1 Form 990 Fallout: Lessons Learned February 26, 2010 Grace Lee, Esq., Presenter.

38

1 Form 990 Fallout: Lessons Learned February 26, 2010 Grace Lee, Esq., Presenter

-

Upload

elizabeth-robbins -

Category

Documents

-

view

226 -

download

3

Transcript of 1 Form 990 Fallout: Lessons Learned February 26, 2010 Grace Lee, Esq., Presenter.

1

Form 990 Fallout: Lessons LearnedFebruary 26, 2010

Grace Lee, Esq., Presenter

© 2010 Venable LLP

2

Overview of redesigned form

Recap of 2008

Who must file in 2009

Lessons Learned and Changes for 2009

– Release of information related to trustees receiving financial aid

– Creation of policies

– Disclosure of compensation for highly compensated

– Private business use of bond proceeds

overview

© 2010 Venable LLP

3

IRS “guiding principles“

– Enhance transparency to provide the IRS and the public with a realistic picture of the organization, along with the basis for comparison to other organizations

– Promote compliance by accurately reflecting the organization’s operations so the IRS may efficiently assess the risk of noncompliance

– Minimize the burden on filing organizations

overview of redesigned form 990

© 2010 Venable LLP

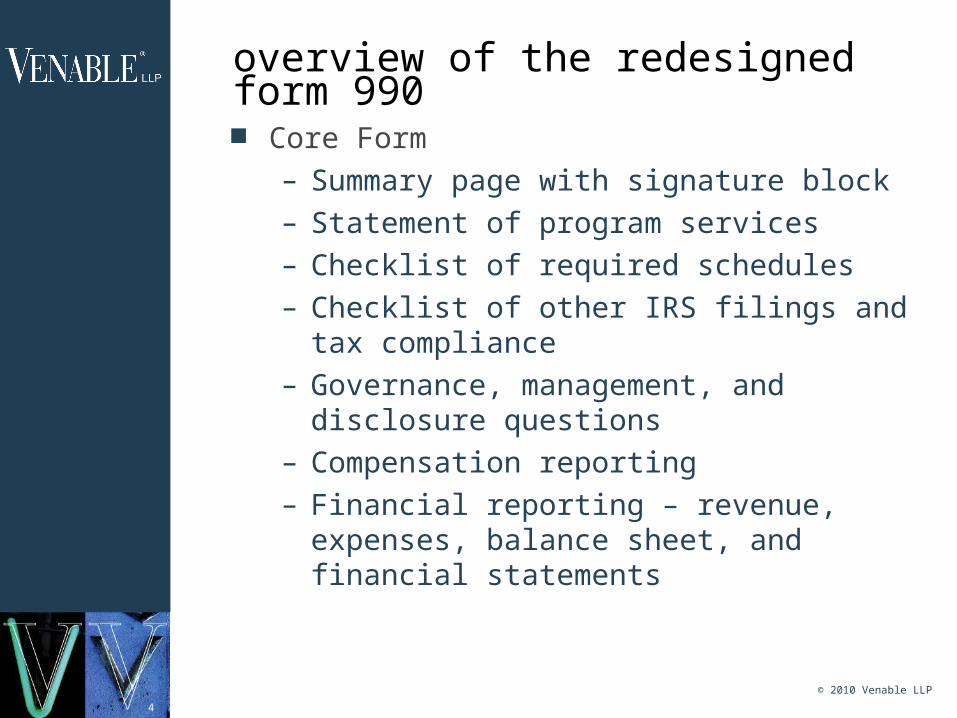

4

Core Form

– Summary page with signature block

– Statement of program services

– Checklist of required schedules

– Checklist of other IRS filings and tax compliance

– Governance, management, and disclosure questions

– Compensation reporting

– Financial reporting – revenue, expenses, balance sheet, and financial statements

