1 Project Management Mission Oriented, Customer Focused.

48

1 Project Management Mission Mission Oriented, Oriented, Customer Focused Customer Focused

-

Upload

christian-perez -

Category

Documents

-

view

220 -

download

2

Transcript of 1 Project Management Mission Oriented, Customer Focused.

1

Project Management

MissionMission Oriented, Oriented,

Customer FocusedCustomer Focused

2

Corporate Mission

Information Security and Training maintains a mission oriented team of talented professionals providing world class, customer focused support to the U.S. Government Interagency Team.

3

What is a PM

1. The Manager of a Program or Project2. Responsible for Project Performance3. Primary Customer Interface for effort4. Leader of personnel5. Accountable for ultimate success6. Responsible for Resources, Risks, Schedule,

cost, process and quality7. Establishes and achieves performance metric 8. Owner of the business

4

Roles and Responsibilities

Project ManagersProject Managers– Maintain Burn Plans– Stay Abreast of Growth Ops– Coordinate New Business– Manages Contract Performance

Business Area ManagersBusiness Area Managers– Bid Opportunities Properly– Manage O/H effectively– Audit Burn Plans– Monitors/Audits Contract Performance

Business DevelopersBusiness Developers– Maintain valid strategic BD Plans– Identifies and Captures New Business– Coordinates directly with all Managers– Maintain Corporate Growth Plans

Business ManagementBusiness Management– Actively Participate in Bids– Compile and Maintains Data – Status Plan– Advise/Counsel Managers on O/H– Provides independent Contract Review

Executive ManagementExecutive Management– Manages to established Division/Group Metrics– Directs overall strategy for growth– Maintains Profit and Loss– Ultimate Responsible for overall Performance

Manage To MetricsAccurate Burn PlansKeep Contracts Sold

Labor RatesGrowth #’s - Existing Clients Provide O/H Inputs

New Customer NumbersOpportunity ROICombined B&P Estimates

Organize/Validate All Budgets Prepare then Status Plans O/H, Profit, Revenue History

Validate Approve Budgets Application of Strategic HiresOverall Accountability

AnnualBudget

Plan

AnnualBudget

Plan

Responsibility

Quality

5

Business Area MgrBusiness Area Mgr

ResourcesResources

Acquisition Life Cycle

Market Develop RFP

ROM BudgetROM BOE

Refined BudgetTentative BOEInitial Burn PlanEPR Package

Execution CloseAward

BudgetFinalize WBSVerify BOEValidate BaselineFinal Burn PlanCreate IWA

Monitor BudgetMonitor WBS Validate BOEStatus BaselineMaintain BurnUpdate IWA

BudgetBOEBaselineBurn PlanEPR Pckg

Operations Manager

Administration

Business Developer

Contracts Subcontracts

Finance

Marketing Mgr BD Mgr Capture Mgr Project Manager

SelectionSelection

FeedbackLessons Learned

6

Typical Company Organization

Business ManagementBusiness Operations

Business Development

Program Management

CEO/President

Human ResourcesAdministrationRecruitingBenefitsCompensationEmployee RelationsPublic RelationsCorporate LegalPerformance Reviews

Finance/CPACost AccountingAccounts ReceivableAccounts PayableTime CollectionReport GenerationContractsSubcontracts

7

Company Resource Associations

Program Manager

ContractsFinance

ProgramControl

Business AreaManager

Primary Contract InterfaceLegal representativeMonitors ComplianceAdministers Contract

Processes Time CardsProvides ActualsMonitors the moneyProduces independent data

Monitors BaselinesTracks Earned ValueProvides objective statusModels alternatives

Provides Qualified ResourcesEnforces Metrics AchievementReceives and reviews timelyEnsures compliance to policies

Represents Company to Customer Plans and Executes ProjectIdentifies Resource NeedsManages RequirementsGathers and provides true statusDocuments and Manages RiskCommunicates progress and status

HumanResources

ComplianceCompensation/BenefitsPerformance ReviewsRecruiting/SourcingRelations

8

Contracts/PM Interaction

• • Everything associated with / affecting contractual instrumentEverything associated with / affecting contractual instrument is worked by Contracts Dept.is worked by Contracts Dept.

