1 Development, Universal Access and Governance in South Africa zCPSR Symposium: One Planet, One Net...

22

1 Development, Universal Access and Governance in South Africa CPSR Symposium: One Planet, One Net - The Public Interest in Internet Governance Boston, 10th - 11th October 1998. Tracy Cohen, Part-time lecturer Telecommunications Law, Wits Law School Assistant to Council, SATRA The views expressed do not necessarily represent the views of SATRA, its Council or any of its employees. The views expressed in this presentation are mine and do not necessarily represent the views of SATRA, its Council or any of its employees.

-

Upload

mavis-carpenter -

Category

Documents

-

view

219 -

download

1

Transcript of 1 Development, Universal Access and Governance in South Africa zCPSR Symposium: One Planet, One Net...

1

Development, Universal Access and Governance in South Africa

CPSR Symposium: One Planet, One Net - The Public Interest in Internet Governance Boston, 10th - 11th October 1998.

Tracy Cohen, Part-time lecturer Telecommunications Law, Wits Law School Assistant to Council, SATRA

The views expressed do not necessarily represent the views of SATRA, its Council or any of its employees.

The views expressed in this presentation are mine and do not necessarily represent the views of SATRA, its Council or any of its employees.

2

Areas of focus

Context and Vitals Definitions: Universal Service v. Universal

Access Universal Access in South Africa

Poverty Telecommunications Teledensity Internet Penetration on the Continent

Governance Policy and Legislation Role of the Regulator

Issues

3

South Africa

4

Definitions - Dedicated service v. reasonable access

Universal Service 3 Components - Availability, Affordability, Accessibility -ITU

“affordable, access to basic voice telephony or its equivalent for all those reasonably requesting it, regardless of where they live.”

- Oftel

Universal Accessall of the above, BUT communal and within a reasonable

distance

Definition depends on the nature of the market Definition informed by technical, social, political

considerations e.g. RDP

5

Universal Access in South Africa

Poverty 36% of all households below the HSL HSL = R1050/month ($180)

• Poorest 20% hh (27% pop) <3% total income• Richest 20% hh (3% pop) >65% total income

Telecommunications Teledensity• 2.8 million residential lines• 1.5 million business lines• 28 000 farm lines• 90 000 Public Pay Phones

National average = 9• Richer areas = 50 • Poorer areas = 0.001

6

The Phone Gap

7

In Summary

8.7 million households in SA2.8 million have telephones55% of the 2.8 million are in white

households5.9 million households have no phones2.1 million households have NO ACCESS to

a telephone within 5km’s of their home

8

SA - ISP Industry Structure

9

Internet in Africa Source: Mike Jensen, AISI

10

Cost Comparative Source: Mike Jensen, AISI

11

The role of Governance in delivering Universal Access in SA

Universal access requires regulation aimed at balancing economic growth and social/policy objectives

History, Policy and legislation - Telecommunications Act No. 103 of 1996

State institutions supporting universal access SATRA

• The public interest - Telkom v Internet Service Providers Association, 1997

The Universal Service Agency • Lifespan - 5 years• Universal Service Fund - Section 59• Administered by the USA subject to the control of SATRA

