Solvency and Financial Condition Report Everest Insurance ...

Solvency and Financial Condition Report

Bupa Insurance Limited31 December 2016

Bupa Insurance Limited Solvency and Financial Condition Report 2016

Contents

Summary ................................................................................................................................................. 3

A. Business and Performance................................................................................................................. 7

A.1 Business ........................................................................................................................................ 7

A.2 Underwriting performance ............................................................................................................. 9

A.3 Investment performance .............................................................................................................. 10

A.4 Performance from other activities ................................................................................................ 11

A.5 Any other information .................................................................................................................. 11

B. System of Governance ..................................................................................................................... 12

B.1 General information on the system of governance ...................................................................... 12

B.2 Fit and proper requirements ........................................................................................................ 14

B.3 Risk management system including Own Risk and Solvency Assessment ................................ 15

B.4 Internal control system ................................................................................................................ 18

B.5 Internal audit function .................................................................................................................. 18

B.6 Actuarial function ......................................................................................................................... 19

B.7 Outsourcing ................................................................................................................................. 19

B.8 Any other information .................................................................................................................. 20

C. Risk Profile ....................................................................................................................................... 21

C.1 Underwriting risk .......................................................................................................................... 21

C.2 Market risk ................................................................................................................................... 22

C.3 Credit risk .................................................................................................................................... 24

C.4 Liquidity risk ................................................................................................................................. 24

C.5 Operational risk ........................................................................................................................... 24

C.6 Other material risks ..................................................................................................................... 25

C.7 Any other information .................................................................................................................. 25

D. Valuation for Solvency Purposes ..................................................................................................... 27

D.1 Assets .......................................................................................................................................... 28

D.2 Technical provisions .................................................................................................................... 30

D.3 Other liabilities ............................................................................................................................. 33

D.4 Alternative methods for valuation ................................................................................................ 35

D.5 Any other information .................................................................................................................. 35

E. Capital Management ......................................................................................................................... 36

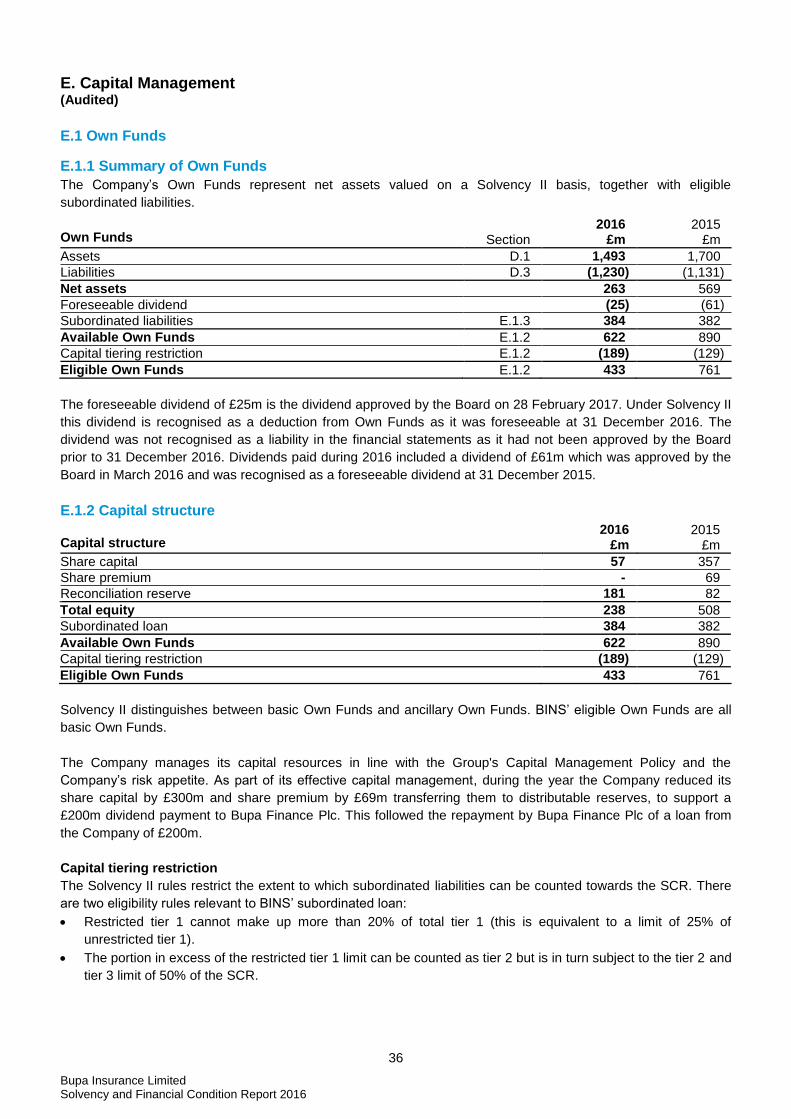

E.1 Own Funds .................................................................................................................................. 36

E.2 Solvency Capital Requirement and Minimum Capital Requirement ........................................... 38

E.3 Use of the duration-based equity risk sub-module in the calculation of the SCR ....................... 39

E.4 Differences between the standard formula and any internal model used ................................... 39

E.5 Non-compliance with the Minimum Capital Requirement and Solvency Capital Requirement ... 39

E.6 Any other information .................................................................................................................. 39

Directors’ responsibility statement ........................................................................................................ 40

Independent auditor’s opinion ............................................................................................................... 41

Glossary ................................................................................................................................................ 44

Annex - Reporting templates ................................................................................................................ 45

3

Bupa Insurance Limited Solvency and Financial Condition Report 2016

Summary (Unaudited)

BUSINESS AND PERFORMANCE SUMMARY

Bupa Insurance Limited (BINS or “the Company”) is part of the Bupa Group (“the Group”). The ultimate parent

undertaking of the Company is The British United Provident Association Limited (“Bupa”).

Bupa’s status, as a company limited by guarantee with no shareholders, enables the Group to make customers its

absolute focus. This means the Group can reinvest its profits to provide more and better healthcare for current

and future customers.

As a service organisation, everything Bupa does for its customers relies on its people and partners, so being a

place where people love to work is critical to its success. Bupa employs 86,000 people principally in the UK,

Australia, Spain, Hong Kong, Poland, New Zealand, Chile, Brazil, Thailand, China, Saudi Arabia, India and the

U.S.

Around 70% of Bupa’s revenue is from health insurance, with the rest from health and care provision. Bupa funds

healthcare around the world and runs clinics, dental centres, hospitals, care homes and retirement villages in a

number of countries.

Bupa’s refreshed strategic framework is driving the next phase of the Group’s development in today’s digital age.

It has three core elements – Customers, People and Performance – underpinned by three operating principles,

with Bupa’s purpose and values guiding everything it does.

Bupa’s refreshed strategic framework:

BINS is Bupa’s UK short-term health, dental and travel insurance underwriter and reinsurer through which the

domestic UK Private Medical Insurance (UK PMI) and International Private Medical Insurance (IPMI) businesses

write insurance contracts.

4

Bupa Insurance Limited Solvency and Financial Condition Report 2016

BINS strategic focus is to deliver great customer outcomes and long-term profitable growth. Our priorities include:

Customer experience, delivering great value and care.

Strengthened risk and compliance management.

Health risk management, assuring quality and supporting customer affordability.

Customer growth and retention, meeting the needs of different customer segments across our domestic UK

PMI and global IPMI markets.

Continued focus on operational efficiency ensuring value for money for all of our customers.

BINS is authorised by the Prudential Regulation Authority (PRA) and regulated by both the Financial Conduct

Authority (FCA) and the PRA.

SYSTEM OF GOVERNANCE SUMMARY

The Company recognises the importance of strong corporate governance and has established a well-defined

governance framework, system of control and committee structure.

BINS and Bupa Insurance Services Limited (BISL) are collectively known as the Regulated Entities. BISL is a

fellow Group company which provides operational services to BINS, including the provision of insurance

mediation and administrative services. The BINS and BISL Boards, collectively known as the Regulated Entities

Board (“the Board”), operate within the agreed strategy, risk appetite and policies of the Bupa Board.

