1 Kestrelman Ltd The Global Steel Market in 2030 – Larger or Smaller? Fatter or Thinner? Roger...

36

1 Kestrelman Ltd The Global Steel Market in 2030 – Larger or Smaller? Fatter or Thinner? Roger Manser (ex-SBB founder/ managing editor) Metal Expert Europe Steel Trade Conference 2014

-

Upload

natalie-norris -

Category

Documents

-

view

217 -

download

2

Transcript of 1 Kestrelman Ltd The Global Steel Market in 2030 – Larger or Smaller? Fatter or Thinner? Roger...

1Kestrelman Ltd

The Global Steel Market in 2030 –

Larger or Smaller? Fatter or Thinner?

Roger Manser(ex-SBB founder/managing editor)

Metal Expert Europe Steel Trade Conference 2014

2Kestrelman Ltd

Structure of presentation

1. What is the big picture? The industrial revolution, steel and global warming

2. Future economic growth, steel demand and production:

- business as usual or - a climate change consistent (CCC)

scenario

3. Conclusions

3Kestrelman Ltd

The big picture: the industrial revolution, steel & global warming

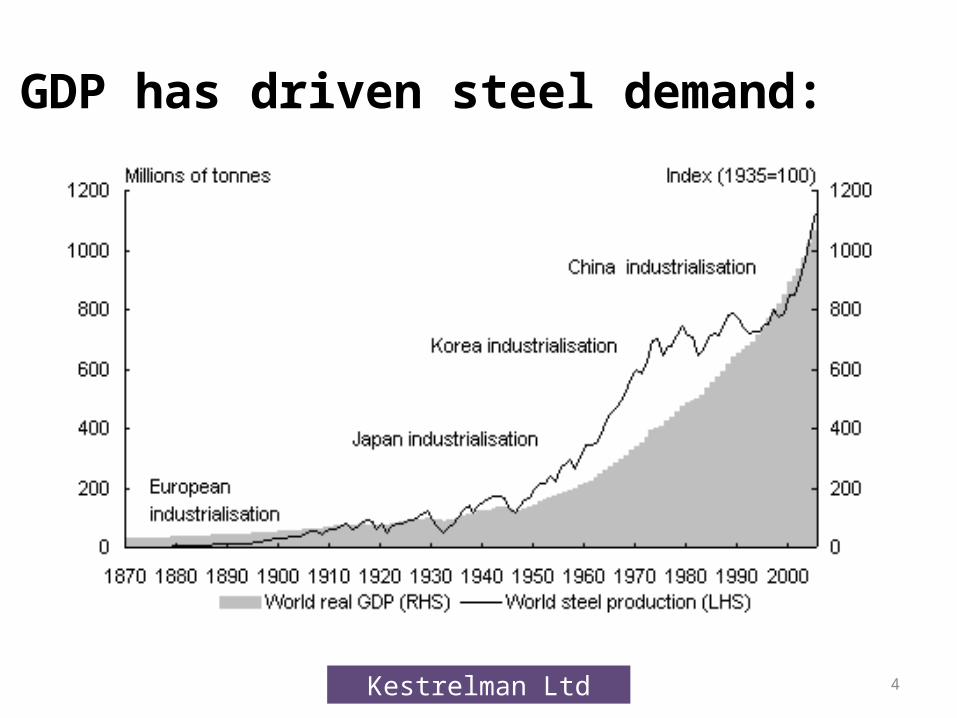

What was the “Industrial Revolution? An economic explosion from the 18 century onwards, which enabled real incomes to overtake population expansion, resulting in exponential GDP rises globally

A step change in innovation/ technology involving much greater productive use of coal & oil, as well as iron, and then steel

But with CO2 from burning fossil fuels as the by-product

4Kestrelman Ltd

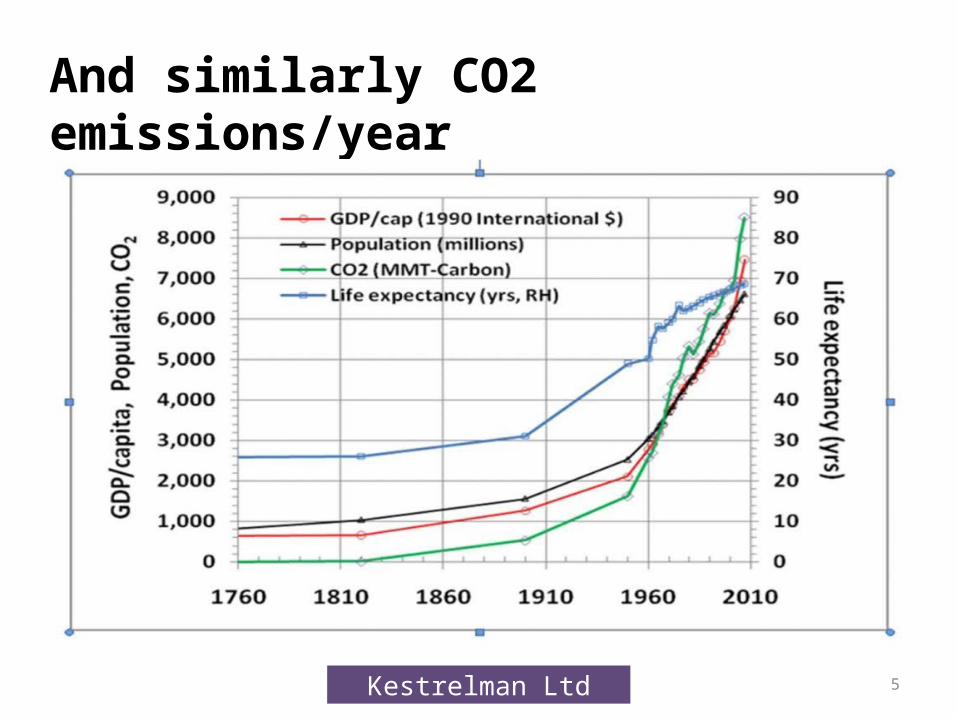

GDP has driven steel demand:

5Kestrelman Ltd

Steel

And similarly CO2 emissions/year

6Kestrelman Ltd

So pictorially, we move from this in 1750

Thmas Gainsborough. Mr. and Mrs. Andrews c.1750, NG, London

7Kestrelman Ltd

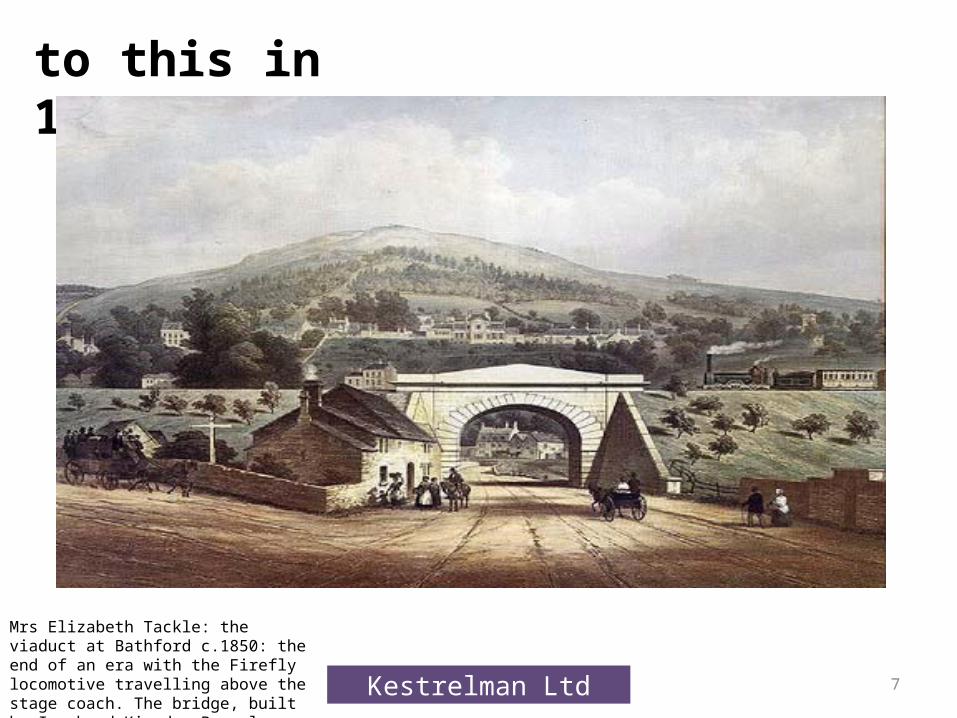

to this in 1850

Mrs Elizabeth Tackle: the viaduct at Bathford c.1850: the end of an era with the Firefly locomotive travelling above the stage coach. The bridge, built by Isambard Kingdom Brunel , was completed in 1841.