• • Contracts Dept. supports Contracts Dept. supports formalformal procurement contracts procurement contracts

• • Contracts Dept. responsible for subcontract issuance and modsContracts Dept. responsible for subcontract issuance and mods

• • PM is responsible for execution & subcontract management.PM is responsible for execution & subcontract management.

• PM must support the Contracts Department PM must support the Contracts Department

* Program Managers cannotcannot contractually obligate the company

9

Company<–>GovernmentInterfaces

ACO(Administrating Contract Officer)

PCO(Procuring Contract Officer)

COTR(Contracting Officers’ Technical Representative)

Company accounting / contracts Company PM

• Post award administration• Administer changes• Compliance

• Negotiates• Obligates the Government (signs)

• Technical direction• Technical directives - Inspection - Acceptance

Delegatesduties after award

10

Typical Product Project Relationships

ID

Programmers

Graphics CORECORE

Production

Quality

Editing

ID

Programmers

GraphicsCORECORE

Project Manager

SMESME

TechnicalManager

Delivery Order 1 Delivery Order 2

“To succeed we must view contracts from the world of the Project Manager”

11

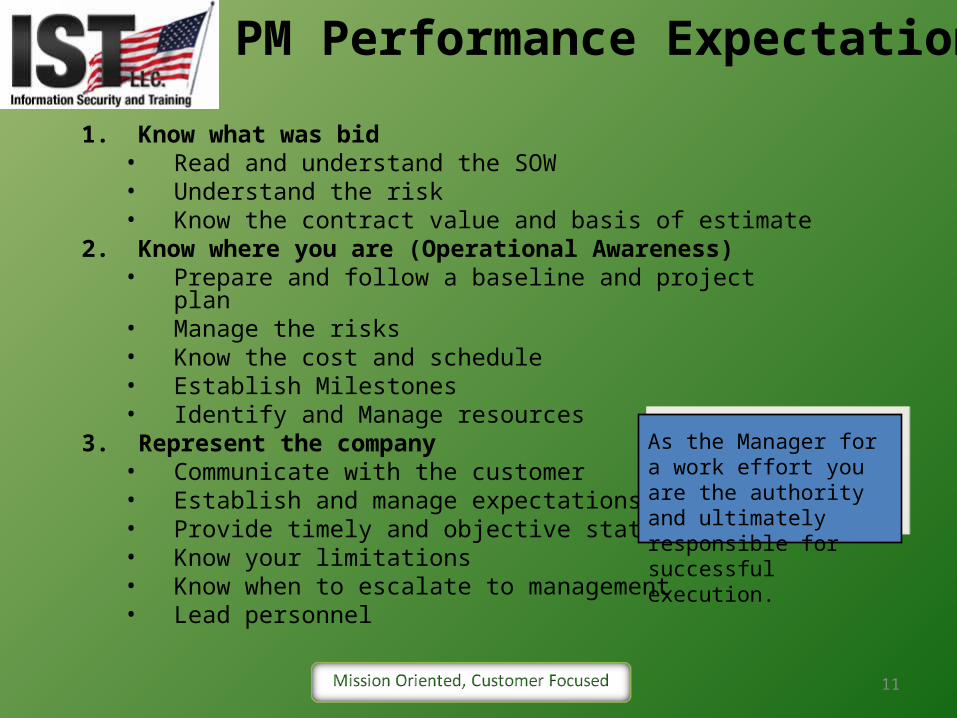

PM Performance Expectations

1. Know what was bid• Read and understand the SOW• Understand the risk• Know the contract value and basis of estimate

2. Know where you are (Operational Awareness)• Prepare and follow a baseline and project plan• Manage the risks• Know the cost and schedule• Establish Milestones• Identify and Manage resources

3. Represent the company• Communicate with the customer• Establish and manage expectations• Provide timely and objective status• Know your limitations• Know when to escalate to management• Lead personnel

As the Manager for a work effort you are the authority and ultimately responsible for successful execution.

