1 Intangible assets. 2 Meaning of Intangible assets Intangible assets are assets which have no...

90

1 Intangible assets

-

Upload

buddy-harrison -

Category

Documents

-

view

289 -

download

4

Transcript of 1 Intangible assets. 2 Meaning of Intangible assets Intangible assets are assets which have no...

1

Intangible assets

2

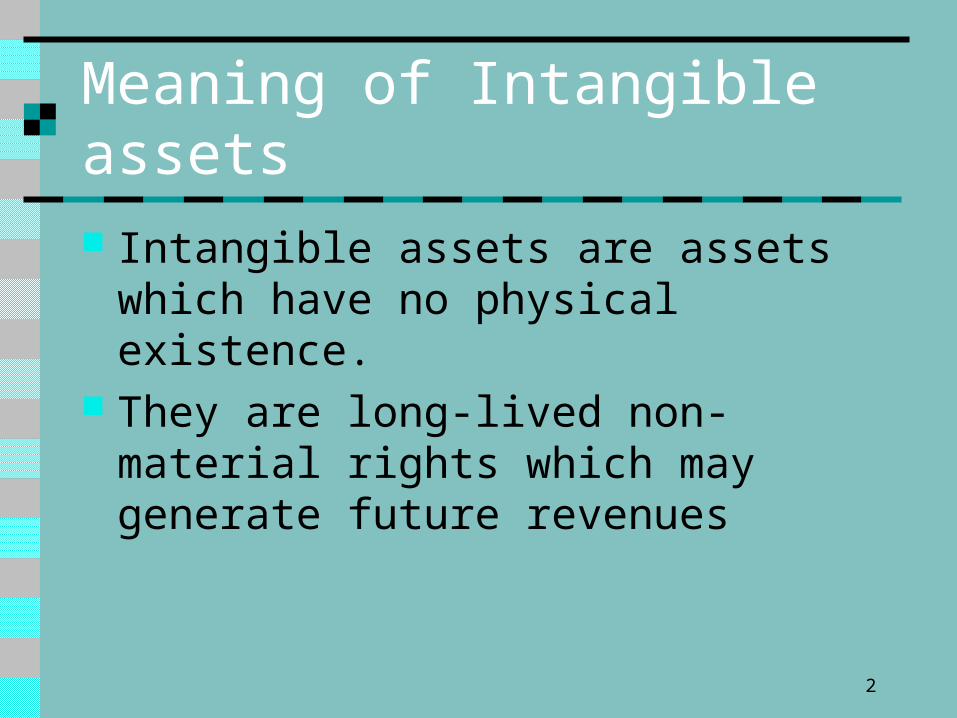

Meaning of Intangible assets

Intangible assets are assets which have no physical existence.

They are long-lived non-material rights which may generate future revenues

3

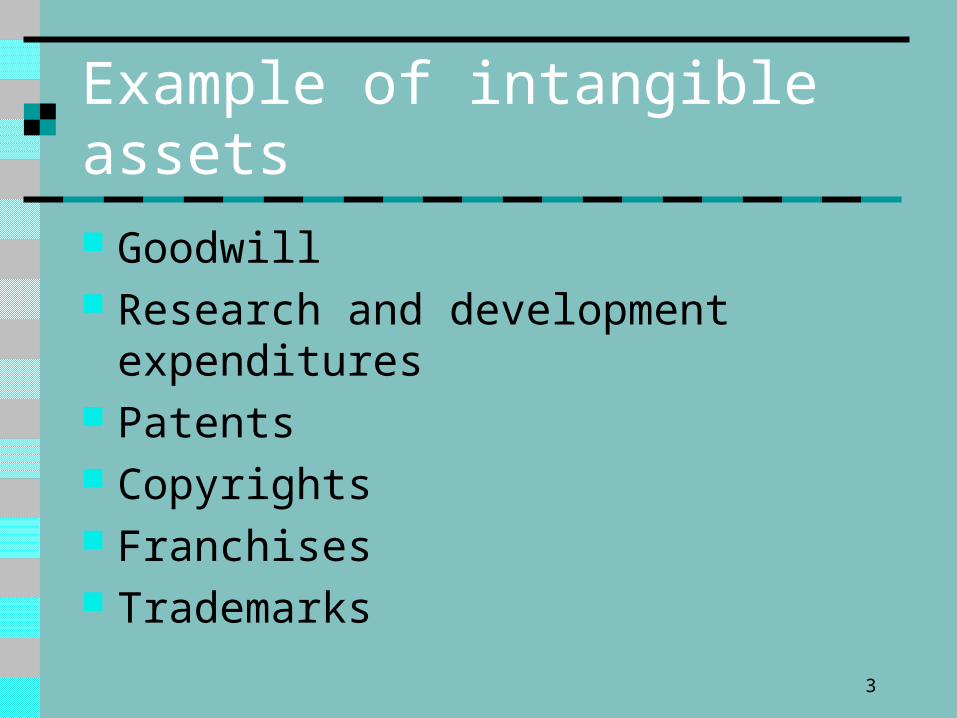

Example of intangible assets

Goodwill Research and development expenditures Patents Copyrights Franchises Trademarks

4

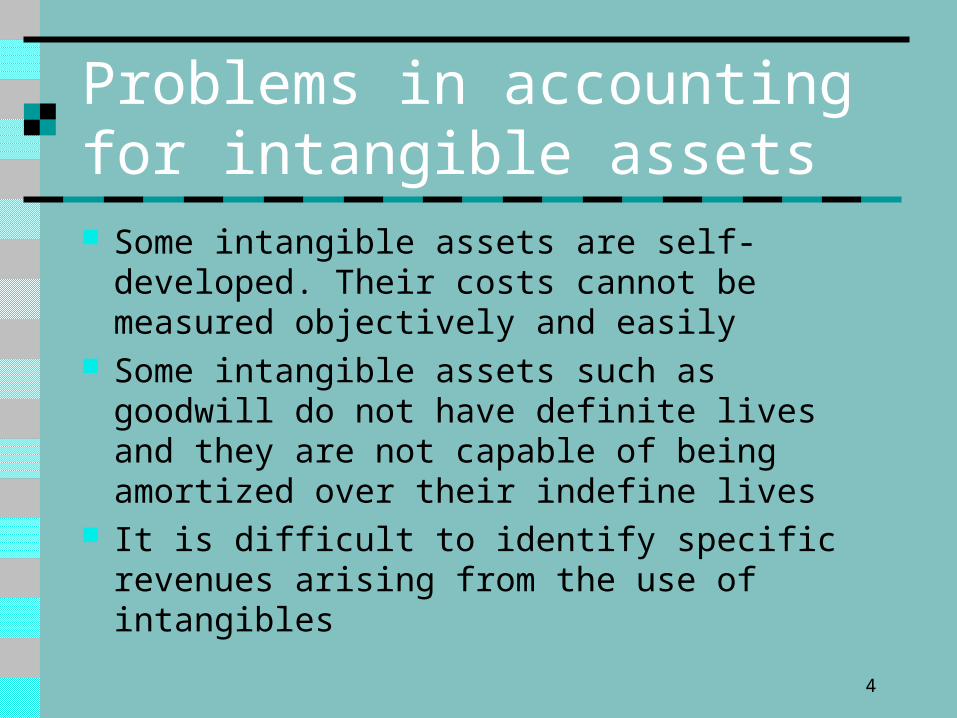

Problems in accounting for intangible assets Some intangible assets are self-developed. Their

costs cannot be measured objectively and easily Some intangible assets such as goodwill do not

have definite lives and they are not capable of being amortized over their indefine lives

It is difficult to identify specific revenues arising from the use of intangibles

5

Accounting for an intangible asset

6

To record the cost of an intangible asset

Dr. Intangible assets

Cr. Bank

7

An intangible asset should be recognized if it is probable that the future economic benefits that are attributable to the asset will flow to the enterprise; the cost of the asset can be measured reliably

An intangible asset should be measured its initially at cost

The cost of an intangible asset comprises its purchase price including all other expenditures on preparing the asset for its intended use such as import duties and professional fees for legal services. Any trade discount and rebates are deducted in arriving at the cost

8

To write off the expenditure incurred from which no intangible asset can be created

Dr. Profit and loss

Cr. Bank

9

With creating intangible assets, the following expenditures should be recognized as expenses when it is incurred: Expenditure on start-up activities which

comprises establishing cost, pre-opening cost for new facility, new operation or business

Expenditure on training activities, advertising and promotional activities and relocating or re-organizing part of all of an enterprises

10

Expenditure on an intangible item that was initially recognized as an expense in previous annual financial statement or interim financial reports should not be recognized as part of the cost of an intangible asset at a later date

11

To recognize the subsequent expenditure as an intangible asset

Dr. Intangible assets

Cr. Bank

12

Subsequent expenditure can be capitalized if the expenditure will enable the asset to generate future economic benefits in excess of its original level; and the expenditure can be measured and attributed to the asset reliably

