1 Education Finance and Adequacy Presentation to the Joint Legislative Oversight Committee on...

23

1 Education Finance and Adequacy Presentation to the Joint Legislative Oversight Committee on Costing an Adequate Education (RSA 193-E:2-d) Room 100, State House September 24, 2007 Steve Norton Executive Director, NHCPPS “…to raise new ideas and improve policy debates through quality information and analysis on issues shaping New Hampshire’s future.” Board of Directors Martin L. Gross, Chair John B. Andrews John D. Crosier Gary Matteson Chuck Morse Todd I. Selig Mike Smith Donna Sytek Georgie A. Thomas James E. Tibbetts Brian F. Walsh Kimon S. Zachos Staff Steve Norton Dennis Delay Ryan Tappin Doug Hall

-

Upload

pierce-flynn -

Category

Documents

-

view

212 -

download

0

Transcript of 1 Education Finance and Adequacy Presentation to the Joint Legislative Oversight Committee on...

1

Education Finance and Adequacy

Presentation to the Joint Legislative Oversight Committee on Costing an Adequate Education (RSA 193-E:2-d) Room 100, State House

September 24, 2007

Steve NortonExecutive Director, NHCPPS

“…to raise new ideas and improve policy debates through quality information and analysis on issues shaping New Hampshire’s future.”

Board of DirectorsMartin L. Gross, Chair

John B. Andrews

John D. Crosier

Gary Matteson

Chuck Morse

Todd I. Selig

Mike Smith

Donna Sytek

Georgie A. Thomas

James E. Tibbetts

Brian F. Walsh

Kimon S. Zachos

StaffSteve Norton

Dennis Delay

Ryan Tappin

Doug Hall

2

Presentation Topics

Education Finance History What Do We Mean by Adequacy? Methods for Costing Out

Adequacy. Data (and it’s limitations) for

Costing Out Adequacy. Targeting to Special Needs

Populations (and data). How Will Costs Grow?

3

% of NH School District RevenueProvided by State Aid 1919-2005

39.7%

54.8%

22.8%

28.5%

0%

10%

20%

30%

40%

50%

60%19

19-2

0

1924

-25

1929

-30

1934

-35

1939

-40

1944

-45

1949

-50

1954

-55

1959

-60

1964

-65

1969

-70

1974

-75

1979

-80

1984

-85

1989

-90

1994

-95

1999

-200

0

2004

-200

5

School Year

Including Statewide property tax

Excluding statewide property tax

4

State Aid as Percent of School RevenueSchool Year 1998-1999

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%N

ew H

amps

hire

Illin

ois

Nev

ada

Virg

inia

Sou

th D

akot

aN

ebra

ska

Pen

nsyl

vani

aC

onne

ctic

utM

isso

uri

Mar

ylan

dN

orth

Dak

ota

New

Jer

sey

Rho

de Is

land

Mas

sach

uset

tsO

hio

New

Yor

kTe

xas

Col

orad

oA

rizon

aM

onta

naM

aine

Tenn

esse

eG

eorg

iaF

lorid

aLo

uisi

ana

Iow

aS

outh

Car

olin

aW

yom

ing

Indi

ana

Wis

cons

inM

issi

ssip

piO

rego

nM

inne

sota

Ark

ansa

sC

alifo

rnia

Okl

ahom

aA

lask

aU

tah

Idah

oA

laba

ma

Kan

sas

Ken

tuck

yW

est V

irgin

iaD

elaw

are

Was

hing

ton

Mic

higa

nN

orth

Car

olin

aN

ew M

exic

oV

erm

ont

Haw

aii

State

Pe

rce

nt

Sta

te A

id

Before reform, NH was last in state aid for schools.

