1 JOINT ECB-MNB CONFERENCE Moving away from a cash-based payment system to a “less cash” society...

18

1 JOINT ECB-MNB CONFERENCE Moving away from a cash-based payment system to a “less cash” society Budapest November 2012

-

Upload

blaise-pearson -

Category

Documents

-

view

213 -

download

0

Transcript of 1 JOINT ECB-MNB CONFERENCE Moving away from a cash-based payment system to a “less cash” society...

1

JOINT ECB-MNB CONFERENCE

Moving away from a cash-based payment system to a “less cash” society

Budapest November 2012

2

Agenda Agenda

• Background of the Brazilian payment system

• Usage of means of payment

• Banking access channels

• The Central Bank’s involvement in the retail payment system

• Moving towards a “less cash” society

3

Background Background

• 2002 - Brazilian payment system reformObjective: Mitigation of systemic risk and credit risk

• 2005 - Report: Brazilian retail payment system diagnosisObjective: To map the retail payment system:

−Payment instruments’ usage−Banking service channels−Clearing and settlement infrastructure− Innovation in payment systems− International experience

• 2010 - Report: Payment card industry Objective: To conduct analysis and studies on competition

in the payment card industry.

4

The market of electronic means of payment The market of electronic means of payment

•High correlation between electronic payment instruments and bank accounts

•Percentage of the population that disposes of electronic means of payment has increased in the last years to 72.4% in 2011

− Debit Cards –> 60%

− Credit Cards –> 53%

− Retailer Cards –> 28%

•Use of electronic means of payment:− Monthly spending among the population –> 42%

− Monthly spending among the owners of electronic means –> 52%

Survey conducted by the Brazilian Association of Credit Card and Service Companies - ABECS

5

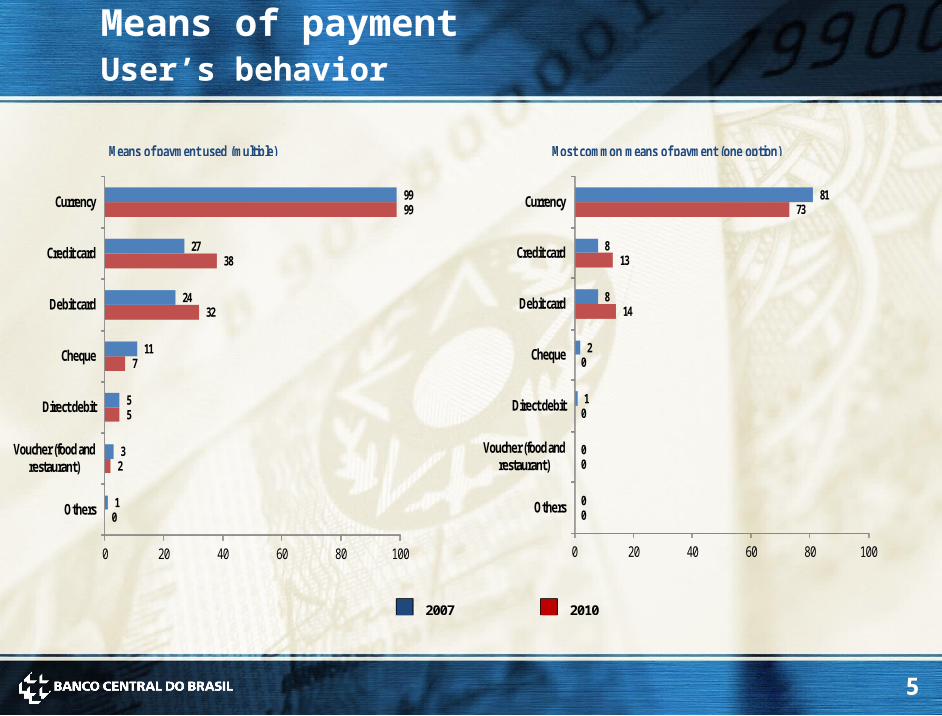

Means of payment User’s behavior

Most common means of payment (one option)Means of payment used (multiple)

1

3

5

11

24

27

99

0

2

5

7

32

38

99

0 20 40 60 80 100

Others

Voucher (food and restaurant)

Direct debit

Cheque

Debit card

Credit card

Currency

0

0

0

0

14

13

73

0

0

1

2

8

8

81

0 20 40 60 80 100

Others

Voucher (food and restaurant)

Direct debit

Cheque

Debit card

Credit card

Currency

2007 2010

6

Usage of access channels Volume of transactions

billion

Access channel

2006 2007 2008 2009

2010

2011

2006– 2011(%)

