1 History of Accounting Standards. 2 JOIN KHALID AZIZ ECONOMICS OF ICMAP, ICAP, MA- ECONOMICS,...

63

1 History of History of Accounting Accounting Standards Standards

-

Upload

shona-long -

Category

Documents

-

view

221 -

download

0

Transcript of 1 History of Accounting Standards. 2 JOIN KHALID AZIZ ECONOMICS OF ICMAP, ICAP, MA- ECONOMICS,...

11

History of History of Accounting Accounting StandardsStandards

22

JOIN KHALID AZIZJOIN KHALID AZIZ

ECONOMICS OF ICMAP, ICAP, ECONOMICS OF ICMAP, ICAP, MA-ECONOMICS, B.COM.MA-ECONOMICS, B.COM.

FINANCIAL ACCOUNTING OF FINANCIAL ACCOUNTING OF ICMAP STAGE 1,3,4 ICAP ICMAP STAGE 1,3,4 ICAP MODULE B, B.COM, BBA, MODULE B, B.COM, BBA, MBA & PIPFA.MBA & PIPFA.

COST ACCOUNTING OF ICMAP COST ACCOUNTING OF ICMAP STAGE 2,3 ICAP MODULE D, STAGE 2,3 ICAP MODULE D, BBA, MBA & PIPFA.BBA, MBA & PIPFA.

CONTACT:CONTACT: 0322-33857520322-3385752 0312-23028700312-2302870 R-1173,ALNOOR SOCIETY, R-1173,ALNOOR SOCIETY,

BLOCK 19,F.B.AREA, BLOCK 19,F.B.AREA, KARACHI, PAKISTAN.KARACHI, PAKISTAN.

33

JOIN KHALID AZIZJOIN KHALID AZIZ

CRASH CLASSES CRASH CLASSES FOR COMPLETION FOR COMPLETION OF IMPORTANT OF IMPORTANT TOPICSTOPICS

ICMAP STAGE 1 & 2ICMAP STAGE 1 & 2FINANCIAL AND FINANCIAL AND

COST ACCOUNTINGCOST ACCOUNTING JOIN NOWJOIN NOW

44

JOIN KHALID AZIZJOIN KHALID AZIZ

FRESH CLASSES FOR ICAP FRESH CLASSES FOR ICAP MODULE B…FINANCIAL MODULE B…FINANCIAL ACCOUNTINGACCOUNTING

REGISTER YOUR SELF REGISTER YOUR SELF NOW.NOW.

COMPLETION OF SYLLABUS COMPLETION OF SYLLABUS WITH ACCENTUATE ON WITH ACCENTUATE ON BASIC CONCEPTS.BASIC CONCEPTS.

55

• Accounting has been called the language of business and accounting standards are grammar of this language. we must have a solid grounding in its fundamentals. Accounting information has been useful for hundreds of years. The double-entry framework was first described in a book written by Luca Pacioli, a fifteenth-century Italian monk and mathematician, although its origins can be traced back another 300 years. The formal structure for processing financial transactions is at least 700 years old.

• What is the definition of accounting? Accounting is the process of providing quantitative information about economic entities to aid users in making decisions concerning the allocation of economic resources.

• The term accounting theory is commonly used, but it has no unified, standardized definition. Very closely related to the realm of accounting theory is the area of measurement. Measurement is concerned with the process of assigning numbers to the attributes or characteristics of the elements being measured.

• In addition to accounting, accountancy has emerged as a profession, alongside the professions of medicine and law.

66

Who have Who have responsibility for responsibility for Accounting StandardsAccounting Standards

International Accounting International Accounting Standards Board (IASB)Standards Board (IASB)

Financial Accounting Standards Financial Accounting Standards Board (FSBB)Board (FSBB)

Accounting Standards Board Accounting Standards Board (ASB)(ASB)

Governmental Accounting Governmental Accounting Standards Board (GASB)Standards Board (GASB)

International Accounting International Accounting Standards Committee (IASC)Standards Committee (IASC)

International Financial International Financial Reporting Standards (IFRS)Reporting Standards (IFRS)

International Public Sector International Public Sector Accounting Standards (IPSAS)Accounting Standards (IPSAS)

77

Who issues standards?Who issues standards?

International Accounting Standards International Accounting Standards (IASs) were issued by the (IASs) were issued by the IASCIASC from from 1973 to 2000. The IASB replaced the 1973 to 2000. The IASB replaced the IASC in 2001. Since then, the IASB has IASC in 2001. Since then, the IASB has amended some IASs and has proposed amended some IASs and has proposed to amend others, has replaced some to amend others, has replaced some IASs with new International Financial IASs with new International Financial Reporting Standards (IFRSs), and has Reporting Standards (IFRSs), and has adopted or proposed certain new IFRSs adopted or proposed certain new IFRSs on topics for which there was no on topics for which there was no previous IAS. Through committees, both previous IAS. Through committees, both the IASC and the IASB also have issued the IASC and the IASB also have issued Interpretations of StandardsInterpretations of Standards. Financial . Financial statements may not be described as statements may not be described as complying with IFRSs unless they complying with IFRSs unless they comply with all of the requirements of comply with all of the requirements of each applicable standard and each each applicable standard and each applicable interpretation. applicable interpretation.

88

Accountancy Age Accountancy Age timeline: 1969 - 2004timeline: 1969 - 2004

1969: Accountancy Age is launched.1969: Accountancy Age is launched. DTI inquiry into Robert Maxwell's DTI inquiry into Robert Maxwell's

Pergamon Press causes its takeover Pergamon Press causes its takeover by LeaseCo to fall apart.by LeaseCo to fall apart.

Touche, Ross, Bailey & Smart becomes Touche, Ross, Bailey & Smart becomes Touche RossTouche Ross

1970: ICAEW's proposal to merge with 1970: ICAEW's proposal to merge with ICAS, ICAI and other bodies failsICAS, ICAI and other bodies fails

1973: Henry Benson appointed first 1973: Henry Benson appointed first chairman of the International chairman of the International Accounting Standards CommitteeAccounting Standards Committee

1974: The Consultative Committee of 1974: The Consultative Committee of Accountancy Bodies (CCAB) is formedAccountancy Bodies (CCAB) is formed

1977: IFAC is founded1977: IFAC is founded 1979: Ernst and Whinney is formed1979: Ernst and Whinney is formed 1980: ACCA's Vera di Palma becomes 1980: ACCA's Vera di Palma becomes

the first female president of an the first female president of an international accounting bodyinternational accounting body

1984: Merger of Deloitte, Haskins & 1984: Merger of Deloitte, Haskins & Sells and Price Waterhouse falls Sells and Price Waterhouse falls throughthrough

99

1987: Peat Marwick International and KMG 1987: Peat Marwick International and KMG merger forms KPMGmerger forms KPMG

1989: Arthur Andersen/Price Waterhouse 1989: Arthur Andersen/Price Waterhouse merger collapses in September.merger collapses in September.

Ernst & Young is formed from Ernst & Ernst & Young is formed from Ernst & Whinney and Arthur Young. Touche Ross Whinney and Arthur Young. Touche Ross and Deloitte Haskins Sells merge to form and Deloitte Haskins Sells merge to form Deloitte & ToucheDeloitte & Touche

1990: The 'Guinness Four' are found guilty 1990: The 'Guinness Four' are found guilty of fraudof fraud

1991: Robert Maxwell drowns. BCCI 1991: Robert Maxwell drowns. BCCI collapses. Polly Peck and Coloroll scandals collapses. Polly Peck and Coloroll scandals lead to Ian Cadbury's report on good lead to Ian Cadbury's report on good corporate governancecorporate governance

1995: Deloitte & Touche creates Deloitte 1995: Deloitte & Touche creates Deloitte Consulting. Barings collapsesConsulting. Barings collapses

1996: Ian and Kevin Maxwell cleared of 1996: Ian and Kevin Maxwell cleared of fraud, Coopers & Lybrand's audits of fraud, Coopers & Lybrand's audits of Maxwell companies face JDS investigation. Maxwell companies face JDS investigation. KPMG produces the first annual report by an KPMG produces the first annual report by an accountancy firm, which reveals senior accountancy firm, which reveals senior partner Colin Sharman earns a total partner Colin Sharman earns a total package of £740,000package of £740,000

1998: Coopers & Lybrand and Price 1998: Coopers & Lybrand and Price Waterhouse form PricewaterhouseCoopers.Waterhouse form PricewaterhouseCoopers.

JDS turns the spotlight on Arthur Andersen JDS turns the spotlight on Arthur Andersen in connection with the £50m overstatement in connection with the £50m overstatement of profits by Wickesof profits by Wickes

1010

2000: European Commission announces in 2000: European Commission announces in July that it intends to make IAS mandatory July that it intends to make IAS mandatory from 2005.from 2005.

The IASC completes its three-year The IASC completes its three-year restructuring programme and creates the restructuring programme and creates the International Accounting Standards Board, International Accounting Standards Board, effective from April 2001.effective from April 2001.

Ernst & Young sells consulting arm to Cap Ernst & Young sells consulting arm to Cap GeminiGemini

2001: SEC's Enron investigation begins. Big 2001: SEC's Enron investigation begins. Big Five issue a joint statement in December Five issue a joint statement in December insisting that self-regulation remains the insisting that self-regulation remains the best policy following the collapse of Enronbest policy following the collapse of Enron

2002: Andersen's Houston office admits to 2002: Andersen's Houston office admits to shredding documents relating to Enron. shredding documents relating to Enron. WorldCom is accused of $4bn fraud, which WorldCom is accused of $4bn fraud, which drags Andersen into another scandal. drags Andersen into another scandal. Andersen UK acquired by Deloitte. SEC Andersen UK acquired by Deloitte. SEC implements Sarbanes-Oxleyimplements Sarbanes-Oxley

2003: Grant Thornton is dragged into €4bn 2003: Grant Thornton is dragged into €4bn accounting 'black hole' at Parmalat.accounting 'black hole' at Parmalat.