Department of Communications• Multimedia Projects/ Public Access Projects

12

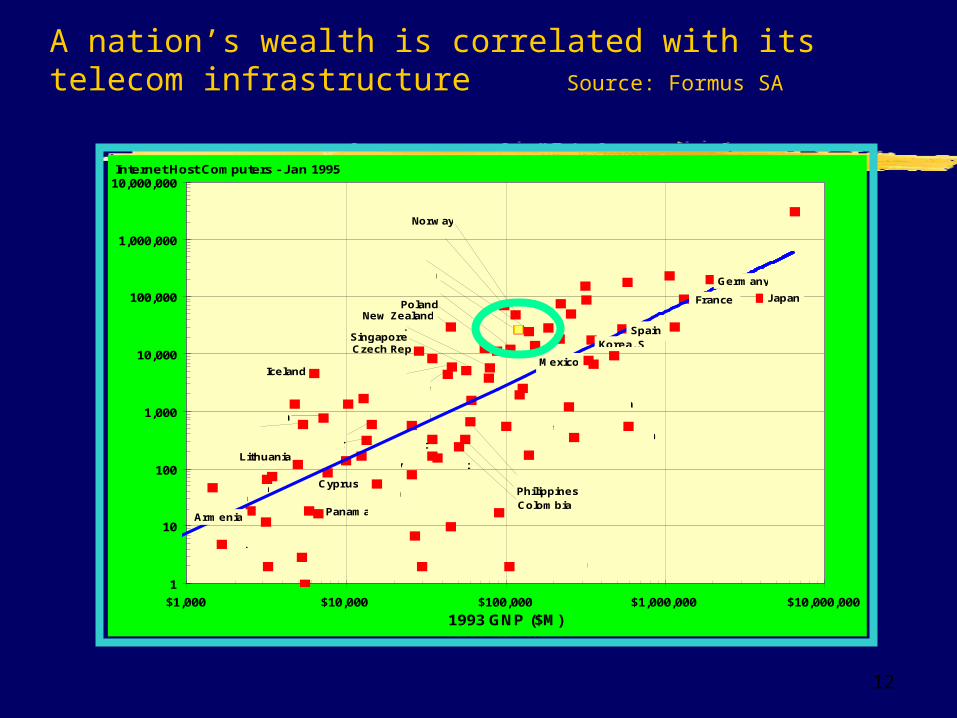

A nation’s wealth is correlated with its telecom infrastructure Source: Formus SA

1

10

100

1,000

10,000

100,000

1,000,000

10,000,000

$1,000 $10,000 $100,000 $1,000,000 $10,000,000

Internet Host Computers - Jan 1995

1993 GNP ($M)

USA

UKGermany

Japan

Australia

France

Italy

China

Russian Fed

Canada

Spain

Brazil

India

Argentina

SwitzerlandNetherlands

Mexico

Korea, S

Sweden

Belarus

Thailand

Portugal

Turkey

Indonesia

Denmark

AustriaBelgium

New Zealand

South Africa

Hong Kong

Finland

Ukraine

Norway

Poland

Czech Rep

Greece

Israel

Hungary

Algeria

Malaysia

Venezuela

Singapore

PhilippinesColombia

Kazakhstan

ChileIrelandIceland

AzerbaijanGuinea

MoldaviaFiji

SlovakiaSlovenia

Estonia

BulgariaUruguay Egypt

LuxembourgEcuador

Puerto Rico

Romania

Kuwait

Tunesia

Peru

Cyprus

Costa Rica

PanamaZimbabwe

Latvia

Lithuania

Jamaica

Armenia

ZambiaNicaragua

Saudi Arabia

Taiwan

Iran

Macau

13

Issues

Infrastructure Sub-Saharan Africa teledensity - <1 in 200 Analogue, unreliable network, urban concentration

Affordability and Costs Services - basic or advanced Sustainability

Social Economic

Infrastructural Priorities Literacy and Language Hegemony

Software solutions

14

Conclusion

Regime is irrelevant - other factors are the determinants.

Socially positive role and purpose of regulation: State has a role in ensuring universal access (more so under the

exclusivity model?) USF Ceiling of R20 Million/year must be raised - post exclusivity

Public/private sector partnerships will be vital to success International and regional co-operation is crucial Degree of success correlates proportionately to degree

of sufficient political will, systematic planning and co-ordination

15

Contact Details

E-mail: [email protected]: SATRA, Private Bag X1,

Marlboro,

Sandton, 2063, South AfricaTel: 27-11-321-8384

16

Useful Sites

http://www.satra.org.za/ http://www3.wn.apc.org/africa/mj.htm http://www.sangonet.org.za/ http://wn.apc.org/technology/ http://demiurge.wn.apc.org/africa/projects.htm http://www.doc.org.za/ http://www.telecom98.co.za/ http://www.sas.upenn.edu/African_Studies/

