1 Lahore Stock Exchange (LSE) “Continuous Professional Development” December 2011 Pakistan’s...

43

1 Lahore Stock Exchange (LSE) “Continuous Professional Development” December 2011 Pakistan’s Capital Markets: Current Challenges Presentation by : Muhammad Farid Alam, FCA Chief Executive Officer AKD Securities Limited

-

date post

19-Dec-2015 -

Category

Documents

-

view

213 -

download

0

Transcript of 1 Lahore Stock Exchange (LSE) “Continuous Professional Development” December 2011 Pakistan’s...

1

Lahore Stock Exchange (LSE)“Continuous Professional Development”

December 2011

Pakistan’s Capital Markets: Current Challenges

Presentation by : Muhammad Farid Alam, FCA

Chief Executive Officer

AKD Securities Limited

2

Contents

AKD Securities Limited

Economy & Capital Markets

Equity Market of Pakistan

Debt Market of Pakistan

Challenges for Capital Markets

The Way Forward

3

AKD Securities Limited

4

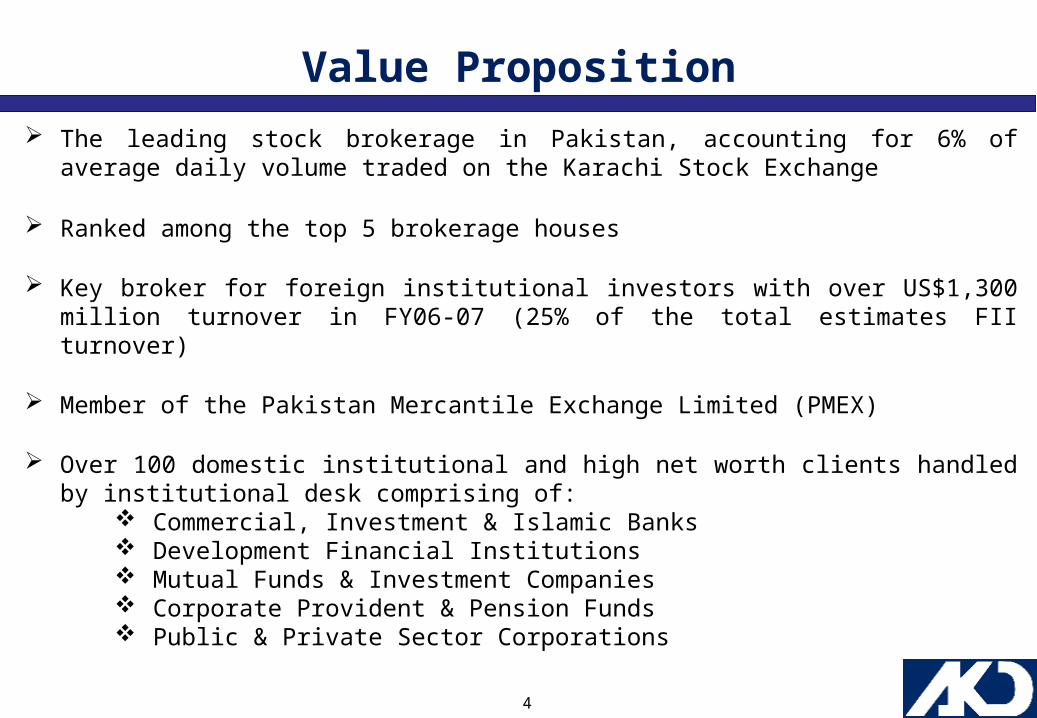

Value Proposition The leading stock brokerage in Pakistan, accounting for 6% of average daily

volume traded on the Karachi Stock Exchange

Ranked among the top 5 brokerage houses

Key broker for foreign institutional investors with over US$1,300 million turnover in FY06-07 (25% of the total estimates FII turnover)

Member of the Pakistan Mercantile Exchange Limited (PMEX)

Over 100 domestic institutional and high net worth clients handled by institutional desk comprising of:

Commercial, Investment & Islamic Banks Development Financial Institutions Mutual Funds & Investment Companies Corporate Provident & Pension Funds Public & Private Sector Corporations

5

Recognition

AKD Securities Limited is a proud recipient of “The Best Equity Brokerage House” Award for the years 2005-06 and 2006–07, awarded by the ‘CFA Association of Pakistan’.

