1 Fees Miscellaneous Fees and Course Materials Fees 2008-2009 February 14, 2008 .

28

1 Fees Miscellaneous Fees and Course Materials Fees 2008-2009 February 14, 2008 http://planning.ucsc.edu/budget/ miscfees.asp

-

date post

22-Dec-2015 -

Category

Documents

-

view

226 -

download

4

Transcript of 1 Fees Miscellaneous Fees and Course Materials Fees 2008-2009 February 14, 2008 .

1

FeesMiscellaneous Fees and Course Materials Fees

2008-2009

February 14, 2008

http://planning.ucsc.edu/budget/miscfees.asp

2

Topics of Discussion About the Miscellaneous and

Course Materials Fee Advisory Committee

Chancellor Approval of Fees

Overview of Miscellaneous Fees

Overview of Course Material Fees

3

Miscellaneous and Course Materials Fee Advisory Committee (MCMFAC)

Membership includes representatives from: - Student Affairs Administration - Student Fee Advisory Committee (Chair and Vice Chair)

- Academic Senate Committee on Planning and Budget- Academic Divisions- Registrar’s Office- Planning and Budget Office- Vice Provost and Dean of Undergraduate Education

4

Role of MCMFAC

Establish procedures Review fee proposals Recommend fee approvals to

Chancellor Establish procedures for handling

the fee revenues, billing, refunds

5

Fee Approvals

Chancellor has authority to set fees levels for: Miscellaneous User Fees Administrative Service Charges/Penalties Course Materials Fees Deposits

Departments may not assess and collect fees that have not been approved by the Chancellor

6

Miscellaneous Fees

7

Miscellaneous Fees Definition of campus Miscellaneous

Fees

Miscellaneous Fees: Administrative service charges, deposits, and fines that are charged to individual users to cover the costs of breakage charges, replacement fees (lost equipment), health center fees, late filing of study list fees, library fees, improper check-out fines, physical education equipment fees, access fees, rental of facilities fees, transcript fees, etc.

8

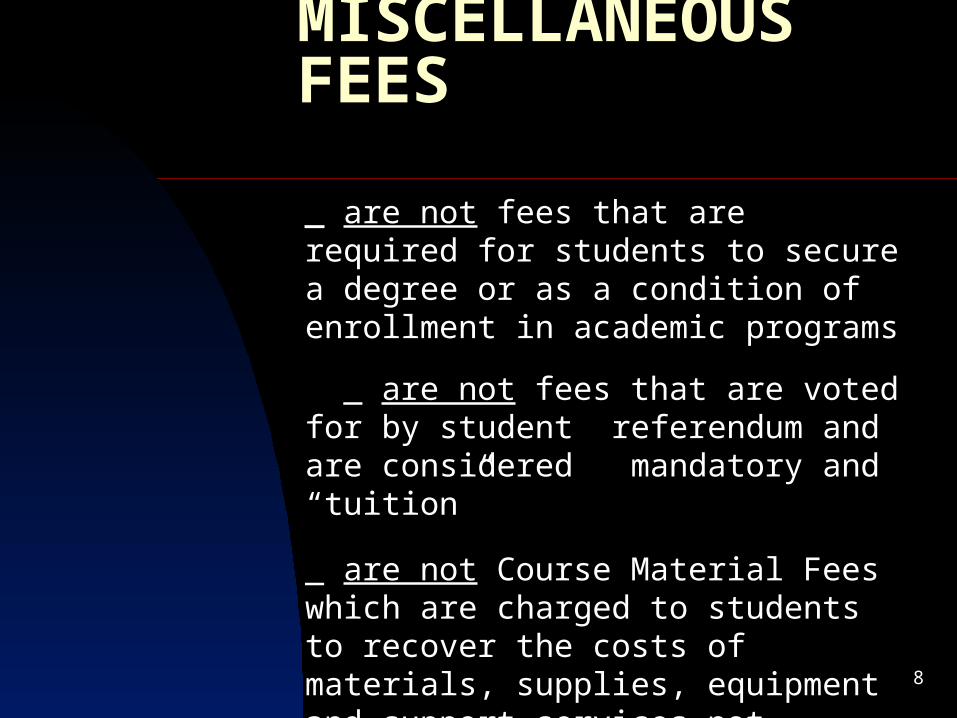

MISCELLANEOUS FEES

_ are not fees that are required for students to secure a degree or as a condition of enrollment in academic programs