Deloitte & Touche rebrands as simply Deloitte & Touche rebrands as simply 'Deloitte'. 'Deloitte'.

Higgs and Smith reports take an Higgs and Smith reports take an evolutionary step on from Cadbury and evolutionary step on from Cadbury and TurnbullTurnbull

2004: The Financial Reporting Council is 2004: The Financial Reporting Council is revamped. Inland Revenue merges with revamped. Inland Revenue merges with Customs & Excise.Customs & Excise.

1111

Who Sets Who Sets Accounting Accounting Standards in UK?Standards in UK?

Who Sets Accounting Standards in USA?Who Sets Accounting Standards in USA? The role of the Accounting Standards Board (ASB) is to The role of the Accounting Standards Board (ASB) is to

issue issue accounting standardsaccounting standards. It is recognized for that purpose . It is recognized for that purpose under the Companies Act 1985. It took over the task of setting under the Companies Act 1985. It took over the task of setting accounting standards from the Accounting Standards accounting standards from the Accounting Standards Committee (ASC) in 1990.Committee (ASC) in 1990.

The ASB also collaborates with accounting standard-The ASB also collaborates with accounting standard-setters from other countries and the International setters from other countries and the International Accounting Standards Board (IASB) both in order to Accounting Standards Board (IASB) both in order to influence the development of international standards influence the development of international standards and in order to ensure that its standards are developed and in order to ensure that its standards are developed with due regard to international developments.with due regard to international developments.

Accounting standards developed by the ASB are Accounting standards developed by the ASB are contained in 'Financial Reporting Standards' (FRSs). contained in 'Financial Reporting Standards' (FRSs). Soon after it started its activities, the ASB adopted the Soon after it started its activities, the ASB adopted the standards issued by the ASC, so that they also fall standards issued by the ASC, so that they also fall within the legal definition of accounting standards. within the legal definition of accounting standards. These are designated 'Statements of Standard These are designated 'Statements of Standard Accounting Practice' (SSAPs). Whilst some of the SSAPs Accounting Practice' (SSAPs). Whilst some of the SSAPs have been superseded by FRSs, some remain in force.have been superseded by FRSs, some remain in force.

Accounting standards apply to all companies, and other Accounting standards apply to all companies, and other kinds of entities that prepare accounts that are kinds of entities that prepare accounts that are intended to provide a true and fair view. The intended to provide a true and fair view. The Foreword to Accounting StandardsForeword to Accounting Standards explains the authority, explains the authority, scope and application of accounting standards.scope and application of accounting standards.

1212

The following institutes work together The following institutes work together to create new and amend older to create new and amend older standards in order to establish and standards in order to establish and maintain a common language for maintain a common language for communicating financial information: communicating financial information:

1-The Financial Accounting Standards 1-The Financial Accounting Standards Board (FASB), Board (FASB),

2-American Institute of Certified Public 2-American Institute of Certified Public Accountants (AICPA),Accountants (AICPA),

3-Securities and Exchange Commission 3-Securities and Exchange Commission (SEC), (SEC),

4-International Accounting Standards 4-International Accounting Standards Board (IASB) Board (IASB)

5-The passage of the Sarbanes-Oxley Act 5-The passage of the Sarbanes-Oxley Act and the creation of the Public and the creation of the Public Company Accounting Oversight Board Company Accounting Oversight Board (PCAOB) signals many significant (PCAOB) signals many significant forthcoming changes in GAAP and the forthcoming changes in GAAP and the current standards setting process. current standards setting process.

Who Sets Accounting Standards in USA?

1313

Who Sets Accounting Who Sets Accounting Standards in EU?Standards in EU?

At a joint meeting in September 2002, the International Accounting At a joint meeting in September 2002, the International Accounting Standards Board (IASB) and the Financial Accounting Standards Standards Board (IASB) and the Financial Accounting Standards Board (FASB) agreed to work together to develop high quality, fully Board (FASB) agreed to work together to develop high quality, fully compatible financial reporting standards that could be used for compatible financial reporting standards that could be used for domestic and cross-border reporting; this co-operative effort is domestic and cross-border reporting; this co-operative effort is sometimes described as international convergence of US GAAP and sometimes described as international convergence of US GAAP and IFRS financial reporting standards. The IASB-FASB convergence IFRS financial reporting standards. The IASB-FASB convergence effort involves two kinds of projects. The first type includes short-effort involves two kinds of projects. The first type includes short-term projects that are intended to remove many of the numerous term projects that are intended to remove many of the numerous individual differences between International Financial Reporting individual differences between International Financial Reporting Standards (IFRS, which include International Accounting Standards Standards (IFRS, which include International Accounting Standards (IAS) issued by the predecessor body to the IASB) and US GAAP. (IAS) issued by the predecessor body to the IASB) and US GAAP. Examples of current and proposed short-term convergence efforts Examples of current and proposed short-term convergence efforts involve the accounting treatments of no monetary exchanges, involve the accounting treatments of no monetary exchanges, discontinued operations, income taxes and interim reporting. The discontinued operations, income taxes and interim reporting. The second type of convergence project involves longer term joint IASB-second type of convergence project involves longer term joint IASB-FASB projects and coordinated projects that are intended to FASB projects and coordinated projects that are intended to provide major pieces of improved accounting guidance. Examples of provide major pieces of improved accounting guidance. Examples of the latter include the joint projects on revenue recognition and the latter include the joint projects on revenue recognition and purchase method procedures and the coordinated project on share-purchase method procedures and the coordinated project on share-based payments. The goal of the IASB-FASB convergence efforts is based payments. The goal of the IASB-FASB convergence efforts is to make US GAAP and IFRS financial reporting standards as nearly to make US GAAP and IFRS financial reporting standards as nearly as possible the same across jurisdictions while also improving the as possible the same across jurisdictions while also improving the overall quality of those standards.overall quality of those standards.

The convergence activities of the IASB and the FASB will of The convergence activities of the IASB and the FASB will of necessity be directly and indirectly affected by regulatory changes necessity be directly and indirectly affected by regulatory changes and shifts in economic conditions throughout the world. The and shifts in economic conditions throughout the world. The purpose of this paper is to identify some possible implications for purpose of this paper is to identify some possible implications for international convergence of a particularly significant regulatory international convergence of a particularly significant regulatory change, namely, the mandated adoption of IFRS by listed change, namely, the mandated adoption of IFRS by listed enterprises in the European Union beginning in 2005. This change enterprises in the European Union beginning in 2005. This change will increase the number of enterprises that apply IFRS to prepare will increase the number of enterprises that apply IFRS to prepare their consolidated reports from several hundred to several their consolidated reports from several hundred to several thousand, and will require the use of IFRS by enterprises that vary thousand, and will require the use of IFRS by enterprises that vary considerably in size, ownership structure, capital structure, political considerably in size, ownership structure, capital structure, political jurisdiction and financial reporting sophistication. The purpose of jurisdiction and financial reporting sophistication. The purpose of this discussion paper is to explore several implications of this major this discussion paper is to explore several implications of this major shift in financial reporting requirements for the overall shift in financial reporting requirements for the overall international convergence of financial reporting standards and international convergence of financial reporting standards and practices. practices.

1414

IASB IASB FrameworkFramework

While not a standard, the IASB While not a standard, the IASB Framework for the Preparation and Framework for the Preparation and Presentation of Financial Statements Presentation of Financial Statements serves as a guide to resolving serves as a guide to resolving accounting issues that are not accounting issues that are not addressed directly in a standard. addressed directly in a standard. Moreover, in the absence of a standard Moreover, in the absence of a standard or an interpretation that specifically or an interpretation that specifically applies to a transaction, IAS 8 requires applies to a transaction, IAS 8 requires that an entity must use its judgment in that an entity must use its judgment in developing and applying an accounting developing and applying an accounting policy that results in information that is policy that results in information that is relevant and reliable. In making that relevant and reliable. In making that judgment, IAS 8.11 requires judgment, IAS 8.11 requires management to consider the definitions, management to consider the definitions, recognition criteria and measurement recognition criteria and measurement concepts for assets, liabilities, income, concepts for assets, liabilities, income, and expenses in the Framework. The and expenses in the Framework. The IASB adopted the Framework in April IASB adopted the Framework in April 2001. It had originally been adopted by 2001. It had originally been adopted by the IASC in 1989. Currently, the IASB is the IASC in 1989. Currently, the IASB is working on a Project to Revise the working on a Project to Revise the Framework.Framework.

1515

What is IFRSs’What is IFRSs’

The term International Financial The term International Financial Reporting Standards (IFRSs) has both a Reporting Standards (IFRSs) has both a narrow and a broad meaning. Narrowly, narrow and a broad meaning. Narrowly, IFRSs refers to the new numbered IFRSs refers to the new numbered series of pronouncements that the IASB series of pronouncements that the IASB is issuing, as distinct from the is issuing, as distinct from the International Accounting Standards International Accounting Standards (IASs) series issued by its predecessor. (IASs) series issued by its predecessor. More broadly, IFRSs refers to the entire More broadly, IFRSs refers to the entire body of IASB pronouncements, body of IASB pronouncements, including standards and interpretations including standards and interpretations approved by the IASB and IASs and SIC approved by the IASB and IASs and SIC interpretations approved by the interpretations approved by the predecessor International Accounting predecessor International Accounting Standards Committee. [On this website, Standards Committee. [On this website, consistent with IASB policy, we consistent with IASB policy, we abbreviate International Financial abbreviate International Financial Reporting Standards (plural) as IFRSs Reporting Standards (plural) as IFRSs and International Accounting Standards and International Accounting Standards (plural) as IASs.] (plural) as IASs.]

