1 Open questions from last class Review homework Foreign tax credit (FTC) –How it works...

27

• Open questions from last class • Review homework • Foreign tax credit (FTC) – How it works – Application of sourcing rules – Interaction with Sec 911 Agenda for Class 3

-

Upload

chrystal-wilcox -

Category

Documents

-

view

220 -

download

0

Transcript of 1 Open questions from last class Review homework Foreign tax credit (FTC) –How it works...

1

• Open questions from last class• Review homework• Foreign tax credit (FTC)

– How it works– Application of sourcing rules– Interaction with Sec 911

Agenda for Class 3

2

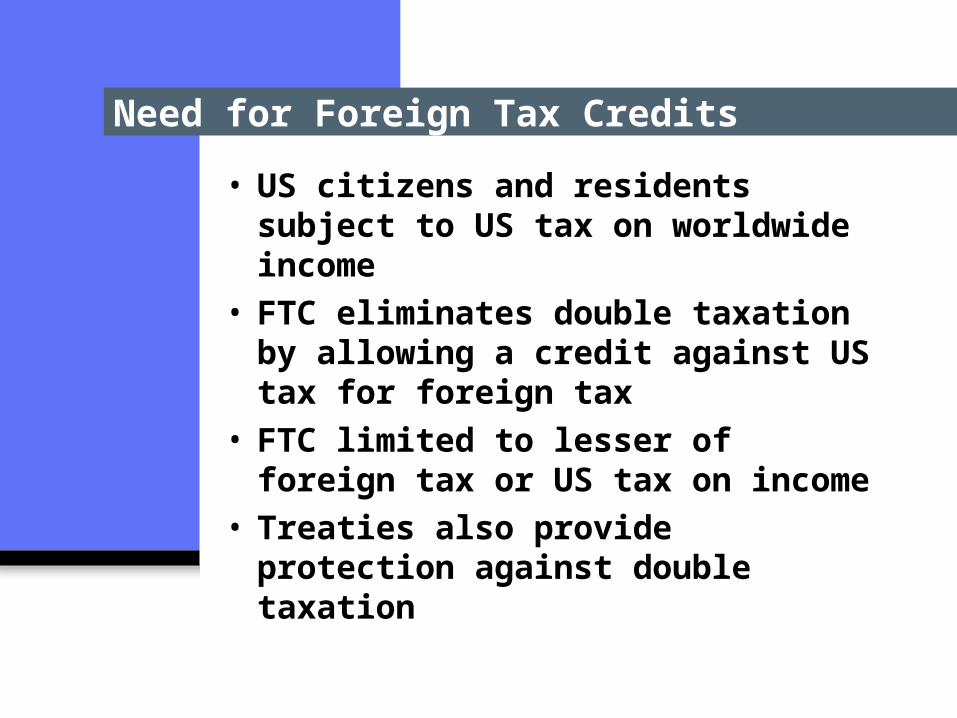

Need for Foreign Tax Credits

• US citizens and residents subject to US tax on worldwide income

• FTC eliminates double taxation by allowing a credit against US tax for foreign tax

• FTC limited to lesser of foreign tax or US tax on income

• Treaties also provide protection against double taxation

3

Foreign Tax Credit

Income $100,000 (foreign source)

US tax rate 30%

Foreign tax rate 40%

US tax $30,000 (a)

Foreign tax $40,000 (b)

Credit – Lesser of (a) or (b)

$30,000

4

Foreign Tax Credit

• Credit (Sec 901(a)) vs. deduction (Sec 164(a))

• Annual election • Compulsory payment• Not payment for economic benefit• What happens if employer pays

tax on behalf of employee?

5

Foreign Tax Credit

• “Foreign Tax” – tax on income or profit imposed by a foreign country

• Income tax in US sense• Specific country guidance provided

by IRS• Some social taxes creditable, unless

totalization agreement in force• Wealth tax, church tax, fringe

benefits tax usually not creditable• “Any political subdivision of any

foreign state” 1.901-2 (g)(2)