12

How to ”fail””fail” as a PM

1. Do not plan the work before you start or allow charges2. Fail to record & communicate performance milestones3. Do not read and understand SOW/Requirements4. Believe your customer knows what’s right5. Do not document your concerns early --“risk”6. Do not establish status meetings and PMRs7. Believe the problem will go away with time 8. Do not manage and communicate metrics9. Neglect to provide regimented status10. Do not properly document acceptance11. Do not track action items and closure12. Make excuses for productivity

13

ProfitProfit– After G&A Tax– After Costs Removed

OverheadOverhead– Cost of Labor– Fringe Benefits– Lease– Other: Travel, Materials

RevenueRevenue– Growth– Stability– Backlog

Financial Performance Measures

10% Minimum10% Minimum

80% Site*80% Site*50% Customer*50% Customer*

20% Growth 20% Growth

MetricsMetrics

* O/H Rates are Examples Only

14

Typical PM Profitability

• Project <10% Profit on notice– Project Mgr documents return to green plan– Weekly meetings with key personnel to status– Public presentation to executive management– Team placed under close observation

• Projects <7% Profit on probation– Project Mgr documents “crash plan” to recover– Project Mgr presents critical path, risks & mitigations – Weekly meetings with ALL team personnel– Mandatory Overtime Instituted

• Projects <5% Profit unacceptable– Program Manager provides accountable leadership to project– Executive Mgmt/Program Management rebaselines project– Critical path documented and options analyzed for efficiency– R-examination of all Team Resources, Utilization, Metrics, Progress– Mandatory Overtime

15

Functional Philosophy

Planning-Bids-Planning-WBS-BOEs-Budgeting-Forecasting-Lessons Learned

Execution Mgmt-Requirements Mgmt-Customer Mgmt-Earned Value Mgmt-Resource Planning-Schedule Mgmt-Subcontracts-Status and reporting

Production-Process Control-Adherence to Schedules-Quality Assurance-Systems Approach to Mgmt-Configuration Management-Adherence to budgets-Forecasting of resources-Productivity/Utilization

Business Development-Strategic Plans - Customer Liaison-Past Performance - Capture Mgmt-Market Approach - Teaming/Partners-Technology Trends - Strategic Hires

Operations Mgmt-Pricing/Bids - Financial Status-Budgets - Profit Realization -Planning - Financial Baselines-Maintaining annual and strategic plans-Subcontracts

CompleteComplete

Working NowWorking Now

16

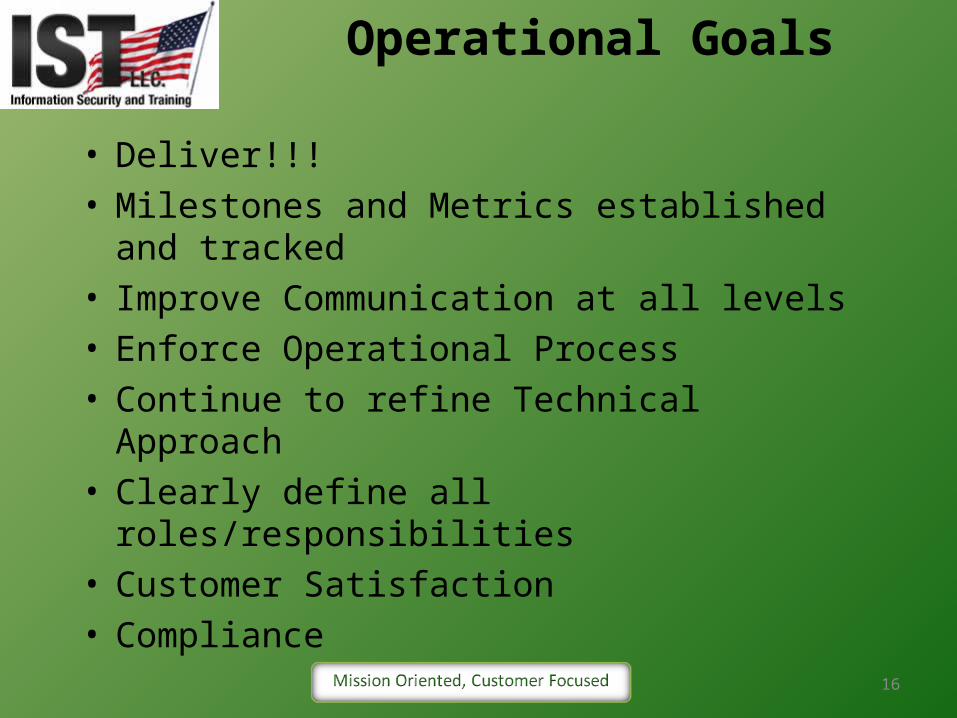

Operational Goals

• Deliver!!!• Milestones and Metrics established and tracked• Improve Communication at all levels• Enforce Operational Process• Continue to refine Technical Approach• Clearly define all roles/responsibilities• Customer Satisfaction• Compliance

