1 HKAS 38 Intangible Assets Date: December 23, 2008.

27

1 HKAS 38 HKAS 38 Intangible Assets Intangible Assets Date: December 23, 2008 Date: December 23, 2008

-

Upload

pamela-sullivan -

Category

Documents

-

view

222 -

download

1

Transcript of 1 HKAS 38 Intangible Assets Date: December 23, 2008.

11

HKAS 38 HKAS 38 Intangible AssetsIntangible Assets

Date: December 23, 2008Date: December 23, 2008

22

ContentsContents

Definition Definition Recognition and Measurement Recognition and Measurement Subsequent measurement Subsequent measurement Useful lifeUseful life Impairment Impairment Retirement and disposalRetirement and disposal

33

DefinitionDefinition

An intangible assets is An intangible assets is

1.1. IdentifiablyIdentifiably : an : an identifiableidentifiable non- non-monetary asset monetary asset without physicalwithout physical substancesubstance

2.2. ControlControl : a resources : a resources controlledcontrolled by an by an entity as a result of entity as a result of past eventspast events

3.3. Future economic benefitFuture economic benefit : : future future economic benefitseconomic benefits are expected to flow are expected to flow to the entityto the entity

44

DefinitionDefinition

1) Identifiably Criterion1) Identifiably Criteriona)a) is separable, i.e. capable of being is separable, i.e. capable of being

separated or divided from the entity and separated or divided from the entity and sold, transferred, licensed, rented or sold, transferred, licensed, rented or exchanged, either individually or exchanged, either individually or together with a related contract, asset or together with a related contract, asset or liability orliability or

b)b) arises from contractual or other legal arises from contractual or other legal rights rights

Identifiable= Separable or contractualIdentifiable= Separable or contractual

55

DefinitionDefinition

2) Control2) ControlAn enterprise controls an asset if An enterprise controls an asset if it has it has power to obtain future economic benefitspower to obtain future economic benefits flowing from the underlying resource and flowing from the underlying resource and also can also can restrict the access others to those restrict the access others to those benefitsbenefits

Its capacity to control such future economic benefits would normally stem from legal rightslegal rights that are enforceable in court of law

66

DefinitionDefinition

3) Future economic benefits3) Future economic benefitsa)a) Revenue from the sales of products or servicesRevenue from the sales of products or services

b)b) Cost saving Cost saving

c)c) Other benefits resulting from the use of the Other benefits resulting from the use of the assets by the entityassets by the entity

77

Recognition and initial measurementRecognition and initial measurement

RecognitionRecognition

Intangible assets should be recognized if:Intangible assets should be recognized if:

1.1. Future economic benefits will flow to the Future economic benefits will flow to the enterpriseenterprise

2.2. Cost can be measured reliably Cost can be measured reliably

Initial measurement Initial measurement

An intangible asset shall be measured An intangible asset shall be measured initially at initially at costcost

88

Generally, 6 ways to create intangible assetsGenerally, 6 ways to create intangible assets

1.1. Separable acquisition (by purchase)Separable acquisition (by purchase)

2.2. Acquisition as part of business Acquisition as part of business combinationcombination

3.3. Acquisition by government grantAcquisition by government grant

4.4. Exchange of assetsExchange of assets

5.5. Internally generated goodwillInternally generated goodwill

6.6. Internally generated intangible assetInternally generated intangible asset

Recognition and initial measurementRecognition and initial measurement

99

1. Separate acquisition1. Separate acquisition

1.1. If acquired by purchase, cost can be measured If acquired by purchase, cost can be measured reliablyreliably

2.2. Cost comprise: Cost comprise: - purchase cost- purchase cost- import duties- import duties- all other direct expenditure of preparing the - all other direct expenditure of preparing the assets for its intended useassets for its intended use

Example of direct attributable costsExample of direct attributable costsa)a) Professional fee arising directly from bringing the asset to its Professional fee arising directly from bringing the asset to its

working conditionworking conditionb)b) Cost of testing whether the asset is functioning properlyCost of testing whether the asset is functioning properly

