1 Lessons from economic principles for the design of a common European tax base and its relation to...

23

1 Lessons from economic principles for the design of a common European tax base and its relation to IAS/IFRS Silvia Giannini (University of Bologna) Alexander Klemm (Institute for Fiscal Studies) Paola Parascandolo (Assonime) Harmonising corporate tax bases in the EU CEPS Task Force Monday, 30 May 2005

-

Upload

andra-cook -

Category

Documents

-

view

214 -

download

0

Transcript of 1 Lessons from economic principles for the design of a common European tax base and its relation to...

1

Lessons from economic principles for the design of a

common European tax base and its relation to IAS/IFRS

Silvia Giannini (University of Bologna)Alexander Klemm (Institute for Fiscal Studies)

Paola Parascandolo (Assonime)

Harmonising corporate tax bases in the EUCEPS Task Force

Monday, 30 May 2005

2

Introduction

• Currently tax rules differ across countries

• Accounting standards however are converging/being harmonised (IAS/IFRS)

• If tax rules are harmonised, the question arises of how?– Can accounting rules be used?– Any lessons from economic theory?

3

Overview

• Lessons from economic theory– Neutrality, equality, simplicity…– Some general guidelines

• Some concrete examples– grouped into examples where

• IAS can easily be applied• IAS can be applied with minor adjustments to reduce taxpayer

discretion• Examples where tax system should not follow IAS

• Conclusion

4

Approach taken

• Assume– Corporate income should be taxed– Rent taxes (e.g. cash-flow taxes) ruled out

• Does economic theory provide guidance on the design of a corporate income tax system?

5

Criteria

• Neutrality/efficiency• Equity• Simplicity• Tax capacity• Enforceability• Revenue provision• Public policy• Cost of reform

6

What do these principles imply?

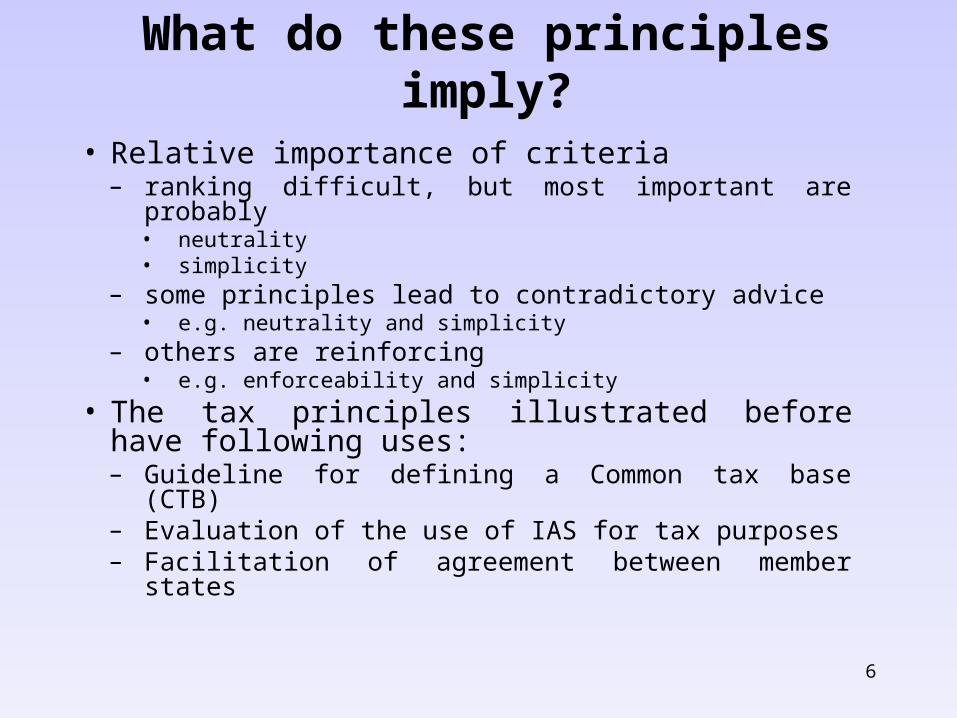

• Relative importance of criteria– ranking difficult, but most important are probably

