1 Revenue Management Program (RMP) Campus Budget October 23 – 24, 2006.

36

1 Revenue Management Program (RMP) Campus Budget October 23 – 24, 2006

-

Upload

gyles-french -

Category

Documents

-

view

213 -

download

0

Transcript of 1 Revenue Management Program (RMP) Campus Budget October 23 – 24, 2006.

1

Revenue Management Program (RMP)Campus Budget

October 23 – 24, 2006

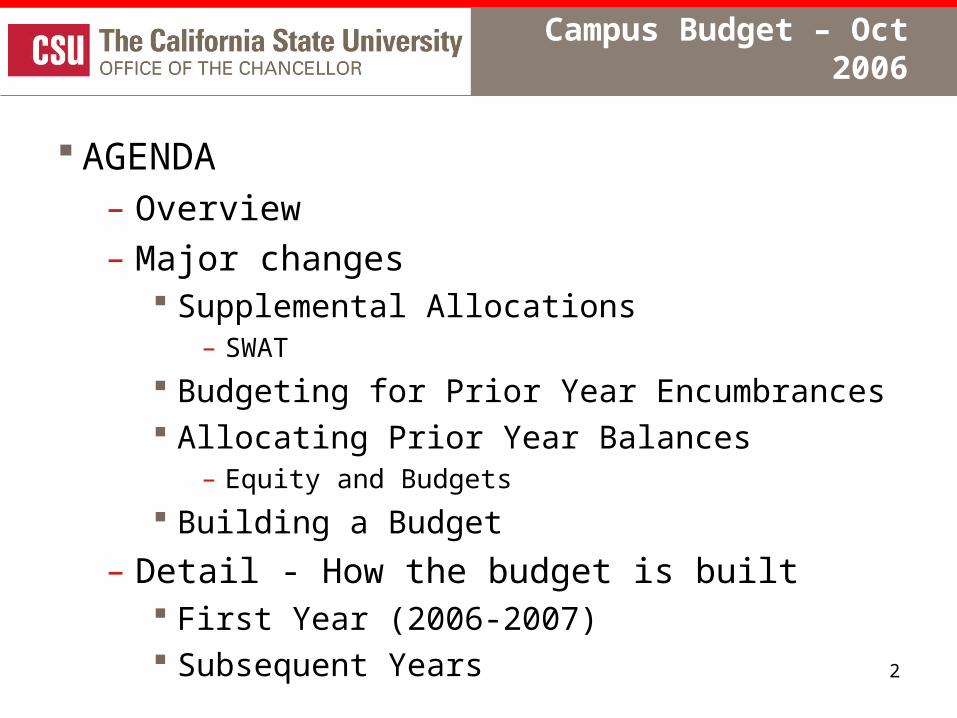

2

Campus Budget – Oct 2006

AGENDA– Overview

– Major changes Supplemental Allocations

– SWAT

Budgeting for Prior Year Encumbrances Allocating Prior Year Balances

– Equity and Budgets

Building a Budget

– Detail - How the budget is built First Year (2006-2007) Subsequent Years

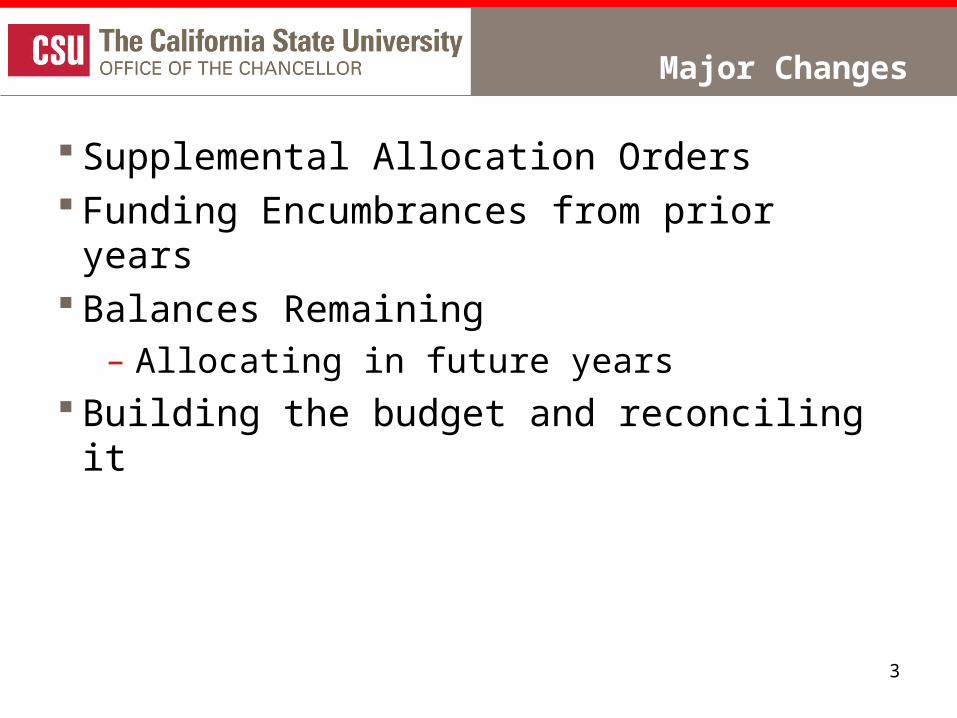

3

Major Changes

Supplemental Allocation Orders Funding Encumbrances from prior years Balances Remaining

– Allocating in future years Building the budget and reconciling it

4

Components of the “New” Campus Budget

General Fund state support Campus Estimated Revenue Supplemental Funds Received (SWAT) Equity Reserve for Prior Period Encumbrances Equity Reserve for “Roll Forward” funds Campus planned use of Unallocated Equity or

