1 Introduction Rabobank Group - Agrobanco · Rabobank’s roots Bank Processor Rabo Development All...

42

Rabo Development A story on Development and Impact

-

Upload

trinhduong -

Category

Documents

-

view

214 -

download

0

Transcript of 1 Introduction Rabobank Group - Agrobanco · Rabobank’s roots Bank Processor Rabo Development All...

12.40

6.40

6.80

5.80

0.80

1.20

7.80

8.80

9.00

0.20

0.20

12.40 7.90

7.50

Guides for gutter

Text colours

R 27 G 66 B 152

R 0 G 0 B 0

R 127 G 127 B 127

Background shading

R 242 G 242 B 242

R 225 G 235 B 244

R 227 G 244 B 236

8.40

Colour order (left to right, top to bottom)

R 59 G 110 B 143

R 251 G 193 B 119

R 115 G 198 B 161

R 103 G 153 B 200

R 186 G 163 B 171

R 191 G 191 B 191

R 127 G 127 B 127

R 201 G 48 B 146

R 27 G 66 B 152

R 84 G 7 B 91

R 248 G 152 B 29

R 241 G 237 B 238

R 254 G 234 B 210

R 211 G 227 B 237

Rabo Development A story on Development and Impact

Introduction Rabobank Group 1

3

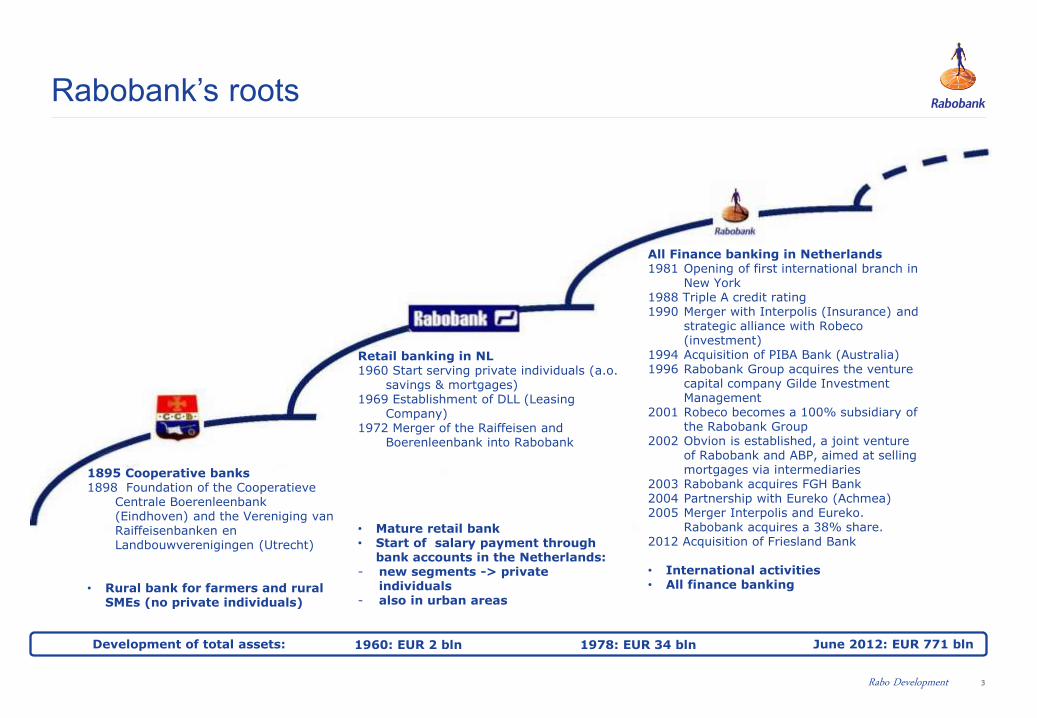

Rabobank’s roots

Bank

Processor

Rabo Development

All Finance banking in Netherlands 1981 Opening of first international branch in

New York 1988 Triple A credit rating 1990 Merger with Interpolis (Insurance) and

strategic alliance with Robeco (investment)

1994 Acquisition of PIBA Bank (Australia) 1996 Rabobank Group acquires the venture

capital company Gilde Investment Management

2001 Robeco becomes a 100% subsidiary of the Rabobank Group

2002 Obvion is established, a joint venture of Rabobank and ABP, aimed at selling mortgages via intermediaries

2003 Rabobank acquires FGH Bank 2004 Partnership with Eureko (Achmea) 2005 Merger Interpolis and Eureko.

Rabobank acquires a 38% share. 2012 Acquisition of Friesland Bank • International activities • All finance banking

Retail banking in NL 1960 Start serving private individuals (a.o.

savings & mortgages) 1969 Establishment of DLL (Leasing

Company) 1972 Merger of the Raiffeisen and

Boerenleenbank into Rabobank

• Mature retail bank • Start of salary payment through

bank accounts in the Netherlands: - new segments -> private

individuals - also in urban areas

1895 Cooperative banks 1898 Foundation of the Cooperatieve

Centrale Boerenleenbank (Eindhoven) and the Vereniging van Raiffeisenbanken en Landbouwverenigingen (Utrecht)

• Rural bank for farmers and rural

SMEs (no private individuals)

Development of total assets: 1960: EUR 2 bln 1978: EUR 34 bln

June 2012: EUR 771 bln

4

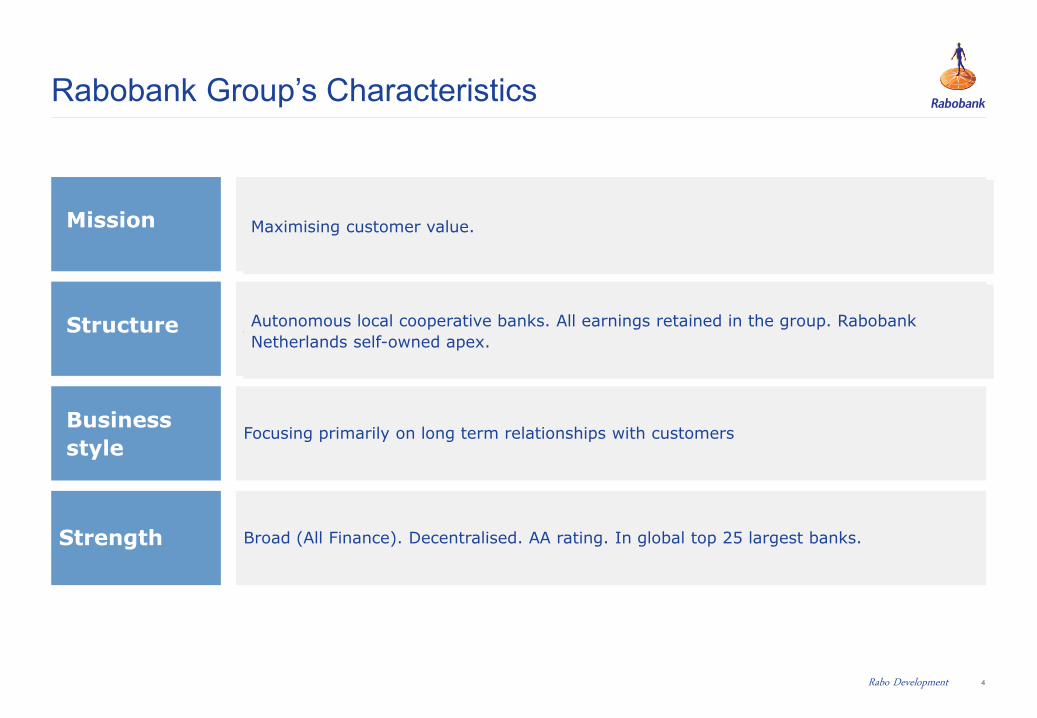

Rabobank Group’s Characteristics

Mission

Structure

Business style

Strength

Maximising customer value.

