1 Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc. Chapter 8 Operating...

46

1 Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc. Chapter 8 Operating Assets: Property, Plant, and Equipment, Natural Resources, and Intangibles

-

date post

21-Dec-2015 -

Category

Documents

-

view

229 -

download

0

Transcript of 1 Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc. Chapter 8 Operating...

1Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc.

Chapter 8

Operating Assets:

Property, Plant, and Equipment, Natural Resources,and Intangibles

2Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc.

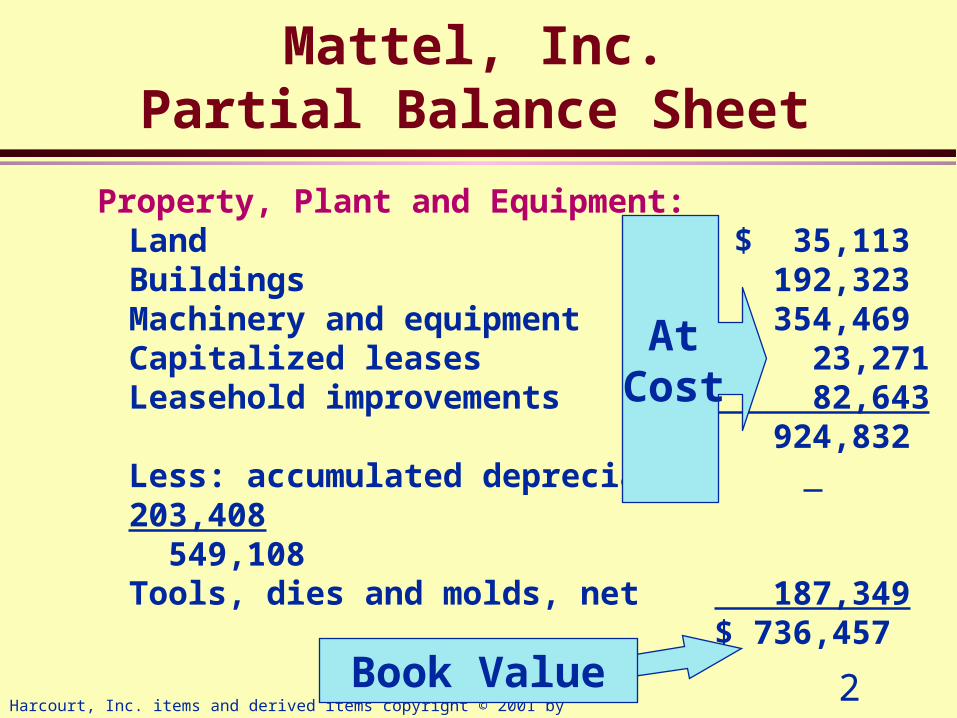

Property, Plant and Equipment:Land $ 35,113Buildings 192,323Machinery and equipment 354,469Capitalized leases 23,271Leasehold improvements 82,643 924,832Less: accumulated depreciation 203,408

549,108Tools, dies and molds, net 187,349 $ 736,457

Mattel, Inc.Partial Balance Sheet

Book Value

AtCost

3Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc.

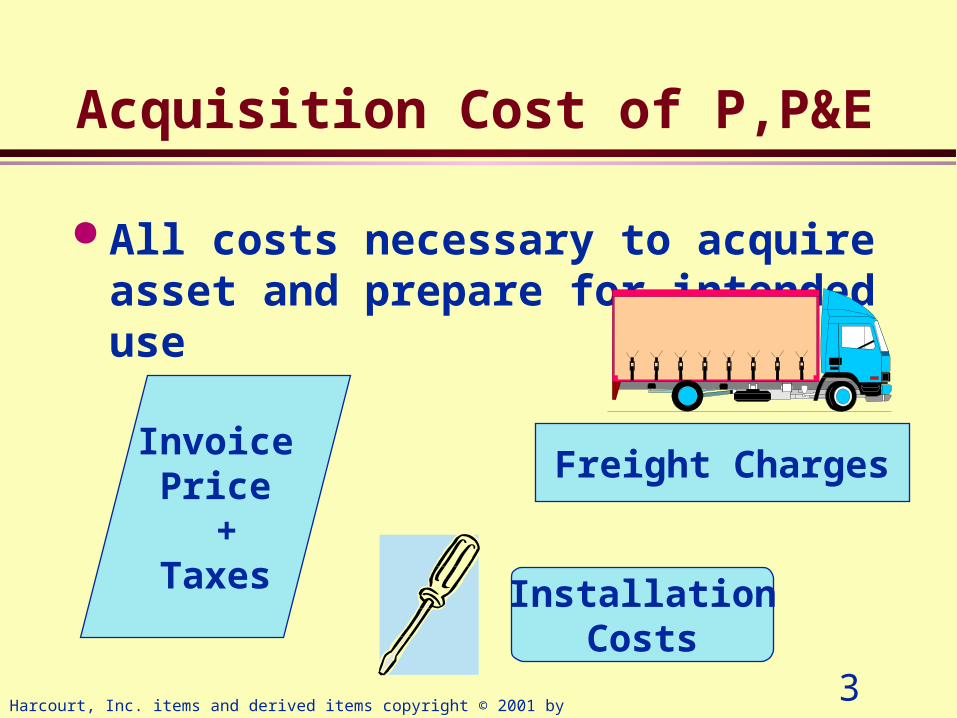

Acquisition Cost of P,P&E

All costs necessary to acquire asset and prepare for intended use

InvoicePrice

+Taxes Installation

Costs

Freight Charges

4Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc.

Group Asset Purchases

Allocate cost of lump-sum purchase based on fair market values

Cost$500,000

$385,000

$115,000

AllocatedCost

Land = $120,000

Building = $400,000

Fair MarketValue

77%

23%

% ofMarketValue

5Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc.

Capitalization of Interest

Interest can be included as part of the cost of an asset if:» company constructs asset

over time, and» borrows money to finance

construction

6Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc.