6

FTC Baskets

• Taxable years beginning after 2007– Passive income

– General category income

• Taxable years beginning before 2007– Passive income

– High withholding tax interest

– Financial services income

– Shipping income

– Dividends from DISC or former DISC

– Distributions from FSC or former FSC

– Lump sum distributions

– Section 901(j) income – sanctioned countries

– General limitation income

• Income resourced by treaties

7

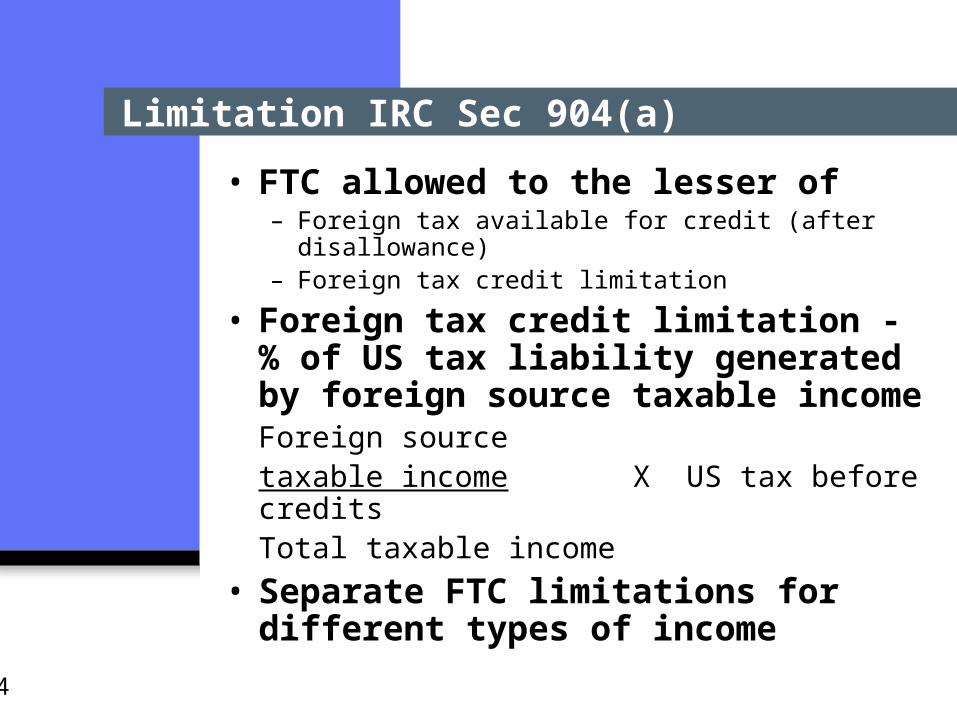

IRC Sec 904(a)

• FTC allowed to the lesser of– Foreign tax available for credit (after disallowance)– Foreign tax credit limitation

• Foreign tax credit limitation - % of US tax generated by foreign source taxable income

Foreign source US incometaxable income X tax beforeTotal taxable income credits

8

Foreign Sourced Income - Expatriate

Total Pd US Source

Foreign Source

Base salary- Pre- During

$82,500

97,500

Bonus 30,000

COLA 25,000

Total $235,000

9

Sourcing

• Interest – source of payment of interest determines whether US or foreign source– § 861(a)(1) and 862(a)(1)– § 871(h) “Portfolio interest received by a NRA

from sources within the US, no tax shall be imposed under [30% withholding tax]”

• Dividends – source of payment– § 861(a)(2) and 862(a)(2)– Paid by domestic US corporation: US source– Paid by foreign corporation: foreign source– Mutual funds provide details of foreign source

income

• 80/20 rule repealed

10

Sourcing

• What happens when US deems US source and foreign country taxes income?– 1/1/2005 Joe was granted 10,000 shares @ $10 – 1/1/2008 shares vest, FMV $15– 1/1/2009 Joe exercised 10,000 shares, FMV $17

– 7/1/2007 Joe went on assignment to X Country– X Country taxes residents on worldwide income

and taxes shares on exercise– Joe’s marginal tax rate in X Country is 50%

What are the US tax consequences?

11

Sourcing

• What happens when US deems US source and foreign country taxes income?– 9/1/2008 Grace moved to Country Y– 3/3/2009 Grace received a bonus of $7,000 related

to services performed in calendar year 2008– Country Y taxes 100% of Grace’s bonus of $7,000

at a marginal tax rate of 40%

What are the US tax consequences?

12

Foreign Source Taxable Income

• Foreign source income• Less deductions specifically

allocable– Rental expenses associated with rental property– State and local tax (directly allocable to US income if

related to US source income)– § 911 exclusion

• Reg §1.861-8T(e)(12)(iv) charitable contributions specifically allocable to US source income

13

Foreign Source Taxable Income

• Less pro-rata deductions not directly allocableGross foreign Total ratably Foreign sourceincome X allocable = expenses/Total gross deductions

deductionsincome

• Less qualified resident interest 1.861-9T(d)(1)(iv)Gross foreign income less

Foreignexcluded income X Qual residence = sourceGross income interest deductionless excludedincome

14

Limitation IRC Sec 904(a)

• FTC allowed to the lesser of – Foreign tax available for credit (after disallowance)– Foreign tax credit limitation

