1 “Finance and Rural Market” Tuesday, 25 April 2006 Renaissance Kota Bharu Hotel by Datuk Seri...

24

1 “Finance and Rural Market” Tuesday, 25 April 2006 Renaissance Kota Bharu Hotel by Datuk Seri Panglima Andrew L.T. Sheng Tun Ismail Ali Professor of Monetary and Financial Economics Faculty of Economics and Administration University of Malaya

-

Upload

jonah-peters -

Category

Documents

-

view

224 -

download

0

Transcript of 1 “Finance and Rural Market” Tuesday, 25 April 2006 Renaissance Kota Bharu Hotel by Datuk Seri...

1

“Finance and Rural Market”

Tuesday, 25 April 2006Renaissance Kota Bharu Hotel

by

Datuk Seri Panglima Andrew L.T. Sheng

Tun Ismail Ali Professor of Monetary and Financial EconomicsFaculty of Economics and Administration

University of Malaya

2

INTRODUCTION

• The bulk of the world poor is in rural areas • Rural finance remains a major policy concern • In the 1960s, there were agricultural banks,

development banks and rural cooperatives to serve rural needs.

• Large nonperforming loans experience of such institutions led the World Bank and others to rethink rural finance strategy.

• In the 1970s and early 1980s, micro finance institutions led by Grameen Bank in Bangladesh started a new trend.

3

WHAT IS RURAL FINANCE?

• Rural finance is defined as financial services offered and used in rural areas by people of all income levels.

• Rural finance covers all the savings, lending, financing and risk minimizing opportunities (formal/informal) and institutions in rural areas.

• Rural financial markets are part of the domestic financial system and are therefore affected by government and central bank policies.

• Rural financial markets tend to be fragmented and consist of formal, semi formal and informal financial intermediaries.

4

COMPLETE RURAL FINANCE

Important to remember that rural finance must cover the following :Payment services, including remittancesSeasonal credit for farming, consumption and

investmentGeneral insurance and cover against

uncertainties

5

RECENT LESSONS

• Formal financial institutions, including development banks, do not always meet the needs of the rural poor, because intermediation costs are too formal and high. They do not understand rural needs.

• Rural credit is complex because it involves different types of crops, with specialist skills for each crop.

• It was always the ready access to credit that mattered, rather than the cost of credit.

• Formal rural financial institutions often prefer to lend to large borrowers, rather than small borrowers. However, the non-performing loan losses were often higher than those for small borrowers.

6

MICRO-FINANCE

• In recent years, efforts to expand access to credit to the poor have focused largely on funneling credit to the poor through micro-finance institution (MFIs).

• A clear strength of such programs has been their ability to reach the poor and to do so with astonishingly small default rates.

• However, as these programs have proliferated, a number of concerns have arisen about the capacity of MFIs to adequately serve the financial needs of poor households on a sustainable basis.

• Evaluation of micro-credit programs to date provide little evidence that they actually enable borrowers to accumulate productive assets or move out of poverty.

7

HISTORY OF MALAY RURAL CREDIT

• The growing monetization of the Malay peasant economy in the 19th century, increased the role of credit.

• The need for production credit as well as consumption credit was most acutely felt by those involved in seasonal agricultural and fishing, livelihoods subject to the monsoons.

• Credit in past was provided by traditional sources, including rural money-lenders

Prof. Mokhzani Abdul Rahim- Credit in a Malay Peasant Economy

8

AGRICULTURE AND DEBT ACCUMULATION

• Rural credit varied with the different requirements of those involved in rubber cultivation, rice farming, fishing, vegetable gardening or mixed farming.

• Although most seasonal loans were usually settled at harvest time, bad harvests and natural disasters cause debt carried over.

• Over time, this could cumulate and result in chronic debt.

9

RURAL INFORMAL CREDIT MARKETS

Two broad types:

1. Traditional sector based kinship, community and religion, which generally stress helpfulness and generosity.

2. Economic and monetary to facilitate consumption, production and trade, based on family friends, shopkeepers, traders, landlords, farm labourers and moneylenders.

10

MORAL ASPECTS OF DEBT

• Receiver becomes indebted in two ways: first, a debt to the economic value of the actual goods or services received and second: a moral debt of gratitude.

• “Hutang emas boleh dibayarHutang budi dibawa mati”.

Formal systems have impersonalized debt relationships.

11

RURAL FINANCE CAN IMPROVE HOUSEHOLD FOOD SECURITY

Three ways to resolve transitory and chronic food insecurity:

1. Capital for financing inputs, labour and equipment for income generation.

1. Households can adopt more effective precautionary savings strategy. Insurance services can reduce the cost of bearing risks.

1. Financial services could stabilize consumption of food and other essential goods during lean times.

12

DEBT IN THE MODERN PERIOD

• Traditional exchange operated very well in a situation in which there was little wealth differences and few incentives and opportunity existed for investment for the creation of further wealth.

• Commercialisation of village economy provides ability to rise out of poverty.

• Also brings with it new risks.

13

CHALLENGES TO RURAL FINANCIAL INTERMEDIATION

1. Information Asymmetry

- Borrowers have more information about the out-turn of their investment and greater capacity to repay loans than lenders.

- Many don’t keep record of their transactions and/or do not use payment facilities of banks

- Access to borrower information is impeded by a lack of efficient transport, communications infrastructure and well-functioning asset registries and databases.

14

RISKS IN RURAL FINANCE

1. Risk

- Agricultural investments have seasonality and long gestation periods, hence uneven cash flow and variable demand for savings and credit.

- Weather and demand cycles cause farmers to face common shocks or income fluctuations.

- Agricultural activities are not diversified, but concentrated on a few crops or livestock activities.