Internet banking 5.1 6.4 7.3 8.4 10.6 12.8 151

ATM 7.2 7.6 8.2 8.1 8.6 9.3 29

Branches 5.4 5.6 5.8 6.5 7.5 8.7 61

Banking agents 1.8 2.2 2.3 2.6 2.9 3.2 76

Call center 1.2 1.7 1.6 1.6 1.6 1.4 9

Wireless (cell phone, PDA) (million) 48 37

65 96 61 196 308

7

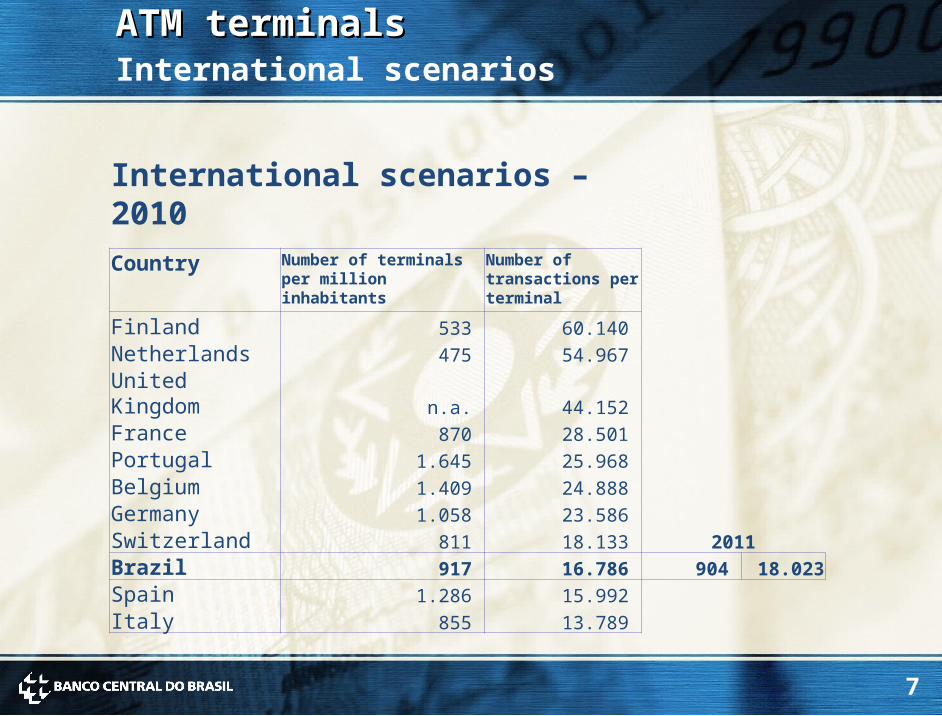

ATM terminalsATM terminals International scenarios

International scenarios – 2010

Country Number of terminals per million inhabitants

Number of transactions per terminal

Finland 533 60.140

Netherlands 475 54.967

United Kingdom n.a. 44.152

France 870 28.501

Portugal 1.645 25.968

Belgium 1.409 24.888

Germany 1.058 23.586

Switzerland 811 18.133 2011

Brazil 917 16.786 904 18.023

Spain 1.286 15.992

Italy 855 13.789

8

POS terminalsPOS terminals International scenarios

International scenarios – 2010

Country Number of terminals per million inhabitants

Number of transactions per terminal

Sweden 21.571 8.858

Belgium 12.663 7.714

United Kingdom 20.208 6.754

Flinland 37.476 5.174

Portugal 26.175 4.195

Germany 8.295 3.900

Switzerland 19.293 3.699 2011Brazil 17.925 1.828 18.275 2.404

Spain 30.149 1.626