8Kestrelman Ltd

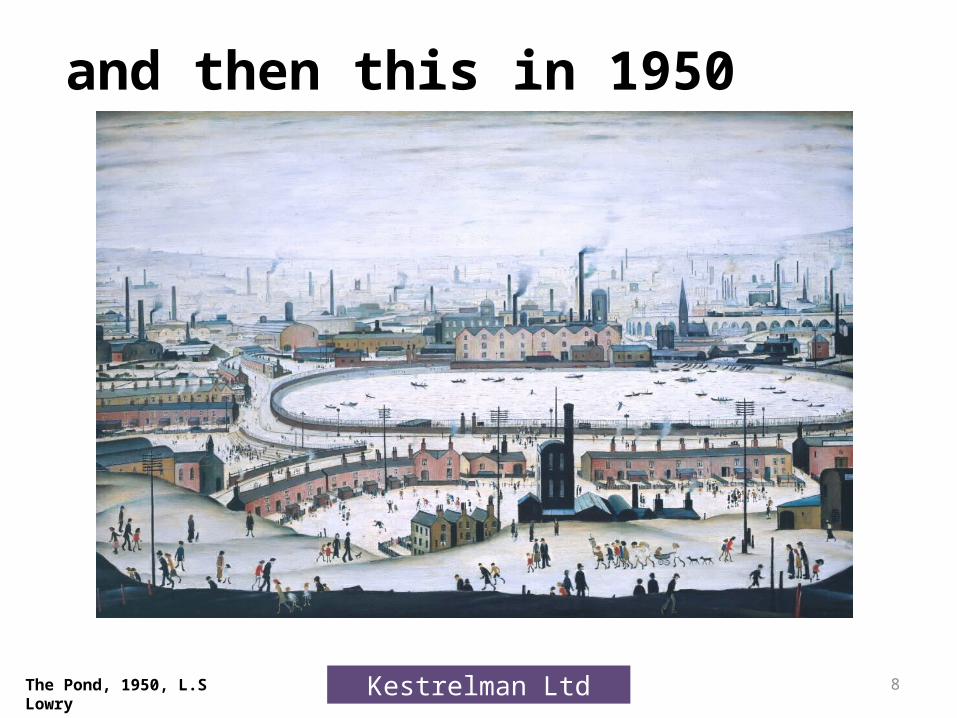

and then this in 1950

The Pond, 1950, L.S Lowry

9Kestrelman Ltd

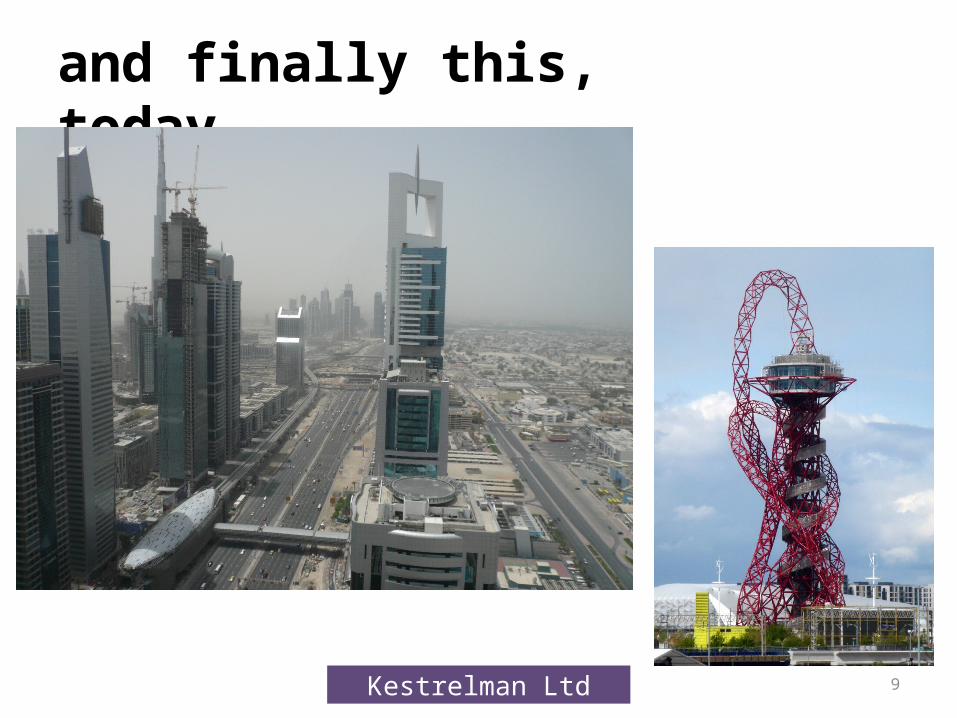

and finally this, today

10Kestrelman Ltd

Where are we in (in terms of world GDP & steel demand) in 2014? (1)

Coming out of a large global financial bubble: GDP growth picking up bit-by-bit

China’s GDP still growing fast economically (7-7.5%), but now rebalancing away from investment towards consumption (NB lower steel growth, but from a much bigger base)

Most other emerging markets are also expanding, but more slowly than in recent years, as lack finance with China’s raw material imports grow only gradually

11Kestrelman Ltd

Where are we in (in terms of world GDP & steel demand) in 2014? (2) Infrastructure and construction remain the key users of steel, powered by economic growth, as in India, Turkey, Mexico, Korea, Indonesia, Africa etc

Developed countries are growing too, but in a less steel intensive way (eg robots, internet, )

Production overcapacity – continues to put pressure on finished prices

Many questions about the pace and direction of future economic growth, due to climate change and other geo-political questions

12Kestrelman Ltd

t/m

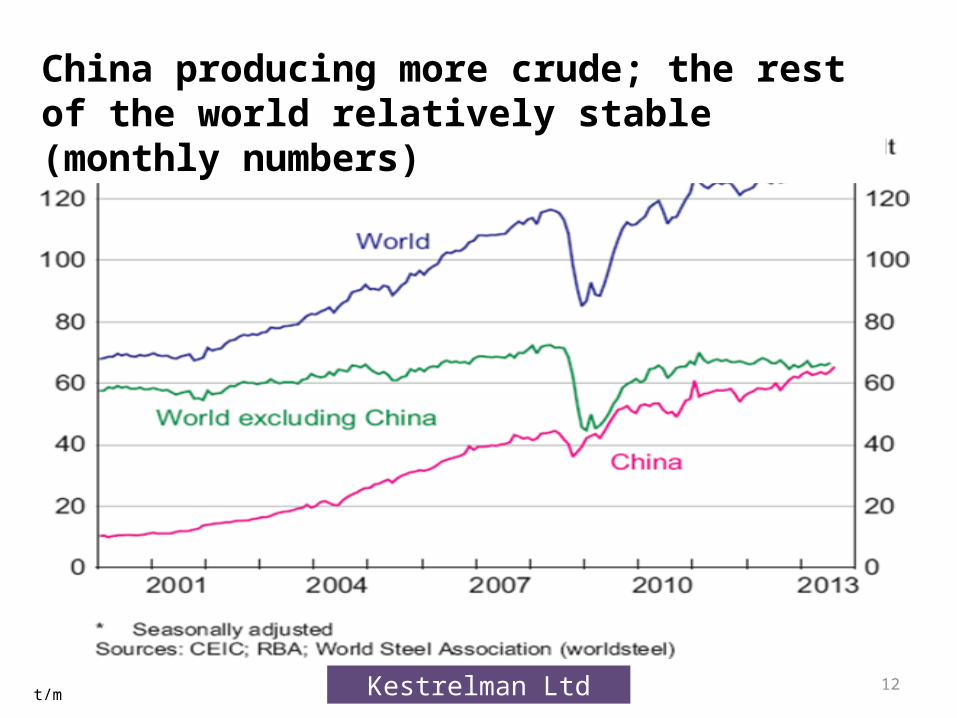

China producing more crude; the rest of the world relatively stable (monthly numbers)

13Kestrelman Ltd

Let’s contrast:

Business as Usual (BAU): 2-3%/yr growth, the consensus scenario: compares with 5-10% pre-crisis

A Climate Change Consistent (CCC): 1%/yr growth – a scenario reflecting lower GDP growth, less fossil fuel use, and resource/ CO2 constraints in steel production

The future world demand for steel?