17

Earned Value Earned Value MeasurementMeasurement

The BasicsThe Basics

18

Managing Cost 101

• Plan and Propose Work Effectively• Establish Productive Work Plan• Document and Manage Risk• Manage requirements early in the project• Manage performance with Earned Value• Enhance Hiring Practices – Productive People• Outsource where Sensible (CLOCs)• Leverage full depth IST Resources• Perform Make-Buy to reduce risk• Monitor and Manage Dept. Resource Plans• “No-Bid” High Risk Opportunities• Overhead Conscious – Quality FY Budget Inputs

19

Establishing Labor Pools

Quality, Production, Technical Management

New New BusinessBusiness

Program Program ManagementManagement

AdministrativeAdministrativeRecruitingRecruitingIT SupportIT Support

DO 01

DO 02DO 03

DO 04

DO 05DO 06

DO 07

Project Mgr Project Mgr

80%80%

5%5%

3%3%

Corporate LevelCorporate LevelBid & Proposals

R&D

BD

Investments

Project Mgr

Dept. Dept. FocusFocus

BUBUFocusFocus

20

Cost Pools & Colors of Money

G&A salariesG&A Facility CostG&A benefitsB&PIR&D

General & Admin

Buyer SalariesSub-contractManagement

Material HandlingOH Customer site

BenefitsComputersFacilitiesManagement

Direct Contract

Salaries ofEmployees Chargingto aContract

OH Contractor Site

Facility CostBenefitsComputerManagement

90%90%60%60%

15%15%

3%3%

* All % above are examples only

21

Contract Performers

Subcontractor• Subcontract

Consultant• Treated as subcontractor• Consultant Agreement

Contract Labor (On-Call)• No Benefits

Full TimeEmployee• Full BenefitsMust be 32 hoursPer week or more

Paid through accounts payable[No Burdenable Labor]

Paid through payroll system[Burdenable Labor]

22

36.5%

Example Company Site RateExample Company Site Rate 80%80%

Fringe Benefits 34.0%

Bonus 2.5%

Overhead Managerial Labor 8.5%

Benefits on OH Labor 1.5%

Rent 12.0%

Depreciation 4.8%

Travel 2.6%

Communications/Telecom 3.6%

Computer Expense 2.9%

Other (misc) 7.6%

80.0%

Typical Site O/H Cost Pool

* O/H % rates are examples only

23

36.5%

Example Customer Site RateExample Customer Site Rate 50%50%

Fringe Benefits 34.0%

Bonus 2.5%

Overhead Managerial Labor 8.5%

Benefits on OH Labor 1.5%

Travel 1.0%

Other 2.5%

50.0%

Typical Customer O/H Cost Pool

24

EVM Terminology

Contract Value (C/V) – Total Contract Worth (Labor+Travel+Material)

Estimate to Complete (ETC) – Cost to complete the work effort

Inception to Date (ITD) – How much is spent to date on the effort

Estimate At Complete (EAC) – Total cost of effort when done

Budget at Complete (BAC) – Funding left when finished (profitprofit)

Variance – How much you are aheadahead or behindbehind the budgeted plan or baseline

Burn Rate – The monthly amount that the project is accumulating cost

25

How a Basic Labor Rate is Built

Employee Salary = $50,000Hourly Equivalent = $24.04Contractor O/H (80%) = $19.23 G&A (15% of Cum) = $ 6.49 Total Burdened = $49.76

Profit (10%) = $4.97Total Customer HR Sell = $54.73

$43.27

26

Creating Productive Labor Bids

Scenario 1: Full Time Employee has 2 Weeks Vacation is 5 days sickAnnual Hours 2080Holiday Hours 80Vacation Hours 80Sick Time 40Productive Hours 1880