Autonomous local cooperative banks. All earnings retained in the group. Rabobank Netherlands self-owned apex.

Focusing primarily on long term relationships with customers

Broad (All Finance). Decentralised. AA rating. In global top 25 largest banks.

Rabo Development

Mission

Structure

Business

style

Maximising customer value.

Autonomous local cooperative banks. All earnings retained in the group. Rabobank

Netherlands self-owned apex.

5

Rabobank Group’s Values

• The interests of our customers and members are key

• Delivering the best possible solutions to our customers

• Offering continuity in our services, thereby serving our

customers’ long-term interests

• Showing commitment to our customers and their

environment, thereby assisting them in realising their

ambitions

• Involved

• Nearby

• Leading

• Respect

• Integrity

• Professionalism

• Sustainability

Core values Rabobank Group Brand values Rabobank

Rabo Development

6

• Focus on customers’ interest

• Member involvement

• Supporting local communities

• Working together

• Members’ council and cooperative dividend

• Social involvement

• Long term relationship with customer

• Meaningful contribution to economic development in

local area

Cooperative characteristics Rabobank

Rabo Development

7

Profile Rabobank Group

International financial services provider based on a cooperative organisation principle

• Retail banking, wholesale banking, asset management, leasing and real estate

• Operating in 47 countries

• 10 million customers around the world

• 766 offices outside the Netherlands

• 61,103 FTEs (total Rabobank Group)

Local Rabobanks in the Netherlands

• 139 independent local banks in the Netherlands

• 7,6 million customers (of which 6.8 mln retail clients)

• 1,9 million members

• 826 offices

• 27,272 FTEs

• 2,898 ATMs

High credit rating by S&P, Moody’s and DBRS

Rabo Development

8

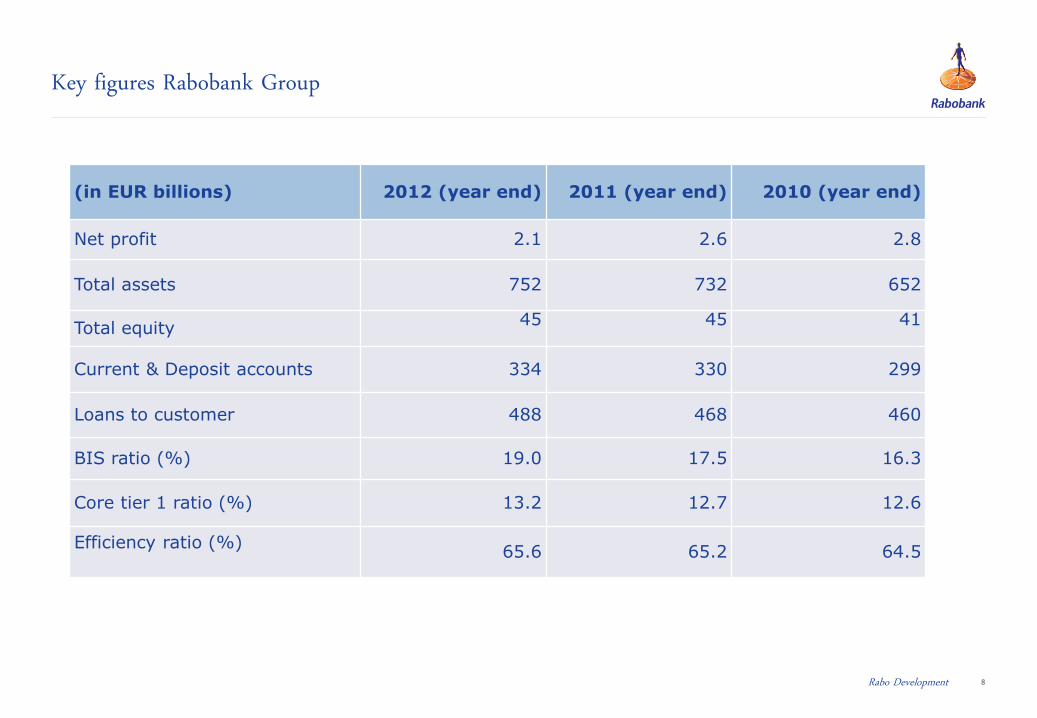

Key figures Rabobank Group

(in EUR billions) 2012 (year end) 2011 (year end) 2010 (year end)

Net profit 2.1 2.6 2.8

Total assets 752 732 652

Total equity 45 45 41

Current & Deposit accounts 334 330 299

Loans to customer 488 468 460

BIS ratio (%) 19.0 17.5 16.3

Core tier 1 ratio (%) 13.2 12.7 12.6

Efficiency ratio (%)