The Regulated Entities Board Committee structure is as follows:

The Company employs a ‘three lines of defence’ governance model to ensure that risk management is effective,

appropriate decisions are made and best practice is implemented and maintained. Broadly the responsibility of

the three lines is as follows:

First line: business management is responsible for the identification and assessment of risks and controls, as

well as for developing and implementing mitigation plans where necessary.

Second line: risk functions provide support and challenge the completeness and accuracy of risk

assessments and the adequacy of mitigation plans.

Third line: internal audit provides independent and objective assurance on the robustness of the risk

management framework, and the appropriateness and effectiveness of internal controls.

RISK PROFILE SUMMARY

The Company’s principal activity is the provision and administration of domestic and international health insurance

providing cover to 2.9 million customers worldwide.

The Company’s product range covers a range of benefit choices and is available in the consumer, small and

medium enterprise (SME) and corporate markets.

Economic ‘Solvency capital’ is held to ensure that the Company can meet its obligations to policyholders as they

fall due in all but the most extreme circumstances, with the likelihood that it will be insufficient no more than once

every 200 years. The Solvency Capital Requirement (SCR) is calculated in accordance with the standard formula

specified in the Solvency II legislation. The Company has obtained approval from the PRA to substitute the

insurance premium risk parameter used in the standard formula with an undertaking specific parameter (USP)

5

Bupa Insurance Limited Solvency and Financial Condition Report 2016

which reflects the Company’s own loss experience. The following charts show the composition of the Company’s

diversified SCR at 31 December 2016 and 31 December 2015:

The SCR profile of the Company has not changed materially over the past 12 months. Underwriting risk

represents the biggest risk to the Company, followed by operational risk.

Underwriting risk refers to the risk that premiums earned are not adequate to cover claims, expenses and profit

margin. It includes the risk that technical provisions for claims incurred prove to be insufficient in the light of later

events and claims experience. This risk is managed by a number of approaches including the regular review of

premium tariffs, effective claims risk management and the ongoing review of claims patterns.

Operational risk is the risk of loss arising from inadequate or failed internal processes, or from personnel, systems

or external events. Maintenance of robust internal control processes and governance frameworks, the approval of

risk policies, and the regular assessment of compliance help mitigate operational risk.

Market risk is the risk of adverse movements in the fair values of financial instruments, arising from fluctuations in

interest rates, foreign exchange rates, commodity prices, credit spreads and equity prices. The focus of the

Company’s long-term financial strategy is to facilitate growth without undue balance sheet risk. The majority of its

cash and investments are held with highly rated credit institutions.

VALUATION FOR SOLVENCY PURPOSES SUMMARY

Solvency II requires an economic market consistent approach to the valuation of assets and liabilities. A number

of assets and liabilities require different valuation methods to those used in the financial statements prepared

under UK Generally Accepted Accounting Practice (UK GAAP). The valuation differences are summarised as

follows:

2016 £m

2015 £m

UK GAAP equity attributable to shareholders 210 512

Valuation differences:

Assets 1 2

Technical provisions 121 124

Deferred tax liabilities (21) (23)

Subordinated liabilities (48) (46)

Solvency II excess of assets over liabilities 263 569

Section D includes information on the valuation basis adopted for each class of assets and liabilities and also

provides an explanation of valuation differences arising when moving from the valuation basis used in the

Company’s financial statements to the Solvency II valuation basis.

6

Bupa Insurance Limited Solvency and Financial Condition Report 2016

CAPITAL MANAGEMENT SUMMARY

The Company’s capital management objective is to maintain sufficient capital to safeguard the Company’s ability

to continue as a going concern and to protect the interests of all of its customers, investors, regulators and trading

partners while also efficiently deploying capital and managing risk to sustain ongoing business development.

The Company has issued a £330m callable subordinated perpetual loan. This loan is accounted for as a liability in

the UK GAAP financial statements but, to the extent that it is eligible, is treated as solvency capital for regulatory

and management purposes.

The Company manages its capital resources in line with the Group's Capital Management Policy and the

Company’s risk appetite. As part of its capital management, during June 2016 the Company carried out a share

capital reduction to support a £200m dividend payment to Bupa Finance Plc, which followed the repayment of a

£200m loan to the Company by Bupa Finance Plc.

The SCR coverage ratio at 31 December 2016 was 160%.

Solvency II capital position 2016

£m 2015

£m

Eligible Own Funds 433 761

SCR 271 252

Surplus 162 509

Solvency ratio 160% 302%

The decrease in coverage during the year reflects the Company’s deliberate actions to improve balance sheet

efficiency, including eliminating the loan to Bupa Finance Plc.

The Company has maintained sufficient capital to exceed both the SCR and the Minimum Capital Requirement

(MCR) throughout the reporting period. Information on the SCR and the MCR is provided in section E.2: Solvency

Capital Requirement and Minimum Capital Requirement.

The Company’s capital position is kept under constant review and is reported monthly to the Board.

OTHER INFORMATION

In line with PRA requirements, sections D. Valuation for Solvency Purposes and E. Capital Management of the

SFCR have been subject to audit by the external auditor. Sections A. Business and Performance, B. System of

Governance and C. Risk Profile are unaudited.

7

Bupa Insurance Limited Solvency and Financial Condition Report 2016

A. Business and Performance (Unaudited)

A.1 Business

A.1.1 Company information

The Company is incorporated in England and Wales under the company registration number 3956433. The

Company is a wholly owned subsidiary of Bupa Finance Plc, a company incorporated in England and Wales.

The ultimate parent undertaking of the Company is The British United Provident Association Limited (“Bupa”), a

company incorporated in England and Wales. Bupa is the parent company of the Bupa group of companies. Bupa

does not have shareholders. Governance over Bupa is exercised by approximately one hundred Association

Members who vote at an Annual General Meeting on director reappointments and adoption of the financial

statements. These Association Members are not entitled to any of the assets or income of Bupa. No individual

has 10% or more voting rights or any other mechanism of control of Bupa.

The Group supervisor is the PRA, Bank of England, 20 Moorgate, London, EC2R 6DA.

The Group supervisor is also the supervisor for the Company.

The Company’s external auditor is KPMG LLP, Chartered Accountants, 15 Canada Square, London, E14 5GL.

The Company’s Annual Report and Accounts, Bupa’s Annual Report and Accounts and Bupa’s Solvency and

Financial Condition Report (SFCR) are available on the Bupa website: bupa.com.

A.1.2 Business

The Company is the UK’s largest health insurer and a leading provider of international health insurance providing

medical cover to 2.9 million customers worldwide. It is wholly owned by the Bupa Group, an international

customer-focused health and care group employing 86,000 people, providing health insurance and running

clinics, dental centres, hospitals, care homes and retirement villages in a number of countries.

Bupa’s purpose is to help people live longer, healthier, happier lives. Bupa’s status, as a company limited by

guarantee with no shareholders, enables us to make our customers our absolute focus, reinvesting our profits to

provide more and better healthcare for current and future customers.

The Company is wholly driven by Bupa’s purpose. It provides consumer, SME and corporate health insurance, as

well as inward reinsurance and a small number of ancillary health insurance products, such as cash plans and

travel insurance.

The Company has two main segments:

UK PMI providing domestic health insurance in the UK market.

IPMI providing individual consumers and employees with international cover.

The principal operations take place in the UK, with further operations sited in Denmark, Cyprus, Malta and

Switzerland. Products underwritten by IPMI are sold in several markets including the United Arab Emirates, Hong

Kong, Singapore and Mexico. The Company reinsures part of its IPMI book of business with Bupa Insurance

Company, a fellow Group company. There are no material reinsurance arrangements external to the Bupa Group.

Operational services, including the provision of insurance mediation and administrative services, are provided by

BISL.