14Kestrelman Ltd

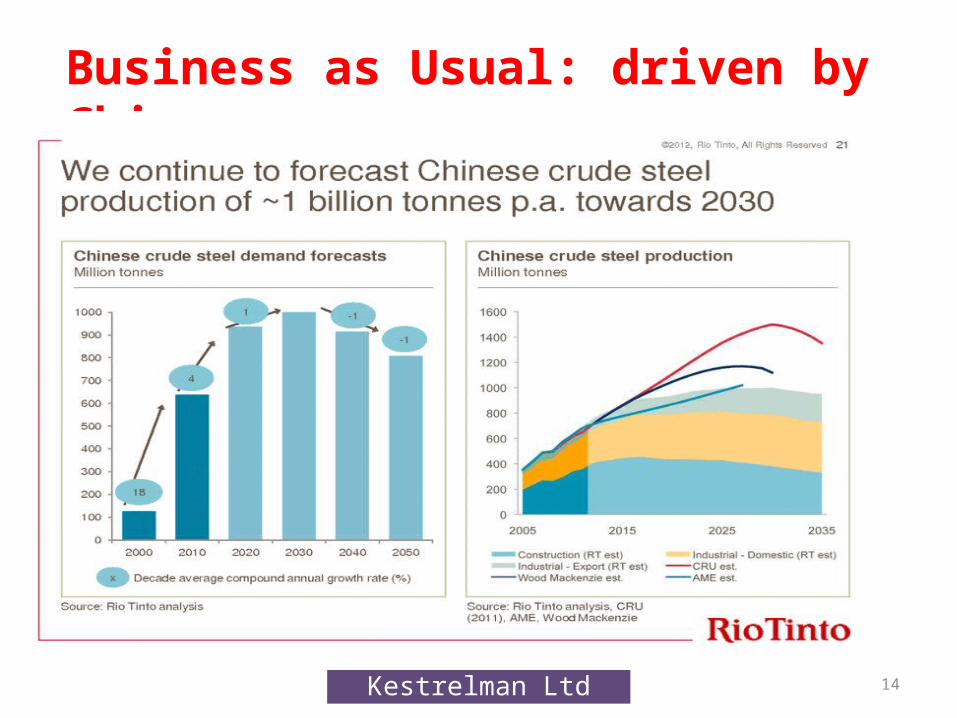

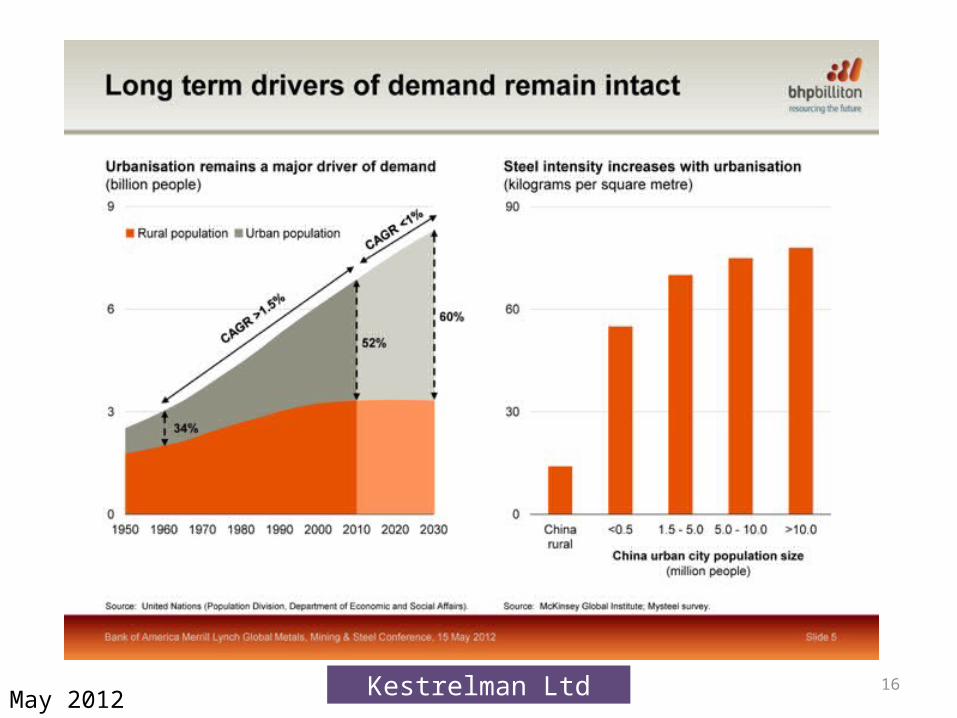

Business as Usual: driven by China

15Kestrelman Ltd

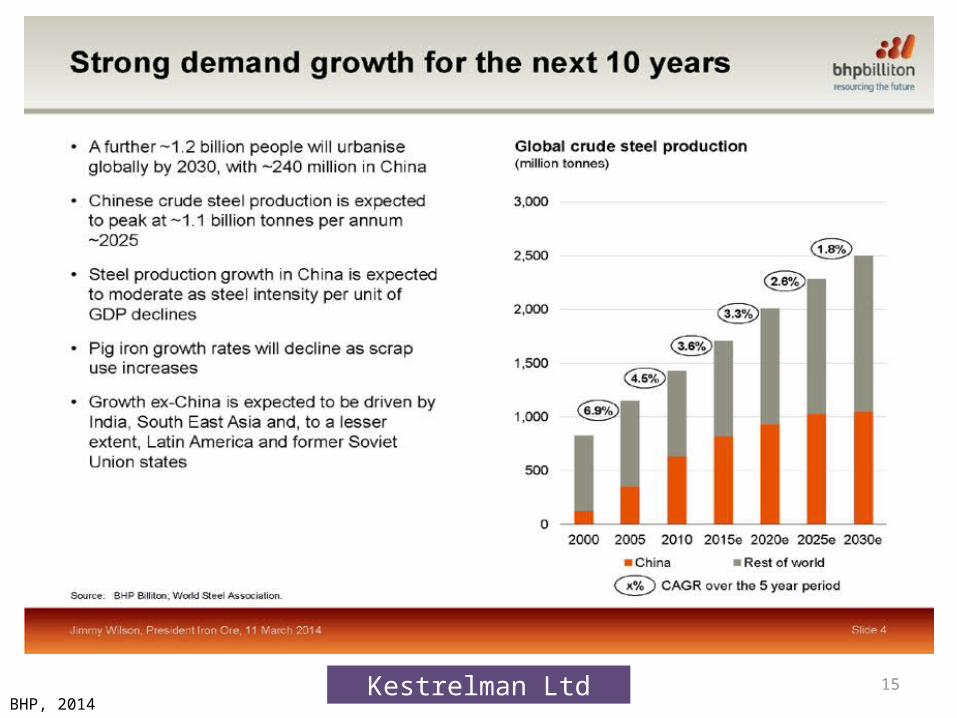

BHP, 2014

16Kestrelman Ltd

May 2012

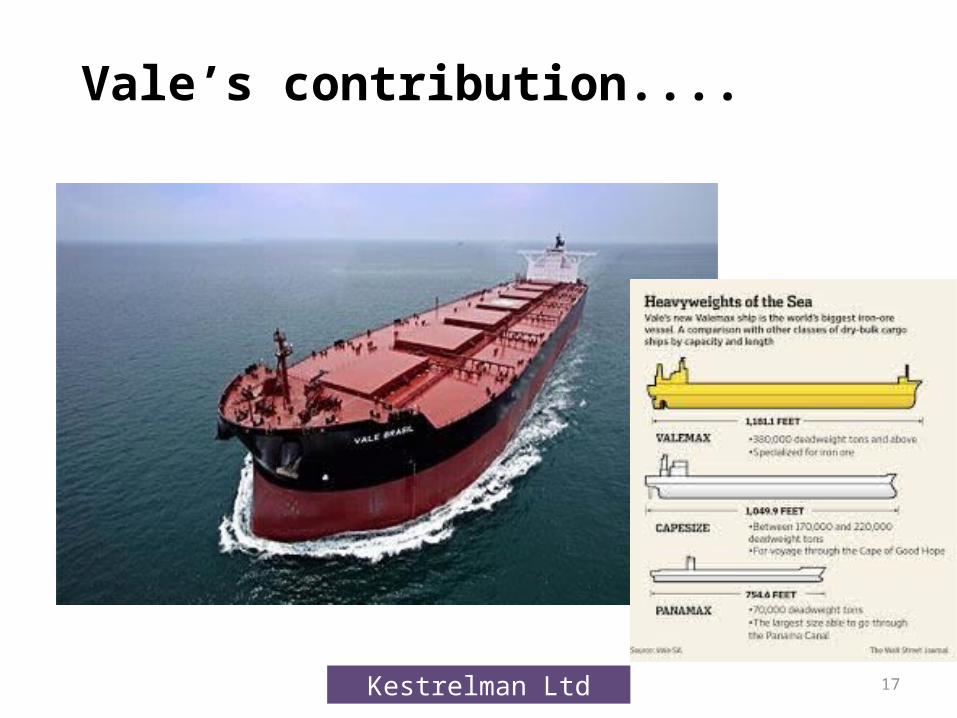

17Kestrelman Ltd

Vale’s contribution....

18Kestrelman Ltd

“We can expect growing pressure points around water, food, and energy scarcity as the century progresses...Hovering over all of this is the merciless march of climate change.” –

Christine Lagarde, Managing Director, International Monetary Fund. From her Richard Dimbleby lecture: February 2014

In Contrast: A Climate Change Consistent (CCC) scenario: much lower rates of growth in economy & steel demand...

