1 Money & Banking Chapters 4 & 5 Debt Instruments and Interest Rates.

29

1 Money & Banking Chapters 4 & 5 Debt Instruments and Interest Rates

-

date post

22-Dec-2015 -

Category

Documents

-

view

215 -

download

1

Transcript of 1 Money & Banking Chapters 4 & 5 Debt Instruments and Interest Rates.

1

Money & Banking

Chapters 4 & 5

Debt Instruments and Interest Rates

2

Debt Instruments

Chapter 4

3

Present Value

What is a future cash flow (FV ) worth now?

ni

FVPV

)1(

4

Rule of the Cash Flow Timeline

Cash flows at the same date can be added together, but cash flows at different dates cannot be added together.

5

Four Types of Credit Market Instruments

1. Simple loan

6

2. Fixed Payment, or Amortized, Loan

Examples: car loans, mortgages

7

3. Coupon Bond

Most bonds with maturities greater than a year are of this form.

Coupons bonds issued byFederal government (Treasurys)State and local governments (munis)Corporations (corporates)

8

9

Special Type of Coupon Bond: Consol or Perpetuity

Fixed coupon received forever.

i

couponPV

10

4. Discount, or Zero Coupon, Bond

Identical in cash flow structure to a simple loan. The difference is that there’s an active secondary market for zero coupon bonds.

11

Draw cash flow diagrams for the four types of credit instruments.

Take the perspective of the lender.

Simple loanAnnuity/Amortized loanCoupon bondZero coupon (discount) bond

12

Yield Curve

13

Bond Page of the

Newspaper

14

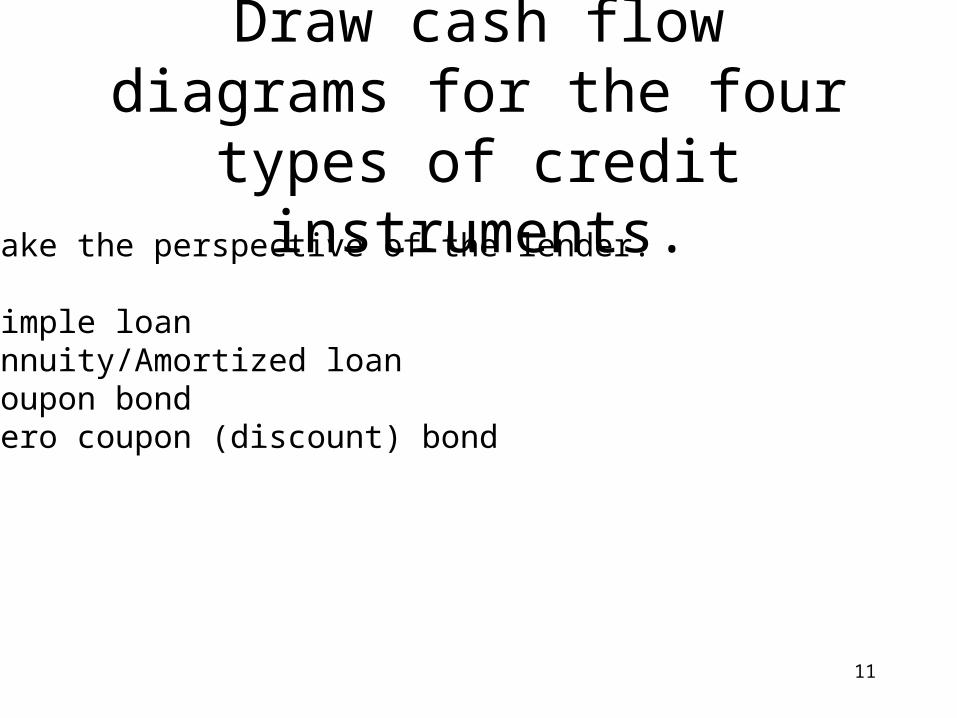

Rate Maturity

Mo/Yr

Bid Asked Chg Asked

Yield13 1/4 May 15 143:01 143:02 +14 6.78

Semi annual coupon on $1 mil of face value?$66,250.00Number of coupons remaining?Nov06 … May15 18Asked price of $1 mil of face value?$1,430,625

15

Pricing a coupon bond

Suppose I need a 4% rate of return.

How much would I be willing to pay for $1 million of face value of the bond on the previous slide?

(FV=1mil, n=18, i = .02, PMT = 66,250)

16

http://online.wsj.com/public/page/8_0004.html?mod=djemITP

17

Yield to Maturity

The rate of discount that equates the present value of future cash flows with the price of the credit instrument.