5

State Aid as Percent of School Revenue(School Year 2002-2003)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

New

Ham

pshi

re

Nev

ada

Illin

ois

Sou

th D

akot

a

Neb

rask

a

Mis

sour

i

Pen

nsyl

vani

a

Con

nect

icut

Nor

th D

akot

a

Mar

ylan

d

Virg

inia

Mas

sach

uset

ts

Tex

as

Rho

de I

slan

d

Mai

ne

New

Jer

sey

Col

orad

o

Flo

rida

New

Yor

k

Ohi

o

Ten

ness

ee

Mon

tana

Iow

a

Geo

rgia

Loui

sian

a

Ariz

ona

Sou

th C

arol

ina

Wyo

min

g

Ore

gon

Wis

cons

in

Mis

siss

ippi

Okl

ahom

a

Uta

h

Ark

ansa

s

Ala

ska

Kan

sas

Cal

iforn

ia

Ken

tuck

y

Idah

o

Ala

bam

a

Indi

ana

Wes

t V

irgin

ia

Was

hing

ton

Del

awar

e

Mic

higa

n

Nor

th C

arol

ina

Ver

mon

t

New

Mex

ico

Min

neso

ta

Haw

aii

State

Per

cen

t S

tate

Aid

If locally retained state property tax is considered state aid

State-imposed minimum property taxes that are retained locally are reported as state aid only by Vermont and NH.

6

Final Local Entitlement Payments for Catastrophic Aid

$15,978,187$17,731,075 $17,561,880

$28,055,251

$20,074,363$18,999,990

$19,089,927

$0

$5,000,000

$10,000,000

$15,000,000

$20,000,000

$25,000,000

$30,000,000

SFY 2000 SFY 2001 SFY 2002 SFY 2003 SFY 2004 SFY 2005 SFY 2006

9.8% Annual Growth Rate

21

Other State Expense? Catastrophic Aid

7

$0

$5,000,000

$10,000,000

$15,000,000

$20,000,000

$25,000,000

$30,000,000

$35,000,000

$40,000,000

$45,000,000

97 98 99 00 01 02 03 04 05 06

Other State Expense? School Building Aid

8

Expenditure Per Elementary Pupil 1999, 2005

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

200%

1 9 17 25 33 41 49 57 65 73 81 89 97 105 113 121 129 137 145 153 161 169 177 185 193 201 209 217

Towns (each year independently sorted in order from low to high)

$ P

er P

up

il a

s %

of

Sta

te M

edia

n

1999 2005

1999 reforms had little impact on per-pupil

expenditures.

9

Equalized Tax Rates for Education 1998, 1999, 2005(compared to median town)

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

one dot for each town (sorted from low to high separately for each year)

Rat

io o

f ta

x ra

te t

o m

edia

n t

ow

n t

ax r

ate

1999

1998 Taxpayer equity:The change in taxpayer equity brought about by the reform of 1999 was almost entirely reversed by 2005. If the trends of 1999-2005 continue for three or four more years, the relative distribution of tax rates for education will be the same as they were immediately before reform in 1999.

2005

1999 reforms had initial impact on

taxpayer equity.

10

Additional NH Property Taxes Collected over Prior Year($ in millions)

$145

$122$132

$50$38

$58 $53$68

$55 $48

$86

($150)

$146$161

$136

$168$150

$116

($200)

($150)

($100)

($50)

$0

$50

$100

$150

$200

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

Year

Big, one-time impact on local

property tax.

11

What about changes in educational attainment as a result

of reform?

We don’t know.

12

Evolution of Judicial Review

Part 1: Constitutional Mandate Part 2: What is Adequacy? Part 2a: Adequacy and Outcomes

No Child Left Behind and proficiency standards State (and local) assessment programs to meet

NCLB requirements.

Part 3: Cost of Adequacy

13

The question of ‘adequacy’ remains.

Adequacy Definition Part 1

HB 927

School Approval Standards

Curriculum Frameworks

Includes content definition of outcomes for some subjects (e.g. NECAP and grade level expectations)

Adequacy Definition Part 2: What is the standard?

States (and the judicial reviewprocess) are increasingly turning to a definition of proficiency

•100% Proficiency by 2014?•79% of districts proficient in 3 years (e.g. Connecticut?)•100% of students pass 10th grade test by 12th grade (e.g. South Carolina?)