1616

IFRSIFRS

International Financial Reporting International Financial Reporting StandardsStandards Preface Preface to International Financial to International Financial Reporting Standards Reporting Standards

IFRS 1IFRS 1 First-time Adoption of International First-time Adoption of International Financial Reporting Standards Financial Reporting Standards

IFRS 2IFRS 2 Share-based Payment Share-based Payment IFRS 3IFRS 3 Business Combinations Business Combinations IFRS 4IFRS 4 Insurance Contracts Insurance Contracts IFRS 5IFRS 5 Non-current Assets Held for Sale and Non-current Assets Held for Sale and

Discontinued Operations Discontinued Operations IFRS 6IFRS 6 Exploration for and Evaluation of Mineral Exploration for and Evaluation of Mineral

Assets Assets IFRS 7IFRS 7 Financial Instruments: Disclosures Financial Instruments: Disclosures IFRS 8IFRS 8 Operating Segments Framework for the Operating Segments Framework for the

Preparation and Presentation of Financial Preparation and Presentation of Financial StatementsStatements

FrameworkFramework for the Preparation and Presentation for the Preparation and Presentation of Financial Statements of Financial Statements

1717

Which are Which are international international accounting accounting standards(IAS)?standards(IAS)?

IAS 1IAS 1 Presentation of Financial Statements Presentation of Financial Statements IAS 2IAS 2 Inventories IAS 3 Consolidated Financial Inventories IAS 3 Consolidated Financial

Statements Statements Originally issued 1976, effective 1 Jan 1977. Originally issued 1976, effective 1 Jan 1977. Superseded in 1989 by Superseded in 1989 by IAS 27IAS 27 and and IAS 28IAS 28..

IAS 4 Depreciation Accounting IAS 4 Depreciation Accounting Withdrawn in 1999, replaced by IAS 16, 22, and Withdrawn in 1999, replaced by IAS 16, 22, and 38, all of which were issued or revised in 1998. 38, all of which were issued or revised in 1998. IAS 5 Information to Be Disclosed in Financial IAS 5 Information to Be Disclosed in Financial Statements Statements Originally issued October 1976, effective 1 Originally issued October 1976, effective 1 January 1997. Superseded by January 1997. Superseded by IAS 1IAS 1 in 1997. IAS 6 in 1997. IAS 6 Accounting Responses to Changing PricesAccounting Responses to Changing PricesSuperseded by Superseded by IAS 15IAS 15, which was withdrawn , which was withdrawn December 2003December 2003 IAS 7 IAS 7 Cash Flow Statements Cash Flow Statements IAS 8 IAS 8 Accounting Policies, Changes in Accounting Estimates Accounting Policies, Changes in Accounting Estimates and Errors IAS 9 Accounting for Research and and Errors IAS 9 Accounting for Research and Development Activities Superseded by Development Activities Superseded by IAS 38IAS 38 effective effective 1.7.991.7.99 IAS 10 IAS 10 Events After the Balance Sheet Date Events After the Balance Sheet Date IAS 11 IAS 11 Construction Contracts Construction Contracts IAS 12 IAS 12 Income Taxes Income Taxes IAS 13 Presentation of Current Assets and Current IAS 13 Presentation of Current Assets and Current Liabilities Liabilities Superseded by Superseded by IAS 1IAS 1.. IAS 14 IAS 14 Segment Reporting. Segment Reporting.

1818

Segment Reporting Segment Reporting IAS 15IAS 15 Information Reflecting the Effects of Information Reflecting the Effects of

Changing Prices Changing Prices Withdrawn December 2003Withdrawn December 2003

IAS 16IAS 16 Property, Plant and Equipment Property, Plant and Equipment IAS 17IAS 17 Leases Leases IAS 18IAS 18 Revenue Revenue IAS 19IAS 19 Employee Benefits Employee Benefits IAS 20IAS 20 Accounting for Government Grants Accounting for Government Grants

and Disclosure of Government Assistance and Disclosure of Government Assistance IAS 21IAS 21 The Effects of Changes in Foreign The Effects of Changes in Foreign

Exchange Rates Exchange Rates IAS 22IAS 22 Business Combinations Business Combinations

Superseded by Superseded by IFRS 3IFRS 3 effective 31 March effective 31 March 2004.2004.

IAS 23IAS 23 Borrowing Costs Borrowing Costs IAS 24IAS 24 Related Party Disclosures Related Party Disclosures

1919

IAS 25IAS 25 Accounting for Investments Accounting for Investments Superseded by Superseded by IAS 39IAS 39 and and IAS 40IAS 40 effective 2001. effective 2001.

IAS 26IAS 26 Accounting and Reporting by Retirement Accounting and Reporting by Retirement Benefit Plans Benefit Plans

IAS 27IAS 27 Consolidated and Separate Financial Consolidated and Separate Financial Statements Statements IAS 28 IAS 28 Investments in Associates Investments in Associates

IAS 29IAS 29 Financial Reporting in Hyperinflationary Financial Reporting in Hyperinflationary Economies Economies

IAS 30IAS 30 Disclosures in the Financial Statements of Disclosures in the Financial Statements of Banks and Similar Financial Institutions Banks and Similar Financial Institutions Superseded by Superseded by IFRS 7IFRS 7 effective 2007. effective 2007.

IAS 31IAS 31 Interests In Joint Ventures Interests In Joint Ventures IAS 32IAS 32 Financial Instruments: Presentation Financial Instruments: Presentation

Disclosure provisions superseded by Disclosure provisions superseded by IFRS 7IFRS 7 effective 2007.effective 2007.

IAS 33IAS 33 Earnings Per Share Earnings Per Share IAS 34IAS 34 Interim Financial Reporting Interim Financial Reporting IAS 35IAS 35 Discontinuing Operations Discontinuing Operations

Superseded by Superseded by IFRS 5IFRS 5 effective 2005. effective 2005. IAS 36IAS 36 Impairment of Assets Impairment of Assets IAS 37IAS 37 Provisions, Contingent Liabilities and Provisions, Contingent Liabilities and

Contingent Assets Contingent Assets IAS 38IAS 38 Intangible Assets Intangible Assets IAS 39IAS 39 Financial Instruments: Recognition and Financial Instruments: Recognition and

Measurement Measurement IAS 40IAS 40 Investment Property Investment Property IAS 41IAS 41 Agriculture Agriculture

2020

FASFASBB

Since 1973 the FASB has been Since 1973 the FASB has been the organization designated to the organization designated to establish authoritative financial establish authoritative financial accounting and reporting accounting and reporting standards (Statements of standards (Statements of Financial Accounting Standards, Financial Accounting Standards, SFAS) for business and other SFAS) for business and other private-sector entities. Its private-sector entities. Its mission is to be responsive to mission is to be responsive to the entire economic community the entire economic community and to operate in full view of and to operate in full view of the entire community through a the entire community through a due-process system.due-process system.

2121

SECSEC

Under the Securities and Exchange Act of Under the Securities and Exchange Act of 1934, the SEC has statutory authority to 1934, the SEC has statutory authority to establish financial accounting and reporting establish financial accounting and reporting standards for publicly-held companies. standards for publicly-held companies. Recent accounting-related scandals, such as Recent accounting-related scandals, such as Enron, prompted the SEC and Congress to get Enron, prompted the SEC and Congress to get more directly involved in the oversight of the more directly involved in the oversight of the standards setting process and the monitoring standards setting process and the monitoring of corporate governance. In August 2002, as of corporate governance. In August 2002, as part of the Sarbanes-Oxley Act, the SEC's part of the Sarbanes-Oxley Act, the SEC's Public Company Accounting Oversight Board Public Company Accounting Oversight Board (PCAOB) was created to crack down on (PCAOB) was created to crack down on corporate accounting scandals. Authorized to corporate accounting scandals. Authorized to conduct inspections and discipline conduct inspections and discipline accountants, the oversight board supplants accountants, the oversight board supplants the self-regulation of CPAs who audit public the self-regulation of CPAs who audit public companies.companies.

2222

IASBIASB

Formed in January 2001, the ISAB replaced Formed in January 2001, the ISAB replaced its predecessor, the International its predecessor, the International Accounting Standards Committee (IASC), Accounting Standards Committee (IASC), as the international standards setting as the international standards setting body. Looking towards greater body. Looking towards greater formalization of international accounting formalization of international accounting standards, IASB is structured similarly to standards, IASB is structured similarly to the FASB. It is currently the focus of the the FASB. It is currently the focus of the IASB, in collaboration with the FASB and IASB, in collaboration with the FASB and other accounting focused organizations, to other accounting focused organizations, to "converge" standards and develop a single, "converge" standards and develop a single, universally accepted set of biding universally accepted set of biding international accounting standards. The international accounting standards. The IASC, and now IASB, issue a series of IASC, and now IASB, issue a series of standards known as International Financial standards known as International Financial Reporting Standards (IFRS), formerly Reporting Standards (IFRS), formerly called International Accounting Standards called International Accounting Standards (IAS).(IAS).

2323

IASB, IASCF, and IASC IASB, IASCF, and IASC DefinedDefined

The The International Accounting Standards BoardInternational Accounting Standards Board is an is an independent, private-sector body that develops and independent, private-sector body that develops and approves International Financial Reporting approves International Financial Reporting Standards. The IASB operates under the oversight Standards. The IASB operates under the oversight of the International Accounting Standards of the International Accounting Standards Committee Foundation. The IASB was formed in Committee Foundation. The IASB was formed in 2001 to replace the International Accounting 2001 to replace the International Accounting Standards Committee. Standards Committee. IASCF: International Accounting Standards IASCF: International Accounting Standards Committee Foundation Committee Foundation The The International Accounting Standards Committee FouInternational Accounting Standards Committee Foundationndation is the independent, non-profit foundation, created is the independent, non-profit foundation, created in 2000 to oversee the IASB. Click for more in 2000 to oversee the IASB. Click for more information about the information about the IASCF StructureIASCF Structure. . IASC: International Accounting Standards IASC: International Accounting Standards Committee Committee From 1973 until a comprehensive From 1973 until a comprehensive reorganization in 2000, the structure for reorganization in 2000, the structure for setting International Accounting Standards setting International Accounting Standards was known as the International Accounting was known as the International Accounting Standards Committee. There was no actual Standards Committee. There was no actual "committee" of that name. The standard-"committee" of that name. The standard-setting board was known as the IASC Board. setting board was known as the IASC Board.