_ are not fees that are voted for by student referendum and are considered mandatory and “tuition”

_ are not Course Material Fees which are charged to students to recover the costs of materials, supplies, equipment and support services not covered by the normal instructional budget

9

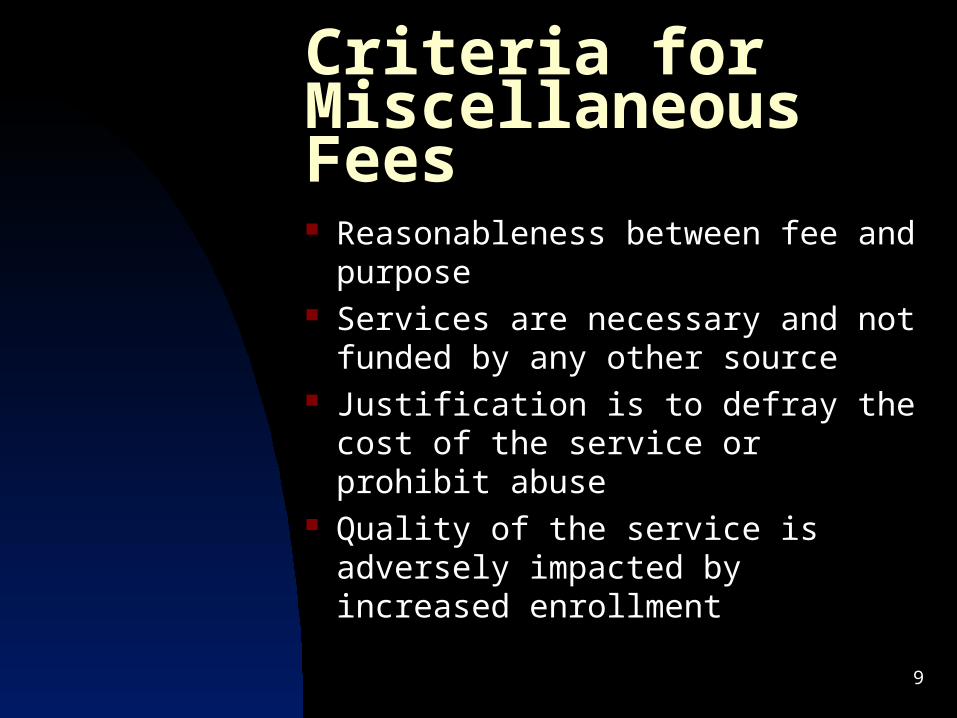

Criteria for Miscellaneous Fees Reasonableness between fee and

purpose Services are necessary and not

funded by any other source Justification is to defray the cost of

the service or prohibit abuse Quality of the service is adversely

impacted by increased enrollment

10

Included in Miscellaneous Fees

Salaries & benefits for providing the service

Supplies/services related to service Leased equipment Equipment depreciation Administrative costs Repairs and maintenance of equipment