14

Methods to Costing-Out Adequacy: An Art NOT a Science

Standards(e.g. levels ofproficiency)

What methods lead to thoseoutcomes (e.g. student teacher ratios, evidenced based practices)

orWhat inputs are necessary to meet thisgoal? (Professional judgment panel)

or

Successful Schools (Use econometric methods to id which schools are efficiently meeting the standard, holding other factors constant)

or

Multiple methodologies

15

2005 Spending by School Districts: $2.42 billionFood Service

0.8%All Other

6.0%

Facility Construction5.7%

Special Education +16.2%

Instruction 41.4%

Support Services8.4%

Plant Operations7.2%

Transportation3.6%

Interest & Principal on Debt

5.7%

Administration8.3%

Spending 2004-05Function AmountInstruction $944,920,571Special Education + $368,625,189Support Services $203,201,425Administration $199,512,144Plant Operations $173,990,944Transportation $86,207,510Interest & Principal on Debt $137,717,033Facility Construction $138,598,107Food Service $19,937,863All Other $144,723,246Total $2,417,434,032

What Expenses are Included? Or, “How Do

You Come up With Cost Estimates?”

16

Data on Expenditures

DOE 25 the primary source of data on school expenditures. These forms were not designed for this purpose. Significant work to identify what is useful. Problems in comparability

Some schools pay for school crosswalk; others rely on municipality to pay for that.

Manchester pays for transportation of out of district students.

While helpful, the DOE 25 cannot be considered precise.

Staff accounts for most of expenditure levels

17

Estimating The Costs of Instruction

Administration Salary - By SAU, the annual salaries of superintendents, assistant superintendents and business administrators is reported.

Teacher Average Salary - By district, the number of full-time classroom teachers and their average salary is reported.

Teacher Attainment - Reported for each district are the percent of individuals who hold a Bachelor's, Master's and beyond Master's Degrees. This data has been collected for full and part-time teachers of grades kindergarten through high school (preschool teachers are not included). This data does not include administrators and non-teacher professionals.

Should all teachers be included in the estimate of adequacy?

18

Targeting: Judicial focus on special-needs populations.

Language, disability, and other factors an increasingly specified factor in other state’s (and judiciary’s) decision-making.

State currently targets general fund aid based on Disability (e.g. special education catastrophic aid

program) Capital decisions at the local level Various other factors (income, free and reduced lunch,

limited english)