65.6 65.2 64.5

Rabo Development

9

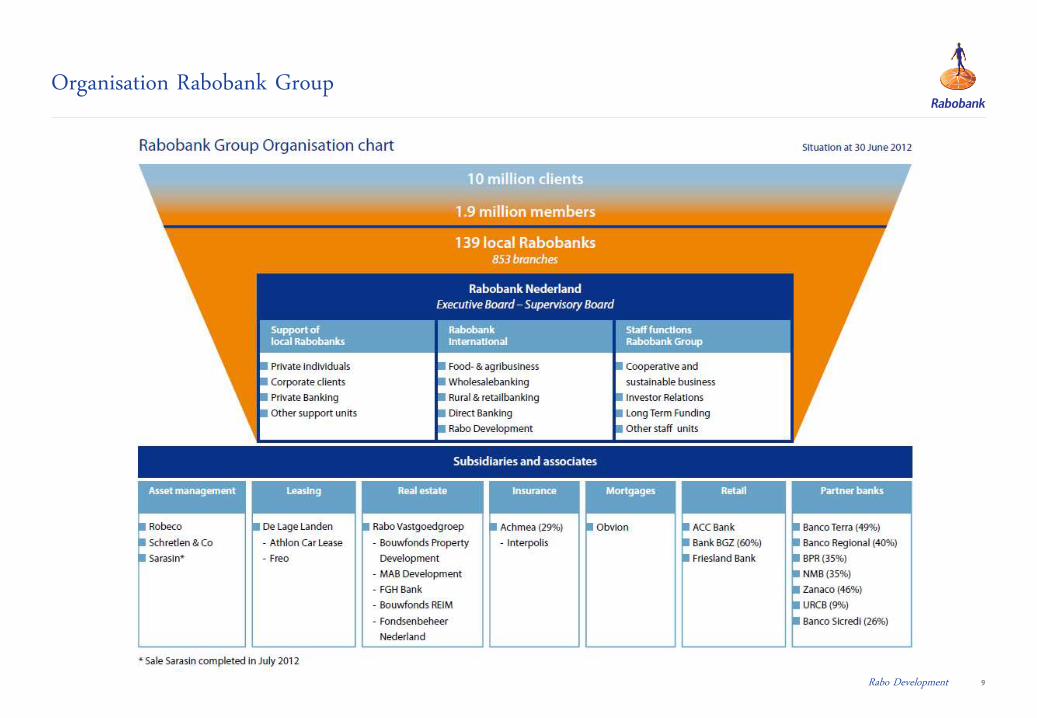

Organisation Rabobank Group

Rabo Development

10

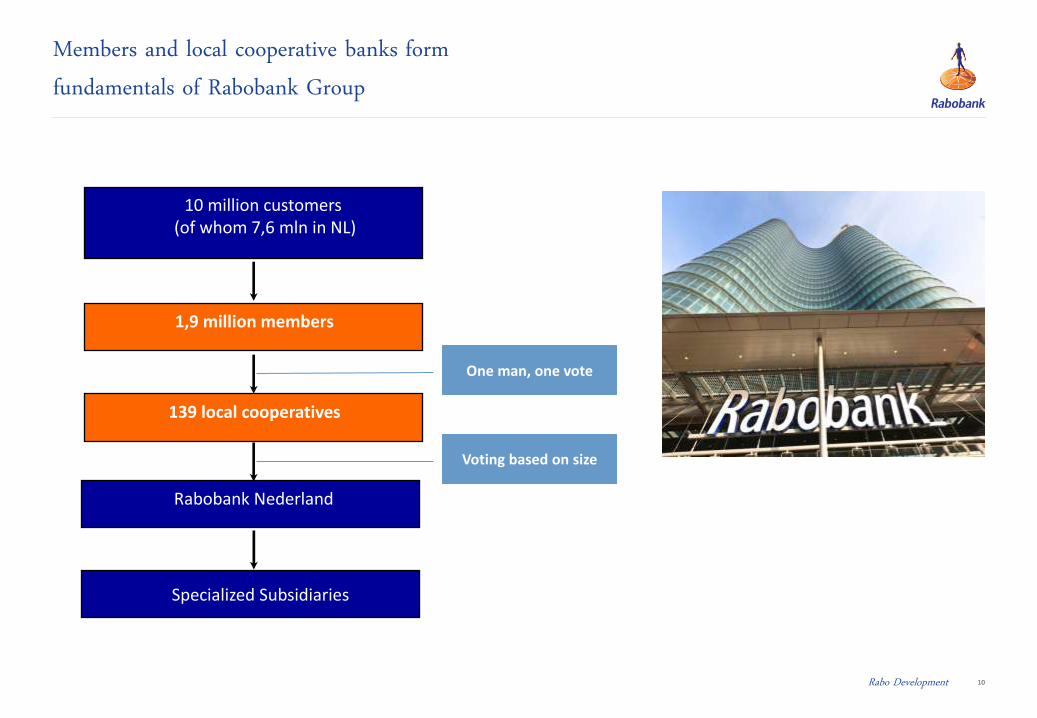

Members and local cooperative banks form fundamentals of Rabobank Group

10 million customers (of whom 7,6 mln in NL)

1,9 million members

139 local cooperatives

Rabobank Nederland

Specialized Subsidiaries

Rabo Development

One man, one vote

Voting based on size

11

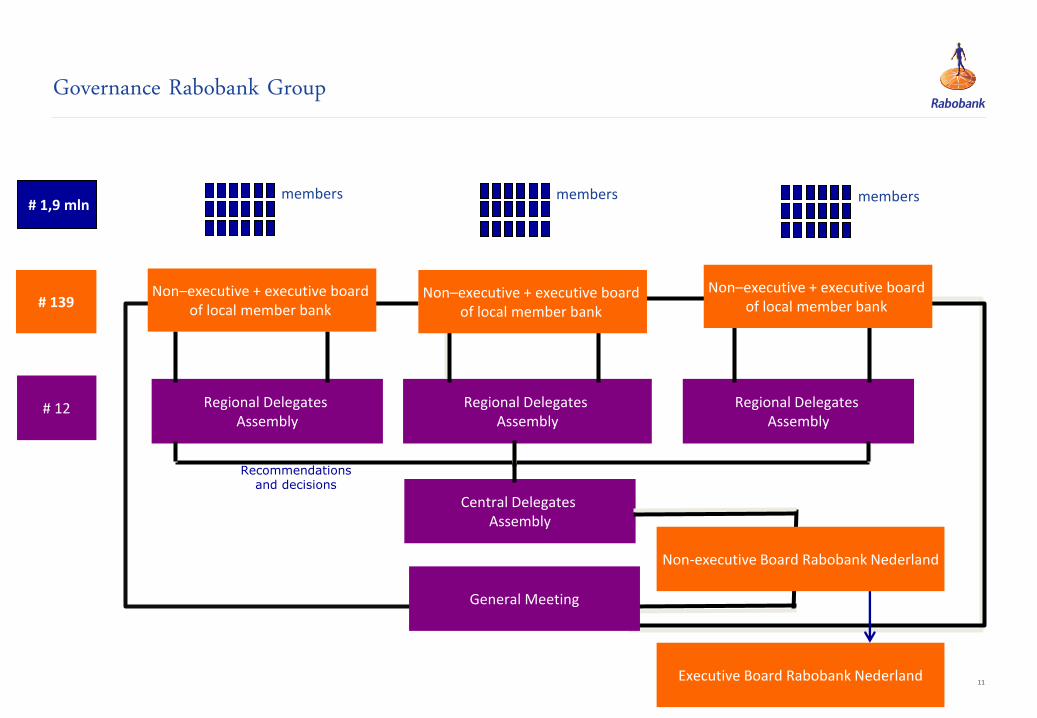

Governance Rabobank Group

Regional Delegates Assembly

Regional Delegates Assembly

Regional Delegates Assembly

Central Delegates Assembly

Non-executive Board Rabobank Nederland

Executive Board Rabobank Nederland

General Meeting

Non–executive + executive board

of local member bank

# 12

# 139

# 1,9 mln members members

Recommendations and decisions

Non–executive + executive board

of local member bank

Non–executive + executive board

of local member bank

members

12

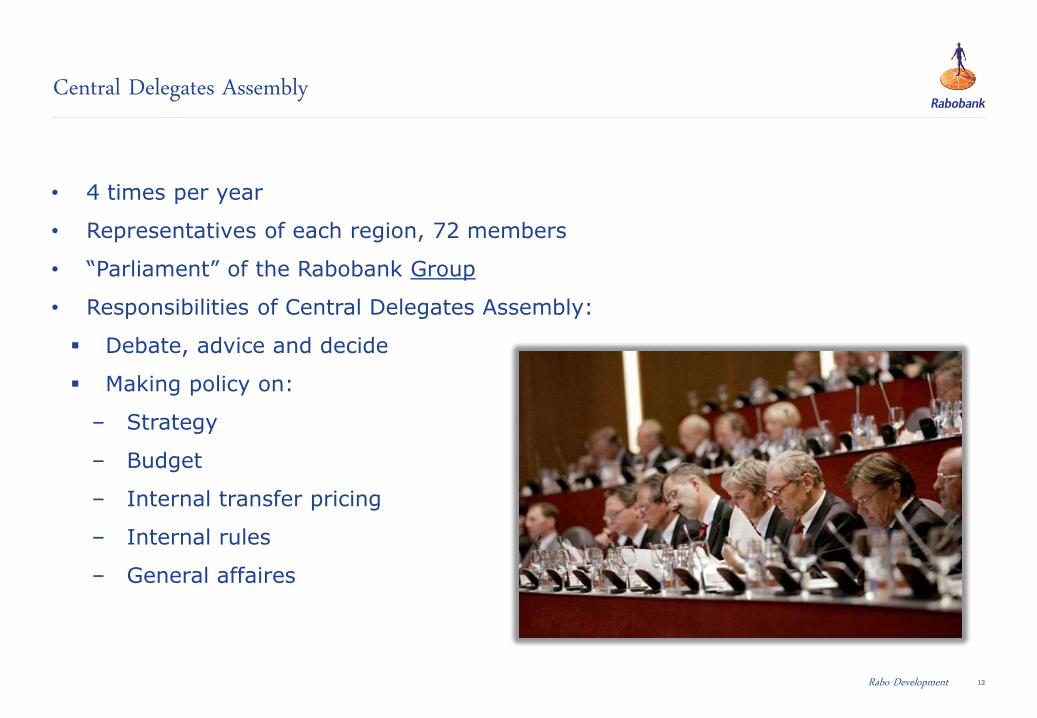

Central Delegates Assembly

• 4 times per year

• Representatives of each region, 72 members

• “Parliament” of the Rabobank Group

• Responsibilities of Central Delegates Assembly:

Debate, advice and decide

Making policy on:

– Strategy

– Budget

– Internal transfer pricing

– Internal rules

– General affaires

Rabo Development

13

General Meeting

• Once a year

• 139 local banks with about 1.500 participants

Responsibilities of General members meeting:

• Approval Annual Report

• Approve changes Articles of Association

• Appoint non-executive Board of Directors

Rabo Development

14

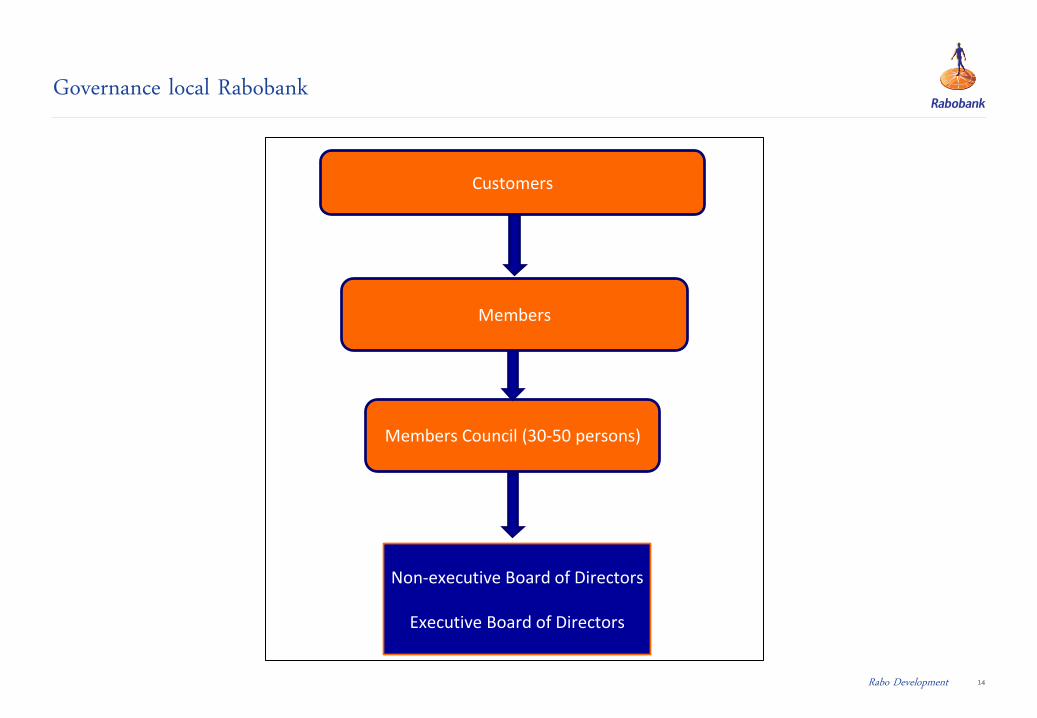

Governance local Rabobank

Rabo Development

Customers

Members Council (30-50 persons)

Non-executive Board of Directors

Executive Board of Directors

Members

15

Local Members Council

• 30 to 50 delegates chosen by members

Responsibilities of Local Members Council:

• Appoints supervisory board;

but especially discussion about direction and policy of the bank;

• Approval of annual report;

• Discharge non-executive board and executive board

Rabo Development

16

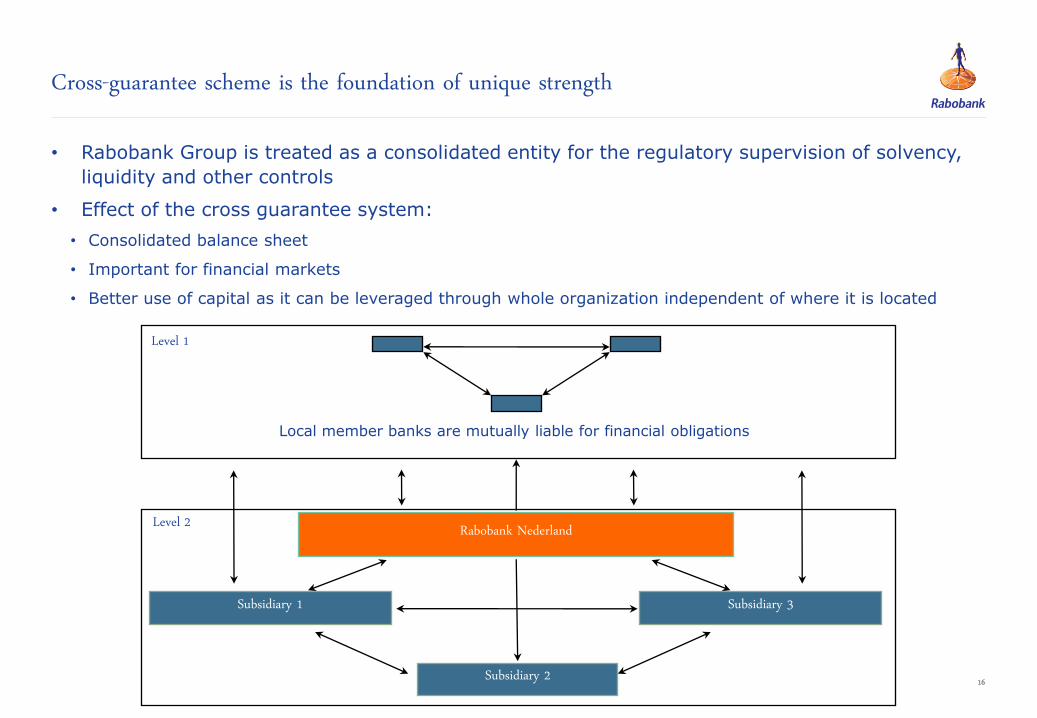

Cross-guarantee scheme is the foundation of unique strength

• Rabobank Group is treated as a consolidated entity for the regulatory supervision of solvency,

liquidity and other controls

• Effect of the cross guarantee system:

• Consolidated balance sheet

• Important for financial markets

• Better use of capital as it can be leveraged through whole organization independent of where it is located

Local member banks are mutually liable for financial obligations

Rabobank Nederland

Subsidiary 1

Subsidiary 2

Subsidiary 3

Level 1

Level 2

Introduction Rabo Development 2

18

Rabo Development’s roots and mission

Rabobank was founded in 1898 by farmers who did not have access to

financial services. Today, more than 4 billion people worldwide do not have

access to financial services.

Rabo Development’s mission:

Drawing on Rabobank’s cooperative heritage and banking knowledge in the

Netherlands, Rabo Development aims to increase access to financial

services in developing countries that have substantial potential in the food

and agri sector.

Rabo Development

19

In 1989 Rabo International Advisory Services (RIAS) was established to offer technical

assistance to (rural) banks in developing countries. In 2006 RIAS became part of Rabo

Development, basically with the objective to:

• Contribute to the wellbeing of world citizens by deploying (financial and non-

financial) resources for stimulating rural development around the globe (social

responsibility)

• Give substance to the cooperative legitimacy of Rabobank

• Enter into strategic alliances with (rural) banks in developing countries that are

important exporters of agri commodities. This way Rabobank intends to create a

network of partner banks that can be considered as part of the global Rabobank

network.

Origin of Rabo Development

Rabo Development

20

• The contribution that Rabo Development makes to the development of the partner

bank initially consists of three elements: capital, management services and technical

assistance.

• Rabo Development does not want to take a majority shareholding. It will look for

consensus views with the other main shareholders. Rabo Development finds it

important that the partner bank is locally owned.

• Profit maximization is not the ultimate objective. The highest ambition is to generate

maximum customer value and a sustainable enterprise.