Campus planned contribution to Unallocated Equity

5

Sample Budget Template

6

7

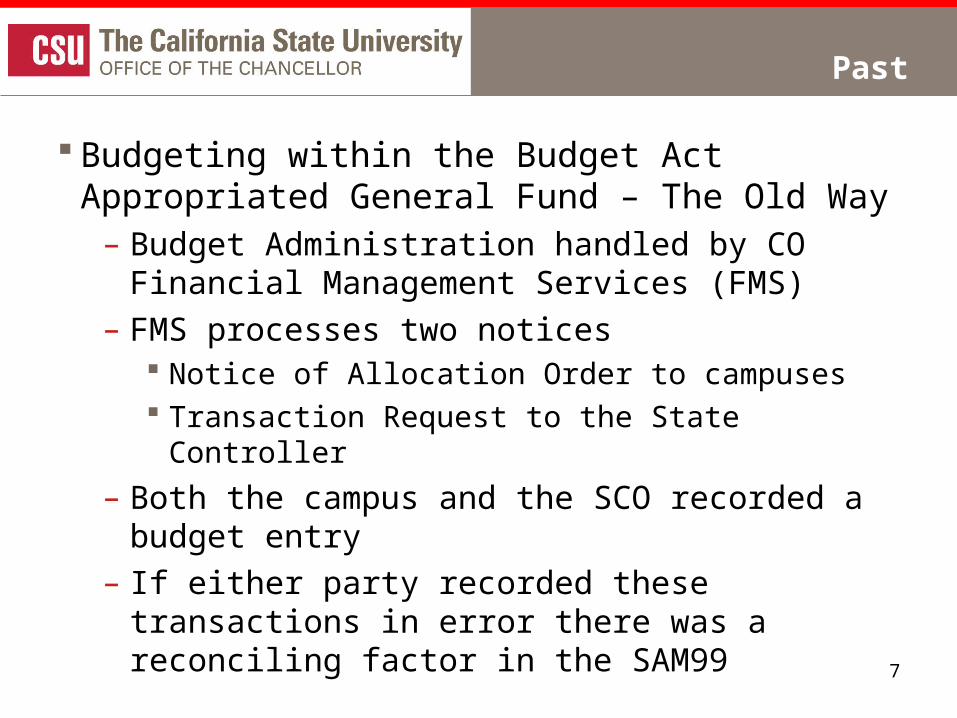

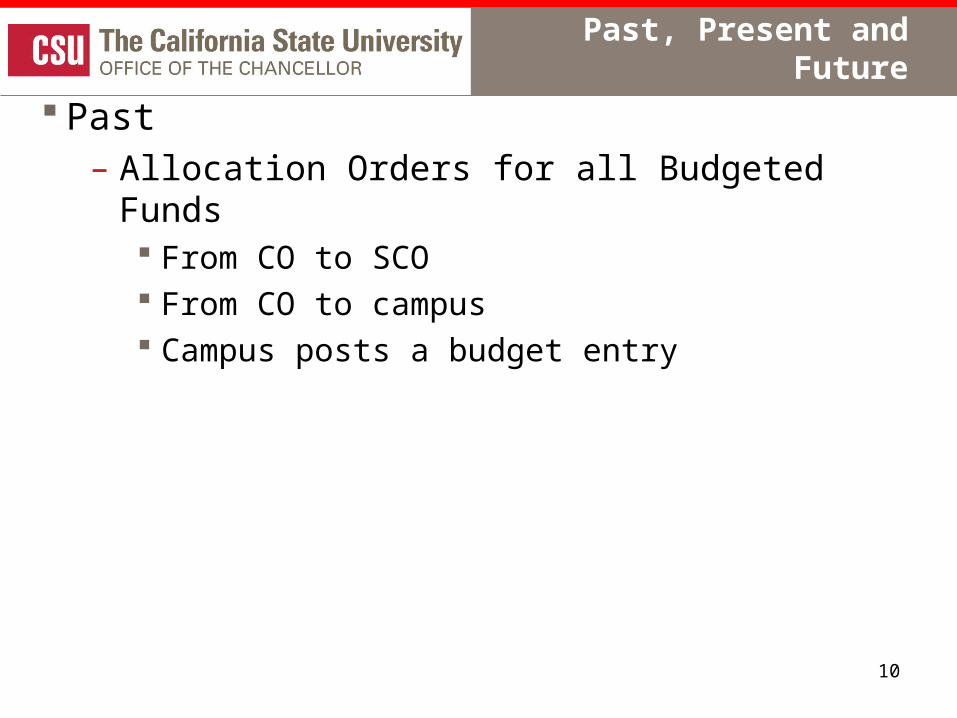

Past

Budgeting within the Budget Act Appropriated General Fund – The Old Way

– Budget Administration handled by CO Financial Management Services (FMS)

– FMS processes two notices Notice of Allocation Order to campuses Transaction Request to the State Controller

– Both the campus and the SCO recorded a budget entry

– If either party recorded these transactions in error there was a reconciling factor in the SAM99

8

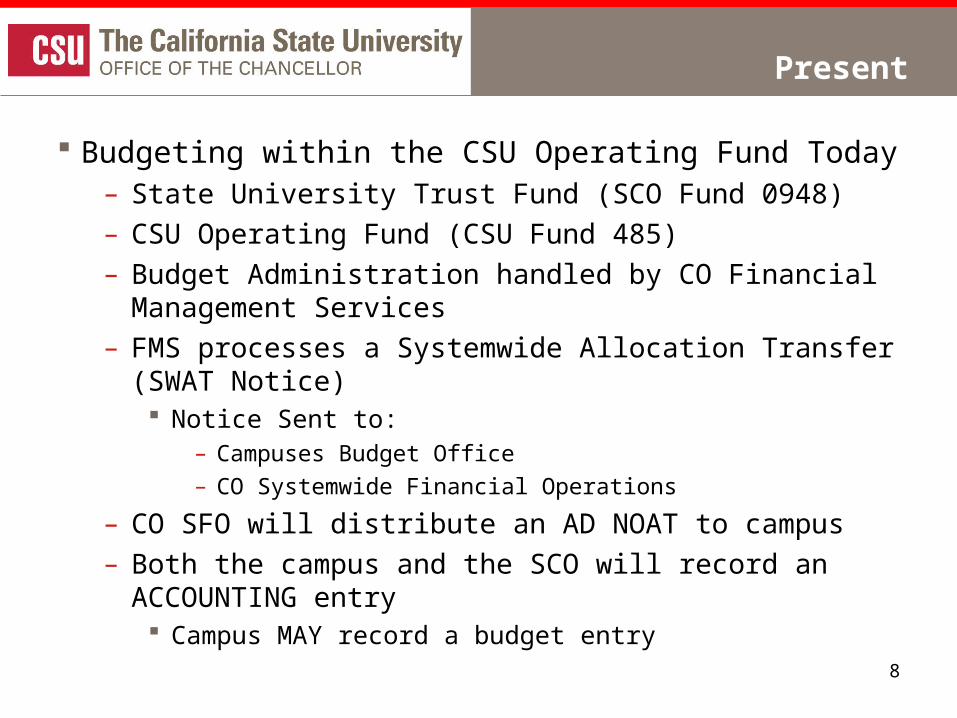

Present

Budgeting within the CSU Operating Fund Today– State University Trust Fund (SCO Fund 0948)

– CSU Operating Fund (CSU Fund 485)

– Budget Administration handled by CO Financial Management Services

– FMS processes a Systemwide Allocation Transfer (SWAT Notice) Notice Sent to:

– Campuses Budget Office

– CO Systemwide Financial Operations

– CO SFO will distribute an AD NOAT to campus

– Both the campus and the SCO will record an ACCOUNTING entry Campus MAY record a budget entry

9

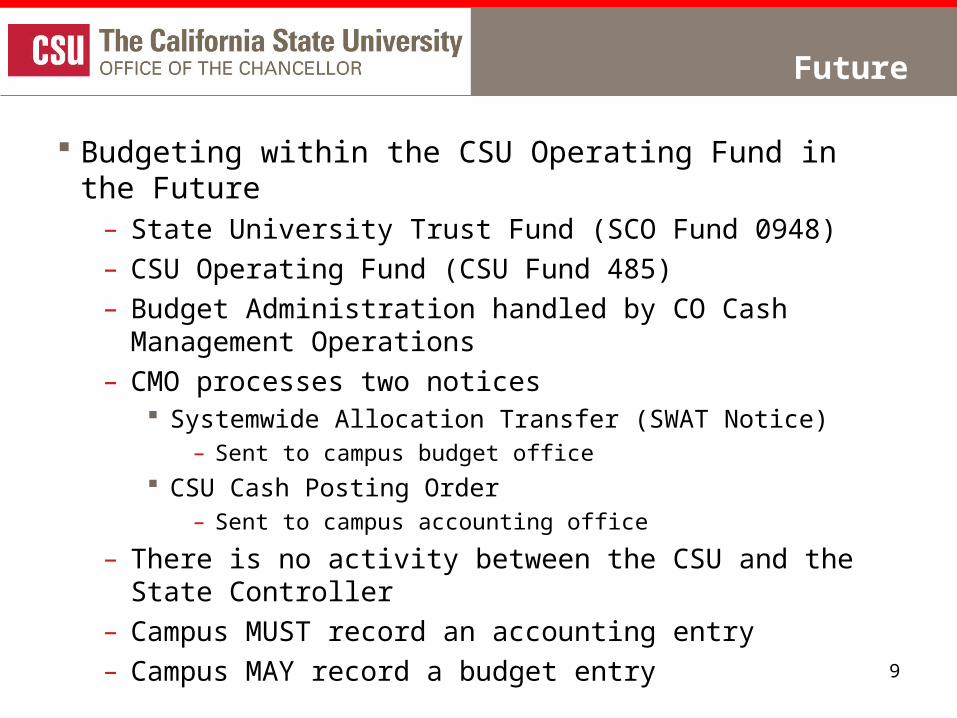

Future

Budgeting within the CSU Operating Fund in the Future – State University Trust Fund (SCO Fund 0948)