8

Bupa Insurance Limited Solvency and Financial Condition Report 2016

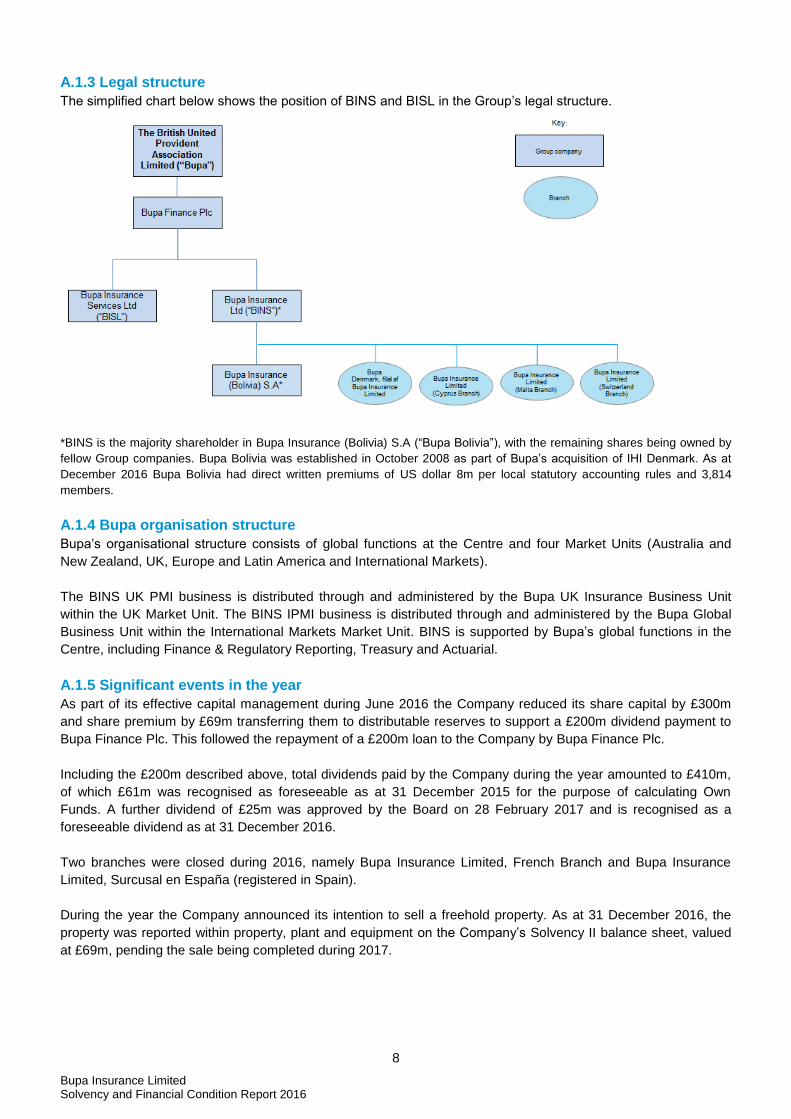

A.1.3 Legal structure

The simplified chart below shows the position of BINS and BISL in the Group’s legal structure.

*BINS is the majority shareholder in Bupa Insurance (Bolivia) S.A (“Bupa Bolivia”), with the remaining shares being owned by

fellow Group companies. Bupa Bolivia was established in October 2008 as part of Bupa’s acquisition of IHI Denmark. As at

December 2016 Bupa Bolivia had direct written premiums of US dollar 8m per local statutory accounting rules and 3,814

members.

A.1.4 Bupa organisation structure

Bupa’s organisational structure consists of global functions at the Centre and four Market Units (Australia and

New Zealand, UK, Europe and Latin America and International Markets).

The BINS UK PMI business is distributed through and administered by the Bupa UK Insurance Business Unit

within the UK Market Unit. The BINS IPMI business is distributed through and administered by the Bupa Global

Business Unit within the International Markets Market Unit. BINS is supported by Bupa’s global functions in the

Centre, including Finance & Regulatory Reporting, Treasury and Actuarial.

A.1.5 Significant events in the year

As part of its effective capital management during June 2016 the Company reduced its share capital by £300m

and share premium by £69m transferring them to distributable reserves to support a £200m dividend payment to

Bupa Finance Plc. This followed the repayment of a £200m loan to the Company by Bupa Finance Plc.

Including the £200m described above, total dividends paid by the Company during the year amounted to £410m,

of which £61m was recognised as foreseeable as at 31 December 2015 for the purpose of calculating Own

Funds. A further dividend of £25m was approved by the Board on 28 February 2017 and is recognised as a

foreseeable dividend as at 31 December 2016.

Two branches were closed during 2016, namely Bupa Insurance Limited, French Branch and Bupa Insurance

Limited, Surcusal en España (registered in Spain).

During the year the Company announced its intention to sell a freehold property. As at 31 December 2016, the

property was reported within property, plant and equipment on the Company’s Solvency II balance sheet, valued

at £69m, pending the sale being completed during 2017.

9

Bupa Insurance Limited Solvency and Financial Condition Report 2016

A.2 Underwriting performance

A.2.1 Overview

Presented below is the Company’s underwriting performance as reported in its financial statements.

Underwriting performance 2016

£m

Premiums:

Gross premiums written 2,378

Outward reinsurance premiums (106)

Premiums written, net of reinsurance 2,272

Change in the net provision for unearned premiums 5

Net insurance premiums earned 2,277

Other technical income, net of reinsurance 5

Claims:

Gross claims paid 1,728

Reinsurers’ share of claims paid (93)

Change in the net provision for claims 15

Net claims incurred 1,650

Net operating expenses 522

Total claims and expenses 2,172

Profit before investment income and expense and tax 110

The Company’s profit before investment income and tax of £110m represents a 38% decrease when compared to

the 2015 profit of £176m. The decrease is driven by an increase in the insurance agency fee recharge from BISL,

which is due to the impact of movements in foreign exchange rates on operating expenses, impairment to

intangible assets and increased governance and compliance costs as the Company strengthens its conduct

environment.

Total revenues increased by 5% in the year despite a challenging market with affordability of health insurance a

key concern for customers. In UK PMI revenue increased across both corporate and SME segments with new

business growth in the consumer segment. This was against a backdrop of a 0.5% increase in the rate of

insurance premium tax. The Company continues to work across the sector to stimulate reform in the private

health care industry and improve affordability for customers. Focus is on containing healthcare costs, particularly

those charged by private hospitals, which make up the majority of total costs.

In the IPMI segment, underlying revenue has reduced due to a fall in customer numbers following the decisions to

exit non-strategic markets and contractions in the corporate and SME business. However, the Company’s

revenue benefited from the devaluation of sterling against the US dollar leading to a slight increase in overall IPMI

revenue.

A.2.2 Underwriting performance by line of business

2016

Medical expense

£m

Assistance

£m Total

£m

Net insurance premium earned 2,233 44 2,277

Net insurance claims incurred 1,561 25 1,586

Expenses 568 15 583

Underwriting profit 104 4 108

The assistance line of business is constituted from benefits sold as part of cash plans and travel insurance.

The information by line of business is presented in accordance with the Solvency II Quantitative Reporting

Template (QRT) S.05.01.02 ‘Premiums, claims and expenses by line of business’ (refer to attached Annex). The

underwriting profit of £108m differs from the £110m profit reported in the financial statements due to minor

differences in the classification of technical expenses and revenues between the financial statements and

Solvency II reporting.

10

Bupa Insurance Limited Solvency and Financial Condition Report 2016

Claims handling costs of £64m are included within expenses on the QRT, in compliance with Solvency II reporting

requirements, but are included in claims in the financial statements.

Expenses

A summary of expenses is provided below:

Operating expenses 2016

£m

Commission and other acquisition costs 145

Expenses payable to Bupa Group companies 349

Staff costs 3

Net loss on foreign exchange transactions 22

Reinsurers share of expenses (11)

Changes in deferred acquisition costs (1)

Other operating expenses 15

Net operating expenses per financial statements 522

Claims handling cost 64

Classification differences between Solvency II and the financial statements (3)

Underwriting expenses 583

A.2.3 Underwriting performance by geographical area

2016 UK £m

United Arab

Emirates £m

Hong Kong

£m Singapore

£m Denmark

£m Others

£m Total

£m

Net insurance premium earned1 1,615 154 51 34 28 395 2,277

Net insurance claims incurred 1,194 111 34 25 14 208 1,586

Expenses2 331 63 16 12 11 150 583

Underwriting profit / (loss) 90 (20) 1 (3) 3 37 108

1. Premiums earned are allocated across geographical areas on a sold-in basis.

2. Expenses include impact of foreign exchange revaluation on the statutory results.

The information is presented in accordance with the QRT S.05.02.01 ‘Premiums, claims and expenses by

country’.