overview of the redesigned form 990

© 2010 Venable LLP

5

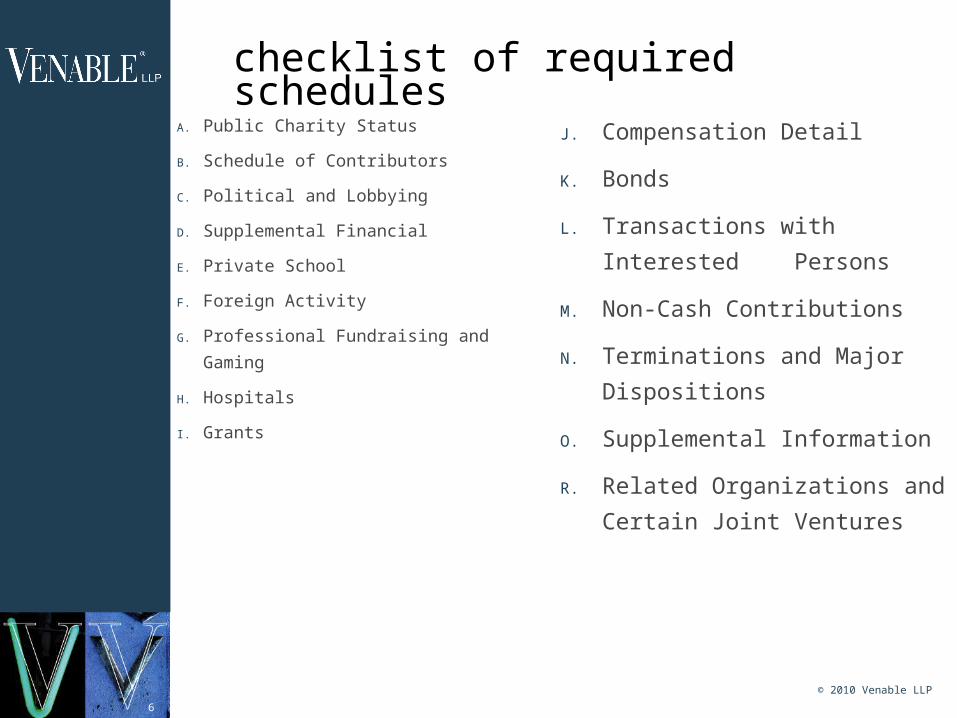

Intended to provide the IRS with an overview of a

school’s activities

Answers to the questions trigger when a school

must complete a schedule

New question 12A in Form 990 for 2009 asks

whether school was included in consolidated

independent audited financial statements

prepared in accordance with generally accepted

accounting principles

New Form 990 has 16 schedules

checklist of required schedules

© 2010 Venable LLP

6

J. Compensation Detail

K. Bonds

L. Transactions with Interested

Persons

M. Non-Cash Contributions

N. Terminations and Major

Dispositions

O. Supplemental Information

R. Related Organizations and

Certain Joint Ventures

A. Public Charity Status

B. Schedule of Contributors

C. Political and Lobbying

D. Supplemental Financial

E. Private School

F. Foreign Activity

G. Professional Fundraising and Gaming

H. Hospitals

I. Grants

checklist of required schedules

© 2010 Venable LLP

7

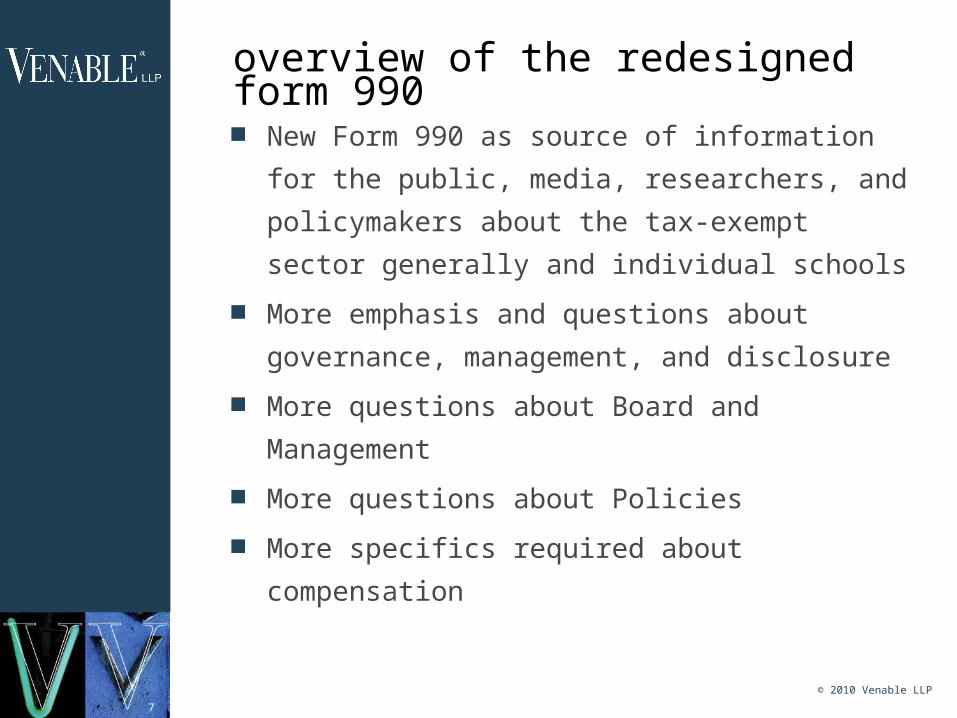

New Form 990 as source of information for the

public, media, researchers, and policymakers

about the tax-exempt sector generally and

individual schools

More emphasis and questions about governance,

management, and disclosure

More questions about Board and Management

More questions about Policies

More specifics required about compensation

overview of the redesigned form 990

© 2010 Venable LLP

8

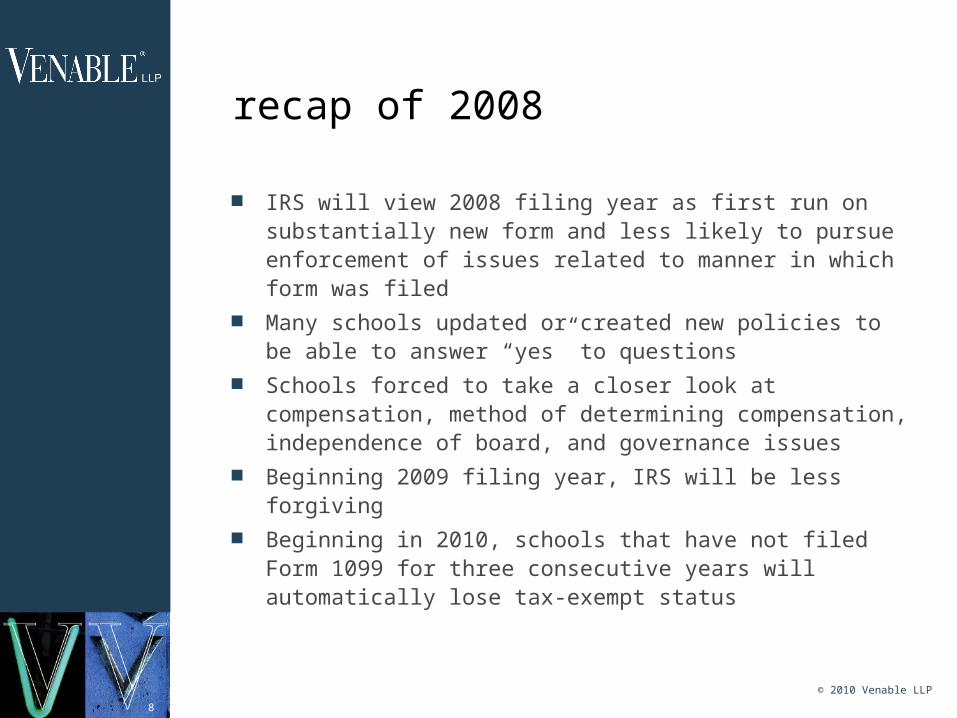

recap of 2008

IRS will view 2008 filing year as first run on substantially new form and less likely to pursue enforcement of issues related to manner in which form was filed

Many schools updated or created new policies to be able to answer “yes” to questions

Schools forced to take a closer look at compensation, method of determining compensation, independence of board, and governance issues

Beginning 2009 filing year, IRS will be less forgiving Beginning in 2010, schools that have not filed Form 1099 for

three consecutive years will automatically lose tax-exempt status

© 2010 Venable LLP

9

Core form must be completed by all filers– Except, Form 990-EZ can be filed by schools

with gross receipts of less than $500,000 in revenue and total assets of less than $1.25 million.

• Lower threshold than 2008 (1 million in revenue and total assets less than $2.5 million for 2008)