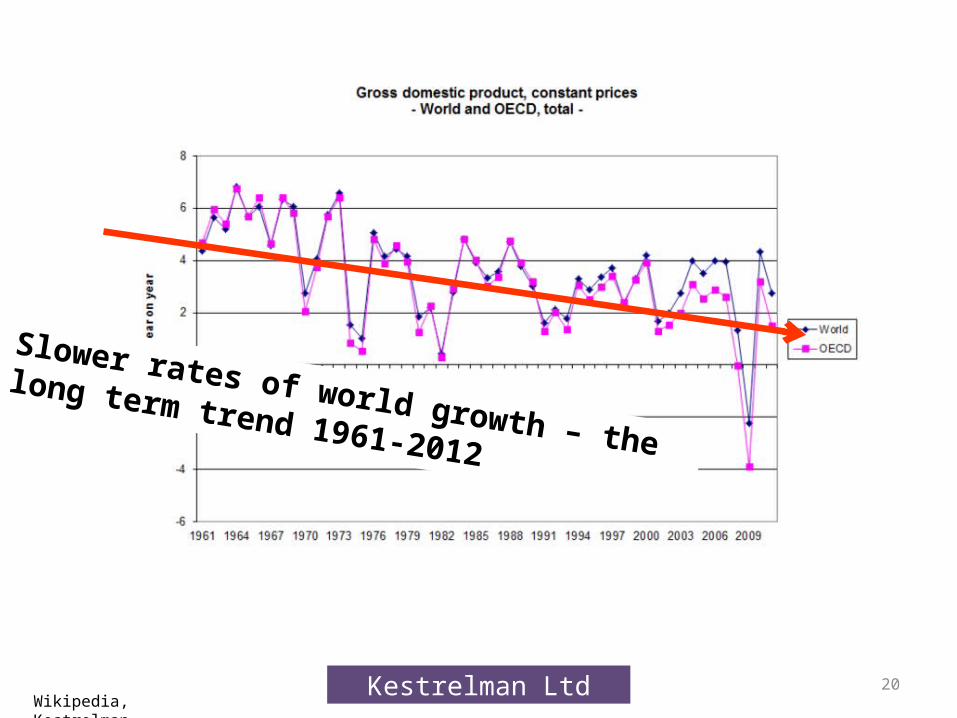

20Kestrelman LtdWikipedia, Kestrelman

Slower rates of world growth – the long term

trend 1961-2012

21Kestrelman Ltd

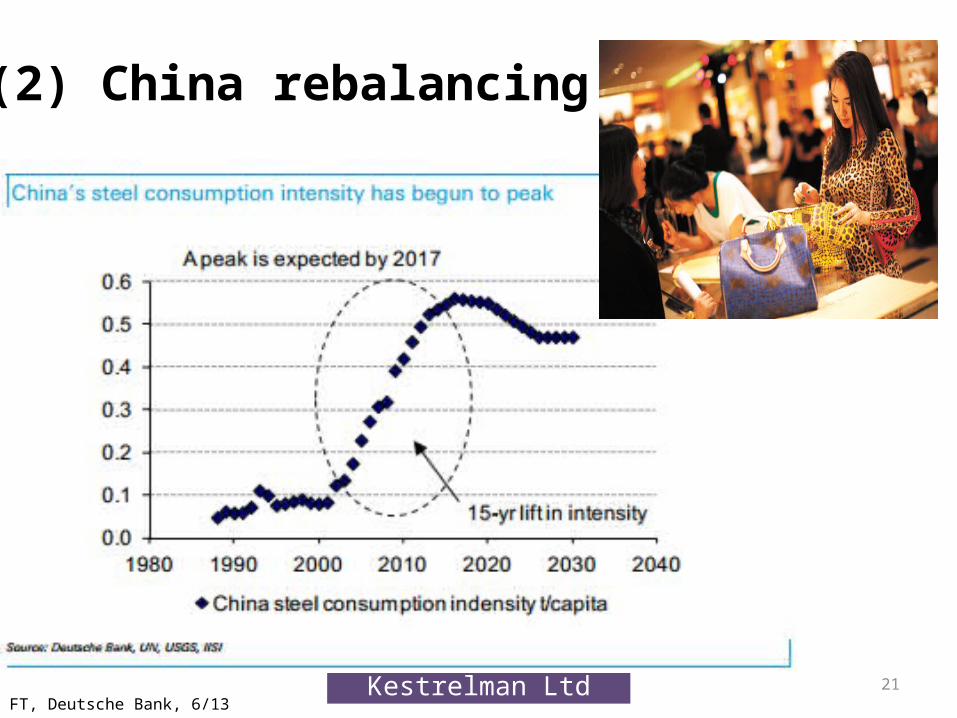

(2) China rebalancing

FT, Deutsche Bank, 6/13

22Kestrelman Ltd

China’s economic growth is becoming less steel intensive

Steel Ease: China steel demand 2011-2030, Oct 2013

23Kestrelman Ltd

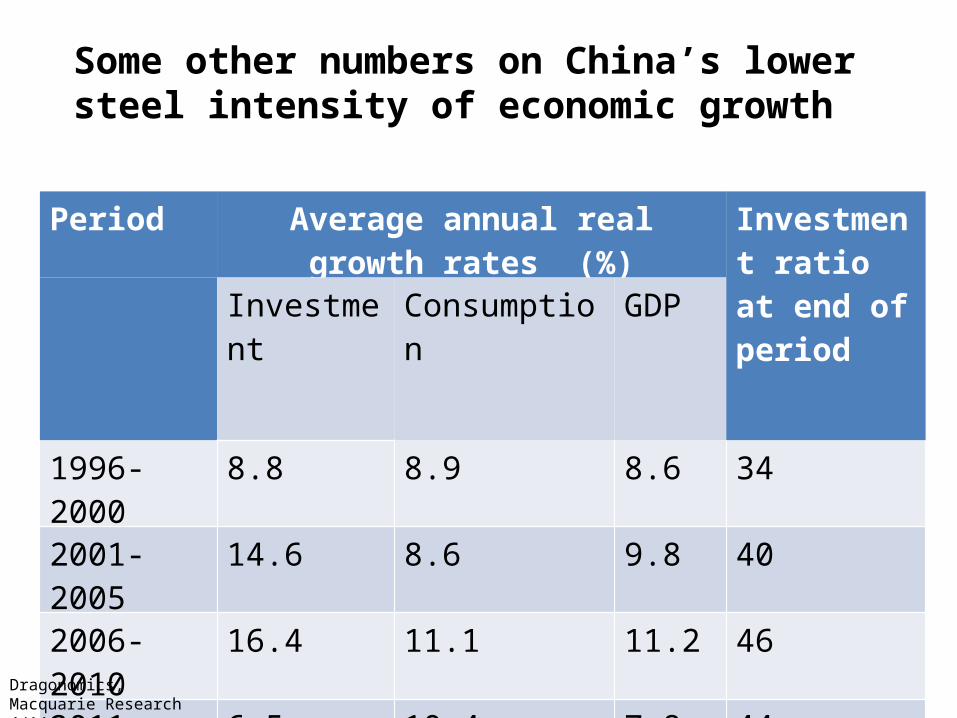

Some other numbers on China’s lower steel intensity of economic growth

Period Average annual real growth rates (%)

Investment ratio at end of periodInvestment Consumption GDP

1996-2000 8.8 8.9 8.6 34

2001-2005 14.6 8.6 9.8 40

2006-2010 16.4 11.1 11.2 46

2011-2015 estimate

6.5 10.4 7.8 44

2016-2020 forecast

3.2 9.8 6.7 39Dragonomics, Macquarie Research 4/14

24Kestrelman Ltd

And per unit of GDP output [not per head]