Key elements of Rabo Development’s objectives

Rabo Development

21

• Little or no commercial banks involved in rural banking

• Typically involvement of state dominated banks

• Micro finance institutions lack scale and ability to grow with their customers

• Financial service delivery is fragmented and targeted to specific customer groups

• Traditional lending is mostly based on collateral

Observations in rural banking

Rabo Development

22

• Lack of infrastructure precludes efficient outreach to customers

• Enabling environment is often suspect (collateral value is questionable, land titles are often an issue)

• Lack of scale at farm level

• Agriculture often not seen as a purely economic activity

• Poor supply chain organisation: power remains with the traders

• Banking environment sometimes distorted by donors, government and development banks

• Poor financial literacy

Hurdles to take in rural banking

Rabo Development

23

• Rural banks also need urban presence

• Banks need to serve all client segments with the right mix of products, services, channels and people

• Sufficient scale and market share is vital

• Banks need to focus on both sides of the balance sheet (asset and liability products)

• IT is key in increasing outreach efficiently, using direct channels (ATMs, mobile banking, internet banking, PoS) next to a physical branch network

• Rural banks need specialised knowledge centers on SMEs and agri

• Alignment between all stakeholders is a must

Key lessons learned in rural banking

Rabo Development

24

Partner banks:

Rabo Development aims to develop existing financial institutions into leading, sustainable local retail banks with a rural orientation and client focus. This is accomplished through the provision of technical assistance and management services after taking minority equity interests. The strategic partnership will be mutually beneficial to these financial institutions, the Rabobank Group and their respective clients.

Advisory services:

By providing knowledge on Food and Agri, retail banking and cooperatives, Rabo International Advisory Services (RIAS) aims to:

• Assist partner banks

• Create leads for new partner banks

• Provide services on demand to the Rabobank Group and its clients

Rabo Development’s strategy

Rabo Development

25

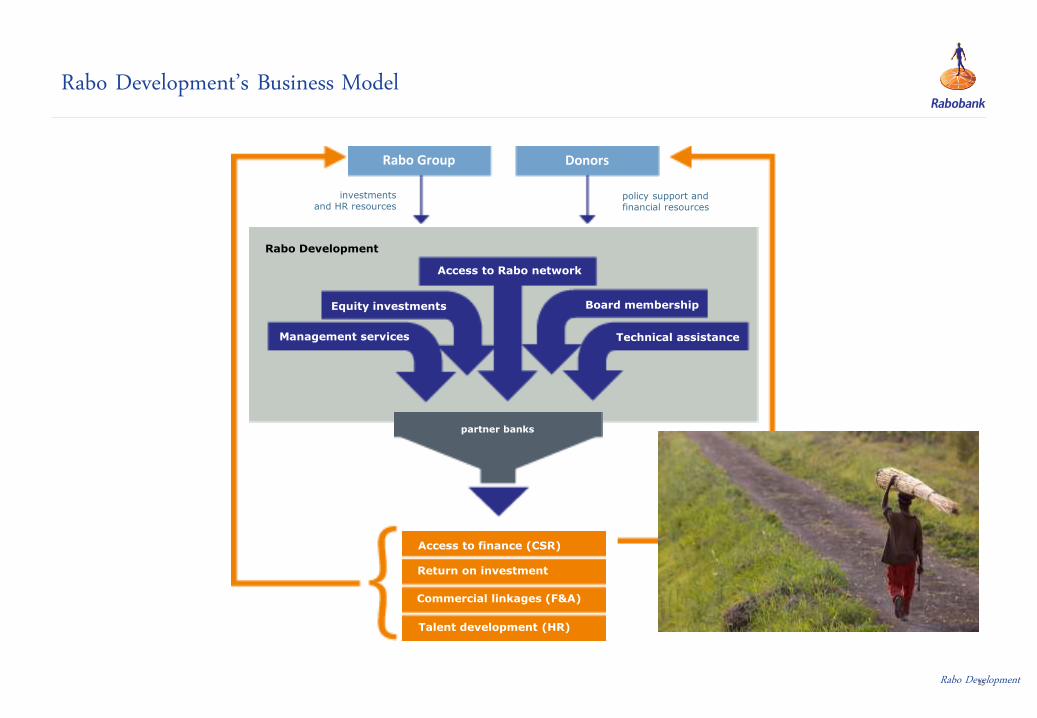

Rabo Development’s Business Model

Rabo Development

investments and HR resources

policy support and financial resources

Rabo Development

Access to Rabo network

Board membership

Technical assistance

Equity investments

Management services

partner banks

Access to finance (CSR)

Return on investment

Commercial linkages (F&A)

Talent development (HR)