• More schools must file the From 990

Only non “church” schools complete– Church schools must obtain approval letter

from IRS

16 schedules filled out based on a school’s

specific indicators

who must file form 990 in 2009

10

Hot Issues and Lessons Learned

© 2010 Venable LLP

11

New Form 990 as source of information for the public

Schools can expect more public scrutiny under redesigned

form (parents, prospective families, media)

Summary section asks for:

– most significant activities

– key financial, compensation, governance, and operational information

– revenue and expense information from current and prior year

Summary section allows reader to spot changes and trends

and draw conclusions on the overall health of the school

Schools should take the opportunity to market itself to

donors, media, and others who may search for public

information about the school

summary section

© 2010 Venable LLP

12

Mission, program services, programmatic changes,

and accomplishments in narrative format– reformatted– upfront so that organization can “tell story” early– another marketing opportunity for schools

Must describe three largest programs measured by

expenses– if a Section 501(c)(3), must include:

• amount of grants to others• total expenses• Revenue

statement of program services

© 2010 Venable LLP

13

Schedule O

Any additional information about the school’s mission

and programs can be reported on a new Schedule O

Asks whether organization makes its governing

documents, conflict of interest policy, and

financial statements, available to the public

– Schools should make sure such documents are updated, sends a consistent message about mission and philosophy, and accurate

Schedule O is required in 2009

© 2010 Venable LLP

14

New section of Form 990

Rationale: independent boards and well-defined

governance and management policies increase

likelihood of tax compliance, safeguarding of

charitable assets, and serving of charitable

interests

IRS encourages higher level of self-regulation

and internal controls

Transparency and accountability

Influenced by the Sarbanes Oxley Act

governance, management, and disclosure

© 2010 Venable LLP

15

Importance of an organization maintaining an

independent board highlighted in the new Form

990

Core Form asks about:

– total number of voting board members

– number of voting board members that are independent

– relationships between officers, directors, and key employees

– relationship with school

questions regarding board and management

© 2010 Venable LLP

16

Any delegation of control to a management company– IRS signaling the importance of having an engaged

Board manage the school, and not ceding control to an outside company

Any material diversion of the school’s assets– Diversion is “material” if it exceeds the lesser of

$250,000 or 5% of the school’s gross receipts for its tax year or total assets as of years end

Minutes taken at board and board committee

meetings– IRS stressing the importance of maintaining

Boards and Committees that do not operate in secrecy, and help foster transparency and accountability

more questions regarding board and management

© 2010 Venable LLP

17

Board receives a copy of Form 990 before filed

– Reviewed at board meeting

– Provided a copy

– Core form but not schedules

Process to review Form 990

– IRS signaling the need for trustees (or at least board committee or top management officials) to play an active role in the Form 990 preparation

and more questions regarding board and management

© 2010 Venable LLP

18

Questions regarding policies are a new addition

to the Form 990 – Answers are yes/no

Questions indicate the importance of self-

regulation and transparency

Policies not legally required

Schools must have policies and procedures in

place by the end of the 2009 tax year to answer

in the affirmative

NOTE: In 2009 Form 990 schools should report

major changes in policies in Part VI rather than in

a letter to EO Determinations

questions regarding policies

© 2010 Venable LLP

19

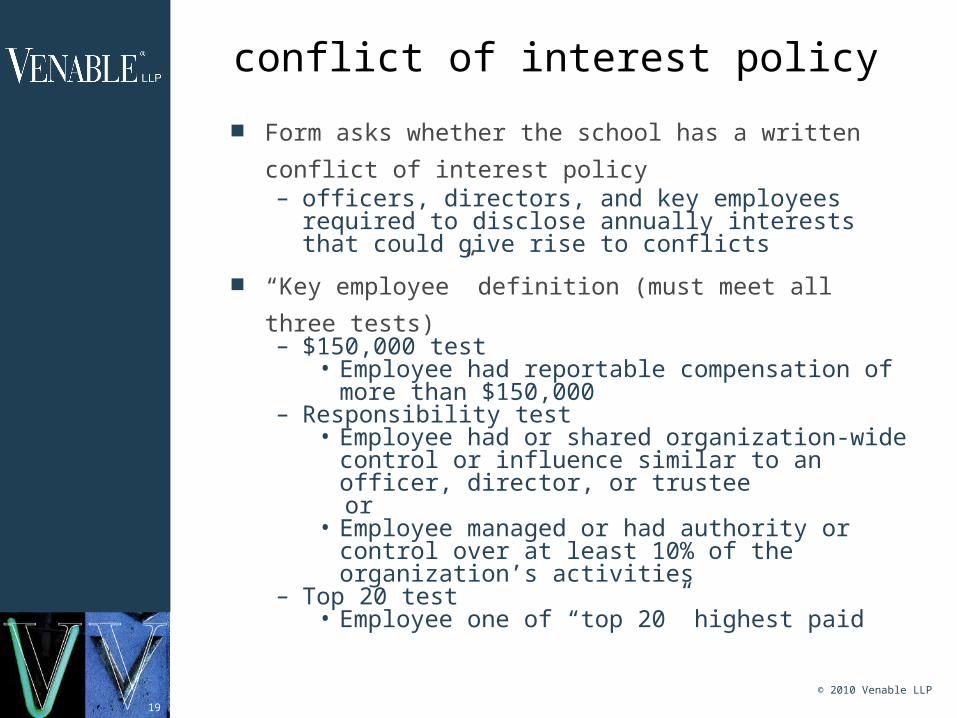

Form asks whether the school has a written conflict of

interest policy– officers, directors, and key employees required to

disclose annually interests that could give rise to conflicts

“Key employee” definition (must meet all three tests)– $150,000 test

• Employee had reportable compensation of more than $150,000

– Responsibility test• Employee had or shared organization-wide

control or influence similar to an officer, director, or trustee

or• Employee managed or had authority or control

over at least 10% of the organization’s activities– Top 20 test

• Employee one of “top 20” highest paid

conflict of interest policy

© 2010 Venable LLP

20

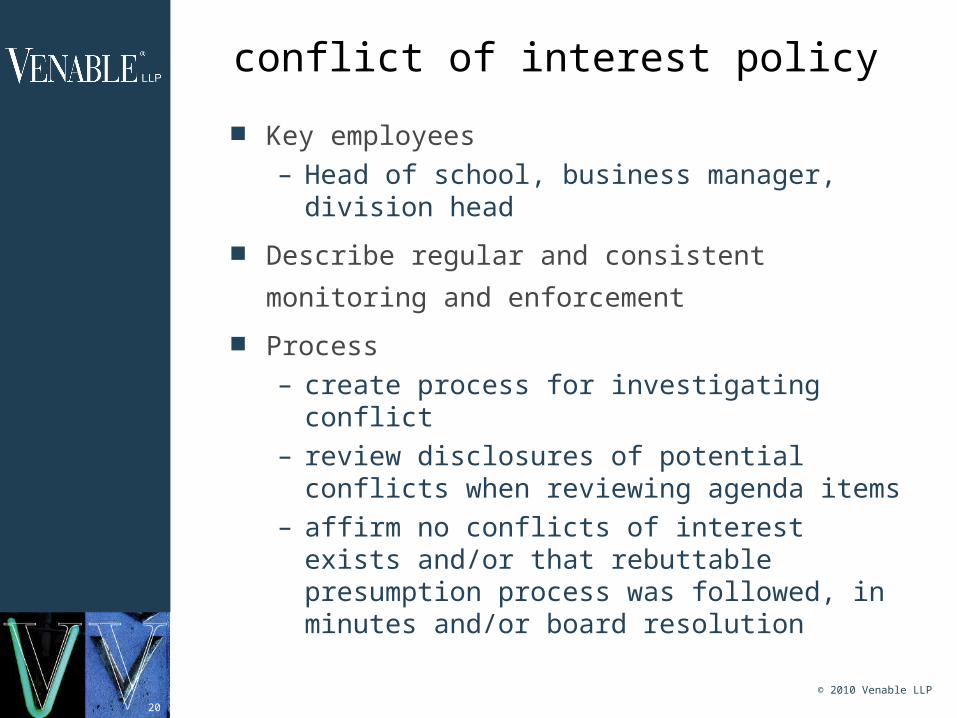

Key employees

– Head of school, business manager, division head

Describe regular and consistent monitoring and

enforcement

Process

– create process for investigating conflict

– review disclosures of potential conflicts when reviewing agenda items

– affirm no conflicts of interest exists and/or that rebuttable presumption process was followed, in minutes and/or board resolution

conflict of interest policy

© 2010 Venable LLP

21

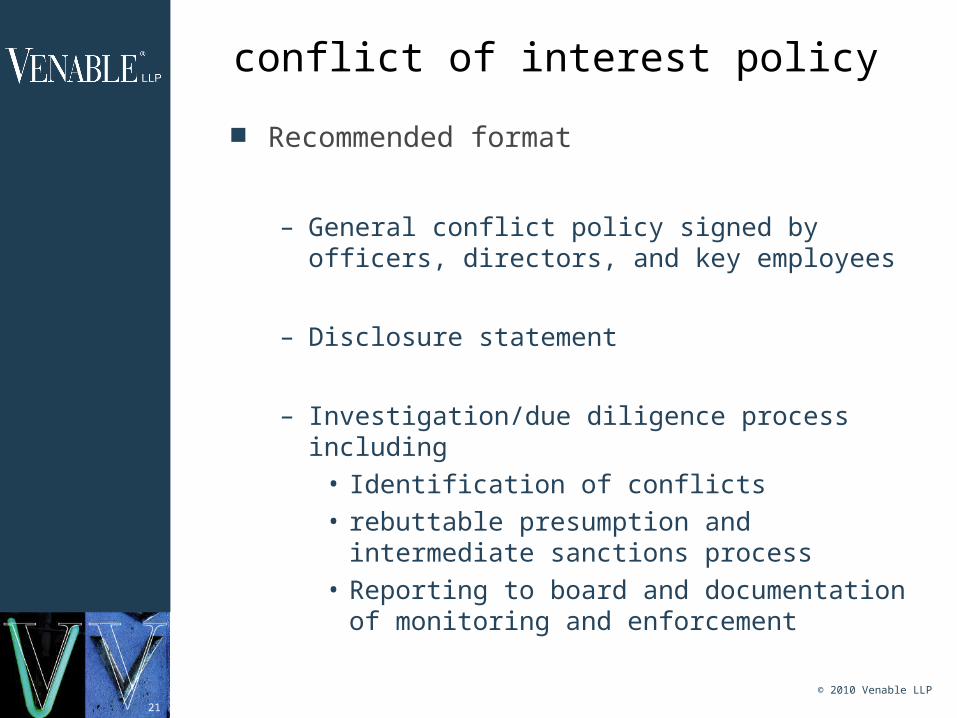

Recommended format

– General conflict policy signed by officers, directors, and key employees

– Disclosure statement

– Investigation/due diligence process including• Identification of conflicts• rebuttable presumption and intermediate