13

To record the provision for amortization

Dr. Profit and loss

Cr. Accumulated amortization

14

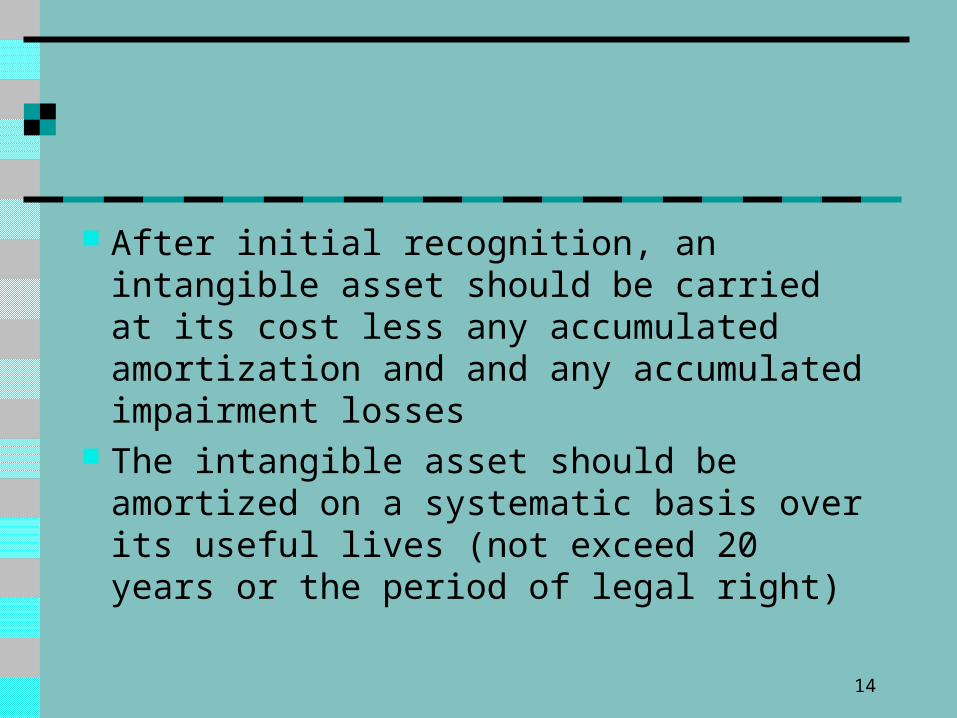

After initial recognition, an intangible asset should be carried at its cost less any accumulated amortization and and any accumulated impairment losses

The intangible asset should be amortized on a systematic basis over its useful lives (not exceed 20 years or the period of legal right)

15

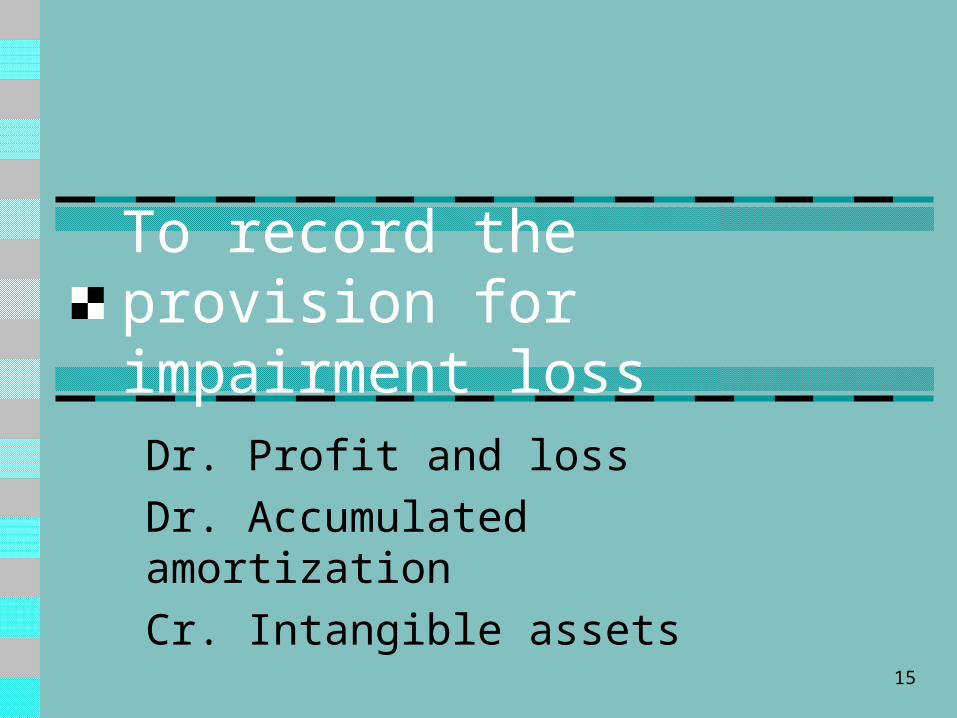

To record the provision for impairment loss

Dr. Profit and loss

Dr. Accumulated amortization

Cr. Intangible assets

16

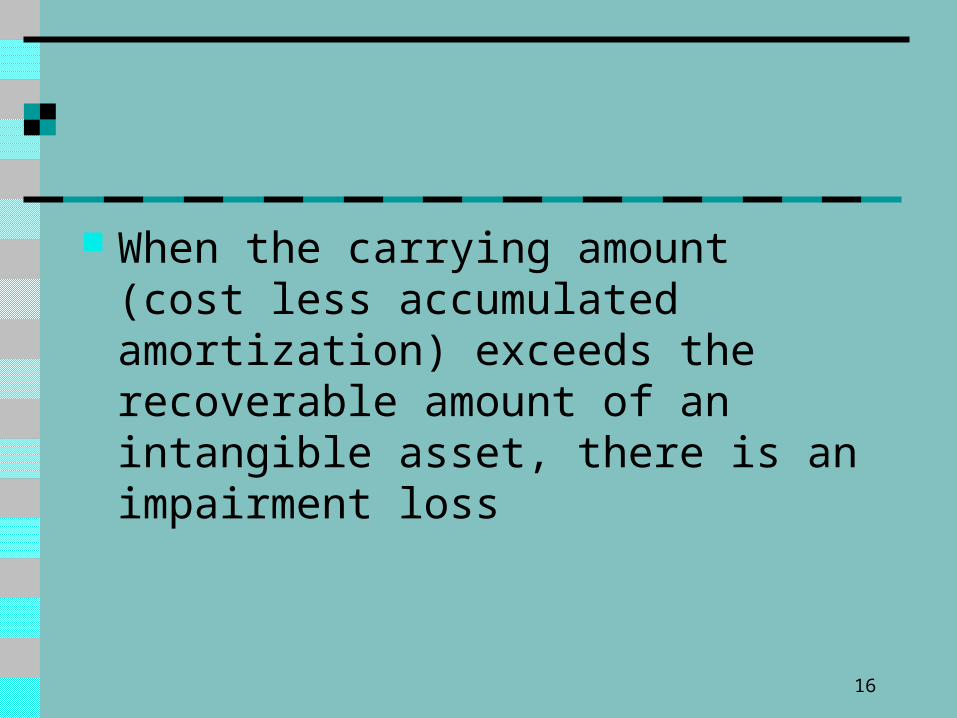

When the carrying amount (cost less accumulated amortization) exceeds the recoverable amount of an intangible asset, there is an impairment loss

17

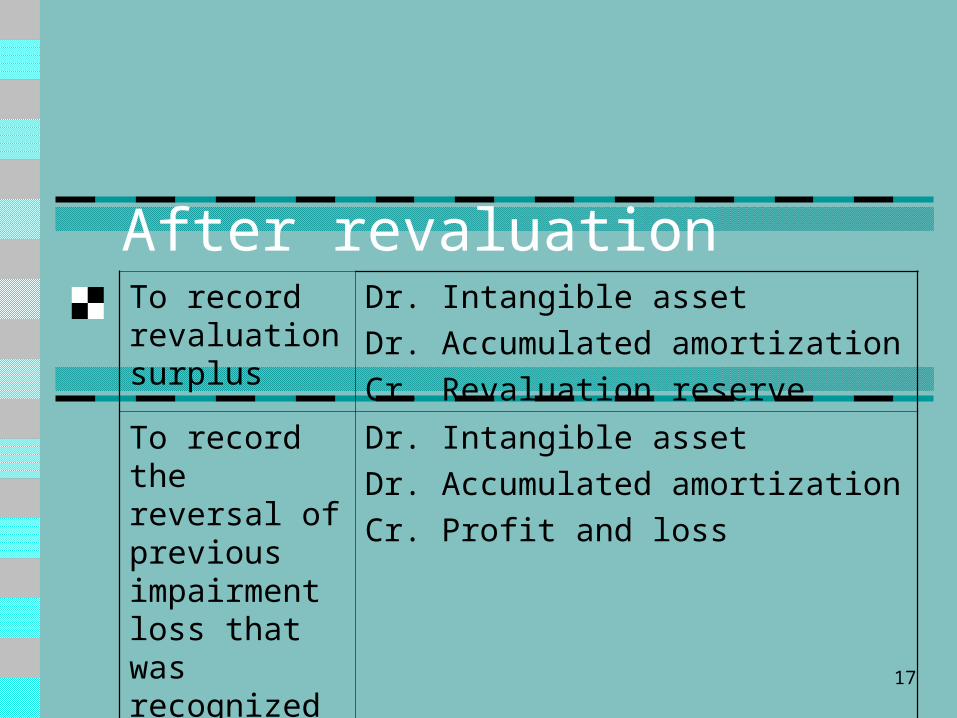

After revaluationTo record revaluation surplus

Dr. Intangible asset

Dr. Accumulated amortization

Cr. Revaluation reserve

To record the reversal of previous impairment loss that was recognized as an expenses