Depreciation of P,P & E

Match Cost ofAssets

with periodsbenefited

1 2 3

4 5 6 7 8 9 10

11 12 13 14 15 16 17

18 19 20 21 22 23 24

25 26 28 29 30 3127

Straight-Line Units ofProduction

AcceleratedMethods

via

7Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc.

$9,0003 year life

Straight-Line Method

Allocates cost of asset evenly over its useful life

$3,000Year 1

$3,000Year 2

$3,000Year 3

8Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc.

Units-of-Production Method

Allocate asset cost based on number of units produced over its useful life

depreciation =

per unit

9Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc.

Double declining-balance Method

Double the straight-line rate on a declining balance (book value)

Accelerated method - higher amount of depreciation in early years

Straight-lineRate

10Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc.

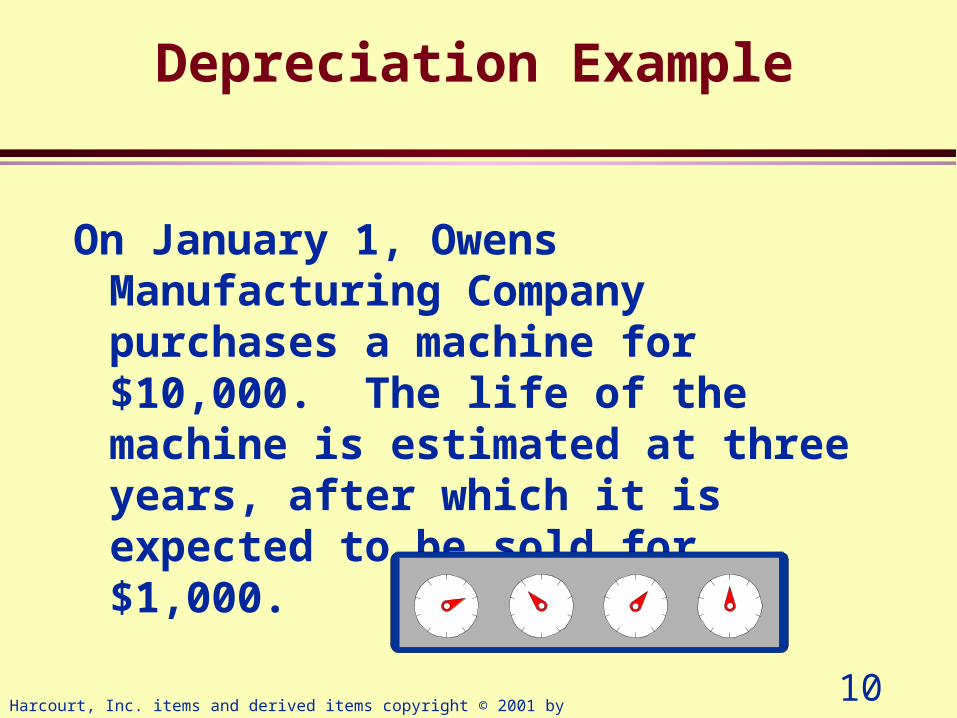

Depreciation Example

On January 1, Owens Manufacturing Company purchases a machine for $10,000. The life of the machine is estimated at three years, after which it is expected to be sold for $1,000.

11Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc.

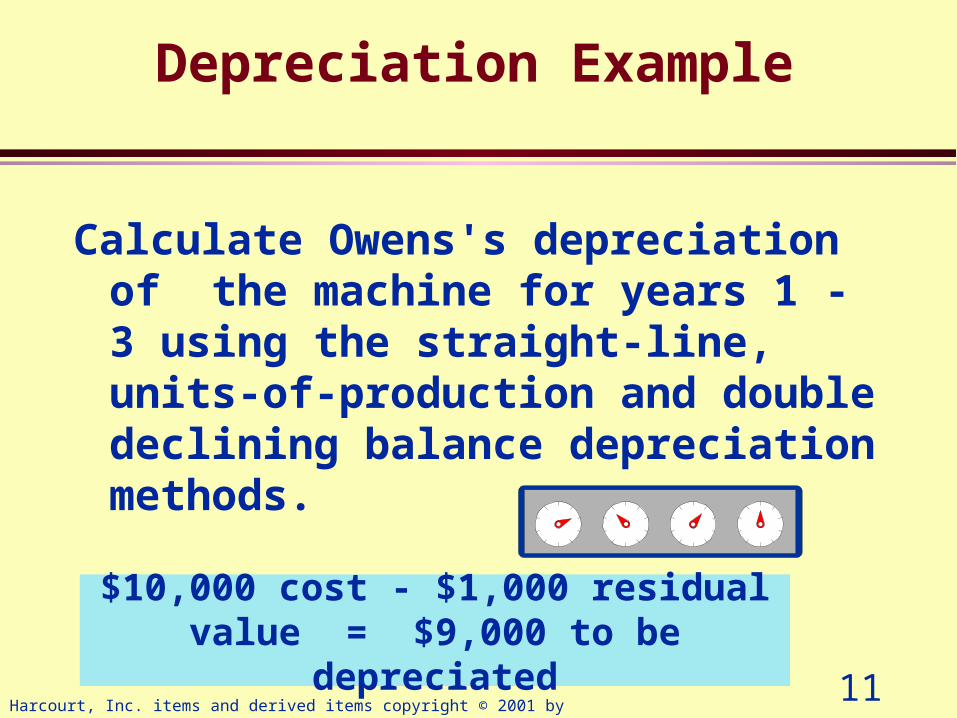

Depreciation Example

Calculate Owens's depreciation of the machine for years 1 - 3 using the straight-line, units-of-production and double declining balance depreciation methods.

$10,000 cost - $1,000 residual value = $9,000 to be depreciated

12Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc.

Straight-Line Depreciation

Depreciation = Cost - Residual Value Life= $10,000 - $1,000

3 years= $3,000

$9,0003 year life

$3,000Year 1

$3,000Year 2

$3,000Year 3

13Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc.