11

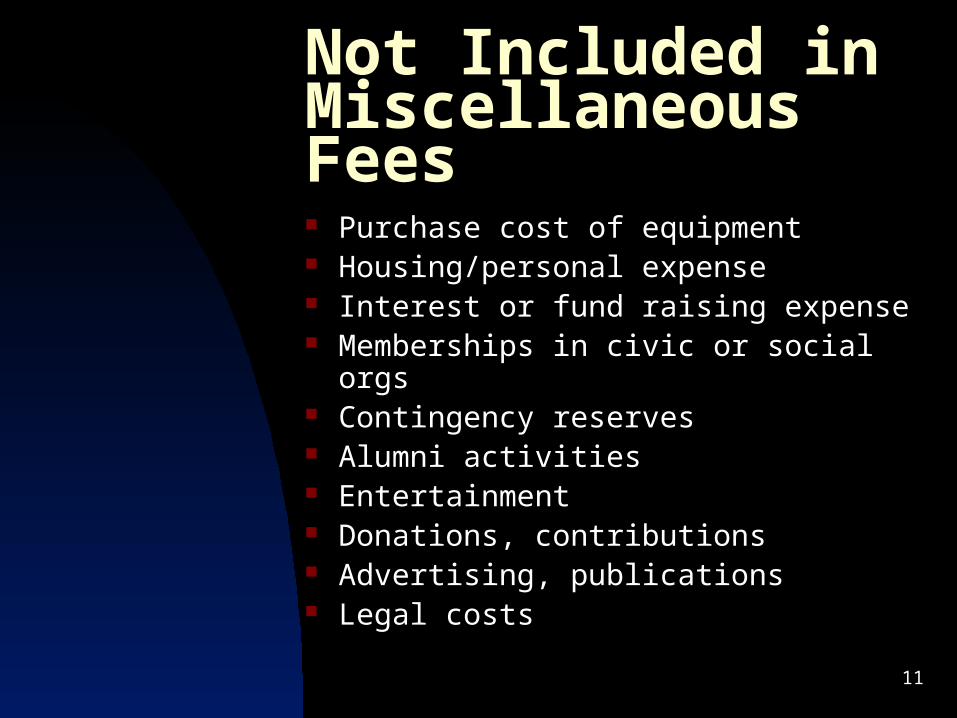

Not Included in Miscellaneous Fees Purchase cost of equipment Housing/personal expense Interest or fund raising expense Memberships in civic or social orgs Contingency reserves Alumni activities Entertainment Donations, contributions Advertising, publications Legal costs

12

Miscellaneous Fee Submittals

Attachment 1 – General Information

Attachment 2 – Financial Statement

Attachment 3 – Miscellaneous Fee Calculation

Attachment 4 – Salary/Benefit Schedule

Attachment 5 – Depreciation Schedule

13

Review Process Miscellaneous Fee proposal submitted

by division to MCMFAC April 1, 2008

MCMFAC reviews proposals during April 2008

Approved – forwarded to Labor Relations and to the Chancellor for approval April/May 2008

Unit notified by May 30, 2008

New fee implemented July 1, 2008

Not approved – division may appeal decision with Chancellor

14

Steps After Approval(Miscellaneous Fees) Division sets up new fund number (General

Accounting – Rob Jarvis 9-5294)

Division establishes permanent budget if volume is significant (For new organization code number call Planning and Budget – Alice Burke 9-5500)

Division communicates to constituencies new/increased fee

Planning and Budget establishes “Official List” of campus miscellaneous fees on website

15

Other MF Issues

Fee limits (existing fees, cost per customer, relationship of fee and purpose)

Fee revenues retained in designated FOAPAL

Fee revenues applied only to costs associated with fee

Year-end balances must be retained in FOAPAL (fees adjusted to compensate for surplus/deficits)

Reserves – equipment depreciation, future expenses

16

Course Materials Fees

17

Course Materials Fees Definition of Course Materials Fees

Fees charged to students to recover the costs of materials, supplies, equipment and support services not covered by the normal instructional budget.

18

Included in Course Materials Fees Materials or supplies consumed,

retained or used by the student.

Examples:

Chemicals, gloves, biological specimens, artist’s media, photographic chemicals, reproduction costs for supplemental materials, providing live models for art classes.