Scenario 2: Full Time Employee has 3 Weeks Vacation takes no sickAnnual Hours 2080Holiday Hours 80Vacation Hours 120Sick Time 20Productive Hours 1860

Work Effort Value:$54.73 x 1880 = $102,892.40

Work Effort Value:$54.73 x 1860 = $101,797.80$101,797.80

Paid Time Off (PTO)

Paid Time Off (PTO)

27

Overhead Components

Contract Revenue• Direct Labor On Contractor Site

Overhead Labor• Indirect Labor• Fringe Benefits on Indirect Labor

Non-Labor Costs• Rent• Fringe on Direct Labor• Company Allocation • Telecom• Recruiting• Computers• Relocation• Sign on Bonus

Combined OH / Direct Labor = Overhead RateCombined OH / Direct Labor = Overhead Rate

80% is an Example O/H Target80% is an Example O/H Target

28

Profit and Contract Type

Cost PlusT&MFFP Labor Hours

FixedPrice

Goal = 10% on Contract

Decisions:• Hire to maximize profit?

• Hire to maximize customer satisfaction?

• Hire a key employee at a loss?

• Lose money on small T.O. to get foot in the door?

• Bid some labor categories at a loss?

Goal = 15%

Decisions:• Minimize execution risk• Management reserve• Use Divisions OH rate• Plan for follow on

Yes, if necessary to win but must obtain overall profit.

Can’t affect profit much!

Yes, but must stay profitable!

Yes, Sometimes!

Yes, Sometimes!

Not Typical Culture!

29

Project ControlsProject Controls

30

Project Planning Phase

Define theProject

Plan theProject

Schedule theProject

IntegrateCost/Schedule

W ork B reak dow n Stru ctu re

S u b sy stem S u b sy stem

Fi rst S y stem

S u b sy stem S u b sy stem

S econ d S y stem

S u b sy stem S u b sy stem

T h i rd S y stem

P ro j ect T i tle

O rgan ization B reak dow n Structure

S ecti on S ecti on

D i v i si on

S ecti on S ecti on

D i v i si on

S ecti on S ecti on

D i v i si on

P ro j ect O ffi ce

System Subsystem Subsystem Subsystem Subsystem Subsystem

System Subsystem Subsystem Subsystem Subsystem Subsystem

System Subsystem Subsystem Subsystem Subsystem Subsystem

$$ LOAD

Labor = O/H+G&A+FeeTravel = G&A + FeeMaterial = MH + FeeSubcontracts = MH + Fee

LOAD

Labor = O/H+G&A+FeeTravel = G&A + FeeMaterial = MH + FeeSubcontracts = MH + Fee

PMPMSubcontractorSubcontractor

ConsultantConsultant

PersonnelofficePersonneloffice

31

Know What We Bid

• Break Work Down (WBS) into logical segments• Validate IMI Hours against analysis• Enforce Technical Personnel Involvement• If Sub Work, Request Plans and Basis• Burn Plans created w/ “Like” Resources• Unique resources clearly identified• Risks Documented with Mitigations• Formal Bid Sign-Off Accomplished• Maintain artifacts in a project folder

32

Work Breakdown Structures

• Segmented & severable items of work when linked together create steps to completing a project.

• Each work section has a measurable item and artifact that proves the effort has been performed and completed.

• When associating a budget to an item of work within a WBS you can determine performance against the plan.

• WBS elements are loaded into the cost system and become the financial baseline for the project. Separate Work Packages are established for each segment of work to accumulate costs and understand progress.

Project XLabor

Planning

Front EndAnalysis

Design

Production

Artifacts

ScheduleWABurn PlanMgmt Plan

Subcontract PlansRisk PlanDeliverablesCommunication

Resources Scope

PM = 80 HoursTM = 80 HoursQA = 20 HoursLead = 20 Hours

2 Weeks200 Hours$13,000 Max.Complexity = 3

SubordinateWork Package 1

SubordinateWork Package 2

SubordinateWork Package 3

SubordinateWork Package 4

(Example)

33

Cost Accounting

• We Won! - REQUIRING approved budget baselines prior to opening work package:– Final Burn Plan w/ staffing & accurate rates– Work Authorization updated/complete– WBS and BOE’s validated & archived– Financial Baseline reviewed & approved

• Project Mgr• Program Mgr• Operations Mgr• Contracting• Finance

* This process provides a control by requiring completed planning documentation.