Example of expenditure that are not part of the cost of IAExample of expenditure that are not part of the cost of IAa)a) Advertising and promotional costsAdvertising and promotional costsb)b) Administration and other general overhead costsAdministration and other general overhead costs

1010

2. Acquisition as part of 2. Acquisition as part of business combinationbusiness combination

1.1. Recognized at its fair value that is either the quoted market priRecognized at its fair value that is either the quoted market prices or price of most recent similar transactionces or price of most recent similar transaction

2.2. If meet recognition criteria, acquirer should recognize it even if If meet recognition criteria, acquirer should recognize it even if it is not originally recognized by the acquiree (e.g. in-process Rit is not originally recognized by the acquiree (e.g. in-process R&D project that were ineligible for recognition in the acquiree's &D project that were ineligible for recognition in the acquiree's books if it is generally internally)books if it is generally internally)

3.3. If in-process research and development project has a fair value,If in-process research and development project has a fair value, it means the market expects there is probable future economi it means the market expects there is probable future economic benefit flow from this asset. So the “probability” criteria is c benefit flow from this asset. So the “probability” criteria is always met. No need to access the future commercial feasibilitalways met. No need to access the future commercial feasibility, technical competence and future recoverable amount, etc. y, technical competence and future recoverable amount, etc.

4.4. Intangible assets should be recognized separately from goodwIntangible assets should be recognized separately from goodwill in a business combination.ill in a business combination.

1111

2. Acquisition as part of 2. Acquisition as part of business combinationbusiness combination

The fair value of intangible assets acquire in the business The fair value of intangible assets acquire in the business combination can normally be measured with sufficient combination can normally be measured with sufficient reliability to be recognized separately from goodwill.reliability to be recognized separately from goodwill.

The only rare circumstances in which it might not be possible The only rare circumstances in which it might not be possible to measure reliably the fair value of an intangible asset to measure reliably the fair value of an intangible asset acquired in a business combination acquired in a business combination

When the intangible asset arises from legal or other When the intangible asset arises from legal or other contractual rights orcontractual rights or

Either is no separable or is separable but there is no history Either is no separable or is separable but there is no history or evidence of exchange transactions for the same or similar or evidence of exchange transactions for the same or similar assetsassets

-> it should be subsumed (grouped) into goodwill-> it should be subsumed (grouped) into goodwill

1212

2. Acquisition as part of 2. Acquisition as part of business combinationbusiness combination

In initially measuring the fair value of an In initially measuring the fair value of an intangible assetintangible asset

1) Active Market1) Active Market

- current bid price - current bid price

- the price of the most recent similar transaction- the price of the most recent similar transaction

2) No active market2) No active market

- fair value is the amount that the entity would - fair value is the amount that the entity would have paid fro the asset, at the acquisition date, in have paid fro the asset, at the acquisition date, in an arm’s length transaction between the an arm’s length transaction between the knowledgeable and willing parties, on the basis of knowledgeable and willing parties, on the basis of the best information availablethe best information available

1313

3.Acquisition by government grant3.Acquisition by government grant

E.g. Airport landing rights, licenses to E.g. Airport landing rights, licenses to operate radio/TV stations, right to assess operate radio/TV stations, right to assess other restricted resourcesother restricted resources

1. Recognized initially at fair value

2. Alternatively, recognize the assets at nominal value + any expenditure directly attibutable to preparing the assets

1414

4. Exchange of assets4. Exchange of assets

The cost of such intangible asset is measured The cost of such intangible asset is measured at fair value unless at fair value unless

The exchange transaction lacks commercial The exchange transaction lacks commercial substance or substance or

The fair value of neither the assets received The fair value of neither the assets received nor the asset given up is reliably nor the asset given up is reliably measurablemeasurable

If the fair value cannot be measured reliably:If the fair value cannot be measured reliably: Cost of the new asset is the carrying amount Cost of the new asset is the carrying amount

of asset given up. of asset given up. No gain or loss resulted.No gain or loss resulted.