Dr. Intangible asset

Dr. Accumulated amortization

Cr. Profit and loss

18

After initial recognition, an intangible asset should be carried at a revalued amount

After revaluation, the intangible asset should be stated at its fair value less any subsequent amortization and any subsequent accumulated impairment losses

19

Accounting for Goodwill

20

Definition

Goodwill is the difference between the value of a business as a whole and the aggregate of the fair value of its separable net assets

Goodwill = Selling price as a going concern – Fair value of separable net assets = Selling price – ( Assets – Liabilities)

21

Nature of Goodwill

A business may be valued higher as a going concern, or a buyer may be willing to pay more for a business as a going concern than the total value of net assets because of the favourable attributes a firm owns.

Some of advantages which may add to the value of a business as a going concern Good location Good customer relations Good reputation Well-known products Experienced and efficient employees and management team Good relation with suppliers

22

Characteristics

Is intrinsic to the business Is self-developed The value of goodwill may fluctuate widely

according to internal and external circumstances

The value of goodwill is subjective according to different valuers.

Why intrinsic?

Its existence depends on the continuance of the business. It cannot be realized separately from the business as a whole.

back

24

Calculation of goodwill

Subjective Judgement Average Sales/Fees/Profits Method Super Profit Method

25

Subject Judgement Estimate the value of goodwill with reference

to some intangible factors and according to their professional judgement

26

Average Sales/Fees/Profit Method It can be calculated on gross average or weight

average

Goodwill = Average annual sales/fees/profits over a stated number of years * a factorThe factor is usually stated as a certain number of years’ purchase of the average sales/fees/profits

27

Example 1

28

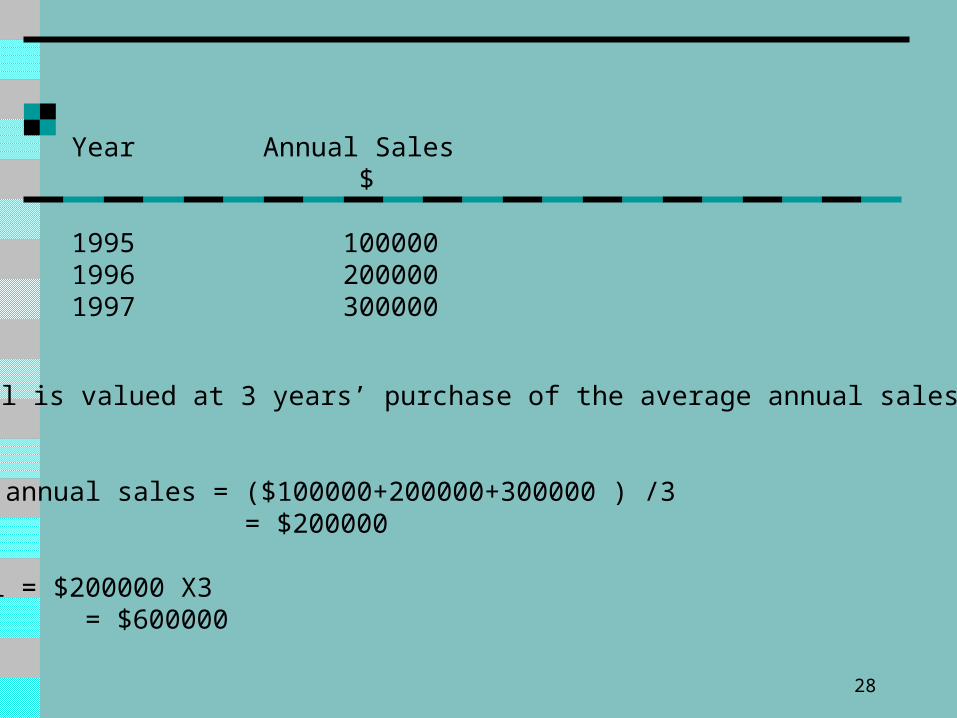

Year Annual Sales$

1995 100000 1996 200000 1997 300000

(a) Goodwill is valued at 3 years’ purchase of the average annual sales of the past3 years:

Average annual sales = ($100000+200000+300000 ) /3 = $200000

Goodwill = $200000 X3 = $600000

29

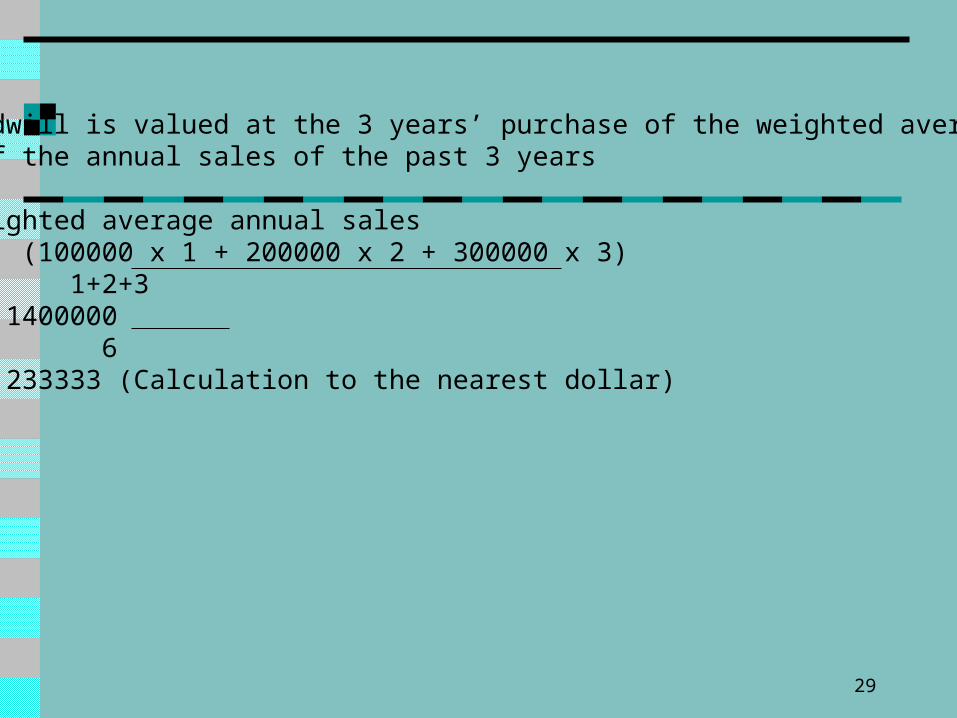

(b) Goodwill is valued at the 3 years’ purchase of the weighted average of the annual sales of the past 3 years

Weighted average annual sales = (100000 x 1 + 200000 x 2 + 300000 x 3)

1+2+3 = 1400000 6 = 233333 (Calculation to the nearest dollar)