19

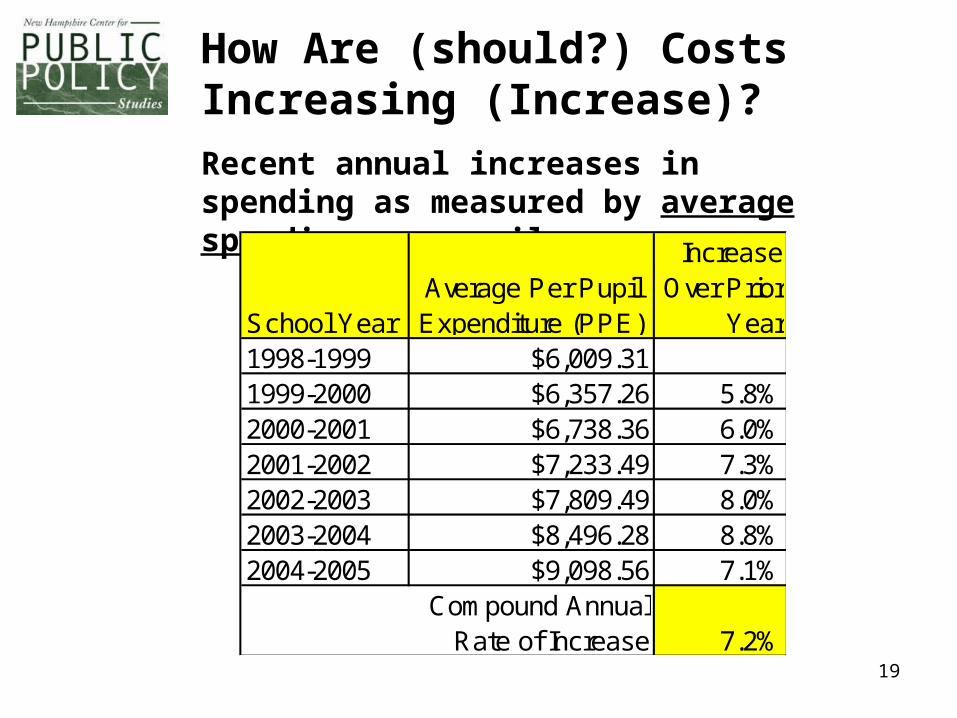

How Are (should?) Costs Increasing (Increase)?

Recent annual increases in spending as measured by average spending per pupil

School YearAverage Per Pupil Expenditure (PPE)

Increase Over Prior

Year1998-1999 $6,009.311999-2000 $6,357.26 5.8%2000-2001 $6,738.36 6.0%2001-2002 $7,233.49 7.3%2002-2003 $7,809.49 8.0%2003-2004 $8,496.28 8.8%2004-2005 $9,098.56 7.1%

7.2%Compound Annual

Rate of Increase

20

Spending of NH School Districts 1915-2005

$1,000,000

$10,000,000

$100,000,000

$1,000,000,000

$10,000,000,000

1915

-16

1920

-21

1925

-26

1930

-31

1935

-36

1940

-41

1945

-46

1950

-51

1955

-56

1960

-61

1965

-66

1970

-71

1975

-76

1980

-81

1985

-86

1990

-91

1995

-96

2000

-200

1

School Year

Sp

end

ing

of

NH

Sch

oo

l D

istr

icts

(Lo

gar

ith

mic

Plo

t)

This straight line represents a 10.95% per annum compound growth rate 1942-1989.

1989-1999 the compound growth averaged 4.45% per annum.

1999-2005 the compound growth rate has been 7.96% per annum.

21

Demographics and the Cost of Adequacy.

Changes in Enrollment and Number of Teachers

188,000

190,000

192,000

194,000

196,000

198,000

200,000

202,000

204,000

1998-1999

1999-2000

2000-2001

2001-2002

2002-2003

2003-2004

2004-2005

2005-2006

Num

ber

of S

tude

nts

11,500

12,000

12,500

13,000

13,500

14,000

14,500

15,000

15,500

Num

ber

of T

each

ers

Number of Teachers

Number of Students

22

Lessons Learned from Previous Efforts?

New Hampshire? HB 999 – Modified successful schools model Funding the Gap - Professional judgment model

National? Decreasing reliance on ‘successful schools’ models because of

statistical issues. Increasing reliance on ‘evidence-based’ models and

professional judgment models. Use of multiple methods on the rise.

What are the lessons learned? Assumptions are critical. Significant variation in the cost estimates depending on which

method is used (Texas=0% increase in state aid; other states generally 20-40% increase)

No single method guaranteed to meet judicial muster. Increasing focus on outcomes and special needs populations. Anything that appears like the traditional ‘foundation aid’

method receives judicial concern.

23

All of our reportsare available on the web:

www.nhpolicy.orgwww.nhpolicy.org

New Hampshire Center New Hampshire Center for Public Policy Studiesfor Public Policy Studies

“…to raise new ideas and improve policy debates through quality information and analysis on issues shaping New Hampshire’s future.”

Board of DirectorsMartin L. Gross, Chair

John B. Andrews

John D. Crosier

Gary Matteson

Chuck Morse

Todd I. Selig

Mike Smith

Donna Sytek

Georgie A. Thomas

James E. Tibbetts

Brian F. Walsh

Kimon S. Zachos

StaffSteve Norton

Dennis Delay

Ryan Tappin

Doug Hall