25Kestrelman Ltd

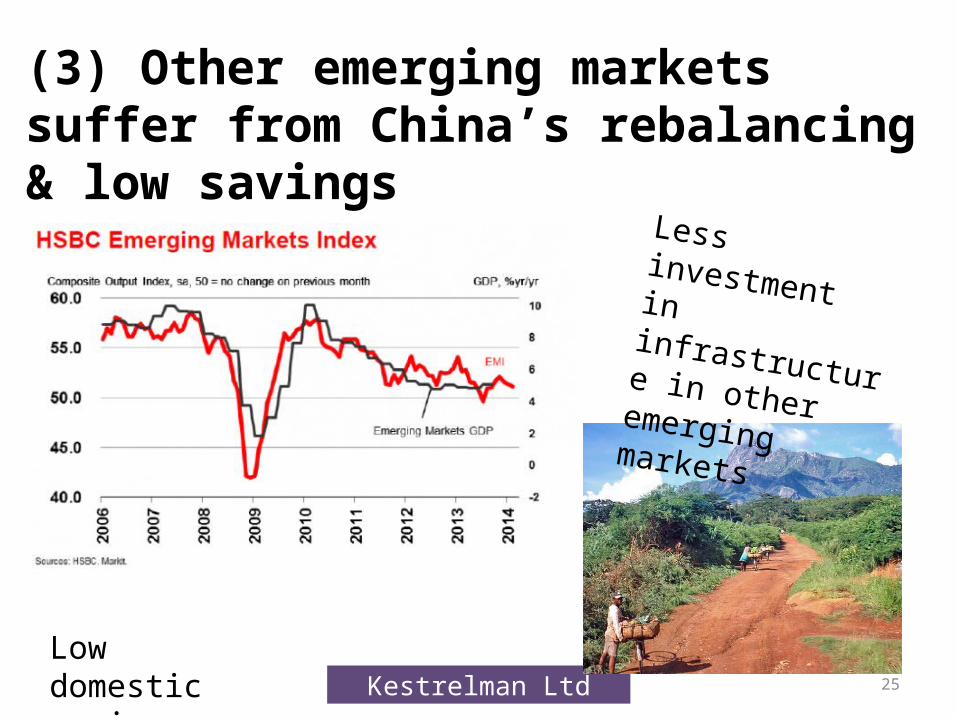

(3) Other emerging markets suffer from China’s rebalancing & low savings

Less investment in infrastructure in other emerging markets

Low domestic savings rates

26Kestrelman Ltd

(4) Climate change: more renewable power generation, as CO2 price rises

€30-40/t/CO2

27Kestrelman Ltd

Accompanied - perhaps - by less investment in fossil fuel power generation?

Higher oil prices?

Lower coal prices?

And natural gas prices: up? or down?

28Kestrelman Ltd

And – perhaps - more steel in pipelines for oil, gas & carbon dioxide (CCS), heat/energy storage, as well as nuclear power

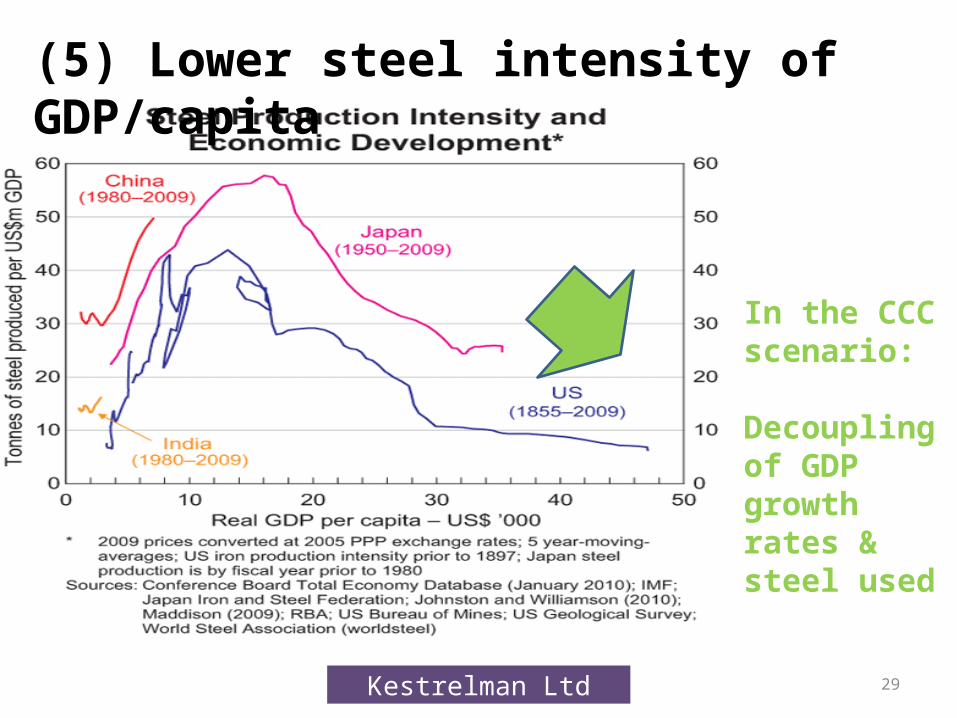

29Kestrelman Ltd

(5) Lower steel intensity of GDP/capita

In the CCC scenario:

Decoupling of GDP growth rates & steel used

30Kestrelman Ltd

(6) Climate change: less steel

Light-weighting: much less steel in cars: lower CO2 emissions/km

By 2020, less than half the weight of a European car will be ferrous (vs almost 80% in 2000)

31Source: OICA, Taub et al, analysis by Roger Emmott

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Other metals

Glass

Other materials

Plastic/composites

Aluminium

High/medium strength steel

Other ferrous

32Kestrelman Ltd

A lower rate of growth (eg 1%) in steel consumption seems possible, if not probable in the period to 2030

Steel-making overcapacity will continue, as crude steel production utilisation rates may well remain low

Over the next 20 years, concerns about climate change will increase – [was the fossil-fuelled/steel-based industrial revolution a one-off event?]