• neutrality• simplicity

– some principles lead to contradictory advice• e.g. neutrality and simplicity

– others are reinforcing• e.g. enforceability and simplicity

• The tax principles illustrated before have following uses:– Guideline for defining a Common tax base (CTB)– Evaluation of the use of IAS for tax purposes– Facilitation of agreement between member states

7

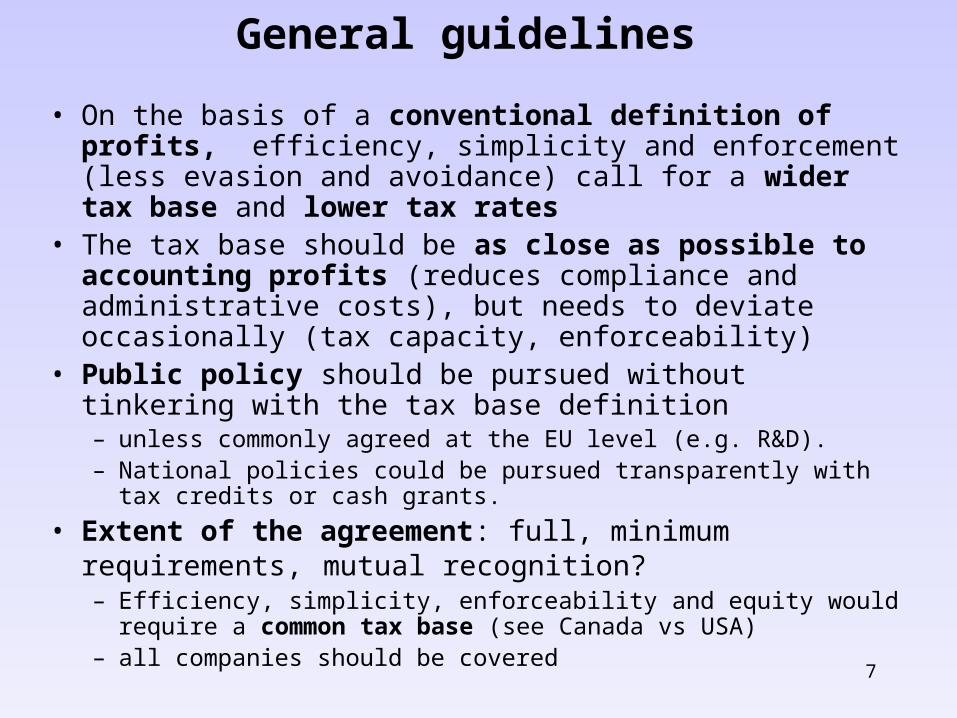

General guidelines

• On the basis of a conventional definition of profits, efficiency, simplicity and enforcement (less evasion and avoidance) call for a wider tax base and lower tax rates

• The tax base should be as close as possible to accounting profits (reduces compliance and administrative costs), but needs to deviate occasionally (tax capacity, enforceability)

• Public policy should be pursued without tinkering with the tax base definition– unless commonly agreed at the EU level (e.g. R&D). – National policies could be pursued transparently with tax credits or cash

grants.

• Extent of the agreement: full, minimum requirements, mutual recognition?– Efficiency, simplicity, enforceability and equity would require a

common tax base (see Canada vs USA)– all companies should be covered

8

Conclusions from theory

• Economic principles provide some guidance between choices about tax laws– Tradeoffs between different principles– Costs and benefits can be difficult to quantify– Need to go through every detail of tax system

to decide where to apply and where to deviate from accounting rules

9

Some concrete examples

• Three groups depending on the principles that are more relevant to decide whether or not to align to accounting principles:

1. Examples in which the overall balance between the different tax principles could make the IAS definition acceptable for tax purposes (Inventories, Stock options, Long term construction contracts, Lease).

2. Examples in which adjustment to IAS accounting would be required to avoid excessive taxpayer discretion (Depreciation of tangible assets, R&D expenses, Goodwill, Contingent liabilities).