PreparePackage

PMApprovals

OpsValidation

OpenBudgets

Budget Turn-on ProcessBudget Turn-on Process

34

What’s a Work Authorization (WA)

• Authorization for someone to work your project.• Must be Maintained by the Project Manager.• Is communicated to the Time Card System • Is auditable and MANDATORY.• Utilized for every cost account whether direct or

indirect to identify personnel authorized to work the project.

• Feeds the Burn Plans and is used by Program Administration to validate resources on projects.

35

Project Burn Plans

• What they are:– A baseline resource plan with hours and rates– An estimate and projection of work in financial view– A model to understand “what ifs?”– A tool for understanding profitability vs. cost– A way to assist business area managers with staffing

• What they are not:– A system for performance measurement (no metrics)– A guarantee of success– An event driven view of your project

36

Project/Job Status Reports (JSR)

• What they are:– Generated by Corporate Finance Monthly– Actuals generated on each cost account– Used to validate burn plans and verify costs– Provides objective evidence of financial position– Doesn’t currently articulate “performance”

37

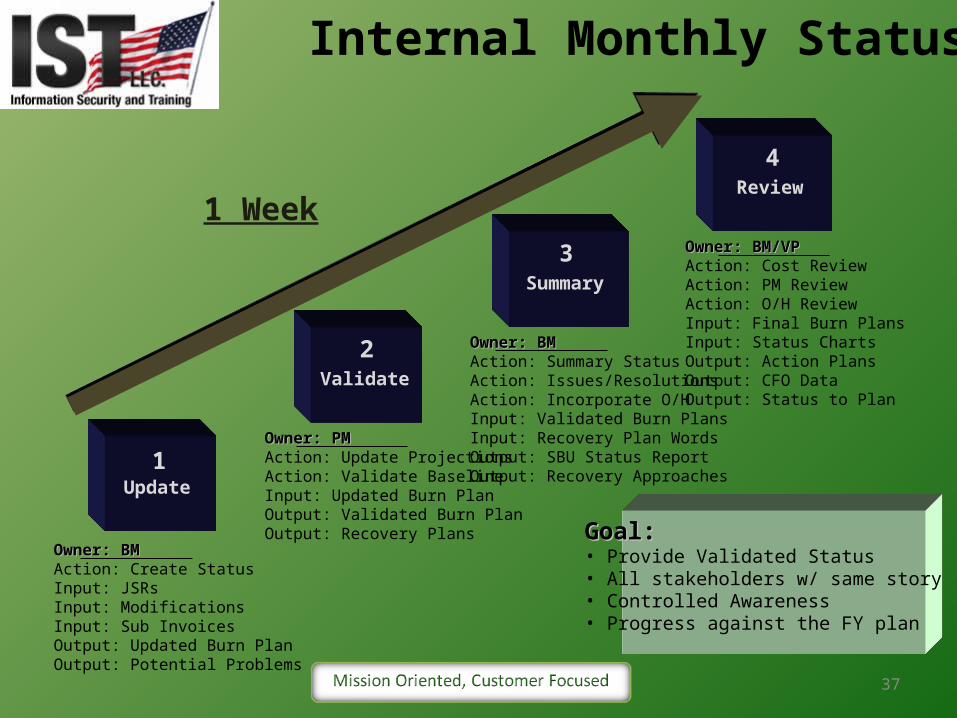

Internal Monthly Status

Owner: BMOwner: BMAction: Create StatusInput: JSRsInput: ModificationsInput: Sub InvoicesOutput: Updated Burn PlanOutput: Potential Problems

Owner: PMOwner: PMAction: Update ProjectionsAction: Validate BaselineInput: Updated Burn PlanOutput: Validated Burn PlanOutput: Recovery Plans

Owner: BMOwner: BMAction: Summary StatusAction: Issues/ResolutionsAction: Incorporate O/HInput: Validated Burn PlansInput: Recovery Plan WordsOutput: SBU Status ReportOutput: Recovery Approaches

Update

Validate

Summary

Review

Owner: BM/VPOwner: BM/VPAction: Cost ReviewAction: PM ReviewAction: O/H ReviewInput: Final Burn PlansInput: Status ChartsOutput: Action PlansOutput: CFO DataOutput: Status to Plan