The globally recognized business journal ‘Asia Money’ conducted a survey, focused on the quality of brokerage firms, with renowned international portfolio fund managers and ranked AKD Securities Limited as the 2nd Best Local Brokerage, 2nd Best Overall Country Research, and 3rd Best Overall Sales Services.

6

First brokerage firm to launch Online Stock Trading Service in 2002, and now a leading franchise in this space

Largest customer base with 7,000 registered clients out of a total market size of approximately 19,000 and contribution significantly to overall broking revenues

Marketing joint-venture & co-branding with Standard Chartered Bank for their online Priority Banking Clientele which allows immediate funds transfer facility to AKD’s broking account while enjoying the banking facilities of SCB

Only online trading service provider with fully dedicated customer call-centre support having trained staff

Dedicated research portal enabling online customers to be fully informed about market & corporate developments, with access to reports on par with institutional investors

AKD Trade

7

Investment Banking Successful track record of

completing huge capital market transactions

Extensive understanding and experience of structuring and executing complex debt & equity transactions

Financial strength to commit resources for large underwriting and participation

In-depth knowledge of investor demand & appetite

Widespread distribution capabilities to a diversified client network through experienced distribution team

Close working relationship and credibility with key regulatory agencies

Experienced senior resources to ensure swift completion of transactions

We believe that with our in-depth understanding of Pakistan’s capital markets, qualified management, and prior experience, we are best positioned to provide our clients the level of services required for making every transaction a resounding success.

8

Investment Banking AKDS has assembled a core team of expert professionals with a high level of integrity,

financial acumen and industry experience. Driven by young and skilled professionals, the team has initiated and successfully executed transactions unique in structure and size.

The team has been involved in numerous Initial Public Offerings, Acquisitions, providing risk capital in underwritings, market-making, various TFC issuances & Asset-back Securitization as well as leading Privatization deals in the country.

AKDS was selected as advisor for IPO of UBL by the Government of Pakistan. It was the BUYSIDE advisor for NRL privatization which was acquired by the Attock Oil Group.

AKDS was also mandated as sell-side advisor to Continental Biscuits Limited for the strategic sale of stake to The Danone Group, France.

The consortium of AKDS, Morgan Stanley and Detusche was mandated as the consultants to the GDR of National Bank of Pakistan (on hold)

As Financial Advisors, AKDS has successfully consummated the acquisition of a listed commercial bank by a well known Saudi bank and have acted as Joint Financial Advisors for the 100% Rights Issue of The Bank of Khyber of up to PkR 2,552mn.

9

Economy & Capital Markets

10

Phase EconomyFiscal Policy

Short-Term Rates

Asset Class

Initial Recovery

•Inflation still declining Stimulatory Low / Declining

Cyclical shares, commodities and other riskier assets

Early Upswing

•Healthy economic growth

•Inflation remains low Moving Up

Shares and real estate

Late Upswing

•Inflation gradually rises

Restrictive RisingBonds, interest rate sensitive shares

Slowdown•Inflation continues to

accelerate Peaking

Bonds, interest rate sensitive shares

Recession

•Inventory correction begins

•Inflation peaks•Production declines

DecliningShares (late in cycle), Commodities (late in cycle)