A.3 Investment performance

A.3.1 Investment income

Investment income for the year was as follows:

Investment income 2016

£m

Income from Bupa Group undertakings:

Interest receivable 2

Rental income 6

Income from deposits with credit institutions 7

Realised capital gains on investments 5

Realised foreign exchange gains 8

Investment income as reported in the Company’s profit and loss account 28

Unrealised gains on investments 46

Realised foreign exchange losses as reported in investment expenses (26)

Total investment income 48

A large proportion of the Company’s investments are in cash or cash-like instruments. The Company has also

invested in a limited portfolio of non-cash assets (return seeking asset portfolio), principally bonds, properties,

loans, collective investment undertakings and segregated funds. Hedging instruments were used to manage the

foreign exchange risks from non-sterling investments.

11

Bupa Insurance Limited Solvency and Financial Condition Report 2016

Investment income by Solvency II asset class is presented in the table below.

Investment income by asset class 2016

£m

Government bonds 10

Corporate bonds 18

Collective investment undertakings 3

Cash and deposits 18

Mortgages and loans 14

Property 5

Hedging instruments (20)

Total investment income 48

A.3.2 Investment expenses

Investment expenses in the year amounted to £1m, covering investment management fees and other costs

relating to investment related activities.

A.3.3 Gains/losses recognised directly in equity

For the year ended 31 December 2016, there were no material gains or losses reported directly in equity.

A.4 Performance from other activities

Financial expense

Interest on borrowings in the year amounted to £23m, comprising £21m payable to Bupa Finance Plc in respect of

the subordinated liabilities which are classified as Own Funds for Solvency II purposes and other interest payable

of £2m.

Leasing arrangements

BINS leases part of an owned office building to other entities in the Group. Rental income of £6m was received by

BINS during 2016 and is included in investment income in the Company’s income statement. During the year the

company announced its intention to sell the property which provides the rental income (refer section A.1.5

Significant events in the year). There are no other material operating lease arrangements.

BINS had no finance leases during 2016.

A.5 Any other information

There is no other material information to be disclosed.

12

Bupa Insurance Limited Solvency and Financial Condition Report 2016

B. System of Governance (Unaudited)

B.1 General information on the system of governance

B.1.1 Board responsibilities

The role of the Board

The Board comprises an independent Non-Executive Chairman, three other Non-Executive Directors (NEDs) and

three Executive Directors. It normally meets six times a year and at other times as required. Minutes of all Board

and Committee meetings are recorded and reflect the substance of the discussion, as well as the decisions made.

The Board closely monitors developments in corporate governance and assesses how these can be applied to

BINS. The Company’s governance arrangements continue to be reviewed in line with developments in best

practice. The Board believes the existing structure is appropriate for the size and complexity of BINS.

The Board is responsible for the oversight of the management of BINS, including:

Agreeing BINS long-term directions and objectives.

Developing and maintaining BINS business model and aligning the BINS business model with the Bupa

Group strategy, while ensuring that local regulation, legislation or market practice is also met.

Determining the nature and extent of the significant risks it is willing to take in achieving its strategic objectives

and setting the risk appetite.

Oversight of BINS operations.

Ensuring the appropriate and necessary financial and human resources are in place to meet BINS objectives.

Providing constructive challenge to the executive directors and senior management.

Ensuring the highest standards of governance are followed.

Developing BINS culture.

The role of the Chairman

The Chairman is responsible for the leadership of the Board and is pivotal in the creation of the conditions

necessary for overall Board and individual director effectiveness, both in and outside the boardroom, including:

The leadership of the Board and ensuring its effectiveness on all aspects of its role.

Ensuring effective Board governance.

Setting agendas.

Ensuring that members of the Board receive accurate, timely and clear information.

Managing the Board to ensure sufficient time is allowed for discussion of key risks and issues.

Facilitating contributions from NEDs.

Considering and addressing the development needs (induction, training and professional development) of

individual directors and the Board as a whole.

The role of the Non-Executive Directors

The role of the NEDs includes the following key elements:

Constructively challenging and helping to develop proposals on longer term direction and strategy.

Scrutinising the performance of management in meeting agreed goals and objectives and monitoring the

reporting of performance.

Satisfying themselves on the integrity of financial information, and that financial controls and systems of risk

management are robust and effective.

The role of the Chief Executive Officer

The Chief Executive Officer (CEO) manages the Regulated Entities in accordance with the business plans

approved by the Board and in accordance with the overall Bupa Group strategy and plans. The CEO leads the

setting and execution of the Regulated Entities business strategy and is accountable for:

Ensuring that the Regulated Entities remain legally solvent at all times and that customers are treated fairly.

13

Bupa Insurance Limited Solvency and Financial Condition Report 2016

Ensuring that the Regulated Entities are compliant with all law and regulations affecting their businesses, their

policyholders and their staff, including fulfilling all relevant obligations as required under the Senior Insurance

Managers Regime.

Managing the Regulated Entities risk profile, in line with the extent and categories of risk identified as

acceptable by the Board.

Approving the apportionment and allocation of roles and responsibilities of the executive management team of

the Regulated Entities.

Approving all capital and revenue transactions, including acquisitions and disposals, not specifically reserved

to the Board.

Embedding BINS culture in the day to day management of BINS.

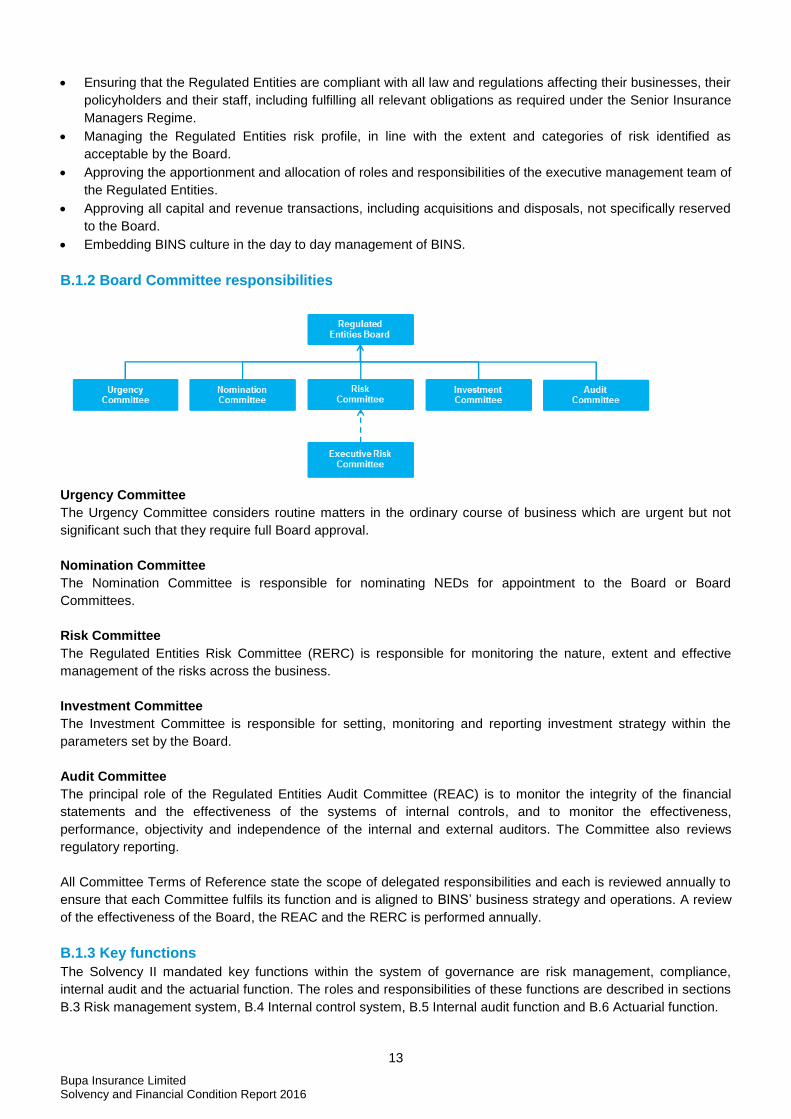

B.1.2 Board Committee responsibilities

Urgency Committee

The Urgency Committee considers routine matters in the ordinary course of business which are urgent but not

significant such that they require full Board approval.

