProblemsSpecial Accounting ProblemsSpecial Accounting ProblemsSpecial Accounting Problems

LO 3 Describe the lessor’s accounting for sales-type leases.

35

For lessees:

1. General description of material leasing arrangements.

2. Reconciliation between the total of future minimum lease

payments at the end of the reporting period and their present

value.

3. Total of future minimum lease payments at the end of the

reporting period, and their present value for periods (1) not later

than one year, (2) later than one year and not later than five

years, and (3) later than five years.

Disclosing Lease Data

Special Accounting ProblemsSpecial Accounting ProblemsSpecial Accounting ProblemsSpecial Accounting Problems

LO 4 List the disclosure requirements for leases.

36

1. General description of the nature of leasing arrangements.

2. The nature, timing, and amount of cash inflows and outflows

associated with leases, including payments to be paid or

received for each of the five succeeding years.

3. The amount of lease revenues and expenses reported in the

income statement each period.

4. Description and amounts of leased assets by major balance

sheet classification and related liabilities.

5. Amounts receivable and unearned revenues under lease

agreements.

Disclosing Lease Data

Special Accounting ProblemsSpecial Accounting ProblemsSpecial Accounting ProblemsSpecial Accounting Problems

LO 4 List the disclosure requirements for leases.

37

EXAMPLES OF LEASE ARRANGEMENTS

38

EXAMPLES OF LEASE ARRANGEMENTS

39

EXAMPLES OF LEASE ARRANGEMENTS

40

EXAMPLES OF LEASE ARRANGEMENTS

41

EXAMPLES OF LEASE ARRANGEMENTS

42

EXAMPLES OF LEASE ARRANGEMENTS

43

EXAMPLES OF LEASE ARRANGEMENTS

44

EXAMPLES OF LEASE ARRANGEMENTS

45

The term sale-leaseback describes a transaction in which the

owner of the property (seller-lessee) sells the property to

another and simultaneously leases it back from the new owner.

Advantages:

1. Financing

2. Taxes

SALE-LEASEBACKS

46

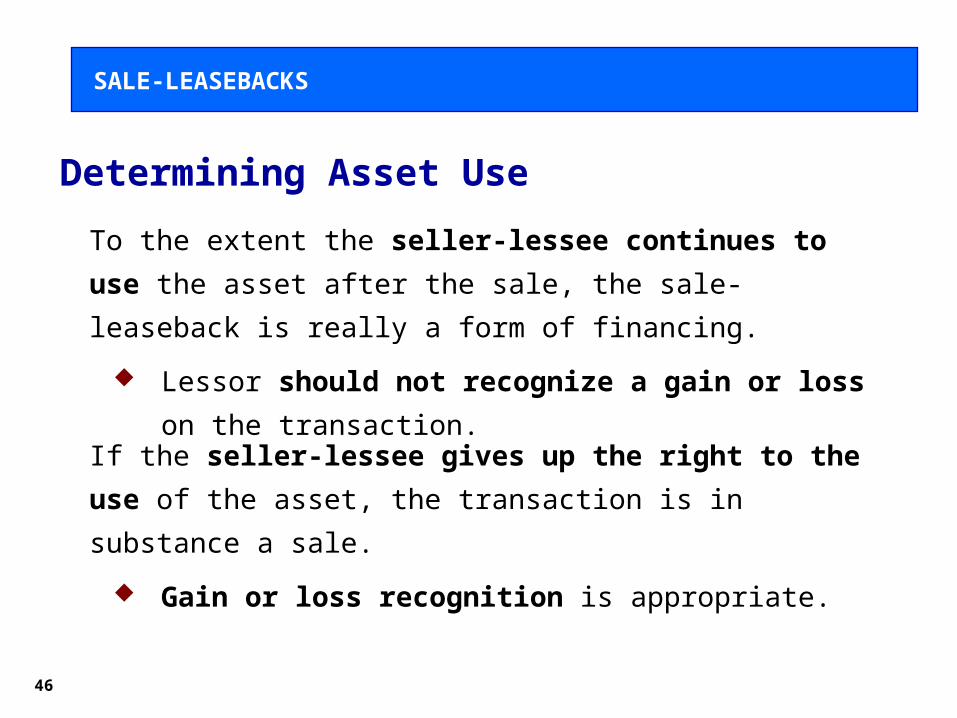

Determining Asset Use

To the extent the seller-lessee continues to use the asset

after the sale, the sale-leaseback is really a form of financing.