1515

5. Internally generated goodwill5. Internally generated goodwill

It should not be recognized as asset It should not be recognized as asset as it is not an identifiable resource as it is not an identifiable resource controlled by the enterprise that can controlled by the enterprise that can measured reliably at cost.measured reliably at cost.

1616

6. Internally generated intangible 6. Internally generated intangible assets – Research & Developmentassets – Research & Development

Research phase Development phase

Internally generated intangible assets

No intangible asset should be recognized

Cost incurred expensed to I/S

Recognize as asset only if 1) Technically feasible

of completing the IA2) Ability to complete 3) Intention to complete4) Availability of adequate technical, financial and other resources 5) Has existing market 6) Able to measure the expenditure

1717

6. Internally generated intangible 6. Internally generated intangible assets – Research & Developmentassets – Research & DevelopmentIf an enterprise cannot distinguish the research If an enterprise cannot distinguish the research phase from the development phase phase from the development phase -> treats the expenditure on that project as if it -> treats the expenditure on that project as if it were incurred in the research phase only were incurred in the research phase only -> cost incurred expensed to I/S -> cost incurred expensed to I/S

However, even the recognition are met, However, even the recognition are met, internally generated brands, mastheads, internally generated brands, mastheads, publishing titles, customer lists and items similar publishing titles, customer lists and items similar substance substance shall not be recognized as intangible shall not be recognized as intangible assets (specially disallowed in HKAS 38)assets (specially disallowed in HKAS 38)

1818

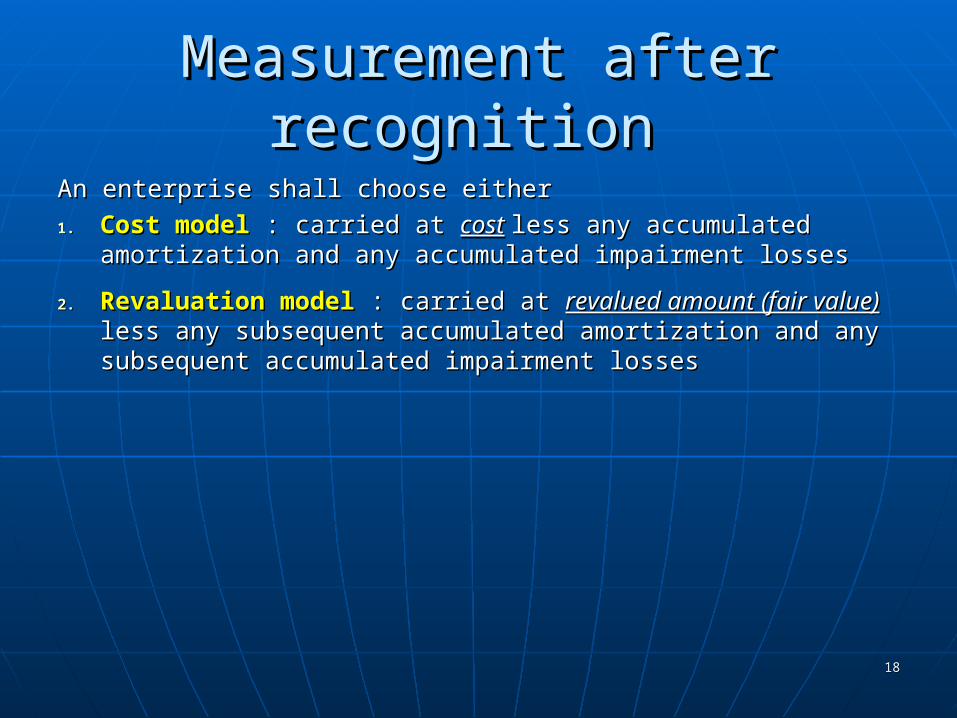

Measurement after recognition Measurement after recognition

An enterprise shall choose either An enterprise shall choose either

1.1. Cost modelCost model : carried at : carried at costcost less any accumulated less any accumulated amortization and any accumulated impairment lossesamortization and any accumulated impairment losses