Nomination Committee

The Nomination Committee is responsible for nominating NEDs for appointment to the Board or Board

Committees.

Risk Committee

The Regulated Entities Risk Committee (RERC) is responsible for monitoring the nature, extent and effective

management of the risks across the business.

Investment Committee

The Investment Committee is responsible for setting, monitoring and reporting investment strategy within the

parameters set by the Board.

Audit Committee

The principal role of the Regulated Entities Audit Committee (REAC) is to monitor the integrity of the financial

statements and the effectiveness of the systems of internal controls, and to monitor the effectiveness,

performance, objectivity and independence of the internal and external auditors. The Committee also reviews

regulatory reporting.

All Committee Terms of Reference state the scope of delegated responsibilities and each is reviewed annually to

ensure that each Committee fulfils its function and is aligned to BINS’ business strategy and operations. A review

of the effectiveness of the Board, the REAC and the RERC is performed annually.

B.1.3 Key functions

The Solvency II mandated key functions within the system of governance are risk management, compliance,

internal audit and the actuarial function. The roles and responsibilities of these functions are described in sections

B.3 Risk management system, B.4 Internal control system, B.5 Internal audit function and B.6 Actuarial function.

14

Bupa Insurance Limited Solvency and Financial Condition Report 2016

B.1.4 Remuneration policy and practices

Bupa’s remuneration policy is designed to deliver market competitive reward to help attract, retain and motivate

high calibre employees, and promote a prudent approach to risk.

The Bupa Remuneration Committee has responsibility for setting remuneration policy, approving the design of the

annual bonus scheme, the management bonus scheme and long-term incentive plan, choosing an appropriate

balance of performance measures and setting appropriate targets and maximums for all such incentive schemes.

The Bupa Remuneration Committee has worked closely with its advisers and with management in developing

these plans and the Group’s remuneration policy, reflecting a shared agenda in how Bupa rewards future

performance, with customers and risk management at the heart of what Bupa does. The Bupa Remuneration

Committee reviews annually the ongoing appropriateness and relevance of the remuneration policy. In doing so, it

takes into account all relevant factors including regulatory requirements, the provisions and recommendations of

the UK Corporate Governance Code and associated guidance, the views of Bupa’s Association Members and

other stakeholders, the risk appetite of Bupa and input from the Bupa Risk Committee. It also takes independent

external advice. The Bupa Remuneration Committee itself comprises independent board directors. There is cross

membership between the Bupa Risk Committee and the Bupa Remuneration Committee.

In determining incentive outcomes, the Bupa Remuneration Committee considers if results have been achieved in

a way that aligns with our values, underlying business performance and approach to risk management, which

includes consideration of risk assessments summarised in annual letters from the Group Risk Committee and

from the Chair of the RERC to the Remuneration Committee. For 2017, all incentive payments are additionally

subject to a risk adjustment which allows for downward adjustments in the event of poor risk decision-making or

risk management, including any breaches of Bupa’s risk appetite.

While BINS did not have a separate remuneration committee during 2016, such a committee is currently in the

process of being established. Formal terms of reference, to be approved by the Board, will ensure that the

responsibilities of this committee are clear, including how it interacts with the Bupa Remuneration Committee.

The Company’s only employees are employed by the Danish branch. All other staff, including the Directors, are

remunerated and employed through the Company’s service company, BISL, with costs recharged to the

Company.

The Remuneration Report on pages 42 to 52 of the 2016 Bupa Annual Report includes detailed information on:

the remuneration policy of the Bupa Group, the components of remuneration and performance criteria on which

entitlements are based. BINS’ remuneration policy is consistent with the Bupa Group policy.

Remuneration in the year for the BINS Directors was as follows:

2016 2015 Directors’ remuneration £m £m

Emoluments 2 2

Amounts receivable under long-term incentive schemes 1 1

3 3

No Director had any material interest in any contracts with Group companies at 31 December 2016 (2015: £nil) or

at any time during the year.

B.2 Fit and proper requirements

BINS implements policies and procedures to ensure persons who effectively run the undertaking or have other

key functions are fit and proper to do so. Before appointment, and on an annual basis, directors and senior

managers are assessed with reference to the specific requirements of their particular role. Certain individuals

holding roles of significant influence are required to have received prior approval from the PRA and/or FCA before

they can perform their role. Individuals holding key functions are also separately notified to the PRA.

15

Bupa Insurance Limited Solvency and Financial Condition Report 2016

An individual’s fitness to perform their role refers to their competence and capability including skills, knowledge

and expertise applicable. Assessments of fitness are tailored to the individual’s particular role, including the

individual’s knowledge and understanding of:

The markets in which they operate (i.e. insurance/financial services and/or care provision).

Business strategy and business model.

System of governance.

Financial and, where relevant, actuarial analysis.

Regulatory framework and requirements.

Individuals are required to maintain their fit and proper status which would include arranging for further

professional training as necessary, so that the individual is also able to meet changing or increasing requirements

of their particular responsibilities.

Appointments are subject to background screening checks, which include verification of ID, previous employment

including references and relevant qualifications; directorship searches; screening against publicly available

information such as the global watch list; disclosure and barring service check; credit checks; and adverse media

searches.

Individuals are regularly monitored to ensure that they maintain fit and proper for their role. This includes

performance management and annual screening checks.

B.3 Risk management system including Own Risk and Solvency Assessment

B.3.1 Risk management framework

Our Risks

BINS’ geographic reach exposes it to a wide range of political, legal and economic contexts. The risks to BINS are

managed by understanding the risk drivers for the business and the balance sheet and by assessing how they

interact. By understanding the risks faced, the Company seeks opportunities to benefit from risk diversification, to

identify emerging risks and to understand and manage any risk concentrations.

BINS accepts risks as part of its business operation. Some risks are avoidable (e.g. certain financial risks) and

others are an accepted consequence of BINS’ business model (e.g. operational risks). The Company has an

effective risk management system and appropriate internal controls in place to mitigate these risks.

BINS maintains significant economic capital as a mitigant against certain inherent risks, reflecting the nature of

the Company’s operations and the level of risk associated with them. The most significant are:

Risks relating to BINS insurance businesses, including the risk of inadequate pricing or underwriting of

insurance policies and the risk of claims experience being materially adversely different to expectations.

Operational risks.

There are certain risks where holding capital is one mitigating action, but there are also other more effective

methods of mitigation. These are significant risks to BINS. The RERC regularly review the residual risks arising

and the mitigating actions in place to reduce the levels of residual risk. This provides management with a view of

the areas of priorities to focus resources. These risks include customer and conduct related risks and specific

operational risks including those related to cybersecurity.

There are also other risks where capital is not an appropriate mitigant and even though they are not highlighted

above they are always a priority issue for management. These include: strategic risks, liquidity risk and

reputational risks.

Further information on BINS’ risk profile is provided at section C: Risk Profile.

Risk governance

The Company adopts a three lines of defence approach for the governance of risk management which is set out

in the Risk Management Framework.

16

Bupa Insurance Limited Solvency and Financial Condition Report 2016

The first line of defence encompasses management and staff in Bupa’s individual Business Units and at the

Centre, who are responsible for the identification and management of risks. In each Business Unit an executive

risk committee, chaired by the Business General Manager scrutinises the risk profile and generates mitigating

actions where necessary. This process culminates in the BINS CEO chairing an executive committee, the

Executive Risk Committee (RE ERC), which brings the whole picture together.

The second line of defence comprises compliance and risk management professionals both at the Centre and

within Bupa’s Business Units. The BINS Risk Function is led by the Chief Risk Officer (CRO). Their role is to

advise, challenge and oversee the first line risk management activities and to collate reports for management and

the Board on their independent views on risk issues.

The RERC is composed entirely of independent NEDs to oversee the execution of the risk management

framework. The RERC receives reports from the BINS CRO and other BINS executives as appropriate. The

RERC is accountable for the Board’s oversight and recommends risk appetite to the Board for approval.

The third line of defence is internal audit. Internal audit provides independent and objective assurance on the

robustness of the risk management framework, and the appropriateness and effectiveness of internal controls.

Information on the Company’s internal audit function is provided in section B.5.