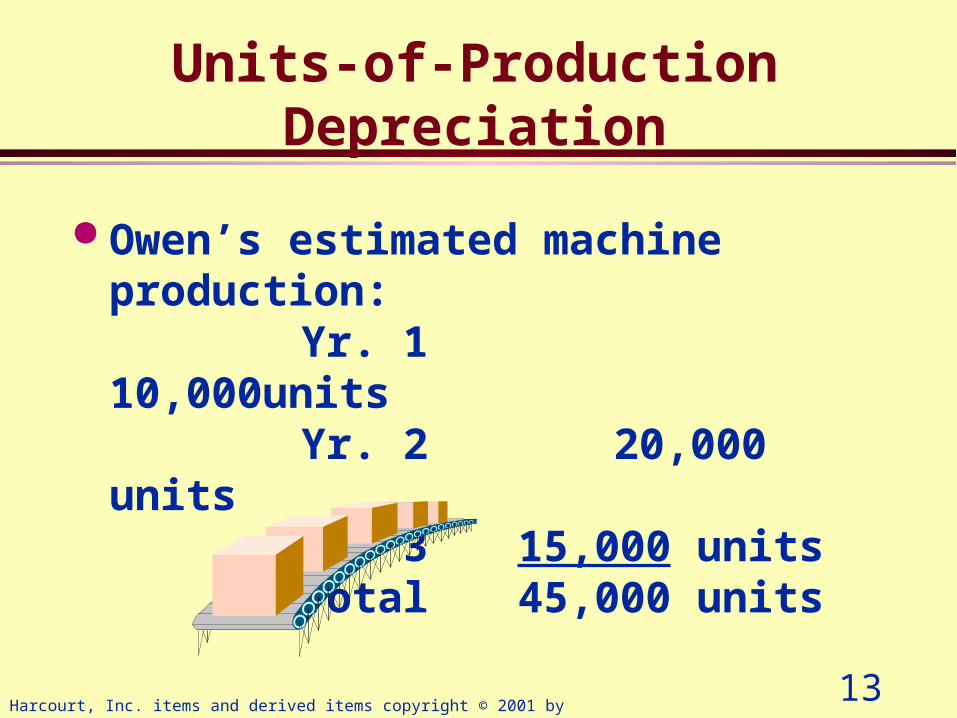

Units-of-Production Depreciation

Owen’s estimated machine production:Yr. 1 10,000unitsYr. 2 20,000 unitsYr. 3 15,000 unitsTotal 45,000 units

14Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc.

Units-of-Production Depreciation

Depreciation = Cost - Residual Valueper unit Total Units in Life

= $10,000 - $1,000 45,000

= $ .20

15Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc.

Owen’s annual depreciation:

Yr. 1 10,000 units x $.20/unit = $2,000

Yr. 2 20,000 units x $.20/unit = 4,000

Yr. 3 15,000 units x $.20/unit = 3,000

$9,000

Units-of-Production Depreciation

16Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc.

Double declining-balance Depreciation

DDB rate = (100% / useful life) x 2

= (100% / 3 years) x 2

= 66.7%

.667

Initiallyignore

residual value

17Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc.

Double declining-balance Depreciation

Year 1 Depreciation = Beginning book value x rate

= $10,000 x 66.7%

= $6,667

Beginning Ending

Year Rate Book Value Depreciation Book Value

1 66.7% $10,000 $6,667 $3,333

18Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc.

Double declining-balance Depreciation

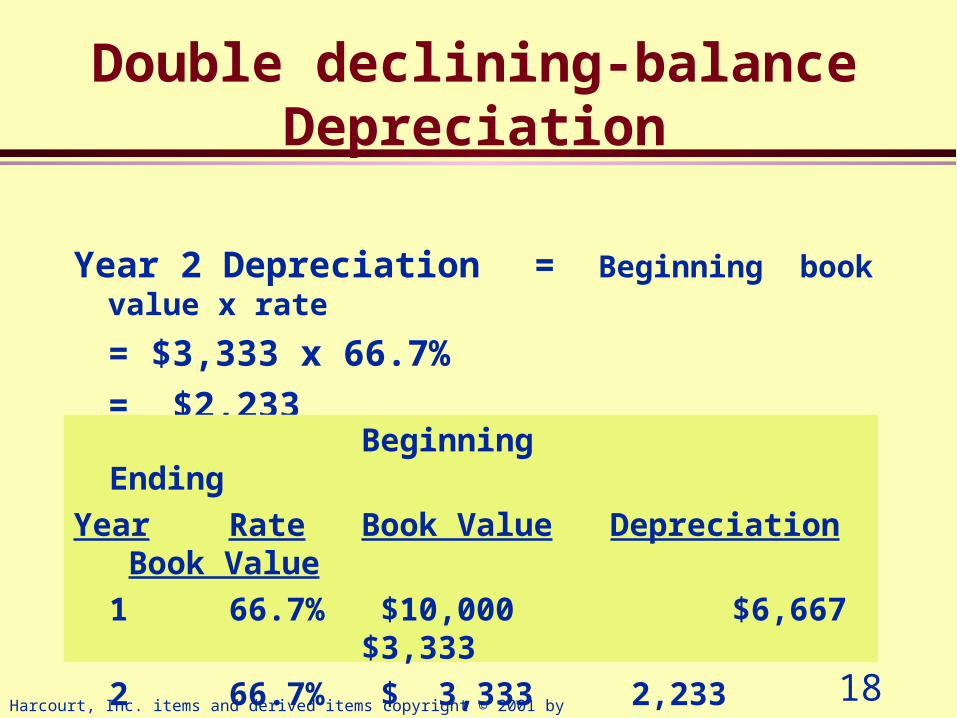

Year 2 Depreciation = Beginning book value x rate

= $3,333 x 66.7%

= $2,233Beginning Ending

Year Rate Book Value Depreciation Book Value

1 66.7% $10,000 $6,667 $3,333

2 66.7% $ 3,333 2,233 1,100

19Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc.