2424

What is IFAC?What is IFAC?

The The International Federation of AccountantsInternational Federation of Accountants (IFAC) is an association of national professional (IFAC) is an association of national professional accountancy organizations that represent accountancy organizations that represent accountants employed in public practice, accountants employed in public practice, business and industry, the public sector, and business and industry, the public sector, and education, as well as some specialized groups education, as well as some specialized groups that interface frequently with the profession. that interface frequently with the profession. IFAC works to develop the profession globally IFAC works to develop the profession globally and to harmonies professional standards and to harmonies professional standards worldwide to enable accountants to provide worldwide to enable accountants to provide services of consistently high quality in the public services of consistently high quality in the public interest across political borders. Currently, IFAC interest across political borders. Currently, IFAC has 155 member bodies and associates in 118 has 155 member bodies and associates in 118 countries, representing over 2.5 million countries, representing over 2.5 million accountants.accountants.

2525

International International Accounting Education Accounting Education Standards Board Standards Board

The International Accounting Education The International Accounting Education Standards Board (IAESB) – formerly the Standards Board (IAESB) – formerly the IFAC Education Committee – develops IFAC Education Committee – develops guidance to improve the standards of guidance to improve the standards of accountancy education around the world accountancy education around the world and focuses on two key areas: and focuses on two key areas:

The essential elements of accreditation, The essential elements of accreditation, which are education, practical experience which are education, practical experience and tests of professional competence; and and tests of professional competence; and

The nature and extent of continuing The nature and extent of continuing professional education needed by professional education needed by accountants. accountants.

2626

International Auditing International Auditing and Assurance and Assurance Standards BoardStandards Board

International Standards on Auditing (ISAs) International Standards on Auditing (ISAs) are set by the International Auditing and are set by the International Auditing and Assurance Standards Board (IAASB) -- until Assurance Standards Board (IAASB) -- until 2002 known as the International Auditing 2002 known as the International Auditing Practices Committee (IAPC). The ISA on the Practices Committee (IAPC). The ISA on the auditor's report on financial statements auditor's report on financial statements requires that the auditor's opinion must requires that the auditor's opinion must clearly indicate the financial reporting clearly indicate the financial reporting framework used to prepare the financial framework used to prepare the financial statements (including the country of origin of statements (including the country of origin of the financial reporting framework when the the financial reporting framework when the framework used is not International framework used is not International Accounting Standards) and state the Accounting Standards) and state the auditor's opinion as to whether the financial auditor's opinion as to whether the financial statements give a true and fair view (or are statements give a true and fair view (or are presented fairly, in all material respects) in presented fairly, in all material respects) in accordance with that financial reporting accordance with that financial reporting framework and, where appropriate, whether framework and, where appropriate, whether the financial statements comply with the financial statements comply with statutory requirements.statutory requirements.

2727

Originally, the AICPA, the memberships association Originally, the AICPA, the memberships association for CPAs, was the body responsible for defining for CPAs, was the body responsible for defining accounting standards.accounting standards.

1939-1959 - issues Accounting Research Bulletins 1939-1959 - issues Accounting Research Bulletins (ARB) (ARB)

1959-1973 - Accounting Principles Board (APB) issues 1959-1973 - Accounting Principles Board (APB) issues series of opinions series of opinions

1973 - Accounting Principles Board dissolved and 1973 - Accounting Principles Board dissolved and standards setting responsibility is transferred to standards setting responsibility is transferred to FASB. The AICPA continues its role as authoritative FASB. The AICPA continues its role as authoritative body for establishing auditing standards (Statement body for establishing auditing standards (Statement of Auditing Standards, SAS) of Auditing Standards, SAS)

In 1973, the AICPA shifted its focus to supporting it In 1973, the AICPA shifted its focus to supporting it membership and constituency and bringing to the membership and constituency and bringing to the attention of the FASB and SEC issues that it attention of the FASB and SEC issues that it determined important to the accounting and auditing determined important to the accounting and auditing professional communities. While the AICPA continued professional communities. While the AICPA continued issuing auditing standards, this responsibility is now issuing auditing standards, this responsibility is now being assumed by the Public Company Accounting being assumed by the Public Company Accounting Oversight Board (PCAOB), a body created by the Oversight Board (PCAOB), a body created by the Sarbanes-Oxley Act of 2002. The Oversight Board's Sarbanes-Oxley Act of 2002. The Oversight Board's recent authorization to become directly involved with recent authorization to become directly involved with issues auditing standards could have significant issues auditing standards could have significant impact on the current standards setting process.impact on the current standards setting process.

AICPA has given a thumbs – up to a Securities and AICPA has given a thumbs – up to a Securities and Exchange Commission plan that would allow U.S. Exchange Commission plan that would allow U.S. corporations to abandon generally accepted corporations to abandon generally accepted accounting principles and report their financial accounting principles and report their financial results using international accounting standards.results using international accounting standards.This concept release was issued on the heels of a This concept release was issued on the heels of a separate SEC proposal that would permit foreign separate SEC proposal that would permit foreign companies filing with the SEC to use IFRS without companies filing with the SEC to use IFRS without reconciling to U.S GAAP.reconciling to U.S GAAP.

2828

Accounting Accounting The House of The House of GAAPGAAP The role that accounting standards play in establishing The role that accounting standards play in establishing

the rules for disclosing both public and private financial the rules for disclosing both public and private financial reporting assumes levels of authority of "more to less" reporting assumes levels of authority of "more to less" which guide reliance on and determines the weight of which guide reliance on and determines the weight of the standards. Understanding this hierarchy is the standards. Understanding this hierarchy is paramount to grasping the meaning of "generally paramount to grasping the meaning of "generally accepted accounting principles" (GAAP), and the many accepted accounting principles" (GAAP), and the many supporting documents. supporting documents.

The concept of the "house of GAAP" was introduced in a The concept of the "house of GAAP" was introduced in a 1984 article from the Journal of Accountancy. The 1984 article from the Journal of Accountancy. The author describes and defines the vast universe of author describes and defines the vast universe of accounting standards as a hierarchy structured along accounting standards as a hierarchy structured along the lines of the floor plan of a house. "Like any other the lines of the floor plan of a house. "Like any other structure, the house of GAAP rests on a foundation, in structure, the house of GAAP rests on a foundation, in this case a foundation of the basic concepts and broad this case a foundation of the basic concepts and broad principles that underlie financial reporting, without principles that underlie financial reporting, without which, like a house of cards, the house of GAAP would which, like a house of cards, the house of GAAP would tumble."tumble."

In 199I the AICPA's Auditing Standards Board In 199I the AICPA's Auditing Standards Board remodeled the house of GAAP by changing some of the remodeled the house of GAAP by changing some of the levels of authority of certain accounting levels of authority of certain accounting pronouncements and distinguishing between the pronouncements and distinguishing between the standards defining state and local government entities, standards defining state and local government entities, established by the Government Accounting Standards established by the Government Accounting Standards Board (GASB) and those for all others, falling under the Board (GASB) and those for all others, falling under the FASB's jurisdiction. FASB's jurisdiction.

2929

PCAOB (USA)PCAOB (USA)

Formed in 2002 to oversee the audit of Formed in 2002 to oversee the audit of public companies that are subject to the public companies that are subject to the securities laws in the preparation of securities laws in the preparation of informative, fair and independent audit informative, fair and independent audit reports. The Board's authority includes: reports. The Board's authority includes:

..Registering public accounting firms that ..Registering public accounting firms that prepare audit reports for issuers prepare audit reports for issuers ..Conducting inspections of registered public ..Conducting inspections of registered public accounting firms accounting firms ..Conducting investigations and disciplinary ..Conducting investigations and disciplinary proceedings and impose appropriate proceedings and impose appropriate sanctions sanctions ..Enforcing compliance by registered public ..Enforcing compliance by registered public accounting firms relating to the preparation accounting firms relating to the preparation and issuance of audit reports and the and issuance of audit reports and the obligations and liabilities of accountants obligations and liabilities of accountants ..Establishing auditing, quality control, ..Establishing auditing, quality control, ethics, independence, and other standards ethics, independence, and other standards relating to the preparation of audit reports relating to the preparation of audit reports for issuersfor issuers

3030

POB (UK)POB (UK)

The Professional Oversight Board The Professional Oversight Board contributes to the achievement of the contributes to the achievement of the Financial Reporting Council's own Financial Reporting Council's own fundamental aim of supporting investor, fundamental aim of supporting investor, market and public confidence in the financial market and public confidence in the financial and governance stewardship of listed and and governance stewardship of listed and other entities by providing:other entities by providing:

Independent oversight of the regulation of Independent oversight of the regulation of the auditing profession by the recognized the auditing profession by the recognized supervisory and qualifying bodies supervisory and qualifying bodies

Monitoring of the quality of the auditing Monitoring of the quality of the auditing function in relation to economically function in relation to economically significant entities significant entities

Independent oversight of the regulation of Independent oversight of the regulation of the accountancy profession by the the accountancy profession by the professional accountancy bodies professional accountancy bodies

Independent oversight of the regulation of Independent oversight of the regulation of the actuarial profession by the professional the actuarial profession by the professional actuarial bodies and promoting high quality actuarial bodies and promoting high quality actuarial work. actuarial work.