Risk appetite

The Board risk appetite expresses the degree of risk the Company is prepared to accept as it works to deliver on

its strategy. The core risk appetite statements are focused on:

management of financial strength

the treatment of customers and employees

the sustainability of the business

operational risk.

The risk appetite statements are a key consideration in the Company’s business planning process and are a

central reference point for key decisions. These statements are not intended to automatically prevent activity

outside of BINS’ risk appetite, but rather to help identify any such instances in a timely manner so that the Board

can consider an appropriate response. There is regular reporting against risk appetite statement limits to the RE

ERC and RERC.

Risk appetite statements are reviewed on an annual basis, with the RERC recommending any changes to the

statements to the Board for approval.

Risk management framework

The Company manages risks according to a Board approved Risk Management Framework. This sets out the

principles underpinning a robust and continuous risk management system for the first line. This ensures:

Current and emerging risks to the business are identified and the potential consequences of them are

understood.

There are clear and established risk appetites within which the Company operates.

Appropriate and effective steps are taken to mitigate and manage identified risks.

Risk management information is utilised to make risk based decisions across the business.

There is clear ownership of, and accountability for, risk.

There is a culture in which:

o appropriate risk behaviours are encouraged and rewarded

o inappropriate behaviours are challenged and sanctioned

o risk events are communicated as quickly as good news without fear of blame.

Well-established regular reporting mechanisms are in place to ensure that all relevant top risks are appropriately

identified and escalated. These processes also ensure that strategies to manage and mitigate the risks to

acceptable levels are identified and executed.

17

Bupa Insurance Limited Solvency and Financial Condition Report 2016

The BINS Enterprise Policies define the way the Company does business. The policies cover all key areas of risk

and are implemented in the Business Units, which monitor compliance against the requirements. These policies

all have designated ownership at both the Company and Business Unit levels with defined roles and

responsibilities. The policies are reviewed on an annual basis.

The processes used to identify, measure, manage, monitor and report risks include a programme of stress and

scenario testing. Specific detailed reviews and deep dives on particular risks are undertaken when considered

necessary.

The effectiveness of the implementation of the Risk Management Framework is tested through the Internal

Control and Risk Management Assessment (ICRMA). This provides a mechanism to assess how well internal

control and risk management practices and policy compliance are embedded across BINS. This is a first line of

defence self assessment, subject to review and challenge by the second and third lines. This assessment is

conducted on an annual basis and the results are presented to the RERC.

Information on the Company’s risk profile is provided at section C. Risk Profile.

Risk management function

The BINS CRO leads the BINS Risk and Compliance function and reports to the Bupa CRO on a day to day

basis. The BINS CRO provides reports directly to the RERC and the Board, and has a direct right of access to the

Chairman of the Board and the Chairman of the RERC. The CRO also attends the REAC by invitation.

The function is split across the Bupa Business Units and a Centre team. Each Business Unit has a Risk and

Compliance Director who is responsible for the operation of the function within the Business Unit. The Risk and

Compliance Directors in the UK Insurance Business Unit and the Bupa Global Business Unit each have a solid

line reporting into the BINS CRO as well as into local Business Unit management.

B.3.2 Own Risk and Solvency Assessment

BINS’ Own Risk and Solvency Assessment (ORSA) comprises the series of activities by which it assesses all the

risks inherent in its business and determines the corresponding capital needs. It therefore includes the following

activities:

The projection of Own Funds and future capital requirements as part of the three-year business plan

presented to the Board for approval annually.

The Economic Capital Assessment (ECA) in which the Company makes its own quantification of how much

capital is required to support its risks. The ECA is used to assess how well the standard formula SCR reflects

BINS’ actual risk profile. The ECA is presented to the RERC for approval on an annual basis.

The annual review of risk appetite which is approved by the RERC.

Regular BINS risk profile and risk appetite reporting as part of the CRO report to the RERC.

Stress and scenario testing and reverse stress testing carried out at least annually and approved by the

RERC.

The outputs of the above activities are set out in papers and reports to the Board or relevant Board Committee

and summarised in the annual ORSA report which is approved by the Board. The conclusions of the ORSA are a

key input into the Board strategy sessions.

The process for carrying out the ORSA is reviewed following the strategy sessions to take account of decisions

made there and also to consider any other enhancements that can be made to the ORSA process. Proposed

changes to the ORSA process are considered by the RERC and then subsequently incorporated into the ORSA

Policy which is approved by the Board.

BINS determines its own solvency needs by reference to the projected Own Funds and future capital

requirements reflecting the risk profile of the Company, its policy of maintaining a substantial buffer over the

18

Bupa Insurance Limited Solvency and Financial Condition Report 2016

capital requirements, potential acquisitions and disposals which might take place over the planning horizon and

the availability of management actions.

B.4 Internal control system

B.4.1 Internal control system

In line with the three lines of defence governance model, internal controls are the responsibility of business

management. Internal controls are implemented as part of the embedding of the suite of Enterprise Policies and

also:

Promote the effectiveness and efficiency of operations.

Ensure the reliability of financial reporting.

Are designed to ensure BINS operates to industry best practice and complies with applicable laws and

regulations.

Enable the Board and RERC to validate that BINS is operating within its risk appetite.

Support the embedding of a strong risk culture throughout the business.

B.4.2 Compliance function

The Compliance function operates within the second line of defence and is concerned with financial services

legislative and regulatory requirements and expectations, including:

Customer outcome standards, e.g. customer fair treatment, training and competence.

High level controls, e.g. governance, skills and competency, systems and controls, conflicts of interest,

regulatory relationships, record keeping, complaints management, strategic risk, market conduct.

Solvency and capital (EU, UK and individual territory prudential requirements).

Regulatory processes, e.g. authorisations and licensing, individual approvals, fines and litigation, breach

management.

B.5 Internal audit function

Bupa has a Global Internal Audit function which is led by the Chief Internal Auditor (CIA). In order to maintain the

function’s independence and objectivity, the primary reporting line for the CIA is to the Chair of the Bupa Group’s

Audit Committee, who is also the Chair of the REAC. Bupa’s internal auditors have no direct operational

responsibility or authority over any of the activities audited.

The CIA has appointed a Bupa UK Market Unit & BINS Audit Director who oversees the execution of the BINS

approved audit plan. The Bupa UK Market Unit & BINS Audit Director reports to the CIA on a day to day basis;

has direct access to the Chair of the REAC as required to maximise independence and objectivity; and attends

the REAC and RERC, by invitation.

The Internal Audit function provides assurance over the effectiveness of governance, risk management and

internal controls. It reviews the effectiveness of controls by undertaking an agreed schedule of internal audits

each year. As the third line of defence, Internal Audit supports BINS in accomplishing its responsibilities by

helping the Board to safeguard the assets, reputation and sustainability of the organisation, and ensure risks to

the customer and the BINS business are appropriately managed. It reports its findings to the REAC and assists

both the Board and management to improve the effectiveness of governance, risk management and internal

controls.

Where specific skills are not available in house, the CIA and the Chair of the Committee have the ability to

procure the services of expert external advisers. During the year, PwC were appointed as Bupa’s first internal

audit co-sourcing provider.

The function acts in accordance with the Global Institute of Internal Auditors’ International standards. In addition to

a regular external assessment of the effectiveness of the function, the internal audit function maintains a quality

assurance and improvement programme that includes an evaluation of the function’s adherence to these

standards.

19

Bupa Insurance Limited Solvency and Financial Condition Report 2016

B.6 Actuarial function

BINS has implemented an Insurance Risk Policy. BINS’ actuarial function activities are conducted by qualified

actuaries in Bupa’s Centre Actuarial function, under the leadership of the Chief Actuary. The Actuarial function

has authority to review all areas of BINS and has full, free and unrestricted access to all activities, records,

property and personnel necessary to complete its work.

Key activities (including all mandatory tasks prescribed under Solvency II) are as follows:

Coordinating and consolidating UK PMI and IPMI technical provisions (for UK GAAP and Solvency II

reporting).

Assessing the appropriateness of technical provision methodology and assumptions used.

Setting methodologies and ensure consistency of use.

Ensuring that data quality and information technology systems meet the required standards.

Reporting to the RERC on the adequacy of technical provisions, the overall underwriting policy and adequacy

of reinsurance arrangements.