sanctions process• Reporting to board and documentation of

monitoring and enforcement

conflict of interest policy

© 2010 Venable LLP

22

conflict of interest policy

Policy should be approved by the Board

Conflict of Interest process/procedures are just as

important as the policy statement

Many schools rushed to establish new policies

and should now ensure enforcement and ongoing

compliance – Annual disclosure statements– Staff or board member should review

disclosure statements for potential issues before each board meeting

© 2010 Venable LLP

23

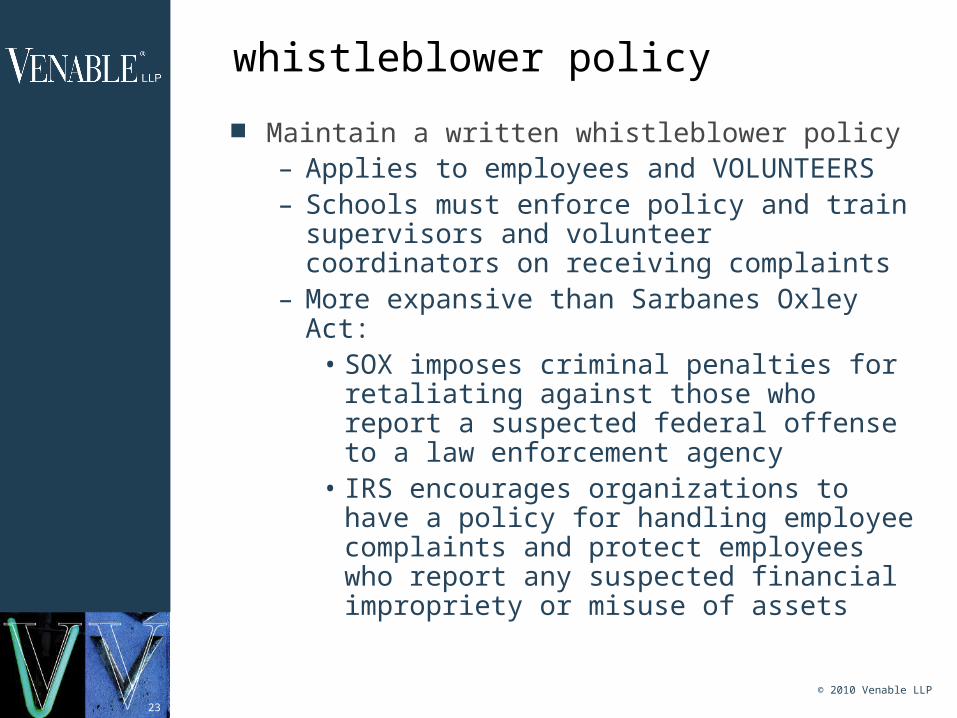

Maintain a written whistleblower policy– Applies to employees and VOLUNTEERS– Schools must enforce policy and train

supervisors and volunteer coordinators on receiving complaints

– More expansive than Sarbanes Oxley Act: • SOX imposes criminal penalties for

retaliating against those who report a suspected federal offense to a law enforcement agency

• IRS encourages organizations to have a policy for handling employee complaints and protect employees who report any suspected financial impropriety or misuse of assets

whistleblower policy

© 2010 Venable LLP

24

More expansive than Sarbanes Oxley Act:

– SOX makes it a crime to destroy documents to prevent their use in an official proceeding

– IRS encourages organizations to have a policy for document integrity, retention, and destruction.

document retention and destruction policy

© 2010 Venable LLP

25

Federal and STATE compliance – Especially for student records

All school documents including admissions,

development, financial aid

Policy should include:– Period of time to retain documents (including

electronic documents)– Destruction timeline– Prohibition on destroying documents when an

investigation is pending

Now that policy is in place, schools must ENFORCE

them in order for them to be effective– Designate and train employees in charge of

ongoing compliance

document retention and destruction policy

© 2010 Venable LLP

26

Form 990 asks whether the organization followed the

procedures for the rebuttable presumption in setting

compensation (for the Head of School and other officers or

key employees of the school)

Form 990 asks schools to describe the process

Rebuttable presumption process should include:

– Independent body

• Approval of transaction by independent board, or committee thereof

– Comparability data

• Reviewing comparable data

– Documentation of decision

• Documentation of process and decision in minutes or other records

Schools must actually FOLLOW the process in their policy

more questions regarding policies

© 2010 Venable LLP

27

Schedule K

Supplemental information on tax-exempt bonds

Significant new information being requested – IRS “is aware

of significant non-compliance with recordkeeping and record

retention requirements” for tax-exempt bonds

%of private business use of bond proceeds on a year to year

basis – Put into place procedures to create a data log– Very complicated regulations; have someone work with

you to create the tracking process In 2009, if school had tax exempt bond issue with an

outstanding principal amount of more than $100,000 as of the last day of the year that was issued after December 31, 2002, must complete entire Schedule K, not just Part I, with even more specific questions.