30

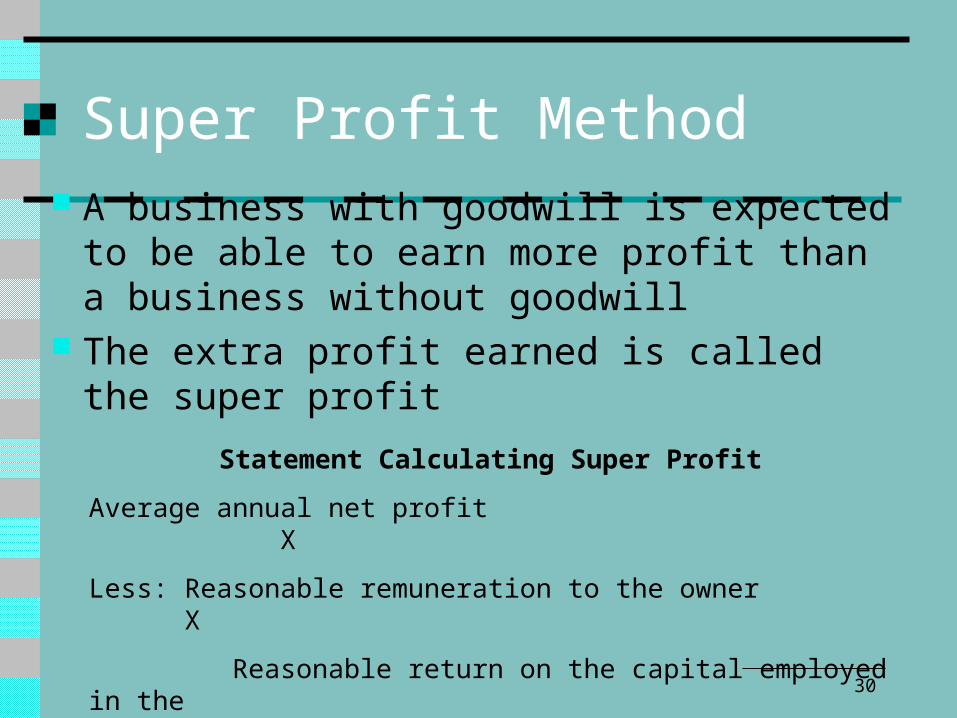

Super Profit Method A business with goodwill is expected to be

able to earn more profit than a business without goodwill

The extra profit earned is called the super profit

Statement Calculating Super Profit

Average annual net profit X

Less: Reasonable remuneration to the owner X

Reasonable return on the capital employed in the

tangible assets X X

Super profit X

31

Example 2

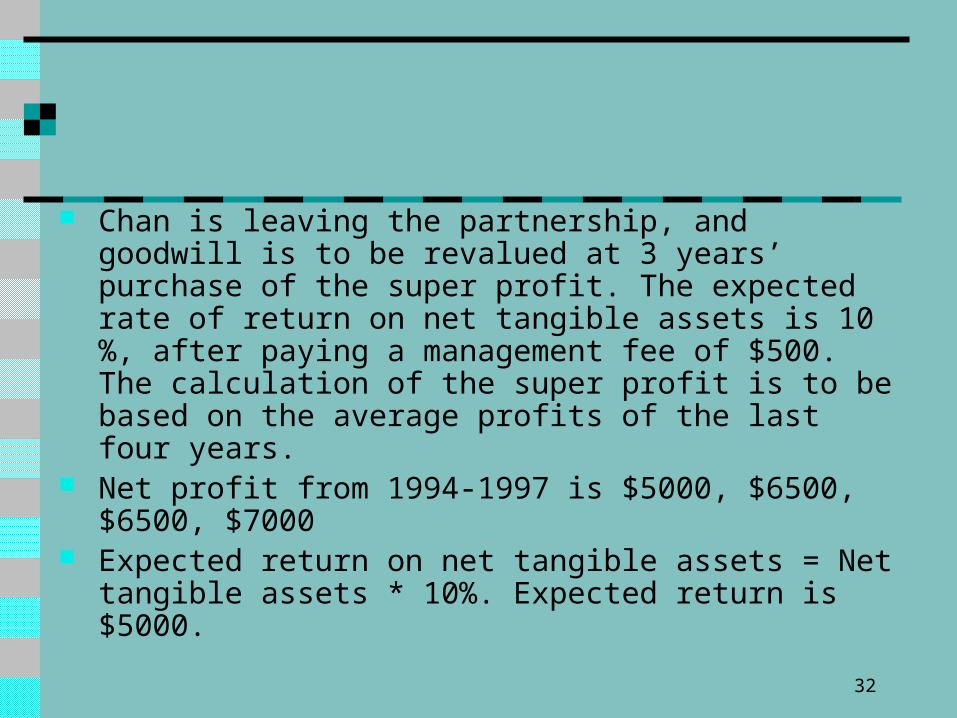

32

Chan is leaving the partnership, and goodwill is to be revalued at 3 years’ purchase of the super profit. The expected rate of return on net tangible assets is 10 %, after paying a management fee of $500. The calculation of the super profit is to be based on the average profits of the last four years.

Net profit from 1994-1997 is $5000, $6500, $6500, $7000

Expected return on net tangible assets = Net tangible assets * 10%. Expected return is $5000.

33

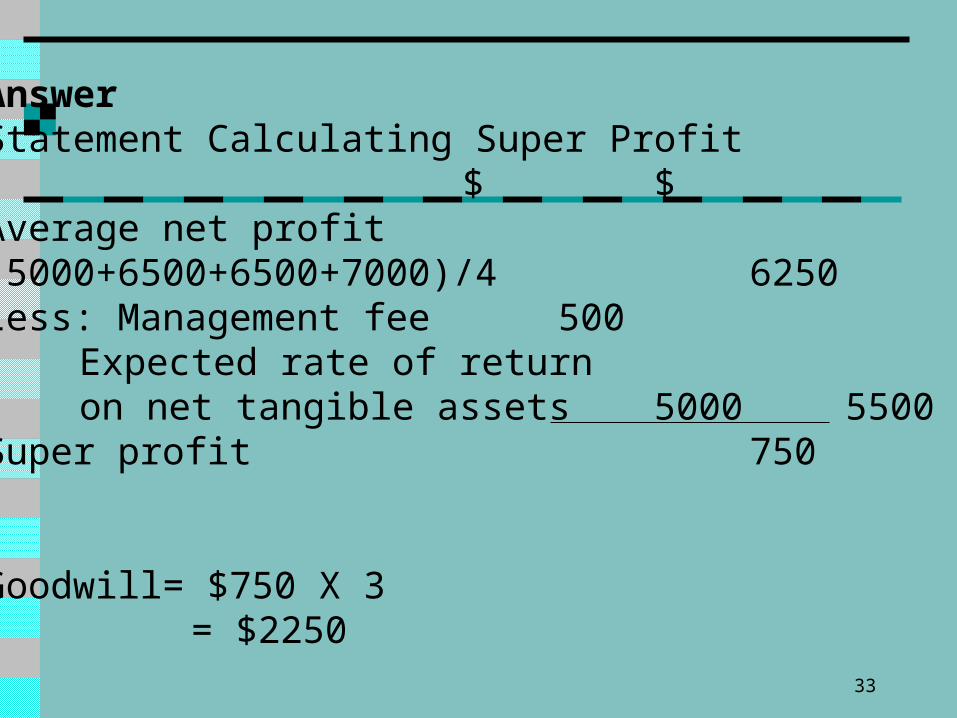

AnswerStatement Calculating Super Profit

$ $Average net profit(5000+6500+6500+7000)/4 6250Less: Management fee 500

Expected rate of returnon net tangible assets 5000 5500

Super profit 750

Goodwill= $750 X 3 = $2250

34

Different types of goodwill

Inherent goodwill Purchased goodwill Negative goodwill

35

Inherent goodwill

36

Definition

It is the goodwill developed by the business internally.

Over a long period in a certain trade, the business has developed many good relations

Therefore, the public estimates that the value of the business as a going concern is higher than the value of its net assets

37

Accounting treatment

Non-purchased goodwill should not be recognized in the financial statements

38

Reasons supporting this argument It is an internally generated goodwill which cannot

be attributed to separately intangible expenditures It is intrinsic to the business. It cannot be sold as a

separate asset The value of non-purchased goodwill may

fluctuate widely according to internal and external circumstances

The valuation and verifiability of the existence of non-purchased goodwill are subjective

39

Purchased goodwill

40

Definition

It arises when a business acquires another as a going concern

It is the difference between the purchase consideration of the company acquired as a going concern and the fair value of its net assets

41

Accounting treatments

Purchased goodwill is recorded at cost less any accumulated amortization and any accumulated impairment losses

42

To record the cost of goodwill

Dr. Goodwill

Cr. Business purchase

43

Purchased goodwill should be measured initially at cost

Reasons Money has been spent to acquire the goodwill,

so it is difficult to argue that purchased goodwill is not an asset

44

To record the provision for amortization

Dr. Profit and loss

Cr. Accumulated amortization

45

After initial recognition, purchased goodwill should be carried at its cost less any accumulated amortization

Purchased goodwill should be amortized on a systematic basis over its useful life (not exceed 20 years)

46

To record the impairment loss

Dr. Other assets

Dr. Goodwill

Cr. Profit and loss

47

When the carrying amount (cost less accumulated amortization) exceeds the recoverable amount of an intangible asset, there is an impairment loss

The impairment loss should be allocated firstly to the goodwill, and then the other assets proportional to the carrying amount of each asset

48

Revaluation

No entry

49

There is no active market, hence goodwill should not be revaluated

50

Negative goodwill

Negative goodwill arises in a business acquisition when the fair market value of the net assets of the acquired company exceeds the purchase price paid

It is an unrealized capital profit which should be credited to the reserves

51

Negative goodwill arises when

There is a bargain purchase due to a quick sale

The purchase price has been reduced for the expected future cost or losses

52

3 steps for accounting negative goodwill Ascertain the amount of the negative goodwill Identify future losses and expenses Remaining negative goodwill