3. Examples in which adjustment to IAS would be required for other reasons, particularly capacity to pay (Financial assets, Investment properties, Post employment benefits).

10

First group: alignment to IAS would be possible

•Inventories, •Stock options, •Long term construction contracts,• Lease

11

Inventories(valuation standard – cost formula)

• NeutralityTo estimate as precisely as possible the actual value of

inventoriesBut for..

• Simplicity and enforceabilityA case by case calculation would be problematic. Better

to use a systematic method (FIFO and weighted average method, as in IAS)

• Inflation is not a problem at present• Open question: IAS valuation standard is the lower between

cost and “net realizable value“. Too subjective for tax purposes? Deduction of unrealised losses should not be allowed? But used in many EU countries and might be justified in many circumstances

12

Stock options

• Neutrality /Equity The application of IAS would restore neutrality

between different forms of remuneration of employees, since stock option pays are treated as an expense on the date they are granted to employees. No other tax deductions should be allowed. (The equivalence of the tax treatment should extend to the granting company as well as the beneficiary…)

• Certainty The fair value evaluation of the cost wouldn’t affect

certainty since the stock option payment is measured only once (at the grant date).

13

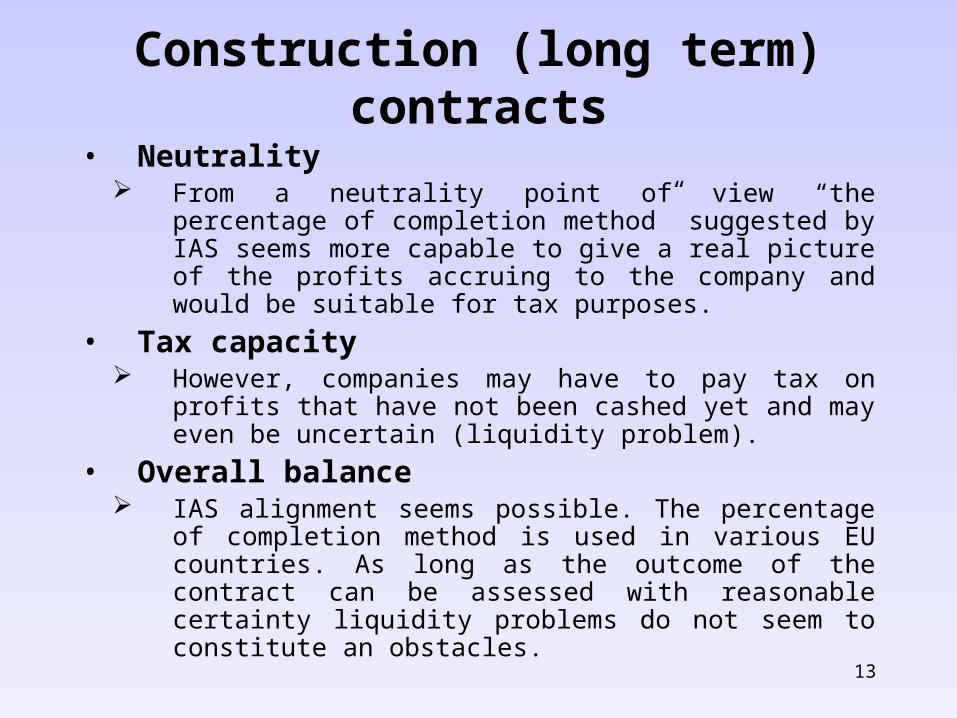

Construction (long term) contracts

• Neutrality From a neutrality point of view “the percentage of

completion method” suggested by IAS seems more capable to give a real picture of the profits accruing to the company and would be suitable for tax purposes.

• Tax capacity However, companies may have to pay tax on profits that

have not been cashed yet and may even be uncertain (liquidity problem).

• Overall balance IAS alignment seems possible. The percentage of

completion method is used in various EU countries. As long as the outcome of the contract can be assessed with reasonable certainty liquidity problems do not seem to constitute an obstacles.