Phases of an Economy

11

Initial Recovery

The Economy of Pakistan

12

Note: FY12B is GoP estimates. FY12AKD is AKD Research Estimates

FY09A FY10A FY11A FY12B FY12AKD

Real GDP growth (%) 1.7 3.8 2.4 4.2 3.50-3.75

Agri growth (%) 4 0.6 1.2 3.4 2.5

Manufacturing growth (%) -3.6 5.5 3.0 3.7 3.0

Services growth (%) 1.7 2.9 4.1 5.1 4.5

Federal budget deficit % of GDP 5.3 6.3 5.7 4.0 5.75

Tax to GDP (%) 9.5 10.1 10 10.3 10.3

Average CPI Inflation Rate (%) 20.8 11.7 14.1 12.0 12.1

Foreign direct investments (US$bn) 3.7 2.2 1.5 2.5 1.5

Exports as % of GDP 11.8 11.1 12.7 12.7 12.5

Imports as % of GDP 19.6 17.6 13.6 17.8 18.0

Current Account as % of GDP -5.7 -1.7 0.5 -0.6 -1.03

Inward Remittances (US$bn) 7.8 8.9 11.2 12.2 12.5

Forex reserves (US$bn) 12.4 16.8 17.5 18.0 16.0

Exchange rate (PkR/US$) 66 84 87 88 91.5

External debt % of GDP 29 28 31 32 30

Actual Budgeted Forecasted

The Economy of Pakistan - Snapshot

13

15

% FY20106.0%

5.4% Emerging Markets

Developed Markets

5.0%

4.0%

3.0%

2.0% 1.7%

1.0%

0.0%Emerging Markets

Developed Markets

Source: EIU; April 2010

Economic Growth Growth is expected to come out of the Emerging Markets because all variables i.e. – consumption, savings etc. are at the lower side.

On the other hand the same variables have reached saturation amongst the Developed Markets.

14

21

Debt % of GDP

90

80

70

60

50

40

29 DEC 2000 – 31 DEC 2009

Developed Markets

Emerging Markets30

20'00

Source: Factset; EIU; April 2010

'01 '02 '03 '04 '05 '06 '07 '08 '09

- Developed Markets : G7. Emerging Markets : 87 non-OECD Countries

- Total domestic, external and IMF government debt, as a % of nominal GDP

- Usually but not exclusively central government

Debt % of GDP

15

Over the past decade total market capitalization’s input in GDP increased phenomenally from 8% in FY01 and kept on growing with its peak during the golden years of 2006 and 2007

GDP Growth

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

FY

00

FY

01

FY

02

FY

03

FY

04

FY

05

FY

06

FY

07

FY

08

FY

09

FY

10

FY

11F

FY

12F

Manufacturing Agri Services GDP Growth

Capital Market Performance

KSE 100 Index

1,273 2,701

4,4726,218

9,55710,041

14,076

5,865

9,387

12,022

11,557

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

Dec

01

Dec

02

Dec

03

Dec

04

Dec

05

Dec

06

Dec

07

Dec

08

Dec

09

Dec

10

01-D

ec-1

1

Index

CAGR CY01-CY11 = 25%

KSE Performance (2001 – 2011)

FY01 FY02 FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY110%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

8% 10%

16%

25%

32%

37%

46%

37%

17%18% 18%

Market Cap. / GDP

16

Role of Capital Markets

Mobilization of long-term resources (capital raising avenue for corporates) & investment avenue of investors including retail

Intermediation Function – Distribution of these resources & investments in various viable projects

Mechanism of entry and exit in a quick and transparent manner

17

Advantages of Capital Markets

Advantages of capital markets to:

Government -

Sponsors –

Society -

Investors -

Regulators -

18

Equity Market of Pakistan

19

KSE-100 Index at a Glance

KSE 100 Index

1,273 2,701

4,4726,218

9,55710,041

14,076

5,865

9,387

12,022

11,557

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

Dec

01

Dec

02

Dec

03

Dec

04

Dec

05

Dec

06

Dec

07

Dec

08

Dec

09

Dec

10

01-D

ec-1

1

Index

CAGR CY01-CY11 = 25%

During the 90s market movement was sideways ranging between the levels of 1,000 to 2,000