Goal:Goal: • Provide Validated Status• All stakeholders w/ same story• Controlled Awareness• Progress against the FY plan

1

2

3

4

1 Week

38

Example Business Unit Summary

J A S O N D J F M A M J JD001$1,345,592

D001$639,046

D004$848,044

D005$826,607

D006$1,386,000

D003$1,892,223$267K Subs

A S O

2010 2011

28 Feb

31 Dec

behind sched70% Spent95% Complete

Revised Plan10% Spent10% Complete

% Complete45% Spent60% Complete

Slow Start15% Spent 10% Complete

New Project0% CompleteJust Started

New Sub Added50% SpentCAI/TMI

23 Feb

19 Nov

19 May

N D

30 May

Jul 10/06

CAICAI

TMITMI

11 Feb 22 Jun 17 Aug 12 Oct

39

Maintaining PlanMaintaining Plan

• Required enforcement measures:– Planning Documents use to measure progress– New Hires must be qualified for positions– H/R Reqs must include cost accounts– Subcontract rates will be continuously validated– Baseline Changes require contract modifications– Work Authorizations Maintained– Changes impacting Corporate established targets require

approval by management

40

Example: 4 Part Chart Example: 4 Part Chart Contract 80000 (Example)Contract 80000 (Example)

Cost PerformanceCost Performance

CV $802K CV% 53%Schedule% 36%CPI Future FutureSPI Future FutureTCPI(EAC) Future

ITD (spent) 428KETC (remaining) 98KEAC (total) 526K526KVAC (variance) 277KMonthly Burn Rate 33KGoal: Deliver within budget

Major Schedule Variances:

Issues:Contract Performance – Slow start may push delivery

slips.Effort not local Requires local Lead and oversight.Task Lead/Management Changes have diluted history and

financial information from past not clear.

Action Plans:Aggressive r Mgmt involvement shifting some personnel

to optimize performance.Continuous customer communication and involvement

on site in Ft. Sill OK. Jan 20

Major Cost Variances:

Top Risks:Contract Performance and delivery of courseware within current schedule.Cost Control for delivery without unanticipated cost growthCustomer expectations managed to avoid schedule/cost growth.

Action Plan:PM, TM and BM Involvement on site and with customer to establish new schedules, cost baseline and monitor major milestones on critical path. Jan 31

Period of performance extension implemented need toComplete Remaining Efforts quickly. May 05

Period of Performance: 6/19/10 – 8/18/11Owner: Frank Luster

STATUSSTATUS

0200,000400,000600,000800,000

1,000,000

Contract Value Baseline Plan Estimate to Complete Actual Cost

41

A word on budget planningA word on budget planning

42

Successful Companies:• Create a Legitimate Plan• Maintain/Status the Plan• Adapt/Evolve the Plan• Project the Plan Forward

Why do we need a budget

* Without input from the bottom up, the plan becomes a corporate level vision only.

RaisesThe Value

of theCompany

Provides Provides Stability &Stability &

FocusFocus

Key InputsVision and GoalsHistorical DataWork BacklogBD PipelinesMarketplace InfoCompetitionInvestment/Resources

43

What’s a Profit Center

• Measured Business Area/Unit– Has Own Overhead Pool– Possesses Direct Bill Contracts– Has Revenue and Profit– Contributes M/H and G&A– May have leases– Has Prescribed Corporate Metrics

*Generally a business unit is aligned to customer, geographic area, or business line.

Revenue

Overhead G&AM/H

Profit

Profit CenterProfit Center

44

Composite Overhead ExampleComposite Overhead Example

01.100

01.02.100 – Virginia Beach

01.02.110 - Arlington

01.01.120 - Chesapeake

01.01.140 – Tampa

Direct = 263KCosts = 212.22KIDSI Rate 80.69%

YTD Avg= 80.7%

01.01.130 – Indiana

Direct = 226.88KCosts = 121.07KCust Rate 53.36%

YTD Avg = 54.1%

Direct 9.96KCosts 9.41K

Direct 99.1KCosts 85.72K

Direct 4.54KCosts 3.57K

Direct 95.2KCosts 74.08K

Direct 54.2KCosts 39.44K

Total Company (1M)

