1 Motivation What is capital budgeting? Analysis of potential additions to fixed assets. In deciding...

25

1 Motivation What is capital budgeting? Analysis of potential additions to fixed assets. In deciding whether to accept or reject a new project, firm needs a benchmark to compare profitability of the project. It is the discount rate the firm will use to compare different cash flows a project will generate. Another interpretation of this discount rate is that it is the minimum % return a firm needs to earn from a project so that the project is an acceptable one. In other words, the firm must earn at least this rate on its investments just to compensate investors for the use of their money.

-

date post

21-Dec-2015 -

Category

Documents

-

view

215 -

download

1

Transcript of 1 Motivation What is capital budgeting? Analysis of potential additions to fixed assets. In deciding...

1

Motivation

What is capital budgeting?

Analysis of potential additions to fixed assets.In deciding whether to accept or reject a new project, firm needs a benchmark to compare profitability of the project.

It is the discount rate the firm will use to compare different cash flows a project will generate.

Another interpretation of this discount rate is that it is the minimum % return a firm needs to earn from a project so that the project is an acceptable one. In other words, the firm must earn at least this rate on its investments just tocompensate investors for the use of their money.

2

Motivation

Every source of capital has its required return. Weighted average of these required returns gives us the

discount rate we have described above. It is called the weighted

average cost of capital (WACC).

It is not valid to use the WACC directly for all the projects of the

firm. The WACC reflects the required rate for a typical investment

with average risk. An investment’s cost of capital should be found

by adjusting WACC to reflect the investment’s risk.

3

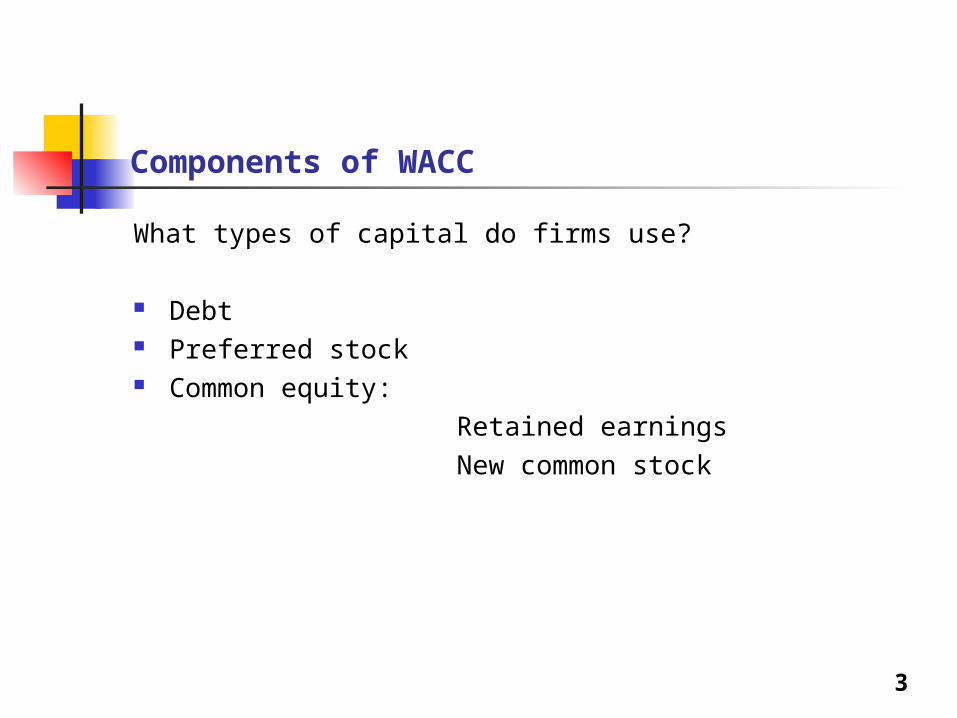

Components of WACC

What types of capital do firms use?

Debt Preferred stock Common equity:

Retained earnings New common stock

4

Two important points

We can calculate WACC on before-tax or after-tax basis.

Since the after-tax WACC shows the net cost we should use it in our calculations.

In finding component costs, we can either use the historical figures (costs we had in financing old projects) or we can try to estimate current costs (costs if we decide raise new capital to be used in new projects).

It is obvious that we should use the current values.