The Decade That Was: The first decade of 21st century was eventful and saw de-regulation opening up the markets, consolidation, privatization, divestments by GoP worth USD 6.7bn that provided for currency stabilization (MCB – GDR) and later by the cursed domestic and international financial crisis

20

KSE Market Dynamics – Volatility is an Opportunity

The KSE-100 Index has posted a 10 year return CAGR of 25% however volatility has remained high historically. We view this as an opportunity to maximize returns. In view of expected spells of volatility following the sell-off in global markets, we believe proactive management can provide for above average market returns.KSE 100 Index CY01 CY02 CY03 CY04 CY05 CY06 CY07 CY08 CY09 CY10 CY11*High 1,550 2,701 4,604 6,218 10,303 12,274 14,815 15,676 9,846 12,031 12,682 Low 1,075 1,273 2,359 4,472 6,218 8,767 10,041 5,865 4,815 9,230 10,842

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011*

CY % -16% 112% 66% 39% 54% 5% 40% -58% 60% 28% -4%*CYTD

Difference between KSE-100 High & Low

44%

112%95%

39%

66%

40%48%

167%

104%

30%17%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011*

Market melt down 2005 and 2008

21

PER vs. EPS Growth (%) ROE (%) vs. PBVS (x)

2012 Dividend Yield (%)

6.0

7.0

8.0

9.0

10.0

11.0

12.0

13.0

14.0

6 9 12 15 18 21 24

EPS Growth (%) 2012

PER

(x)

201

2

Singapore

Hong Kong

Thailand

Malaysia

China

Philippines IndiaIndonesia

Regional Avg.

Pakistan 1.00

1.20

1.40

1.60

1.80

2.00

2.20

2.40

2.60

10 12 14 16 18 20 22

ROE (%) 2012

P/BV

(x)

201

2

Singapore Hong Kong

Thailand

Malaysia

China

Philippines

India

Indonesia

Regional Avg.

Pakistan

8.59

4.16 4.14 4.03 3.63 3.22 3.122.56 2.30

1.85

-1.0

2.03.0

4.05.06.0

7.08.0

9.010.0

Paki

stan

Thai

land

Hon

gKo

ng

Mal

aysi

a

Sing

apor

e

Reg

iona

lA

vg.

Phili

ppin

es

Indo

nesi

a

Chi

na

Indi

a

Pakistan Market Valuation vs Regional Markets

22

Features of Equity Markets in Pakistan

Exposure to Corporate GrowthProvides opportunity with some of Pakistan’s best corporate stories

Inflation ProtectionSale price will increase according to inflation if company will be able to pass through inflation

LiquidityEase of entry & exit with market mechanism ensuring availability of buyers and sellers

Higher Returns The KSE-100 Index has on averaged returned 25% p.a. since Dec’01

Ease of TradeOnline trading

Companies become SICK but Sponsors get HEALTHIER!!!

23

KSE-100 can reach 13,750 points by Jun’12 based on target price mapping

In absence of any catastrophic event, downside limited by: High dividend yield

(2012F: 8.6%) Corporate earnings

resilience Largely cash based

market

Market likely to focus on: Political situation & US relations World economy & stock markets Foreign funding release Central bank’s monetary policy Macroeconomic Performance

Flags for 2011-12

Key drivers to include: Corporate results & Earnings

outlook Interest rate / liquidity trajectory Release of U.S. / multilateral

funding Actual vs. FY12 Budget targets Equity Market regulations

Check Points

Weather related agriculture sector failure

Commodity price shock

Fiscal indiscipline Major terrorism event Disruptive political change

KEY MACRO RISKS

Valuation expansion if political risk reduces, economic growth accelerates while monetary easing continues

KSE-100 Index can reach 14,250 points by Jun’12 if monetary easing sustains

Is it Bulls or Bears in Pakistan’s Equity Market?

24

Is it Bulls or Bears in Pakistan’s Equity Market?