The amount of negative goodwill not exceeding the fair value of acquired identifiable non-monetary assets should be recognized as income on a systematic basis over the remaining weighted average useful life of the identifiable acquired depreciable/amortizable asset

The amount of negative goodwill in excess of the fair value of acquired identifiable non-monetary assets should be recognized as income immediately

53

Example

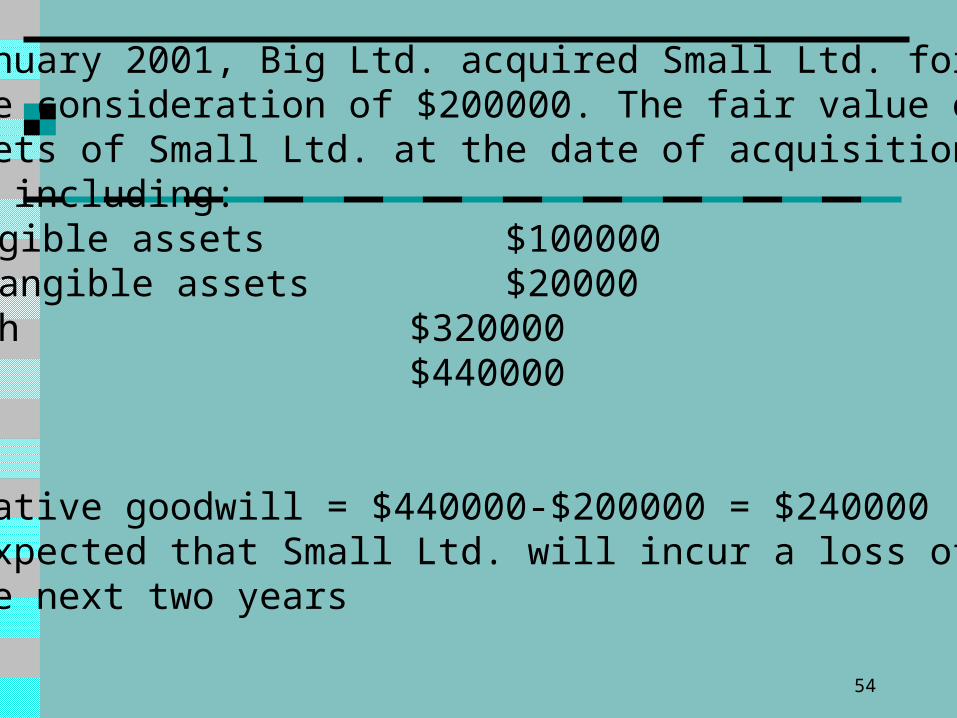

54

On 1 January 2001, Big Ltd. acquired Small Ltd. for a purchase consideration of $200000. The fair value of the net assets of Small Ltd. at the date of acquisition was $440000 including:

Tangible assets $100000Intangible assets $20000Cash $320000

$440000

The negative goodwill = $440000-$200000 = $240000It is expected that Small Ltd. will incur a loss of $30000Over the next two years

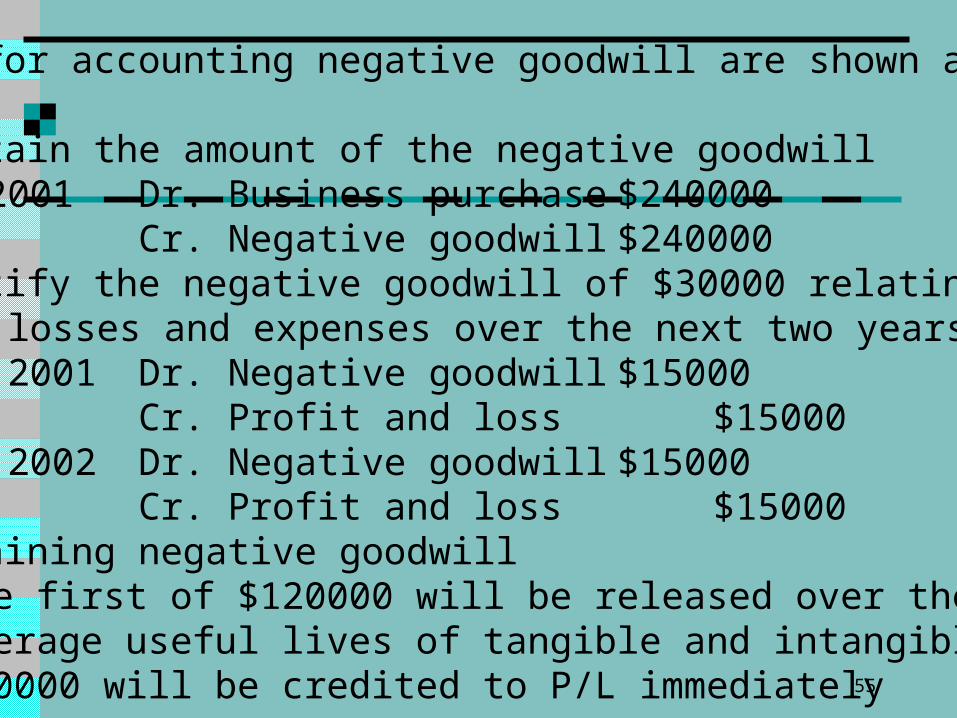

55

3 steps for accounting negative goodwill are shown as follows:(a) Ascertain the amount of the negative goodwill

1 Jan 2001 Dr. Business purchase $240000Cr. Negative goodwill $240000

(b) Identify the negative goodwill of $30000 relating to future losses and expenses over the next two years31 Dec 2001Dr. Negative goodwill $15000

Cr. Profit and loss $1500031 Dec 2002Dr. Negative goodwill $15000

Cr. Profit and loss $15000( c) Remaining negative goodwill• the first of $120000 will be released over the weighted

average useful lives of tangible and intangible asset• $90000 will be credited to P/L immediately

56

Accounting for Goodwill in Partnership

57

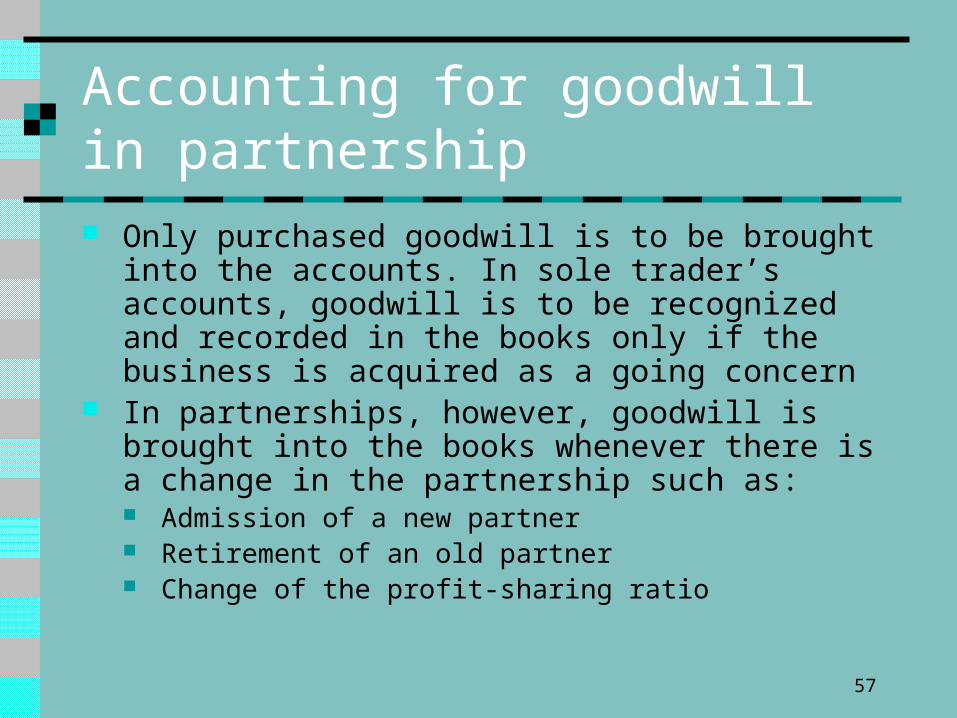

Accounting for goodwill in partnership

Only purchased goodwill is to be brought into the accounts. In sole trader’s accounts, goodwill is to be recognized and recorded in the books only if the business is acquired as a going concern

In partnerships, however, goodwill is brought into the books whenever there is a change in the partnership such as: Admission of a new partner Retirement of an old partner Change of the profit-sharing ratio

58

Each partner has a share of the profit-sharing ratio. At a change in the partnership, goodwill must be taken into account and shared among the existing partners, according to the existing profit-sharing ratio

59

Goodwill on the admission of a new partner

60

Goodwill on the admission of a new partner

The new partner is required to pay for his share of the tangible assets as well as the goodwill, according to the profit-sharing ratio

On the admission of a new partner, goodwill must be revalued

However, not all business keep a goodwill account in their books. Goodwill adjustments can be done: Goodwill account opened Goodwill account not opened

