1 Mergers, Acquisitions, and Reorganizations Asset Deal Stock Deal “F” Reorganization Statutory...

15

1 Mergers, Acquisitions, and Reorganizations Asset Deal Stock Deal “F” Reorganization Statutory Merger 338(h)(10)

-

Upload

corey-norris -

Category

Documents

-

view

220 -

download

1

Transcript of 1 Mergers, Acquisitions, and Reorganizations Asset Deal Stock Deal “F” Reorganization Statutory...

1

Mergers, Acquisitions, and Reorganizations

Asset Deal

Stock Deal

“F” Reorganization

Statutory Merger

338(h)(10)

2

Mergers, Acquisitions, and Reorganizations

Asset Deal–Buyer purchases the assets of a target company (partial or total)–Typically, the acquired employees will be immediately reported on the purchaser’s payroll–In the case of partial acquisitions, the target company continues to survive and report payroll–For both partial and total acquisitions there is generally a movement of employees and related assets

3

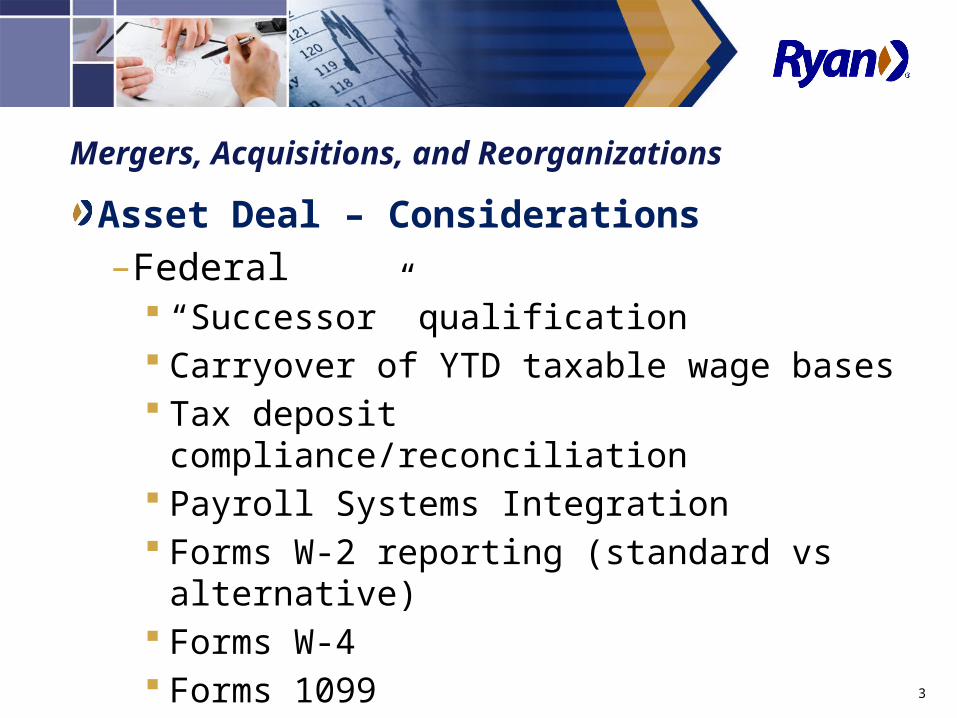

Mergers, Acquisitions, and Reorganizations

Asset Deal – Considerations–Federal

“Successor” qualification Carryover of YTD taxable wage bases Tax deposit compliance/reconciliation Payroll Systems Integration Forms W-2 reporting (standard vs

alternative) Forms W-4 Forms 1099 Year-end notifications to IRS

4

Mergers, Acquisitions, and Reorganizations

Asset Deal – Considerations–State

“Successor” qualification Carryover of YTD taxable wage bases SUI experience transfers (optional or

mandatory) Payroll Systems Integration State Employee Withholding Allowance

Certificate State correspondence/notification Account closures

5

Mergers, Acquisitions, and Reorganizations

Stock Deal–Buyer purchases the stock of a target company–Typically, the acquired company remains “alive” and all employees will continue to be reported under the target company’s payroll id numbers–Generally no change in target company’s business–Generally no initial movement of employees from target company payroll to purchaser’s payroll

6

Mergers, Acquisitions, and Reorganizations

Stock Deal – Considerations–Federal and State

There are generally no tax considerations in stock deals as the employees of the acquired company will continue to be reported under the acquired company’s federal/state ID numbers.