Rabo Group Donors

26

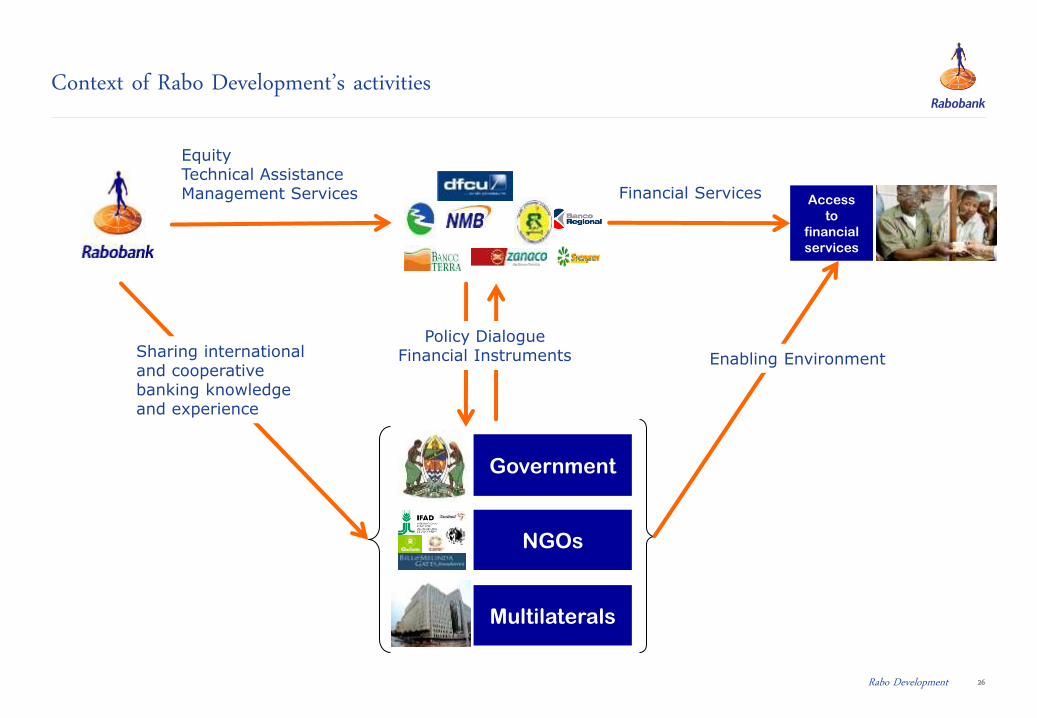

Context of Rabo Development’s activities

Financial Services

Multilaterals

NGOs

Government

Access

to

financial

services

Equity Technical Assistance Management Services

Sharing international and cooperative banking knowledge and experience

Enabling Environment

Policy Dialogue Financial Instruments

Rabo Development

27

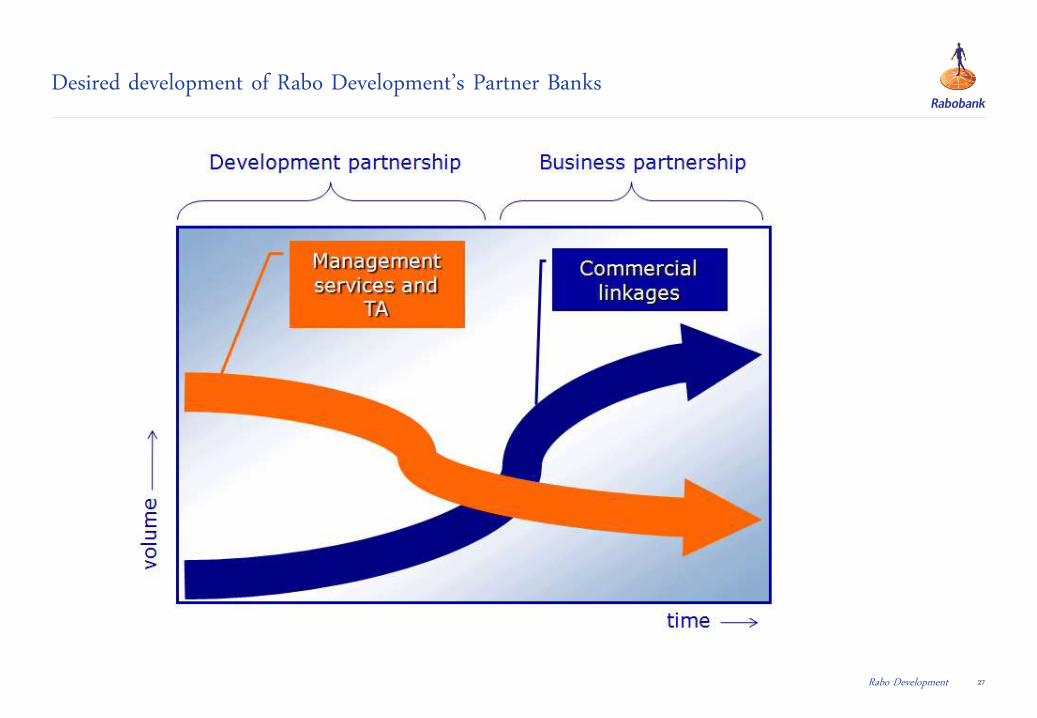

Desired development of Rabo Development’s Partner Banks

Rabo Development

28

Rabo Development partner banks and advisory projects 2013

-

Rabo Development

Partner banks

Advisory projects

29

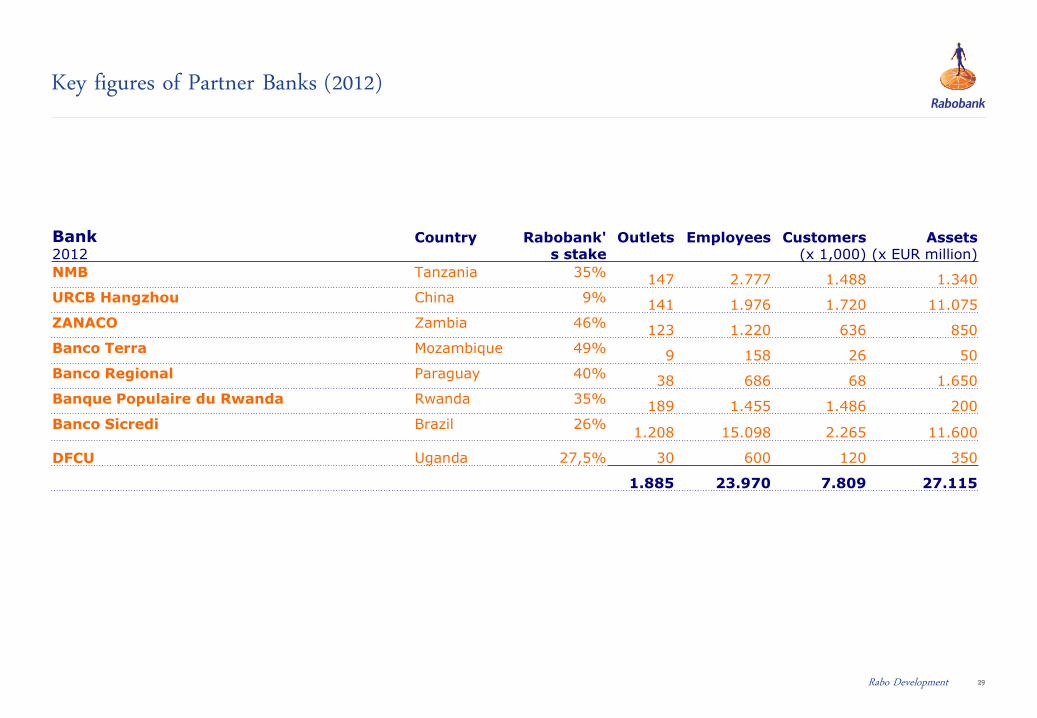

Key figures of Partner Banks (2012)

Rabo Development

Bank 2012

Country

Rabobank's stake

Outlets

Employees

Customers (x 1,000)

Assets (x EUR million)

NMB Tanzania 35% 147 2.777 1.488 1.340

URCB Hangzhou China 9% 141 1.976 1.720 11.075

ZANACO Zambia 46% 123 1.220 636 850

Banco Terra Mozambique 49% 9 158 26 50

Banco Regional Paraguay 40% 38 686 68 1.650

Banque Populaire du Rwanda Rwanda 35% 189 1.455 1.486 200

Banco Sicredi Brazil 26% 1.208 15.098 2.265 11.600

DFCU Uganda 27,5% 30 600 120 350

1.885 23.970 7.809 27.115

30

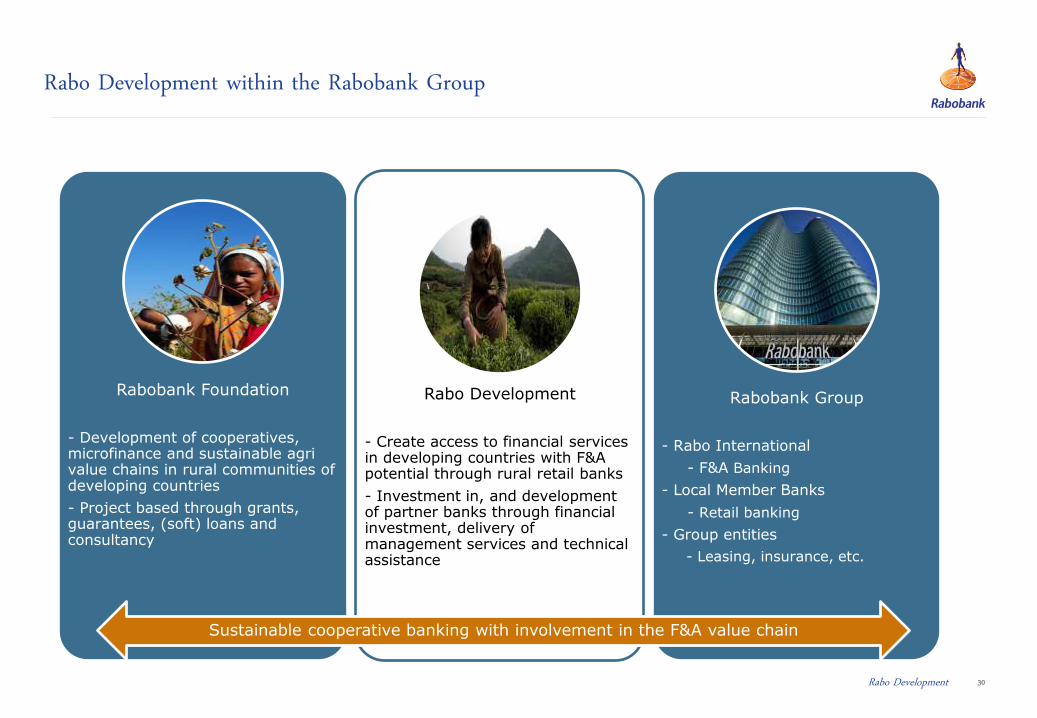

Rabo Development within the Rabobank Group

Rabobank Foundation

- Development of cooperatives, microfinance and sustainable agri value chains in rural communities of developing countries

- Project based through grants, guarantees, (soft) loans and consultancy

Rabo Development

- Create access to financial services in developing countries with F&A potential through rural retail banks

- Investment in, and development of partner banks through financial investment, delivery of management services and technical assistance

Rabobank Group

- Rabo International

- F&A Banking

- Local Member Banks

- Retail banking

- Group entities

- Leasing, insurance, etc.