Double declining-balance Depreciation

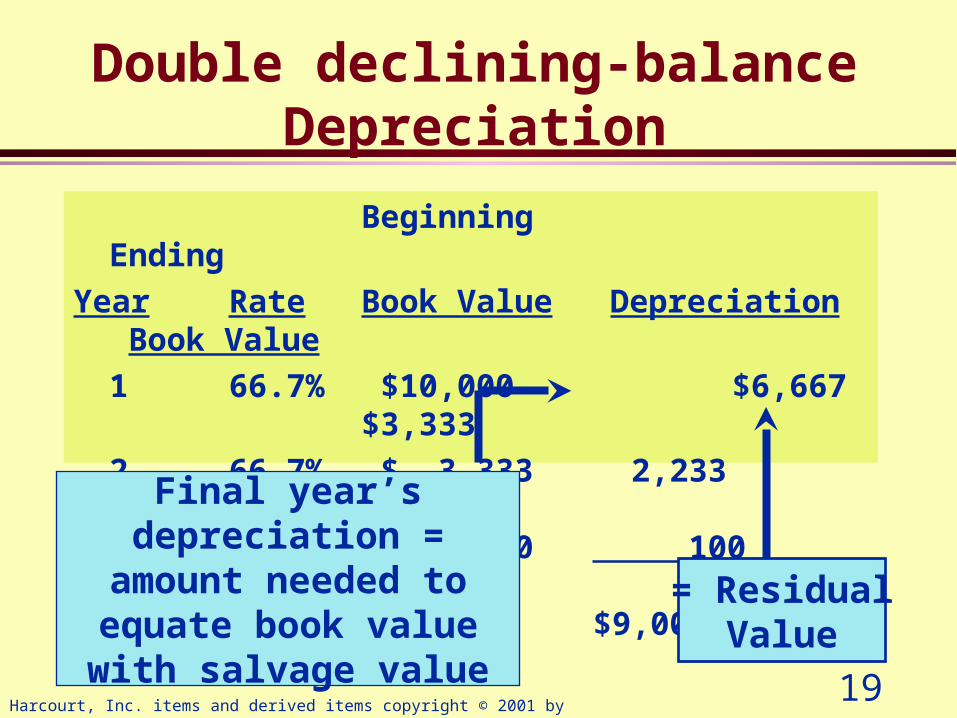

Beginning Ending

Year Rate Book Value Depreciation Book Value

1 66.7% $10,000 $6,667 $3,333

2 66.7% $ 3,333 2,233 1,100

3 66.7% $ 1,100 100 1,000

$9,000Final year’s depreciation = amount needed to equate book value with salvage

value

= ResidualValue

20Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc.

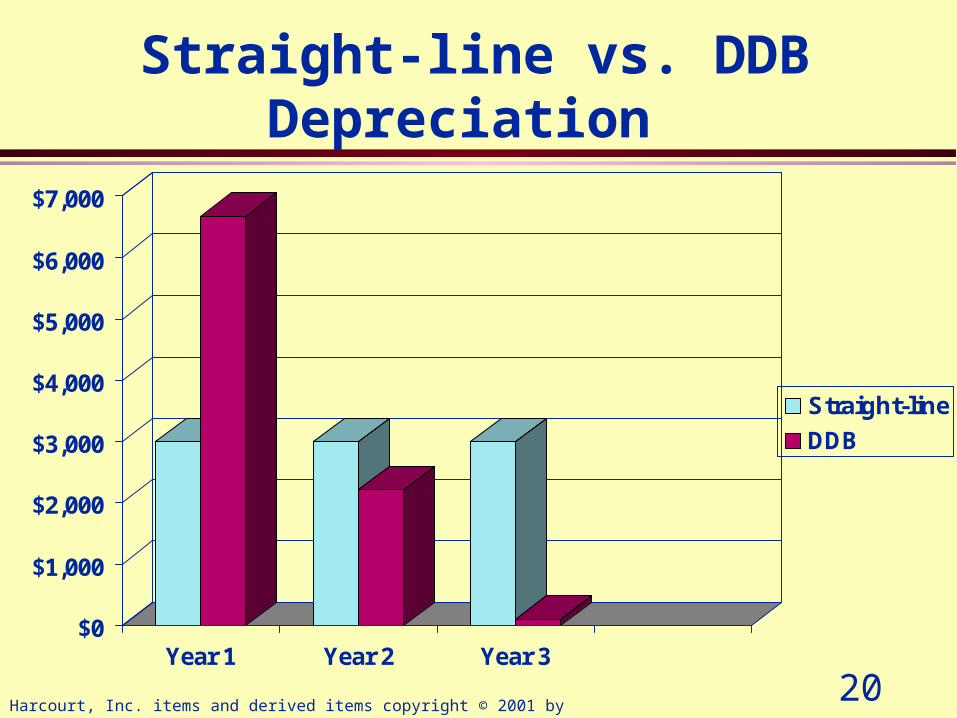

Straight-line vs. DDB Depreciation

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

Year 1 Year 2 Year 3

Straight-line

DDB

21Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc.