25

Debt Market of Pakistan

26

Features Largest market size PkR 7trn M2 + NSS (PkR 6.6trn + PkR

1.7trn) compared to PkR 600bln size of equity market free-float which is less than 8% of fixed income

Certain and regular cash flows with lower volatility in comparison to equities

Two classes of investors: growing segment of investors with Islamic segment & normal fixed income seekers

Opportunities in Pakistani Fixed Income Medium to Long term investment:

• National Saving Certificates• Pakistan Investment Bonds• Sukuks• Term Finance Certificates

Short term investment:• T- Bills• Term Deposits in Banks• Investor Portfolio Security Account

Aug-0

8

Oct-0

8

Dec-0

8

Feb-

09

Apr-0

9

Jun-

09

Aug-0

9

Oct-0

9

Dec-0

9

Mar-1

0

May-1

0

Jul-1

0

Sep-

10

Nov-1

0

Jan-

11

Mar-1

1

May-1

1

Jul-1

1

Sep-

11

Nov-1

102468

1012141618

Pakistan Investment Bond Yield

Pakistan In-vestment Bond Yield

Fixed Income Market

27

Source: SBP

0

2

4

6

8

10

12

14

Pakis

tan

USA

UK

EC

B

Japan

Aust

ralia

Chin

a

India

South

Kore

a

Mala

ysi

a

Indonesi

a

Thailand -2.0

0.0

2.0

4.0

6.0

8.0

10.0

12.0

Policy Rate (%) LHS YoY Inflation (%)

Country Policy Rate (%) YoY Inflation (%)

Pakistan 12 10.90

USA 0-0.25 3.50

UK 0.5 5.00

ECB 1.25 3.00

Japan 0-0.10 -0.20

Australia 4.50 3.50

China 6.56 5.50

India 8.50 10.10

South Korea 3.25 3.90

Malaysia 3.00 3.40

Indonesia 6.00 4.40

Thailand 3.50 4.20

Fixed Income Market

The classical theory of positive RIR is now a myth!

28

Outlook of Fixed Income Securities

Declining interest rates provide opportunities for higher returns

With projection of decreasing interest rate, medium term fixed income instruments look attractive

Risks in Fixed Income Securities

Interest Rate Risk Reinvestment Risk Credit Risk Event Risk Inflation Risk

8/20

/200

8

10/1

3/20

08

12/6

/200

8

1/29

/200

9

3/24

/200

9

5/17

/200

9

7/10

/200

9

9/2/

2009

10/2

6/20

09

12/1

9/20

09

2/11

/201

0

4/6/

2010

5/30

/201

0

7/23

/201

0

9/15

/201

0

11/8

/201

0

1/1/

2011

2/24

/201

1

4/19

/201

1

6/12

/201

1

8/5/

2011

9/28

/201

1

11/2

1/20

110

2

4

6

8

10

12

14

16

18

Pakistan Investment Bond Yield

Pakistan Investment Bond Yield

Fixed Income Market

29

Challenges for Capital Markets

30

Challenges for Capital Markets in Pakistan

Capital markets move with overall economy - rather more sensitive

Lack of confidence amongst sponsors and investors – most wiped off

CGT/documentation and high handedness by tax authorities

Poor law & order conditions

Circular debt and energy crisis deteriorating company profitability, cash flow and balance sheets

Inconsistent policy response and reform implementation

Reluctance by sponsors to take viable companies to the stock market with limited response risk and lack of regulatory incentive

A required concerted effort by members to revive markets lowering mistrust and rebuilding relationships with regulators and stakeholders

“People of accomplishment rarely sat back and let things happen to them. They went out and happened to things.”

