1 SHAREHOLDER MANAGEMENT MODEL: STATUS REPORT & WAY FORWARD PRESENTATION TO PORTFOLIO COMMITTEE ON...

25

1 SHAREHOLDER MANAGEMENT MODEL: STATUS REPORT & WAY FORWARD PRESENTATION TO PORTFOLIO COMMITTEE ON PUBLIC ENTERPRISES 07 JUNE 2006

-

Upload

felix-walters -

Category

Documents

-

view

218 -

download

2

Transcript of 1 SHAREHOLDER MANAGEMENT MODEL: STATUS REPORT & WAY FORWARD PRESENTATION TO PORTFOLIO COMMITTEE ON...

1

SHAREHOLDER MANAGEMENT MODEL:STATUS REPORT & WAY FORWARD

PRESENTATION TO PORTFOLIO COMMITTEE ON PUBLIC ENTERPRISES

07 JUNE 2006

2

Outline of Presentation• SOE context• Shareholder Management: Historical• Shareholder Management: Current• Rationale for SOE• Current Classification• Strategic Intent• Shareholder Reserved Rights• Board Appointment & Remuneration• Accountability to Parliament• Planning & Reporting Schedule• Shareholder Status & Capacity• Shareholder Management Model• Process Forward

3

SOE contextCOMPANIES IN GENERAL

COMPANIES ACT

MEMORANDUM OF ASSOCIATION (company specific founding document, basis for corporate structure, nature & scope of company, exclusion of powers

ARTICLES OF ASSOCIATION (company specific, sub-ordinate to MoA, rights, duties & powers of shareholders, directors & AGM, manner in which affairs are to be managed & administered

+

STATE OWNED ENTERPRISES

CONSTITUTION (individual & collective accountability of Members of the Cabinet to Parliament)

PUBLIC FINANCE MANAGEMENT ACT (PFMA) (transparency, accountability & sound management of revenue, expenditure, assets & liabilities of eg. Public Entities

ENABLING LEGISLATION (not required and not provided in all cases, served to corporatize SOEs & define powers, functions & duties)

4

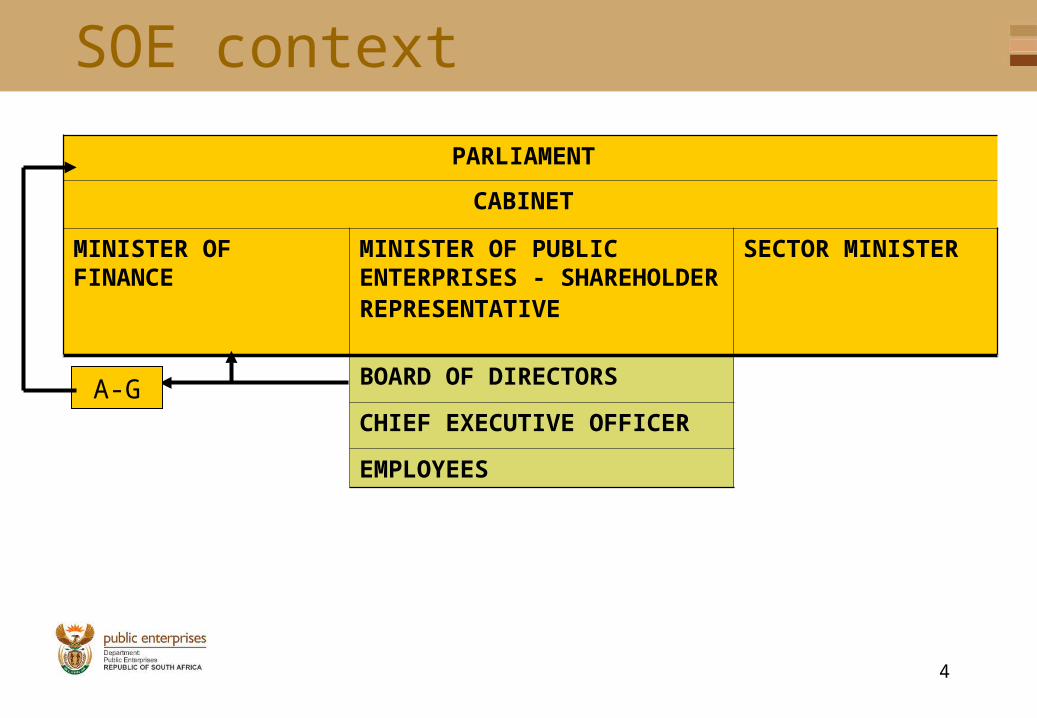

SOE context

PARLIAMENT

CABINET

MINISTER OF FINANCE

MINISTER OF PUBLIC ENTERPRISES - SHAREHOLDER REPRESENTATIVE

SECTOR MINISTER

BOARD OF DIRECTORS

CHIEF EXECUTIVE OFFICER

EMPLOYEES

A-G

5

Shareholder Management: Historical • Historical perspective:

– Parastatal era: no shareholder-enterprise distinction, exclusive state ownership, governance (performance management & accountability) weak, unaccountable interference by executive

– Corporatization era: shareholder-enterprise role distinction & corporate governance introduced but slow assumption of shareholder control rights & loss of mechanisms to align commercial direction with strategic intent of the state

– PFMA era: mainly focused at improvement in financial management (accountability & sound management of revenue, expenditure, assets & liabilities)

– Privatization of some enterprises: different models ranging from complete privatization to minority shareholding by the state (eg Aventura, Safcol, Telkom); strategic interest of state not always aligned with corporate structure

6

Shareholder Management: Current

• Challenge is focused at shareholder empowerment:– Rationale for state ownership– Classification of SOE– Definition of state’s intent with shareholding in an SOE & transparent

communication of intent– Definition of shareholder reserved decision-making & Updating Shareholder

Agreements, Memoranda & Articles– Alignment of Board of Directors composition & remuneration with enterprise

mandate– Improvement of Board accountability – Improved accountability to Parliament– Integrity of reporting & decision-making at shareholder & enterprise level– Status & capacity of shareholder oversight entities

7

Rationale for SOE

• Natural Monopoly• Market Failure• Developmental requirements

Where shareholding is purely for financial returns consideration may be given to shareholding via vehicles such as IDC or disposal

8

Current Classification • PFMA classification of “public entities” with reference to:

– Definition of “public entities” & “national/ provincial government business enterprises”; and

– Schedule listing.• PFMA listing:

– Schedule 2: Major Public Entities & “ownership control” subsidiaries; all DPE-SOE are Schedule 2 entities; ownership control subsidiaries at least 20 (overall about 40 subsidiaries)

– Schedule 3A: National Public Entities– Schedule 3B: National Business Enterprises– Schedule 3C: Provincial Public Entities– Schedule 3D: Provincial Business Enterprises

• No definition of major public entity, but characteristics match definition of “national government business enterprise”

• “national government business enterprise” – Juristic person (company) under ownership control of national executive– Operational & financial authority to carry on business activity– Provides goods & services according to ordinary business principles– Financed fully or substantially from sources other than Nat. Revenue Fund,

taxes or other statutory money

9

Current Classification• “ownership control”

– Appoint/remove all or majority of directors;– Appoint/remove CEO;– Cast all or majority votes at board meetings; or– Control all or majority votes at general meetings.

• “National public entities”: Board, commission, corporation, fund or other entity:– Established in terms of national legislation;– Fully or substantially funded from Nat. Revenue Fund, taxes or statutory money– Accountable to Parliament

• Distinct difference between national public entities & national government business enterprise: sources of funding

• Difference between Schedule 2 and 3B in practice: Schedule 3B entities are generally more dependent on national revenue fund, tax or statutory money

10

Classification - conclusion

• Current classification of SOE in terms of PFMA is potentially confusing and directly linked to the financial management objectives of the PFMA– No definition of major public enterprises– Schedule 2 (major public entities) and Schedule 3B (national government

business enterprises) possibly same definition• DPSA re-classification model distinguishes between Government Business

(departments, government agencies & public entities) and Government Enterprises

• Government Business Enterprises further classified as State Corporations and State Owned Enterprises (difference whether established by own legislation)

• Classification of Government Business Enterprises require further refinement and simplification to include all state strategic interest but distinction between ownership control and reporting & accountability requirements in relation to shareholding & reserved rights

• Considering distinction between State Owned Enterprises & State Reporting Entities

• New classification model and distinguished oversight to be empowered through SOE legislation and amendment to PFMA

11

Strategic Intent• Performance targets of SOE are determined in absence of

communication of strategic intent• Strategic Intent = economic return to be achieved• DPE developed strategic intent statements for all SOE • Mechanisms being considered to instruct strategic intent in a

transparent & accountable manner, eg. “ministerial charter/ strategic intent obligation” to be published in Gazette

• Legislative mandate required• Enterprise performance targets to be aligned with strategic intent

12

Shareholder Reserved Rights• Companies Act provides for standard reserve rights such as approval of

Annual Financial Statements, dividends, appointment of directors• In addition, reserved rights over and above rights in terms of the