Lessor should not recognize a gain or loss on the

transaction.

If the seller-lessee gives up the right to the use of the asset,

the transaction is in substance a sale.

Gain or loss recognition is appropriate.

SALE-LEASEBACKS

47

If the lease meets one of the four criteria for treatment as a

capital lease, the seller-lessee should

Account for the transaction as a sale and the lease as a

capital lease.

Defer any profit or loss it experiences from the sale of the

assets that are leased back under a capital lease.

Amortize profit over the lease term .

Lessee

SALE-LEASEBACKS

48

If none of the capital lease criteria are satisfied, the seller-

lessee accounts for the transaction as a sale and the lease as

an operating lease.

Lessee defers such profit or loss and amortizes it in

proportion to the rental payments over the period when it

expects to use the assets.

Lessee

SALE-LEASEBACKS

49

If the lease meets one of the lease capitalization criteria, the

purchaser-lessor records the transaction as a purchase and a

direct-financing lease.

If the lease does not meet the criteria, the purchaser-lessor

records the transaction as a purchase and an operating lease.

Lessor

SALE-LEASEBACKS

50

American Airlines on January 1, 2011, sells a used Boeing 757 having a carrying

amount on its books of $75,500,000 to CitiCapital for $80,000,000. American

immediately leases the aircraft back under the following conditions:

1. The term of the lease is 15 years, noncancelable, and requires equal rental

payments of $10,487,443 at the beginning of each year.

2. The aircraft has a fair value of $80,000,000 on January 1, 2012, and an

estimated economic life of 15 years.

3. American pays all executory costs.

4. American depreciates similar aircraft that it owns on a straight-line basis

over 15 years.

5. The annual payments assure the lessor a 12 percent return.

6. American’s incremental borrowing rate is 12 percent.

Sale-Leaseback Example

SALE-LEASEBACKS

51

This lease is a finance lease to American because the lease

term is equal to the estimated life of the aircraft and because

the present value of the lease payments is equal to the fair

value of the aircraft to CitiCapital.

CitiCapital should classify this lease as a direct financing lease.

Sale-Leaseback Example

SALE-LEASEBACKS

52

SALE-LEASEBACKS

53

RELEVANT FACTS

Both GAAP and IFRS share the same objective of recording leases by lessees and lessors according to their economic substance—that is, according to the definitions of assets and liabilities.

GAAP for leases uses bright-line criteria to determine if a lease arrangement transfers the risks and rewards of ownership; IFRS is more general in its provisions.

One difference in IFRS and GAAP is that finance leases are referred to as capital leases in GAAP.

Under IFRS, lessees and lessors use the same general lease capitalization criteria. GAAP has additional lessor criteria that payments are collectible and there are no additional costs associated with a lease.

54

RELEVANT FACTS

IFRS requires that lessees use the implicit rate to record a lease, unless it is impractical to determine the lessor’s implicit rate. GAAP requires use of the incremental rate, unless the implicit rate is known by the lessee and the implicit rate is lower than the incremental rate.

Under GAAP, extensive disclosure of future noncancelable lease payments is required for each of the next five years and the years thereafter. Although some international companies (e.g., Nokia) provide a year-by-year breakout of payments due in years 1 through 5, IFRS does not require it.

55

End of Lecture 29End of Lecture 29End of Lecture 29End of Lecture 29