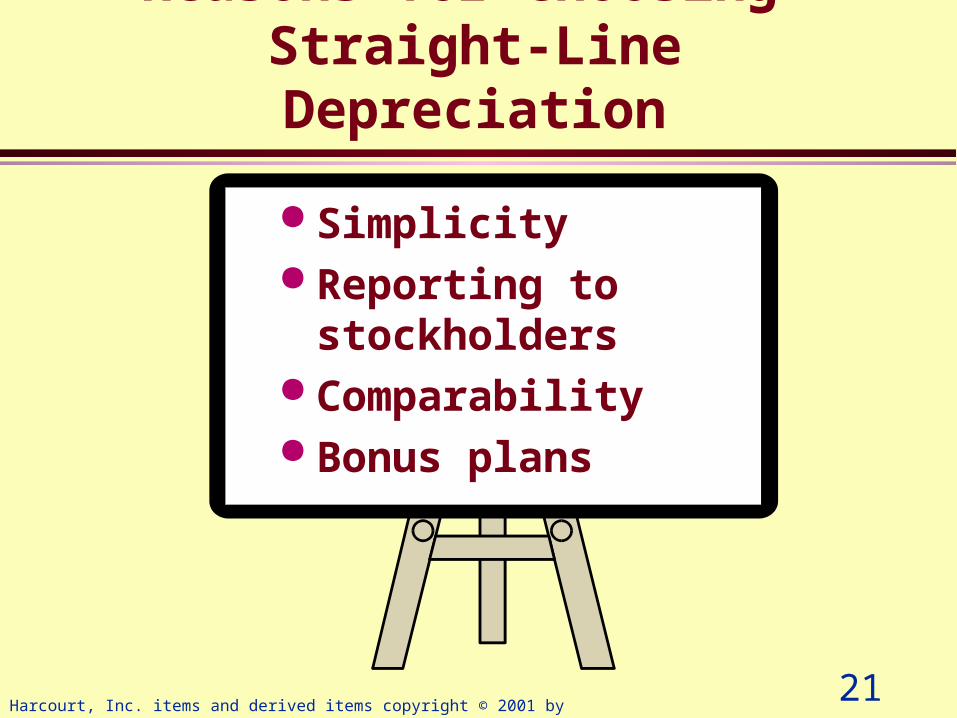

Reasons for Choosing Straight-Line Depreciation

Simplicity Reporting to

stockholders Comparability Bonus plans

22Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc.

Reasons for Choosing Accelerated Methods

Technological rate of change and competitiveness

Minimize taxable income

Income Taxes

23Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc.

Changes in Depreciation Estimates

Recompute depreciation schedule using new estimates

Record prospectively (i.e. change should affect current and future years only)

Useful life is 7 years vs. 5?

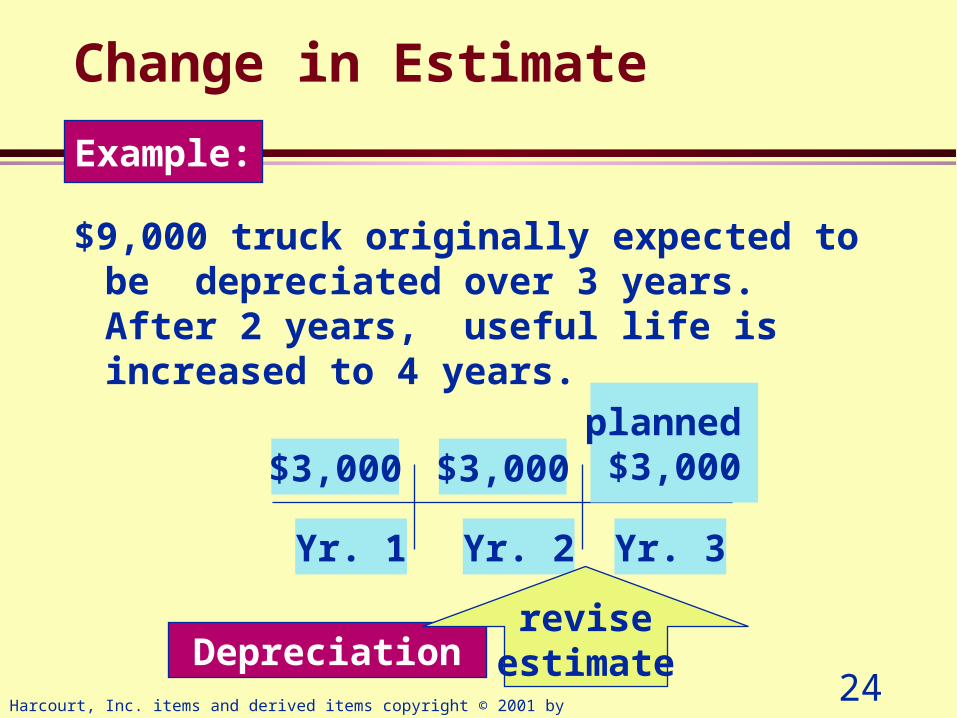

24Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc.

Depreciation

Change in Estimate

$9,000 truck originally expected to be depreciated over 3 years. After 2 years, useful life is increased to 4 years.

$3,000planned $3,000$3,000

Yr. 1 Yr. 2 Yr. 3

Example:

reviseestimate

25Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc.

Depreciation

Change in Estimate

$3,000 remaining book value allocated prospectively over remaining life

Yr. 1 Yr. 2 Yr. 3 Yr. 4

reviseestimate

$1,500 $1,500$3,000 $3,000

Example:

26Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc.

Capital vs. Revenue Expenditures

IncomeStatement

Revenue Expenditure» Expense immediately

BalanceSheet

Capital Expenditure» Treat as asset addition to

be depreciated over a period of time

27Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc.

Capital vs. Revenue Expenditures

Capitalize

Capitalize

Expense

General Guidelines:

» Increase asset life

» Increase asset productivity

» Normal maintenance

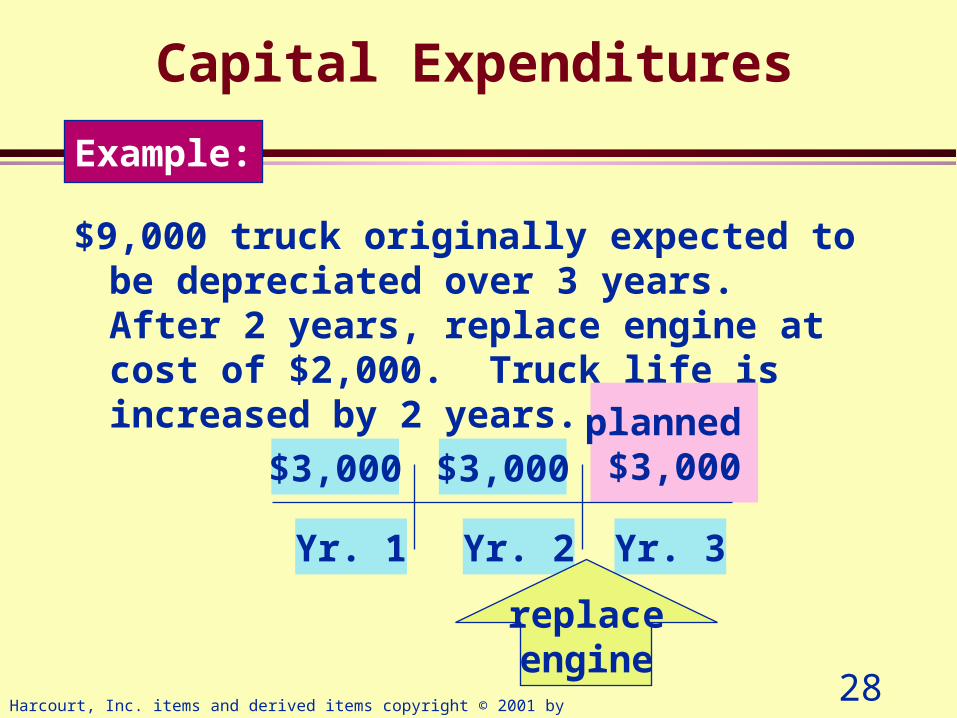

28Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc.