5

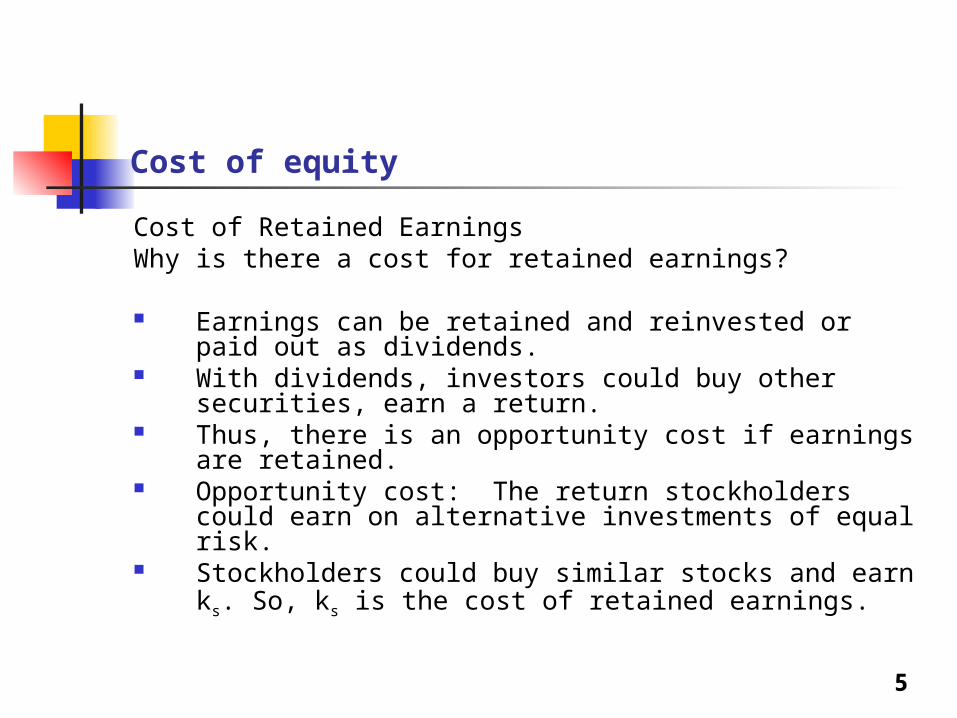

Cost of equity

Cost of Retained EarningsWhy is there a cost for retained earnings?

Earnings can be retained and reinvested or paid out as dividends.

With dividends, investors could buy other securities, earn a return.

Thus, there is an opportunity cost if earnings are retained.

Opportunity cost: The return stockholders could earn on alternative investments of equal risk.

Stockholders could buy similar stocks and earn ks. So, ks is the cost of retained earnings.

6

Three Approaches

CAPM Approachks = kRF + (kM – kRF) b

Bond Yield plus Risk-Premium Approachks = kd + RP

Discounted Cash Flow Approachks = D1/P0 + g

7

CAPM Approach

What’s the cost of common equity based on the CAPM?

Given: kRF = 7%, RPM = 6%, b = 1.2

ks = kRF + (kM – kRF )b

= 7.0% + (6.0%)*1.2 = 14.2%.

8

Discounted Cash Flow Approach

What’s the DCF cost of common equity, ks? Given: D0 = $4.19; P0 = $50; g =5%.

gP

)g(Dg

P

Dk̂s

0

0

0

1 1

= %....$

).(.$8130500880050

50

051194

9

bond-yield-plus-risk-premium method

Find ks using the own-bond-yield-plus-risk-premium method.

recall kd = 10%, assume RP = 4%

ks = kd + RP = 10.0% + 4.0% = 14.0%

What’s a reasonable final estimate of ks ?

Method EstimateCAPM 14.2%DCF 13.8%kd + RP 14.0%Average 14.0%

10

Why is the cost of retained earnings cheaper than the cost of issuing new

common stock? When a company issues new common stock they also

have to pay flotation costs to the underwriter.

Issuing new common stock may send a negative signal to the capital markets, which may depress stock price.