Companies Act and/or in relation to shareholding are secured through PFMA and possibly shareholders agreements, Memoranda & Articles

• In the case of 100% state shareholding the key issue is the decision-making parameters of the Board vis-à-vis the shareholder; PFMA currently reserves shareholder decision-making rights in relation to:– borrowing powers– significant & material transactions– establishment of subsidiaries

• PFMA reserved rights require further precisioning with reference to significance & materiality (dileneation of Board & shareholder authority”), procedures and criteria for exercising such rights

13

Shareholder Reserved Rights• Where the state is a minority shareholder, the reserved rights relate to

both the parameters of decision-making of the Board and other shareholders; examples of latter include rights to:– Appoint Chairperson & CEO– Decisions on capital investment– Control management contracts based on performance– Call options for shares if performance targets not met (eg. Investment &

service delivery)– Pre-emptive rights to purchase shares– Material disposals, acquisitions & mergers– Ownership of intellectual property

14

Shareholder Reserved Rights• Interventions to improve definition & exercise of shareholder reserved

rights:– Significance & materiality, criteria, format & process guidelines for

transactions (done)– Guidelines for borrowing powers (working with NT towards a guideline)– National Treasury Regulations already specify requirements for

establishment of subsidiaries - DPE is developing guidelines for shareholders agreements as well as Memoranda & Articles to supplement the requirements

– Dividend policy: NT developing in consultation with DPE– Board appointments – see next slide

15

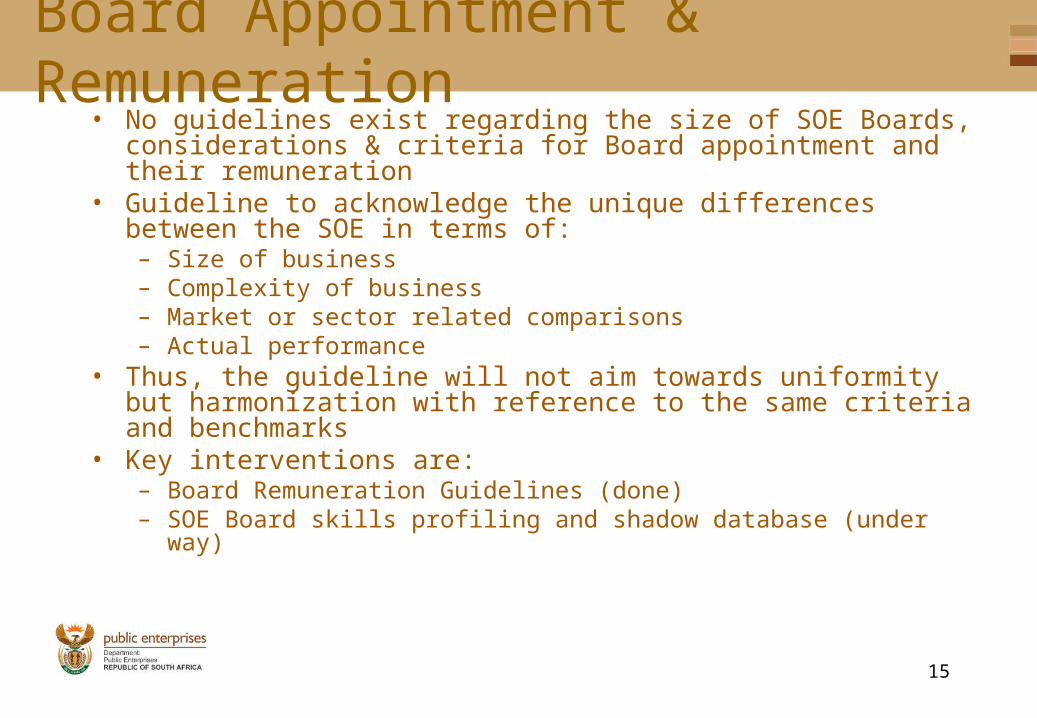

Board Appointment & Remuneration• No guidelines exist regarding the size of SOE Boards, considerations &

criteria for Board appointment and their remuneration• Guideline to acknowledge the unique differences between the SOE in

terms of:– Size of business– Complexity of business– Market or sector related comparisons– Actual performance

• Thus, the guideline will not aim towards uniformity but harmonization with reference to the same criteria and benchmarks

• Key interventions are:– Board Remuneration Guidelines (done)– SOE Board skills profiling and shadow database (under way)