– CSU Operating Fund (CSU Fund 485)

– Budget Administration handled by CO Cash Management Operations

– CMO processes two notices Systemwide Allocation Transfer (SWAT Notice)

– Sent to campus budget office

CSU Cash Posting Order– Sent to campus accounting office

– There is no activity between the CSU and the State Controller

– Campus MUST record an accounting entry

– Campus MAY record a budget entry

10

Past, Present and Future

Past– Allocation Orders for all Budgeted Funds

From CO to SCO From CO to campus Campus posts a budget entry

11

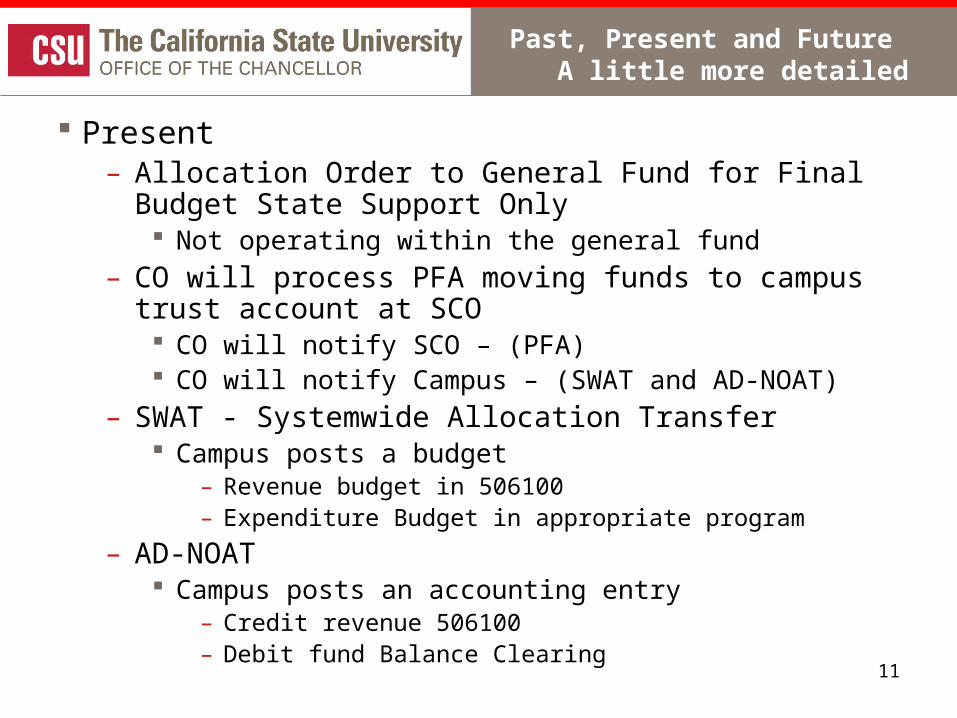

Past, Present and Future A little more detailed

Present– Allocation Order to General Fund for Final Budget State

Support Only Not operating within the general fund

– CO will process PFA moving funds to campus trust account at SCO CO will notify SCO – (PFA) CO will notify Campus – (SWAT and AD-NOAT)

– SWAT - Systemwide Allocation Transfer Campus posts a budget

– Revenue budget in 506100 – Expenditure Budget in appropriate program

– AD-NOAT Campus posts an accounting entry

– Credit revenue 506100– Debit fund Balance Clearing

12

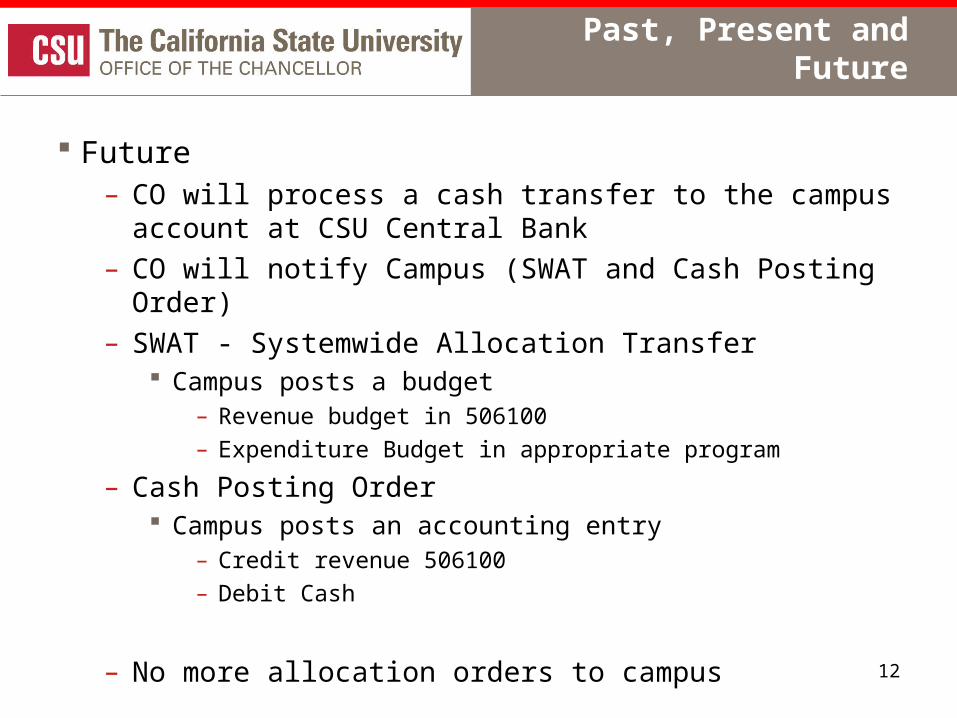

Past, Present and Future

Future– CO will process a cash transfer to the campus account at

CSU Central Bank

– CO will notify Campus (SWAT and Cash Posting Order)