Italy 24.920 1.228

9

Cost of payments in terms of percentage of GDP

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

Actual cost Cost with total migration to electronic payments

Comparison of cost electronic payment instruments x paper based instruments

Comparison of cost electronic payment instruments x paper based instruments

10

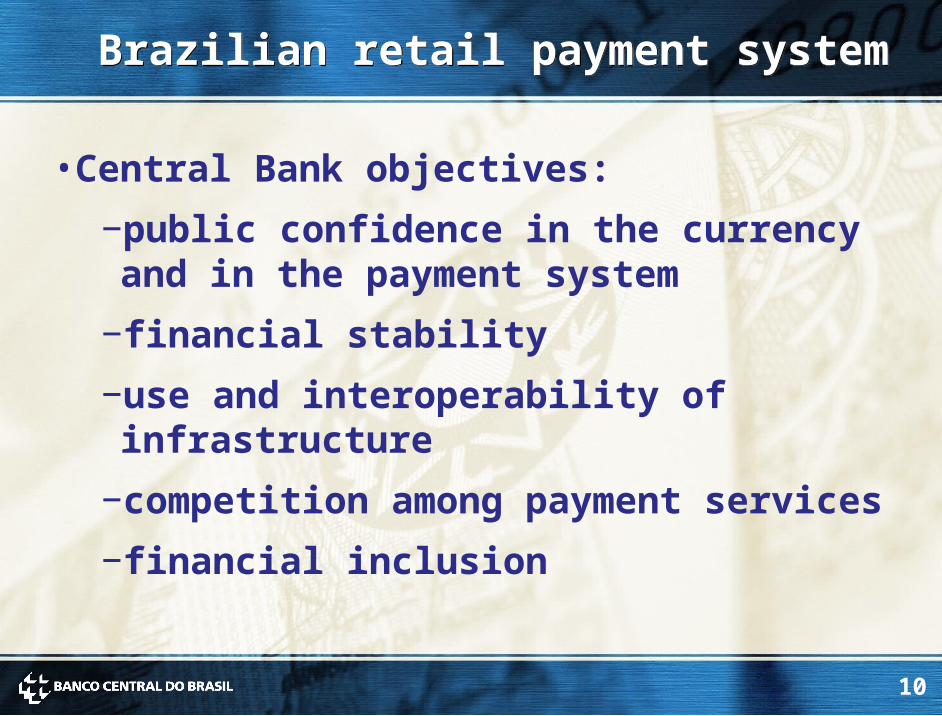

Brazilian retail payment system Brazilian retail payment system

•Central Bank objectives:−public confidence in the currency and in the

payment system−financial stability−use and interoperability of infrastructure−competition among payment services−financial inclusion

11

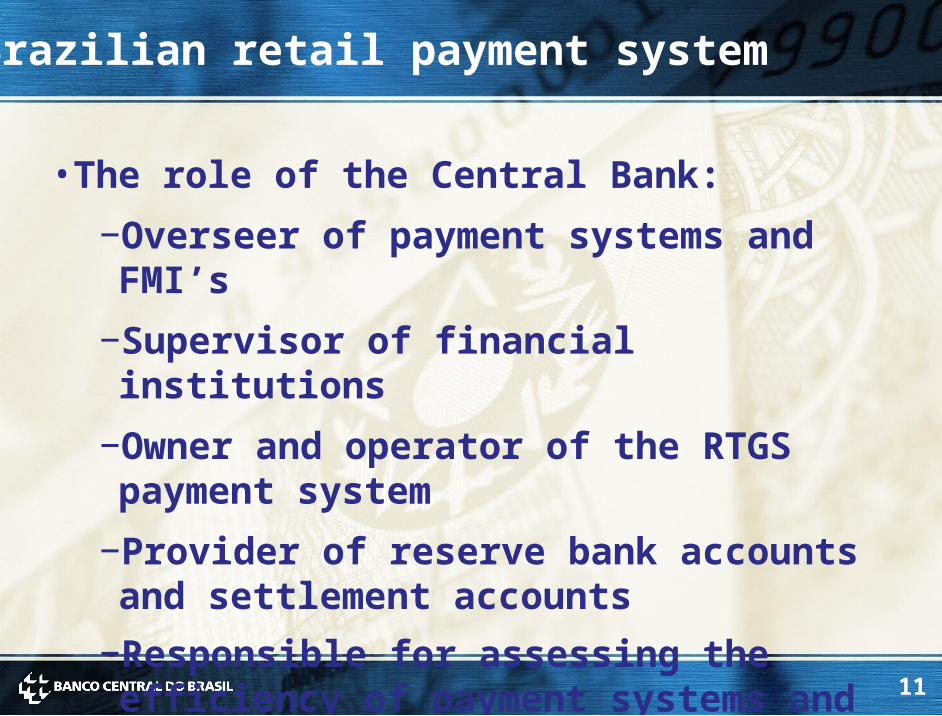

•The role of the Central Bank:−Overseer of payment systems and FMI’s−Supervisor of financial institutions−Owner and operator of the RTGS payment system−Provider of reserve bank accounts and settlement

accounts−Responsible for assessing the efficiency of

payment systems and payment instruments

Brazilian retail payment system

12

From a cash-based to a less cash society From a cash-based to a less cash society