The Professional Oversight Board for The Professional Oversight Board for Accountancy has changed its name as of 5 Accountancy has changed its name as of 5 May 2006 to the Professional Oversight May 2006 to the Professional Oversight Board. This reflects the extension of its Board. This reflects the extension of its board's remit to include oversight of the board's remit to include oversight of the regulation of the actuarial profession.regulation of the actuarial profession.

3131

AADB (UK)AADB (UK) The Accountancy & Actuarial Discipline Board ("AADB") The Accountancy & Actuarial Discipline Board ("AADB")

is the independent, investigative and disciplinary body is the independent, investigative and disciplinary body for accountants and actuaries in the UK. It has up to for accountants and actuaries in the UK. It has up to eleven memberseleven members..

The AADB is responsible for operating and administering The AADB is responsible for operating and administering an independent disciplinary scheme (the Accountancy an independent disciplinary scheme (the Accountancy Scheme) covering members of the following Scheme) covering members of the following accountants' professional bodies:- the Association of accountants' professional bodies:- the Association of Chartered Certified Accountants, the Chartered Institute Chartered Certified Accountants, the Chartered Institute of Management Accountants, the Chartered Institute of of Management Accountants, the Chartered Institute of Public Finance and Accountancy and the Institute of Public Finance and Accountancy and the Institute of Chartered Accountants in England and Wales; The Chartered Accountants in England and Wales; The Institute of Chartered Accountants of Ireland and the Institute of Chartered Accountants of Ireland and the Institute of Chartered Accountants of Scotland.Institute of Chartered Accountants of Scotland.

The AADB will operate & administer a separate The AADB will operate & administer a separate independent disciplinary scheme (the Actuarial Scheme) independent disciplinary scheme (the Actuarial Scheme) covering members of the Faculty & Institute of covering members of the Faculty & Institute of Actuaries, which will be adopted as soon as necessary Actuaries, which will be adopted as soon as necessary formalities have been completed.formalities have been completed.

The focus of the AADB is on cases of public interest; The focus of the AADB is on cases of public interest; other cases will continue to be dealt with by the other cases will continue to be dealt with by the individual accountancy body of the member concerned individual accountancy body of the member concerned or by the Faculty & Institute of Actuaries. The normal or by the Faculty & Institute of Actuaries. The normal channel of reference to the AADB for 'public interest' channel of reference to the AADB for 'public interest' cases will be the accountancy or actuarial body primarily cases will be the accountancy or actuarial body primarily concerned. However, the AADB also has the power to concerned. However, the AADB also has the power to call in cases whether or not they have been referred to call in cases whether or not they have been referred to it by an accountancy body. The AADB will also have the it by an accountancy body. The AADB will also have the power to call in actuarial cases. power to call in actuarial cases.

The AADB was formerly known as the Accountancy The AADB was formerly known as the Accountancy Investigation & Discipline Board (AIDB). It changed its Investigation & Discipline Board (AIDB). It changed its name to the AADB on 16/08/2007.name to the AADB on 16/08/2007.

3232

GAASGAAS

Generally Accepted Auditing Standards Generally Accepted Auditing Standards (GAAS). Established by the AICPA, these (GAAS). Established by the AICPA, these standards govern the conduct of external standards govern the conduct of external audits by public accountants. The Statement audits by public accountants. The Statement of Auditing Standards (SAS) provide of Auditing Standards (SAS) provide guidelines for the auditors' field work and guidelines for the auditors' field work and financial reporting. They frame the format financial reporting. They frame the format and contents of the Auditor's Report or and contents of the Auditor's Report or Opinion, which is the formal expression of Opinion, which is the formal expression of their examination of a company's financial their examination of a company's financial statements. In May 2003, the PCAOB was statements. In May 2003, the PCAOB was given the official go-ahead to assume given the official go-ahead to assume responsibility for establishing GAAS. It responsibility for establishing GAAS. It remains to be seen exactly how the PCAOB's remains to be seen exactly how the PCAOB's new role will play out, its impact on the new role will play out, its impact on the AICPA's responsibilities, and the form in AICPA's responsibilities, and the form in which the two entities will co-exist.which the two entities will co-exist.

3333

GASGAS

Governmental Accounting Standards Governmental Accounting Standards (GAS). While GAAP defines the accounting (GAS). While GAAP defines the accounting for public and private business entities, for public and private business entities, there also exist standards specific to there also exist standards specific to governmental organizations. Organized in governmental organizations. Organized in 1984 to establish standards of financial 1984 to establish standards of financial accounting and reporting for state and accounting and reporting for state and local governmental entities, the local governmental entities, the Governmental Accounting Standards Board Governmental Accounting Standards Board (GASB), began issues these standards to (GASB), began issues these standards to guide the preparation of external reports guide the preparation of external reports for these types of organizations. for these types of organizations.

3434

Sarbanes-Oxley Sarbanes-Oxley Act of 2002Act of 2002

The S&O Act was passed as a direct result of The S&O Act was passed as a direct result of a series of major corporate financial a series of major corporate financial accounting scandals. This legislation directly accounting scandals. This legislation directly impacts accountants and attorneys, officers impacts accountants and attorneys, officers and owners of publicly traded companies, as and owners of publicly traded companies, as well as brokers, dealers, investment bankers, well as brokers, dealers, investment bankers, and financial analysts. The Act, PL 107-204, and financial analysts. The Act, PL 107-204, established the Public Company Accounting established the Public Company Accounting Oversight Board (PCAOB), responsible for Oversight Board (PCAOB), responsible for registering, monitoring, investigating, and registering, monitoring, investigating, and disciplining the activities of public accounting disciplining the activities of public accounting firms, including establishing the guidelines firms, including establishing the guidelines for the conduct of several key auditing for the conduct of several key auditing procedures no delineating the types of procedures no delineating the types of services that CPAs are prohibited from services that CPAs are prohibited from providing to audit clients. The Act providing to audit clients. The Act additionally sets forth a number of additionally sets forth a number of requirements for corporations, their officers requirements for corporations, their officers and Board members, by redefining working and Board members, by redefining working and reporting relationships with their internal and reporting relationships with their internal audit committee members and public audit committee members and public accounting firms, creating changes in internal accounting firms, creating changes in internal controls procedures and enhancing financial controls procedures and enhancing financial disclosures.disclosures.

3535

What is Corporate What is Corporate Governance?Governance?

Good corporate governance is essential to the effective Good corporate governance is essential to the effective operation of a free market, which enables wealth operation of a free market, which enables wealth creation and freedom from poverty. creation and freedom from poverty. The main point of The main point of Corporate governance same Sarbox ,EU & UK Corporate governance same Sarbox ,EU & UK regulation requires CEOs and CFOs to sign off on their regulation requires CEOs and CFOs to sign off on their companies' internal controlscompanies' internal controls

A framework which should ensure that timely and A framework which should ensure that timely and accurate disclosure is made on all matters regarding accurate disclosure is made on all matters regarding the corporation, including the financial, performance, the corporation, including the financial, performance, ownership, and governance of the company. It relies on ownership, and governance of the company. It relies on mechanisms and rules which ensure the protection of mechanisms and rules which ensure the protection of all interest groups and help to build and consolidate all interest groups and help to build and consolidate the reputation and the market value of the company. the reputation and the market value of the company.

The mechanisms of corporate governance apply to The mechanisms of corporate governance apply to every level of authority in the corporation - Board of every level of authority in the corporation - Board of Directors, Audit Committee, Compensation Committees Directors, Audit Committee, Compensation Committees and others. The Board of Directors must have strong and others. The Board of Directors must have strong independent representation. The Audit Committee independent representation. The Audit Committee provides the main point of communication between the provides the main point of communication between the external auditors and the shareholders. external auditors and the shareholders.

Auditors also play a primary role in corporate Auditors also play a primary role in corporate governance. An important aspect of their work involves governance. An important aspect of their work involves independence from any pressure, from either independence from any pressure, from either management or shareholders. The terms of management or shareholders. The terms of engagement of their work, and constant contact with engagement of their work, and constant contact with both operating management, boards of directors and both operating management, boards of directors and related committees will guarantee the independence related committees will guarantee the independence and reliability of financial statementsand reliability of financial statements

3636

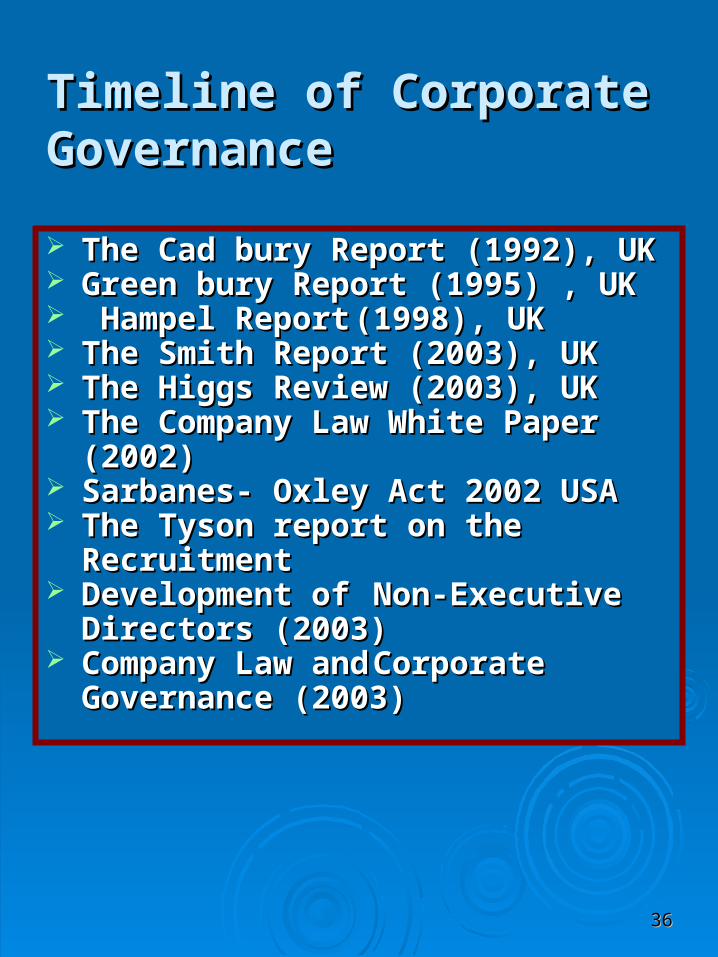

Timeline of Corporate Timeline of Corporate GovernanceGovernance

The Cad bury Report (1992), UK The Cad bury Report (1992), UK Green bury Report (1995) , UKGreen bury Report (1995) , UK Hampel ReportHampel Report (1998), UK(1998), UK The Smith Report (2003), UKThe Smith Report (2003), UK The Higgs Review (2003), UKThe Higgs Review (2003), UK The Company Law White Paper The Company Law White Paper