28

Compensation Reporting on the Form 990

© 2010 Venable LLP

29

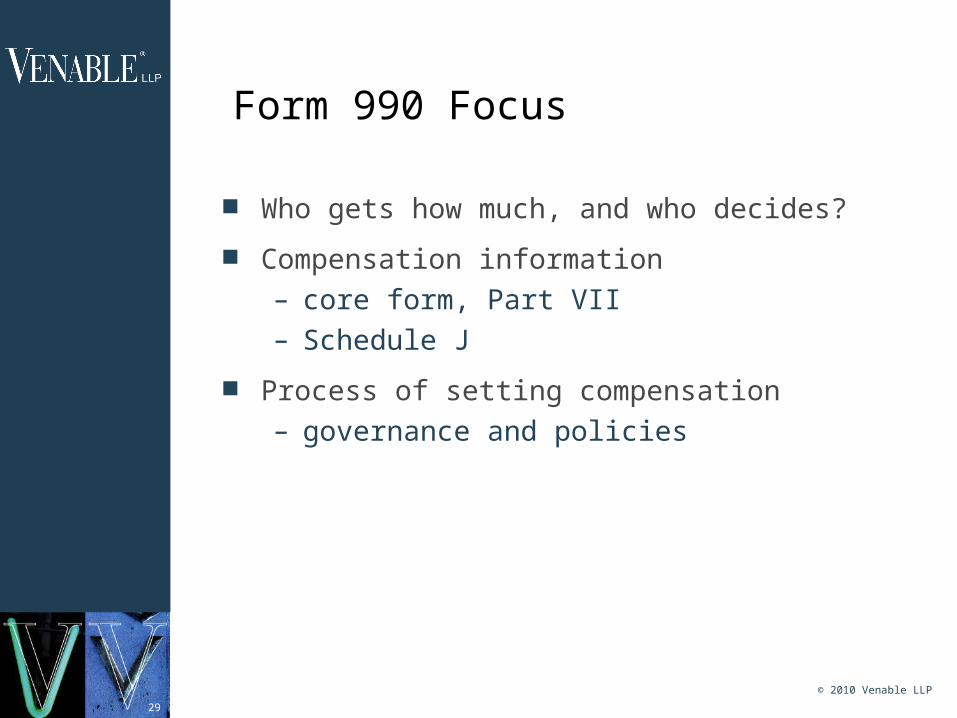

Who gets how much, and who decides?

Compensation information– core form, Part VII– Schedule J

Process of setting compensation– governance and policies

Form 990 Focus

© 2010 Venable LLP

30

Setting Compensation

General requirements– knowledge in compensation matters– no financial interest

IRS safe harbor process– independent body– comparability data– documentation of decision

Schools should follow own policies

© 2010 Venable LLP

31

Core Form Reporting – Reportable Compensation Definition

For employee, compensation reported on Form W-2,

Box 5, i.e., Medicare wages (includes vested

nonqualified deferred compensation and 401(k) and

403(b) deferrals)