• Foreign tax credit limitation - % of US tax liability generated by foreign source taxable incomeForeign source taxable income X US tax before creditsTotal taxable income

• Separate FTC limitations for different types of income

15

Disallowance/Scaledown/Kickout/Reduction

• Can’t claim 911 exclusion and FTC per § 911(d)(6)

• Foreign taxes disallowed to extent attributed to excluded income

Foreign tax paid Net 911 exclusion

or accrued during X Net foreign earned

taxable year income

16

Disallowance/Scaledown/Kickout/Reduction

• Net Sec 911 exclusion includes– Housing and foreign earned income exclusions– Less disallowed expenses relating to excluded

income (e.g., employee business expenses)

• Net foreign earned income includes– Total foreign earned income– Less expenses relating to excluded income– US source income on which foreign tax is imposed

(e.g., US workday income)– Amounts deductible on US return but are subject to

tax in the foreign country (e.g., 401(k) contributions)

17

Process

• Step 1 – allocate foreign assignment compensation into US and foreign components

• Step 2 – calculate 911 exclusion– Determine number of qualifying days in year– Calculate housing exclusion– Calculate maximum allowable foreign earned

income exclusion– Calculate actual foreign earned income

exclusion

• Step 3 – scale-down any expenses related to excluded income (e.g., employee business expenses)

18

Process

• Step 4 – calculate disallowed foreign taxes

Foreign tax paid Net 911 exclusion

or accrued during X Net foreign earned

taxable year income

• Step 5 – calculate the foreign taxes available for credit or deduction

Total Foreign taxes paid/accrued

Less Disallowed from Step 4

Equals Foreign tax available for credit/deduction

19

Process

• Must be calculated for each year• If taxpayer on “paid” basis and

paid several years’ taxes in one year, calculate different scaledown ratios for exclusion for each year

20

Paid or Accrued Method

• Paid basis– Foreign taxes actually paid during the year– Regardless of the year to which the taxes relate

• Accrued basis– Total estimated/actual foreign tax liability for that

tax year regardless of whether paid or settled during the year

– Fiscal year end jurisdictions taken on US return in year in which foreign tax year ends

– Example: UK tax year ends April 5

HK tax year ends March 31

Australia tax year ends June 30

21

Paid or Accrued Method

• Elect to take as paid or accrued• Election is made by checking box

on Form 1116– Paid method may be changed in subsequent

year to accrued method– Accrued method may be changed with consent

of IRS Commissioner– In practice, can’t switch to paid method

• Documentation must be available upon request

22

Exchange Rate

• Paid method– Exchange rate in effect on day tax paid or

withheld– Tax refund uses conversion rate on date tax

paid

• Accrual method– Average exchange rate for the year – Use exchange rate on date of payment

• If paid more than 2 years after the close of the tax year

• If paid in the prior year

23

Redetermining FTC

• Paid method – if receive refund in later year, must file amended tax return reducing the tax credited by the amount refunded

• Accrued method– Accrued taxes when paid differs from amount

claimed as a credit– Amount not paid within 2 years after close of tax

year (utilize exchange rate on date of payment)– After accrued taxes paid, received refund of tax

• Practical approach – change FTC carry forward

24

FTC Carrybacks and Carryovers

• Unused credit can be carried back and carried forward

• New law– Applicable to credits generated in 2005– Back 1 year– Forward 10 years– Credits generated 1999 or later can be carried forward

10 years

• Old law (2004 and previous tax return)– Back 2 years– Forward 5 years

25

FTC Carryovers

• Current year FTC used before carryovers

• Interaction with scaledown– If credit allocated to excluded income, no c/o– No further scaledown required when c/o

• FTC carrybacks claimed on 1040X• Utilizing excess FTC• Benefit of tax planning in non-US

countries

26

FTC

• States may not recognize foreign tax credits, e.g., California does not recognize

• Alternative minimum tax (AMT)– Foreign tax credit can offset AMT– May have different FTC c/o for AMT purposes– Effective beginning in 2005, law allows full FTC

for AMT purposes– Prior law limited FTC to 90% of AMT tax

27

• Foreign tax credit (FTC)– How it works– Sourcing– Interaction with Sec 911

Key Points

![PlanSwift - E-5 ne...co. co co co. MSR co AREA A A co 9.3 FTE 5.3 FTC] 396.1 FTC 25.8 85.6 FTC] 42.6 FTC 17.2 FTC] 8.0 EAO 1.0 EAS EDI co EXT co](https://static.fdocuments.us/doc/165x107/5e51eb57b6d9eb55ec160d6c/planswift-e-5-co-co-co-co-msr-co-area-a-a-co-93-fte-53-ftc-3961-ftc.jpg)