– SWAT - Systemwide Allocation Transfer Campus posts a budget

– Revenue budget in 506100

– Expenditure Budget in appropriate program

– Cash Posting Order Campus posts an accounting entry

– Credit revenue 506100

– Debit Cash

– No more allocation orders to campus

13

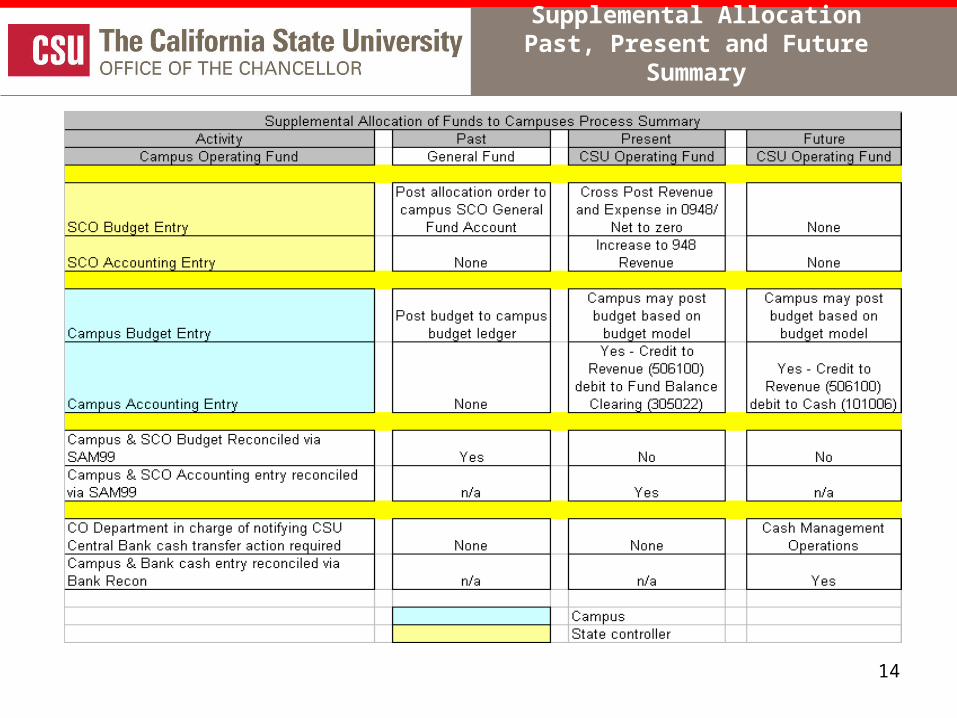

Supplemental AllocationPast, Present and Future Summary

14

Supplemental AllocationPast, Present and Future Summary

15

16

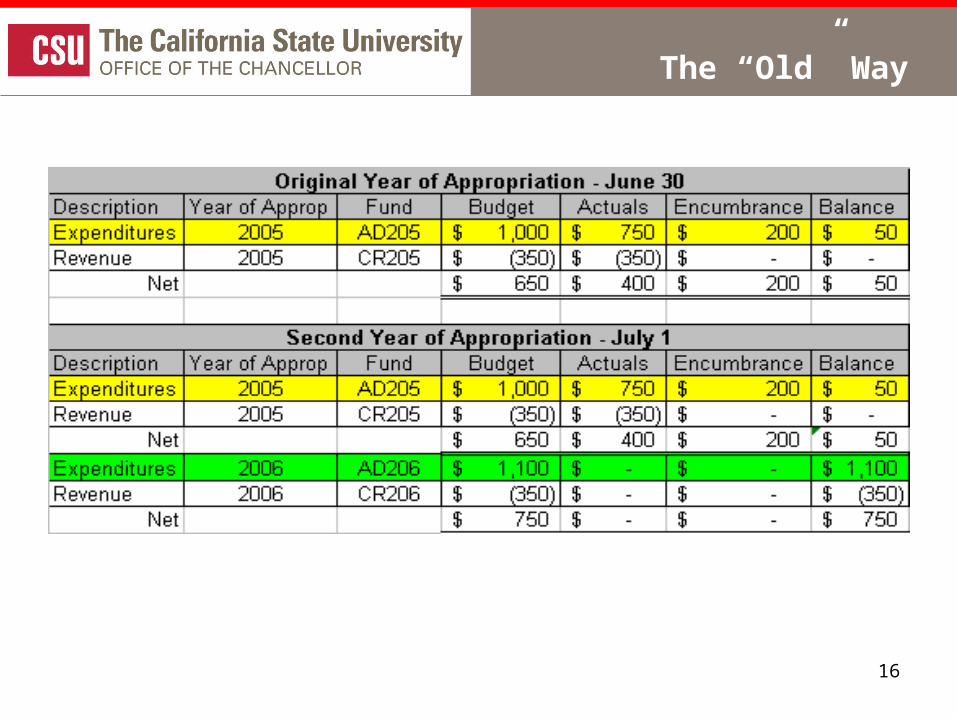

The “Old” Way

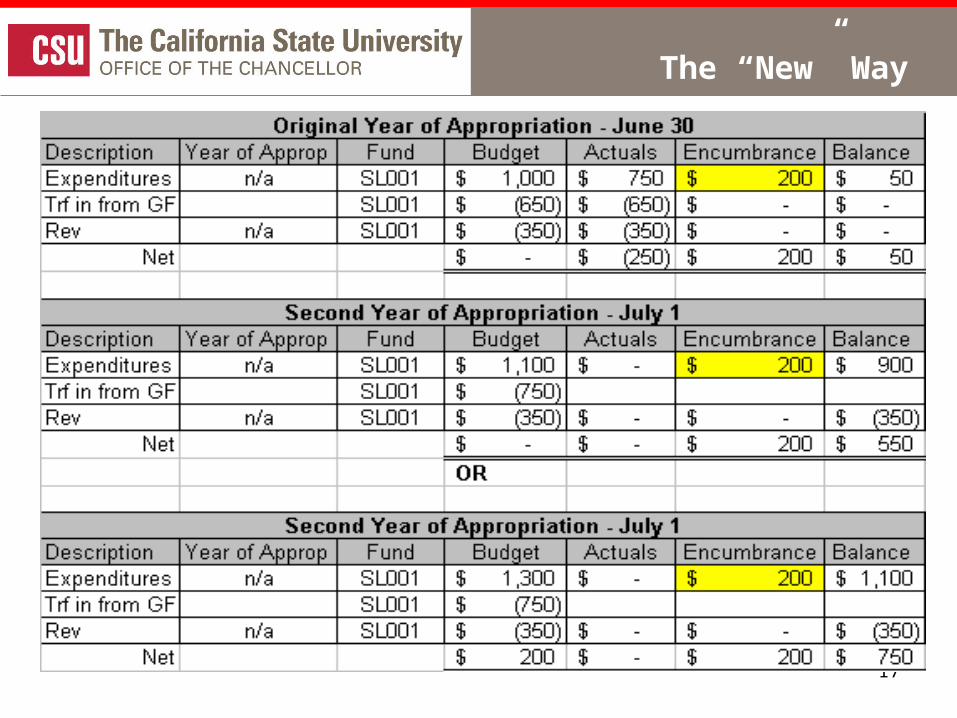

17

The “New” Way

18

19

20

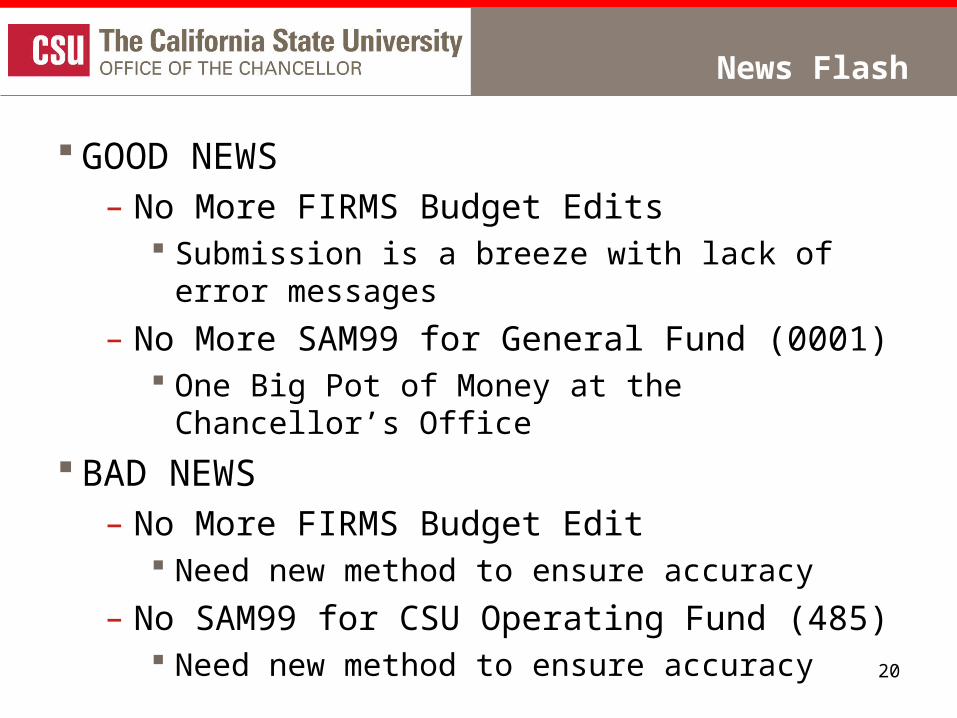

News Flash

GOOD NEWS– No More FIRMS Budget Edits

Submission is a breeze with lack of error messages

– No More SAM99 for General Fund (0001) One Big Pot of Money at the Chancellor’s Office