Sustainable cooperative banking with involvement in the F&A value chain

Rabo Development

31

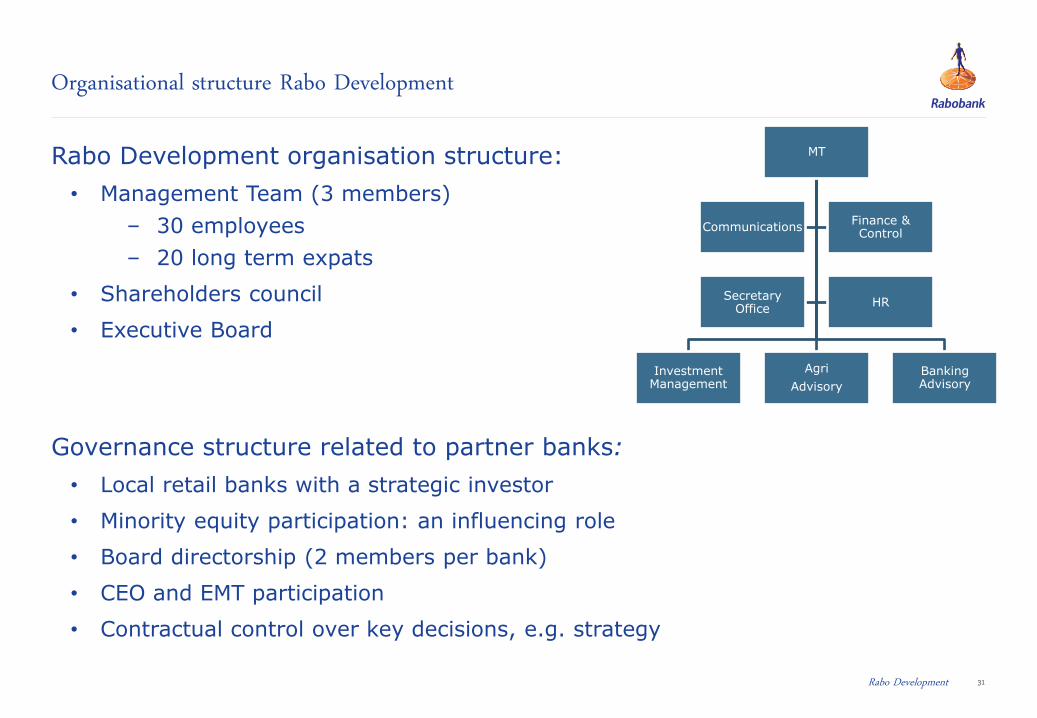

Rabo Development organisation structure:

• Management Team (3 members)

– 30 employees

– 20 long term expats

• Shareholders council

• Executive Board

Governance structure related to partner banks:

• Local retail banks with a strategic investor

• Minority equity participation: an influencing role

• Board directorship (2 members per bank)

• CEO and EMT participation

• Contractual control over key decisions, e.g. strategy

Organisational structure Rabo Development

MT

Investment Management

Agri

Advisory

Banking Advisory

Communications Finance & Control

Secretary Office

HR

Rabo Development

32

• Linking partner banks to each other • Linking partner banks to the international network of Rabobank • Linking Rabobank’s existing client base to the value proposition of its African

partners

Commercial opportunities with partner banks

Rabo Development

Examples of Rabo Development’s activities 3

35

• Warehouse Receipt Finance in the Cashew sector via a three partite agreement

• Increased small scale cashew farmers outreach from zero in 2005 to more than 200,000 in

2011

• Integrating the value chain, connecting parties in the F&A chain

Tanzania

Bank

Cooperative Processor

Rabo Development

36

BPR Mobile Banking

Launched September 2010, currently more than:

• 110,000 customers using BPR Mobile

• 8,000 client contacts on average per day via

the mobile channel only

• Works on every cell phone

Functionalities of BPR mobile banking, regardless the

client’s (often rural) location

1. Balance Inquiry

2. Mini-Statements

3. Money Transfer to other BPR Accounts

4. Prepaid Airtime

5. Bill Payments

Rwanda

Rabo Development

37

Capacity Building project rural cooperatives

Rice - UCORIBU: Capacity building of 10 cooperatives, 18,000 members, Sponsored

by Rabobank Foundation and supported by ICM and USAID (post harvest handling and

storage)

Tea - Assophté: capacity building of the Assophté tea cooperative (5,000 members)

sponsored by Rabobank Foundation and supported by Sorwathé (US owned tea

factory) and OCIR Thé

Dairy - project related to Inyange, a leading dairy processor: improving the supply

chain of fresh milk linked to Inyange, sponsored by Rabobank Foundation and

supported by Land O’Lakes.

Capacity Building Agri Finance BPR

- BPR & AGRIfin World Bank

Rwanda

Rabo Development

38

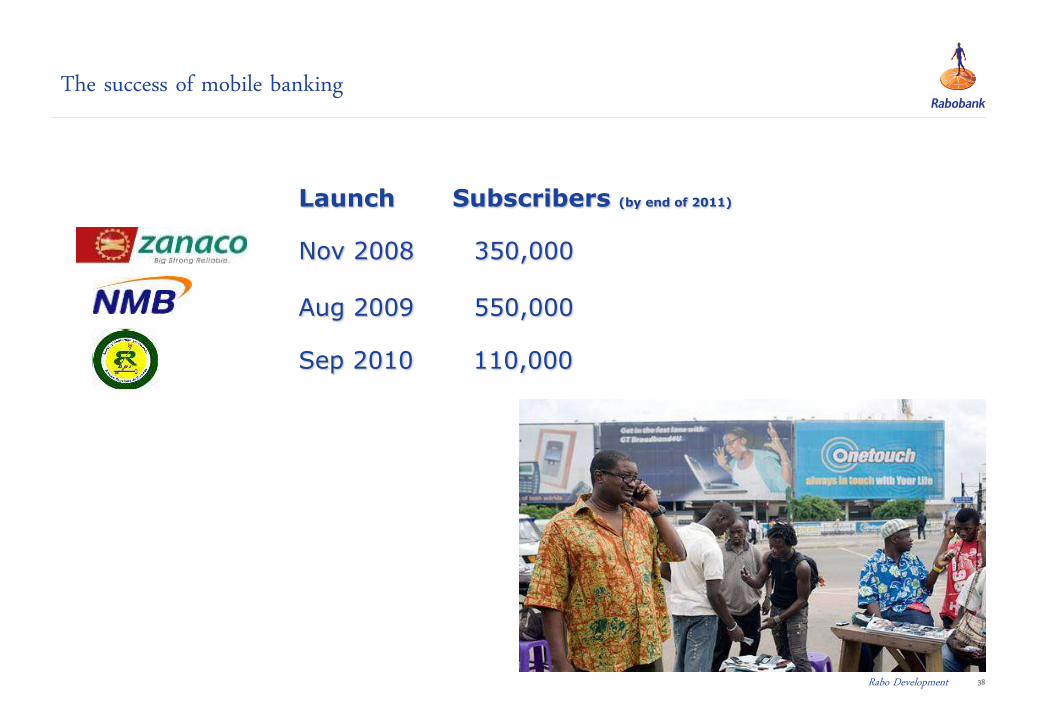

Launch Subscribers (by end of 2011)