- Leonardo Da Vinci

31

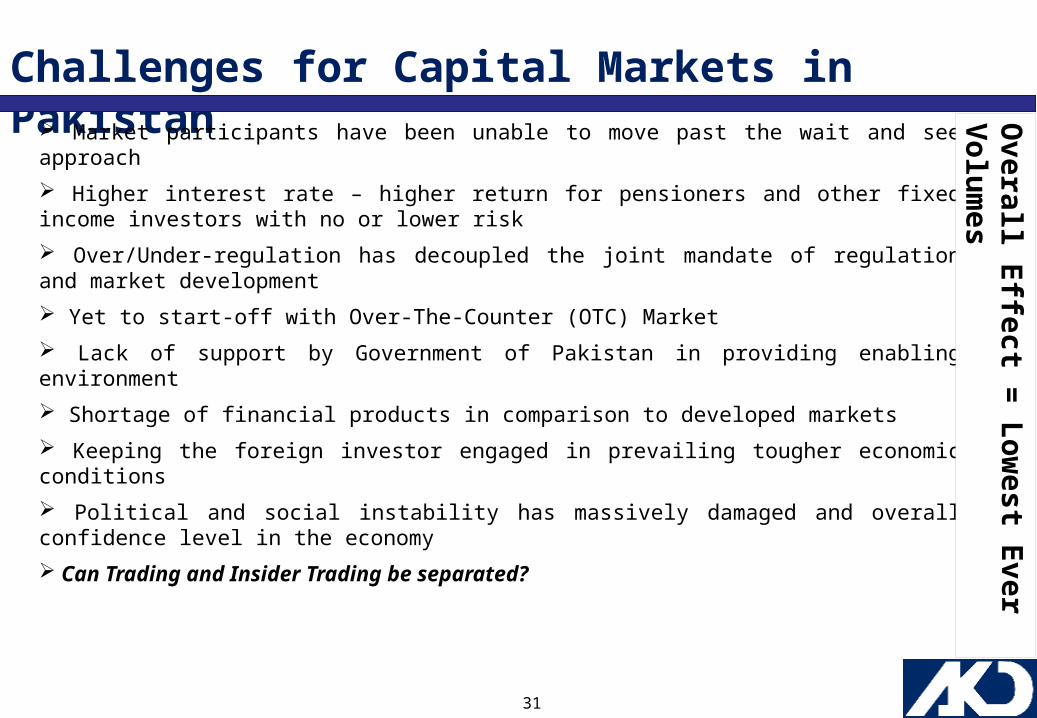

Challenges for Capital Markets in Pakistan Market participants have been unable to move past the wait and see approach

Higher interest rate – higher return for pensioners and other fixed income investors with no or lower risk

Over/Under-regulation has decoupled the joint mandate of regulation and market development

Yet to start-off with Over-The-Counter (OTC) Market

Lack of support by Government of Pakistan in providing enabling environment

Shortage of financial products in comparison to developed markets

Keeping the foreign investor engaged in prevailing tougher economic conditions

Political and social instability has massively damaged and overall confidence level in the economy

Can Trading and Insider Trading be separated?

Overall E

ffect = L

ow

est Ever V

olu

mes

32

South Asia Others3%Trading

2%

Equities Broking95%

Need for Re-defining Business Model

UK

Treasury25%

Interest Rate

Derivative20%

Fixed Income33%

Others11%

Information Sales

3%

Equities Broking

8%

Comparison of Products ( South Asia vs UK)

33

Sole Proprietorship

Partnership

Private Limited Company

Public Limited Company

LISTED Public Limited Company

Pathway to Glory – Phases Towards Listing

It is vital for local companies to get listed in the equity markets of our country not only for the enhancement and growth of the markets but also to gain access to a more convenient & robust form of capital raising

Year KSE No. of IPOs Amount Raised (USD mn)