61

Goodwill account opened

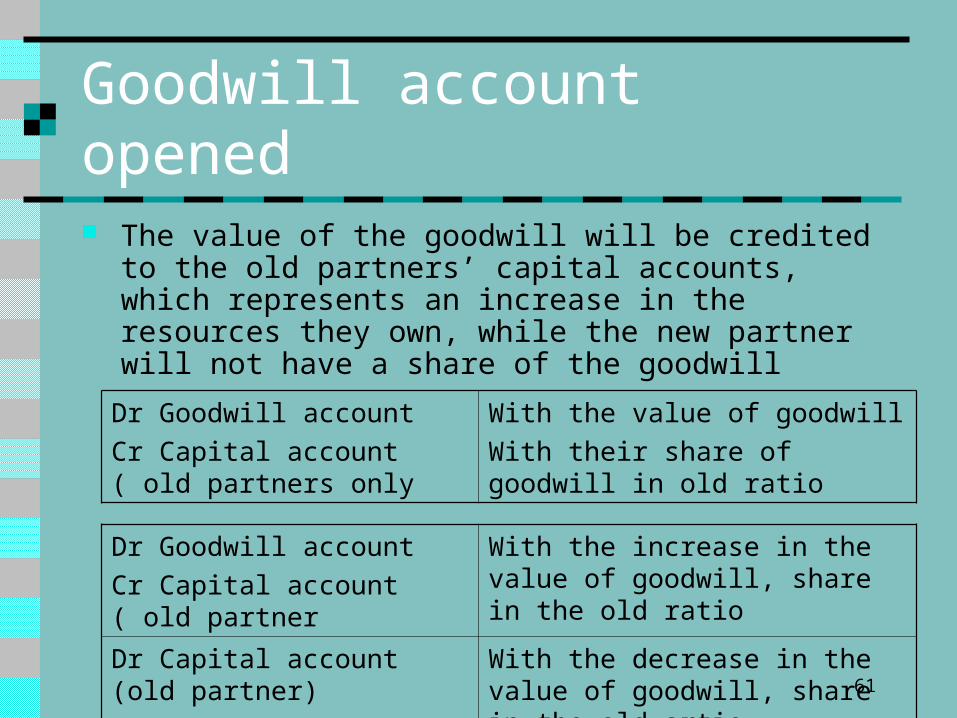

The value of the goodwill will be credited to the old partners’ capital accounts, which represents an increase in the resources they own, while the new partner will not have a share of the goodwill

Dr Goodwill account

Cr Capital account ( old partners only

With the value of goodwill

With their share of goodwill in old ratio

Dr Goodwill account

Cr Capital account ( old partner

With the increase in the value of goodwill, share in the old ratio

Dr Capital account (old partner)

Cr Goodwill account

With the decrease in the value of goodwill, share in the old artio

62

Goodwill account not opened

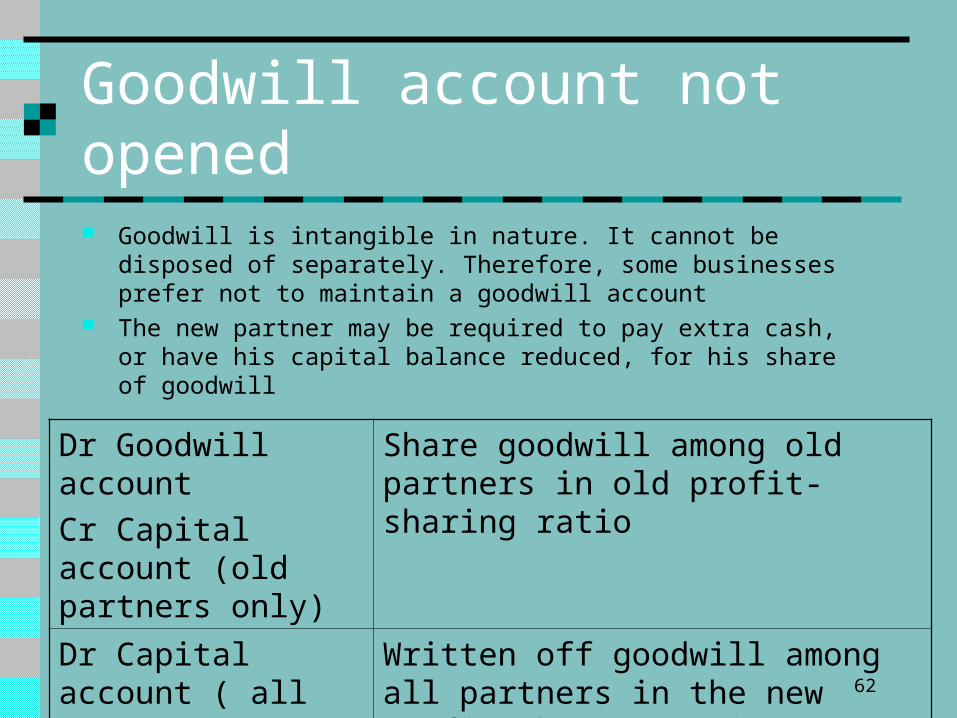

Goodwill is intangible in nature. It cannot be disposed of separately. Therefore, some businesses prefer not to maintain a goodwill account

The new partner may be required to pay extra cash, or have his capital balance reduced, for his share of goodwill

Dr Goodwill account

Cr Capital account (old partners only)

Share goodwill among old partners in old profit-sharing ratio

Dr Capital account ( all partners)

Cr Goodwill account

Written off goodwill among all partners in the new profit-sharing ratio

63

Example 3

64

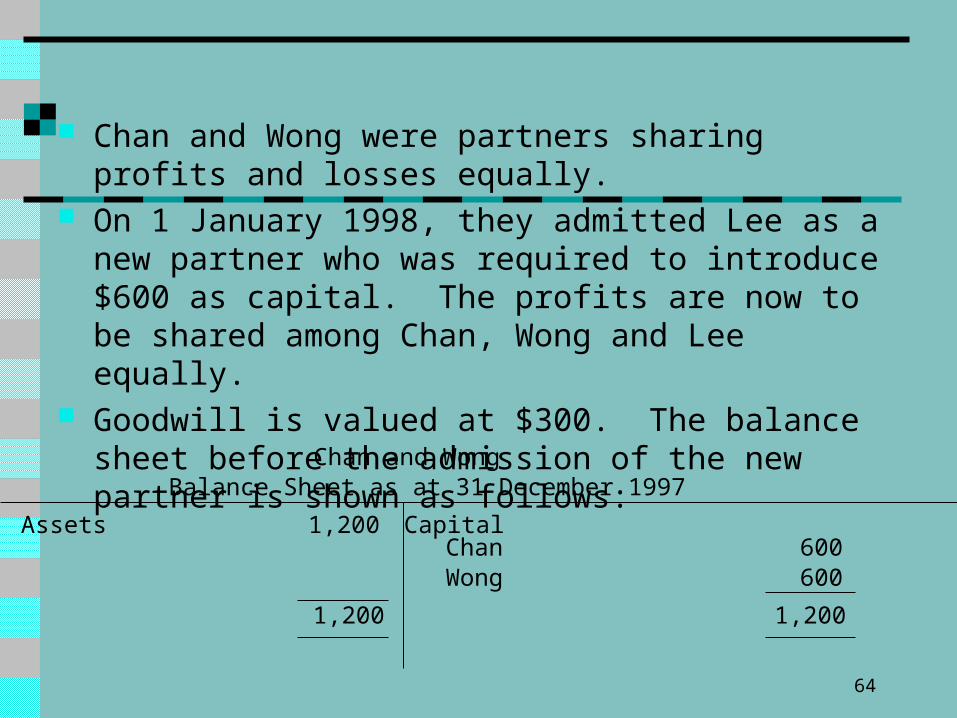

Chan and Wong were partners sharing profits and losses equally.

On 1 January 1998, they admitted Lee as a new partner who was required to introduce $600 as capital. The profits are now to be shared among Chan, Wong and Lee equally.