19

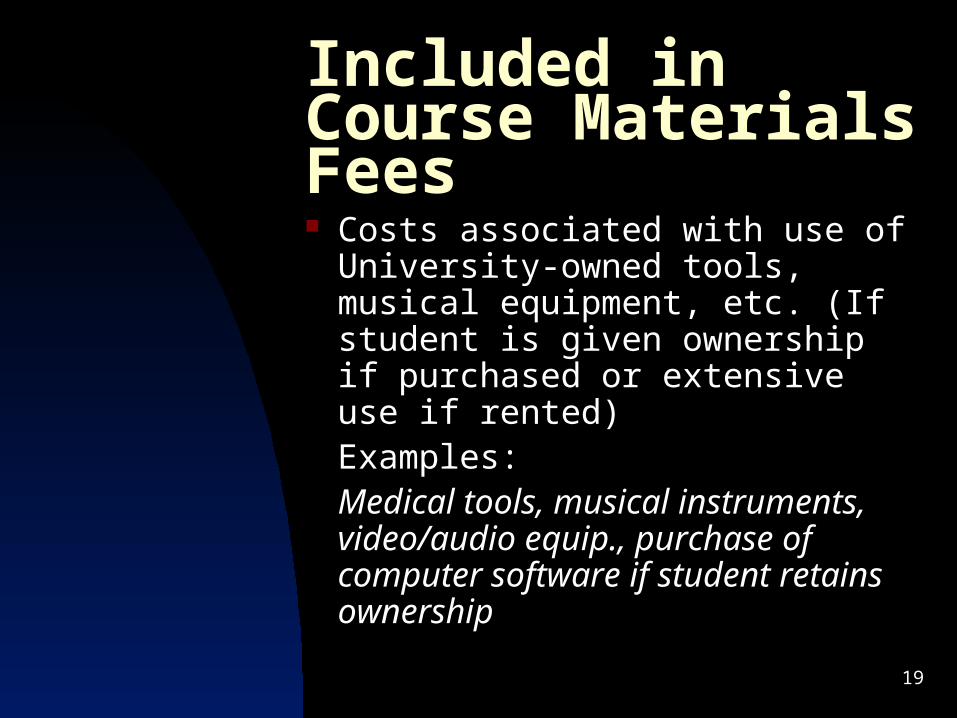

Included in Course Materials Fees Costs associated with use of

University-owned tools, musical equipment, etc. (If student is given ownership if purchased or extensive use if rented) Examples:Medical tools, musical instruments, video/audio equip., purchase of computer software if student retains ownership

20

Included in Course Materials Fees Cost of materials or services to

provide a special supplemental educational experience of direct benefit to the student

Examples:

Travel costs for archeological digs, film rentals, Physical Education dance classes

21

Not Included in Course Material Fees Salaries/benefits of support

personnel Maintenance, depreciation,

replacement of instructional equip Reproduction of copyrighted

materials for course readers or audio or video collections

Course syllabi Software license costs Other items: see misc. fees

22

Not Included Specific to UCSC

Costs that should be borne by the division as costs related to instruction: Divisional computer upgrades Computer software or licenses that

enhance divisional property Equipment used to enhance the division Honoraria, including the cost for guest

lecturers as part of a course Expenses that support faculty or staff when

a course is offered off-campus,• such as airfare, other transportation, or food and