Lower growth rates in steel demand in the coming 20 years likely

33Kestrelman Ltd

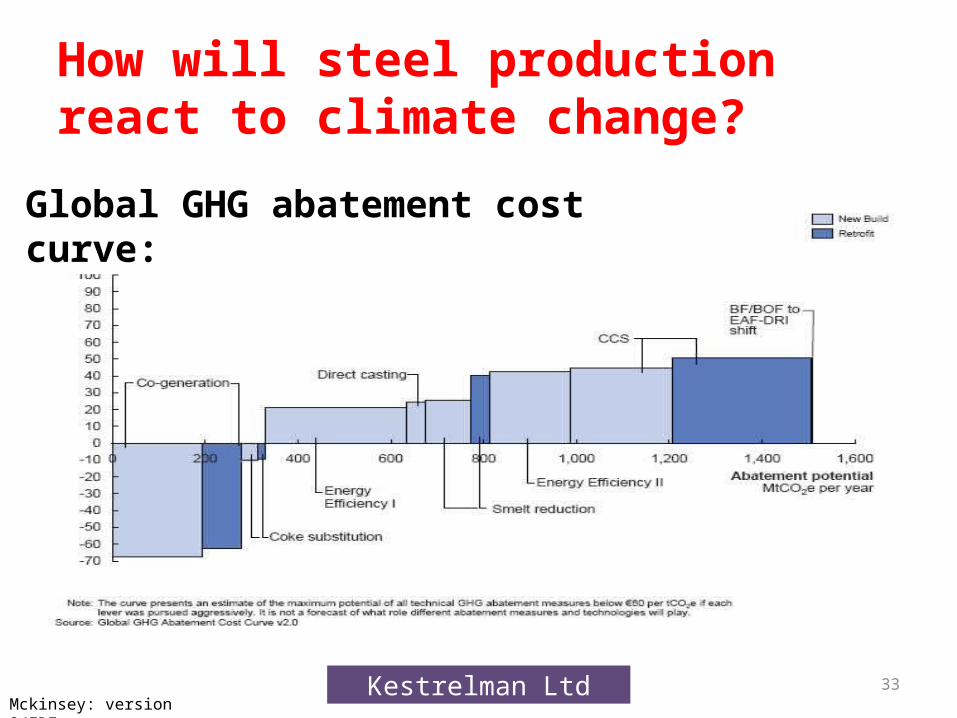

How will steel production react to climate change?

Global GHG abatement cost curve:

Mckinsey: version 2/EDF

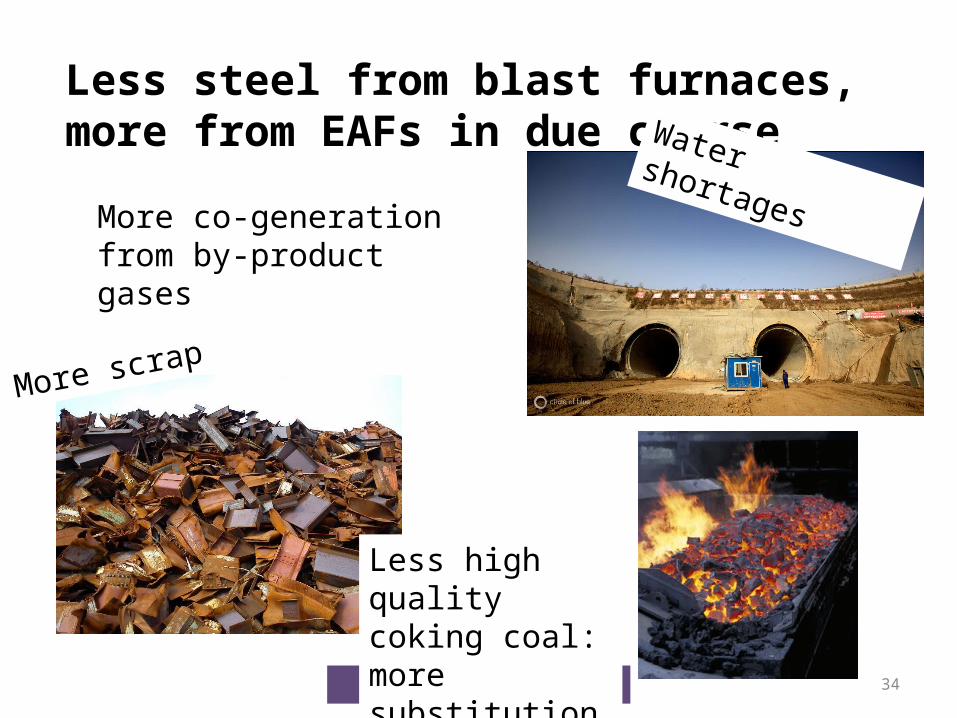

34Kestrelman Ltd

Less steel from blast furnaces, more from EAFs in due course Water shortages

More scrap

Less high quality coking coal: more substitution

More co-generation from by-product gases

35Kestrelman LtdCSC, Taiwan

Steel consumption: less demand and more alloys

36Kestrelman Ltd

Overall Conclusions

A larger or smaller market? Larger perhaps – some growth, but not as rapid as with BAU;

Some say that in tonnage terms, finished steel consumption might even decline.

More production from scrap/EAFs; possibly more from DRI

Fatter or thinner? A leaner industry: - more efficient, and producing more alloys, and if so, maybe lower tonnages and higher values

37Kestrelman Ltd

Thank You