14

Lease

• Neutrality The IAS distinction between operating (do not transfer

substantially all risks/rewards) and finance (transfer substantially all risks/rewards) lease seems more capable to ensure neutrality (debt vs lease)

• Certainty IAS distinction may give room to uncertainty and discretion:

better a special statutory definition for tax purposes?

• Costs For the leasing sector For SMEs, especially start up IAS distinction may give room to

uncertainty and discretion: better a special statutory definition for tax purposes?

In case compensation for these costs is needed, better to use other instruments

15

Second group: adjustment to IAS accounting would be required to avoid excessive taxpayer’s

discretion

•Depreciation of tangible assets,• R&D expenses, •Goodwill, •Contingent liabilities

16

Depreciation (tangible assets)• Neutrality

Tax depreciation should be as close as possible to true economic depreciation of each asset/firm. IAS could be acceptable in principle, but..

• Revenue stability/certainty Specific rules: historical cost valuation, fixed rate of depreciation

(better than boundaries) and systematic method. An option between the Straight line and Declining balance method could be allowed.

• Simplicity/enforceability Better to have few asset categories (Radical solution: pooling of

some assets eg.equipment and machinery)

• Public policyAccelerated depreciation should not be allowed: business

incentive to investment should be given through tax credit.

17

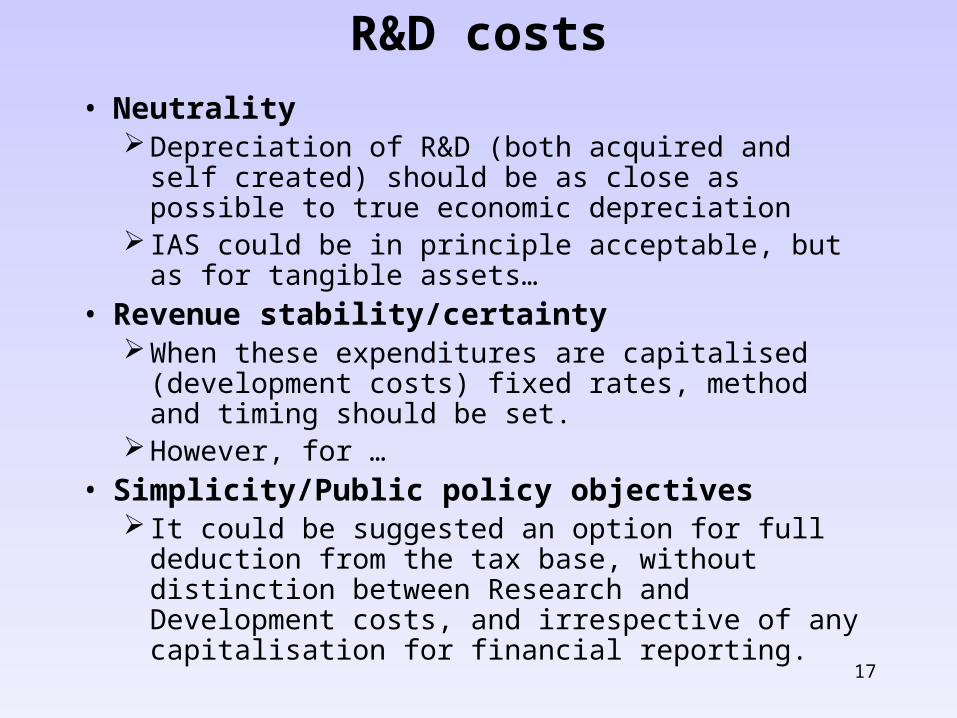

R&D costs

• NeutralityDepreciation of R&D (both acquired and self created)

should be as close as possible to true economic depreciation

IAS could be in principle acceptable, but as for tangible assets…

• Revenue stability/certaintyWhen these expenditures are capitalised (development

costs) fixed rates, method and timing should be set. However, for …

• Simplicity/Public policy objectives It could be suggested an option for full deduction from

the tax base, without distinction between Research and Development costs, and irrespective of any capitalisation for financial reporting.