(2002)(2002) Sarbanes- Oxley Act 2002 USASarbanes- Oxley Act 2002 USA The Tyson report on the The Tyson report on the

Recruitment Recruitment Development of Development of Non-ExecutiveNon-Executive

Directors (2003)Directors (2003) Company Law andCompany Law and CorporateCorporate

Governance (2003)Governance (2003)

3737

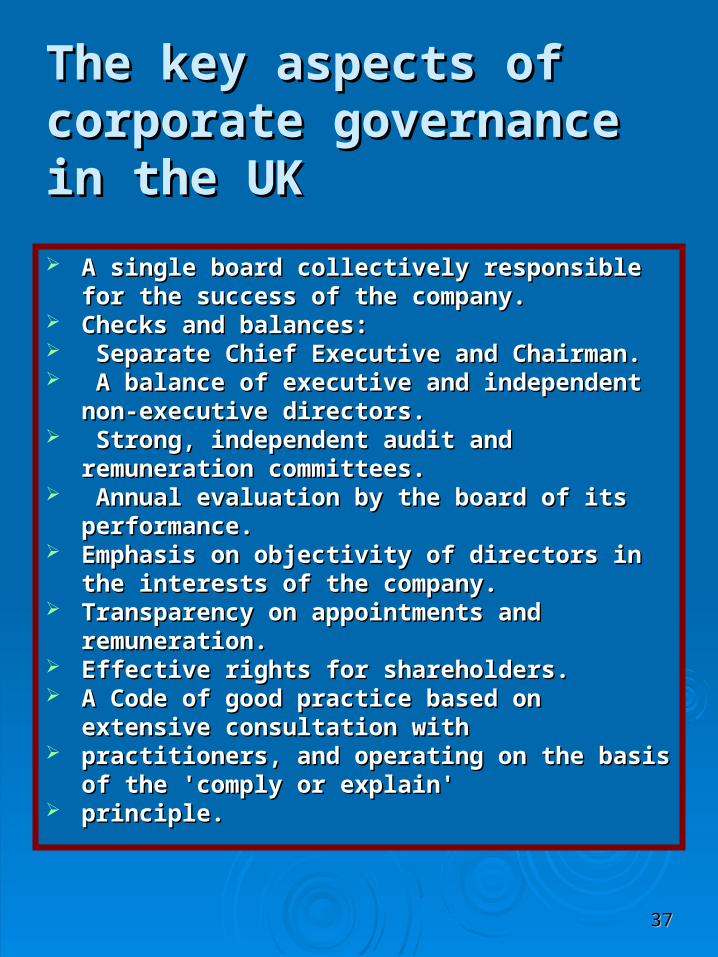

The key aspects of The key aspects of corporate governance corporate governance in the UKin the UK

A single board collectively responsible for A single board collectively responsible for the success of the company.the success of the company.

Checks and balances:Checks and balances: Separate Chief Executive and Chairman.Separate Chief Executive and Chairman. A balance of executive and independent A balance of executive and independent

non-executive directors.non-executive directors. Strong, independent audit and Strong, independent audit and

remuneration committees.remuneration committees. Annual evaluation by the board of its Annual evaluation by the board of its

performance.performance. Emphasis on objectivity of directors in the Emphasis on objectivity of directors in the

interests of the company.interests of the company. Transparency on appointments and Transparency on appointments and

remuneration.remuneration. Effective rights for shareholders.Effective rights for shareholders. A Code of good practice based on A Code of good practice based on

extensive consultation withextensive consultation with practitioners, and operating on the basis of practitioners, and operating on the basis of

the 'comply or explain'the 'comply or explain' principle.principle.

3838

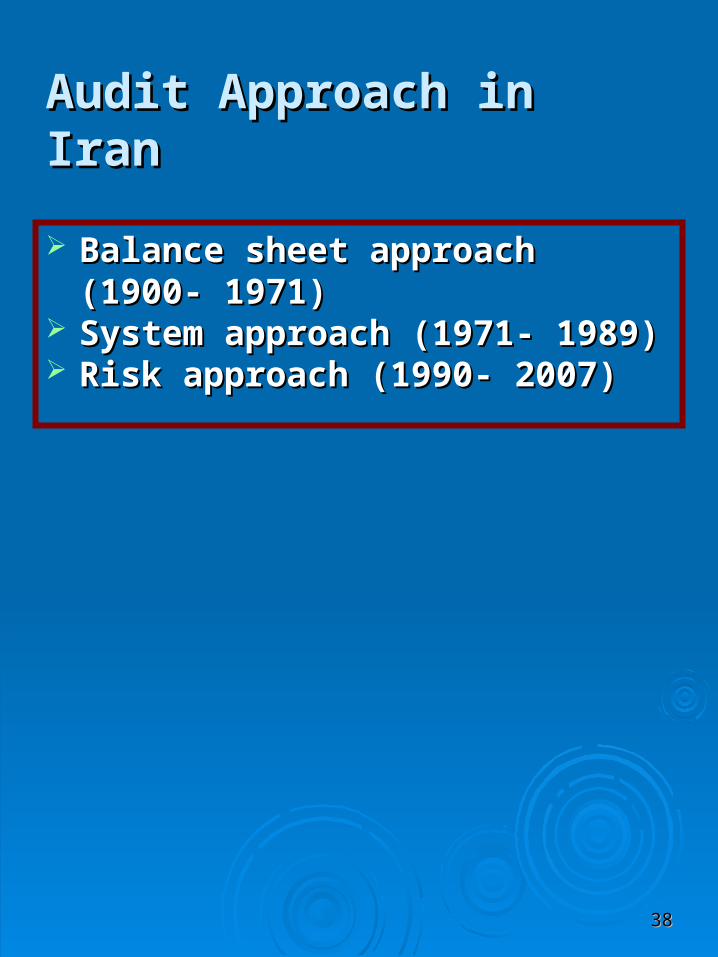

Audit Approach in IranAudit Approach in Iran

Balance sheet approach (1900- Balance sheet approach (1900- 1971)1971)

System approach (1971- 1989)System approach (1971- 1989) Risk approach (1990- 2007)Risk approach (1990- 2007)

3939

Chronology of Events Chronology of Events in the History of the in the History of the Iranian Accounting Iranian Accounting Profession (1)Profession (1)

YearYear EventEvent

19321932(enactment of (enactment of

business law)business law)

Appointment of Inspector to examine the accounts and Appointment of Inspector to examine the accounts and documents of companiesdocuments of companies

19471947(the tax law (the tax law

amended)amended)

Use of public accountants services in matters of tax Use of public accountants services in matters of tax documentation was permitteddocumentation was permitted

1949, 19561949, 1956(income tax law (income tax law

enacted)enacted)

Acceptance of the results of the “Accountant Under Acceptance of the results of the “Accountant Under Oath” ’s examinations concerning the accounts or Oath” ’s examinations concerning the accounts or balance sheets of businessmen and companies for the balance sheets of businessmen and companies for the purpose of tax assessmentpurpose of tax assessment

19611961 Approval of operating regulations for the use of Approval of operating regulations for the use of “Accountants Under Oath)“Accountants Under Oath)

19621962 Formation of the first association of “Accountant Under Formation of the first association of “Accountant Under Oath”Oath”

19631963 Approval of the articles of association of the Center Approval of the articles of association of the Center “Accountant Under Oath”“Accountant Under Oath”

19641964 Foundation of the Iranian Accounting AssociationFoundation of the Iranian Accounting Association

19661966(enactment of the (enactment of the

law of direct law of direct taxes)taxes)

Formation of the “Center of Public Accountants” Formation of the “Center of Public Accountants” permittedpermitted

19671967 Approval of regulations governing the selection of Approval of regulations governing the selection of public accountantspublic accountants

19681968(amendment of (amendment of

business law)business law)

Requirement for the use of public accountant’s reportRequirement for the use of public accountant’s report

19701970 Approval of operational regulations governing the Approval of operational regulations governing the appointment of persons licensed for the inspection of appointment of persons licensed for the inspection of corporation- type companiescorporation- type companies

19711971 Foundation of the Audit Firm, Inc.Foundation of the Audit Firm, Inc.

19721972 Use of public accountant’s report is made a Use of public accountant’s report is made a requirement/approval of the Articles of Association of requirement/approval of the Articles of Association of the Center of Public Accountantsthe Center of Public Accountants

4040

Chronology of Events Chronology of Events in the History of the in the History of the Iranian Accounting Iranian Accounting Profession (2)Profession (2)19801980 Foundation of the Audit Institute Under the Organization of National Foundation of the Audit Institute Under the Organization of National

Industries and the Planning and Budget OrganizationIndustries and the Planning and Budget Organization

19831983 Enactment of the law decreeing the Establishment of the Iranian Audit Enactment of the law decreeing the Establishment of the Iranian Audit organizationorganization

19871987 Approval of the Articles of Association of the Audit OrganizationApproval of the Articles of Association of the Audit Organization