Contributing into risk management activities by undertaking the SCR calculation, periodic monitoring and

annual calculation of the USP for premium risk and validation of standard formula appropriateness through

development of the ECA.

Coordinating actuarial community development activity such as leading and sharing actuarial best practices,

and contributing to risk management practices.

An actuarial function report containing the Chief Actuary’s opinions, recommendations and an account of key

activities is prepared and provided to the RERC annually.

The Chief Actuary for BINS and Bupa’s Centre Actuarial team are independent of the Chief Actuaries in the

Business Units and their teams. This independence effectively eliminates any potential conflicts of interest arising

from the commercial responsibilities of Business Unit actuarial functions.

B.7 Outsourcing

BINS has implemented an Enterprise External Suppliers Policy. The purpose of this policy is to ensure that the

Company has effective processes for the selection, contracting and management of all suppliers, allowing the

risks posed by suppliers to be managed throughout the supplier relationship lifecycle. The policy is based on four

main principles; knowing our suppliers, selecting our suppliers, contracting with suppliers and managing our

suppliers. The policy applies to the suppliers of intra-group outsourcing arrangements as well as to suppliers who

are external to the Group.

All key, critical or important outsourced arrangements are required to be identified and managed with additional

rigour. The appointment of these arrangements must follow supplier selection criteria, with appropriate due

diligence and robust contracts in place following legal terms. Contingency measures must be in place and the

relationships managed by a named supplier relationship manager. The arrangements are reported to the local risk

and compliance team to assess the need for regulatory notification.

BINS chooses to outsource services where it is in the best interest of the Company, it conforms to its regulatory

standards and ensures the correct customer outcomes. BINS’ strategy is to form long-term strategic partnerships

with suppliers who share the same values, focus on customer service and have an understanding of the current

regulatory and risk landscape.

BINS continues to assess the need for outsourcing on an ongoing basis. Each outsourced activity is viewed on its

own merits against in-house capability, activity already outsourced and activity being undertaken. This allows

BINS to leverage the relevant external expertise to undertake the activity efficiently and effectively. With robust

oversight (systems & controls) this ensures the correct customer outcomes are achieved with reduced risks and

cost to serve.

20

Bupa Insurance Limited Solvency and Financial Condition Report 2016

Each outsourced supplier has a named supplier relationship manager. This individual is responsible for the

oversight of the arrangement and relationships ensuring appropriate safeguards are in place, such as termination

clauses, continuity plans and agreed service levels. The relationship manager is also responsible for holding

regular meetings to manage the relationship. Comprehensive dashboards have been created to manage the

outsourced suppliers.

Intra-group outsourcing

BINS outsources insurance administration and mediation activities to BISL via an agreement for services. BISL

outsources certain of these services to third parties, including claims processing to a provider located in India.

Where it has outsourced to third parties BISL is responsible for the oversight and management of these

relationships. BISL is required to comply with the Group’s Enterprise External Suppliers Policy, which is also the

basis of the BINS policy.

BISL services all UK PMI and a large proportion of the IPMI contracts that are written by BINS. The Latin America

book of business, and the IPMI business serviced primarily in Denmark are serviced through outsourcing

arrangements with Bupa Worldwide Corporation and USA Medical Services Corporation, and Bupa Denmark

Services A/S respectively.

BINS also outsources elements of its risk management, finance and governance, compliance, internal audit,

information technology, actuarial, treasury and people functions to fellow Group companies: BISL, Bupa Finance

Plc and Bupa.

External outsourcing

BINS has chosen to outsource some of its operational functions and activities to external providers, including

investment management in the UK and customer servicing to an outsource provider in Malta.

B.8 Any other information

There is no other material information to be disclosed.

21

Bupa Insurance Limited Solvency and Financial Condition Report 2016

C. Risk Profile (Unaudited)

General information

BINS’ risk profile is a key driver of the SCR. The distribution of the Company’s quantifiable risks, as reflected in

the SCR, is as follows:

Analysis of the SCR % of diversified SCR

2016

Underwriting risk 57%

Market risk 17%

Credit risk 4%

Operational risk 22%

100%

Information on each of the risk categories is provided in sections C.1 to C.5 below. Information is also provided on

liquidity risk in section C.4. Liquidity risk does not form part of the standard formula SCR and is therefore not

included in the above table.

Information on the calculation of the SCR is provided in section E.2 Solvency Capital Requirement and Minimum

Capital Requirement.

Risk Mitigation

As noted in section B.3.1 risks are managed according to a Board approved Risk Management Framework and

the effectiveness of our implementation of the Risk Management Framework is tested through the ICRMA.

Specific risk mitigations are identified in section C.1 to C.6 where relevant.

C.1 Underwriting risk

Underwriting risk affects future cash flows of the Company. It can be subdivided into pricing risk, claims risk and

reserving risk.

Pricing risk

Pricing risk arises from routine revisions to premium tariffs and from the processes, in certain cases, to set

bespoke premiums for large corporate health insurance customers. The adequacy of pricing rests on thorough

actuarial analysis of past and most recent claims levels, combined with forward projections of the most recent

observed trends. Pricing risk affects only future cash flows since new tariffs impact on levels of premium earned

when health insurance contracts renew.

The Company’s dominant product style is of an annually renewable health insurance contract. The annual

renewability feature permits tariff revisions to be made in response to changes in claim experience. This is a

significant mitigant to pricing risk. The Company underwrites no material business that commits it to cover risks at

premiums fixed beyond a twelve month period from inception or renewal.

Claims risk

Claims risk is the risk of failure to manage BINS exposure to claims inflation and fluctuations in claims leading to

losses. This can be driven by an adverse fluctuation in the amount and incidence of claims incurred, higher than

expected future claims on existing policies, and external factors such as medical inflation.

Claims risk is managed and controlled by means of pre-authorisation of claims, outpatient benefit limits, the use of

consultant networks and agreed networks of hospitals and charges.

Specific claims management processes vary across the Company depending on local conditions and practice.

Generally, the Company’s health insurance contracts contain terms and conditions that provide for the

reimbursement of incurred medical expenses for treatment related to acute medical conditions. The contracts do

22

Bupa Insurance Limited Solvency and Financial Condition Report 2016

not provide for capital sums or indemnified amounts. Therefore claims experience is necessarily underpinned by

prevailing rates of illness. Additionally, claims risk is generally mitigated by the Company running control

processes to ensure that both the treatments and the consequent reimbursements are appropriate.

Reserving risk

Reserving risk is the risk that technical provisions for claims incurred prove to be insufficient in light of later events

and claims experience. There is a relatively low exposure to reserving risk due to the short-term nature of claims

development patterns. The short-tail nature of the Company’s insurance contracts means that movements in

claims development assumptions are generally not significant. The development patterns are kept under constant

review to maintain the validity of the assumptions and hence, the validity of the estimation of recognised technical

provisions.

The amount of claims provision at any given time that relates to potential claims payments that have not been

resolved within one year is not material. Also, of the small provisions that do relate to longer than one year, it is

possible to predict with reasonable confidence the outstanding amounts.

Other risks related to underwriting health insurance business

Claims provisions are not discounted. The premiums provisions are discounted but their short-term nature means

that changes in interest rates have no material impact on reserving risk. In addition, the future premium income

and claims outflows of health insurance premium liabilities are not affected directly by changes in interest rates.

However, changes to inflationary factors such as wage inflation and medical provider cost inflation can affect the

financial soundness of health insurance business.

The Company only uses reinsurance in selected circumstances. Reinsurance contracts give rise to credit risk

which is described further in section C.3.

Concentrations of risk

Although the majority of the Company’s activities are single line health portfolios, the Company does not have

significant concentrations of insurance risk for the following reasons:

Product diversity between domestic PMI and expatriate IPMI, and individual and corporate health insurance.

A variety of claims type exposures across diverse medical providers - consultants, nursing staff, clinics,

individual hospitals and hospital groups.

The Company is exposed to the risk that a single event occurs in a location which would result in a large number

of claims. This is mitigated by writing a diverse portfolio of business, in particular group policies, both within and

across geographies.

Catastrophe risk

Either a natural disaster or a man-made disaster could potentially lead to a large number of claims and thus

higher than expected claims costs. In the majority of jurisdictions BINS is not liable for claims relating to these

risks. Bupa’s Centre Risk function oversees the risk management of this risk exposure, and Bupa’s Centre

Actuarial function oversees and implements strategic improvements to ensure overall adequacy of these

arrangements.