BAD NEWS– No More FIRMS Budget Edit

Need new method to ensure accuracy

– No SAM99 for CSU Operating Fund (485) Need new method to ensure accuracy

21

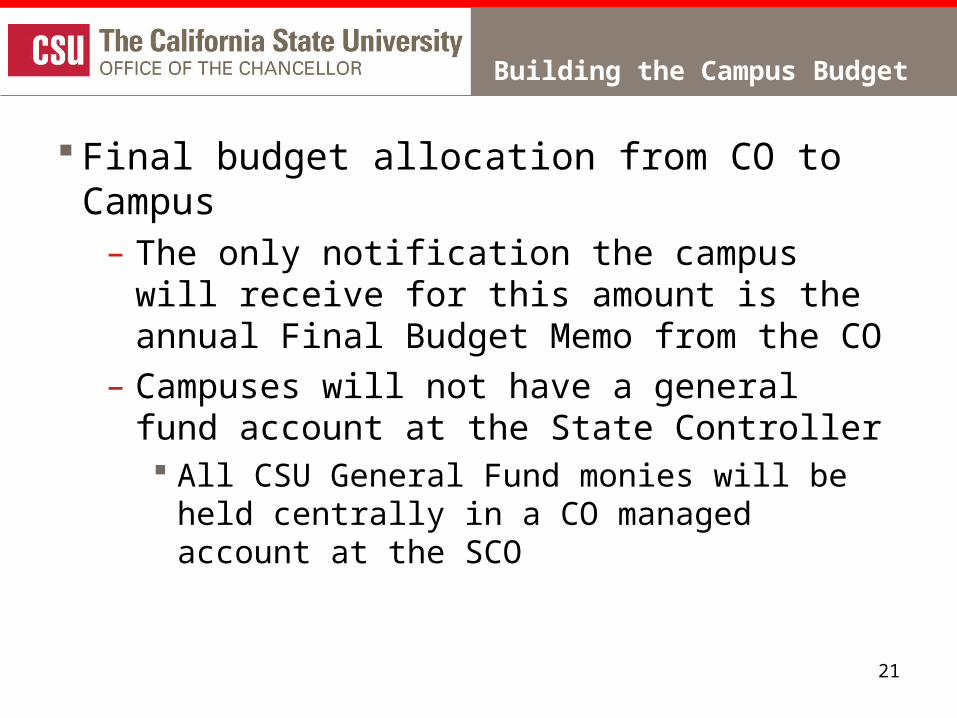

Building the Campus Budget

Final budget allocation from CO to Campus– The only notification the campus will receive for

this amount is the annual Final Budget Memo from the CO

– Campuses will not have a general fund account at the State Controller All CSU General Fund monies will be held centrally

in a CO managed account at the SCO

22

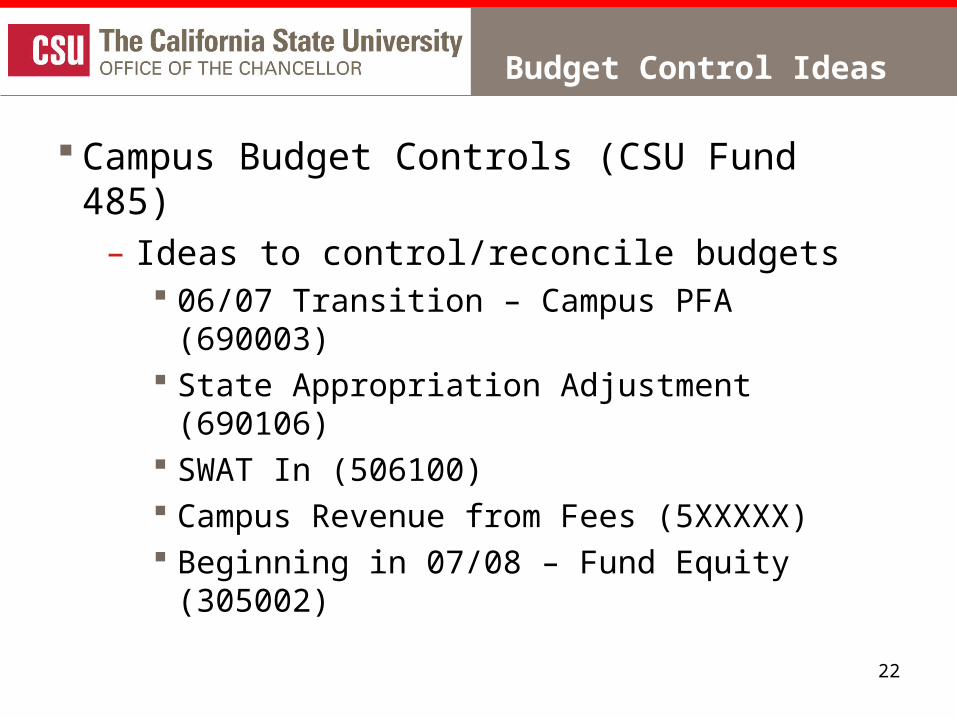

Budget Control Ideas

Campus Budget Controls (CSU Fund 485)– Ideas to control/reconcile budgets

06/07 Transition – Campus PFA (690003) State Appropriation Adjustment (690106) SWAT In (506100) Campus Revenue from Fees (5XXXXX) Beginning in 07/08 – Fund Equity (305002)