No Forms W-2, W-4, and 1099 issues No SUI transfer of experience issues Potential Payroll Systems Integration Subsequent movement of employees

7

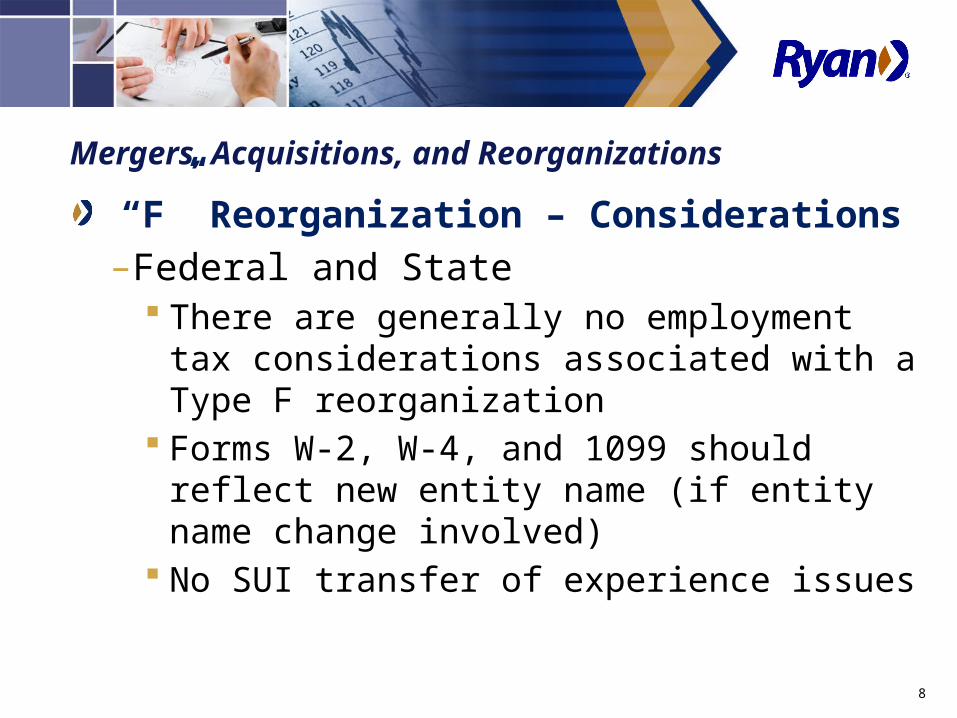

Mergers, Acquisitions, and Reorganizations

“F” Reorganization–Typically involved when a corporation changes its name, the state where it does business, or makes changes to its corporate bylaws/charter–Does not change the federal or state identification numbers of the entity–No movement of employees–No movement of assets

8

Mergers, Acquisitions, and Reorganizations

“F” Reorganization – Considerations–Federal and State

There are generally no employment tax considerations associated with a Type F reorganization

Forms W-2, W-4, and 1099 should reflect new entity name (if entity name change involved)

No SUI transfer of experience issues

9

Mergers, Acquisitions, and Reorganizations

Statutory Merger–Also known as a Type A merger. It is a merger between two entities that is effected under the laws of the U.S., a state or territory or the District of Columbia. Statutes of foreign jurisdictions will also qualify as long as the statute operates in a similar manner to a domestic merger statute.–Post merger, one company continues to exist while other ceases to exist–Movement of employees and assets

10

Mergers, Acquisitions, and Reorganizations

Statutory Merger – Considerations–Federal

“Successor” qualification Carryover of YTD taxable wage bases Tax deposit compliance/reconciliation Payroll Systems Integration Successor must file one Forms W-2 for

entire year Forms W-4 Successor must file one Forms 1099 for

entire year Year-end notifications to IRS

11

Mergers, Acquisitions, and Reorganizations

Statutory Merger – Considerations–State

“Successor” qualification Carryover of YTD taxable wage bases SUI experience transfers (optional or

mandatory) Payroll Systems Integration State Employee Withholding Allowance

Certificate State correspondence/notification Account closures

12

Mergers, Acquisitions, and Reorganizations

338(h)(10) election–Jointly made election between purchaser and target company of a stock purchase–The stock purchase is ignored for corporate tax purposes–The target company is generally treated as having made a deemed sale of its assets and then liquidated

13

Mergers, Acquisitions, and Reorganizations

IRC 338(h)(10) – Considerations– Federal/State

Generally same considerations as that of an asset acquisition.

SUI regulations/rules should be consulted as some states will consider the transaction a stock transaction.

14

Mergers, Acquisitions, and Reorganizations

General considerations– Are employees AND assets involved– Related party transactions

In some states, the employees are enough to establish common ownership/management

– Working with 3rd party payroll processors– Potential Forms 1099-B requirements– Local Tax compliance– Forms W-4 Compliance

15

This document is presented by Ryan, LLC for general informational purposes only, and is not intended as specific or personalized recommendations or advice. The application and effect of certain laws can vary significantly based on specific facts, and professional advice of any nature should be sought only from appropriate professional advisors. This document is not intended, and shall not be

deemed, to constitute legal, accounting, or other professional advice.

© 2013 Ryan, LLC. All rights reserved. All logos and trademarks are the property of their respective companies and are used with permission.