lodging

23

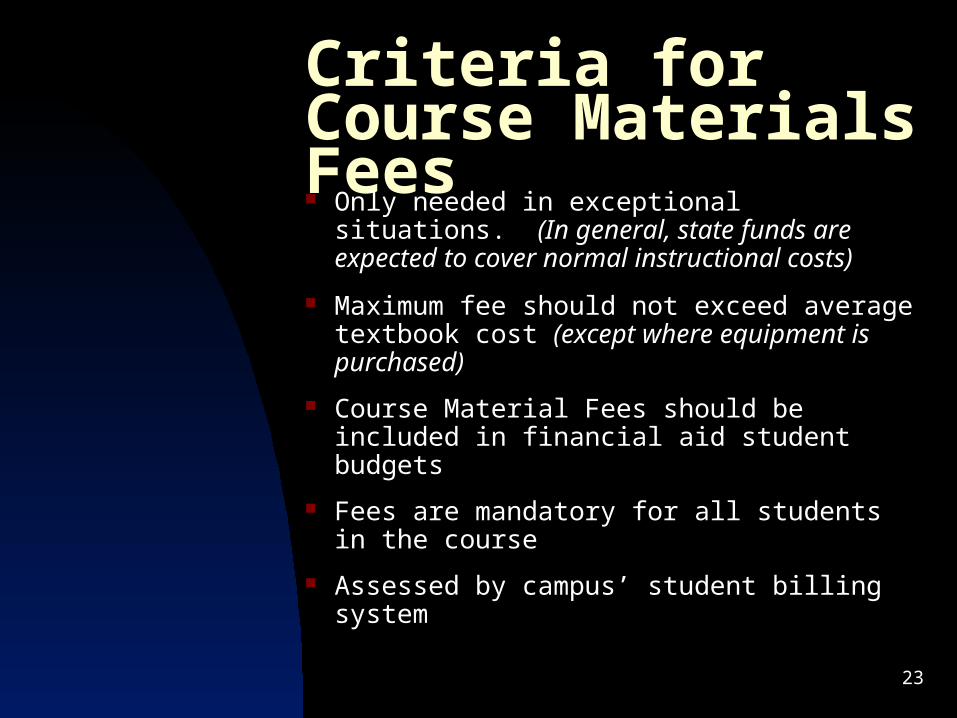

Criteria for Course Materials Fees Only needed in exceptional situations. (In

general, state funds are expected to cover normal instructional costs)

Maximum fee should not exceed average textbook cost (except where equipment is purchased)

Course Material Fees should be included in financial aid student budgets

Fees are mandatory for all students in the course

Assessed by campus’ student billing system

24

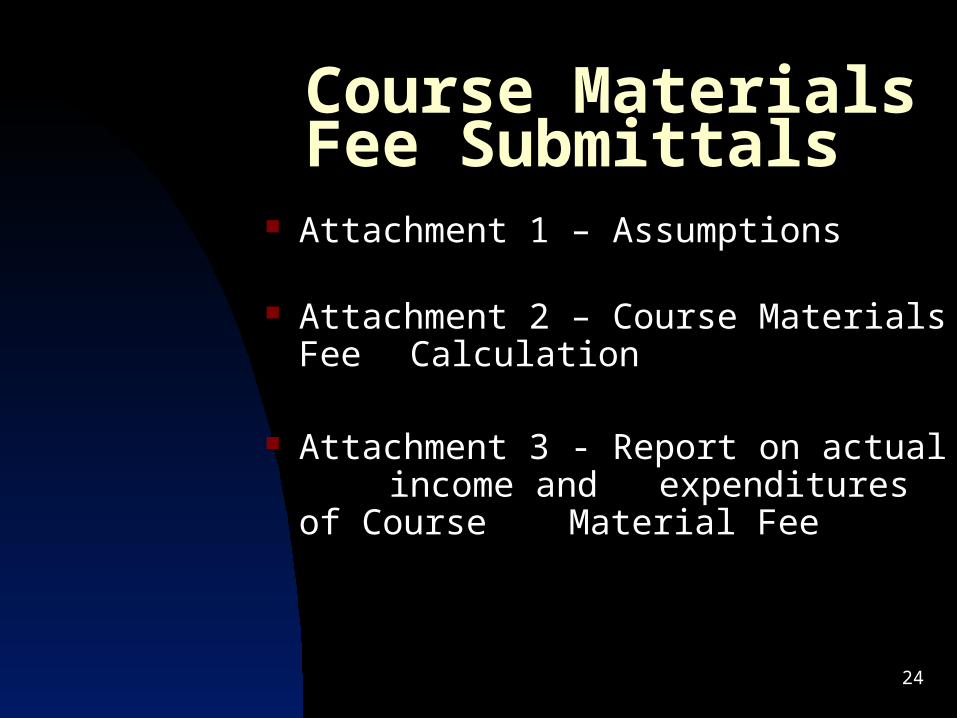

Course Materials Fee Submittals

Attachment 1 – Assumptions

Attachment 2 – Course Materials Fee Calculation

Attachment 3 - Report on actual income and

expenditures of Course Material Fee

25

Review Process Course Material Fee proposal submitted by division

to MCMFAC (February 27, 2008)