23

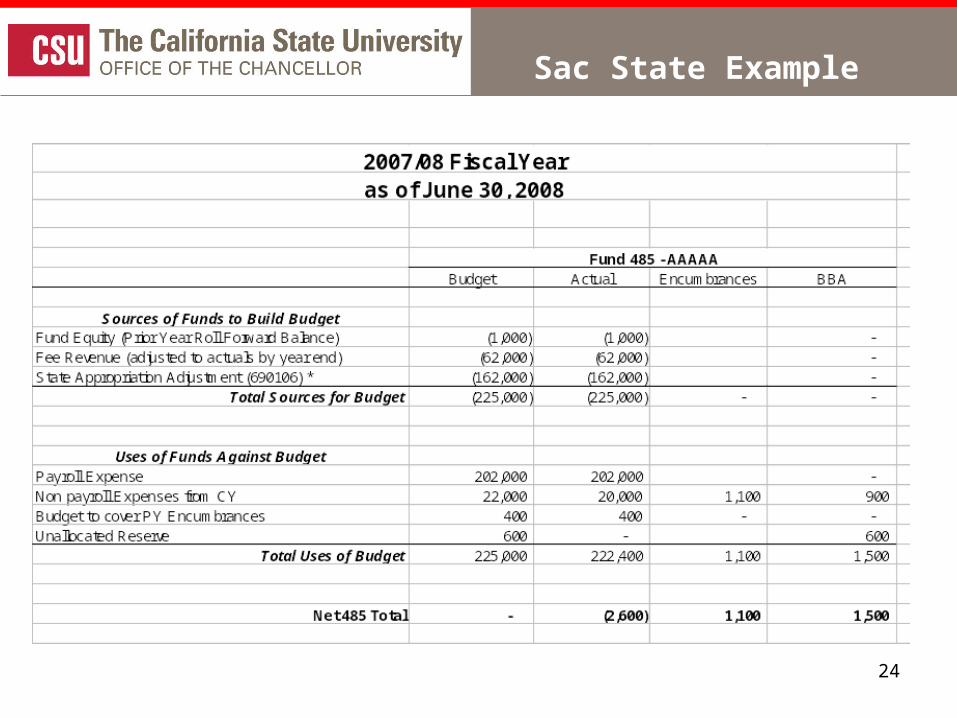

Sacramento State Example

SAM99 Budget Actual

Mgmt Budget Actual Encumb. BBA

Sources of Funds to Build BudgetCO Allocation Order AO#1-2006 153,000 - CO Allocation Order AO#1A-2006 4,000 - CO De-Allocation Order * (91,000) - Fee Revenue (60,000) (60,000) - State Appropriation Adjustment (690106) * (91,000) (91,000) -

Total Sources for Budget 66,000 - (151,000) (151,000) - -

Uses of Funds Against BudgetPayroll Expenses 198,000 198,000 - Transfer for Payroll before Central PFA (690003) 66,000 66,000 (66,000) (66,000) - Non payroll Expense 19,000 18,000 400 600

Total Uses of Budget 66,000 66,000 151,000 150,000 400 600

Net 485 Total - (1,000) 400 600

* State Appropriation Adjustment (Object Code 6901XX) = CO De-allocation Order Amount for this first transition year

Fund 001 Fund 485 - AAAAA

2006/07 Fiscal Yearas of June 30, 2007

24

Sac State Example

25

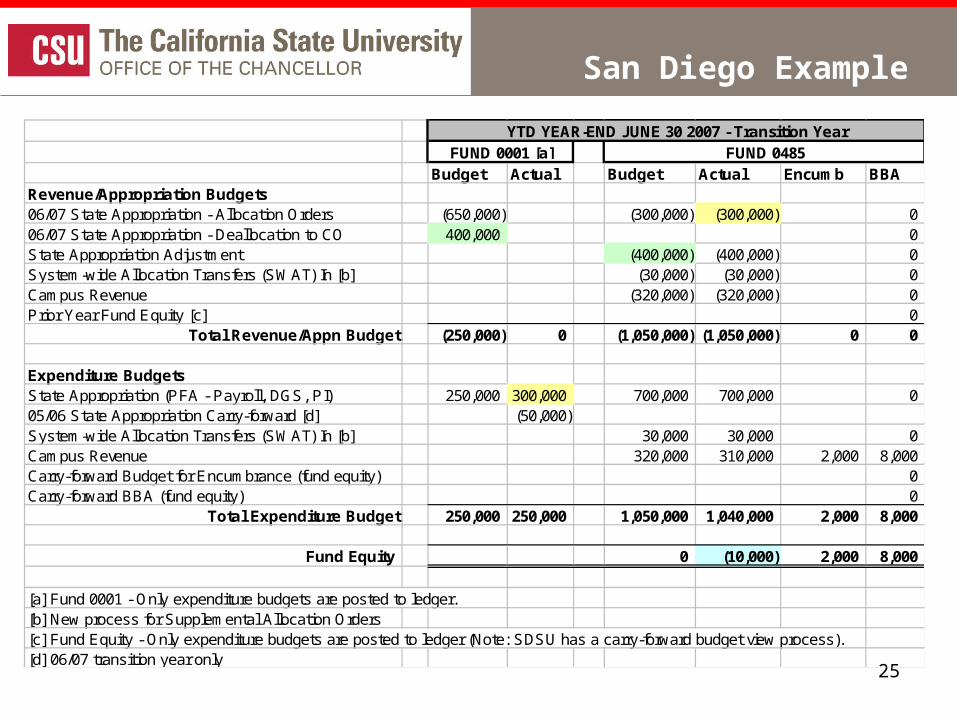

San Diego Example

Budget Actual Budget Actual Encumb BBARevenue/Appropriation Budgets06/07 State Appropriation - Allocation Orders (650,000) (300,000) (300,000) 006/07 State Appropriation - Deallocation to CO 400,000 0State Appropriation Adjustment (400,000) (400,000) 0System-wide Allocation Transfers (SWAT) In [b] (30,000) (30,000) 0Campus Revenue (320,000) (320,000) 0Prior Year Fund Equity [c] 0

Total Revenue/Appn Budget (250,000) 0 (1,050,000) (1,050,000) 0 0

Expenditure BudgetsState Appropriation (PFA - Payroll, DGS, PI) 250,000 300,000 700,000 700,000 005/06 State Appropriation Carry-forward [d] (50,000)System-wide Allocation Transfers (SWAT) In [b] 30,000 30,000 0Campus Revenue 320,000 310,000 2,000 8,000Carry-forward Budget for Encumbrance (fund equity) 0Carry-forward BBA (fund equity) 0

Total Expenditure Budget 250,000 250,000 1,050,000 1,040,000 2,000 8,000

Fund Equity 0 (10,000) 2,000 8,000

[a] Fund 0001 - Only expenditure budgets are posted to ledger.[b] New process for Supplemental Allocation Orders[c] Fund Equity - Only expenditure budgets are posted to ledger (Note: SDSU has a carry-forward budget view process).[d] 06/07 transition year only

YTD YEAR-END JUNE 30 2007 - Transition YearFUND 0485FUND 0001 [a]

26

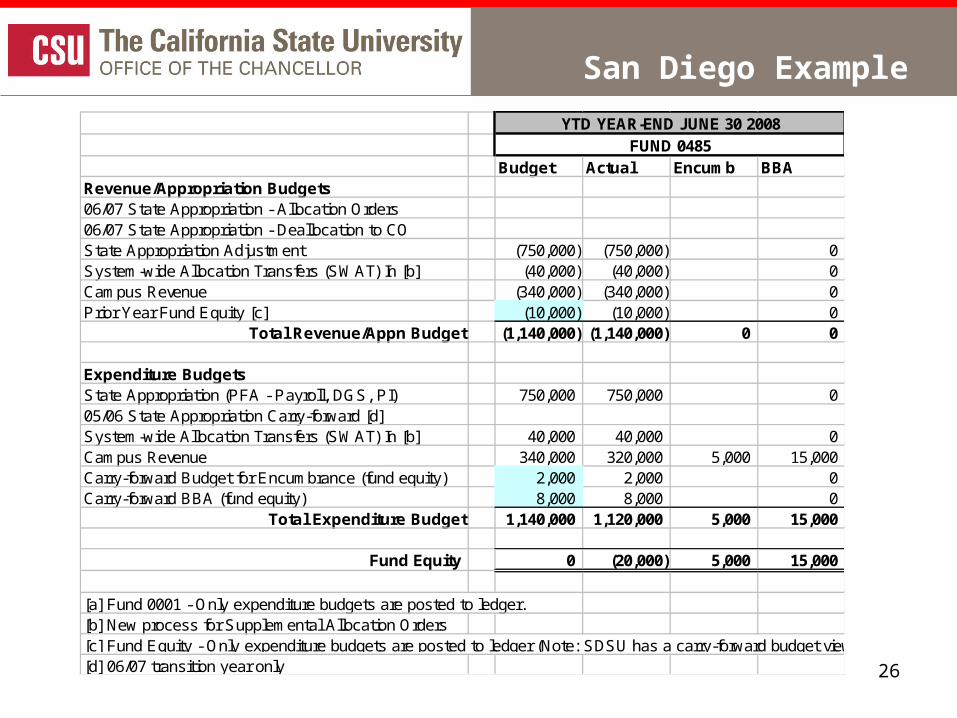

San Diego Example

Budget Actual Encumb BBARevenue/Appropriation Budgets06/07 State Appropriation - Allocation Orders06/07 State Appropriation - Deallocation to COState Appropriation Adjustment (750,000) (750,000) 0System-wide Allocation Transfers (SWAT) In [b] (40,000) (40,000) 0Campus Revenue (340,000) (340,000) 0Prior Year Fund Equity [c] (10,000) (10,000) 0