Capital Expenditures

$9,000 truck originally expected to be depreciated over 3 years. After 2 years, replace engine at cost of $2,000. Truck life is increased by 2 years.

$3,000planned $3,000$3,000

Yr. 1 Yr. 2 Yr. 3

Example:

replaceengine

29Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc.

Capital Expenditures

$3,000 remaining book value + $2,000 capital expenditure depreciated prospectively over remaining life

$2,500 $2,500

Yr. 1 Yr. 2 Yr. 3 Yr. 4

replaceengine

$3,000 $3,000

Example:

30Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc.

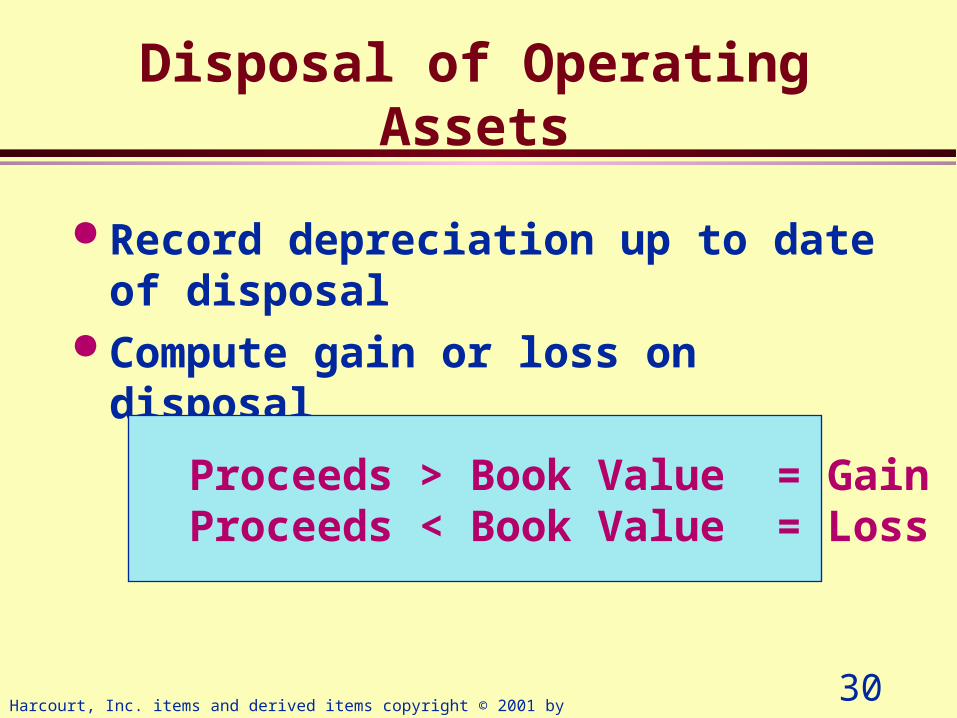

Disposal of Operating Assets

Record depreciation up to date of disposal

Compute gain or loss on disposal

Proceeds > Book Value = Gain Proceeds < Book Value = Loss

31Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc.

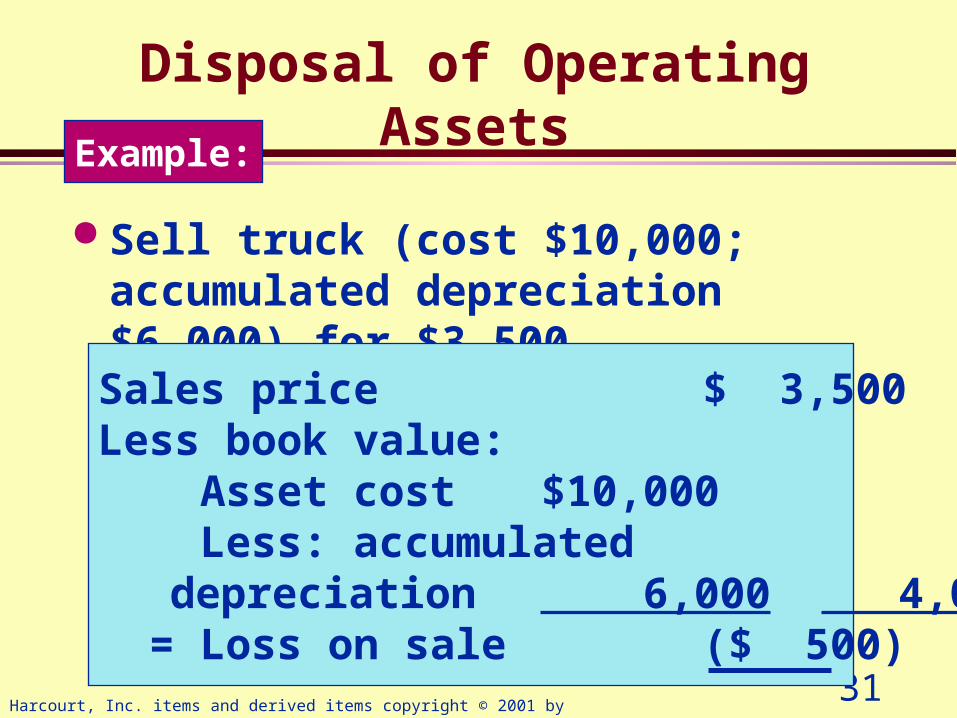

Disposal of Operating Assets

Sell truck (cost $10,000; accumulated depreciation $6,000) for $3,500

Sales price $ 3,500 Less book value: Asset cost $10,000 Less: accumulated

depreciation 6,000 4,000 = Loss on sale ($ 500)