19931993Enactment of the law decreeing the Establishment of the Iranian Audit Enactment of the law decreeing the Establishment of the Iranian Audit OrganizationOrganization

19951995 Approval of the regulations governing the determination of the public Approval of the regulations governing the determination of the public accountant’s qualificationsaccountant’s qualifications

19991999 Formulation of the Iranian Association of Certified Public Accountants Formulation of the Iranian Association of Certified Public Accountants Articles of AssociationArticles of Association

20002000 Formulation of the regulations governing the use of the public Formulation of the regulations governing the use of the public accountant’s services and reportsaccountant’s services and reports

20002000 Formulation of guide for elections to the supreme council of the Iranian Formulation of guide for elections to the supreme council of the Iranian Association of Certified Public AccountantsAssociation of Certified Public Accountants

20012001 Announcement of the first group of public accountants and the convening Announcement of the first group of public accountants and the convening of the first general meeting of the Iranian Association of Certified Public of the first general meeting of the Iranian Association of Certified Public AccountantsAccountants

20042004 The second electing of high council of Iranian Association of Certified Public The second electing of high council of Iranian Association of Certified Public Accountants (IACPA)Accountants (IACPA)

20072007 The third electing of high council of Iranian Association of Certified Public The third electing of high council of Iranian Association of Certified Public Accountants (IACPA)Accountants (IACPA)

4141

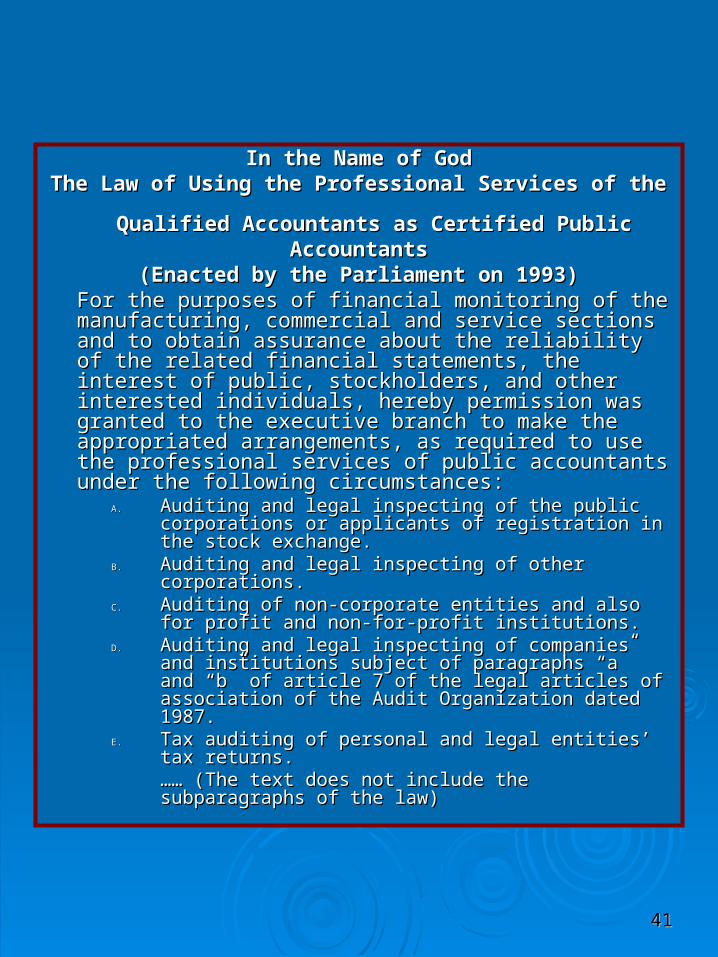

In the Name of GodIn the Name of GodThe Law of Using the Professional Services of The Law of Using the Professional Services of

the the Qualified Accountants as Certified PublicQualified Accountants as Certified Public

AccountantsAccountants(Enacted by the Parliament on 1993)(Enacted by the Parliament on 1993)

For the purposes of financial monitoring of the For the purposes of financial monitoring of the manufacturing, commercial and service sections manufacturing, commercial and service sections and to obtain assurance about the reliability of the and to obtain assurance about the reliability of the related financial statements, the interest of public, related financial statements, the interest of public, stockholders, and other interested individuals, stockholders, and other interested individuals, hereby permission was granted to the executive hereby permission was granted to the executive branch to make the appropriated arrangements, as branch to make the appropriated arrangements, as required to use the professional services of public required to use the professional services of public accountants under the following circumstances:accountants under the following circumstances:

A.A. Auditing and legal inspecting of the public Auditing and legal inspecting of the public corporations or applicants of registration in the corporations or applicants of registration in the stock exchange.stock exchange.

B.B. Auditing and legal inspecting of other Auditing and legal inspecting of other corporations.corporations.

C.C. Auditing of non-corporate entities and also for Auditing of non-corporate entities and also for profit and non-for-profit institutions.profit and non-for-profit institutions.

D.D. Auditing and legal inspecting of companies and Auditing and legal inspecting of companies and institutions subject of paragraphs “a” and “b” of institutions subject of paragraphs “a” and “b” of article 7 of the legal articles of association of the article 7 of the legal articles of association of the Audit Organization dated 1987.Audit Organization dated 1987.

E.E. Tax auditing of personal and legal entities’ tax Tax auditing of personal and legal entities’ tax returns. returns. …… …… (The text does not include the (The text does not include the subparagraphs of the law)subparagraphs of the law)

4242

USE OF Certified Public USE OF Certified Public ACCOUNTANTS AND ACCOUNTANTS AND ACCEPTANCE OF RETURNS BY ACCEPTANCE OF RETURNS BY TAX ASSESSORS (1)TAX ASSESSORS (1)

State tax organization issued a notice to all State tax organization issued a notice to all manufacturing, trading and services entities as follows: manufacturing, trading and services entities as follows: According to the Law on the Use of Specialized and According to the Law on the Use of Specialized and Professional Services of Qualified (Official) Accountants Professional Services of Qualified (Official) Accountants ratified on 11.01.1994 and the Amendment made by the ratified on 11.01.1994 and the Amendment made by the Islamic Consultative Assembly in the said Law on Islamic Consultative Assembly in the said Law on 16.02.1994 as well as Article 2 of the Executive 16.02.1994 as well as Article 2 of the Executive Regulation of Note 4 of the above Law ratified in the Regulation of Note 4 of the above Law ratified in the form of a decree by the Council of Ministers on form of a decree by the Council of Ministers on 03.09.2000, the following taxpayers are under the 03.09.2000, the following taxpayers are under the obligation to appoint the statutory “Inspectors” of their obligation to appoint the statutory “Inspectors” of their companies from among the auditing firms being companies from among the auditing firms being members of the IACPA. Appointment may be made from members of the IACPA. Appointment may be made from among natural persons accepted as official accountants among natural persons accepted as official accountants by IACPA by taxpayers mentioned in Sub-clause “f” by IACPA by taxpayers mentioned in Sub-clause “f” below, only: below, only:

• CompaniesCompanies accepted by or applying for accepted by or applying for acceptance by the Stock and Negotiable acceptance by the Stock and Negotiable Instruments Exchange as well as the companies Instruments Exchange as well as the companies affiliated to the said companies.affiliated to the said companies.

• Public joint stock companies as well as their Public joint stock companies as well as their subsidiary and affiliate companies.subsidiary and affiliate companies.

• The companies described in Sub-clauses a & b of The companies described in Sub-clauses a & b of Article 7 of the Audit Organization in due Article 7 of the Audit Organization in due compliance with the procedure set forth in Note 1 compliance with the procedure set forth in Note 1 of Article 132 of the Public Accounts Law.of Article 132 of the Public Accounts Law.

• Branches and representative offices of foreign Branches and representative offices of foreign companies which are registered in Iran pursuant to companies which are registered in Iran pursuant to the permission granted under the Law Authorizing the permission granted under the Law Authorizing Registration of Branches and Representative Registration of Branches and Representative Offices of Foreign Companies, ratified 1997 Offices of Foreign Companies, ratified 1997 (Liaison offices excluded).(Liaison offices excluded).

4343

USE OF OFFICIAL USE OF OFFICIAL (CHARTERED) ACCOUNTANTS (CHARTERED) ACCOUNTANTS AND ACCEPTANCE OF AND ACCEPTANCE OF RETURNS BY TAX RETURNS BY TAX ASSESSORS(2)ASSESSORS(2)

E.E.Non government public entities, foundations, Non government public entities, foundations, companies, and organizations and the entities companies, and organizations and the entities affiliated thereto.affiliated thereto.

F.F.Other natural persons and legal entities whose Other natural persons and legal entities whose aggregate turn-over (sale of commodities or services aggregate turn-over (sale of commodities or services and aggregate income in respect of contractors made and aggregate income in respect of contractors made and signed by them) shall not exceed eight billion and signed by them) shall not exceed eight billion rails or whose total assets shall not exceed sixteen rails or whose total assets shall not exceed sixteen billion Rails.billion Rails.

According to Article 2 of the above Executive Regulation, According to Article 2 of the above Executive Regulation, the financial statements of the persons and entities the financial statements of the persons and entities mentioned in the above sub-clauses being devoid of a mentioned in the above sub-clauses being devoid of a confirmatory audit report by firms of auditors being confirmatory audit report by firms of auditors being members of IACPA or official accountants acceptable to members of IACPA or official accountants acceptable to IACPA may not be acceptable to the ministries, government IACPA may not be acceptable to the ministries, government organizations and companies, banks and insurance organizations and companies, banks and insurance companies, non bank credit institutes, the Organization of companies, non bank credit institutes, the Organization of Stock and Negotiable Instruments Exchange and non Stock and Negotiable Instruments Exchange and non government public foundations and institutes. No such government public foundations and institutes. No such statements may be used as evidence in favour of the said statements may be used as evidence in favour of the said persons and entities.persons and entities.