Total Revenue/Appn Budget (1,140,000) (1,140,000) 0 0

Expenditure BudgetsState Appropriation (PFA - Payroll, DGS, PI) 750,000 750,000 005/06 State Appropriation Carry-forward [d]System-wide Allocation Transfers (SWAT) In [b] 40,000 40,000 0Campus Revenue 340,000 320,000 5,000 15,000Carry-forward Budget for Encumbrance (fund equity) 2,000 2,000 0Carry-forward BBA (fund equity) 8,000 8,000 0

Total Expenditure Budget 1,140,000 1,120,000 5,000 15,000

Fund Equity 0 (20,000) 5,000 15,000

[a] Fund 0001 - Only expenditure budgets are posted to ledger.[b] New process for Supplemental Allocation Orders[c] Fund Equity - Only expenditure budgets are posted to ledger (Note: SDSU has a carry-forward budget view process).[d] 06/07 transition year only

YTD YEAR-END JUNE 30 2008FUND 0485

27

How the budget is built

Source of funds to consider– Prior Year Unspent Amounts

(Fund Equity)– This will be left over Student Fee Money as all CSU

State appropriated amounts will be spent in the year of appropriation

– Current Year State Appropriation Amount (e.g., $ .70)

– Student Fee / Revenue Amounts (e.g., $ .30)

28

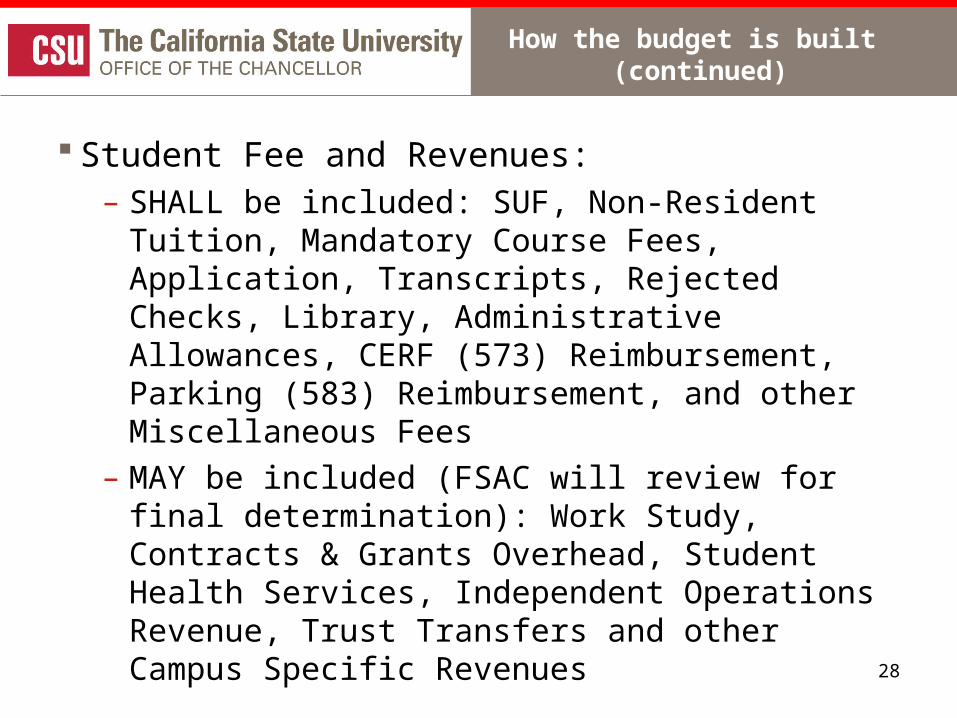

How the budget is built (continued)

Student Fee and Revenues:– SHALL be included: SUF, Non-Resident Tuition,

Mandatory Course Fees, Application, Transcripts, Rejected Checks, Library, Administrative Allowances, CERF (573) Reimbursement, Parking (583) Reimbursement, and other Miscellaneous Fees

– MAY be included (FSAC will review for final determination): Work Study, Contracts & Grants Overhead, Student Health Services, Independent Operations Revenue, Trust Transfers and other Campus Specific Revenues

29

How the budget is built(continued)

How the budget is built (continued)– CMS Tools for Managing the Campus Budget

Sac State Example - CMS Scenario ChartField– Unique 485 Fund with a Global DeptID

$.06 ROLLFWD – Prior Year Unspent <.03> ROLLFWD – PY Enc to Departments <.01> ROLLFWD – BBA to Division Level .70 APPROP – State Appropriation for CY ~ Agrees to CO ACR (or new report) .30 FEES – Student Fee/Revenue for CY <.90> ALLOC – Budget Out to Campus Departments

– Primary 485 Fund with Campus User DeptID’s $.03 ROLLFWD – PY Encumbrances for Departments .01 ROLLFWD – BBA for Division Level .90 ALLOC – Budget In for Campus Departments .00 BUDTX – Internal Campus Budget Transfers

30

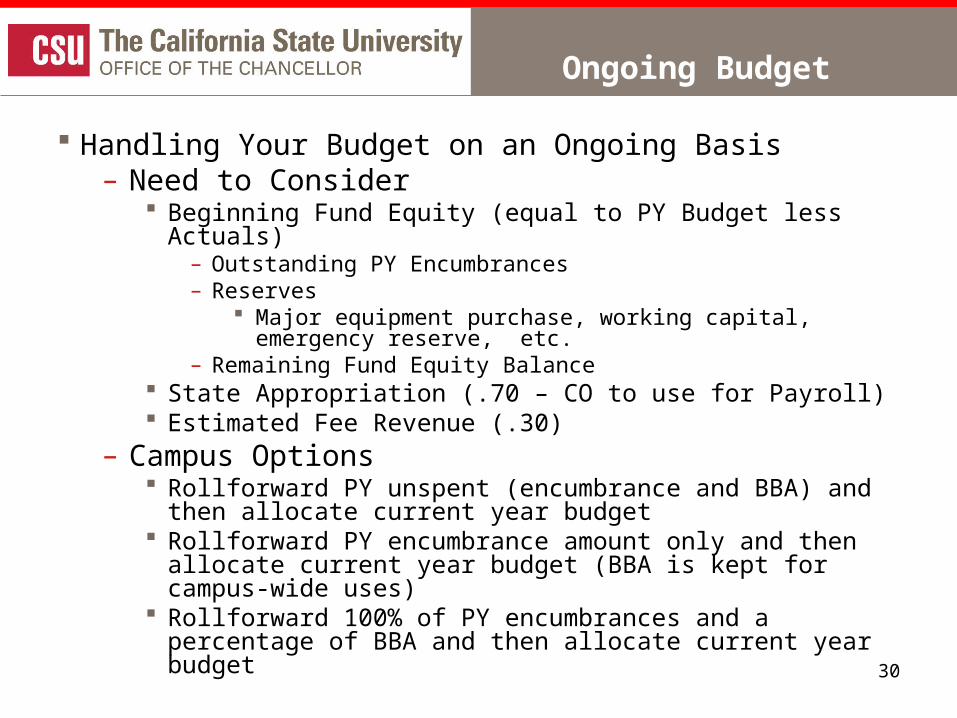

Ongoing Budget

Handling Your Budget on an Ongoing Basis– Need to Consider

Beginning Fund Equity (equal to PY Budget less Actuals)– Outstanding PY Encumbrances– Reserves

Major equipment purchase, working capital, emergency reserve, etc.