11

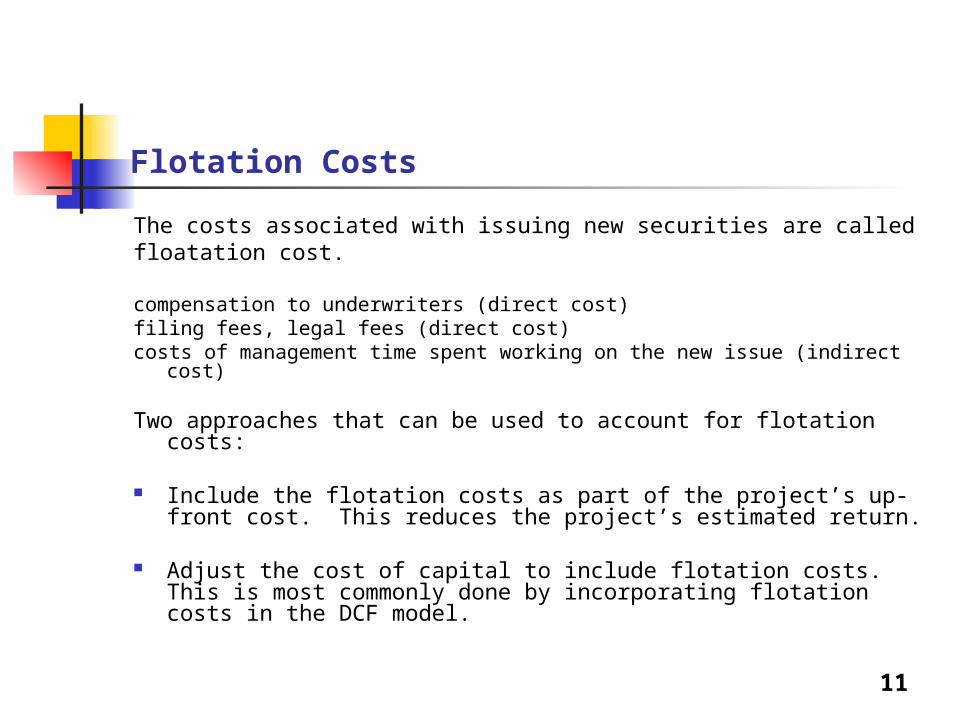

Flotation Costs

The costs associated with issuing new securities are calledfloatation cost.

compensation to underwriters (direct cost) filing fees, legal fees (direct cost) costs of management time spent working on the new issue (indirect cost)

Two approaches that can be used to account for flotation costs:

Include the flotation costs as part of the project’s up-front cost. This reduces the project’s estimated return.

Adjust the cost of capital to include flotation costs. This is most commonly done by incorporating flotation costs in the DCF model.

12

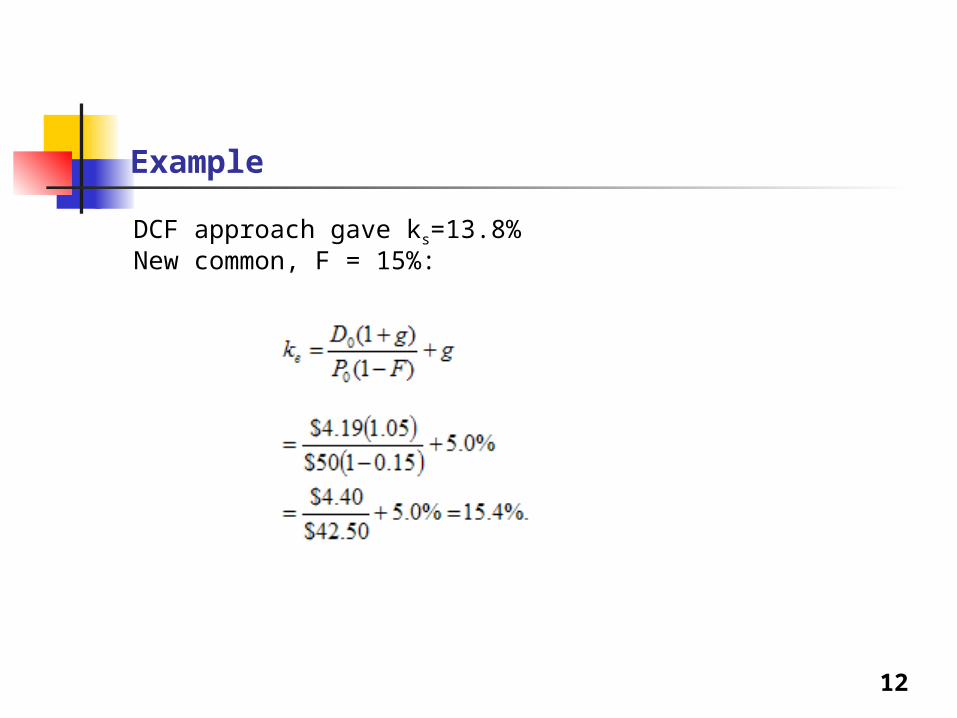

Example

DCF approach gave ks=13.8%New common, F = 15%:

13

Comments about flotation costs:

Flotation costs depend on the risk of the firm and the type of capital being raised.

The flotation costs are highest for common equity. However, since most firms issue equity infrequently, the per-project cost is fairly small.

We will frequently ignore flotation costs when calculating the WACC.

14

Cost of debt

For our firm, 15-year, 12% semiannual bond sells for $1,153.72. What’s kd?

15

Cost of debt

Why is the cost of debt 10%, rather than 12%?if the firm were to issue new bonds with time-to-maturity of 15 years,

thento be able to sell those new bonds at par value the coupon rate of

thosebonds should be 10%. Thus 10% is current cost of borrowing.

Interest is tax deductible, so

kd AT = kd BT(1 – T) = 10%(1 – 0.40) = 6%.

Use nominal rate. Flotation costs small. Ignore.

16

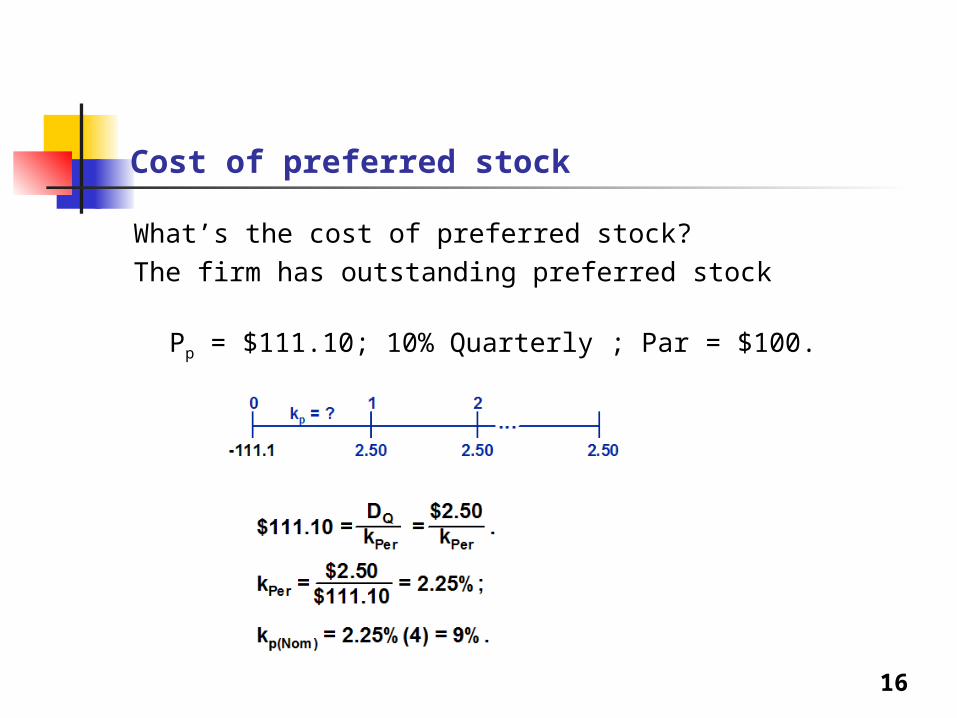

Cost of preferred stock

What’s the cost of preferred stock? The firm has outstanding preferred stock

Pp = $111.10; 10% Quarterly ; Par = $100.

17

Cost of preferred stock

Preferred dividends are not tax deductible, so no tax adjustment. Just kp.

Nominal kp is used. Our calculation ignores flotation costs.

18

WACC

Each firm has an optimal capital structure: Advantage of issuing debt: tax deductibility Disadvantage of issuing debt: increased likelihood of

bankruptcy Some debt can reduce the agency problem between

managers and stockholders by reducing free cash flow. We will be given optimal (target) capital structure of the

firm explicitly.