2007 14,076 10 85

2008 6,037 9 66

2009 9,387 3 17

2010 12,022 6 62

2011 11,762 4 35

32 USD 265mn

Realization and efforts by all stakeholders to give depth to the market

34

KSE – Value & VolumeM

ar-

07

Ap

r-0

7M

ay

-07

Jun

-07

Jul-

07

Au

g-0

7S

ep

-07

Oct

-07

No

v-0

7D

ec-

07

Jan

-08

Feb

-08

Ma

r-0

8A

pr-

08

Ma

y-0

8Ju

n-0

8Ju

l-0

8A

ug

-08

Se

p-0

8O

ct-0

8N

ov

-08

De

c-0

8Ja

n-0

9Fe

b-0

9M

ar-

09

Ap

r-0

9M

ay

-09

Jun

-09

Jul-

09

Au

g-0

9S

ep

-09

Oct

-09

De

c-0

9Ja

n-1

0Fe

b-1

0M

ar-

10

Ap

r-1

0M

ay

-10

Jun

-10

Jul-

10

Au

g-1

0A

ug

-10

Oct

-10

No

v-1

0D

ec-

10

Jan

-11

Feb

-11

Ma

r-1

1A

pr-

11

Ma

y-1

1Ju

n-1

1Ju

l-1

1A

ug

-11

Se

p-1

1O

ct-1

1N

ov

-11

De

c-1

1

-

100.00

200.00

300.00

400.00

500.00

600.00

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

Volume (mn LHS) KSE-100 Index (RHS)

KSE-100 Index + Volume

35

If Volumes Don’t Improve…

36

Corporate Profitability – Is it intact?

• ACCOUNTING PROFITS REAL PROFITS

Numerous profit generating corporate entities in Pakistan are facing liquidity dry-outs recently, mainly due to the energy crisis and mounting circular debt

Growth in Earnings is essential but Dividends must increase in the same

proportion as well

37

Can Capital Markets Perform Independent of the Economy?

P un ja bG ove rn oras sassin at

ME NA cris ise sca late s

R aym on dD avisi ssuea ffe ctsP a k-UStie s

P M L - Np a r ts wa ysw i th P P Pi n P u n j a b

MTSlau n che d

A d d i t i o n a lr e v e n u em e a s u r e sa n n o u n ce da ft e r I M Ft a l k s

S e c u r i t i e sL e n d i n ga n dB o r r o w i n gP r o d u c tl a u n c h e d

US says Pa kistan no td oi ng en ou gh toco mb at m il itan cy

U S for ces k il lO sa m a BinL a de n inA b bo tta b ad

M o o d y ’sg i v e sa s su r a n ceo nP a k i s ta n ’ sso v e r e i g nd e b t

FY 1 2 B u d g e ta n n o u n ce d

MQ M pa rtsways fro mcoa lit io n

Se llo ff in lin ew ith g lo ba leq ui ti es

D Rr e d u ce db y 5 0 b p s

D e te r i o r a ti n gl a w & o r d e ri n K h i

C P I t u m b l e sd u e t or e b a s i n g

G l o b a lr e c e s s i o nco n c e r n s +U S p r e ss u r eo n P a k i st a n

1 0 ,5 0 0

11 , 00 0

11 , 50 0

1 2 ,0 0 0

1 2 ,5 0 0

1 3 ,0 0 0

J a n -11 F e b -11 A p r-11 M a y -11 J u n -11 A u g -11 S e p -1 1 N o v - 11

U S a n n o u n c e sO p e r a ti o n Tw i s to n g l o b a lr e ce s si o n fe a r s

D R c u t b y1 5 0 b p s to1 2 %

F S V b e n e fi te n h a n ce d

C i r c u l a r d e b te x p o su r eco n v e r t e d t oG o P s e cu r i t i e s

P a k - I M FA r t i c l e IVta l ks

F B R t o e x a m i n es o u r c e o fi n v e s tm e n t i nc a p i ta l m kt s

N A T Oa tt a c k s a n dm e m os c a n d l e

38

Friendly Opposition

Political parties lack financial and economic

expertise

PTI talks about

revolution; Reality or Over-confidence?

Challenging Political Environment

I feel that the failure of Common-Wealth Games and success of China Olympics shows that Democracy may not be the solution to all the ills!