AS.html

17

18

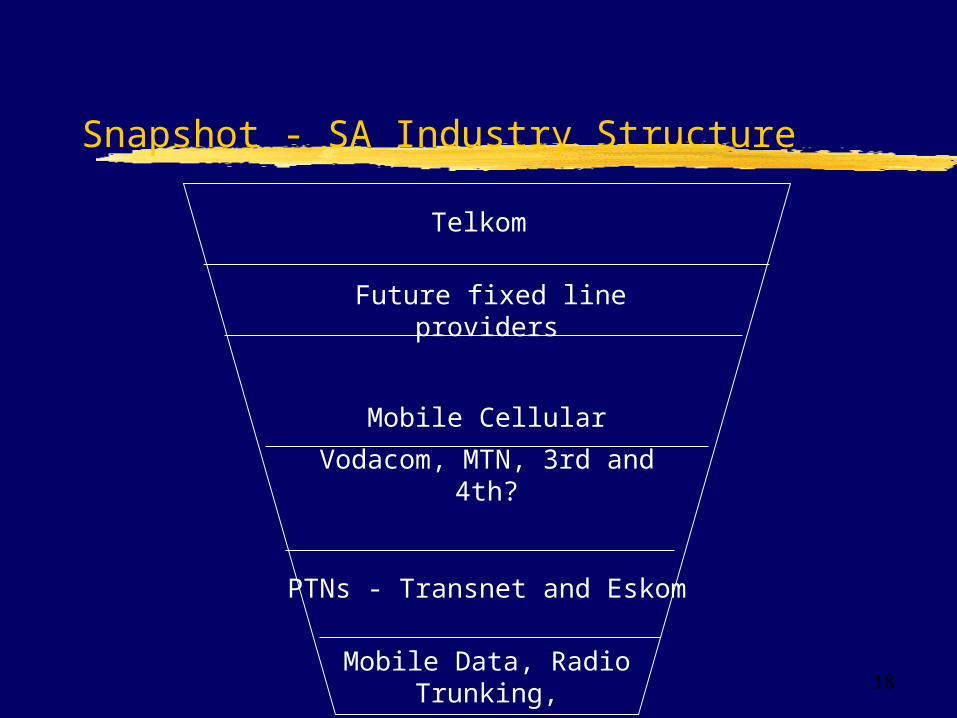

Snapshot - SA Industry Structure

Telkom

Future fixed line providers

Mobile Cellular

Vodacom, MTN, 3rd and 4th?

PTNs - Transnet and Eskom

Mobile Data, Radio Trunking,

VANS

- including ISPs

19

Governance = Regulation?

Fact: Government involvement in the creation and extension of services

Regulation aims to achieve: the delivery of basic services acceptable ranges and quality of services fair competition facilitate economic growth and global competitiveness

Regulation is aimed at balancing economic growth and social/policy objectives

Universal Access requires regulation

20

24 Months Ago…

21

Africa - Continental Connectivity Indicators - Source: Mike Jensen, AISI

46/54 Countries and territories in Africa have Internet access in the Capital cities

6 Countries have plans for full Internet access in the capital cities

2 Countries remain without plans for full Internet access 7 Countries have only one full public access ISP after 12

months 11 Countries have local ISPs or POPs in some secondary

towns 10 Countries have local dial-up Internet access

nationwide

22

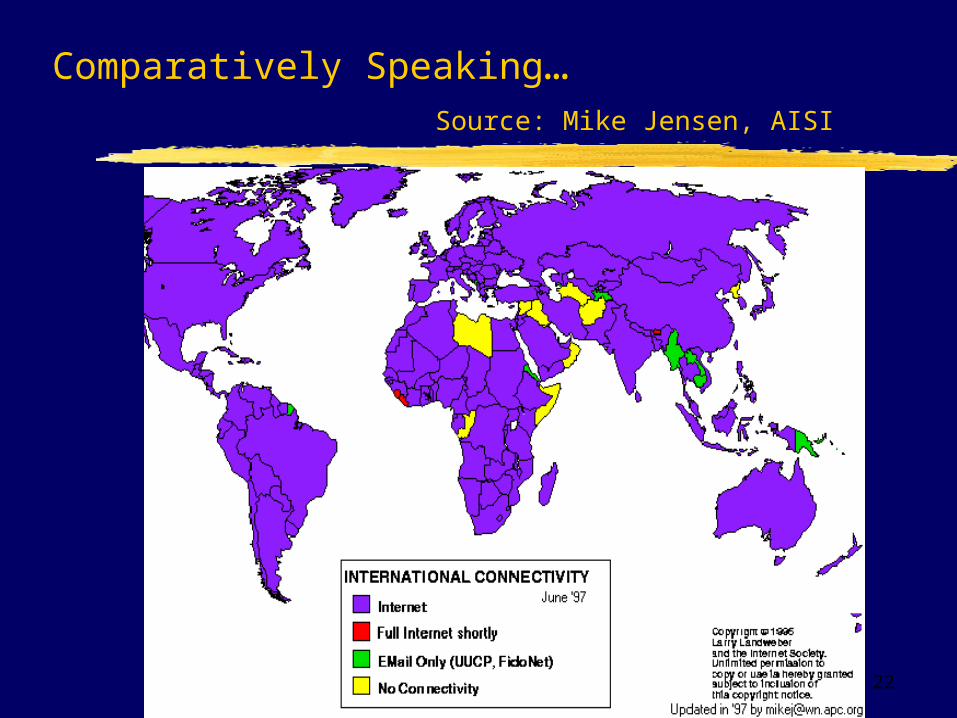

Comparatively Speaking…Source: Mike Jensen, AISI