Example:

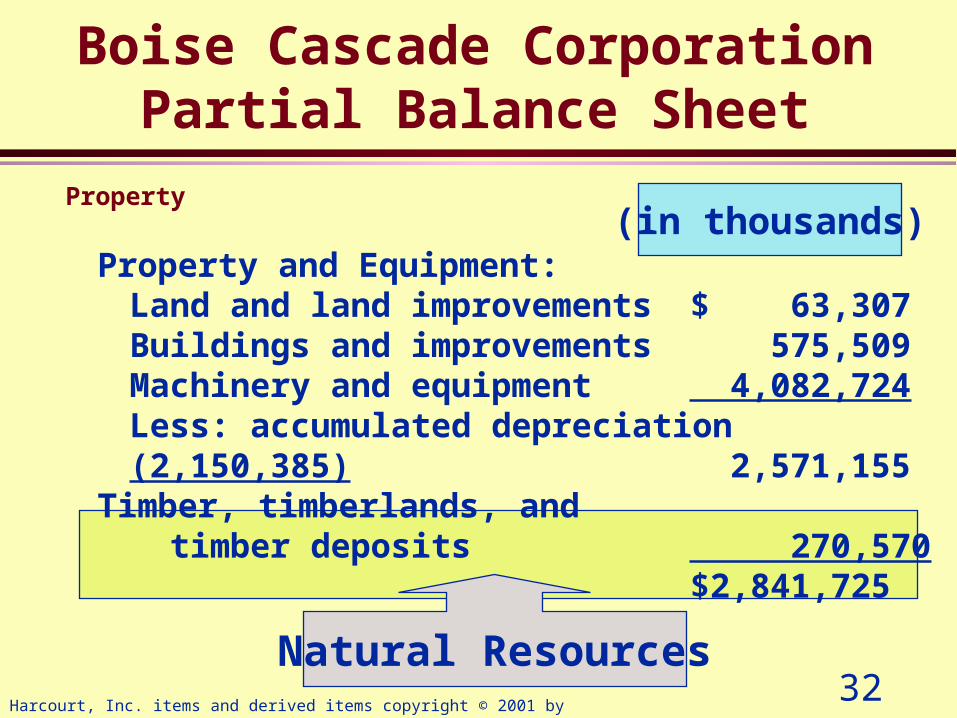

32Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc.

Natural Resources

(in thousands)

Boise Cascade CorporationPartial Balance Sheet

Property

Property and Equipment:Land and land improvements $ 63,307Buildings and improvements 575,509Machinery and equipment 4,082,724Less: accumulated depreciation (2,150,385)

2,571,155Timber, timberlands, and

timber deposits 270,570 $2,841,725

33Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc.

Natural Resources

Resource consumed as it is used Expense called depletion vs. depreciation Depletion method similar to units of

production

34Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc.

Intangible

Assets

(in millions)

Time Warner, Inc.Partial Balance Sheet

Operating Assets:Property, plant and equipment, net $ 1,991

Music catalogues, contracts

and copyrights 876

Cable television and sports franchises 2,868

Goodwill 11,919

35Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc.

Patents

Intangible Assets

Long-term assets with no physical properties

Goodwill

Trademarks

Copyrights

36Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc.

Intangible Assets

Includes cost to acquire and prepare for intended use

+Purchase Price

Acquisition Costs

(i.e. legal fees, registration

fees, etc.)

37Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc.

Research & Development

Must be expensed in period incurred

Difficult to identify future benefits

38Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc.

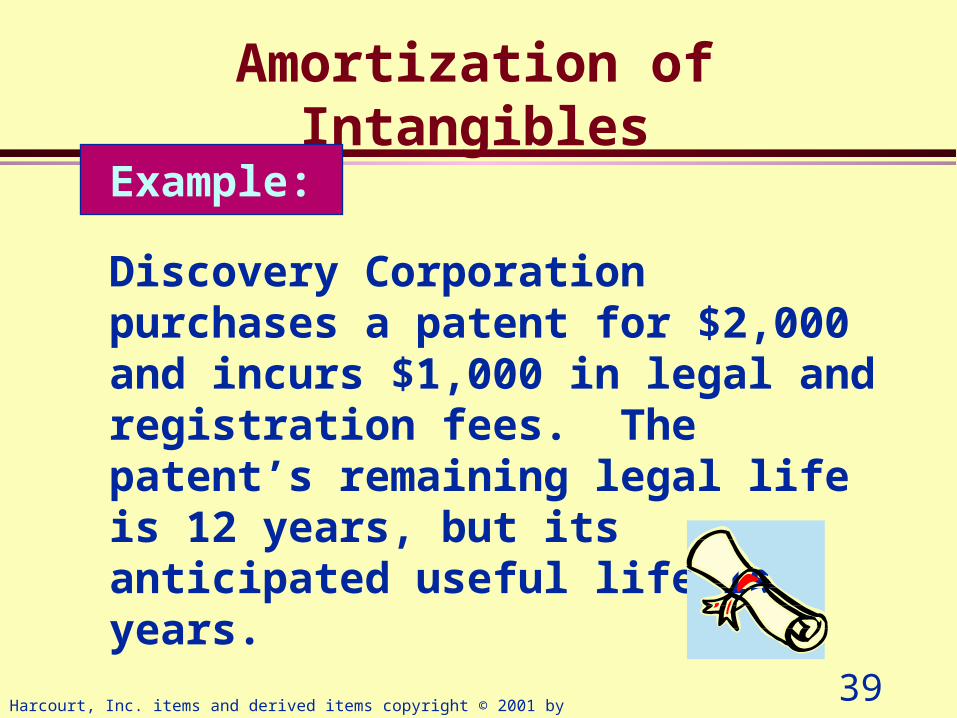

Amortization of Intangibles

Normally recorded using straight-line method

Reported net of accumulated amortization

Amortized over legal or useful life, whichever is shorter

39Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc.