– Remaining Fund Equity Balance State Appropriation (.70 – CO to use for Payroll) Estimated Fee Revenue (.30)

– Campus Options Rollforward PY unspent (encumbrance and BBA) and then

allocate current year budget Rollforward PY encumbrance amount only and then allocate

current year budget (BBA is kept for campus-wide uses) Rollforward 100% of PY encumbrances and a percentage of

BBA and then allocate current year budget

31

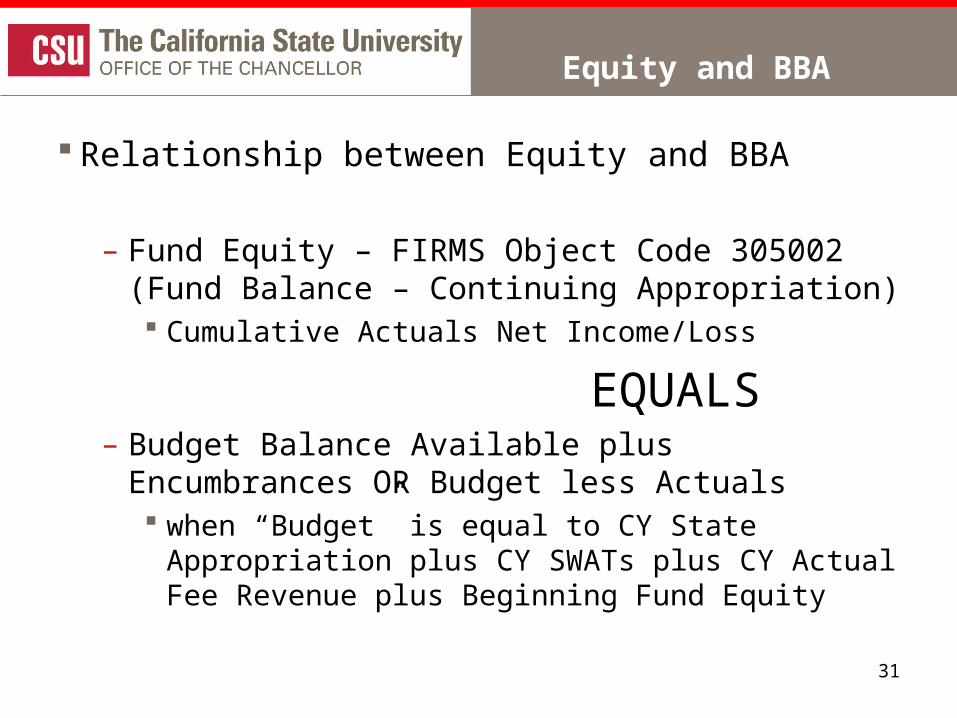

Equity and BBA

Relationship between Equity and BBA

– Fund Equity – FIRMS Object Code 305002 (Fund Balance – Continuing Appropriation) Cumulative Actuals Net Income/Loss

EQUALS– Budget Balance Available plus Encumbrances

OR Budget less Actuals when “Budget” is equal to CY State Appropriation

plus CY SWATs plus CY Actual Fee Revenue plus Beginning Fund Equity

32

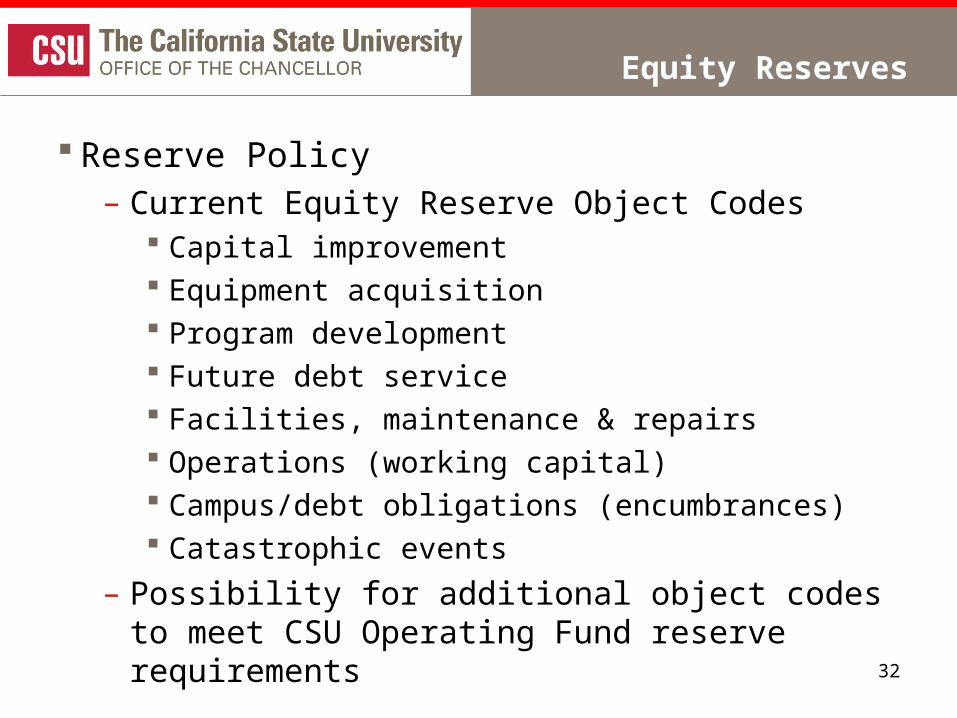

Equity Reserves

Reserve Policy– Current Equity Reserve Object Codes

Capital improvement Equipment acquisition Program development Future debt service Facilities, maintenance & repairs Operations (working capital) Campus/debt obligations (encumbrances) Catastrophic events

– Possibility for additional object codes to meet CSU Operating Fund reserve requirements

33

It is what it is

It is what it is– Not required to accrue to Zero in CSU Fund 485

at Year End

– Legal Expenditures and Encumbrances will reflect what really happened in that Fiscal Year

– Management will want to establish Campus Reserve Policy with CO guidance Major Equipment Purchases Business Continuity Planning Cash Flow / Working Capital Needs Other

34

Things to Remember

During 2006-2007 all campuses will de-allocate their remaining general fund balance to the CO (By year end 690106 in CSU Fund 485 will equal this amount)

Campus generated Payroll PFA transactions between General fund and Trust have been recorded in CSU Fund 485 FIRMS Object Code 690003

CO generated Payroll PFA transactions shall be recorded in CSU Fund 485 FIRMS Object Code 690106

For 2006-2007 the sum of 690003 and 690106 in CSU Fund 485 will equal the campus state support allocation

2007-2008 690003 no longer used– State support = 690106

35

Example Worksheets

Excel Files from Presentation– Sac State Example

– Summary of SWAT – PAST Present and Future

– San Diego Example

Microsoft Excel Worksheet

Microsoft Office Excel Worksheet

Microsoft Excel Worksheet

36

Questions - Contacts

Questions???– Debbie Brothwell, SLO

– Crystal Little, San Diego

– Kendal Chaney-Buttleman, Sac State

– Stacy Hayano, Sac State