18

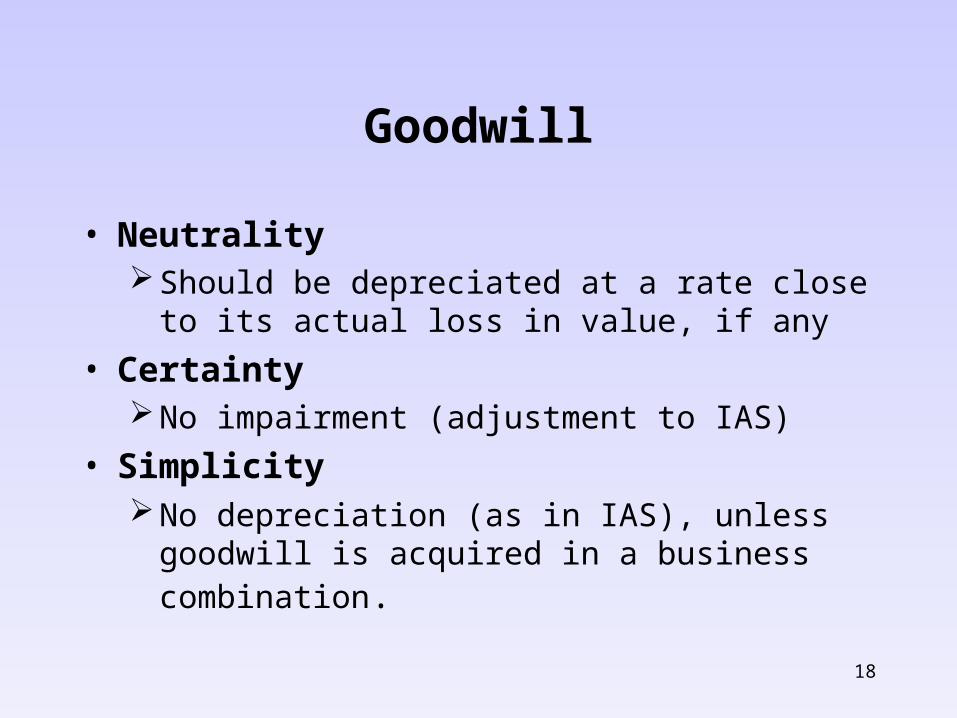

Goodwill

• NeutralityShould be depreciated at a rate close to its actual loss

in value, if any

• CertaintyNo impairment (adjustment to IAS)

• SimplicityNo depreciation (as in IAS), unless goodwill is

acquired in a business combination.