94.50%

86.50%

78.60%

77.82%

72.76%

01.01.100 – Virginia Beach

01.01.110 - Arlington

01.01.120- Chesapeake

01.01.140 – Tampa

01.01.130 – Indiana

Direct 8.27KCosts 5.13K

Direct 10.52KCosts 5.83K

Direct 179.53KCosts 95.60K

Direct 16.32KCosts 7.92K

Direct 12.24KCosts 6.59K

62.0%

55.4%

53.25%

48.54%

53.86%

110 Personnel 489.88K DL 333.29K O/H823.17M Total823.17M Total123.47K G&A123.47K G&A

946.64K Burdened946.64K Burdened

Monthly Revenue: $1.02MMonthly Profit (9%): $76.2K

FY Projected: $12.3MFY Project Profit: 914K

Profit down due to O/H

ContractorContractor Site SiteCustomerCustomer Site Site

45

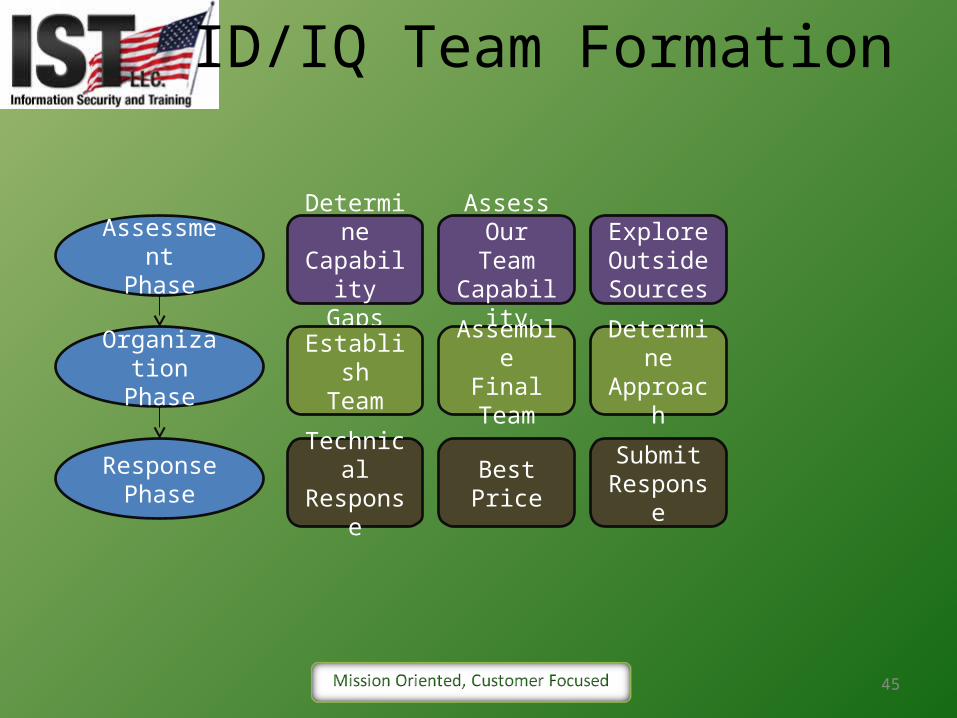

ID/IQ Team Formation

AssessmentPhase

DetermineCapability

Gaps

ExploreOutside Sources

AssessOur Team Capability

EstablishTeam

DetermineApproach

AssembleFinal Team

OrganizationPhase

Technical Response

SubmitResponse

BestPrice

ResponsePhase

46

Risk

M M H H H

L M M H H

L L M M H

L L L M M

L L L L M

RISK RATING

High Certainty5

Highly Likely4

Unlikely2

Remote1

Likely3

Consequence

Minimala

Minorb

ModerateModeratec

Significantd

Severee

47

The Way AheadAt IST we pride ourselves on customer satisfaction the first time, every time. When you partner with IST, we mesh your vision and supporting concepts with our innovative approaches to provide world class products and services. You communicate directly with our management team which translates to more customer satisfaction and value returned for your investment. We are ready to team with you now to provide leading edge solutions to your 21st Century challenges.

48

Mission OrientedMission Oriented

Customer FocusedCustomer Focused