2.2. Revaluation modelRevaluation model : carried at : carried at revalued amount (fair value)revalued amount (fair value) less any subsequent accumulated amortization and any less any subsequent accumulated amortization and any subsequent accumulated impairment losses subsequent accumulated impairment losses

1919

Measurement after recognitionMeasurement after recognition

Revaluation modelRevaluation model

Fair value – determined by reference to an Fair value – determined by reference to an active active marketmarket

Active marketActive market

1.1. the items traded in the market are homogeneousthe items traded in the market are homogeneous

2.2. willing buyers and sellers can normally be found at any time, willing buyers and sellers can normally be found at any time, and and

3.3. prices are available to the publicprices are available to the public

Frequency of revaluationsFrequency of revaluations

Revaluation shall be made with such regularity that Revaluation shall be made with such regularity that at the balance sheet date the carrying amount does at the balance sheet date the carrying amount does not differ materially from its fair value not differ materially from its fair value

2020

Measurement after recognitionMeasurement after recognitionRevaluation modelRevaluation model If there is revaluation surplus:

Dr. Intangible assetsDr. Intangible assetsCr. Revaluation reserveCr. Revaluation reserve

However the increase shall be credited I/S to the extent that it reverses a revaluation decrease of the same asset previously charged to I/S

If an IA’s carrying amt is decreased as a result of revaluation:

Dr. Loss on revaluation (I/S)Dr. Loss on revaluation (I/S)Cr. Intangible assetsCr. Intangible assets

However the decrease shall be debited to revaluation reserve to the extent of that any credit balance in the revaluation surplus in respect of that asset

2121

Measurement after recognitionMeasurement after recognition

Revaluation effect on accumulated Revaluation effect on accumulated amortizationamortization

1.1. Restated proportionatelyRestated proportionately with the change in with the change in the gross carrying amount of the asset so that the gross carrying amount of the asset so that the carrying amount of the asset after the the carrying amount of the asset after the revaluation equals its revalued amount revaluation equals its revalued amount

2.2. Eliminated against the gross carrying amountEliminated against the gross carrying amount of the asset and the net amount restated to the of the asset and the net amount restated to the revalued amount of the assetrevalued amount of the asset

2222

Useful lifeUseful life

Finite

The length of, or number of production or similar unit constituting, that useful life

Amortization requiredAmortization required

Indefinite

Based on an analysis of all of the relevant factors, there is no foreseeable limit to the period over which the asset is expected to generate net cash inflows for the entity

Amortization not Amortization not requiredrequired

2323

Useful lifeUseful life

The useful lifeThe useful life• shall not exceed the period of the contractual or shall not exceed the period of the contractual or

other legal rightsother legal rights• but may be shorter depending on the period over but may be shorter depending on the period over

which the enterprise expects to use the assetwhich the enterprise expects to use the asset• If the contractual or other legal rights can be If the contractual or other legal rights can be

renewed, the useful lift of the intangible asset shall renewed, the useful lift of the intangible asset shall include the renewal period only ifinclude the renewal period only if- there is evidence to support renewal by the - there is evidence to support renewal by the enterprise without significant costsenterprise without significant costs

2424

Amortization (IA with finite useful Amortization (IA with finite useful life)life)

Amortization method should reflect pattern in which the asset’s Amortization method should reflect pattern in which the asset’s economic benefits are consumed.economic benefits are consumed. Straight line methodStraight line method Diminishing balance Diminishing balance Unit of productionUnit of production

Residual value of intangible assetResidual value of intangible asset

1.1. Assumed to be zero unless there is Assumed to be zero unless there is - a commitment by a third party to purchase the - a commitment by a third party to purchase the assetasset- an active market exist at the end of asset’s economic - an active market exist at the end of asset’s economic

life where residual value can be determinedlife where residual value can be determined