Goodwill is valued at $300. The balance sheet before the admission of the new partner is shown as follows:

Chan and WongBalance Sheet as at 31 December 1997

Assets 1,200 Capital Chan 600 Wong 600

1,200 1,200

65

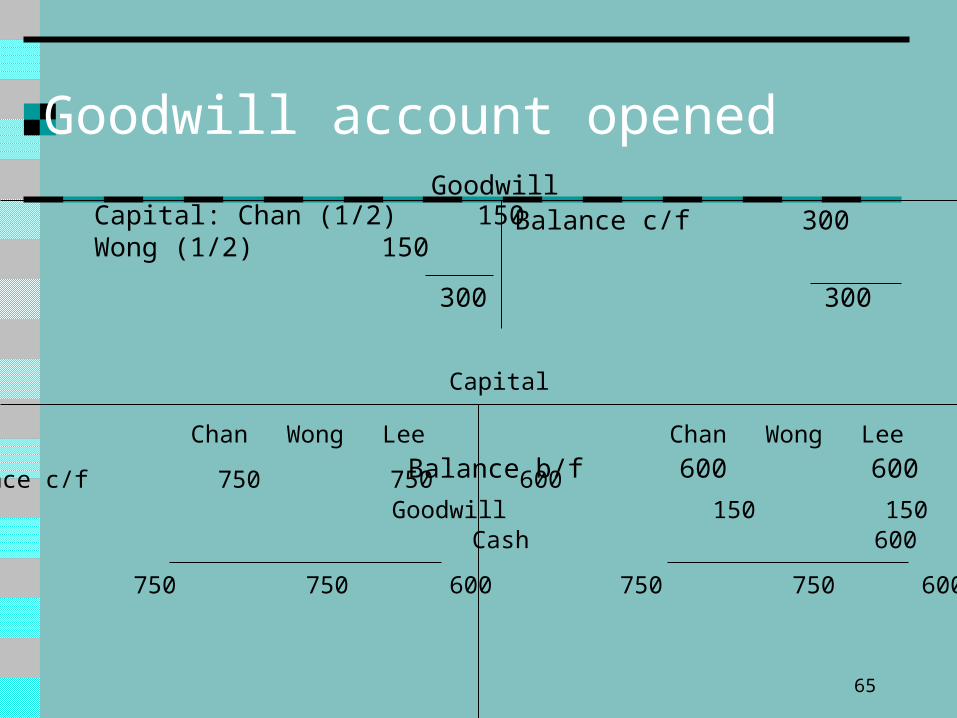

Goodwill account openedGoodwill

Capital: Chan (1/2) 150 Wong (1/2) 150

300 300

Capital

Chan Wong Lee Chan Wong Lee

Balance c/f 750 750 600 Goodwill 150 150

Cash 600

750 750 600 750 750 600

Balance c/f 300

Balance b/f 600 600

66

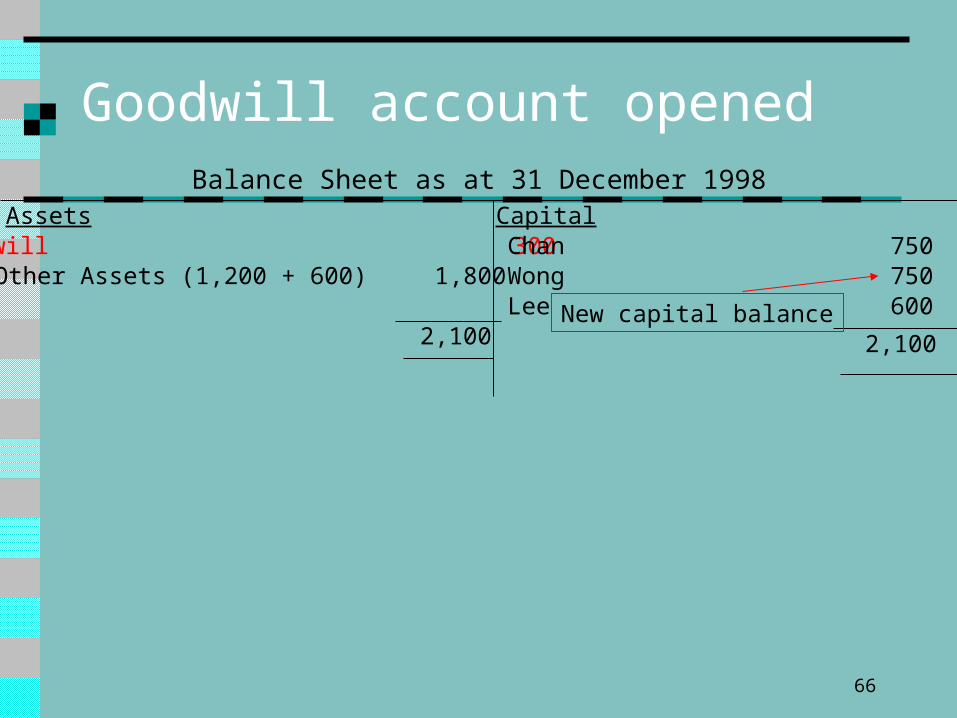

Goodwill account openedBalance Sheet as at 31 December 1998

AssetsGoodwill 300

CapitalChan 750

Other Assets (1,200 + 600) 1,800 Wong 750Lee 600

2,100 2,100New capital balance

67

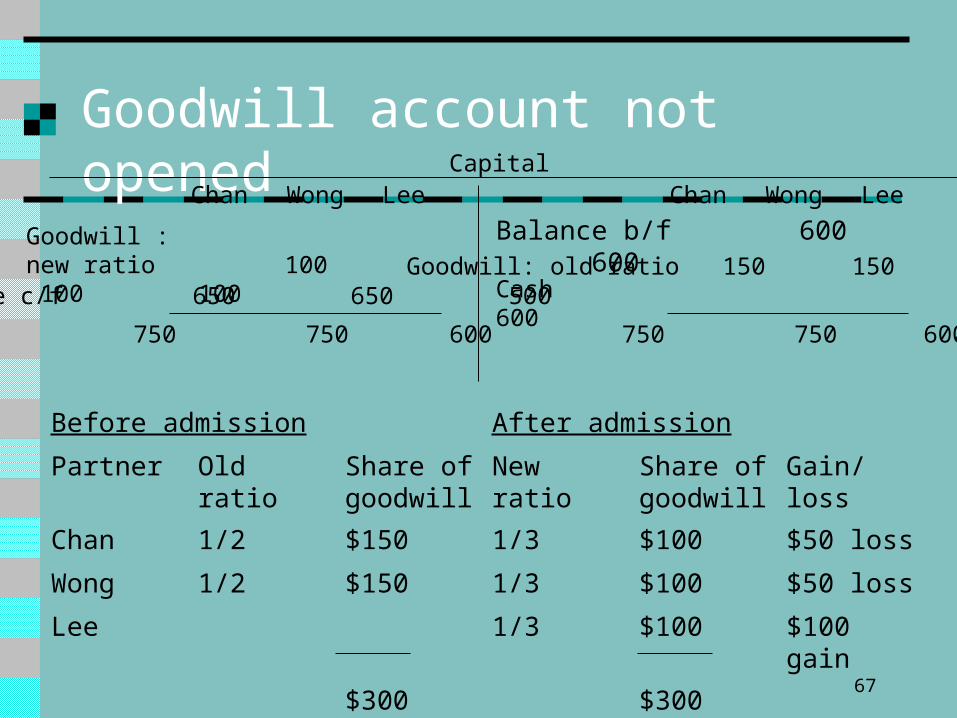

Goodwill account not opened CapitalChan Wong Lee Chan Wong Lee

Goodwill : new ratio 100 100 100

Goodwill: old ratio 150 150Cash 600

750 750 600 750 750 600

Balance c/f 650 650 500

Balance b/f 600 600

Before admission After admission

Partner Old ratio Share of goodwill

New ratio Share of goodwill

Gain/loss

Chan 1/2 $150 1/3 $100 $50 loss

Wong 1/2 $150 1/3 $100 $50 loss

Lee 1/3 $100 $100 gain

$300 $300

68

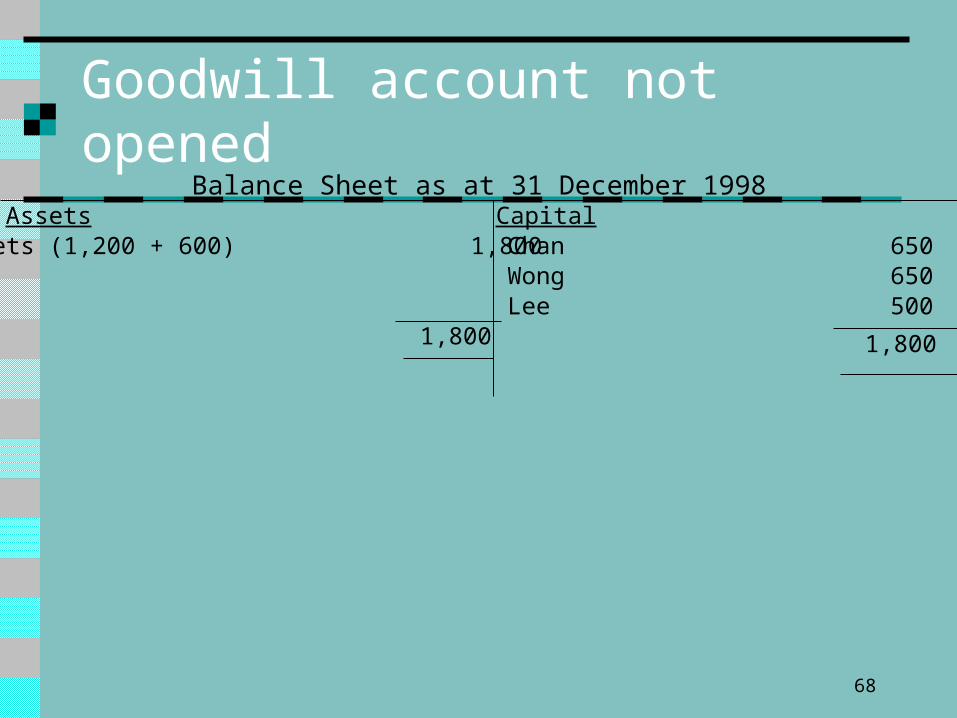

Goodwill account not openedBalance Sheet as at 31 December 1998

Assets CapitalChan 650Wong 650Lee 500

1,800 1,800

Assets (1,200 + 600) 1,800

69

Accounting for Research and Development Expenditures

70

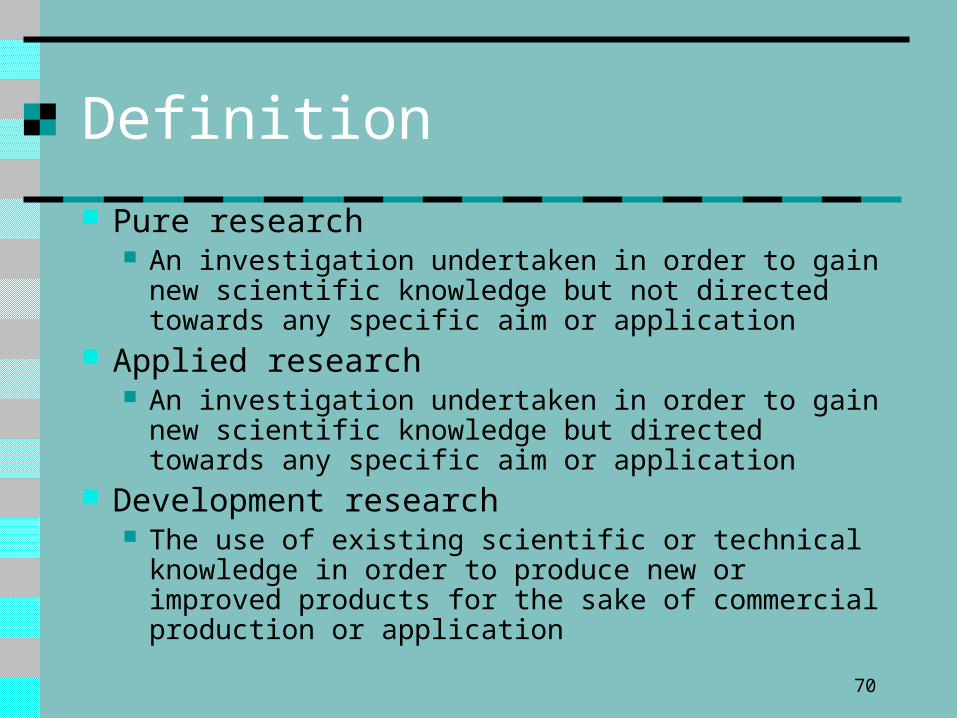

Definition

Pure research An investigation undertaken in order to gain new

scientific knowledge but not directed towards any specific aim or application

Applied research An investigation undertaken in order to gain new

scientific knowledge but directed towards any specific aim or application

Development research The use of existing scientific or technical knowledge in

order to produce new or improved products for the sake of commercial production or application

71

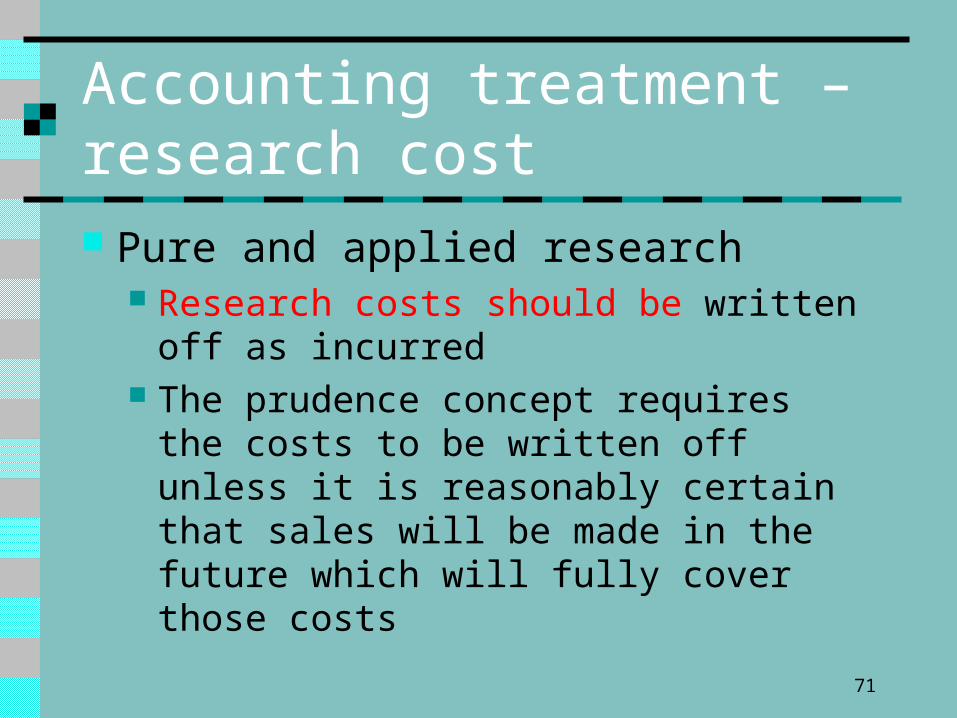

Accounting treatment – research cost Pure and applied research

Research costs should be written off as incurred The prudence concept requires the costs to be

written off unless it is reasonably certain that sales will be made in the future which will fully cover those costs

72

Accounting treatment – development cost Development expenditures

Development expenditures should be written off as incurred

Development expenditures can be deferred to future periods and recorded as an asset

OR

73

Development expenditures can be deferred to future periods and recorded as an asset,when the following conditions are satisfied: The project is clearly defined The expenditures are identified separately There is reasonable certainty about the outcome of the

project The deferred development expenditures are expected to

be recover from related future sales or other revenues The business has adequate resources to complete the

project

74

Deferred development expenditures should be amortized on a systematic basis over the period in which the product is sold. The amortization starts in the year that commercial production starts