For non-employee, compensation reported on Form

1099-MISC

Other taxable compensation

For calendar year ending with or within organization’s

fiscal year

© 2010 Venable LLP

32

Core Form Reporting – “Other” Compensation

Includes nontaxable deferred compensation (qualified

and nonqualified, vested and nonvested) and most

nontaxable benefits

Reporting exclusion for items under $10,000, but with

various exceptions

IRS requested comments on whether non vested,

nonqualified deferred compensation should be excepted

© 2010 Venable LLP

33

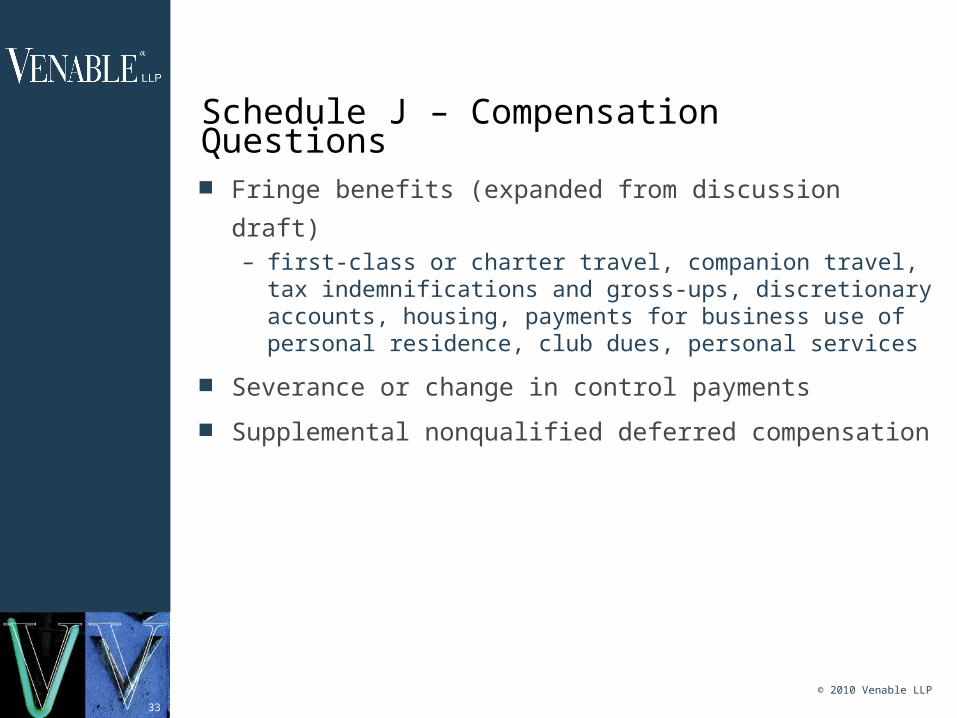

Schedule J – Compensation Questions

Fringe benefits (expanded from discussion draft)– first-class or charter travel, companion travel, tax

indemnifications and gross-ups, discretionary accounts, housing, payments for business use of personal residence, club dues, personal services

Severance or change in control payments

Supplemental nonqualified deferred compensation

© 2010 Venable LLP

34

General Structure for Compensation Reporting

Basic reporting on core form with more detail on

Schedule J

New thresholds for reporting on key employees,

highest paid non-key employees, and formers

and for more detailed reporting

Same structure for all organizations

© 2010 Venable LLP

35

Schedule J – Compensation Questions for 501(c)(3) Organizations

Compensation based on revenues or net earnings

Other non-fixed payments

Payments under the initial contract exception– 2009 Schedule J asks if rebuttable presumption

process was used for initial contract

© 2010 Venable LLP

36

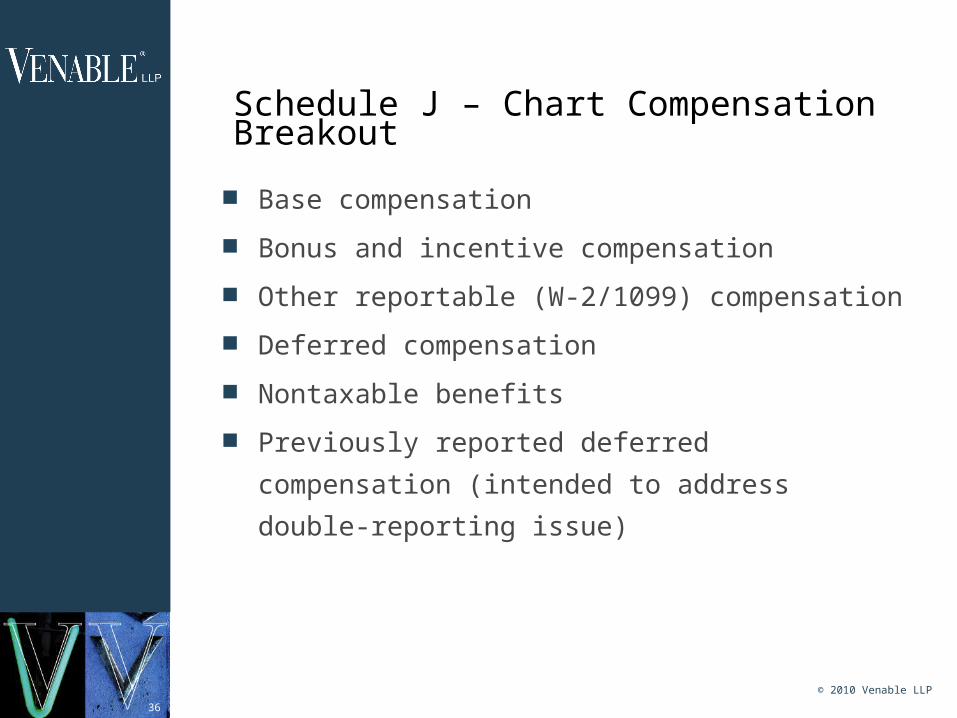

Schedule J – Chart Compensation Breakout

Base compensation

Bonus and incentive compensation

Other reportable (W-2/1099) compensation

Deferred compensation

Nontaxable benefits

Previously reported deferred compensation

(intended to address double-reporting issue)

© 2010 Venable LLP

37

Questions?

© 2010 Venable LLP

38

contact informationYOUR VENABLE INDEPENDENT SCHOOLTEAM

Caryn G. Pass, [email protected] 202.344.8039f 202.344.8300

Heather J. Broadwater, associate

t 202.344.8042f 202.344.8300

Grace H. Lee, [email protected] 202.344.8043f 202.344.8300

www.Venable.com