18

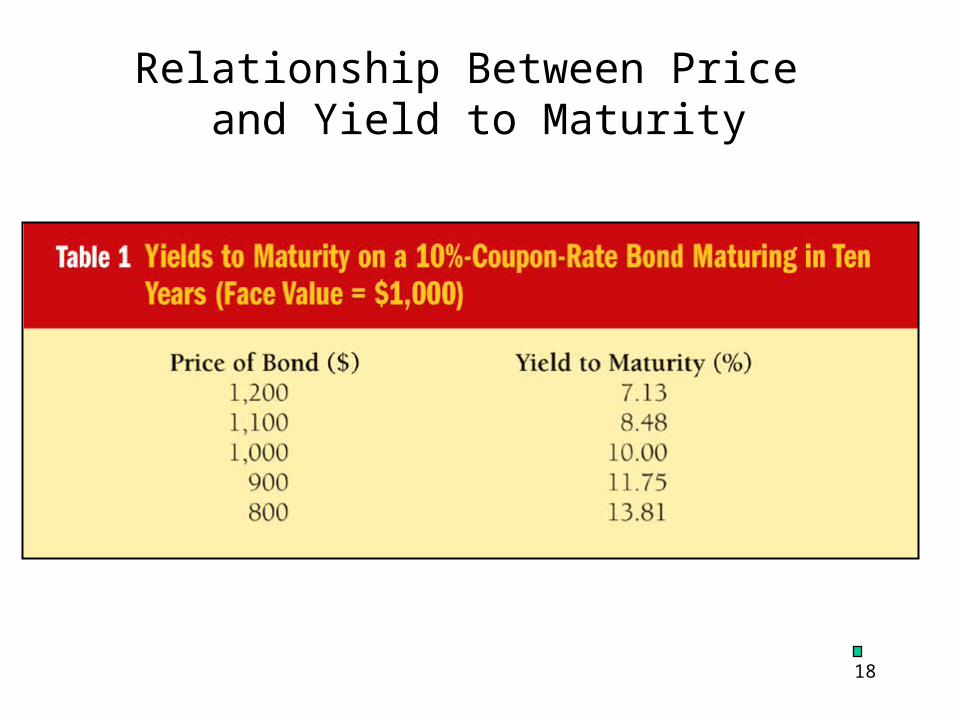

Relationship Between Price and Yield to Maturity

.

19

Calculate the yield to maturity on a consol that pays $100 a year and is

priced at $2,500.

Recall formula for present value of a consol:

i

couponPV

20

Approximation for YTM: Current Yield

P

Cic

21

Approximation to Yield to Maturity: Yield on a Discount Basis for Bills

ritydaystomatuF

PF 360

22

Fisher Equation

The nominal (actual) interest rate equals the real rate plus the expected inflation rate.

e

rii

23

TIPS (Treasury Inflation Protection Securities)

• Originally issued in 1997.

• Interest and principal payments are adjusted for inflation.

• In times of high inflation the $ amount paid to investors rises.

• Return on TIPS provides information on expected inflation.

24

Supply and Demand

Analysis ofthe Bond Market

Market Equilibrium

1. Occurs when Bd = B

s, at P* =

$850, i* = 17.6%

2. When P = $950, i = 5.3%, Bs >

Bd (excess supply): P to P*, i

to i*

3. When P = $750, i = 33.0, Bd >

Bs (excess demand): P to P*,

i to i*

25

Loanable Funds Terminology

1. Demand for bonds = supply of loanable funds

2. Supply of bonds = demand for loanable funds

26

Shifts in the Bond Demand Curve

27

Factors that Shift the Bond Demand Curve

1. WealthA. Economy grows, wealth , Bd , Bd shifts out to right

2. Expected ReturnA. i in future, Re for long-term bonds , Bd shifts out to rightB. e , Relative Re , Bd shifts out to rightC. Expected return of other assests , Bd , Bd shifts out to right

3. RiskA. Risk of bonds , Bd , Bd shifts out to rightB. Risk of other assets , Bd , Bd shifts out to right

4. LiquidityA. Liquidity of Bonds , Bd , Bd shifts out to rightB. Liquidity of other assets , Bd , Bd shifts out to right

28

Shifts in the Bond Supply Curve

1. Profitability of Investment Opportunities

Business cycle expansion, investment opportunities , Bs , Bs shifts out to right

2. Expected Inflation

e , Bs , Bs shifts out to right

3. Government Activities

Deficits , Bs , Bs shifts out to right

29

Changes in e: the Fisher Effect

If e 1. Bd shifts in to

left2. Bs , Bs shifts

out to right3. P , i

© 2005 Pearson Education Canada Inc.