15

COLLATERAL AND ENFORCEMENT

1. Lack of Collateral

- Limits access to rural credit and is related to poorly defined property and land-use rights and weak land property markets (costs of land registration).

1. Enforcement problems

- Efficient contract enforcement, related to a supportive legal framework and robust procedures in formal financial intermediaries key to success in credit development [creation of credit culture].

16

COSTS AND INSTITUTIONAL CAPACITY

1. High operating cost

- Small size of most rural accounts increases cost of service delivery.

- Economies of scale cannot be reached because of low level of economic activity, low rural population density and poor infrastructure.

1. Weak institutional capacity

- Limited availability of educated and well-trained people in smaller rural communities and reluctance of urban professionals to work in rural areas.

17

WORLD BANK APPROACHES

1. Bring the commercial system closer to the rural client

- done through improving business environment and designing products closer to client needs.

2. Bring the client closer to the financial system

- Grassroots training in financial skills, business management, building community associations and institutions, and organizing community NGOs support improved access to markets and finances.

3. Link rural finance to non-financial activities- In particular to product processing, input

supply, and marketing activities.

18

POSSIBLE WAY FORWARD

Sustainable Development of Rural Finance requires:

Continual growth and diversification of rural economy

Access of all segments of the population including rural microentrepreneurs, farmers and the poor to sustainable financial services such as savings, credit and insurance

Provide self reliant, sustainable financial institutions

In a conductive macroeconomic policy environment

19

TECHNOLOGY TO PROMOTE RURAL FINANCE

• Technology (ICT) have contributed to improvements in financial service delivery and lowered transaction costs.

• Internet reduces Information Asymmetry and improves market through reduction of time and transactions (eg Indian farmer experience)

• Development of ICT to rural areas key to rural prosperity

• Government should provide R&D to improve crop yields, types and crop management

20

KEY IS PROMOTING RURAL SMEs

• Sustainable poverty reduction is contingent upon the dynamic growth of self-reliant institutions.

• The essence of self-reliance of the poor and their institutions is local resources (including local skills):Savings deposited and accumulated by the poor

in local financial institutions are the basis of self-financing and household risk management;

How to finance and nurture successful rural SMEs is key to rural growth and development.

21

Savings(low-return activities)

Growth Growth

Credit(High-return activities)

HOUSEHOLD CYCLE OF SAVINGS AND CREDIT

Source : International Fund for Agricultural Development

22

SAVINGS FIRST OR CREDIT FIRST?

Savings first is appropriate in subsistence agriculture and low-return activities

Credit first is more appropriate in high return activities.

• Savings driven investments in low-yielding activities may generate the start-up capital for credit financed activities with high returns.

• These, in turn, may generate profits and savings to be plowed back into low-return activities, including subsistence agriculture

23

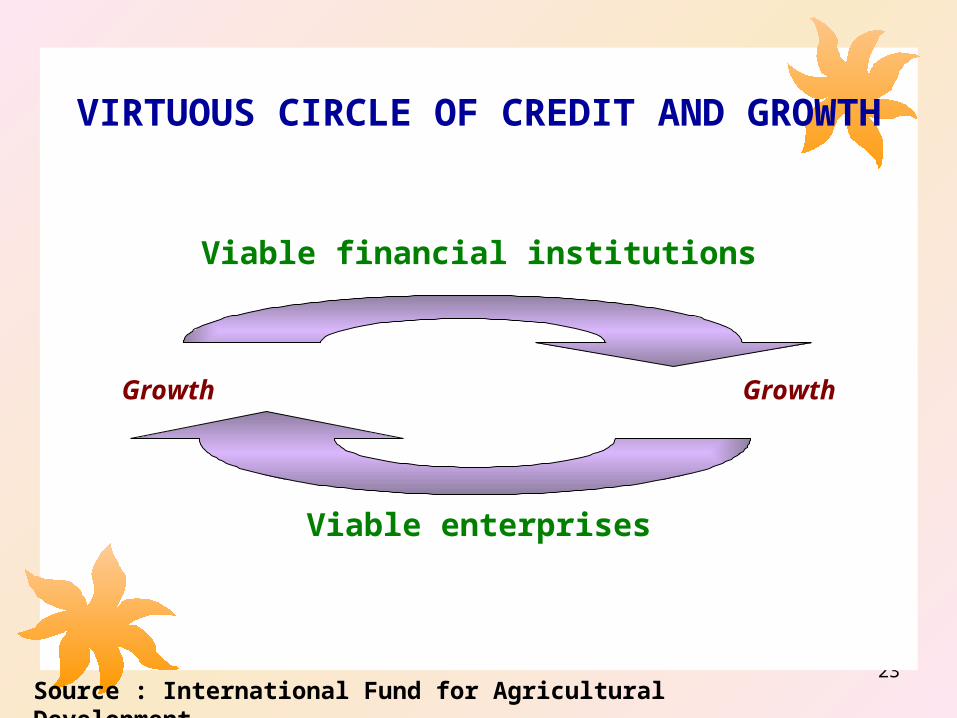

VIRTUOUS CIRCLE OF CREDIT AND GROWTH

Viable financial institutions

Growth Growth

Viable enterprises

Source : International Fund for Agricultural Development

24

CONCLUDING THOUGHTS

• To be successful, rural finance must assist borrowers in total income generation, including marketing and improving product.

• Formal financial institutions have scale but find administrative costs too high in rural finance. Micro-finance has reach, but can’t break out of small scale.

• Investment in human capital is key to empowering the poor to break out of poverty. [Teach a man to fish, not to eat fish].

• Substantial poverty reduction requires holistic approach, not just finance.