19

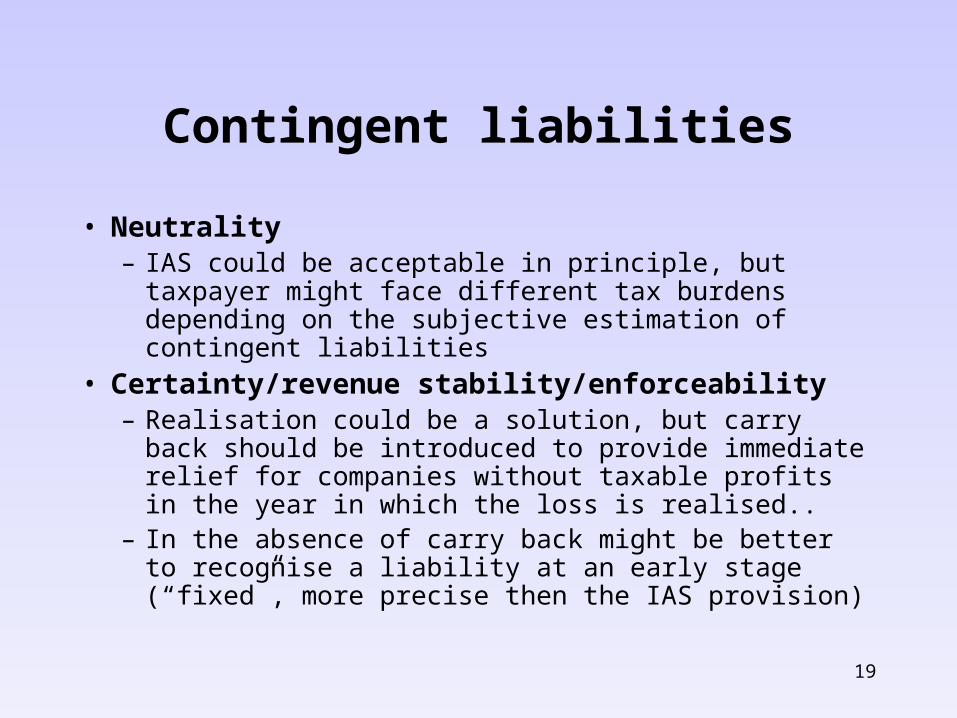

Contingent liabilities

• Neutrality– IAS could be acceptable in principle, but taxpayer might

face different tax burdens depending on the subjective estimation of contingent liabilities

• Certainty/revenue stability/enforceability– Realisation could be a solution, but carry back should be

introduced to provide immediate relief for companies without taxable profits in the year in which the loss is realised..

– In the absence of carry back might be better to recognise a liability at an early stage (“fixed”, more precise then the IAS provision)

20

Third group: adjustment to IAS accounting would be required for other reasons, particularly

capacity to pay

•Financial assets, •Investment properties, •Post employment benefits

21

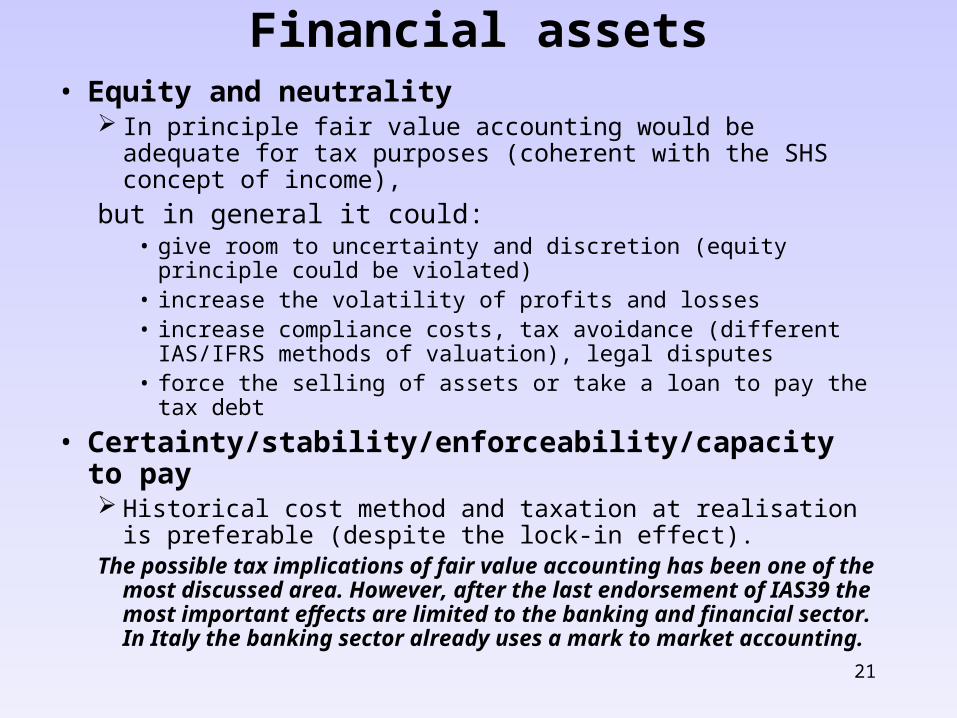

Financial assets• Equity and neutrality

In principle fair value accounting would be adequate for tax purposes (coherent with the SHS concept of income),

but in general it could:• give room to uncertainty and discretion (equity principle could be

violated) • increase the volatility of profits and losses• increase compliance costs, tax avoidance (different IAS/IFRS

methods of valuation), legal disputes• force the selling of assets or take a loan to pay the tax debt

• Certainty/stability/enforceability/capacity to pay Historical cost method and taxation at realisation is preferable

(despite the lock-in effect). The possible tax implications of fair value accounting has been one of

the most discussed area. However, after the last endorsement of IAS39 the most important effects are limited to the banking and financial sector. In Italy the banking sector already uses a mark to market accounting.