2.2. If intangible asset is carried at cost, residual value is set at If intangible asset is carried at cost, residual value is set at selling price of similar assets at time of asset acquisitionselling price of similar assets at time of asset acquisition

3.3. If intangible asset is carried at revalued amount, residual If intangible asset is carried at revalued amount, residual value is re-estimated at date of revaluationvalue is re-estimated at date of revaluation

2525

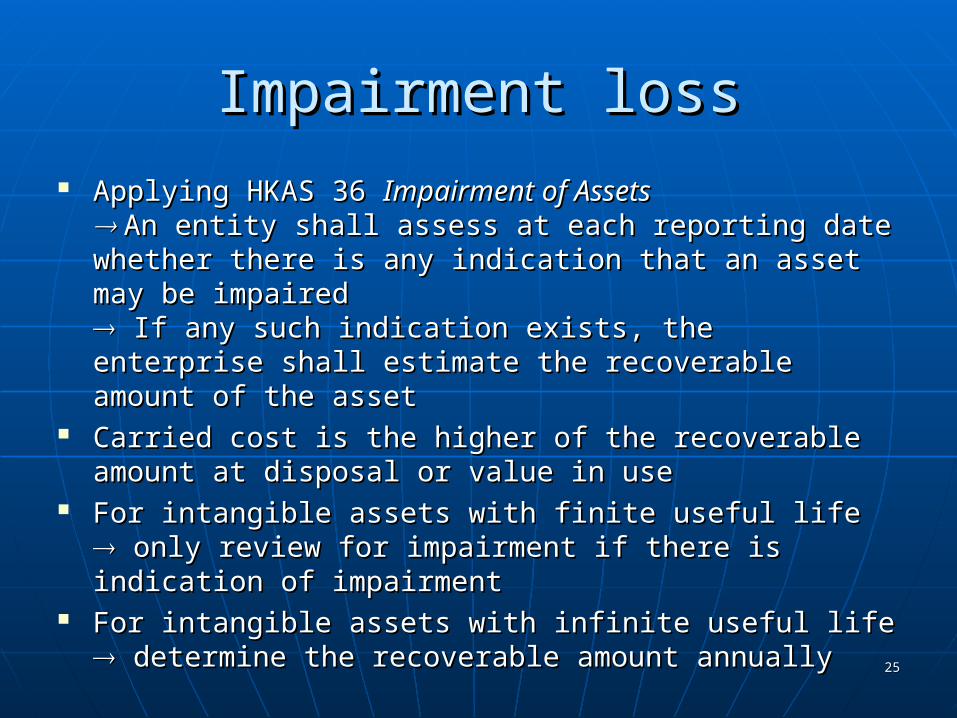

Impairment lossImpairment loss

Applying HKAS 36 Applying HKAS 36 Impairment of AssetsImpairment of Assets An entity shall assess at each reporting date An entity shall assess at each reporting date whether there is any indication that an asset may whether there is any indication that an asset may be impairedbe impaired If any such indication exists, the enterprise shall If any such indication exists, the enterprise shall estimate the recoverable amount of the assetestimate the recoverable amount of the asset

Carried cost is the higher of the recoverable Carried cost is the higher of the recoverable amount at disposal or value in useamount at disposal or value in use

For intangible assets with finite useful lifeFor intangible assets with finite useful life only review for impairment if there is indication of only review for impairment if there is indication of impairment impairment

For intangible assets with infinite useful lifeFor intangible assets with infinite useful life determine the recoverable amount annually determine the recoverable amount annually

2626

Retirement and disposalRetirement and disposal

An intangible asset shall be derecognizedAn intangible asset shall be derecognized• on disposal oron disposal or• when no future economic benefits are expected when no future economic benefits are expected

from its use or disposalfrom its use or disposal

The gain or loss arising from the de-recognition shall be The gain or loss arising from the de-recognition shall be the difference between the net disposal proceed, and the the difference between the net disposal proceed, and the carrying amount of the asset and it shall be recognized carrying amount of the asset and it shall be recognized in the I/S. in the I/S.

2727