According to Article 272 of the Direct Taxation Act as According to Article 272 of the Direct Taxation Act as Amended on 16.02.2002 by the Islamic Consultative Amended on 16.02.2002 by the Islamic Consultative Assembly, those who are in charge of accounting works or Assembly, those who are in charge of accounting works or carry out the duties of statutory inspectors of the taxpayers carry out the duties of statutory inspectors of the taxpayers mentioned in the above sub-clauses shall be under the mentioned in the above sub-clauses shall be under the obligation to submit an audit report on the activities of the obligation to submit an audit report on the activities of the said taxpayers and submit same to the taxpayer for said taxpayers and submit same to the taxpayer for submission to the State tax office concerned in case of a submission to the State tax office concerned in case of a request by the taxpayers in this regard. In such case, the request by the taxpayers in this regard. In such case, the State tax office concerned shall be bound to accept the said State tax office concerned shall be bound to accept the said audit report without examination and issue a tax audit report without examination and issue a tax assessment sheet based on the said report.assessment sheet based on the said report.

Acceptance of the audit report by the State tax office Acceptance of the audit report by the State tax office concerned shall be subject to submission of a tax audit concerned shall be subject to submission of a tax audit report drawn up by the same auditor who prepared the report drawn up by the same auditor who prepared the above audit report on the basis of auditing norms and above audit report on the basis of auditing norms and standards together with tax return or within a maximum standards together with tax return or within a maximum period of three (3) months after the date of expiry of the period of three (3) months after the date of expiry of the respite provided for submission of returns to the State tax respite provided for submission of returns to the State tax office concerned.office concerned.

4444

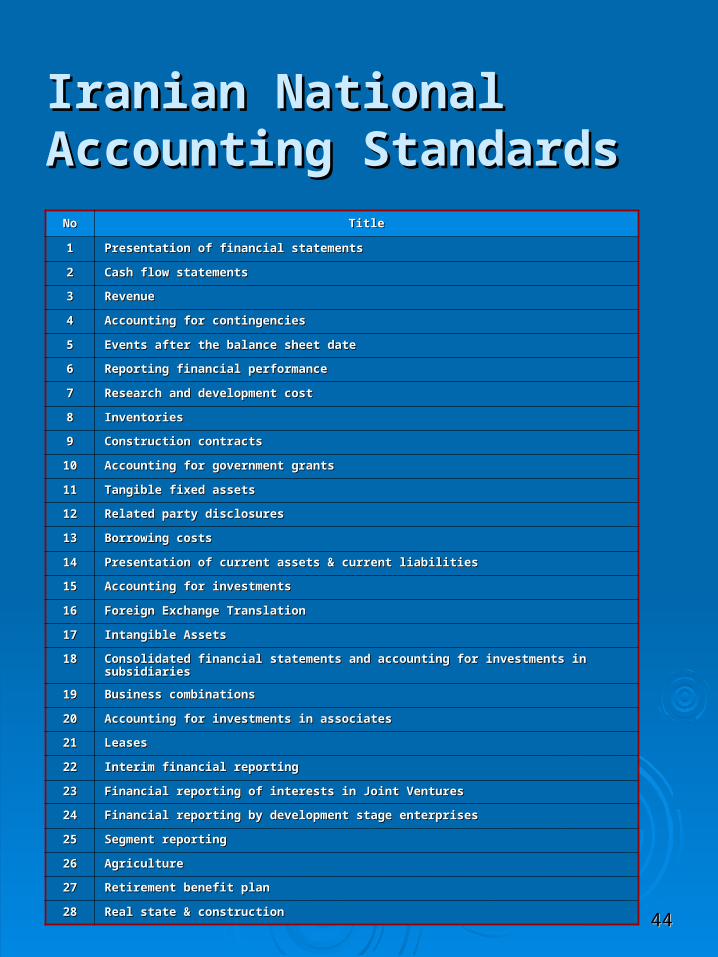

Iranian National Iranian National Accounting StandardsAccounting Standards

NoNo TitleTitle

11 Presentation of financial statementsPresentation of financial statements

22 Cash flow statementsCash flow statements

33 RevenueRevenue

44 Accounting for contingenciesAccounting for contingencies

55 Events after the balance sheet dateEvents after the balance sheet date

66 Reporting financial performanceReporting financial performance

77 Research and development costResearch and development cost

88 InventoriesInventories

99 Construction contractsConstruction contracts

1010 Accounting for government grantsAccounting for government grants

1111 Tangible fixed assetsTangible fixed assets

1212 Related party disclosuresRelated party disclosures

1313 Borrowing costsBorrowing costs

1414 Presentation of current assets & current liabilitiesPresentation of current assets & current liabilities

1515 Accounting for investmentsAccounting for investments

1616 Foreign Exchange TranslationForeign Exchange Translation

1717 Intangible AssetsIntangible Assets

1818 Consolidated financial statements and accounting for investments in Consolidated financial statements and accounting for investments in subsidiariessubsidiaries

1919 Business combinationsBusiness combinations

2020 Accounting for investments in associatesAccounting for investments in associates

2121 LeasesLeases

2222 Interim financial reportingInterim financial reporting

2323 Financial reporting of interests in Joint VenturesFinancial reporting of interests in Joint Ventures

2424 Financial reporting by development stage enterprisesFinancial reporting by development stage enterprises

2525 Segment reportingSegment reporting

2626 Agriculture Agriculture

2727 Retirement benefit planRetirement benefit plan

2828 Real state & constructionReal state & construction

4545

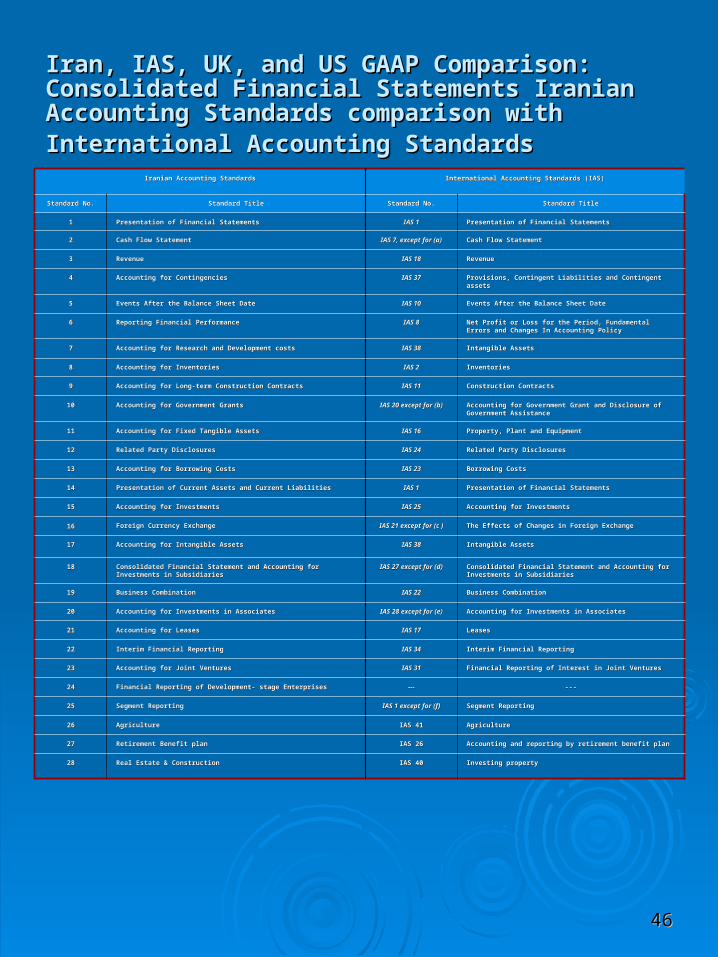

What is comparative table What is comparative table between Iran & IAS Auditing between Iran & IAS Auditing standardsstandards

NoNo TitleTitle Compatible withCompatible with

------ Introductory MattersIntroductory Matters PrefacePreface

2020 Objectives and General Principle Governing Audit of Financial StatementsObjectives and General Principle Governing Audit of Financial Statements ISA 200ISA 200

2121 Terms of Audit EngagementsTerms of Audit Engagements ISA 210ISA 210

2222 Quality Control for Audit WorkQuality Control for Audit Work ISA 220ISA 220

2323 DocumentationDocumentation ISA 230ISA 230

2424 Fraud and ErrorFraud and Error ISA 240ISA 240

2525 Consideration of Laws and Regulations in an Audit of financial statementsConsideration of Laws and Regulations in an Audit of financial statements ISA 250ISA 250

3030 PlanningPlanning ISA 300ISA 300

3131 Knowledge of BusinessKnowledge of Business ISA 310ISA 310

3232 Audit MaterialityAudit Materiality ISA 320ISA 320

4040 Risk Assessments and Internet ControlRisk Assessments and Internet Control ISA 400ISA 400

5050 Audit EvidenceAudit Evidence ISA 500ISA 500

5151 Initial Engagement- Opening BalancesInitial Engagement- Opening Balances ISA 510ISA 510

5252 Analytical ProceduresAnalytical Procedures ISA 520ISA 520

5353 Audit SamplingAudit Sampling ISA 530ISA 530

5454 Audit of Accounting EstimatesAudit of Accounting Estimates ISA 540ISA 540

5555 Related PartiesRelated Parties ISA 550ISA 550

5656 Subsequent EventsSubsequent Events ISA 560ISA 560

5757 Going ConcernGoing Concern ISA 570ISA 570

5858 Management RepresentationsManagement Representations ISA 580ISA 580

6060 Using the work of another auditorUsing the work of another auditor ISA 600ISA 600

6161 Considering the work of internal auditingConsidering the work of internal auditing ISA 610ISA 610

6262 Using the work of and expertUsing the work of and expert ISA 620ISA 620

7070 The auditor report on financial statementsThe auditor report on financial statements IAS 700*IAS 700*