22

Investment property

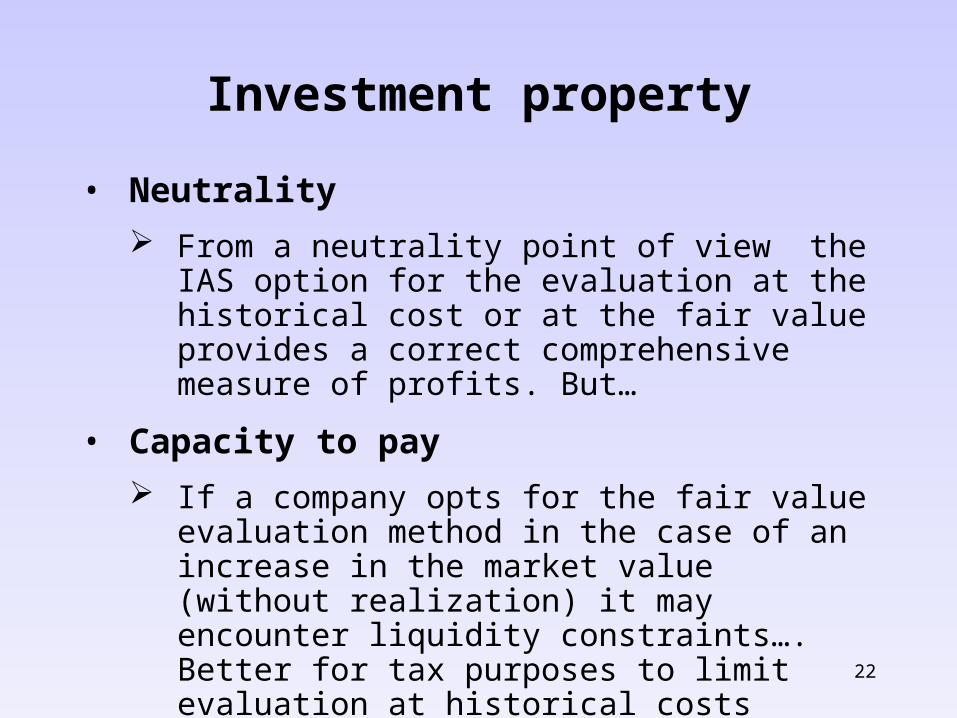

• Neutrality

From a neutrality point of view the IAS option for the evaluation at the historical cost or at the fair value provides a correct comprehensive measure of profits. But…

• Capacity to pay

If a company opts for the fair value evaluation method in the case of an increase in the market value (without realization) it may encounter liquidity constraints…. Better for tax purposes to limit evaluation at historical costs

23

Post-employment benefits (defined benefit plans)

• Neutrality Actuarial evaluation of assets and liabilities related to plans

would give a real picture of the assets and liabilities of a company. But in general the actuarial evaluation of defined benefit plans could:

• give room to uncertainty and discretion • increase compliance costs, tax avoidance (related to differences in the

actuarial methods of valuation), legal disputes• Since under certain conditions actuarial gains and losses are recognised

this would affect the capacity of the firm, in case of capital gains.

• Certainty/stability/enforceability/capacity to pay It would be better not to consider actuarial gains and losses

related to these benefit plans in the taxable income.

![Linda Giannini and Carlo Nati1 [Esep-teachers]. Linda Giannini and Carlo Nati2 Teacher Group Adrian Anton - Romania - Linda GianniniLinda Giannini - Italy.](https://static.fdocuments.us/doc/165x107/5542eb65497959361e8d0bcf/linda-giannini-and-carlo-nati1-esep-teachers-linda-giannini-and-carlo-nati2-teacher-group-adrian-anton-romania-linda-gianninilinda-giannini-italy.jpg)