16

Board Accountability • Current mechanisms to communicate performance areas & targets not

effective:– Corporate Plan: PFMA requires submission but not approval– Shareholder Compacts: annual (short-term) instruments requiring

rationalization & harmonization – Quarterly Reports– Annual General Meetings: agenda mainly focused to ensure

compliance with statutory obligations in terms of Companies Act: annual financial statements, dividends, appointment & remuneration of directors

• Direct reference to strategic intent is absent & consistent flow of integrity of reporting from Corporate Plans – Shareholder Compacts – Quarterly Reports & Annual General Meeting lacking

17

Board Accountability

• Key interventions:– Draft Corporate Plans be required for comment & final plans be

approved by shareholder – corporate plans to focus on end of 3-year performance targets within framework of strategic intent

– Annual Shareholder Compacts to focus on annual targets within framework of 3-year plan

– Quarterly Reports to focus on demonstrating that SOE is on track to meet annual & 3-year targets

– Strategic Planning general meeting with Board scheduled after the AGM to convey expectations of the shareholder for the preparation of the Corporate Plan for the next year

– Board Induction Programme

18

Accountability to Parliament • Accountability through submission of Annual Financial Statements &

Annual Report (retrospective assessment)• Submission of Shareholder Compacts considered (forward looking

expectation & benchmark for assessing achievement with reference to Annual Financial Statements & Annual Report)

• Publication of strategic intent & submission of Shareholder Compact to Parliament should improve the integrity flow of reporting on performance

19

Planning & Reporting ScheduleJ F M A M J J A S O N D

CorpPlan

End

Fin Year

Start

Fin

Year

Annual

Fin. Statement & Annual

Report to Executive Authority

Annual

Fin. Statement & Annual

Report to Parliament

Annual General Meetings

1st Quarter

Report

2nd

Quarter

Report

3rd

Quarter Report

4th

Quarter Report

Shareholder Compact

20

Planning & Reporting Schedule (future)J F M A M J J A S O N D

Draft

Corp.

Plan

Corp.

Plan

Approved

End

Fin

Year

New

Fin Year

Annual General Meetings

AFS &

Annual

Report to EA

AFS & Annual Report of previous financial year AND Shareholder Compacts of current year to Parliament

Strategic Intent Meetings with

Boards

Shareholder

Compacts

1st Quarter

Report

2nd Quarter

Report

3rd Quarter Report

4th Quarter

Report

21

Shareholder Status & Capacity • Lack of intra-governmental role & function definition (policy makers/

regulators/ shareholders) increases oversight challenge of shareholder departments especially in case of natural monopolies: enterprise level, industry & sector level efficiencies often blurred

• Concurrency & convergence of jurisdiction within government to be clarified to avoid duplication & improve intra-governmental coordination

• Asymmetry of information generation & availability and resources between SOE & shareholder departments constrains effective oversight

• Developing conceptual framework for government-wide shareholder management and to serve as drafting framework for SOE legislation & recommendations for PFMA amendment

• DPE function shares some characteristics of a holding company profile – proposals being developed to improve oversight balance

• Within DPE developing governance workflow

22

Shareholder Management Model• Shareholder Management = combination of people/entities, legal rules,

management tools & process and healthy personal relationships

• Managing Relationships:– Other shareholders– Board of Directors – Parliament– Intra-Governmental Objectives

• In terms of Rights & Duties:– Constitution– Public Finance Management Act (PFMA) & National Treasury Regulations (NTR)– Companies Act & Regulations– Founding document: Memorandum of Association (Memorandum)– Contract between Shareholders and Board on respective rights & duties: Articles of

Association (Articles) for example reserved shareholder decision-making– Agreement between shareholders on their respective rights & duties: Shareholders

Agreement (SHA) for example minority shareholder rights (golden shareholding)

23

Shareholder Management Model• Applying Effective Performance Management Tools:

– Corporate Plan– Quarterly Reports– Shareholder Compacts– Annual Financial Statements– Annual Reports

• Through:– clear & transparent instruction – Integrity of information– Informed decision-making

• Within statutory time-frames

APPROACH IS NOT TO RE-INVENT BUT TO STRENGTHEN EXISTING RIGHTS & DUTIES THROUGH CLEARER DEFINITION OF INTENT & ACCOUNTABILITY CHAIN

24

Process Forward1. Conceptual Framework to serve as basis for Government-wide

consultation2. Consultation within Government 3. Draft Legislation & implementation of reforms not requiring legislative

change

• Key aspects to be addressed in legislation– Classification– Strategic Intent Interventions with reference to types of entities– Mechanism to issue guidelines for consistency in approach to corporate

structure, SOE shareholder rights & performance monitoring & reporting– C-operative governance principles within Government– Reporting to Parliament

25

Thank you