Nov 2008 350,000

Aug 2009 550,000

Sep 2010 110,000

The success of mobile banking

Rabo Development

39

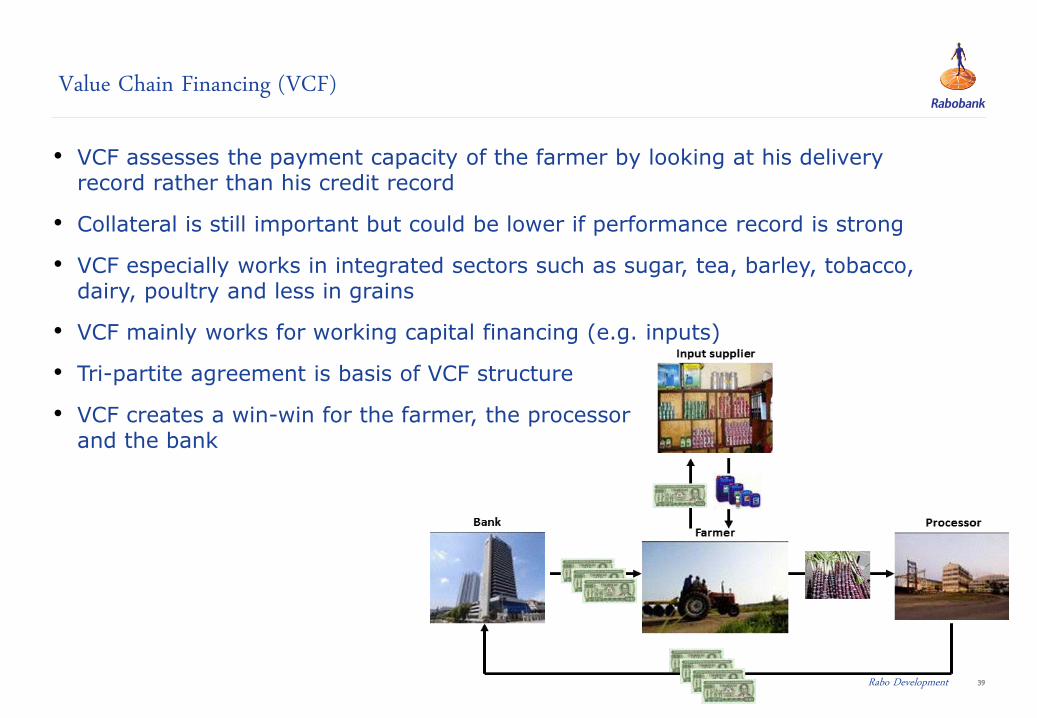

• VCF assesses the payment capacity of the farmer by looking at his delivery record rather than his credit record

• Collateral is still important but could be lower if performance record is strong

• VCF especially works in integrated sectors such as sugar, tea, barley, tobacco, dairy, poultry and less in grains

• VCF mainly works for working capital financing (e.g. inputs)

• Tri-partite agreement is basis of VCF structure

• VCF creates a win-win for the farmer, the processor and the bank

Value Chain Financing (VCF)

Rabo Development

40

• Exporting Farmer-based Organisations (FOs) have an advantage compared to locally selling FOs

• The export contracts can be pledged to banks whereby the foreign buyer pays directly in the bank’s account

• In fact, it is also a form of value chain financing

• Social lenders (e.g. Rabobank Rural Fund and Root Capital) are specialised in PXF

• Eligible sectors especially are coffee, cocoa, sesame and tea

Pre-Export Financing (PXF)

Cooperative Collection

Cooperative Storage

Coffee farmer Production

Importer Cooperative export

Cooperative transport

Cooperative processing

Rural Fund

$ loan

$ coffee purchase

Coffee supply

Payment by importer

Rabo Development

41

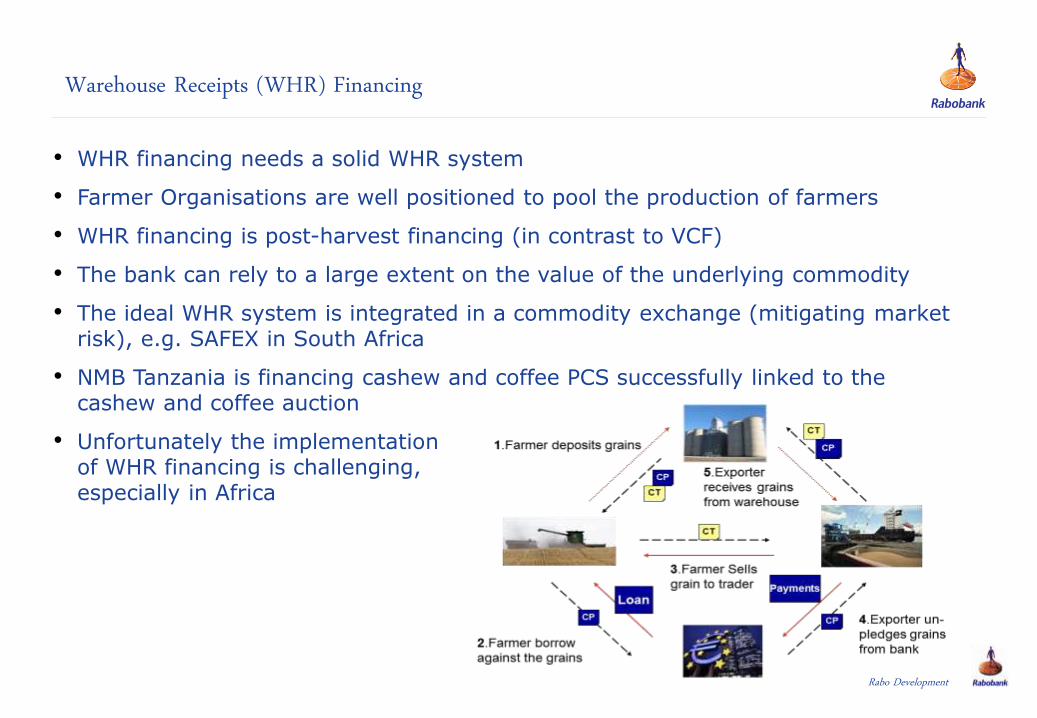

• WHR financing needs a solid WHR system

• Farmer Organisations are well positioned to pool the production of farmers

• WHR financing is post-harvest financing (in contrast to VCF)

• The bank can rely to a large extent on the value of the underlying commodity

• The ideal WHR system is integrated in a commodity exchange (mitigating market risk), e.g. SAFEX in South Africa

• NMB Tanzania is financing cashew and coffee PCS successfully linked to the cashew and coffee auction

• Unfortunately the implementation of WHR financing is challenging, especially in Africa

Warehouse Receipts (WHR) Financing

Rabo Development

12.40

6.40

6.80

5.80

0.80

1.20

7.80

8.80

9.00

0.20

0.20

12.40 7.90

7.50

Guides for gutter

Text colours

R 27 G 66 B 152

R 0 G 0 B 0

R 127 G 127 B 127

Background shading

R 242 G 242 B 242

R 225 G 235 B 244

R 227 G 244 B 236

8.40

Colour order (left to right, top to bottom)

R 59 G 110 B 143

R 251 G 193 B 119

R 115 G 198 B 161

R 103 G 153 B 200

R 186 G 163 B 171

R 191 G 191 B 191

R 127 G 127 B 127

R 201 G 48 B 146

R 27 G 66 B 152

R 84 G 7 B 91

R 248 G 152 B 29

R 241 G 237 B 238

R 254 G 234 B 210

R 211 G 227 B 237

Any questions?

Rabo Development

12.40

6.40

6.80

5.80

0.80

1.20

7.80

8.80

9.00

0.20

0.20

12.40 7.90

7.50

Guides for gutter

Text colours

R 27 G 66 B 152

R 0 G 0 B 0

R 127 G 127 B 127

Background shading

R 242 G 242 B 242

R 225 G 235 B 244

R 227 G 244 B 236

8.40

Colour order (left to right, top to bottom)

R 59 G 110 B 143

R 251 G 193 B 119

R 115 G 198 B 161

R 103 G 153 B 200

R 186 G 163 B 171

R 191 G 191 B 191

R 127 G 127 B 127

R 201 G 48 B 146

R 27 G 66 B 152

R 84 G 7 B 91

R 248 G 152 B 29

R 241 G 237 B 238

R 254 G 234 B 210

R 211 G 227 B 237

Thank you for your kind attention https://www.rabobank.com/en/rabo_development/index.html

Rabo Development