When there is any doubt about the certainty of the future revenue, the unamortized amount of deferred expenditures must be written off immediately

Reinstatement of previously written-down deferred expenditure should be credited to P/L

75

Reversal of impairment loss is rstricted to the amount that would restore the carrying amount as if no impairment loss has been recognized

Any fixed assets acquired for development activities should be capitalized and depreciated over their useful lives

76

Accounting for Trademark

77

Definition

A trademark is the legal protection afforded the names, symbols, and other specific identities assigned to a product

78

Valuation of trademark

The costs capitalized include design, registration and the legal cost of successfully defending the trademark in court

79

Accounting for trademark

A trademark is deferred and amortized as an expense over the shorter if the legal life or economic life

It is generally considered to have no limited term of existence or natural limited life. However, the legal protection of a trademark is subject to renewal after a number of years

80

Accounting for Patent

81

Definition

A patent is an exclusive right to use, manufacture, process, or sell a product granted by the government

82

The valuation of patent

Patent can be purchased from the inventor or holder, or they can be generated internally

When a patent is purchased from the inventor, the cost capitalized include the acquisition cost, legal cost and the legal costs of successfully defending a patent in court

It a patent results from successful research and development efforts, the costs capitalized include only the legal costs such as registration fees and attorney fees, incurred in obtaining the patent

83

Accounting treatment

The research and development costs spent to develop the patent must be written off to expenses as they are incurred

A patent should be amortized over its remaining legal life or economic life, whichever is shorter

It the patent is lost in court, it should be written off and shown as an exceptional loss

84

Accounting for Copyright

85

Definition

A copyright is the exclusive rights of the creator or heirs to reproduce or sell an artistic or published work

86

Valuation of copyright

It is recorded at its acquisition price

87

Accounting treatment

A copyright should be amortized over the shorter of its economic or legal life

88

Accounting for franchise

A franchise is an exclusive rights granted to a franchise permitting him to operate using the franchiser’s name

89

Valuation of franchise

The franchise must pay a franchise fee for such rights

90

Accounting treatment

A franchise should be amortized over its economic life

![INTANGIBLE VALUE –FACT OR FICTION - AI Home | … · [IAS 38.8] 3. INTANGIBLE VALUE –FACT OR FICTION ... 2.36 INTANGIBLE PROPERTY (INTANGIBLE ASSETS): Non-physical assets, …](https://static.fdocuments.us/doc/165x107/5af0812f7f8b9ac2468e1bc2/intangible-value-fact-or-fiction-ai-home-ias-388-3-intangible-value.jpg)