39

Lessons Learned

Imposition of floor was a disastrous decision

Failure of regulator to save the Non-Banking Financial Institutions (NBFIs)

Monopolistic scenario in the banking sectorCapital hoardingBig 5 only protecting their RoEEnjoying highest banking spreads

A few industries were over-leveraged due to which they had to face the music

Success stories like Engro and Nishat need to be respected rather than envied

Over-regulated equity market creates no value

•“Interfering with market mechanism BACKFIRES!!!”

The brokerage community in Pakistan was content with plain-vanilla trading services dealing primarily in the Ready Market which led to overdependence on market volumes and vulnerability in the earnings stream.

40

The Way Forward???

41

It has been a tough period for all financial markets since the economic meltdown began in 2008, but there is always a new beginning

Integration

Demutualization

IPOs to keep the primary markets alive

De-regulation

New products

Tax structure

Investor awareness

The Way Forward!!!

42

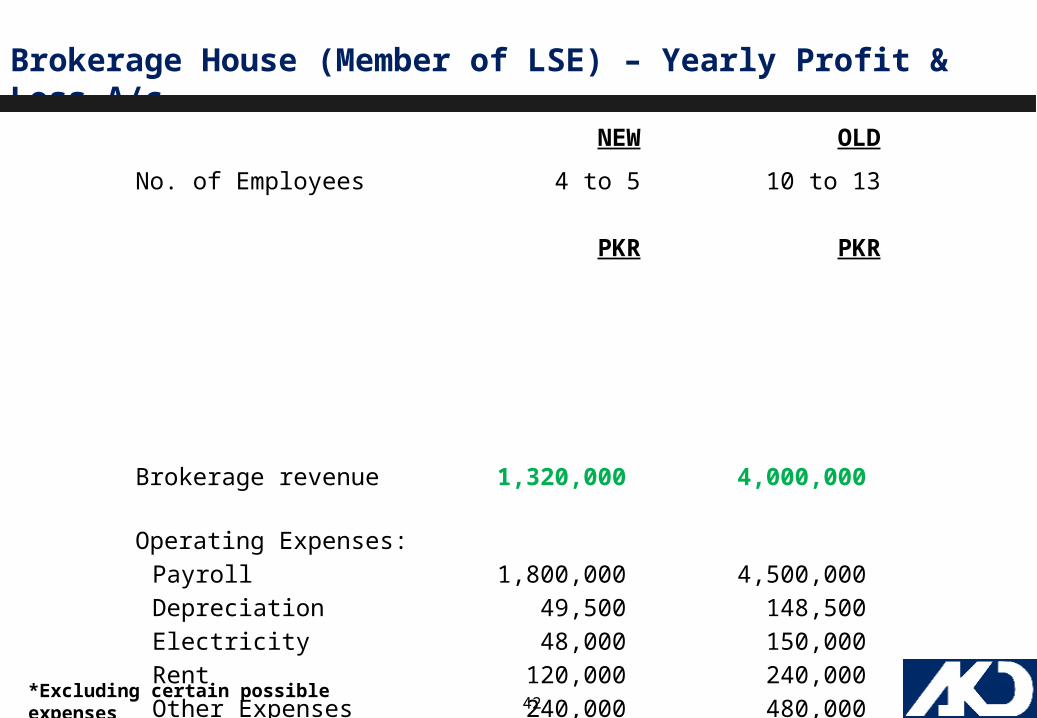

Brokerage House (Member of LSE) – Yearly Profit & Loss A/c

NEW OLD

No. of Employees 4 to 5 10 to 13

PKR PKR

Brokerage revenue 1,320,000 4,000,000

Operating Expenses:Payroll 1,800,000 4,500,000 Depreciation 49,500 148,500 Electricity 48,000 150,000 Rent 120,000 240,000 Other Expenses 240,000 480,000 Audit & Certification Fee 50,000 150,000

2,307,500 5,668,500

Net Loss Per Annum* (987,500) (1,668,500)

*Excluding certain possible expenses

43

Thank You!!!