Underwriting risk sensitivity

For the year ended 31 December 2016 a £23m increase in claims would have resulted in a 1% increase in the

loss ratio and a reduction in the solvency coverage ratio from 160% to 151%.

C.2 Market risk

Market risk is the risk of adverse financial impact due to changes in fair values of financial instruments, arising

from fluctuations in interest rates, foreign exchange rates, commodity prices, credit spread and equity prices. The

focus of the Company’s long-term financial strategy is to facilitate growth without undue balance sheet risk.

23

Bupa Insurance Limited Solvency and Financial Condition Report 2016

The Company actively manages price risk by ensuring that the majority of its cash and investments is held with

highly rated credit institutions. For the portion of surplus cash invested in a limited portfolio of return seeking

assets (principally corporate bonds and loans), the Company uses a value at risk analysis to quantify risk, taking

account of asset volatility and correlation between asset classes. At year end 2016 BINS had loan assets of £66m

on its Solvency II balance sheet, primarily reflecting its investments in a loans portfolio as part of its return seeking

assets. The loans portfolio is managed by an external fund manager under an investment management

agreement set by BINS.

The approach to investment decision making is governed by the Board and its Investment Committee. The Board

determines the overall investment risk appetite for BINS which is articulated through the risk parameters

contained in the Treasury Policy and its Statement of Investment Principles. BINS’ Investment Committee is

responsible for setting the investment strategy and asset allocation, within the Board approved investment risk

appetite and the Treasury Policy. The day to day management of BINS’ financial investments is done by the

Group’s Centre Treasury function.

Foreign exchange risk

The Company is exposed to foreign exchange risks arising from commercial transactions and from recognising

assets, liabilities and investments in overseas operations. The majority of the foreign exchange exposures arise in

the IPMI business as a result of trading in non-sterling currencies. The IPMI business receives premiums in US

dollar and euro as well as sterling. Claims are primarily paid in these currencies but also in a range of other

currencies such as UAE dirham, South African rand, Hong Kong dollar and Singapore dollar.

In order to reduce the foreign exchange exposure generated by the IPMI business the Company has a hedging

programme in place to manage a large proportion of its material foreign currency economic balance sheet

exposures. This seeks to reduce the impact of foreign exchange risk on the Company’s economic balance sheet

and its capital position.

Interest rate risk

Interest rate risk is the risk that the fair value of future cash flows of a financial instrument will fluctuate because of

changes in market interest rates.

The Company is exposed to interest rate risk arising from fluctuations in market rates. This affects the return on

floating rate assets and the balance sheet value of its investment in fixed rate bonds. The Company’s interest rate

duration is agreed by the Investment Committee as part of strategic asset allocation, taking into account the short

interest rate duration of the Company’s liabilities and its investment risk appetite.

The Company’s sole interest bearing financial liability is the £330m subordinated loan from Bupa Finance Plc,

which is treated as capital under Solvency II reporting. This is a fixed interest liability which has no repayment

date, but BINS has an option to call it in 2020. If BINS does not exercise the call option, the interest rate will be

reset in 2020.

Market risk sensitivities

The following analysis shows the relative sensitivities of the Company’s estimated solvency coverage ratio as at

31 December 2016 to a variety of market conditions. These sensitivities are all independent stresses to a single

risk and do not take into account management actions or represent the Company’s expectation of future market

conditions.

Sensitivity analysis Coverage ratio post stress

Base case solvency coverage ratio 160%

Interest rate +/-100bps 160%

Credit spreads +100bps (assuming no credit transition) 160%

Equities market -20% 160%

Property values -10% 157%

Sterling appreciates by 10% 162%

24

Bupa Insurance Limited Solvency and Financial Condition Report 2016

Credit spreads are the differences between the risk free rates and the yields achieved on both corporate and

sovereign bonds.

Interest rate and credit spread sensitivities do not impact the solvency coverage ratio materially due to the strong

matching of assets and liabilities and the fact that investments are held with highly rated credit institutions.

C.3 Credit risk

Credit risk is the risk that the Company will suffer a financial loss as a result of a counterparty failing to meet all or

part of their contractual obligations. Bupa’s Centre Treasury function manages the Company’s credit risk under

the guidance of the Investment Committee.

Investment exposure with external counterparties is managed by ensuring there is a sufficient spread of

investments and that all counterparties are rated at least A by two of the three key rating agencies used by the

Company (unless specifically approved by the Investment Committee). Other factors are also considered

including credit default swap levels and counterparty specific information. All rating movements are reported to the

Investment Committee, which reviews the suitability of the counterparty for continued investment.

C.4 Liquidity risk

Liquidity risk is the risk that the Company will not have available funds to meet its liabilities when they fall due.

The Company’s liquidity risk is addressed by holding liquid assets and through controls.

The Company enjoys a strong liquidity position and adheres to strict liquidity management policies as set by its

Investment Committee. The liquidity management policy is reviewed at least annually.

Liquidity is managed by currency and by considering the segregation of accounts required for regulatory

purposes.

Expected profit included in future premiums

Under Solvency II, expected profit included in future premiums is included in Own Funds, recognised in the

calculation of technical provisions. Expected profit included in future premiums does not form part of the liquidity

position as 31 December, but is taken into consideration when assessing the Company’s future liquidity. Expected

profit included in future premiums amounted to £129m at 31 December 2016 (31 December 2015: £112m).

C.5 Operational risk

Operational risk is the risk of loss arising from inadequate or failed internal processes, or from personnel, systems

or external events. This includes conduct risk which is the risk that BINS’ behaviour or actions result in unfair

outcomes or detriment for customers.

The Company is committed to managing operational risk effectively. This includes continued close attention to

management of regulatory risk and proactive engagement with regulators. Maintenance of robust internal control

processes and governance frameworks, the approval of risk policies, and the assessment of compliance help

mitigate this risk.

The services provided by the Company are underpinned by information technology systems and infrastructure

that enable the delivery of core processes and products. Failure of these systems may reduce the ability of the

Company to deliver products and services to its customer base or increase the risk of information security

breaches.

The Company’s information technology services are provided by BISL, which has dedicated information

technology teams responsible for the development, maintenance and monitoring of information technology

services.

25

Bupa Insurance Limited Solvency and Financial Condition Report 2016

The Company has detailed business continuity plans for all businesses with dedicated specialised resource in

place to ensure appropriate operation of key processes and controls. Business continuity issues are reported to

the RE ERC, with significant issues being escalated to the RERC, which is responsible for ensuring appropriate

controls are in place to mitigate potential risks. As a result of the governance structures and controls in place,

there was no significant business disruption event during 2016.

Operational Risk does not lend itself to sensitivity analysis. Operational risk scenario analysis exercises are

conducted to provide an understanding of the specific risks that BINS faces on a daily basis, the likelihood of them

occurring and the severity of the impact if they were to occur. This understanding allows for a more focused

allocation of resources targeted at mitigating or controlling the more material exposures.

C.6 Other material risks

The Company is also exposed to strategic risk, being the risk of an inability to design or implement appropriate

business plans and strategies, make decisions, allocate resources, or adapt to changes in the business

environment. The political and economic backdrop to BINS’ business is uncertain, with powerful global social

trends. Populations are ageing, public health solutions are continuously evolving, governments are facing funding

issues in healthcare and aged care, and competition is intense, both from traditional and non-traditional players.

In order to effectively manage strategic risk, the Company has refreshed its strategy, and remains focused on

delivering great customer outcomes and long-term profitable growth. Through the identification and assessment of

emerging risks the Board is able to react to issues in a timely and appropriate manner.

C.7 Any other information

C.7.1 Prudent person principle

BINS investments operate in accordance with the prudent person principle. BINS approach to investment is as

follows:

The Board is responsible for setting the overall investment risk appetite for BINS which is articulated through

the risk parameters contained in the Treasury Policy and its Statement of Investment Principles. The Board

approves the expected investment return as part of the annual operating plan process and monitors

investment performance against plan on a monthly basis.

The BINS Investment Committee is responsible for setting investment strategy and asset allocation, within the