MCMFAC reviews proposals (fee limit and purpose of fee consideration given first and foremost to students) March 2008

Recommendation forwarded to the Chancellor for approval – March 2008

Registrar’s Office notified of approved Course Material Fees – March 30, 2008

Not approved – division may appeal decision with Chancellor

26

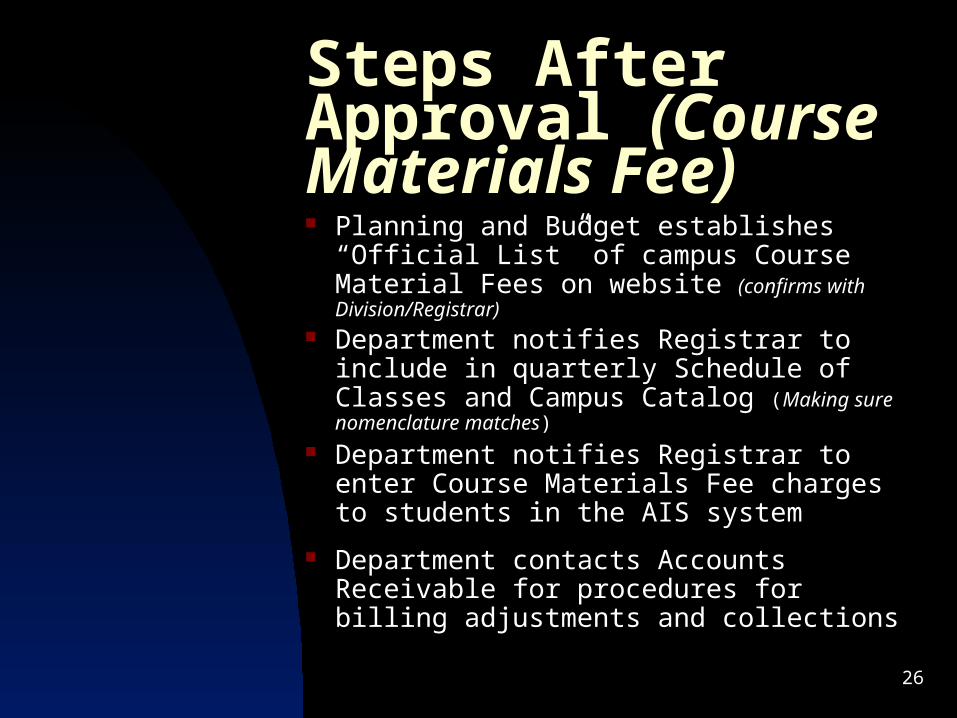

Steps After Approval (Course Materials Fee) Planning and Budget establishes “Official

List” of campus Course Material Fees on website (confirms with Division/Registrar)

Department notifies Registrar to include in quarterly Schedule of Classes and Campus Catalog (Making sure nomenclature matches)

Department notifies Registrar to enter Course Materials Fee charges to students in the AIS system

Department contacts Accounts Receivable for procedures for billing adjustments and collections

27

Steps After Approval (Course Materials Fee) Department contacts General

Accounting for distribution and reconciliation of CMF income

Permanent budget FOAPAL established (contact Rob Jarvis in Accounting 9-5294 for student fee fund number and Alice Burke in P&B 9-5500 for organization code)

28

Other CM Issues Be sure to look at existing fees (existing

fees, cost per student, relationship of fee and purpose)

Fee revenues retained in designated FOAPAL

Fee revenues applied only to costs associated with fee

Year-end balances must be retained in FOAPAL (fees adjusted to compensate for surplus/deficits)

Fee waivers may be granted as an exception. (Each division must specify appeal process in CMF proposal)