19

What’s the firm’s WACC (ignoring flotation costs)?

WACC = wdkd(1 – T) + wpkp + wsks

= 0.3(10%)(0.6) + 0.1(9%) + 0.6(14%)= 1.8% + 0.9% + 8.4% = 11.1%.

Weights should be based on market values of securities that provide capital.

If firm’s book value weights are close to market value weights then either of these can be used.

20

Adjusting WACC for risk

Consider two firms H (high risk) and L (low risk) and two projects A and BWACCL=8% WACCH=12%

Expected return: project A=10.5% project B=9.5%

21

Divisional and project cost of capital

Same logic holds for divisions within a firm Should the company use the WACC as the hurdle rate for each

of its projects? NO! The WACC reflects the risk of an average project

undertaken by the firm. Therefore, the WACC only represents the “hurdle rate” for a typical project with average risk.

Different projects have different risks. The project’s WACC should be adjusted to reflect the project’s risk.

22

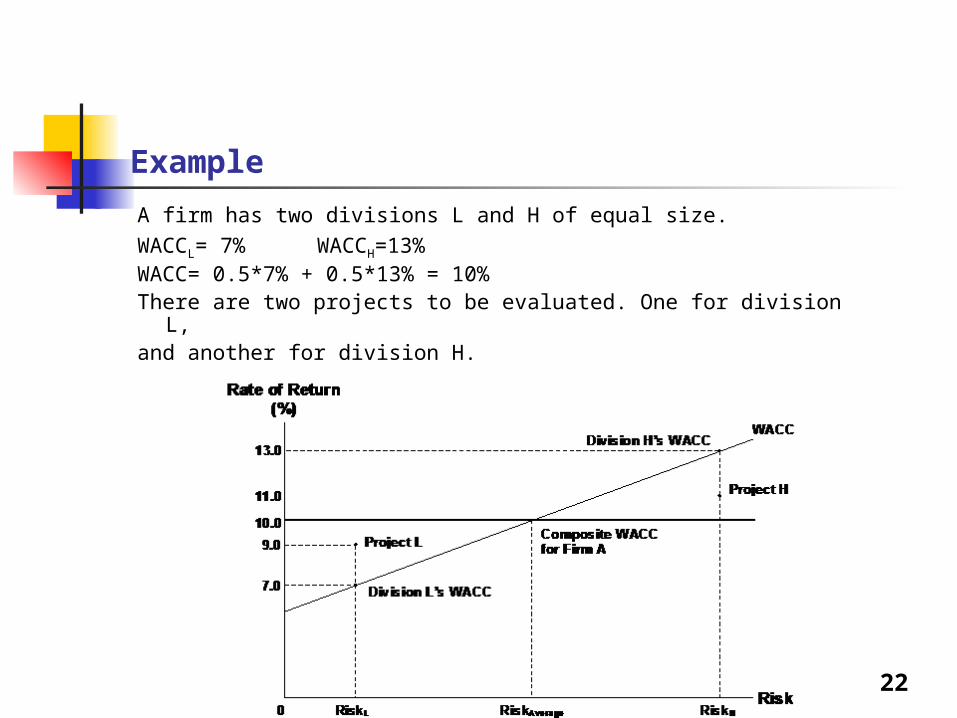

Example

A firm has two divisions L and H of equal size.WACCL= 7% WACCH=13%WACC= 0.5*7% + 0.5*13% = 10%There are two projects to be evaluated. One for division L, and another for division H.

23

But how is risk measured?

Alternatives:

1. Stand-alone risk2. Corporate or within-firm risk3. Market (beta) risk

Which measure is the best?Which measure is the easiest to calculate?

24

Best risk measure

A project’s cash flows will be correlated with the cash flows of the firm (excluding CFs of the project)So project may provide diversification benefits. 2 is better than 1.

Shareholders are probably well-diversified. i.e. they should only care about market risk. 3 is better than 2.

Unfortunately, market risk appears to be the most difficult to estimate.

If we can find beta of the project, we can calculate the cost of equity

by using the SML. Then WACC can be found by adding the remaining

cost components.

25

How to estimate beta of the project?

Pure play method: Identify firms whose only business is to produce

the product in question.

Use average of betas of these firms.