•40% of the population does not have a bank account

• insufficient financial literacy

•high banking concentration

•prevalence of competition in infrastructure instead of in products

• lack of interoperability in ATM and POS networks

• legal and regulatory risks for new entrants

•geographical dimensions and demographic distribution

Challenges

13

From a cash-based to a less cash society

From a cash-based to a less cash society

•social mobility•costs of IT and CT•new main banks’ revenue source•number of mobile phone service subscribers•access to internet•direct government access to the payment system•new entrants• foreign investment•financial crisis / financial stability

Drivers

14

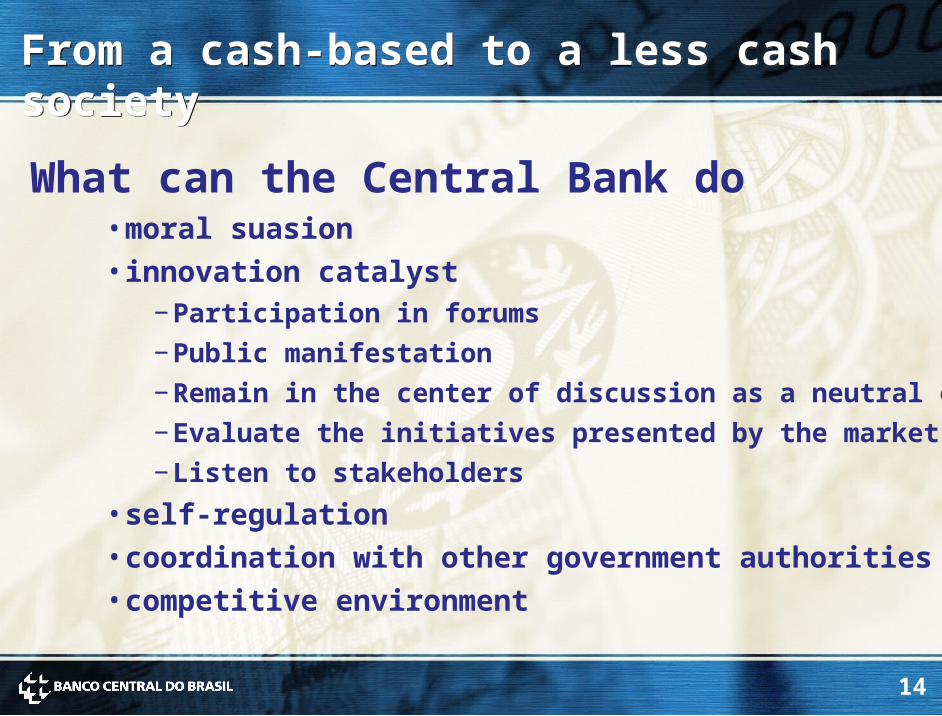

From a cash-based to a less cash societyFrom a cash-based to a less cash society

• moral suasion• innovation catalyst

− Participation in forums− Public manifestation− Remain in the center of discussion as a neutral entity− Evaluate the initiatives presented by the market − Listen to stakeholders

• self-regulation• coordination with other government authorities• competitive environment

What can the Central Bank do

15

From a cash-based to a less cash society From a cash-based to a less cash society

•since 1993, interbank exchange of information related to credit orders occur only through electronic means

•since 2010 there’s no physical exchange of cheques between banks

•reduced requirements for individuals opening simplified deposit accounts

•creation of banking agents that extended the banking capillarity to 100% of Brazilian municipalities (5.564 cities)

What has the Central Bank done

16

From a cash-based to a less cash society From a cash-based to a less cash society

•performed a stocktaking exercise on the Brazilian retail payment system (World Bank)

•widespread direct access to Central Bank money (settlement accounts) by entities other than financial institutions

•since 2011 interoperability of POS machines

•new law on payments schemes – Central Bank mandate

What has the Central Bank done (cont.)

17

From a cash-based to a less cash societyFrom a cash-based to a less cash society

• achieve financial inclusion

• reduce social costs / banking costs

• reduce “shadow economy” activities

• avoid tax evasion

• reduce crimes related to the high use of paper currency

• increase e-commerce business

• keep up with innovations

18

Daso M. Coimbra

Department of Banking Operations and Payments System

+55 (61) 3414-1340

Daso M. Coimbra

Department of Banking Operations and Payments System

+55 (61) 3414-1340

![Petronet MNB Ltd [Compatibility Mode]](https://static.fdocuments.us/doc/165x107/55cf99f7550346d0339feadc/petronet-mnb-ltd-compatibility-mode.jpg)