Amortization of Intangibles

Discovery Corporation purchases a patent for $2,000 and incurs $1,000 in legal and registration fees. The patent’s remaining legal life is 12 years, but its anticipated useful life is 5 years.

Example:

40Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc.

Amortization of Intangibles

Discovery’s Annual Amortization:

Purchase price $2,000

Acquisition costs 1,000

Total 3,000

divide by:

lesser of legal or useful life 5 years

Annual amortization $ 600

41Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc.

Amortization of Intangibles

Discovery’s Balance Sheet Presentation:

Upon End ofPurchase Yr. 1 Yr. 5

Long-term Assets:

Intangible assets, net of accum.

amortization $3,000 $2,400 $ 0

42Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc.

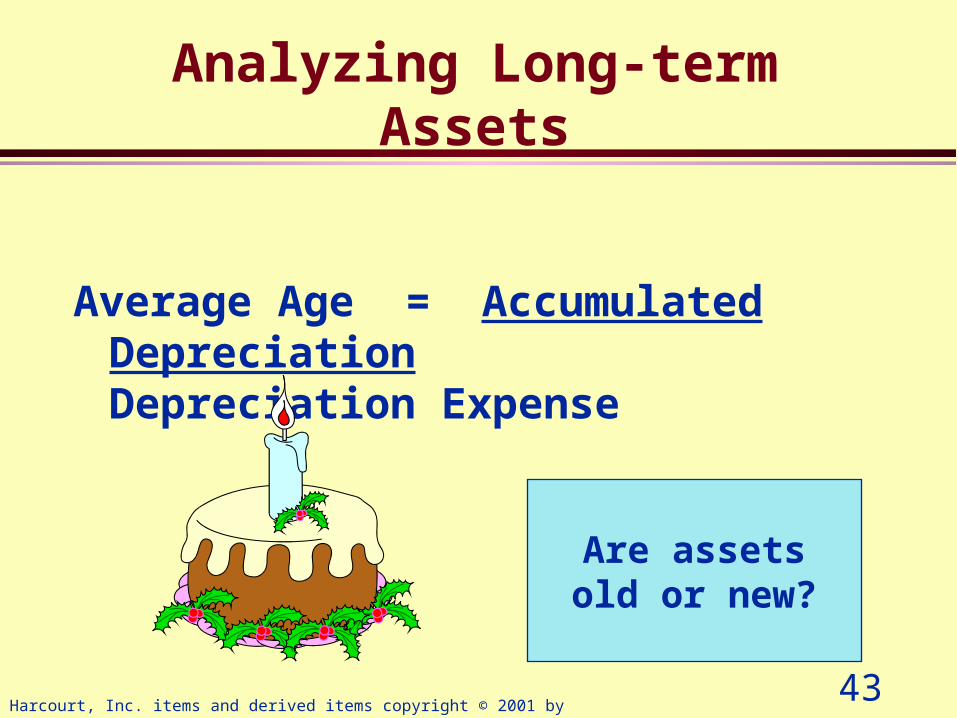

Analyzing Long-term Assets

Average Life = Property, Plant & Equipment

Depreciation Expense

What is the average

depreciable period of the

company’s assets?

43Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc.

Analyzing Long-term Assets

Average Age = Accumulated Depreciation Depreciation Expense

Are assets old or new?

44Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc.

Analyzing Long-term Assets

Asset Turnover = Net Sales

Average Total Assets

How productive are the company’s

assets?

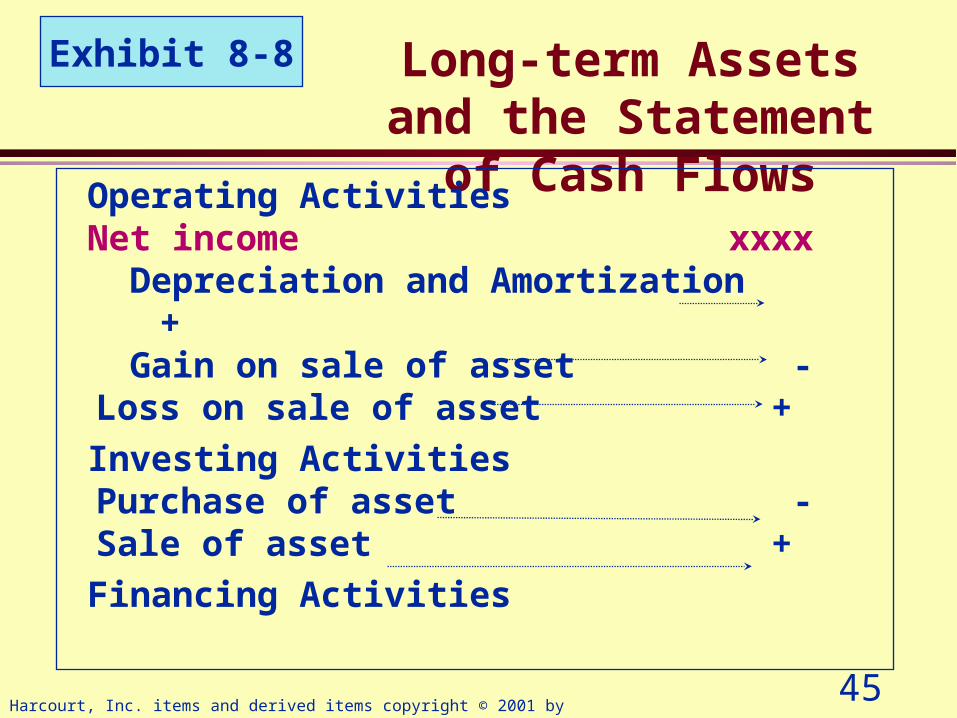

45Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc.

Long-term Assets and the Statement of Cash Flows

Operating Activities Net income xxxx Depreciation and Amortization + Gain on sale of asset -

Loss on sale of asset +

Investing ActivitiesPurchase of asset -Sale of asset +

Financing Activities

Exhibit 8-8

46Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc.

End of Chapter 8